Abstract

This study extends regulatory capture theory to investigate how and to what extent a firm’s political and nonpolitical ties jointly influence corporate regulatory participation. In the context of regulatory standards setting, although firms with political ties are better able to promote firm standards into industry regulations, it remains unclear whether the coexistence of firms’ nonpolitical ties (i.e., university ties and interlocked firms in our study) is more or less likely to reduce the effect of political ties. Although corporate leaders with political and nonpolitical ties may provide complementary resources, they may follow different mechanisms to drive firm actions. We, thus, argue that nonpolitical ties likely reduce the effect of political ties on regulatory standards setting. Using a sample of public manufacturing firms in China, we find evidence that supports our predictions. Our study contributes to the regulatory capture literature by redirecting attention to the dynamics of political versus nonpolitical ties.

Keywords

Regulatory capture theory, which stems from the work of Stigler (1971) in the political economy literature, posits that regulated firms likely manipulate the regulator to control outcomes for their private interests (Dal Bó, 2006; Etzioni, 2009). Studies that draw on this theory have explored the consequences of government regulations (Dal Bó, 2006) and regulation establishments through such nonmarket strategies as lobbying, election manipulation, grassroots movements, campaigns to influence legislators, and job offers to politicians and regulators (Hillman et al., 2004; Holburn & Vanden Bergh, 2014). At its core, the theory focuses on involvement in regulation-making as a firm’s strategic decisions are shaped by its interests (Peltzman, 1976; Ping, 2013) but pays little attention to how the roles of different stakeholders may affect the firm’s decisions. Nevertheless, decisions made by a firm must balance the potentially conflicting claims of multiple stakeholders (Evan & Freeman, 1993) and their countervailing influences may determine firm actions (Neville & Menguc, 2006; Oliver, 1991).

To address the issue of stakeholder influence, we extend regulatory capture theory (Stigler, 1971) to consider how potentially divergent stakeholder preferences (J. Li et al., 2018) affect firm participation in regulation-making. Drawing on the theory, we argue that corporate participation in regulation-making may occur when Firm A gains support from the regulator (e.g., government agencies) to set new regulations, whereby a set of Firm Bs (e.g., competitors or exchange partners) must comply. A firm can be broadly embedded in relations with two types of stakeholders—political and nonpolitical—and they may jointly affect firm decisions. In general, firms with political ties tend to act in line with government expectations (Wei et al., 2023), whereas firms with nonpolitical ties may shape political participation by following professional norms or mutual firm interests (Freeman, 2010; J. Li et al., 2018). A firm that attempts to satisfy the expectations of one type of stakeholders may go against the expectations of another type of stakeholders (Oliver, 1991). As such, these two types of stakeholders (ties) compete for firm attention, with nonpolitical ties potentially weakening the effect of political ties.

To examine this notion, we leverage regulatory standards setting to standardize products across firms in a given industry, 1 given that, to develop such standards, firms must gain approval from relevant government agencies (Gibson, 2007; Greenstein, 1992; Guilloux et al., 2013). From the regulatory capture perspective, without government approval, a firm is unable to promote its private technology standard as a regulatory standard to shape other firms’ operations. The regulator, however, also relies on firm participation. Without a voluntary effort, as well as the prowess and expertise of business organizations, the government cannot set regulatory standards due to its lack of technical knowledge (Greenstein, 1992). Because the capture literature has largely ignored the joint effect of political and nonpolitical ties on corporate nonmarket actions, we raise the following question:

Research Question 1 (RQ1): To what extent do a firm’s political and nonpolitical connections jointly affect its tendency to engage in regulatory standards setting?

We start from research on political capital (Hillman et al., 2004; Lowndes & Wilson, 2001), which is also called political connections or political ties (for a recent review, see Wei et al., 2023), to argue that firms with political ties are more likely to gain government approval to set regulatory standards, as these firms are embedded in the political system and, thus, gain political endorsements (Fisman, 2001) and political opportunities (Pfeffer & Salancik, 1978). A growing body of research in management has focused on how political ties may generate favorable firm outcomes (Wei et al., 2023), but few studies have focused on boundary conditions under which the effect of political ties on firm outcomes may vary. As firms are often embedded in nonpolitical stakeholder relations, a firm’s social capital may also affect its decisions (Lowndes & Wilson, 2001). It is useful to explore the joint effect of political and nonpolitical ties.

