Abstract

We investigate the association between a wide range of community-level environmental, social, and governance (ESG) outcomes and the credit risk of U.S. municipal finance fixed-income securities. We develop a novel dataset of multiple ESG outcomes for U.S. counties and connect it to a 2001-2020 panel of municipal bonds issued within those counties. Overall, we find supportive evidence that collective increases in community-level ESG factors (i.e., ESG outcomes) are associated with reductions in credit risk for U.S. municipal finance instruments over time. We theorize that these associations arise from variations in investor perceptions and manifested changes in fiscal health over time as a function of changing ESG outcomes. Post hoc analyses leveraging quasi-exogenous shocks to uncertainty, as well as connecting ESG outcomes to various measures of fiscal health at the county-year level, and credit ratings at the bond-year level, help validate this theory. Our research suggests that even socially agnostic investors should investigate the environmental and social performance of a municipality as part of their credit due diligence.

Despite a strong history in the study of corporations, business and society research has only recently made important strides in understanding how certain individual Environmental, Social, and Governance (ESG) factors are priced into municipal bonds, a $4 trillion market (SIFMA, 2022) that supports community projects from infrastructure to the running of schools throughout the United States. While investing in public-purpose entities that fund health care, education, safety, and public services seems, at first glance, to possess a stronger ESG orientation than investments in for-profit corporations, municipal entities, like their private sector or sovereign counterparts, differ substantially in and across their ESG outcomes. Furthermore, the study of municipalities offers opportunities to directly associate ESG factors at the ecosystem level, 1 where they manifest as society-level outcomes (i.e., ESG outcomes), to the financial performance of public sector organizations and their investors. This “place-based” assessment of ESG outcomes addresses an important link underdeveloped in ESG research that often detaches organizational efforts from where they are located (Nyberg et al., 2022) as well as the study of corporate social responsibility and finance performance, where corporate social initiatives are often disconnected from real-world outcomes (Margolis & Walsh, 2003).

However, much as the developing research on municipal finance has linked place-based climate risk (Gilmore et al., 2022; Goldsmith-Pinkham et al., 2023; Liao & Kousky, 2022; Painter, 2020) and opioid addiction (Cornaggia et al., 2022) to subsequent strain in the financial health of public entities and race-based discrimination to arbitrage opportunities (Dougal et al., 2019; Ponder, 2021; Smull et al., 2023), similar associations may be present with other environmental (e.g., preparedness for the energy transition or emissions) and social (e.g., violent crime, excess mortality, poverty, malnutrition, housing affordability, policing and incarceration) outcomes that influence quality of human life. Although there is a strong interdependence among these ESG factors, research typically studies them in isolation. To address this gap, we explore whether the municipal bond market correctly prices a broad spectrum of ESG outcomes. To clarify the reasons behind the market’s potential mispricing of ESG outcomes, we construct theoretical arguments that link ESG outcomes to investors’ perceptions of credit risk, as well as municipal financial health, which ultimately affect realized credit risk.

We develop a novel dataset and use it to demonstrate that better aggregate ESG outcomes are associated with reductions in credit yields (i.e., risk) for municipal finance securities. Specifically, we combine data from a variety of sources (see Data Appendix 1) to construct an ESG dataset for U.S. counties from 2001 to 2018. We then explore the association between aggregate county-level ESG outcomes and credit risk (until 2020) both contemporaneously and over the long term (i.e., five to seven years). This analysis suggests that ESG outcomes in the aggregate are negatively associated with credit risk, even in specifications that control for time-varying economic (e.g., income) and fiscal (e.g., state aid, property taxes) performance, bond and state-year fixed effects, and a full set of three-way fixed effects that control for the shape of yield curves and other time-varying factors.

The negative association between aggregate ESG outcomes and credit risk generally increases over time. Supplemental bond-year analyses examining the quasi-exogenous shock of increased uncertainty via the Great Financial Crisis and COVID-19 pandemic on investor’s perceptions of credit risk, as well as county-year analyses of migration provide general support for our theory development that better ESG outcomes drive increased perceptions of credit quality, as well as individual and business migration over time, supporting realized changes in creditworthiness. An exploratory analysis attempting to explain who is mispricing, treating ESG index performance as exogenous versus endogenous to credit ratings, suggests that investors and credit rating agencies differentially evaluate the risk of ESG outcomes. We find that county-level ESG outcomes do associate with bond-year credit ratings in most time periods, but whether the changes in credit ratings as a function of ESG are reflected in pricing lessens several years into the future. That ESG outcomes still associate with realized credit risk after this time period suggests that investors perceive a reduced likelihood of credit risk for better ESG outcomes above what is reflected in credit ratings.

Our research contributes to the business and society and municipal finance literature in several ways. First, we highlight an understudied asset class in ESG research. Indeed, the role of municipalities in business and society scholarship has been called out as an underexplored area of inquiry (Dentchev et al., 2017). Akin to the study of green building utilization within real estate investment trusts (Eichholtz et al., 2016), municipal finance provides an ideal context for the study of a variety of ESG outcomes, as municipal governments are directly responsible for such outcomes in their jurisdiction, as opposed to having loose and often debated discretion like corporations (Carroll, 1979, 1999). Municipalities also issue tradeable bond securities like corporations. Due to these unique characteristics, the study of municipal issues overcomes the problems of ambiguity between the integration of organizational activities and social impact as well as the general detachment from place in the business and society literature that focuses on corporations (Margolis & Walsh, 2003; Nyberg et al., 2022). This development allows for objective geospatial measures of ESG outcomes that do not rely on subjective third-party ratings (Atz & Bruno, 2023; Berg et al., 2022; Chatterji et al., 2016; Crane et al., 2017), supporting an ESG research agenda that moves beyond company-level analyses and directly affects public policy. Furthermore, the characteristics of municipalities allow ESG outcomes to directly connect to a municipal jurisdiction to allow for a stronger semblance of ecological validity that has been called for (Busch et al., 2016).

Second, we show that ESG outcomes correlate with credit risk in bundles. Prior municipal finance research had placed emphasis on well-identified individual ESG outcomes, such as sea-level rise (Goldsmith-Pinkham et al., 2023) or increases in drug overdose death rates (Cornaggia et al., 2022), rather than assessing them in aggregate. Such non-pecuniary outcomes may not only influence investors’ perceptions of a municipality or costs associated with addressing them in isolation but in bundles affect the attractiveness of a municipality for (potential) residents (Michalos, 1996), particularly for those with high-incomes (Florida, 2002) and businesses seeking to attract them (Gottlieb, 1995; Granger & Blomquist, 1999).

Relatedly, we introduce a novel database to the study of municipal finance and show how ESG outcomes relate to credit risk over time. To our knowledge, the combination of several aspects of our methodology are unique, such as our use of time-varying yield estimates based on trade data over very long periods of time accompanied by historical credit ratings. Our database allows for the study of realized long-term changes in credit risk through ratings and yield, as opposed to “long vs. short-term” characteristics of bonds at issue (e.g., long vs. short maturity bonds), allowing for analysis of dynamic mispricing over a multi-year period often ignored by focusing on at issue and current yield and pricing.

Third, we show the possibility of a future research agenda that expands the role of government in business and society research. The government is often portrayed as a background actor, engaging in public–private partnerships, providing basic public services, or placing regulatory constraints on organizations with the goal of alleviating societal ails. Yet, seldom do business scholars consider that governments—at the national and township levels alike—have multiple levers, including bond issues, to alleviate long-term social issues. If investors and creditors misprice these levers (i.e., ESG-related investments, such as municipal issues for incarceration programming or toxic emission reduction), they undermine government incentives to invest in ESG outcomes, impacting society and future business prospects in a given region. Recognizing the ways in which these levers may impact perceptions of credit risk and fiscal health re-orients the role of municipal bond creditors. These creditors can better consider the positive impact of municipal ESG investments in supporting fiscally responsible sustainable development. Furthermore, municipal ESG outcomes may support, complement, or demote corporate voluntarism and may accordingly be associated with corporate ESG performance within the same jurisdiction. These insights accordingly support an open systems view of organizational environments in solving social issues, as opposed to narrowly focusing on set groups of organizations in isolation (Schneider, 2020; Stern & Barley, 1996).

Fourth, we contribute to research on ESG and financial performance, a mainstay of business and society research for close to 50 years (Atz et al., 2023; Busch & Friede, 2018; Friede et al., 2015; Margolis & Walsh, 2003; Orlitzky et al., 2003). We demonstrate that connecting ESG outcomes, as opposed to disclosures or certification, to financial performance at the municipal level requires the application of theoretical arguments that draw from residential sorting and migration literature that are not historically applied to this conversation while connecting it to broader public policy discourse. Furthermore, research on ESG and financial performance seldom examines municipalities as an asset class although they provide an ecologically valid unit of analysis for investors looking to connect real-world outcomes to financial performance. There are arbitrage opportunities for investors who recognize this. Our sample, for example, had more than US$2.5 trillion of bond issuance across all years. One basis point of this equates to $250 million.

Strong performance in environmental and social outcomes comes at a cost yet also provides benefits that are factored into municipal finance pricing. Deficit spending, debt, and deteriorations in fiscal health (i.e., measures of the governance of a public entity) typically influence perceived credit risk and are therefore priced. We extend this logic to show that ESG outcomes that may impact future fiscal health are differentially priced by investors and credit rating agencies over time. Such differences provide room for arbitrage. Much as sovereign and corporate investors undertake independent analysis to differentiate between profligate and productive investments, municipal finance investors should similarly develop the data and tools to distinguish between fiscal policies that enhance ESG outcomes which may provide long-term benefits to business growth, migration, and tax base.

Literature

Municipal Bonds Pricing of ESG Outcomes

The risk and pricing of governance factors related to municipal spending, such as levels of debt, have been studied for quite some time (Bahl, 1971; Capeci, 1991; Michel, 1977). Geographic-based environmental and social quality of human life indicators, on the other hand, have been of growing interest mostly in recent years. We discuss studies focused on social factors and environmental factors, respectively, in turn.

Denison et al. (2007) connected school performance to the fiscal management of school districts. Relatedly, poverty rates have been correlated with credit ratings (Grizzle, 2010; Maher et al., 2016), credit yields, and spreads (Grizzle, 2010). Butler and Yi (2019) find that aging populations increase municipal bond yield spreads due to changes in income tax revenue and health care and pension liabilities. In a recent working paper, Chordia and colleagues (2022) find a positive relationship between mass shootings and credit risk. Li et al. (2018) construct a social capital index and show its association with decreased credit yields, arguing that community social capital affects the likelihood of paying future tax obligations.

Studies on the opioid crisis and racial biases have also come to fore. Li and Zhu (2019) and Cornaggia and colleagues (2022) explore the impact of the opioid epidemic and its associated health care costs on credit yields and ratings. Using different identification strategies, they both argue that their results are causal. They also demonstrate evidence that current opioid addiction can predict future fiscal deterioration. Investor biases with respect to race also contribute to perceptions of credit risk, despite the lack of such a substantive relationship to credit quality (Dougal et al., 2019; Fuster et al., 2022; Smull et al., 2023).

