Abstract

More and more firms have a chief sustainability officer (CSO) to support the organizational focus on corporate social responsibility (CSR). Yet, there is much to learn about the boundary conditions that make the presence of CSOs particularly effective for firms’ CSR. Using an attention-based view lens, we investigate the relationship between having a CSO as attention carrier of CSR activities and examine the potential boundary conditions related to the three attention principles (attention selection, represented by board diversity; attention structures, represented by a CSR committee; and situated attention, represented by country-level CSR standards). We test our hypotheses using a global sample of 3,470 firms across 54 countries. Our results show that the influence of the CSO on internal and external CSR is most important in the absence of attention principles that may act as alternative attention carriers of CSR. In other words, attention principles form boundaries to the CSO’s influence on internal and external CSR. Our study contributes to research on the attention-based view, CSOs, and CSR.

“Our business transformation connects sustainability and corporate strategy, recognizing that ESG issues are business issues. As a consequence, sustainability, in all its dimensions, is at the absolute core of our business strategy”

Many firms have chief sustainability officers (CSOs) in the highest echelons of their firm’s leadership (Matten & Moon, 2008) to function as attention carriers of corporate social responsibility (CSR; Fu et al., 2020). We define CSR as organizational actions and policies regarding economic, social, and environmental performance (Aguinis & Glavas, 2012). CSOs can help advance CSR by drawing it into the core strategic focus of firms (Velte & Stawinoga, 2020), and consequently, stimulating organizational action (Ocasio, 1997), for example, in the form of devoting specific resources to CSR projects and changing practices that enhance CSR activities (Zhao et al., 2016). CSOs can increase the legitimacy of CSR activities in the eyes of internal stakeholders and can be the bridge to external stakeholders that wish to advance a certain CSR issue (Velte & Stawinoga, 2020). Several studies indeed show that having a CSO is instrumental for the implementation of CSR activities (Kanashiro & Rivera, 2019; Karn et al., 2023; Strand, 2013, 2014). Others, however, question whether having a CSO contributes to actual change in the organization (Hawn & Ioannou, 2016), or that it may be a more symbolic act, aimed at improving the firm’s CSR image (Peters et al., 2019). Hence, literature is ambiguous on the influence of a CSO on a firms’ CSR activities.

A recent review of studies testing the influence of CSOs concludes that it remains unclear whether CSOs indeed succeed in improving CSR (Velte & Stawinoga, 2020). Furthermore, while a growing body of literature on CSOs has primarily focused on the relationship between CSO presence and CSR, we know less about the boundary conditions that define when CSO presence is most beneficial for firm CSR. After all, both organization- and country-level characteristics may influence the effect of a specialist to the top management team (Oehmichen et al., 2017), suggesting that a CSO may not be equally beneficial for all types of firms around the globe. Therefore, this study examines whether CSOs indeed increase CSR activities in firms, and under which boundary conditions they are particularly instrumental to positively influence CSR.

Grounded in the attention-based view (ABV) (Ocasio, 1997; Pinkse & Gasbarro, 2019), we argue that firms will have more attention for and hence devote more resources to CSR when CSOs are present, resulting in more CSR activity. We specifically distinguish between internal (focused on substantive CSR policies and practices) and external (focused on symbolic CSR communication) CSR activities to examine what type of impact the CSO has on the firm. We argue that CSOs, as CSR attention carriers (Fu et al., 2020), have a positive influence on both types of activities. However, we argue that the effect is stronger for the more substantive internal CSR activities than for more communication-focused external CSR, as the CSOs’ main goal as an attention carrier is to constitute organizational action (Ocasio, 1997).

Furthermore, we examine whether firm-related and contextual characteristics based on the attention principles form boundary conditions for the predicted positive influence of CSOs on CSR. ABV proposes three attention principles that direct organizational attention and subsequent decisions and action: attention selection, attention structures, and situated attention (Ocasio, 1997; Pinkse & Gasbarro, 2019). We argue that the positive influence of the CSO as attention carrier can be confounded by boundary conditions reflecting these attention principles that also direct organizational attention to CSR, as they can act as alternative attention carriers of CSR. To test the boundary conditions of the CSO’s effectiveness, we examine whether board diversity (as an expression of attention selection), the presence of a CSR committee (attention structures), and the CSR standards in the home country (situated attention) mitigate the relationship between the presence of a CSO and the firm’s CSR.

Using an instrumental variable analysis, we test our hypotheses using unique data on a global sample of 3,470 firms from 54 countries between 2012 and 2019. Our tests provide support for our hypotheses that CSOs as attention carriers have a positive influence on the CSR activities within their firms and show how alternative attention carriers of CSR mitigate the influence of the CSO on CSR activities. Especially, we find that the direct influence of CSOs on internal and external CSR is partly substituted if these firms have a diverse board and are in home countries with high country-level CSR standards. Furthermore, we find that the presence of a CSR committee does not alleviate the “burden” of the CSO as sole attention carrier toward CSR, nor does it strengthen the attention to CSR.

Our study contributes to the literature in three ways. First, we extend literature on ABV testing the combined influence of multiple principles of attention; that is, we show that the principles of attention selection, attention structures and situated attention can mitigate the direct influence of attention carriers. These findings suggest that diverse organizational and contextual factors that represent the three attention principles can partly substitute the attention carrier of specific issues. Second, we contribute to literature on the influence of the CSO on CSR as it has produced inconclusive results (Velte & Stawinoga, 2020). Our findings suggests that the presence of a CSO is related to both internal and external CSR, but that this effect is greater for the more substantive, internal organizational activities than external communicated CSR. This suggests that, globally, CSOs are related to substantively increased CSR activities, thus reinstating the faith that CSOs transcend their symbolic function (Eccles & Taylor, 2023; Peters et al., 2019). Third, we contribute to CSR literature as we examine boundary conditions regarding firm- and country-level characteristics (e.g., CSO, CSR committee, board diversity, and home country CSR standards) that firms can potentially use to increase their CSR. We find that these firm- and country-level characteristics may affect a CSO’s positive influence on CSR, suggesting that they act as alternative attention carriers of CSR and alleviate the role of the CSO as the sole attention carrier. Hence, we underline the interdependencies of firm- and country-level characteristics and their influence on CSR activities of firms.

Literature Review

CSOs and CSR

Research acknowledges that top management is crucial for organizational outcomes (Carpenter et al., 2004), including CSR (Endrikat et al., 2021; Galbreath, 2018; O’Sullivan et al., 2021). Upper echelons theory explains firm behavior through its senior executives’ recognition and interpretation of issues in their environment (Hambrick & Mason, 1984). In support of this, several studies find that the characteristics of executives are connected to the CSR activities of firms (Slater & Dixon-Fowler, 2009; Tang et al., 2015; Wong et al., 2011). However, others argue that executives like CEOs cannot focus solely on CSR-oriented strategies (Waldman et al., 2006). Therefore, recent research has shifted toward other top management team members (Peters et al., 2019), focusing on the CSO when discussing CSR-related topics.

We define a CSO as a top management team member or executive who is primarily responsible for CSR-related topics in an organization (Strand, 2013, 2014). The CSO increases the awareness of CSR topics in the organization, relative to the many other issues that compete for top management’s attention and resources (Fu et al., 2020). A CSO’s main role is to formulate, execute, and subsequently supervise a firm’s CSR strategy (Fu et al., 2020). Firms with a CSR strategy integrate CSR initiatives and solutions in their framework to achieve a competitive advantage (Fatima & Elbanna, 2023; Porter & Kramer, 2006).