Among various nonpolitical stakeholders, we choose those highly related to our conceptualization in the context of regulatory standards setting. Specifically, we focus on a firm’s university ties through university professors and corporate ties through interlocking directorates (Burt, 1983; Gao et al., 2008; Gargiulo, 1993; Selznick, 1949; Shropshire, 2010). University and corporate ties can respectively enhance the perception of a firm’s professional norms and reciprocal benefits to participate in regulatory standards setting. We argue that, when firms have nonpolitical ties, the positive effect of political ties on regulatory standards setting may diminish because political and nonpolitical actors with different mindsets and expectations may not always be congruent in how they affect firm nonmarket actions.

Our study contributes to the capture literature (for a review see, Dal Bó, 2006), which is based on research rooted in regulatory capture theory (Peltzman, 1976; Stigler, 1971), by highlighting the joint effect of political and nonpolitical ties in affecting a firm’s involvement in regulation-making. This approach is important, given that the concept of regulatory capture remains an undertheorized but overused notion with a wide variety of conceptually distinct definitions of self-interest in the literature (D. Carpenter & Moss, 2013). While previous research has emphasized the importance of political connections in navigating market regulations (Holburn & Vanden Bergh, 2014) and industry regulations (Carboni, 2017), its effect remains unclear when considering influences stemming from nonpolitical ties (Wei et al., 2023). Moreover, although the organization-regulation relationship has been described through a substantial body of case studies and anecdotes in the capture literature (Dal Bó, 2006; Fremeth & Holburn, 2012; Macher et al., 2011), theoretically driven research with large samples to conceptualize and examine such a relationship is rare. Previous studies have focused on political activities such as lobbying and donations in the hope of influencing regulations through politicians, legislators, and regulators (Aranda & Simons, 2018; Holburn & Vanden Bergh, 2014; Katic & Hillman, 2023), but we cannot simply equate political connections to political activities (Wei et al., 2023). Our study extends the political connection literature by showing the extent to which political ties affect regulatory standards setting as a unique type of nonmarket firm strategy.

Theoretical Background and Hypotheses

Regulatory Capture Theory

Stigler (1971) introduced the idea that regulation may be a “commodity” captured by firms. Research has traditionally adopted a dyadic approach that focuses on the distinction, conflict, or independence of public and private interests (Mahoney et al., 2009). The purpose of regulation for the public interest, however, is not necessarily achieved, as firms may dominate the regulation-making process to ensure private interests (Chalmers et al., 2012; Peltzman, 1976). That is, “the public interest may be a fictionalized construct in which public policy is shaped in negotiations among parties that pursue private interests” (Mahoney et al., 2009, p. 1036). Because asymmetrical information exists between the regulator and the regulated firms, regulation-making relies on firms to take professional approaches to problem-solving, which enables the firms to exercise capture by participating in regulation creation for their private interests (Goldberg & Maggi, 1999; Posner, 1974). Laffont and Tirole (1991) showed, for example, that, due to technical issues related to pension regulation, it is one area that regulated firms may capture.

Thus, the regulation-making process is widely regarded as a competition among interest firms (or groups) in which one firm may use the coercive power of the state to obtain benefits at the expense of other firms (Goldberg & Maggi, 1999). As a result, “regulation is supplied in response to the demands of interest groups struggling among themselves to maximize the incomes of their members” (Posner, 1974, p. 335). Although regulatory capture theory provides important implications for understanding corporate involvement in regulation-making, we know little about how multiple, incongruent stakeholder expectations may jointly affect organizational decisions. To enrich the literature on the organization-regulation relationship, we first explain how private and public interests drive regulatory standards setting as a nonmarket strategy and then incorporate divergent stakeholder interests and expectations into the capture literature to explain how political and nonpolitical ties jointly shape firm decisions.

Regulatory Standards Setting as a Nonmarket Strategy

Firms attempt to create a “more favorable environment by establishing . . . government regulations” (Wry et al., 2013, p. 447). Prior research has emphasized the role of the government in regulatory standards setting, assuming that the government “can carry tremendous weight to support a standard, superseding the market processes” (Narayanan & Chen, 2012, p. 1390). Firms often strive to promote private standards as regulatory standards, as doing so can create an advantage, such as a favorable exchange infrastructure (Garud et al., 2007), that can stabilize operations and ensure constancy to exchange partners (e.g., suppliers and buyers) that adopt the standard (Cargill, 1989). Observations show that certain firms gained government approval to create national and global industry standards in mobile telecommunications (Funk & Methe, 2001). Nippon Telegraph and Telephone Corporation, for example, leveraged its close relationship with the Japanese government to promote its own private technology to become a national standard for the analog cellular market (Funk & Methe, 2001).