On the environmental front, Painter (2020) and Goldsmith-Pinkham and colleagues (2023) find that sea level rise causes long-term credit risk. Early evidence from Rizzi (2022) suggests that natural capital—protected wildlife habitat, such as floodplains—mitigates this risk. A related literature on green bonds, which concerns bonds with the use of proceeds targeted at alleviating climate issues, suggests that investors are willing to take on lower yield for equivalent green, as opposed to conventional, municipal bonds (Baker et al., 2022; Flammer, 2020, 2021; Zerbib, 2019), although the empirical evidence is mixed (Larcker & Watts, 2020).

Sovereign Bonds

Within the sovereign debt market, four recently published papers have brought these arguments together and studied the association between a wide range of ESG factors on sovereign credit risk, particularly over longer time horizons and the incidence of financial crises. Crifo and colleagues (2017) demonstrated that the Vigeo country ESG rating which incorporates information on a variety of environmental (e.g., a country’s air emissions) and social (e.g., health) factors is negatively associated with credit risk. Capelle-Blancard and colleagues (2019) build on this initial finding by constructing their own transparent ESG index based on World Bank data rather than relying on Vigeo’s composite measure and extending the analysis to 1996-2014. Margaretic and Pouget (2018) extend this analysis to 33 emerging markets showing both an association with credit yields as well as the likelihood of financial crisis. Finally, Hübel (2022) further extends the analysis to 60 countries using Robeco SAM data and shows more pronounced effects over longer time horizons.

Corporate Bonds

Following a similar logic, a larger body of academic and practitioner literature has argued and demonstrated that the management of ESG factors reduces future cashflow variance or loan spreads (Bae et al., 2018a, 2018b; Goss & Roberts, 2011), thereby increasing credit ratings (Attig et al., 2013) and reducing the cost of capital and yields (Bahra & Thukral, 2020; Chava, 2014; Sharfman & Fernando, 2008). While ESG operationalization in the corporate sector is distinct from sovereign or municipal public organizations (i.e., it is further from manifested ecosystem-level outcomes), the strong empirical support for an analogous relationship between ESG and credit risk at the sovereign and corporate levels suggests potential extension to municipal entities if a suitable dataset could be constructed.

Theory Development

Why do ESG outcomes relate to municipal credit risk? We emphasize two key factors: investors’ perceptions of future adverse credit events based on ESG outcomes, and actual changes in a municipality’s fiscal health due to ESG outcome variations. It is crucial to acknowledge how these factors build upon existing conceptual frameworks.

A segment of the ESG and financial performance literature investigates how ESG affects credit risk. This is evident in the emerging research on municipal and corporate green bonds (Baker et al., 2022; Flammer, 2020, 2021; Larcker & Watts, 2020; Zerbib, 2019), which primarily focuses on investor preferences for robust ESG, decoupling, and signaling of capabilities (Flammer, 2021). For instance, investors may accept lower yields from high ESG-performing investments (e.g., green bonds) due to their environmental commitment.

Our study concentrates on ESG outcomes rather than ESG labeling (e.g., green bond certification), media-based, or self-reported ESG performance measures as much of this work. Consequently, we use a different set of arguments that prioritize actual ESG outcomes over signaling and information provided by municipal issuers. First, we consider investor perceptions of a municipality based on its ESG outcomes. Second, we predict actual changes in a municipality’s fiscal health due to changes in ESG outcomes.

ESG Outcomes and Perceptions of Credit Risk

There is an increasing body of evidence showing that investors value ESG performance as it influences perceptions of the quality of an organization’s management (Henisz & McGlinch, 2019) and reduces uncertainty when evaluating an issuer’s credit risk (Painter, 2020). These arguments also apply to municipal bonds. Indeed, better ESG performance has translated into lower cost of capital among corporate bonds (Chava, 2014; Sharfman & Fernando, 2008). As Sharfman and Fernando (2008) highlight, credit risk is a function of uncertainty regarding an entity’s future activities (Orlitzky & Benjamin, 2001). Stronger ESG outcomes signal to municipal bond investors a reduced likelihood of future extreme and costly events, such as infrastructure collapses, which could adversely affect a municipality’s ability to pay its creditors.

Such perceptions of credit risk influence bond pricing and corresponding yields, even if associated measures of risk (e.g., credit ratings) do not match those perceptions (Dougal et al., 2019; Smull et al., 2023). Similarly to how corporate social responsibility signals a better reputation and stronger capabilities (Orlitzky & Benjamin, 2001), investors may view a municipality with better ESG outcomes as having superior stakeholder and financial risk management capabilities, leading to lower risk over time. Furthermore, such ESG outcomes may lead investors to trust municipalities with debt accumulation during times of economic uncertainty (Amiraslani et al., 2023). This reciprocal feedback loop leads to a lower cost of capital for future financing of improved ESG outcomes and continually lowers credit risk. Such perceptions of stronger ESG outcomes based on trust in management over the long-term are particularly important to recognize for municipal bonds, which are predominantly owned by retail investors (i.e., households, individuals), have longer maturities than most other bonds, and do not trade as often as most securities after issuance (Green et al., 2007).

Not only do ESG outcomes influence perceptions of municipal management, but they also influence the underlying fiscal health of municipalities. Changes in fiscal health manifest into changes in creditworthiness over time that may not be apparent at issue, or when an investor first purchases or sells a municipal bond. These changes can lead to increased long-term risk as evidenced in recent studies on the impacts of opioid rates (Cornaggia et al., 2022) and climate change (Goldsmith-Pinkham et al., 2023; Painter, 2020) on yield spreads.

Long-term oriented investors may recognize that this development takes time, and accept higher initial risk, investing in low-performing municipalities that are pushing future investment into ESG outcomes. As the studies on wildfires, sea level rise, and opioid mortality highlight, these changes are not just perceptual but also influence the mechanics underlying a municipality’s fiscal performance, such as its revenues and expenditures. Rising opioid mortality rates associate with higher health care costs (Cornaggia et al., 2022), rising sea levels require cities to invest in sea walls (Fankhauser, 1995), and changes in other ESG outcomes, such as the prevalence of wildfires, may influence housing value appraisals and thus the revenue a municipality receives in property taxes (Gilmore et al., 2022). To better understand how ESG outcomes may influence the fiscal performance of a municipality (e.g., its revenues, expenditures, and tax base), we turn next to the theory on amenities and migration.

From Perceptions to Reality: ESG Outcomes, Amenities, and Migration

As we discuss briefly in the introduction, the study of ESG and financial performance has seldom been connected to research on amenities and migration. ESG outcomes at the municipality level can signal a lower risk of extreme negative events analogous to arguments within the sovereign and corporate bond research streams we discussed in the previous sections. However, they may also impact rates of migration, business founding, and the need for increased expenditures to address issues, each of which affects a municipality’s tax revenue and ability to provide public services. Within economics, migration is argued to be the result of Tiebout (1956) sorting into communities that provide the desired array of public services at minimum cost in terms of taxation. In sociology, similar patterns are explained with reference to ecological theory (Massey & Denton, 1985; Massey & Mullan, 1984) where in-migration is an effort, by those who can afford it, to improve status or position “by selecting neighborhoods with richer resources and more amenities” (Massey et al., 1987).

Higher quantity and quality of amenities require investment. Accordingly, perceptions of municipal risk focused on short-term costs from investment in positive ESG outcomes (e.g., expenditure on infrastructure, schools, and public services) may neglect the long-term benefits of migration from such investment. Much as there are time-invariant (or slow moving) regional features, such as moderate temperatures and coastal views (Albouy et al., 2016; Scott, 2010), that affect migration, there are also amenities that residents have a more direct effect on. In the same manner as a migrating family invests in a house, they also invest in a neighborhood and its schools, health, natural environment, and safety (Liu, 1975; Porell, 1982). Empirical results for residential sorting hypotheses have been highly supportive although there has been important concern over whether the benefits of such sorting or benefit-seeking are equally available to disadvantaged racial groups (Massey, 1990, 2007; Massey & Denton, 1988).

Research explaining individual employee and family migration suggests amenities that promote migration (see recent examples of Grimes et al., 2023; Hakim et al., 2022; Hoogerbrugge & Burger, 2022; Howe & Huskey, 2022); however, the study of business migration as a function of amenities is slightly less developed. Transportation infrastructure, agglomeration benefits (Rosenthal & Strange, 2004), and taxes are often cited for such movement (Faggio et al., 2017; Grimes et al., 2023; Strauss-Kahn & Vives, 2009) although broader amenities may cause re-location and openings as well. A complementary pair of papers explores the association between similar quality of human life indices on the rate of business entry into a geographic area. Building on the migration studies cited earlier and executive surveys highlighting the importance of local “amenities,” Gottlieb (1995) demonstrates associations between a wide variety of outcomes (e.g., toxic emissions, crime rates) and the relative growth in employment in high technology workers. Granger and Blomquist (1999) extend this logic by demonstrating the associations between measures of climate, urban conditions, and environmental quality and the density of urban manufacturing locations across the United States. Following this literature, we expect better aggregate ESG outcomes—such as a broader compilation of those we mentioned in the Municipal Bonds Pricing of ESG Outcomes section that have been connected to municipal credit risk—are also associated with increased municipal expenses in the short term, complemented by increases in migration over time.

Considering Perceptions and Migration Simultaneously: Short and Long-Term Mispricing

Investors make decisions based on the information available to them at the moment. Current prices and yields reflect how they trade today, while prices and yields years into the future represent the outcome of the initial investment, indicating how the underlying fundamentals have evolved over time.

In our context, the migration arguments described in the previous section are more focused on the fundamentals and the long-term impact of changes in ESG outcomes, whereas the perception arguments outlined in earlier center on the present situation as evaluated by municipal investors and those who provide them information for evaluating credit risk (e.g., credit rating agencies). It can be challenging to reconcile that perceptions of credit risk can affect manifested changes in credit risk as well as perceptions of credit risk over time. However, it is possible to argue that ESG outcomes can have a dual effect on municipal bond yields over time. Differences between perceptions of and realized credit risk manifestations that are systematic lead to arbitrage opportunities for investors.

First, ESG outcomes can signal a perception of better municipal management that is differentially captured by market actors (e.g., investors vs. credit rating agencies), above and beyond what is captured through standard measures of credit risk, leading to a lower yield in the short term. Second, if the municipal yield decreases more over time as a function of the same ESG outcomes, it suggests that the ESG outcomes are, in fact, affecting the fundamentals of the underlying investment. This, in turn, influences market participants to trade the bonds at even lower yields in the future, as they trade on the recognized long-term benefits of the past improvements in ESG outcomes. Investors may not pick up on these changes if they do not trade much after an initial transaction or do not follow changes in credit ratings over time. They may also believe that the likelihood of a rare credit risk event is higher than what the credit rating agencies believe, leading to lower yields as a function of ESG outcomes.

In summary, ESG outcomes can have both short-term and long-term impacts on municipal yields. In the short term, they can signal better municipal management that hasn’t been fully recognized by the market, leading to lower yields. In the long term, ESG outcomes can influence the fundamentals of the underlying investment, resulting in even lower yields as investors acknowledge the long-term benefits of strong ESG outcomes.