In terms of CSR, the literature (Hawn & Ioannou, 2016; Surroca et al., 2020) distinguishes between substantive CSR activities with a long-term orientation (internal CSR), and initiatives that seemingly focus more on receiving public endorsement than on making long-term changes to a firm’s practices and routines (external CSR). Internal CSR “reflects an inward-looking perspective and involves substantive actions targeting those internal stakeholders upon which the firm relies on developing intangible resources that are critical for business success.” (Surroca et al., 2020, p. 901). Internal CSR thus focuses on generating policies and a corporate governance structure for the firm to set up a long-term plan for changing core practices, norms and routines that substantially advance CSR. External CSR, on the other hand, “reflects communication patterns and highly visible public initiatives intended to influence external audiences to generate public endorsements of the firm, its management, and its practices.” (Surroca et al., 2020, p. 901). In essence, external CSR is more about claims that firms are making about their CSR activities, as well as reports and other communications about past CSR successes, and future goals or targets of the firm.

Some argue that the very presence of a CSO already signals a firm’s commitment to CSR activities to its stakeholders (Velte & Stawinoga, 2020). This suggests that the presence of a CSO may also merely be a symbolic action, taken to satisfy stakeholders without resulting in actual substantive CSR activities by the firm (Peters et al., 2019). This questions the actual influence of CSOs on CSR (Aguilera et al., 2021; Bams & van der Kroft, 2023; Velte & Stawinoga, 2020). Existing research and stakeholders at large have expressed concerns that the presence of a CSO could be interpreted as “marketing” or “greenwashing” instead of resulting in actual CSR activities (Eccles & Taylor, 2023; Peters et al., 2019). For instance, critics may argue that CSR activities are primarily there to seek public endorsement without generating substantive content or contributions (Surroca et al., 2020). Indeed, some studies show that firms with a CSO did not perform any better in financial, environmental, and social terms, in comparison with their non-CSO counterparts (Henry et al., 2019). Strand (2013), for example, shows that firms with CSOs are more likely to be listed on indexes like the Dow Jones Sustainability Index, which can increase the image of the firm toward investors and other stakeholders. Relatedly, CSOs are likely to be included in the C-suite after a crisis that compromises the legitimacy of the firm (Strand, 2014). These studies seem to support the idea that having a CSO may be more symbolic, primarily focused as a signal and external communication of CSR rather than actual organizational action (Surroca et al., 2020).

However, research also shows that the influence of the CSO transcends this symbolic value, as CSOs are leading the CSR-related discussion, initiatives, and strategy development in firms (Eccles & Taylor, 2023) and are likely to substantially improve CSR performance (Eccles & Taylor, 2023; Fu et al., 2020; Peters et al., 2019; Wang et al., 2024). For instance, Peters and colleagues (2019) argue that, depending on their specific sustainability expertise, CSOs positively influence the firm’s CSR performance. CSOs can substantively influence CSR of firms by, for example, initiating concrete projects to advance ethical labor circumstances and gender equality within their organization, or to mitigate the negative environmental impact of the firm (Gupta et al., 2021). Hence, existing research is inconclusive about the issue whether CSOs are present for symbolic reasons only, or to improve CSR actively and substantively within their firms.

An ABV on CSR

Attention is defined as “the noticing, encoding, interpreting and focusing of time and effort by organizational decision-makers on both (a) issues: the available repertoire of categories for making sense of the environment; and (b) answers: the available repertoire of action alternatives” (Ocasio, 1997, p. 189). Attention is a scarce resource, and organizational decision-makers have to decide which issues they select to attend, at the expense of other issues (Ocasio, 1997; Simon, 1947). ABV highlights that a firm’s attention process, and thus its strategic decisions and behavior are connected to cognitive explanations, like senior executives’ perception and attention (Hambrick & Mason, 1984), as well as the structural organization and channels in firms that direct attention (Joseph & Ocasio, 2012). The attention determines or facilitates “organizational moves,” or actions (Ocasio, 1997), meaning that an organization devoting attention to certain specific issues rather than others will also increase its related activities. For instance, Zhao et al. (2016) show that top managers exhibiting higher levels of attention to social issues will initiate more practices and programs to address such issues. Furthermore, a study by Muller and Whiteman (2016) shows that firms with a philanthropic orientation are more likely to make corporate donations to regions impacted by natural disasters. These studies support the idea that focusing attention on certain issues results in organizational actions in that same direction.

ABV discusses three principles that influence firms’ attention toward a specific issue and related action (Ocasio, 1997; Pinkse & Gasbarro, 2019). First, firms’ attention is limited. Due to time and resource constraints, firms cannot focus on all aspects within their environment and thus cannot act upon them all (Pinkse & Gasbarro, 2019). Instead, firms selectively focus on stimuli based on their own and their decision-makers’ preconceptions: selective attention. Without making a conscious decision to include CSR goals in a firm’s strategy, it is unlikely that it will direct attention toward CSR issues and take organizational action to advance them. Second, attention depends on the organizational structures of the firm. Important attention structures are procedural and communication channels, like committees and regular meetings, that can support the guiding of attention toward specific issues (Joseph & Ocasio, 2012; Ocasio et al., 2018), like CSR. If firms do not have the structures in place to allocate focus toward CSR, they are more likely to ignore the issue (Galbreath, 2011). Third, attention depends on the context in which the firm and its decision-makers are situated (Ocasio, 1997). An example of a salient context that may influence situated attention is the national environment where a firm operates, as it may enhance or suppress a firm’s focus on a particular issue (Marano et al., 2022). In the context of our study, CSR-specific standards in the national environment may direct firms’ attention to CSR or not (Durand & Jacqueminet, 2015; Hengst et al., 2020).

CSOs can be seen as influential attention carriers of CSR. Firms with a CSO have reserved specific resources and time to be allocated to their CSR strategy. In addition, CSOs likely have or develop the expertise and cognitive framing that enables them to focus a firm’s attention on CSR. Nevertheless, research on the role of CSOs in influencing firms’ CSR remains limited (Fu et al., 2020; K. P. Miller & Serafeim, 2014). In the upcoming sections, we will hypothesize the influence of CSOs on internal and external CSR and continue to investigate boundary conditions related to the three principles of attention, acting as alternative attention carriers, to further examine the influence of CSOs on CSR.

Hypothesis Development

CSO as Attention Carrier

Attention is an important antecedent of strategic change (Cho & Hambrick, 2006). Especially the upper echelons of the top management team affect a firms’ attention allocation processes (Menz, 2012). Top executives make decisions about the strategic focus of the firm, that is, they decide where the scarce attention of a firm is directed. In turn, the attention devoted to specific topics aligns with the level of resources dedicated to the topic, influencing organizational activities (S. Chen et al., 2015; Ocasio, 1997). Therefore, the more attention specific strategies receive from senior executives, the more resources will be allocated to them, the more action will be undertaken to advance these issues (Muller & Whiteman, 2016; Zhao et al., 2016).

Specifically, CSOs may focus a firm’s attention to CSR activities by putting it on the corporate strategic agenda (Kanashiro & Rivera, 2019). According to ABV, an issue for the strategic agenda is assessed by the executive with the appropriate expertise and legitimacy to judge the issue (Wilson & Joseph, 2015), also called the corresponding attention carrier (Fu et al., 2020). In our context, the CSO acts as the attention carrier of the firm’s CSR strategy. The CSO develops CSR initiatives and solutions, increases their salience among other competing issues, influences firm decisions, and convinces others to spend more time and resources on CSR activities (Wiengarten et al., 2017). The CSO can also further promote and execute specific projects related to CSR issues like ethical labor circumstances, gender equality, or environmental impact (Gupta et al., 2021). In other words, the CSO can support the anchoring of a CSR focus throughout the organization (K. P. Miller & Serafeim, 2014), by making sure attention and subsequent resources are devoted to CSR activities. Hence, we argue that the presence of a CSO is positively related to CSR activities. More formally:

CSR activities can be distinguished into internal CSR, focused on organizational actions, and external CSR, focused on external communication. First, through organizing projects and trainings, CSOs can enhance internal CSR by forming and spreading internal organizational norms and routines, enabling long-term change in the organization (Hawn & Ioannou, 2016). For example, the CSO of a large food and beverage supplier called GEA mentioned that she set up a mentoring program for women to improve the gender balance in the firm (Interview with Dr. Nadine Sterley, Chief Sustainability Officer, 2023). As such, CSOs can shift the allocation of attention and resources to CSR activities, making sure that CSR initiatives are implemented (Fu et al., 2020; Henry et al., 2019; Kanashiro & Rivera, 2019; Peters et al., 2019; Peters & Romi, 2015; Velte & Stawinoga, 2020; Wang et al., 2024).