Moreover, given different path dependencies among industry firms in innovation processes, it is difficult to acquire information before new regulatory standards are announced (Fremeth & Holburn, 2012). In this regard, relying solely on private standards is riskier, especially in industries in which competing (regulatory) standards may emerge and change the market landscape and competitive dynamics. Regulatory capture may shift firm competition away from market principles. For example, in a case study on two open business-reporting data standards (EDIFACT and XBRL) 2 developed simultaneously but separately, Guilloux and colleagues (2013) showed that, when XBRL gained approval from the French government, it became the regulatory standard of the data communication infrastructure to which all other industry firms had to conform to survive. In regard to EDIFACT, in line with the argument of Schilling (1998), if a firm’s innovation is based on a private technology standard that is not interoperable with a competing regulatory standard, the firm may, paradoxically, experience the effect of technological lockout.

From a regulator’s perspective, regulatory standards may ensure the public interest to improve product quality and safety as well as to upgrade technology. From a firm’s perspective, participation in regulatory standard-making provides opportunities to capture the process to pursue firm interest by influencing regulatory bodies. The political opportunity may increase competitors’ costs and change the allocation of market resources (Getz, 1997; Mahon et al., 1989). Specifically, once a firm’s private standards become government regulations, that will impose coercive pressure on competing firms and their exchange partners to adopt the newly established regulatory standards (Bacon et al., 1994). For the competing firms, switching to regulatory standards may lead to technological discontinuities that can be “competence destroying” and negatively affect operation continuity (Jenkins, 2010), jeopardizing firms’ stability and even existence (Getz, 1997). What remains unclear is how a firm’s political and nonpolitical ties may jointly affect the firm’s participation in regulatory standards-making.

Political Ties and Regulatory Standards Setting

Regulatory standards setting is a type of techno-political collaboration, defined as a “strategic practice of designing or using technology to constitute, embody, or enact political goals” (Hecht, 2001, p. 256). Through regulation, regulators may respond to market failure, ensure policy stability, or better manage firms to meet certain technical criteria as a public interest safeguard (Baldwin et al., 1999). According to regulatory capture theory (Stigler, 1971), however, regulators have neither sufficient information nor the industry expertise necessary to make regulatory standards (Yackee & Yackee, 2006). When making such standards, the tendency of the government to rely on business organizations provides opportunities for the organizations to influence the legislative process (Ayres & Braithwaite, 1992). Although firms struggle to find ways to widely displace their private standards to enhance competitiveness (Cargill, 1989; David & Greenstein, 1990; Suarez, 2005) and shape regulations (Peltzman, 1976), regulators may choose certain organizations over others in the regulation-making process and balance competing sets of views and demands when promoting the practice of a given organization (Wry et al., 2013).

We argue that corporate elites with political ties, as a firm’s intangible capital (Hillman et al., 1999; Hillman & Hitt, 1999) or institutional capital (Oliver, 1997), are more likely to gain opportunities to shape the regulation-making process, as they are more likely to gain trust and confidence from government agencies (Faccio et al., 2006). Relational connections typically exert a favorable influence on organizational outcomes when a firm’s actions align with stakeholder expectations. For instance, firms with an external connection to one type of stakeholders, such as underwriters, can use this connection to validate or confirm their credibility, which, in turn, helps persuade other types of stakeholders, such as investors, for trust or support (Higgins & Gulati, 2003). In our context, political ties may help validate a firm’s credibility to other stakeholders (Baum & Oliver, 1991; Waguespack & Fleming, 2009). In China, individual-based political connections, known as guanxi in Chinese, are deemed a substitute for formal institutional support (Buckley et al., 2007; Xin & Pearce, 1996), which may help to justify future actions to other stakeholders such as regulators.

More importantly, political connections may have implications for institutional consequences such as regulatory changes (Wei et al., 2023). For example, Volkswagen benefited from political ties in gaining auto-market information and establishing regulatory standards for the Chinese auto industry (Luo & Peng, 1998). Thus, political ties have been regarded as critical in initiating new state regulations, as corporate leaders with political resources are more likely to gain government support (Frynas et al., 2006). The basic reason is that political ties can create opportunities for firms to establish and nurture good relationships with government officials to enhance mutual dependence (Hillman, 2005; Lester et al., 2008).