Data and Method

Explanatory Variables

We construct a novel U.S. county-level dataset of measures drawn from broader social sciences research to assess how environmental and social factors are priced in the municipal bond market. Our choice of variables for inclusion was motivated by a desire to include broad coverage of environmental and social factors into the analysis of the price of municipal securities that typically focuses on measures of fiscal policy (i.e., governance). We sought to replicate the coverage of variables explored in the studies of ESG on sovereign bonds surveyed above. Our choice was, however, constrained by the availability of data across more than 3,000 U.S. counties or county equivalents over a sufficiently long period to allow for panel data analysis. As we assessed the trade-offs of breadth versus temporal coverage, we elected to initially focus on variables available for a large portion of counties from 2001 to 2018. Data Appendix DA3.3 provides details on the data sourcing process and limiting factors of other possible sources.

There was also a set of variables of theoretical interest that were amenable to our temporal design but had less coverage across counties. In combination, these variables led to a high rate of case-wise deletion in our sample. We did not include them in the primary analysis but ran earlier results using them, which are generally consistent with the findings we present, available upon request. We outline each variable in the following section. Further detail and summary of each county-level variable are included in the Supplementary Data Appendix (DA1).

Environmental Outcomes

We first capture the presence, amount of, and weighted toxicity of toxic emissions in a given county. The measures rely on the latitude and longitude location of toxic emissions facilities available in the Environmental Protection Agency’s (EPA) Toxic Release Inventory (TRI) database. The TRI database has been used for a variety of academic studies, such as those looking at housing values near toxic plant locations (Currie et al., 2015), the inequality in plant distribution (Daniels & Friedman, 1999), and the ability of certain groups to avoid polluted neighborhoods (Downey & Hawkins, 2008). We recognize with each of our TRI-based measures that the TRI picks up a set of identified toxic emissions that are above a certain legal threshold. Accordingly, TRI data do not capture all toxic emissions nor do they adequately capture overall emissions in a region (Currie et al., 2015).

Close proximity to toxic emissions facilities measures the percentage of people within a county who live in a census tract containing a toxic emissions facility. 2

The amount of toxic air and water emissions measures the aggregate pounds of stack air, fugitive air, and water emissions from all facilities in each county-year. We mapped these facilities to specific counties using geocod.io based on latitude and longitude.

Toxicity-weighted toxic emissions provide a weighted measure of overall toxic emissions based on the channel of toxic release (e.g., through water, air, or soil) and the specific chemical’s effect on human health. We followed Rousseau and colleagues (2019), connecting data on human toxicity potential (HTP) factors from the environmental science literature, specifically Hertwich et al. (2001) and their updated paper (Hertwich et al., 2006) to assess the relative toxicity of chemicals reported in the TRI basic files.3,4

Social Outcomes

Age-adjusted mortality rates capture the mortality rate of a county’s population per 100,000 residents adjusting for its demographic profile, collected from CDC WONDER. This information has been used in a variety of contexts in health and social sciences—from studies of civic engagement (Lee, 2010) to those predicting life expectancy in areas with less racial disparity (Levine et al., 2013). We expect that counties with lower mortality rates are more attractive to migrants and experience lower health care costs thereby promoting fiscal strength. 5

Poverty rate is provided annually by the U.S. Census Bureau’s SAIPE program. Poverty imposes myriad social costs from reducing life expectancy (Arora et al., 2016) and increasing homicide rates (Messner, 1982) to undermining the productivity of the workforce by slowing childhood brain development (Luby et al., 2013).

Supplemental Nutrition Assistance Program (SNAP) rates provide a proxy for food-related hardship or insecurity in a county (Ratcliffe & McKernan, 2010). As SNAP is an entitlement-based federal program, its rates reflect dynamic food insecurity within a municipality. Food insecurity has been associated with obesity, hypertension, and other negative health outcomes (Gundersen & Ziliak, 2015). We recognize that SNAP rates may also reflect increased access to federal assistance within a particular region. Empirically, we try to account for this with the CUSIP fixed effects (which encompass county fixed effects), allowing for the dynamic, entitlement basis of SNAP to serve as a proxy for changing levels of food insecurity. This aspect of our design helps ameliorate the concern that changing rates may not relate to worse food insecurity but better administration or availability of SNAP in a region. Another limitation is that SNAP rates are highly correlated with poverty rates.

Incarceration rates measures the “total jail population rate” per 100,000 residents aged 15 to 64, defined as the “average daily number of people held in jail through December 31 of a given year” (Incarceration Trends Dataset Codebook: pg. 9) from the Incarceration Trends dataset of The Vera Institute of Justice. 6 The dataset incorporates prison data from various U.S. Bureau of Justice Statistics surveys. High levels of incarceration impose substantial social costs on society, much of which is borne by local governments (Schmitt et al., 2010). A few important limitations are worth considering with these data. First, it may be challenging to trace an incarcerated person to their permanent residence (as there are no prisons or jails in every county). Second, some states such as Connecticut, have limited data availability so consistency and missingness are a concern. Third, incarceration can reflect cross-county patterns given the shared nature of law enforcement and corrections staff.

Property and violent crime rates are the number of property (burglary, larceny-theft, and motor vehicle theft) and violent crimes (murder and nonnegligent manslaughter, rape, robbery, and aggravated assault; FBI UCR). Raw data were provided to us directly from the U.S. Federal Bureau of Investigation’s Universal Crime Reporting (UCR) program. Scholars have studied the impact of government relief spending on crime rates (Fishback et al., 2010), mass shootings and credit risk (Chordia et al., 2022), and the relationship between race, crime rates, and government expenditures (Jackson & Carroll, 1981). A limitation of these data is that some jurisdictions do not always report, or potentially underreport, crimes. Many crimes go undetected, suggesting that the administrative ability to track crime within a county affects the usefulness of these measures.

Fines and forfeits as a percent of own revenues captures the dependence of a county upon revenue deriving from fines and forfeits related to legal violations. Such dependence signals a heavy reliance on legal enforcement action and high conflict within a community. Furthermore, these revenue lines disproportionately affect minority racial groups. Governments with higher revenue from fines often have higher ratios of Black residents (Sances & You, 2017). Data on various government expenditures and revenues were collected from the Government Finance Database (Pierson et al., 2015). Details of the calculation are provided in DA3.1.

Public safety expenditures as a percent of direct expenditures. Drawing from the same Government Finance Database, we also include the percentage of a county’s fiscal expenditure devoted to police protection, fire protection, and correctional institutions. DA3.4.1 provides further details on how the variable was calculated at the county level using county and sub-county municipalities. We calculate “overlapped” county-year measures of these government census-derived variables. By aggregating, this approach accounts for the many sub-municipalities within a county, but it does not adequately reflect sub-county variation in these measures.

Dependent Variable

Yield to worst (yield) is a time-varying estimate of an individual bond’s yield which we capture on the last trading day of the year, except for 2020 wherein November was the last month of available data we were able to acquire. We obtained annual evaluated yields from the monthly price files for the entire population of U.S. municipal bonds from the Intercontinental Exchange (ICE Data Services). These were available to us from April 2001 to November 2020 ICE leverages settlement and price information from 12 global exchanges to provide estimates of market price and yield for a variety of securities. Yield to worst obtained from ICE has the primary advantage that it is the yield metric investors often use to assess how a bond is trading—it is reflective of actual trade activity and what investors see when they check on yield curves (e.g., ICE yield underlies the S&P Municipal Yield Index). 7 Often used synonymously with “yield to call” (Karpf & Mandel, 2018), yield to worst is calculated based on a bond’s price, coupon rate, and years to maturity (or earlier redemption date).

Controls

Bond-Level Controls

ICE Data Services also provided us with bond-level reference data on the full population of U.S. municipal bonds that were active at any point between 2000 and 2020 in their archives. We merged this data with data from the Mergent Fixed Income Database through March of 2018. This allowed us to verify the reference data from both sources. Both files together allowed us comprehensive coverage of bond characteristics, such as whether it was a general obligation (GO) issue, state and/or federally taxable, was issued in a competitive or private offering, insured, callable, issued with a fixed coupon rate, or bank qualified. An overview of these variables is provided in Data Appendix Table DA2. As these represent time-invariant characteristics of bonds, they are captured in our main models with bond fixed effects.

We calculate years to maturity for each bond in each year that it has yield information from ICE. We then round the variable to the nearest year to create year bins to use in our fixed effects. We separately acquired historical long-term credit ratings on all possible U.S. municipal bonds from Moody’s, S&P, and Fitch. Moody’s was acquired directly, S&P was acquired through Wharton Research Data Services (WRDS), and Fitch was used from Mergent. We interpolated long-term credit ratings between years, assuming that ratings were constant unless upgraded, downgraded, or withdrawn. Furthermore, we transformed Moody’s and S&P ratings to an ordinal scale ranging from 1 = missing or not rated to 22 = AAA equivalent and used an average of both ratings where available (Supplemental Appendix Table A1). To capture variation across time in the shape of the yield curve, we follow Baker and colleagues (2022) and construct three-way fixed effects with all categories of credit ratings, all bins of years to maturity, and year.

Macroeconomic and Trends Controls

Several municipal finance studies use the bond buyer index as a control for market risk in assessing interest cost and yields (Johnson & Kriz, 2005; Li et al., 2018; Robbins & Simonsen, 2007). In addition, industry practice would be to control for market demand for bonds. We capture these types of market risk and demand indicators through year fixed effects.

Regional and Issuer Controls

Recognizing that some states are more likely to support a distressed municipality than others through state programs triggered upon debt defaults and the ability to restructure debt, labor, or taxes and fees contracts (Gao et al., 2019), we apply state fixed effects to our model. Furthermore, we include state-year two-way effects to consider changes in state tax policy.

Following the logic that a county’s economic strength and fiscal health impact its ability to repay creditors as operationalized in the analysis of county and city general obligation (GO) credit rating by Palumbo and Zaporowski (2012), we include income levels (median household income), change in income levels, changes in average wages and salaries, the log of own revenue per capita, the log of debt per capita, change in population, unemployment rate, state aid as a percent of revenue, and economic diversity (largest industry GDP / total GDP). A replication of the Palumbo and Zaporowski (2012) study for purposes of verifying our county-level controls is shown in Supplemental Appendix Table A2. To supplement the main results, we also include additional county-year controls for time-varying changes in property taxes (often a local municipality’s main revenue source) as well as possible investor bias (percent Nonwhite population) in robustness checks. 8 In combination with our credit ratings data, our control of historical bond ratings at the bond and county level is very comprehensive. Furthermore, our bond-level fixed effects also account for county and issuer time-invariant characteristics, as bonds are nested within issuers within counties.

Variable Transformations

After an extensive data cleaning process, described in Data Appendix section DA3.2., we assessed the descriptive statistics of our key variables. Given the size of the dataset, we visually assessed the quantiles of each ESG variable in the county-level dataset with the quantiles of the normal distribution. Based on this assessment, we adjusted for outliers (reference Data Appendix 3.2.5) and log-transformed the following variables: controls: own revenue per capita and debt per capita (and property taxes per capita in additional specifications); E&S variables: total jail population rate, age-adjusted mortality rate—all causes, violent crime rates, and property crime rates. We also added one then log transformed the air and water emissions and toxicity-weighted emissions variables, given that many county-years had legitimate zeros. We further standardize the variables before running our regression models to make the results more easily interpretable.