Second, the CSO is also likely to focus on external CSR by communicating a firm’s CSR efforts and achievements. It is part of the CSO’s task to develop and maintain relationships with internal and external stakeholders (K. P. Miller & Serafeim, 2014). The communication about CSR commitments and achievements can include symbolic CSR, meant to appease stakeholders’ expectations rather than to make substantial changes in a firm’s behavior (Hawn & Ioannou, 2016; Surroca et al., 2020), but can also concern communications about actual CSR activities. For instance, CSOs externally communicate that their firm attaches importance to CSR issues, how it progresses on them, and which successes have been achieved regarding CSR goals. As internal and external CSR are interconnected, we expect CSOs to have a positive influence on both internal and external CSR.

From an ABV point of view, CSOs are the attention carriers of the firm’s CSR strategy and help to direct organizational attention to CSR issues and solutions (Fu et al., 2020). This attention is primarily related to organizational action (Ocasio, 1997). As CSOs contribute to increase the awareness, legitimacy, and importance of CSR issues among all potential strategic issues for the firm, more CSR activities are undertaken that directly contribute to social and environmental aims both within the organization and its environment (Gupta et al., 2021; Muller & Whiteman, 2016; Zhao et al., 2016). This organizational action, including donations, trainings, and projects, enables the long-term change of organizational norms and routines, which represent internal CSR activities (Hawn & Ioannou, 2016). For instance, in a recent article, scholars show that CSOs are primarily responsible for eight tasks: ensuring regulatory compliance, environmental, social, and governance (ESG) monitoring and reporting, overseeing the sustainability projects portfolio, managing stakeholder relations, building organizational capabilities, fostering cultural change, scouting and experimenting, and embedding sustainability into processes and decision-making (Farri et al., 2023).

While the activities of CSOs reflect both internal and external CSR, we argue that CSOs as CSR attention carriers, are likely to emphasize the initiation of substantive, internal, CSR activities more than the external communication of CSR achievements toward external stakeholders. This is because, according to ABV, the devotion of attention directly relates to actual organizational action (Muller & Whiteman, 2016; Zhao et al., 2016), that is, to internal CSR. Furthermore, extensive research confirms the focus of CSOs on substantive CSR activities (Eccles & Taylor, 2023; Peters et al., 2019; Wang et al., 2024), suggesting a stronger influence of the CSO on internal CSR than external CSR. Therefore, while we highlight that CSOs will positively influence both internal and external CSR activities, we expect that this influence will be especially strong for internal CSR. Formally:

Boundary Conditions of CSO Influence

The presence of CSOs may not always relate to more firm CSR activities (Henry et al., 2019; Peters et al., 2019; Velte & Stawinoga, 2020). The extent to which a CSO as attention carrier influences CSR can be affected by the three attention principles that also influence the attention of firms for CSR topics. In other words, we argue that certain characteristics of the firm and its environment may act as alternative attention carriers of CSR. Specifically, we argue that the influence of CSOs on CSR is less dominant when the composition of top management in other ways enhances the attention capacity of the firm for CSR (selective attention principle), when organizational structures also direct attention to CSR issues (attention structures principle), and when the national context affects CSR behavior of firms (situated attention principle). We will discuss each consecutively.

Selective Attention Through Board Diversity

In general, attention is limited. Time and resource constraints prevent firms from allocating attention and resources to all issues that are advanced by actors within the firm (Ocasio, 1997; Pinkse & Gasbarro, 2019). According to the selective attention principle of ABV, people and firms focus their attention selectively, based on their own preconceptions and experience, instead of trying to focus on all issues collectively. An influential group of actors in terms of CSR decision-making is the board. A diverse board equals a diverse set of preconceptions and knowledge, which improves decision-making, as diverse boards can present and discuss distinct opinions and perspectives and can source information and issues from a wide variety of stakeholders in the environment (Endrikat et al., 2021). Specifically, having a more diverse board enables companies to increase attention to issues like CSR (Bear et al., 2010).

Boards can be diverse in many ways. For example, research shows that the gender of managers influences their perspective on CSR (Bear et al., 2010; G. Chen et al., 2016; Francoeur et al., 2019; Wu et al., 2022), and as such board diversity makes it more likely that these boards devote attention to CSR. Other research shows that diversity in, among others, tenure, demographic characteristics, and previous board experience can influence firm performance in general (Fernández-Temprano & Tejerina-Gaite, 2020), while CSR-specific research shows that demographic diversity is associated with increased CSR, such as eco-innovation (Zaman et al., 2024). In addition to demographic characteristics, board diversity based on industry experience can increase firm value (Huang et al., 2023). For example, research implies that the firm’s attention allocation on CSR is often inspired by the CSR of their industry peers (Wang et al., 2024). Specifically for boards, directors’ industry experience represents their information and knowledge generated in that specific industry context, where the more diverse the industry experiences, the more diverse the knowledge (Ortiz-de-Mandojana & Aragon-Correa, 2015).

Based on the above, we argue that board diversity influences the relationship between CSO presence and CSR. Generally, more diverse boards are receptive to more diverse issues, having more diverse individual preconceptions that influence their attention span. A low board diversity will mean that the board has a more singular focus area as the selective attention of the board members is based on similar preconceptions and experiences of the board members. Boards with low diversity are therefore more likely to focus primarily on their main task, which is, to monitor executive managers to maximize shareholder wealth (Fama, 1980; Sandvik, 2020). A higher board diversity means that collectively, the board members themselves may contribute with a multiplicity of issues based on their individual experiences, including CSR issues that came to their attention through previous appointments and experiences. This increases the likelihood that the board also directs attention to CSR issues and solutions, meaning that the CSO will not be the only actor that focuses on CSR. In other words, the level of board diversity can act as an alternative attention carrier of CSR, which mitigates the influence of CSOs on CSR. More formally:

Attention Structure Through a CSR Committee

In line with the second ABV principle, organizational structures can support the channeling of attention toward certain issues at the expense of others (Pinkse & Gasbarro, 2019). Organizational structures that influence a firm’s attention are the internal channels that support strategic decision-making and implementation (Ocasio, 1997). An example of such structures that may support top management to achieve certain strategic outcomes (Johnson et al., 2013), are committees that boards appoint to act as communication channels for specific strategic topics. Especially CSR committees, defined as “corporate subcommittees of boards of directors that make social and/or environmental recommendations to the boards and assist board members in their CSR-related functions” (Velte & Stawinoga, 2020, p. 337), may be valuable for the channeling of organizational attention to CSR topics. For instance, Velte and Stawinoga (2020) show that the presence of the CSR committee positively influences CSR reporting.