Indeed, firms with political ties are likely to benefit from this relational advantage in shaping the policy-making process (Van de Ven, 2007). Hillman and colleagues (1999) showed that firms benefit from their executives’ serving on a U.S. government committee to address regulatory uncertainties through established contacts. Luo and Peng (1998, p. 159) observed that “in China, a large number of early [market] movers have been rewarded handsomely due to their collaboration with the government.” Political ties also can help firms anticipate and identify potential threats in a timely manner as well as solicit advice regarding policy changes (Hadjikhani & Ghauri, 2001). As such, corporate elites’ political ties can improve a firm’s standing vis-à-vis rivals to gain government approval and support (Hillman & Hitt, 1999; Luo, 2001). In line with regulatory capture theory, we propose the baseline hypothesis:

Taking Nonpolitical Ties Into Consideration

As new regulations involve coercion (e.g., other firms are required to adopt the newly established standards), different stakeholders with their own corresponding interests may compete in the regulation-making process (Wade-Benzoni et al., 2002). As a firm’s action is embedded in its relationships with multiple stakeholders (Shipilov et al., 2014)—and such stakeholders often have diverse preferences and expectations as well as place diverse demands on firm actions—firms may not respond to each stakeholder individually but, instead, balance such diverse expectations in its action (Oliver, 1991; Rowley, 1997). Thus, a firm that attempts to make a regulatory technological standard may find it difficult to do so, as it must convince various stakeholders to support the standard that offers the firm an advantage in the marketplace while balancing the demands of different stakeholders (Garud et al., 2002; Narayanan & Chen, 2012).

In this study, we focus on the joint influence of political and nonpolitical ties on corporate participation in regulation-making, which presents a puzzle in the stakeholder literature, as such an effect can be synergistic or antagonistic (J. Li et al., 2018) as well as conflicting or complementary (Neville & Menguc, 2006). On one hand, corporate leaders with political and nonpolitical ties may provide complementary resources to support corporate political action (CPA) and reinforce each other. For example, political connections may serve as channels to mobilize political and nonpolitical resources for political actions (Brady et al., 1999; Lim, 2008). On the other hand, different stakeholders may compete for a firm’s attention (Abdurakhmonov et al., 2021). For example, political stakeholders expect firms to fulfill state policies, whereas market stakeholders expect firms to satisfy customer demands (J. Li et al., 2018). The puzzle to date has not been fully addressed in the corporate political connection literature (Wei et al., 2023).

A Multistakeholder Approach: The Joint Influence of Political and Nonpolitical Ties

To address this issue, we adopt a multistakeholder approach to argue that the joint influence of political and nonpolitical ties on regulatory standards-making is more likely to be conflicting than complementary as different stakeholder expectations may create internal conflicts in organizational arrangements and routines (J. Li et al., 2018; Oliver, 1991). Our incorporation of nonpolitical stakeholders is important, given that various interorganizational ties can also affect firm decisions (Leblebici et al., 1991). As noted, we focus on two types of nonpolitical connections—university ties, as an indication of connections through professors who tend to promote professional norms, and corporate ties, as an indication of business connections through interlocking directorates that may promote market principles (Allen, 1974) and reciprocal firm benefits (Mahmood et al., 2011; Shropshire, 2010), which may draw organizational attention away from policy-based CPA advocated by political ties.

As the example of lithium battery standard setting for new energy vehicles (EVs) in China illustrates, many firms in the EV industry have pursued high energy density, leading to numerous safety accidents, such as fire and explosions (Huang et al., 2015; Koch et al., 2018). Leading firms in this industry, such as BYD, participated in setting the national standard (i.e., regulatory standard in China) or Guojia Biaozhun (GB; e.g., GB 38031) for lithium batteries in line with government expectations to regulate the industry. BYD has close ties with the government. The CEO of BYD, Chuanfu Wang, was a representative of the National People’s Congress and a State Council Special Allowance expert. BYD and its CEO leveraged its political ties to actively participate in setting the GB standards in the EV industry. 3 Based on its own blade battery and lithium iron phosphate battery technology, BYD added a specification, “The battery system does not ignite or explode for at least 5 minutes, allowing time for passengers to leave the vehicle in case of fire or explosion hazards,” into the national standard, GB 38031. 4