Dimensionality Reduction—Principal Component Analysis

Given the multicollinearity between the ESG variables we collected, we opted to first create and analyze a composite index that accounted for as much of the between county-year variation in ESG factors as possible. Principal component analysis (PCA) is an ideal method for reducing the number of variables to create an index—it has been used in a wide range of social sciences research (Ringnér, 2008), including in the context of municipal credit risk (Li et al., 2018) and with panel data (Çoban & Topcu, 2013).

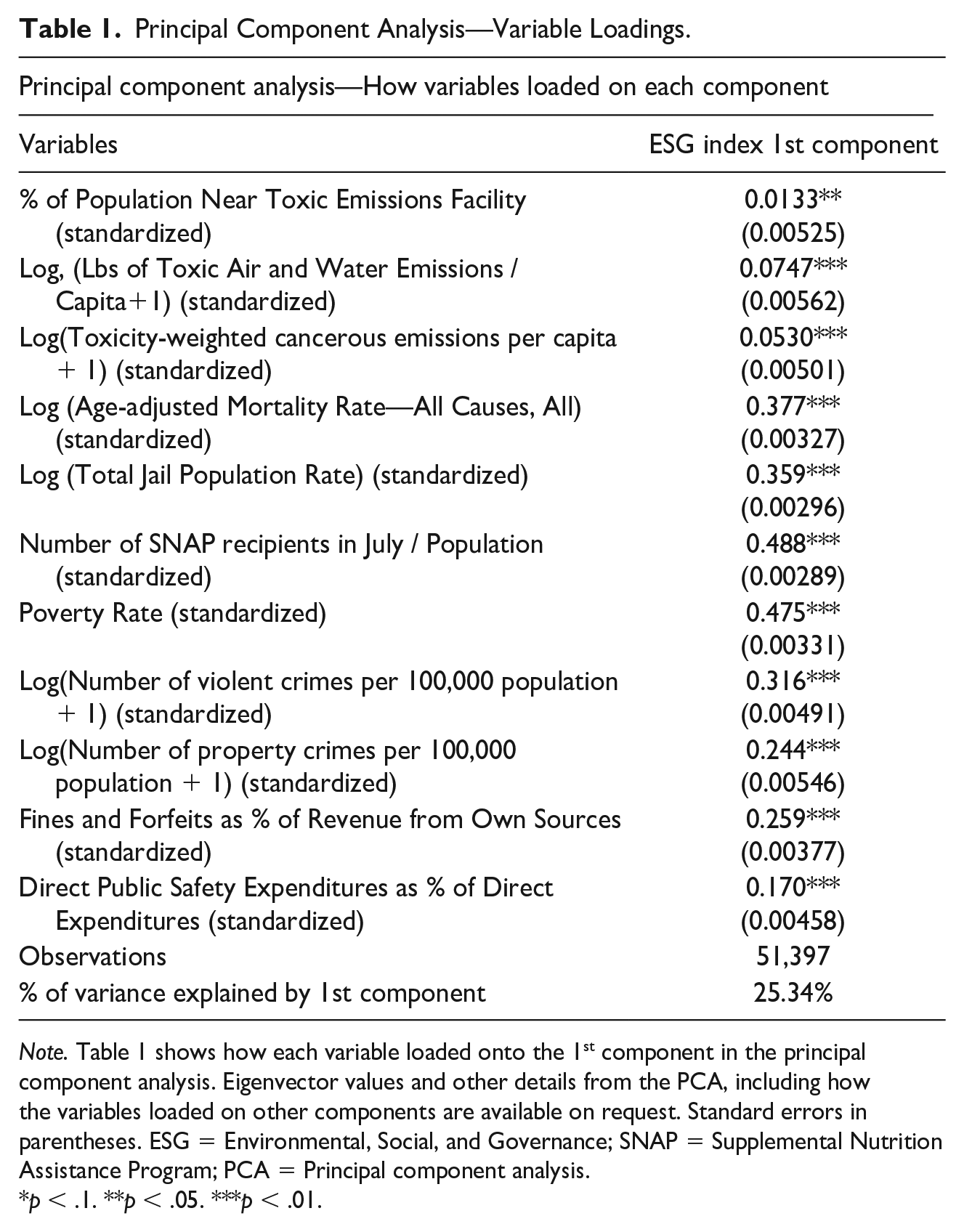

For purposes of our analysis, we created an ESG index using PCA, after standardizing the variables in the county-year dataset. The results from the PCA and variable loadings are reported in Table 1.

Principal Component Analysis—Variable Loadings.

Note. Table 1 shows how each variable loaded onto the 1st component in the principal component analysis. Eigenvector values and other details from the PCA, including how the variables loaded on other components are available on request. Standard errors in parentheses. ESG = Environmental, Social, and Governance; SNAP = Supplemental Nutrition Assistance Program; PCA = Principal component analysis.

p < .1. **p < .05. ***p < .01.

Column 1 reports how the variables load onto the primary ESG index. These variables load together, creating a relatively balanced index wherein higher values signal worse ESG performance. The first component explains more than 25% of the variation across the ESG variables. For reference, the second component only explains approximately 16% of the variation and does not load positively on all the variables. This process suggests that the ESG variables do indeed tend to move together, further motivating their analysis as a group. For further interpretability, we multiply the index by a negative one to signal that a higher value equates to stronger ESG (e.g., lower crime rates).

Sample Descriptives

Our final sample reflects all tax-exempt U.S. municipal bonds that had available credit ratings and yield estimates from December 2001 to November 2020. That is, we capture a full census of bonds that fit these characteristics and are likely those most traded in the market. The final maturity offering amount (bond issue size) for bonds in the sample was over $2.5 trillion.