If there is no CSR committee, there is no dedicated organizational structure that supports the channeling of attention toward CSR other than the CSO. Hence, the CSO remains the prime attention carrier of CSR strategy within the firm. If firms do have a CSR committee, however, it may influence the role of the CSO in such a way that the CSR committee could partially substitute for the CSR attention carrier role of the CSO (Dixon-Fowler et al., 2017). In other words, the presence of a CSR committee forms part of the procedural and communication channels within the organizational structure that direct attention to CSR as well (Dixon-Fowler et al., 2017; Endrikat et al., 2021; Radu & Smaili, 2022; Velte & Stawinoga, 2020). In sum, the CSR committee can act as an alternative attention carrier for CSR; its presence mitigates the influence of the CSO on CSR. More formally:

Situated Attention Through National CSR Standards

Situated attention refers to the context in which firms and decision-makers are situated and which influences the issues they focus attention on (Ocasio, 1997; Pinkse & Gasbarro, 2019). In essence, it relates to the social and environmental context that influences the social cognition of decision-makers in firms (Ocasio, 1997). The social cognition of decision-makers is influenced in a way that issues are more likely to receive attention from these decision-makers when the direct environment of their firm emphasizes those issues as salient and urgent (Joshi & Hemmatian, 2018). For example, Pinkse and Gasbarro (2019) explain that climate change is an issue that firms focus more attention on when they experience climate-related threats in their direct institutional environment. Others also show that environmental pressures in the form of national governmental actions play a role in environmental behavior of firms (Dharmapala & Khanna, 2018; Kanashiro & Rivera, 2019; Qi et al., 2020).

In our study, context refers to the CSR standards of the firm’s home country. Countries have different CSR standards and regulations that firms need to comply with to secure their legitimacy in the country (Beddewela & Fairbrass, 2016; Durand & Jacqueminet, 2015; Fooks et al., 2013; Hunter & Bansal, 2007; J. Miller, 2008). If a country has low CSR standards, the underdeveloped institutional regulations are less likely to pressure firms into developing CSR practices (Tashman et al., 2019). In other words, this contextual situation does not motivate firms to focus attention to CSR. If a country has high CSR standards, it will put pressure on firms to focus attention on CSR to increase their legitimacy (Beddewela & Fairbrass, 2016; Fooks et al., 2013; J. Miller, 2008). It is thus likely that firms, striving to enhance their legitimacy, allocate attention and resources toward CSR when the behavioral norms and regulatory pressures regarding CSR in the national environment stimulate CSR activities (Campbell, 2007; Reddy & Hamann, 2018; Rhee et al., 2021). In such situations, when institutional pressures in the form of CSR standards steer a firm’s attention to CSR (Beddewela & Fairbrass, 2016; Fooks et al., 2013; J. Miller, 2008), the role of a CSO as attention carrier is less important. In other words, higher CSR standards in the home country of firms can act as an alternative attention carrier for CSR, which diminishes the influence of the CSO on CSR. More formally:

Methods

Data Sources and Sample

We created a sample from two main data sources: Thomson Reuters’ EIKON ESG Database, and BoardEx. First, EIKON is a global CSR data set that captures ESG-related data for a wide range of global firms (Ioannou & Serafeim, 2012; Rathert, 2016). We first obtained ownership information on all globally listed firms in this database, after which we matched them with the BoardEx data. From this database, we extended our data with other data sources like Compustat. Excluding missing values, we compiled a final sample of 3,470 firms, from 54 countries and a total of 16,570 firm/year observations between 2012 and 2019.

Dependent Variables: Internal and External CSR

The EIKON data set is used to construct our measure of Internal CSR and External CSR. Research analysts of EIKON annually collect 900 evaluation points per firm from their CSR reports, annual reports, nongovernmental firms’ websites, and numerous other news sources. Subsequently, they create ESG-related scores, in which they account for industry and firm size biases. Similar to existing research (Hawn & Ioannou, 2016; Surroca et al., 2020), we use the developed indexes by Hawn and Ioannou (2016) for internal and external CSR, as we take the average of the combined single items of the EIKON dataset and standardize the resulting two measures. 1 The items used for both measures were carefully selected and represent CSR activities that reflect more internally, or externally oriented actions and policies in terms of reporting and disclosure of claims (Hawn & Ioannou, 2016). For instance, the items for internal CSR reflect activities that are integrated in the organization to reach long-term CSR sustainability (e.g., using ISO 14000 in their selection process of suppliers). In essence, internal CSR reflects activities that require a significant commitment of resources and organizational changes in practices, norms, and routines (Surroca et al., 2020).

The items for external CSR reflect the reporting of different CSR activities (e.g., reporting on initiatives to reduce environmental impact). They often reflect communication to external stakeholders about the firm’s past activities or future plans (Surroca et al., 2020). Hence, while both internal and external CSR cover a range of different CSR-related topics (i.e., from human rights to environmental issues), the measures as defined distinguish between actual policies and implementation of activities that require a vast sense of resource commitment and change of routines (internal CSR) and lower-cost actions of reporting of CSR-related activities and plans (external CSR). The Cronbach’s alpha is 0.792 for internal CSR, and 0.800 for external CSR, showing a good internal consistency and reliability of both measures. The complete list of items, including their description, can be found in our Supplementary Appendix. The mean CSR scores per country can be found in Appendix A. 2

Independent Variable: CSO

Following existing research (Fu et al., 2020), we determined whether a CSO was present in a firm based on the BoardEx database. BoardEx primarily uses information from proxy statements and 10-K reports. Following Fu and colleagues (2020), we determined whether firms had a CSO in two steps. First, we retrieved all information about all senior managers and executives for the firms in the sample from BoardEx. Second, we used the words listed by Fu and colleagues (2020), that is, “sustainable,” “sustainability,” “ethics,” “responsibility,” “environment,” and checked whether they were present in the position titles of the top managers of the firm. Subsequently, we coded the existence of a CSO in a firm/year observation as 1 if we found one or more top managers with such words in the position title and 0 for each firm/year observation without such words mentioned. Appendix B provides information on the number of firms with a CSO for each country in our sample. Appendix C shows a figure of the percentage of firms in our sample that had a CSO over the years. For instance, we see that around 20% of our total sample has a CSO, while this increases up to 26% in 2019; the presence of a CSO is especially booming since 2017.

Moderators

Board Diversity

The literature measures board diversity in many ways. For instance, Harjoto et al. (2018) examine board diversity based on gender, race, age, tenure, and expertise. Zaman and colleagues (2024) use aspects related to both demographic diversity (e.g., gender, tenure) and structural diversity (e.g., size, board compensation). Katmon et al. (2019), finally, use a combination of gender, educational level and background, age, ethnicity, tenure, and nationality to measure board diversity. However, in the context of studying CSR activities, some diversity measures may cause endogeneity issues as having a diverse board can also be viewed as CSR. Therefore, we examine board diversity based on a measure that is relevant for, but not directly related to CSR: the diversity in terms of industry experience within the board. Industry diversity reflects the experience background of the board members, in which a diverse set of experiences will create a diverse set of viewpoints toward organization assets. Experience diversity enhances the boards’ understanding of the firms’ external environment, creating a more effective decision-making within the board. In turn, it enhances a board’s capability to come up with alternative solutions and innovations to increase the focal firms’ business environment and CSR (Bear et al., 2010).

Following existing research (Sabanci & Elvira, 2024; Semadeni et al., 2022), we measure board industry diversity with the Blau Index based on individual members’ dominant industry background (the industry in which each board member served longest before commencing their current board position). We measure the industry based on the three digit SIC codes. The measure ranges from 0 to 1, where 1 means maximum diversity. The data of all board members’ working history are derived from BoardEx, and the SIC industry information is from Compustat.

CSR Committee

For this measure, we created a dummy variable that expresses whether the firm had any CSR-related committees in each year. We identified a CSR committee similarly to how we identified a CSO (Fu et al., 2020), coding it as a CSR committee if the committee description of BoardEx included any of the words as described previously.