The continuing rise in battery fire incidents, however, calls for a higher standard for battery safety in China. University professors, who serve as independent board members as well as interlocked board members, have pushed for a stricter EV battery standard. For example, Yanbo Jiang, a professor at the Law School of Jiangxi University of Finance and Economics, and Min Zhang, a professor at Renmin University of China, both of whom served as independent directors of BYD, have actively pushed for battery safety, reliability, and energy efficiency as well as drafted policy reports to revise the battery standards. As a result of these efforts, the Chinese government has further improved the national standards, related to lithium batteries, initiating the revision of the standards for electric vehicles and electric vehicle batteries (GB 38031-2020 for Traction Battery Safety Requirements; GB 18384-2020 for Electric Vehicles Safety Requirements; GB 38032-2020 for Electric Bus Safety Requirements). This example illustrates how firms can leverage their political ties to influence the formulation of regulatory standards and, subsequently, how university and corporate ties can go beyond the political influence by focusing more on professionalism, moral obligations, and mutual benefits of multiple firms.

University Ties

University ties refer to professionals from prominent universities who are invited to serve as firms’ independent outside directors. In the context of China, university ties and political ties may coexist in a public firm. On one hand, firms often have established political connections with the government to access critical resources, given that the Chinese government in the economic transition process has controlled substantial national resources needed by business organizations. On the other hand, the Chinese government requires that 30% of board members must be independent outside directors (Xie et al., 2021). Most of these directors are professors from prominent universities and work in functional areas, such as science, engineering, finance, accounting, or law (Peng, 2004). These professionals not only offer such benefits as advice and counsel, information access, resources, and legitimacy (Pfeffer & Salancik, 1978) but also confer credentials (Heugens & Lander, 2009) to influence firm decisions.

Recent studies have shown that firms may engage in regulatory capture with different motives (Gatignon et al., 2023; Giorgi et al., 2019) by emphasizing firms’ practices in manipulating the regulatory process for their own interests or highlighting the congruence of firms’ practices in line with government expectations for the interdependence of private and public interests (Mahoney et al., 2009). In line with this viewpoint, stakeholders with different tendencies may promote incongruent firm practices. University professors and politically connected firm leaders may follow different pathways and advocate different procedures, arrangements, and routines within the firm when in pursuit of political participation. Specifically, politically connected firms are more likely to set new regulations in line with the expectation of political stakeholders (X. Deng et al., 2010; Jia, 2014) in exchange for resources and policy support (J. Li et al., 2018; Wry et al., 2013) or to gain advantages (Laffont & Tirole, 1991).

In contrast, university ties essentially follow professional norms for nonpolitical purposes, rather than simply follow expectations of political stakeholders. Professionals on corporate boards, as a combination of credentials and knowledge available to a firm (Lin, 2002; Payne et al., 2011), likely draw a firm’s attention to professionalism and monitor their moral obligations (Freeman, 2010). University professors prefer to serve on the boards of high-quality firms because their own reputation is also at stake (Higgins & Gulati, 2003; Stuart et al., 1999). To maintain their reputation, and given their background and ethical orientation, these professors may be more likely to resist using “unfair” tactics to suppress competition. 5 Moreover, regulatory standards setting is related to a firm’s technological development. University professors on corporate boards as resource providers (Hillman et al., 2009) may drive corporate innovation through their advice and connectivity channels, but politicians as independent directors do not have such an effect (A. Wang, 2020). D. Jiang and colleagues (2023) showed that professors, as independent directors, can improve corporate innovation performance, especially in regions with a low level of state intervention. These studies imply that, unlike politically connected leaders, university professors tend to follow professional norms and technological trends, rather than pursuing political goals in affecting CPA decisions, which may create a conflict for the firm to make an internal arrangement.

Taking together, the multistakeholder approach posits that managing diverse expectations and demands of multiple stakeholders can be challenging, as action by the firm may sacrifice the interests of certain stakeholders for the good of others (Meznar et al., 1994; Oliver, 1991). Given the diverse interests of connections to different stakeholders, such as universities and government agencies, their expectations may conflict in establishing firm routines, procedures, and arrangements, impeding a firm’s action (J. Li et al., 2018). That is, professional norms followed by university professors may not be congruent with the way of organizing advocated by politically connected corporate leaders. For these reasons, university ties may mitigate the effect of political ties on regulatory standards setting. Thus, we propose:

Corporate Ties

Corporate ties occur when individual directors serve simultaneously on two or more boards (Johnson et al., 2013; Mizruchi, 1996). Centrality in the interlocking network represents an advantage because central firms are better able to gain support from network partners than periphery firms (Lin, 1999; Portes, 1998; Shropshire, 2010). In our study, corporate ties are captured by the centrality of a firm’s position in the interlocking network, indicating that the firm is well connected with other important firms (Johnson et al., 2013; Mizruchi, 1996). We argue that corporate ties may weaken the effect of political ties on regulatory standards setting. The leveraging of political ties in regulatory capture is often coupled with such obligations as pursuing political objectives. In contrast, an interlocking network often acts under reciprocal norms for mutual benefit and manages mutual dependence. As Shropshire (2010, p. 253) argued, “Directors with more outside experience have broader exposure to and awareness of practices, given the number of firms they are connected to.” Because interlocked directors are aware of the needs of their connected firms in the network, they tend to look at the interests of multiple firms and resist any action that could potentially benefit only one firm and be detrimental to others.

Specifically, whereas political ties can improve a firm’s standing vis-à-vis rivals to search for certain policy-making information unavailable to its rivals (Hillman, 2005; Hillman & Hitt, 1999; Lester et al., 2008; Wilts, 2006), corporate ties provide firms with an advantage to search for business opportunities for mutual benefit (Mahmood et al., 2011; Shropshire, 2010). The different search directions may compete for firm attention. Firms may struggle to make decisions that satisfy the expectations of political stakeholders but defy business stakeholders’ expectations (J. Li et al., 2018; Oliver, 1991). Interlocking boards, however, can affect the decisions of well-connected firms (Lin, 1999; Portes, 1998) based on reciprocity by shifting away from political objectives, as interlocking directorates are more likely to emphasize the mutual interests of their well-connected firms to guide firm actions (Jensen, 2008). Thus, we propose:

Method

Research Setting

In 2008, China became the sixth permanent member of the International Organization for Standardization (ISO) after the United States, Germany, Britain, France, and Japan. Today, the China National Standards Service Center provides professional services for about 200,000 standards within four categories: national standards, industry standards, local standards, and enterprise standards. 6 In this study, we focus on GB, the highest standards requiring firm compliance. GB standards-making provides an appropriate empirical setting to test our theory. Firms are able to set GB standards, given that the regulator has limited technical knowledge and relies on the firms’ expertise in the standards-making process.

GB standards are typically characterized by complex technical details. For example, there are 20 GB standards that stipulate the requirements for the safety, operation, evaluation, and equipment of electric cars. The complexity of GB standards increases the information asymmetry between the regulator and the regulated firms, leading to a higher reliance on the regulator in regard to firms’ technical capabilities in setting standards. Such reliance allows the regulated firms to shape regulatory standards to their own benefit. In practice, once a new GB standard is issued, other industry firms must make technical adjustments to obtain a China Compulsory Certificate before they can sell products in the market (Niu & Fan, 2015).

In addition, a firm must gain government support and approval to successfully promote its private standard as a regulatory standard (Gibson, 2007; Greenstein, 1992; Guilloux et al., 2013). The Standardization Administration of China (SAC) serves as the regulator and represents China in the ISO and the International Electrotechnical Commission (IEC), among other relevant organizations. The GB-making process, which follows the guidance of ISO and IEC, has nine phases: (a) work preparation, (b) proposal development, (c) workgroup draft initiation, (d) consultation, (e) examination, (f) approval, (g) publication, (h) review, and (i) suppression. 7 According to our interviews, 8 firms often voluntarily initiate a standard proposal to the SAC on the condition that the proposed standards do not conflict or overlap with existing GB or international standards. Consultation is the critical phase for checks and balances between the firm and regulator on the proposed standards. The regulator invites university professors, industry technical experts, and relevant firm representatives to evaluate the proposals and provide feedback on behalf of the regulator. Based on these evaluations, the firms that proposed the standards will modify the proposals to meet their expectations. The proposed standards may gain government approval, pending the final assessment of government agencies. This setting allows us to test how firms balance political and nonpolitical ties to engage in regulatory standards-making.