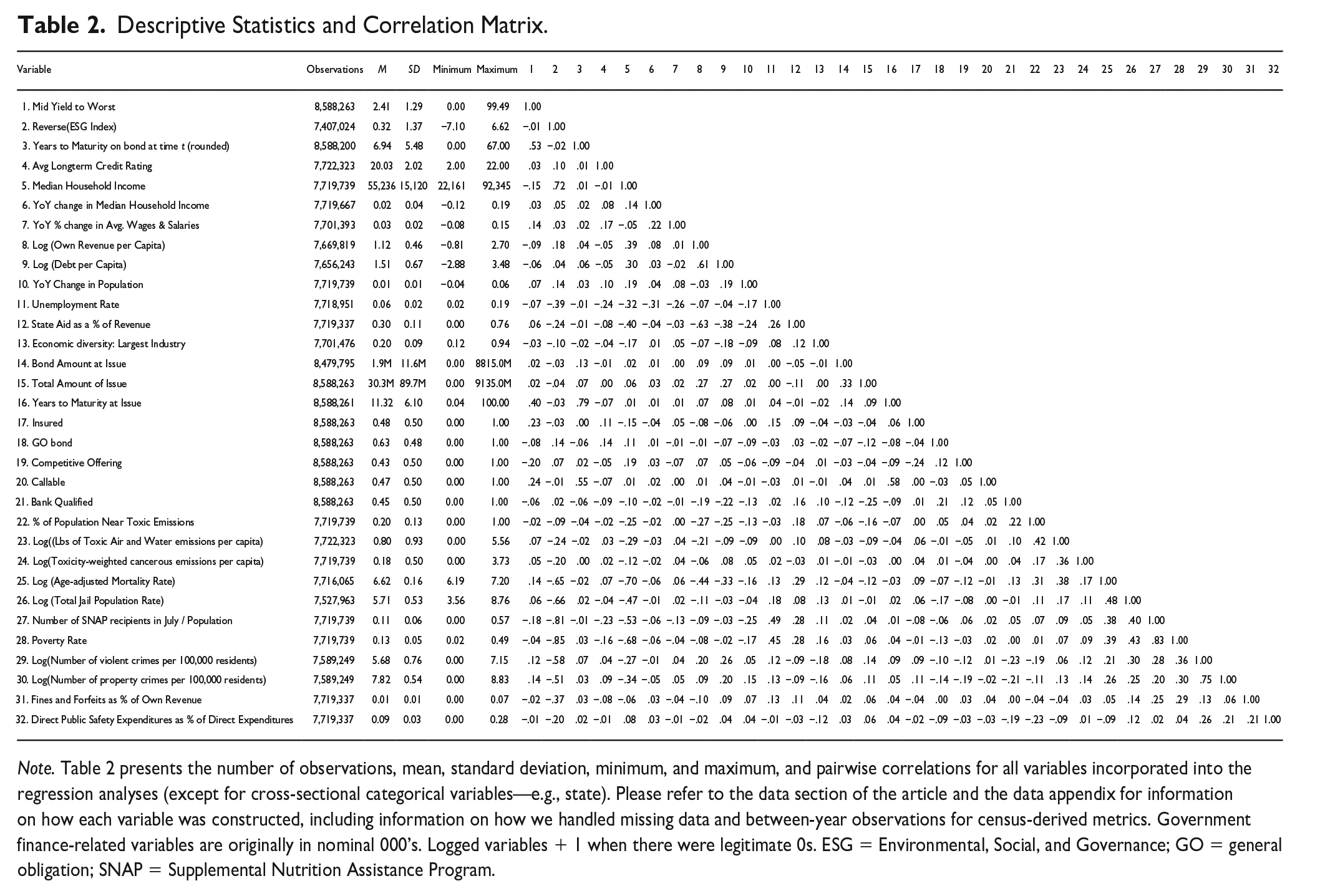

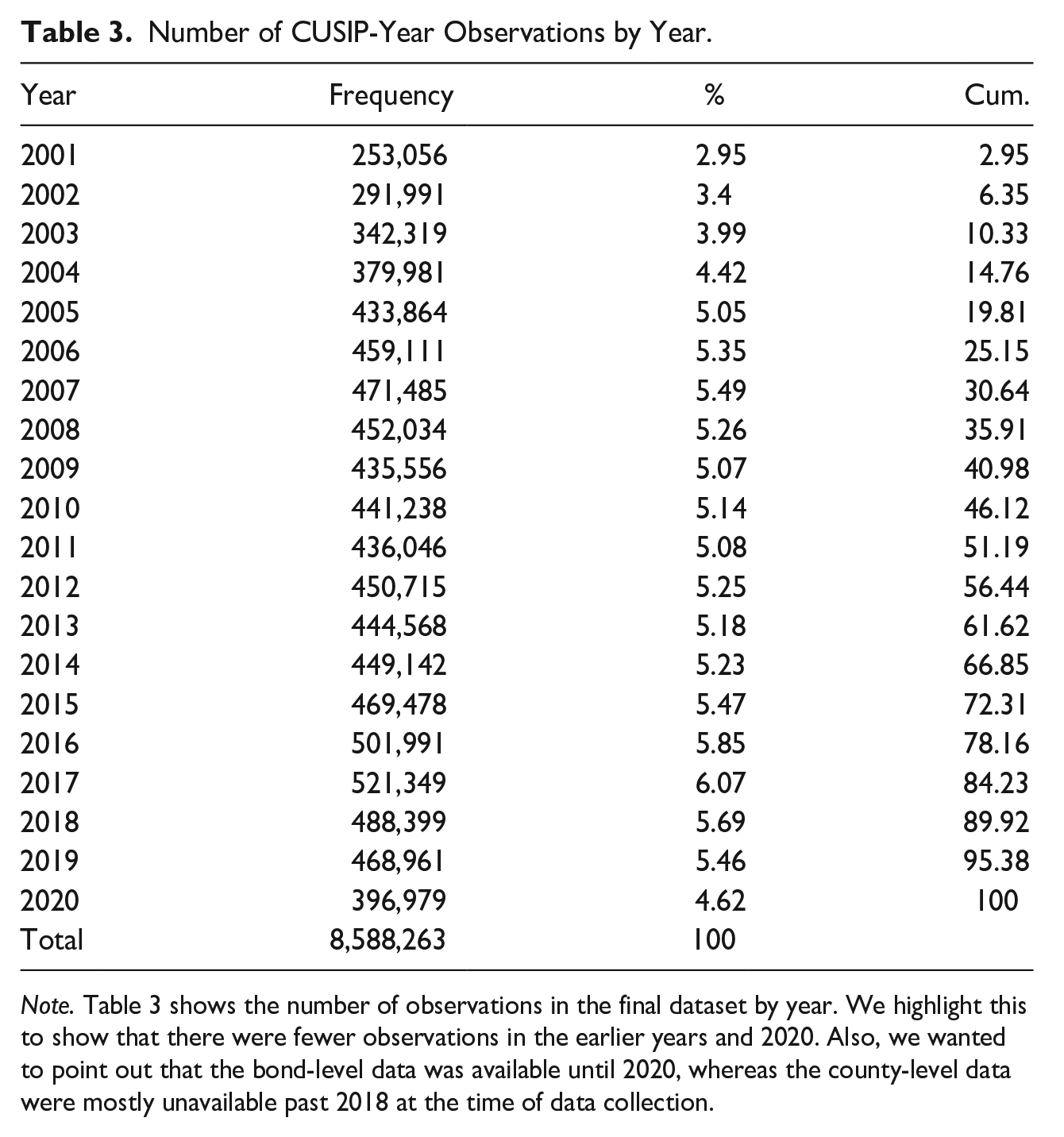

We report the sample means, standard deviations, and pairwise correlations of the variables in the final bond-year level dataset in Table 2. We also provide the number of observations by year in the final CUSIP-year dataset in Table 3. We provide the number of observations by year recognizing that the county data was mostly unavailable after 2018 at the time of data collection.

Descriptive Statistics and Correlation Matrix.

Note. Table 2 presents the number of observations, mean, standard deviation, minimum, and maximum, and pairwise correlations for all variables incorporated into the regression analyses (except for cross-sectional categorical variables—e.g., state). Please refer to the data section of the article and the data appendix for information on how each variable was constructed, including information on how we handled missing data and between-year observations for census-derived metrics. Government finance-related variables are originally in nominal 000’s. Logged variables + 1 when there were legitimate 0s. ESG = Environmental, Social, and Governance; GO = general obligation; SNAP = Supplemental Nutrition Assistance Program.

Number of CUSIP-Year Observations by Year.

Note. Table 3 shows the number of observations in the final dataset by year. We highlight this to show that there were fewer observations in the earlier years and 2020. Also, we wanted to point out that the bond-level data was available until 2020, whereas the county-level data were mostly unavailable past 2018 at the time of data collection.

Model

We apply panel regression models with varying levels of fixed effects to assess time-varying yield (Y). The base specification is as follows:

wherein i indexes on the cross-sectional unit (CUSIP), t indexes on time,

Results

Main Results—ESG and Municipal Bond Yields

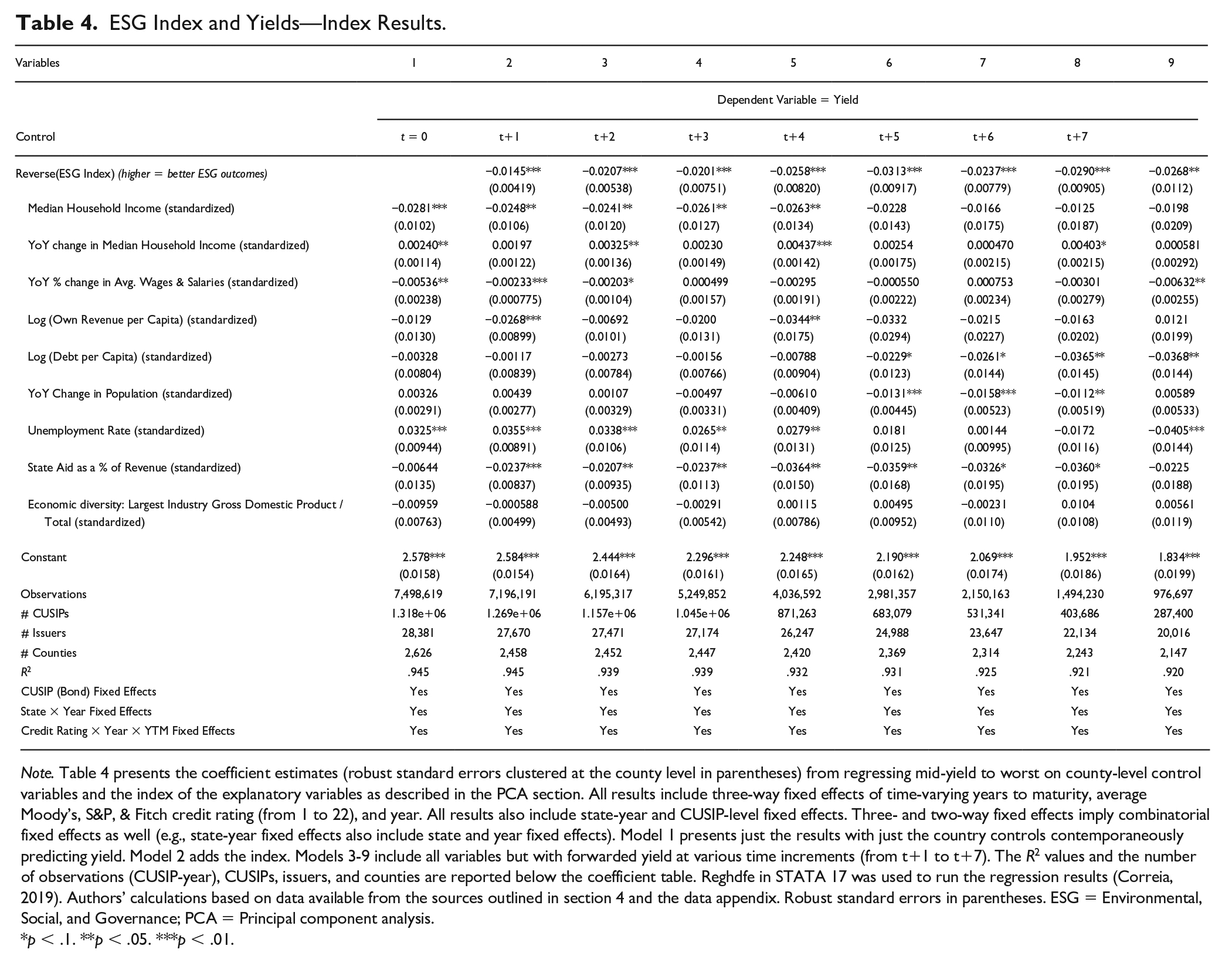

We first present results using the indices we created using PCA, also incorporating county controls, state-year fixed effects, and bond-level fixed effects. This specification is the most rigorous, focusing on within-bond variation and also controlling for the primary inputs to time-varying yield (the three-way interaction of years to maturity, credit rating, and time). The explanatory variable is the ESG index that is reverse coded for interpretability (higher = stronger ESG outcomes), capturing the largest amount of variation among the ESG outcomes we included. Table 4 reports the results of the main specification. For these results, higher values of the ESG index can be interpreted as stronger ESG outcomes.

ESG Index and Yields—Index Results.

Note. Table 4 presents the coefficient estimates (robust standard errors clustered at the county level in parentheses) from regressing mid-yield to worst on county-level control variables and the index of the explanatory variables as described in the PCA section. All results include three-way fixed effects of time-varying years to maturity, average Moody’s, S&P, & Fitch credit rating (from 1 to 22), and year. All results also include state-year and CUSIP-level fixed effects. Three- and two-way fixed effects imply combinatorial fixed effects as well (e.g., state-year fixed effects also include state and year fixed effects). Model 1 presents just the results with just the country controls contemporaneously predicting yield. Model 2 adds the index. Models 3-9 include all variables but with forwarded yield at various time increments (from t+1 to t+7). The R2 values and the number of observations (CUSIP-year), CUSIPs, issuers, and counties are reported below the coefficient table. Reghdfe in STATA 17 was used to run the regression results (Correia, 2019). Authors’ calculations based on data available from the sources outlined in section 4 and the data appendix. Robust standard errors in parentheses. ESG = Environmental, Social, and Governance; PCA = Principal component analysis.

p < .1. **p < .05. ***p < .01.

Table 4 shows a summarily negative association between the index and credit yields (p<.01 from t =0 to t+6 and p<.05 at t+7) implying that higher ESG performance is associated with lower credit risk. The coefficient estimate steadily decreases as we predict yield farther into the future—from -0.0145 at t=0 to -0.0268 at t+7, with some oscillation. As the standard deviation at the county-year level of the index is approximately 1.67 at the county-year level (1.37 at the bond-year level), this accounts for a between approximately −2.5 and −4 bps lower yield predicted by a +1 standard deviation increase in the ESG index.

To ensure the robustness of our results, we also looked at between bond analysis with extensive bond level controls (bond amount at issue, total issue amount, years to maturity at issue, bond insured, GO bond, competitive offering, bond callable, and bank qualified), index results without controls (for the between- and within-bond specifications), and time periods beyond 7 years (unreported). We also ran separate specifications with the log of yield as the outcome. Finally, we ran the main specifications with additional controls related to possible racial bias (percent of non-White population), as well as changes to property taxes (the largest source of local municipal finance revenue). The results were generally consistent though the importance of the ESG index in predicting yield varied with the within- and between-bond models. 9 Earlier disaggregate results for higher and lower missingness variables are consistent with the findings shown here (consistent with Supplemental Figure A1). Finally, Supplemental Appendix Figure A1 summarizes the results if all significant coefficient estimates were aggregated when examining the variables in a disaggregated manner. Using this method of interpretation, a one standard deviation improvement in all ESG variables (i.e., better overall ESG outcomes) is associated with lower credit risk for all years of analysis from t=0 to t+7 (-7.1 bps and -5.3 bps, respectively).