CSR Standards

To measure the CSR standards of the given country, we focus on its institutional quality as this is widely used in CSR literature to measure counties’ norms and regulations, including those for CSR (Keig et al., 2019; Marano et al., 2017; Rathert, 2016). Following existing research (Kaufmann et al., 2006; Klopf & Nell, 2018; Kostova et al., 2020), we use the first principal component analysis (PCA) of the World Governance Indicators (WGI), which involves six categories to proxy for key dimensions of the countries’ institutional quality: control of corruption, government effectiveness, voice and accountability, rule of law, regulatory quality, and political stability. The higher the score, the higher the CSR standards of the country. These data are from The World Bank.

Control Variables

In addition to our previously described variables, we included various controls. First, we controlled for firm size as the natural logarithm of the total assets (Ioannou & Serafeim, 2012). In addition, we control for the return on assets (ROA) as the natural logarithm of the ratio between net income and total assets. Furthermore, we control for the liquidity of the firm as extra liquidity can be invested in CSR-related initiatives (Bansal, 2005). Following Marano et al. (2017), we measure this as the natural logarithm of the ratio between current assets to current liabilities. Firm size, ROA and liquidity were derived from Compustat. Second, we controlled for several board-related characteristics like the independent director ratio, board size, and number of board committees. The independent director ratio is measured as the total number of independent directors relative to the total number of board directors in that given firm/year (Fu et al., 2020). The other two board-level controls are count measures, in which board size is the number of total directors, and board committees the total number of committees. All board-level measures are derived from BoardEx. Third, similar to existing research (Surroca et al., 2020), we controlled for the previous internal and external CSR levels of the firm to show which effects go above and beyond the expected pattern. Fourth, we also include the natural logarithm of the total number of total subsidiary countries and total subsidiaries. CSR is heavily affected by both home and host country pressures (Campbell et al., 2012; Rathert, 2016), where firms may need to devote more attention to different units and countries depending on the breadth and depth of their MNE portfolio. Therefore, a larger exposure of the country can generate more pressures for CSR, meaning that these two international MNE portfolio characteristics can influence CSR as well.

Estimation Model

First, we conducted the Hausman test to check for the unobserved heterogeneity. This test was statistically significant (p < .001), which suggests that the fixed and random effects models differ significantly from each other. Therefore, similar to existing research on CSOs, we opt for a panel linear regression model with firm fixed effects (Fu et al., 2020), which automatically controls for industry and country effects. The variance inflation factor (VIF) for our models is on average 1.70, which is considerably below the threshold signaling multicollinearity risks (Cohen et al., 2014). To control for autocorrelation and heteroskedasticity, we added robust standard errors clustered on firm level to our models. Finally, we lagged all independent variables with 1 year.

When choosing our main analysis method, we need to consider that the presence of a CSO is not necessarily a random decision by the firm. In essence, the presence of a CSO may come with endogeneity issues as the current CSR activities of a firm may be a strong determinant of appointing a CSO (Fu et al., 2020). To adjust for this, we instrumented the potentially endogenous variable (in our case the presence of a CSO) with an instrumental variable that is exogenous to the dependent variable of firm CSR. We argue that firms are likely to follow their industry peers in terms of their executive positions (DiMaggio & Powell, 1983) but that this trend may not have a direct link to a focal firm’s CSR activities (Fu et al., 2020). Furthermore, existing research argues that the industry average of an independent variable accounts for an appropriate instrument to address endogeneity concerns (Fu et al., 2020; Liu et al., 2020). Therefore, following existing research, we instrument the CSO presence in the focal firm with the number of firms with a CSO in the same industry of the focal firm (Fu et al., 2020). This accounts for the main assumptions in an instrumental variable approach that the IV is strongly correlated with the main independent variable (likelihood that the focal firm has a CSO), that the IV does not directly influence our dependent variable (CSR activities), and that it is uncorrelated with the error term in the second-stage model of the approach. Following Flammer (2018), we regress a two-stage-least-squares (2SLS) model that calculates the likelihood of CSO presence on the previously mentioned variables and the total number of CSOs per industry in a given year. The industry is determined by means of the two-digit SIC code. This results in a predicted CSO presence that is reliant on the industry instead of the information from the firm itself. The final CSO count ranges from 0 to 114 with around 29 CSOs per industry/year on average.

For the analysis, we use the instrumental variable analysis approach in STATA (xtivreg), which creates a first-stage model and automatically regresses the instrumental variable for the main independent variable and interactions in the second-stage model. Table 1 displays the results from our first-stage regression results of the 2SLS with firm-fixed effects, in which we instrument our CSO dummy using the instrumental variable of the total CSOs per industry per year. We see that, consistent with prior research (Fu et al., 2020), the industry CSO count was positive and significant (β = 0.005, p < .001), which confirms that the instrument predicts the likelihood of having a CSO in the focal firm. Subsequently, to evaluate the strength of our instrument, we conduct the Stock–Yogo weak ID test (Hennig et al., 2023; Stock & Yogo, 2005), and see that our F-statistic exceeds the critical value of 16.38, which confirms that the instrument is strong.

First-stage Regression Results.

Note. Table reports the first-stage regression of the 2SLS analysis using industry CSO total per year as the instrument variable. Robust standard errors are clustered at the firm level, and p values are provided in parentheses. Number of observations: 16,570. Number of firms: 3,470.

Are in natural logarithm.

Our final approach is a 2SLS approach with instrumented main variables and subsequent interaction variables, firm-fixed effects, 1-year lagged independent variables, and firm-clustered robust standard errors. We additionally performed several robustness checks, including different measures and a different type of analysis. These will be discussed after the results.

Results

Descriptive Statistics

Table 2 shows the descriptive statistics and correlations for our variables. For instance, the average board has around 10 directors, and around 22% of the firms have a CSO. Furthermore, on average, boards have around 4 committees; 2 out of 10 firms have a specific CSR-committee.

Descriptive Statistics.

Note. Total observations = 16,570. Internal and external CSR are standardized in the models and thus have a mean of 0 and a SD of 1.

Are in natural logarithm.

Second-Stage Regression Results

We performed all our regressions on both internal and external CSR as our main dependent variables. Table 3, Models 1 and 2 show the results of Hypothesis 1, which suggested that the presence of a CSO positively influences internal (Model 1) and external CSR (Model 2). The coefficient of CSO presence on CSR is positive and significant for both internal CSR (β = 1.902, p < .001) and external CSR (β = 1.470, p < .001). This indicates that having a CSO is significantly related to higher CSR, supporting Hypothesis 1a. To examine Hypothesis 1b, which argues that the positive effect of the CSO on CSR is greater for internal than external CSR, we compare the effect sizes between Model 1 and Model 2. As our dependent variables are standardized, we can directly compare the effect sizes between both models. We see that the effect of a CSO is stronger for internal CSR than external CSR as the former increases with 1.9 standard deviation with the presence of the CSO, whereas external CSR increases with 1.5 standard deviation with the presence of the CSO. This supports Hypothesis 1b. However, as we base these conclusions on our instrumental variable analysis, we need to interpret the effect sizes with caution. We will discuss this in our robustness section.

Instrumental Variable Analysis With Instrumented CSO and Moderators, Firm-Fixed Effects, and Clustered Standard Errors.

Note. Table reports the second-stage regression of the 2SLS analysis using industry CSO total per year as the instrument variable. Robust standard errors are clustered at the firm level, and p values are provided in parentheses. All independent variables are lagged with 1 year. The dependent variable is the standardized measure of internal CSR for the uneven models, and external CSR for the even models. Number of observations: 16,570. Number of firms: 3,470.

Are in natural logarithm.

Models 3 and 4 show the results of Hypothesis 2, which suggested that board diversity mitigates the relationship between the CSO and internal and external CSR. The interaction coefficient is negative and significant for internal CSR (β = −5.157, p < .001) and external CSR (β = −3.876, p < .005), meaning that we can support Hypothesis 2. Models 5 and 6 display the results for Hypothesis 3, which argued that the presence of a CSR committee mitigates the relationship between the presence of a CSO and internal and external CSR. The coefficient for internal CSR is negative and significant (β = −0.847, p < .1), but not significant for external CSR (β = −0.524, p = .185). In addition, the effect for internal CSR does not remain significant when including our other moderators (Model 9 and 10). Hence, our results only marginally support Hypothesis 3, showing that a CSR committee only slightly diminishes the influence of a CSO on internal CSR. The results for Hypothesis 4 are displayed in Models 7 and 8 of Table 3. The interaction coefficient is negative and significant for internal CSR (β = −0.393, p < .05) and external CSR (β = −0.048, p < .1). However, this effect does not remain significant when including our other moderators (Model 9 and 10). Therefore, we find marginal support for Hypothesis 4. The main hypotheses and the board diversity interaction results remain robust across all models. In sum, we support Hypotheses 1a, 1b, and 2, marginally support Hypothesis 3 for internal CSR, and marginally support Hypothesis 4.

Robustness Checks

We provide additional tests to check for alternative explanations and the robustness of our results. First, while we follow previous research and include year effects indirectly through our year-sensitive instrumental variable (Fu et al., 2020), we additionally control for the year effects by including a continuous year variable to our model (Menz & Scheef, 2014). The year control is positive and significant, meaning that later years will increase the CSR of a firm. Our main results largely remain unchanged, while we find stronger evidence for the moderating effects for internal and external CSR.

Second, instead of measuring the CSR standards of a country based on institutional quality, we use a more CSR-specific variable; the sustainable competitiveness index of Solability (Hoinaru et al., 2020; López-Ruiz et al., 2019). Solability comprises a global sustainability competitiveness index (GSCI) based on 131 quantitative indicators from sources like the World Bank and UN (Strand et al., 2015). In turn, these indicators are categorized in five sub-indexes namely: natural capital, resource efficiency and intensity, intellectual capital, governance efficiency, and social cohesion. The index essentially captures a country’s capability and standards in terms of several CSR-related issues. For instance, it captures the health, security, freedom, equality, and life satisfaction within a country, and includes the efficiency of using available resources as a measurement of operational competitiveness in a resource-constraint world. We use the aggregate GSCI based on the subindexes, where a higher score characterizes a higher CSR standard within the country. We manually collected these data per year from the Solability annual documents that are published on their website. The interaction results remain robust for internal CSR, but not for external CSR. Furthermore, Hypothesis 2 did not remain robust, while Hypothesis 1a, 1b, and Hypothesis 3 did for internal CSR.

Third, while we use a global sample, a considerable number of U.S.-based firms are included. To check whether our results remain robust without the U.S. firms, we ran our models with a subsample (N = 9,828) excluding them. Our results remain robust for most of our hypotheses, while our moderation effects of CSR standards for external CSR loses explanatory power. This shows that our findings are also applicable to, but not solely driven by, U.S. firms.

Fourth, as mentioned, board diversity can be measured in various ways. To check for different ways of diversity, we ran robustness checks based on four often-used diversity measures: gender diversity, experience diversity, demographic diversity, and the combination of all three. First, we based our measure on the gender diversity ratio of BoardEx, where reverse-scoring this measure gives us the female board representation ratio. The higher the ratio, the higher the proportion of women on the board. Second, experience diversity is often used as different types of experiences (e.g., firm/board tenure and board interlocks) can provide different perceptions on how to manage an organization (Karn et al., 2023). We include measures of experience diversity as we include the standard deviation in the board based on their time in the company, their time on the board, their total number of listed boards they sat on, the total number of current boards they sat on, and the number of qualifications they had. Third, we focus on demographic diversity based on the age distribution and the nationality differences within the board. All variables are from BoardEx and standardized before taken their equally weighted average. Fourth, we combined three dimensions of board diversity, specifically the distribution of age, number of boards, years on board, education, gender, and nationality, to grasp an overarching board diversity measure (Fernández-Temprano & Tejerina-Gaite, 2020). We ran our models with each of the four separate diversity measures and find similar effects for gender-, demographic-, and overall diversity, but fail to find an interaction effect for experience diversity. This shows that, in general, board diversity will likely have a mitigating influence on the effect of CSOs on CSR.

Fifth, we ran a fixed-effects panel regression without the use of our instrumental variable to get a feeling for the magnitude of the effect (Hennig et al., 2023). In our analysis, we see that the presence of a CSO remains to have a positive significant effect, and our attention-based structures mitigate the influence of the CSO. The results especially hold for board diversity on internal and external CSR and are moderately significant for the interaction of CSR standards on internal CSR. The CSR committee moderation is insignificant, meaning that this result does not stay robust over this alternative method of analyzing the influence of CSOs. In terms of effect sizes, we see that the presence of a CSO is positively associated with internal CSR (β = 0.061, p < .001), and external CSR (β = .037, p <.05), which means that the presence of a CSO will enhance a firm’s CSR with 0.061 and 0.037 standard deviation for internal and external CSR, respectively. While this is in congruence with our main results, it also shows that the actual effect of CSO presence may be less influential than suggested in our 2SLS analysis. Specifically, we see that Hypothesis 1a, 1b, and 2 are supported, Hypothesis 3 is not supported, and Hypothesis 4 is marginally supported for internal CSR. Therefore, this test incorporates a nuance to the magnitude of the positive effect of a CSO. We plotted the moderation effects of board diversity to illustrate our results (see Appendix D). We see that, regardless of the level of board diversity, having a CSO accounts for higher internal and external CSR. If there is no CSO, a higher board diversity increases internal CSR up to the same levels when board diversity is high. This suggests that the effect of the CSO is at some point substituted by a high board diversity.

Sixth, when examining our CSR committee moderation effect with the fixed-effects panel regression, we did not find support for our hypothesis. We examine this further by focusing on specific subsamples that consider the timing of the introduction of CSOs versus CSR committees. Here, we build on the fixed-effect regression to examine the effects on the “real-time” data instead of on the instrumented variable. We focused on firms that had a CSO and a CSR committee at some time in our sample. Including this criterion, we created two subsamples: one where the CSO started before the CSR committee (1,199 observations), and one where the CSR committee started before the CSO (1,437 observations). The analyses show a positive and significant moderation only for internal CSR for the subsample where the CSO was introduced after the CSR committee. These results suggest that, for this specific situation only, the CSR committee and the CSO are complementary rather than substituting each other as attention carriers, contradicting H3. This shows that the effect of the CSO, in firms that have a CSR committee as well, depends on the order of the CSO and CSR committee introduction. 3

Seventh, we use a similar instrumental variable panel regression model with firm-level fixed effects to examine the direct effects of the three attention principles and that of the CSO based on our original model but use different dependent variables: social, environmental, governance performance, and on CSR strategy. We include the same control variables as in our main model. All dependent variables are retrieved from the EIKON database, in which the first three represent the three ESG pillars, together covering the complete CSR domain. CSR strategy “reflects a company’s practices to communicate that it integrates economic (financial), social and environmental dimensions into its day-to-day decision-making processes.” (Refinitiv, 2020). For instance, the CSR strategy performance measure reflects whether the firm has an integrated strategy, whether it signed the global compact signatory and whether it adheres to the GRI reporting guidelines. The results show that the presence of a CSO is positively and significantly related to all types of CSR, while the magnitude of the effect is highest for internal and social CSR. In addition, the presence of a CSR committee and board diversity has no direct influence on any type of CSR, and the country-specific CSR standards only has a direct effect on internal-, social-, and environmental CSR, while the magnitude of this effect is at least one standard deviation lower than the effect of the CSO. All in all, the results show that the examined boundary conditions have a minor to no direct effect on different types of CSR when accounting for a CSO as well, which endorses our theoretical underpinning that the CSO primarily influences CSR.