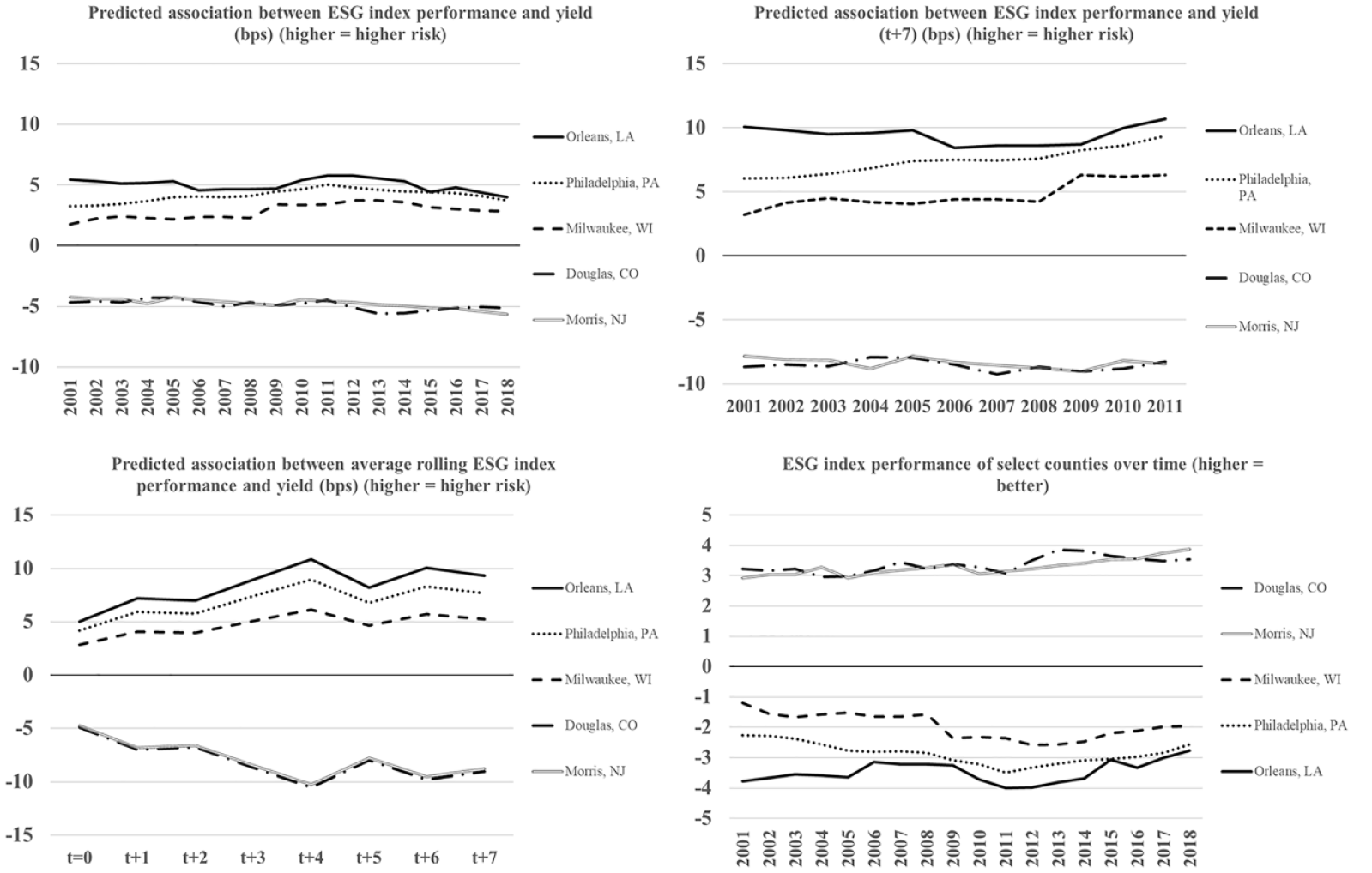

Case Examples

In addition to looking at how a one standard deviation of ESG performance is associated with yield, we illustrate the importance of considering ESG outcomes in predicting credit risk through a few case examples. We chose five populous counties that have historically outperformed (Morris, NJ and Douglas, CO) or underperformed other regions (Philadelphia, PA, Orleans, LA, and Milwaukee, WI) on ESG. Pairwise comparisons between these counties show predicted differences in yield between 10 and 20 bps when looking at a 7-year time horizon—an economically significant amount, considering the billions invested in municipal bonds every year.

In the bottom right corner of Figure 1, we also highlight that some underperforming counties have improved ESG outcomes between 2001 and 2018. For example, Orleans’ index score improved by approximately 26%. These increases in performance may motivate investors to consider time varying ESG outcomes, especially recognizing that the risk association we report generally increases over a longer time horizon.

Index Results: Difference in Predicted Yield Between County and “Average” County for an Average Bond

Post Hoc Analysis of Investor Perception Mechanism

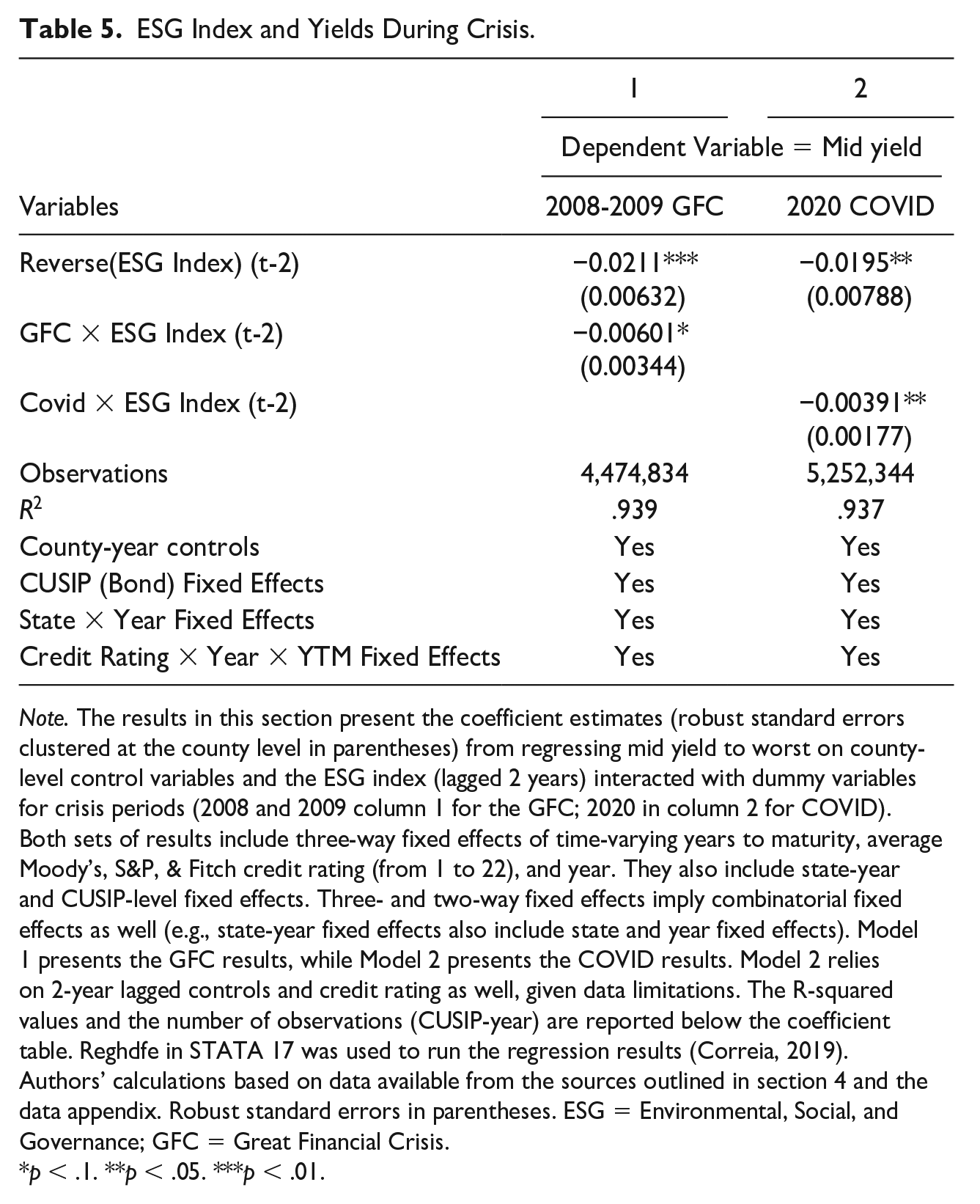

To test whether stronger ESG outcomes are associated with investor’s short-term perceptions of lower credit risk (i.e., via reduced uncertainty), we applied the same models described in section 5.1 to two recent crises: the Great Financial Crisis (GFC) of 2008 and the COVID-19 pandemic which caused stay at home orders across the United States in March of 2020. Indeed, times of economic crisis test which organizations an investor is willing to trust (Amiraslani et al., 2023). We argue that both events greatly increased uncertainty in the evaluation of municipal entities. The GFC applied pressure on public provision, such as welfare services, for those affected by higher unemployment rates, as well as wage stagnation across the U.S. economy. The COVID-19 pandemic similarly caused widespread economic uncertainty, and associated work-from-home orders brought salient the question of which municipalities would people migrate to.

The results shown in Column 1 below in Table 5 reflect the same models described in section 5.1 with interaction terms for each of the crises. The ESG index is lagged by two years in both models. For the COVID-19 crisis (column 2), we used a two-year lagged ESG index and controls due to much of our data being limited to 2018. Consistent with our theorizing, the results suggest that higher ESG outcome counties experience an additional approximately -0.5 bps (0.60 bps during the GFC, and 0.39 bps during COVID, respectively) decrease in yield when uncertainty is high, even when controlling for standard fiscal and bond level factors.

ESG Index and Yields During Crisis.

Note. The results in this section present the coefficient estimates (robust standard errors clustered at the county level in parentheses) from regressing mid yield to worst on county-level control variables and the ESG index (lagged 2 years) interacted with dummy variables for crisis periods (2008 and 2009 column 1 for the GFC; 2020 in column 2 for COVID). Both sets of results include three-way fixed effects of time-varying years to maturity, average Moody’s, S&P, & Fitch credit rating (from 1 to 22), and year. They also include state-year and CUSIP-level fixed effects. Three- and two-way fixed effects imply combinatorial fixed effects as well (e.g., state-year fixed effects also include state and year fixed effects). Model 1 presents the GFC results, while Model 2 presents the COVID results. Model 2 relies on 2-year lagged controls and credit rating as well, given data limitations. The R-squared values and the number of observations (CUSIP-year) are reported below the coefficient table. Reghdfe in STATA 17 was used to run the regression results (Correia, 2019). Authors’ calculations based on data available from the sources outlined in section 4 and the data appendix. Robust standard errors in parentheses. ESG = Environmental, Social, and Governance; GFC = Great Financial Crisis.

p < .1. **p < .05. ***p < .01.

Post Hoc Analysis of Migration and Fiscal Health Mechanisms

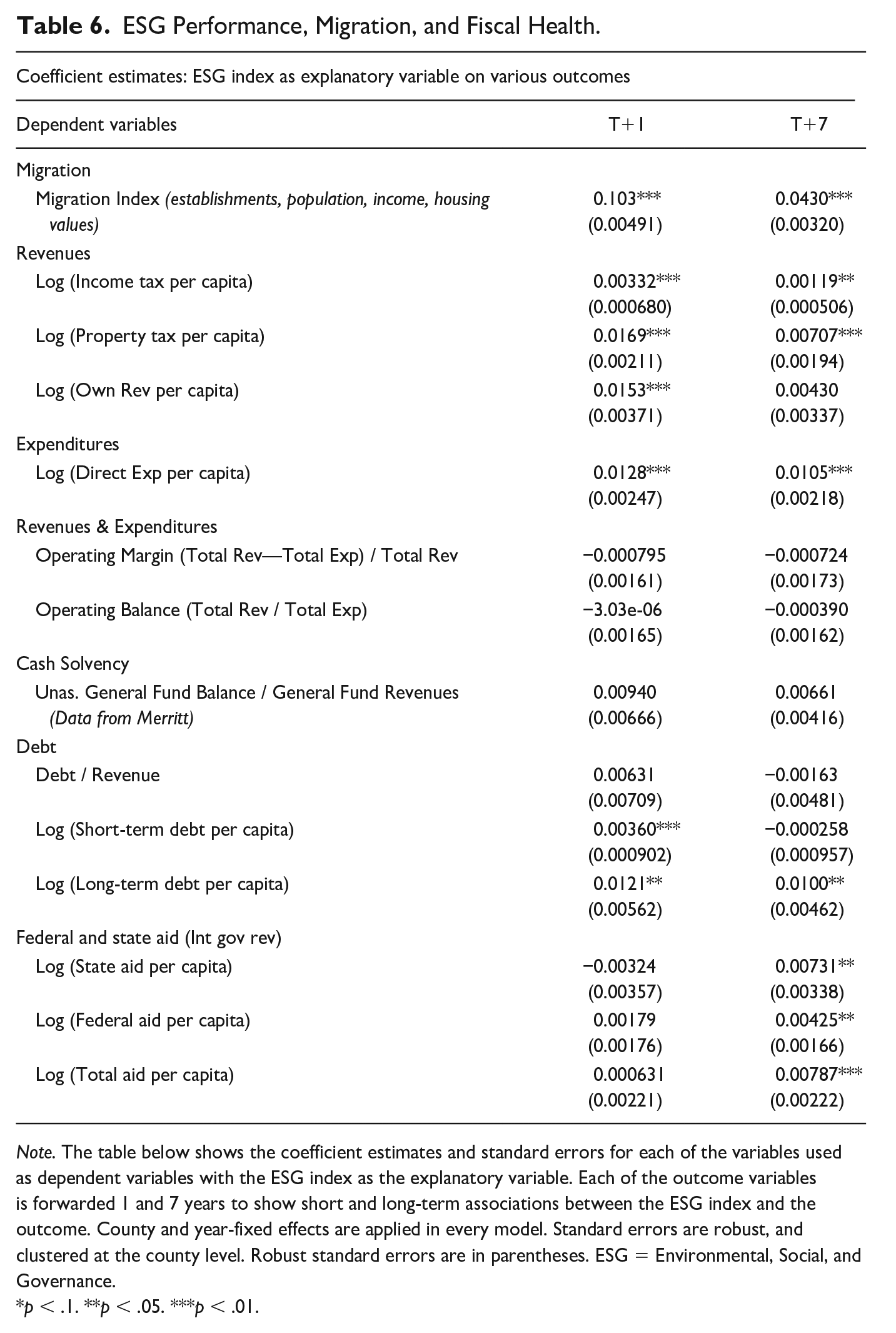

We conducted additional post hoc analysis to examine our theory development on ESG outcomes associated with migration and future fiscal health. First, we examined whether ESG outcomes were associated with patterns of migration, based on an index of population, business establishments, housing values, and income levels, over time. Next, we examined whether ESG outcomes are associated with changes in revenues and expenditures over time. Finally, following the literature on municipal fiscal health in public finance and administration, we examined associations between the ESG index and common measures of fiscal performance. For all of these analyses, we relied on county-year panel models with county and year fixed effects.

ESG and Migration

We applied principal component analysis to the log of population, the log of the number of business establishments, median household income, and median housing values to create an index of absolute levels of migration that varied by county year. All four variables loaded strongly and well-balanced onto the first component. We regressed this index (forwarded by 1 and 7 years) on the ESG index with county and year-fixed effects. We found that the ESG index is strongly associated with higher migration rates in the short (t+1) and long-term (t+7). Table 6 shows the results of these analyses:

ESG Performance, Migration, and Fiscal Health.

Note. The table below shows the coefficient estimates and standard errors for each of the variables used as dependent variables with the ESG index as the explanatory variable. Each of the outcome variables is forwarded 1 and 7 years to show short and long-term associations between the ESG index and the outcome. County and year-fixed effects are applied in every model. Standard errors are robust, and clustered at the county level. Robust standard errors are in parentheses. ESG = Environmental, Social, and Governance.

p < .1. **p < .05. ***p < .01.

ESG, Revenues, and Expenditures

We regressed the following revenue and expenditure-based variables on the ESG index with panel models using county and year-fixed effects: log (own revenue per capita), log (income taxes per capita), log (property taxes per capita), log (direct expenditures per capita), operating margin and operating balance (based on revenues relative to expenses), and cash solvency (unassigned general fund balance relative to general fund revenues). Overall, the ESG index was significantly positively associated with increases in tax income and property taxes in the short and long term as well as direct expenditures per capita. It was also significantly associated with own revenue per capita in the short-term, but marginally insignificant in the long-term. It was not significantly associated with the operating balance, margin, or cash solvency measures as operationalized. These results suggest that ESG outcomes are associated with increasing revenues, but come with increasing expenses—likely for upkeep of amenities—as well.

ESG and Other Measures of Fiscal Health

We also captured how federal, state, and overall aid per capita, as well as different measures of debt (short, long, and debt as a percentage of revenue), were associated with ESG outcomes. The ESG index was associated with the log of short-term debt per capita in the short-term, but not the long-term. The index was associated with higher long-term debt per capita in the short- and long-term. Interestingly, ESG was not strongly associated with aid per capita in the short-term (t+1) but was strongly associated with aid per capita in the long term. Whether this is driven by rising rates of inequality in areas with higher income, higher overall population, better administration, a track record of improvements, or other system-level factors is an outstanding question to be explored further.

Overall, our analysis of migration and fiscal health mechanisms generally supports our theorizing that ESG outcomes are associate with increased migration and fiscal health in the long term. However, our analyses did reveal the presence of important trade-offs, such as higher levels of long-term debt per capita, more federal and state aid per capita in the long term, and higher expenditures that also associated with higher ESG outcomes. The trade-offs between these measures of fiscal health and the benefits from increases in absolute levels of migration and revenues provide ample room for future research.

Exploratory Analysis: Who Is Mispricing Municipal Credit Risk?

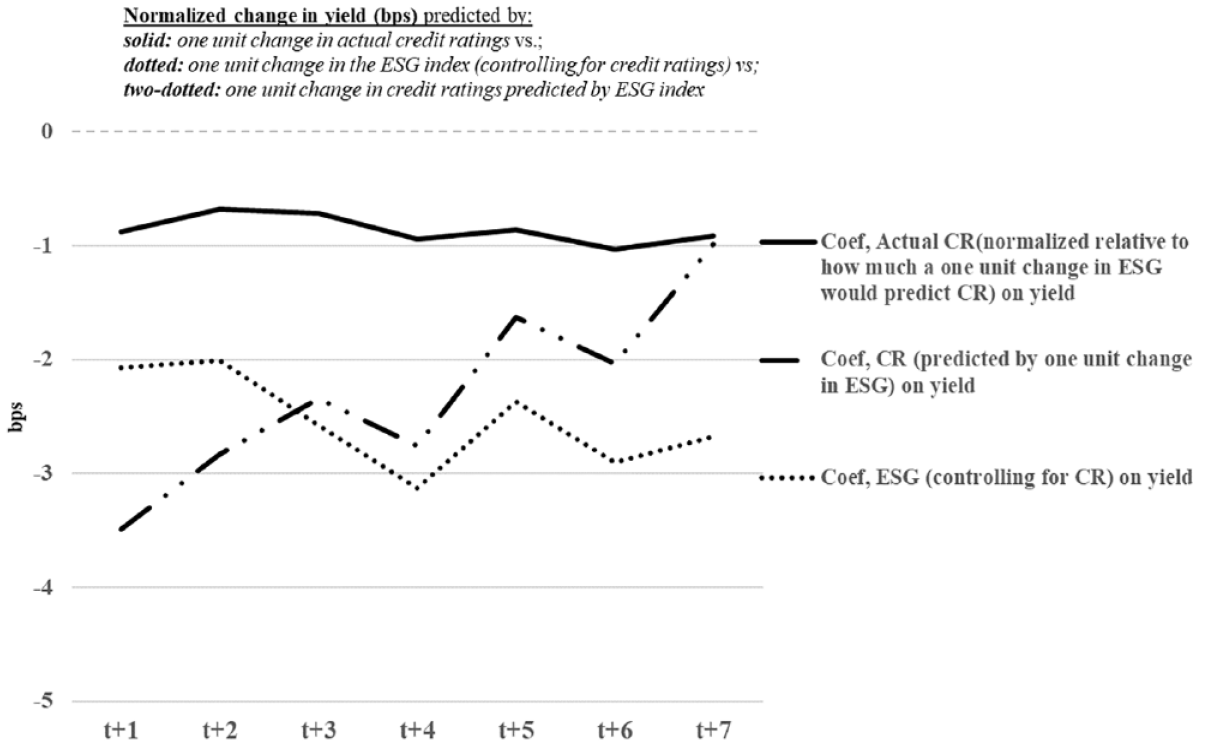

We conducted an additional set of analyses relying on the same base specification outlined in 5.1. First, we assessed how the ESG index is associated with time-varying bond-year credit ratings. To fit within our two-stage design with a robust set of controls, we rely on a linear model for this stage. Second, we assessed how a one-unit change in credit rating (e.g., a change from Aa1 to Aaa) is associated with yield over time. Third, we assessed how a one-unit change of future bond-year credit ratings associated with yield, instrumenting future bond-year credit ratings with current values of the county-level ESG index. These models included CUSIP fixed effects, years to maturity—year fixed effects (the yield curve without the credit ratings), state-year fixed effects, and standard controls.

The first analysis suggested that stronger performance on the ESG index consistently predicted higher credit ratings (Supplemental Appendix Table A4). The second analysis consistently showed that a one-unit change in credit rating is associated with an approximately 10 bps decrease in yield (Supplemental Appendix Table A5). The third analysis shows that credit ratings predicted by the ESG index predicted a strong and significant negative association with yield from t+0 to t+4, and t+6, and an insignificant negative association at t+5 and t+7 (Supplemental Appendix Table A6). The first analysis shows the first stage of this analysis (Supplemental Appendix Table A4). Figure 2 plots the coefficient estimates normalized to the equivalent of a one-unit change in the ESG index on each respective variable.

Normalized Coefficient Estimates—How ESG and Credit Ratings Associate With Yield.

The results help reconcile the overall association we see with ESG and yield when controlling for the yield curve. The results suggest that credit ratings consider ESG outcomes more in the short term than municipal bond investors, whereas investors price ESG outcomes more than ratings in the long term (after t+4). This is counterintuitive as compared to the results of the analysis where we interacted with two different crises with ESG, suggesting that investors value ESG outcomes more when uncertainty is high. This could reflect an insurance-like premium that ESG outcomes provide a municipal entity, wherein the likelihood of perceived risk in the long-term is even less than actual risk based on assessed measurement.

Discussion and Conclusion

Summary of Results

We show that improvements in environmental, social, and governance (ESG) outcomes at the county level are associated with reduced municipal credit risk. Our analysis draws on a wide range of environmental (e.g., cancerous toxic emissions) and social performance measures, such as revenues earned from fines and forfeits, many of which have not previously been used in assessments of the pricing of municipal credit. The associations between these ESG outcomes and credit risk are economically significant, particularly for consistently high- versus low-performing counties.