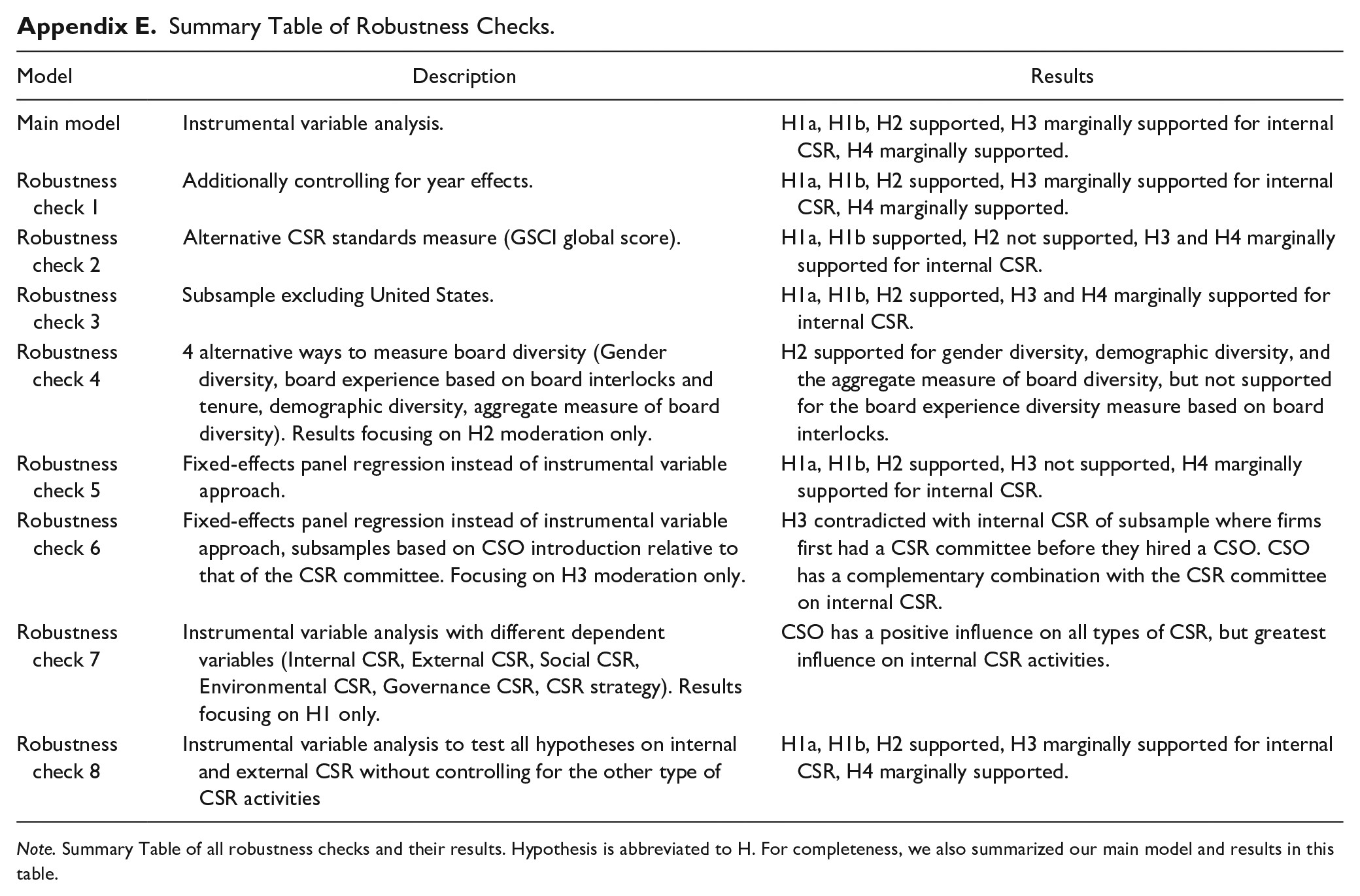

Last, our measures of internal and external CSR activities are interconnected as the disclosure of the CSR activities (more external CSR) is about the activities that are being integrated (internal CSR). To circumvent potential endogeneity issues related to the inclusion of both CSR measures within the same model, we only control for previous internal (external) CSR instead of both internal and external CSR when examining the influence of a CSO on internal (external) CSR. The results remain robust. An overview of all robustness checks can be found in Appendix E.

Discussion and Implications

The rise of CSOs within the upper echelons of firms reflects that the corporate world is aware of the importance of social responsibility and sustainability (Eccles & Taylor, 2023; Fu et al., 2020; K. P. Miller & Serafeim, 2014). While some research has been done on the effects of appointing a CSO (Fu et al., 2020; Henry et al., 2019; Kanashiro & Rivera, 2019; Peters et al., 2019; Peters & Romi, 2015; Velte & Stawinoga, 2020; Wang et al., 2024), existing research remains ambiguous about under which circumstances the presence of CSOs influence CSR (Velte & Stawinoga, 2020). With our global sample, we find that the presence of a CSO relates positively to a firms’ internal and external CSR, with a stronger influence on internal CSR. In addition, we show that the positive effect of the CSO is mitigated when other attention principles form boundary conditions to the effectiveness of the CSO, and act as alternative attention carriers of CSR. We specifically show the mitigating effects of a diverse board (selective attention), a CSR committee (attention structure), and home country CSR standards (situated attention).

Our study has several implications for the literature. First, our work contributes to ABV literature through investigating how the presence of an attention carrier and multiple principles of attention (as alternative attention carriers) for a certain issue result in strategic decisions of firms. While Ocasio (1997) theorized that organizational outcomes are influenced by the three principles of attention, that is, selective attention, attention structure, and situated attention, only few studies provide formal tests of combinations of these principles in firms (Angulo-Ruiz et al., 2020; Galbreath, 2018; Pinkse & Gasbarro, 2019). In particular, a recent review of the use of ABV for understanding behavior of international firms calls for more research that studies the interaction of internal (related to organizational structures) and external (based on situatedness in diverse environements) attention determinants (Andrews et al., 2022). Our study responds to that call as it integrates all three attention principles, and shows that these principles can mitigate the effect of the attention carrier, in our context the CSO. This suggests that the combination of attention principles at different levels (board, governance structure, and national pressures) diminishes the role of the attention carrier and its ability to shape organization behavior. Furthermore, it suggests that the effect of an attention carrier could be substituted with attention principles. We invite future research to design studies to test these findings in other settings and alternative strategic issues.

Second, we contribute to CSR literature (Halme et al., 2020; Hunoldt et al., 2020; Muller, 2020; Velte & Stawinoga, 2020), as we examine the effect of the CSO on internal and external CSR. We complement existing literature that so far produced inconclusive results about the CSO-CSR relationship (Velte & Stawinoga, 2020) as we find strong and consistent evidence that the presence of a CSO is positively related to CSR. Furthermore, we show that CSO presence is particularly related to firms’ internal CSR activities, which suggests that their role goes beyond being merely symbolic or focused on external communication of CSR (Henry et al., 2019; K. P. Miller & Serafeim, 2014; Peters et al., 2019). Our finding that CSOs increase the internal focus on CSR activities supports recent assertions in the literature that CSOs indeed have a role in enhancing substantive CSR (Eccles & Taylor, 2023) rather than the pure symbolic role that has been suggested by others (Aguilera et al., 2021; Henry et al., 2019).