In post hoc analyses, we demonstrated evidence that changes in ESG outcomes were associated with shifts in migration and fiscal health. These analyses point to the benefits, such as increased property taxes, and costs, such as increased direct expenditures, associated with collective improvements in such outcomes as crime rates, and reductions in residential fines, poverty, mortality, and related outcomes. These results suggest the need for a more nuanced model of credit risk which recognizes that not all fiscal deficits and debt that many accompany these bond issues in the short term are inimical to long-term fiscal health. Beyond the importance of recognizing ESG outcomes’ relationship with municipal fiscal health, we further attempted to isolate the effect of ESG outcomes on investor perceptions of credit risk by leveraging quasi-exogenous shocks to uncertainty during 2008 and 2009, as well as 2020 COVID-19 pandemic. The results from these tests were consistent with our theorization that investors would assume counties with better ESG outcomes were less risky during a crisis even when controlling for bond, time, economic, and fiscal factors. In this way, ESG outcomes act as an indicator to investors of strong municipal management. Furthermore, exploratory analysis of ESG outcomes on credit ratings suggests that investors and credit rating agencies differentially evaluate the importance of ESG over time.

Implications for Research, Limitations, and Specific Suggestions for Future Research

Implications for Research

We believe that our findings have implications for research on public finance and the current study of the links between sustainable business practices, ESG, and financial performance. The theory development and findings also provide a perspective to the business and society literature that allows for a systems-level integration of politics, corporations, and community actors (e.g., local NGOs) through analysis of municipalities, or geographic communities, as the focal unit of analysis. We discuss each of these areas in turn.

To our knowledge, the emerging research on ESG is seldom linked to the study of public finance. While this may be equated to a simple syntax issue, we believe this is due to differences in the unit of analysis across fields and challenges related to data availability. Whereas the unit of analysis when studying ESG’s relationship to financial performance is typically the corporation, recent research at the sovereign level (Capelle-Blancard et al., 2019) suggests a need for re-consideration. We build on this research by articulating how ESG performance can be operationalized at the municipal level (as ESG outcomes) via publicly available data. When we initiated data collection for our study, very few ESG data providers for municipalities existed. This may be partly due to issues of data aggregation, wherein municipalities encompass towns, cities, school districts, and other geographic boundaries that are hard to compare side by side.

The corporate-centered ESG research stream should recognize that connecting ESG to financial performance across units of analysis (e.g., corporates, sovereignties, and municipalities) requires different theoretical argumentation. In this study, we argue that theory on residential sorting and migration—unique to the study of ESG performance and municipal financial performance—adds to ESG research, and describes business re-location (migration) as an important variable heretofore not described as a mediating factor between ESG and financial performance (cf., Atz et al., 2023 for a recent review of hundreds of articles on this relationship).

By articulating ESG at the municipal level as a place-based quality of human life-related outcomes opens doors for business and society research at different units of analysis. Typically focused on individual corporations and placeless ESG or sustainability-related activities (Nyberg et al., 2022), we believe re-orienting business and society research toward geographic communities unlock new doors that connect sustainable investing practices (Kölbel et al., 2020; Marti et al., 2023) to real-world outcomes, reflecting more objective changes in the societal impact that can be compared vis-à-vis third-party ESG ratings. Such orientation also complements existing research to understand corporate-government relations on solving social issues (Knudsen & Moon, 2022; Nilsson, 2023). For example, do efforts to attract business migration via tax incentives curb public policies aimed at improving local ESG outcomes? Research focused on the community level of analysis developed by organizational theory (Marquis, 2003; Marquis & Battilana, 2009; Marquis et al., 2013; Marquis & Tilcsik, 2016) and non-market and stakeholder strategy scholars (Dorobantu & Odziemkowska, 2017; Henisz et al., 2014), in particular, can help tease out the causal mechanisms underlying corporate ESG activities, community ESG outcomes, and community incentives to attract corporations and the implications to stakeholders and companies themselves for (mis)fit between them.

Limitations

This study explored the correlational relationships between a set of county-level ESG outcomes and municipal credit risk. While the study shows the promise and potential economic significance of recognizing a new set of geo-spatial ESG outcomes, there are a variety of limitations outside of those we noted with the individual ESG outcome variables, and room for extension.

First, this study focused on the U.S. municipal bond market. While it is one of the largest sub-sovereign debt markets in the world, the results may not be applicable to other countries. Also related to the generality of the results is the nested nature of our data—county-level ESG factors may have different associations with credit risk of an issuer than census tract-level factors. The bonds in the analysis reflect all CUSIPs from public issuers within a county, not just county government issuers. Furthermore, in creating county-level measures, measurement error can be introduced equating different censuses over time.

Second, there are likely nonlinear relationships between the ESG variables and bond risk, as well as endogeneity between our ESG index and fiscal health, that we may not fully capture in our panel regression models. Our PCA approach and selection of fiscal controls (e.g., income levels) captures some of these concerns, though we noticed that the first components often did not account for much more than 20% to 30% of the variation between variables. We further attempt to account for nonlinearities by analyzing specific case counties, however, more sophisticated data analytic techniques could offer additional insights.

Third, our empirical identification strategies in line with our theorizing were mostly targeted at short-term investor perceptions rather than long-term changes in fiscal health. Our analyses of long-term fiscal health were more associational and suggestive. Therefore, we cannot assume that our empirical findings causally apply to the long-term relationship between ESG and credit risk. Furthermore, our use of COVID and the great financial crises as shocks to uncertainty present a weak form of identification as these events were associated with broader changes, including U.S. migratory patterns.

Fourth, our specifications focused on within-county changes in ESG outcomes over time and our robustness checks were slightly less supportive of mispricing across counties with the full set of controls. While we believe models accounting for bond-level fixed effects provide for a more rigorous analysis controlling for various time-invariant factors, this is an important caveat to the understanding of our results.

Suggestions for Future Research

There is a promising future for the study of ESG outcomes within municipalities and beyond. First, there is very limited research on the connection between racial inequality and credit risk. Improvements in ESG outcomes are not equally distributed, as disadvantaged groups do not have the luxury to migrate to areas with better amenities. Further, investor bias may affect disadvantaged groups (Dougal et al., 2019; Smull et al., 2023).

Second, to our knowledge, there is not much known about the relationship between sub-national ESG outcomes and credit risk beyond the U.S. context or ESG and municipal credit risk at geographic units of analysis very close to the issuer level (i.e., sub-county in many cases). Investor biases, information arbitrage, and the ability of businesses and individuals to migrate may strongly depend on the institutional context. We believe the lack of data—especially longitudinally—has created barriers to these research streams.

Third, there are complex inter-relationships between local governments that issue municipal bonds, companies which they may be dependent on for resources, local nonprofits, and civilians that are seldom explored at the system level empirically. We see an opportunity to examine how cohesion across these groups affects municipal credit risk through supporting or undermining efforts to invest in long-term ESG outcomes vs. short-term fiscal improvements. For example, do political tensions within a community affect the likelihood of long-term municipal issues targeting improvements in ESG outcomes?

Fourth, we see a large opportunity to connect municipal ESG outcomes to green or social bond issuance and certification. Municipal green bond certification in the United States is a relatively new phenomenon that is not highly regulated. Connecting objective ESG outcomes at the municipal level would help substantiate green bond certification and track long-term improvement on stated uses of proceeds. More broadly, we believe an emphasis on objective ESG outcomes at the geographic community level (e.g., county) can help assuage greenwashing across asset classes. How are ESG outcomes trending where municipalities, impact investing efforts, and corporations are located? Do stated reasons for certified bond issues relate to these outcomes?

Finally, we believe there is a strong case to connect geography-based ESG outcomes to the locations of corporations and their associated financial performance. Such ESG outcomes correlate with migration; what are the human capital costs to businesses related to attraction and retention accordingly?

Conclusion

Jenkins (2021) concludes his book powerfully questioning the power of municipal bondholders and raters on their impacts on community outcomes:

The social crisis of austerity, the hollowing out of urban liberal democracy, the truncation of long-term commitments of local government to the citizenry, and the deepening of inequality—social realities lazily treated as products of neoliberalism, financialization or federal failure—are rooted in the politics of municipal debt. Yet, rarely does anyone ask why the water systems on which we rely for daily hydration, the underground network of sewage systems that sort our toxins, and the recreational spaces in which our children play should be steeped in the municipal bond market in the first place; why is it that bondholders and raters should have so much influence over our collective welfare (228).

Our results support his concerns but also potentially offer an opportunity for market self-correction and responsible sustainable development within local communities. Even socially agnostic investors should investigate the environmental and social performance of a municipality as part of their credit due diligence. Improvements in ESG outcomes that drive positive migration, increases in household income, and the tax base should be rewarded with lower credit yields. If we allow for some investors to also exhibit pro-social behavior in the desire to invest in municipalities that are higher performers on ESG outcomes, we have an additional potential impetus for environmental and social factors to move markets in a manner that improves social welfare and reduces racial injustice.

This research contributes to the municipal finance and business and society literature in several ways. First, it provides a context that connects ESG performance to system-level outcomes to develop the idea of ESG outcomes. Second, it shows that ESG outcomes merit study in bundles given their interrelatedness. Empirical results suggest that these outcomes are highly interrelated and predict credit risk in a group. Third, the theory development and empirical context support a call for further research on the role of governments in sustainable development and business and society. We open doors for future research examining how the traits of municipalities support or constrain businesses’ social initiatives. Fourth, it extends the theoretical discussion on ESG-financial performance to consider long-term changes in fiscal health as a function of migration and changes in the tax base, factors unique to municipalities, and the instruments they issue. Empirical results suggest that municipal investors place differential emphasis on the short-term implications of changes in ESG outcomes, and value ESG differently than credit rating agencies. The results are policy-relevant, suggesting that objective outcome-based ESG measures from secondary, publicly available sources can facilitate better investment information.

As regulatory bodies, such as the SEC, continue to increase the attention paid to ESG measures and put forth scrutiny on practical application, investors should consider the use of normalized, temporally available community outcome metrics such as those highlighted in this study. Such measures are mostly available through public, secondary sources, although usage agreements can restrict their use for commercial purposes. We anticipate that ESG measurement not only of municipalities but also the corporates within them may incorporate more geo-coded, location-specific outcomes. We put additional emphasis on this point as ESG data for smaller and privately held firms tends to be limited. In ongoing debates about the merits of ESG ratings data, analysts can consider the use of objective, secondary data available through public sources (such as many we highlighted) to assess the outcomes in places where firms are located when they do not have ESG ratings otherwise. As we described in section 6.2.3, such data unlocks new doors for the burgeoning field of ESG research which is starting to move beyond the level of corporations. For example, does corporate philanthropy target geographic communities with higher poverty levels or does it mostly serve elite interests? Do “place-based” measures of ESG (e.g., whether a corporation donates to high-need areas) align with common third-party ESG measures? Such nuanced analysis—that may drive the next wave of ESG research—requires place-based, objective ESG metrics in harmony with organizational-level information.

Supplemental Material

sj-docx-1-bas-10.1177_00076503231220541 – Supplemental material for Environmental, Social, and Governance (ESG) Outcomes and Municipal Credit Risk

Supplemental material, sj-docx-1-bas-10.1177_00076503231220541 for Environmental, Social, and Governance (ESG) Outcomes and Municipal Credit Risk by Christopher C. Bruno and Witold J. Henisz in Business & Society

Footnotes

Acknowledgements