Third, we contribute to CSR research related to the boundary conditions of certain CSR-specific organizational and country-level characteristics. Specifically, we examined the boundary conditions based on board diversity, the presence of a CSR committee, and the CSR standards within a country. While we find that the effect of CSOs on firms’ CSR remains positive, we also find that the mentioned characteristics of firms and environments can act as alternative attention carriers of CSR, hereby alleviating the task of the CSO to be the sole attention carrier of a firms’ CSR activities. This implies that the incorporation of multiple CSR-oriented organizational characteristics (e.g., a CSR committee, a diverse board, and a CSO) may not invariably contribute positively to a firm’s overall CSR activities, and, in certain cases, may substitute one another to advance CSR.

For instance, we show that the magnitude of the effect of a CSO depends on the home country as we show that firms from countries with high CSR standards are less in need of a CSO to increase their CSR activities. The United States, for example, has fewer or less-strict CSR standards and regulations in place than Norway, meaning that U.S. firms benefit more from having a CSO to promote the CSR strategy and activities to internal and external stakeholders than Norwegian firms. In addition, whereas existing research shows that having CSR committees weakens the effect of the CSO (Fu et al., 2020), our results are inconclusive. This warrants further research on the interdependence between a CSR committee and the CSO; and whether they substitute or complement one another. For instance, future studies could investigate whether having more focused CSR committees, working for example for issues like gender equality or circularity, can influence a CSO’s work to advance CSR activities. With regards to board diversity, existing research especially examines the direct relationship between board diversity and CSR (Bear et al., 2010; Fernandez-Feijoo et al., 2012; Katmon et al., 2019; Wu et al., 2022; Zaman et al., 2024), while we show that board diversity mitigates the positive influence of CSOs on CSR, up to a point that a high board diversity could potentially substitute for the effect of having a CSO.

Our findings also have managerial implications. First, our study shows that it is beneficial for firms to appoint a CSO if they are determined to engage in CSR. Appointing a CSO can drive a CSR-focus toward both internal as well as external stakeholders. Furthermore, CSOs may be able to collect relevant information and place CSR issues on the strategic agenda of decision-makers in firms. As such, they can induce a stable focus on the firm’s CSR strategy and subsequently embed CSR practices within the firm. Second, we notice that the presence of a CSO is especially needed in some situations; firms in less CSR-focused countries could strengthen the legitimacy of their CSR ambitions toward both internal and external stakeholders by including a CSO in their executives’ team, and firms with less diverse boards could enable a clear CSR focus by appointing a CSO.

As with every research, our study has some limitations that need addressing. First, while our sample is global, our study uses keywords to identify the presence of a CSO designed for an U.S.-based sample (Fu et al., 2020), whereas other countries may use different words to describe a CSO equivalent. We performed interviews with global headquarters of multiple firms to analyze the title and word-usage in other countries, which gave us the confidence that our current measure for CSO presence is representative for global firms as well. However, future studies may use this research by including case studies or survey research to examine the influence of CSOs further in different international settings.

Second, we did not distinguish among different types of CSOs. Future research may want to examine the personal characteristics of CSOs (e.g., professional background, personality traits, or specific expertise) (Kanashiro & Rivera, 2019), and investigate whether the characteristics of the CSOs result in different levels of CSR. This would create a richer understanding of the influence of CSOs in their firm. Third, our analysis does not explain why firms appointed a CSO in the first place. A CSO may be hired due to the intrinsic motivation of the firm (Fu et al., 2020), or as symbolic signal toward external stakeholders (Peters et al., 2019), or a combination of the two. To mitigate this potential endogeneity issue, we used an instrumental variable approach in our main analysis. While the outcomes may remain similar, future research may want to investigate the mechanisms that explain why certain firms choose to appoint a CSO.

Fourth, especially our hypothesized effect that the CSR committee mitigates the influence of CSOs on CSR remains ambiguous, given that we could not find support for this moderation effect in our alternative fixed-effects regression analysis. We found that the order of introduction of the CSO and the CSR committee as (alternative) attention carriers of CSR in a firm shapes the influence of CSO presence on CSR. Future research may want to investigate the effectiveness of a CSO in combination with a CSR committee by, for instance, examining whether the CSO is appointed by or on instigation of the CSR committee.

Conclusion

Our study emphasizes that CSOs play a positive role in advancing sustainability strategies of firms. Particularly, we find that CSOs, as attention carriers of the firm’s CSR strategy, significantly increase internal and external CSR. In addition, we find that the influence of CSOs is particularly effective in the absence of attention principles that may influence CSR activities; especially when firms have limited board diversity or when they are in countries with low CSR standards. While these alternative attention principles can also attract firms’ attention to CSR, our results suggest that they reduce the influence of the CSO specifically. In other words, we conclude that the economic notion of “marginal returns” also corresponds to the CSO-CSR context, as a combination of attention principles presents boundary conditions and thus mitigates the exclusive influence of CSOs on CSR.

Supplemental Material

sj-docx-1-bas-10.1177_00076503241271224 – Supplemental material for Beyond the CSO: How Alternative Attention Carriers Influence the Role of CSOs on CSR

Supplemental material, sj-docx-1-bas-10.1177_00076503241271224 for Beyond the CSO: How Alternative Attention Carriers Influence the Role of CSOs on CSR by Marloes Korendijk and Rian Drogendijk in Business & Society

Footnotes

Appendix

Summary Table of Robustness Checks.

| Model | Description | Results |

|---|---|---|

| Main model | Instrumental variable analysis. | H1a, H1b, H2 supported, H3 marginally supported for internal CSR, H4 marginally supported. |

| Robustness check 1 | Additionally controlling for year effects. | H1a, H1b, H2 supported, H3 marginally supported for internal CSR, H4 marginally supported. |

| Robustness check 2 | Alternative CSR standards measure (GSCI global score). | H1a, H1b supported, H2 not supported, H3 and H4 marginally supported for internal CSR. |

| Robustness check 3 | Subsample excluding United States. | H1a, H1b, H2 supported, H3 and H4 marginally supported for internal CSR. |

| Robustness check 4 | 4 alternative ways to measure board diversity (Gender diversity, board experience based on board interlocks and tenure, demographic diversity, aggregate measure of board diversity). Results focusing on H2 moderation only. | H2 supported for gender diversity, demographic diversity, and the aggregate measure of board diversity, but not supported for the board experience diversity measure based on board interlocks. |

| Robustness check 5 | Fixed-effects panel regression instead of instrumental variable approach. | H1a, H1b, H2 supported, H3 not supported, H4 marginally supported for internal CSR. |

| Robustness check 6 | Fixed-effects panel regression instead of instrumental variable approach, subsamples based on CSO introduction relative to that of the CSR committee. Focusing on H3 moderation only. | H3 contradicted with internal CSR of subsample where firms first had a CSR committee before they hired a CSO. CSO has a complementary combination with the CSR committee on internal CSR. |

| Robustness check 7 | Instrumental variable analysis with different dependent variables (Internal CSR, External CSR, Social CSR, Environmental CSR, Governance CSR, CSR strategy). Results focusing on H1 only. | CSO has a positive influence on all types of CSR, but greatest influence on internal CSR activities. |

| Robustness check 8 | Instrumental variable analysis to test all hypotheses on internal and external CSR without controlling for the other type of CSR activities | H1a, H1b, H2 supported, H3 marginally supported for internal CSR, H4 marginally supported. |

Note. Summary Table of all robustness checks and their results. Hypothesis is abbreviated to H. For completeness, we also summarized our main model and results in this table.

Acknowledgements

The authors thank the associate editor and the four anonymous reviewers for their insightful comments and support in further developing the article. The authors are also grateful for the feedback and suggestions of Sebastian Firk in earlier drafts of this paper, as well as the comments of Rieneke Slager, Alan Muller, and Hammad ul Haq.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.