Sample

We collected information on all publicly listed manufacturing firms from the China Stock Market and Accounting Research (CSMAR) database, which has been widely used in academic research on publicly listed firms (Calomiris et al., 2010; Fan et al., 2007; H. Wang & Qian, 2011). We initially collected a complete list of all GB standards made by Chinese firms between 2004 and 2013 from the database maintained by the SAC. The SAC database serves as an open information portal, providing details on each national standard, including the drafter and name of the standard as well as technical requirements (Breznitz & Murphree, 2013). 9 We constructed a longitudinal data set by merging the two databases (i.e., CSMAR and SAC) into a firm-year format. The sample consisted of 1,539 manufacturing firms within our observation window (2004-2013), with a total of 8,547 firm-year observations.

Variables of Interest

Our dependent variable, regulatory standards-making, was measured by a dummy variable, coded as 1 if the firm developed new national standards (GB standards) in the year as reported in the SAC database, and 0 otherwise. We lagged all predictor variables by 1 year to avoid possible simultaneity concerns.

Political tie was measured by the number of a firm’s politically connected corporate leaders (executives and directors; Jia, 2014) if a leader is (a) a member of the People’s Congress, (b) a member of the People’s Political Consultative Conference (PCC), or (c) a government official. In China, the Congress and the PCC are two essential bodies of the political system (M. Chen, 2015; Yan, 2011). 10 The Congress is responsible for drafting laws, supervising the enforcement of laws, appointing government officials, and making major jurisdictional decisions (Manion, 2008). The PCC offers crucial advice to the Congress and monitors governments via regular meetings (Jia, 2014). Congressional or conference deputies are legitimate channels through which firms voice opinions to affect government policies (H. Li et al., 2006; Manion, 2008), and past government officials can leverage guanxi to influence political decision-making (Buckley et al., 2007). Thus, these three types of political ties play an important role in affecting government decisions. According to our interview with a central-government official in charge of the regulatory standards-making process in China, 11 politically connected firms are more likely to convince government officials on the merits of their regulatory standards setting.

University tie was measured by the number of universities whose professors served as independent directors on a firm’s board (Zhou & Xie, 2007; Zhu & Lou, 2011). 12 In China, at least one-third of a firm’s board members must be independent outside directors, and most are professors (Peng, 2004). For example, in 2013, university professors comprised 67 of the 110 independent directors of 33 public firms in Jiangxi Province, China (People.cn., 2013).

Corporate tie was measured by the eigenvector centrality of a firm in the board interlocks. We first constructed board interlocks among all publicly listed firms in China on an annual basis. We then calculated each firm’s eigenvector centrality score (Bonacich, 1972), multiplied by 100 using UCINET. 13 Board interlocks are widely considered a conduit by which firms exchange information (Lin, 1999; Mizruchi, 1996; Portes, 1998). Eigenvector centrality evaluates the importance of a firm’s position in the network, suggesting that central firms are better able to access information and resources than are peripheral firms (Bonacich, 1972; M. A. Carpenter et al., 2012). Following prior studies (H. Jiang et al., 2017, 2021), we used eigenvector centrality in the interlocking network to capture corporate ties. We obtained the information from CSMAR.

Control Variables

We controlled for a set of variables that could potentially affect a firm’s decision to engage in political action. Firm size is regarded as a measure of firms’ “importance, power, and success, and so large firms may strongly legitimate the practices they adopt” (Davis & Greve, 1997, p. 15). Large firms are more able to capture regulators than are small firms (Peltzman, 1976). In our study, firm size was measured by the amount of total assets (Anderson & Reeb, 2004; Peng, 2004). Using alternative measures for firm size, such as sales (Hambrick & Cannella, 2004), yielded results consistent with those subsequently reported. Firm age, profitability, and slack are commonly used variables in the political strategy literature because they represent a firm’s visibility, performance, and resources, respectively (Getz, 1997; Hillman et al., 2004). Firm age was measured by the number of years since the firm was established. Firm profitability was measured by the annual return on assets. Firm slack was measured by the quick ratio, sum of cash, and short-term marketable securities and receivables, divided by the total current liabilities (Baucus & Near, 1991; Davis & Mizruchi, 1999). Firm state ownership was measured by the percentage of state ownership of the firm.

At the industry level, we controlled for peer pressure, measured as the number of firms in the focal firm’s industry that have issued regulatory standards with government approval in the previous year at the two-digit industry level. Firms in highly concentrated industries are more likely to engage in lobbying and campaign contributions (Schuler et al., 2002). Thus, we included industry concentration at the four-digit industry level, which was measured by the Herfindahl index (i.e., the sum of the squares of the market shares of each firm within the same industry). This index ranges from 0 to 1.0, denoting the range from a large number of very small firms to a single monopolistic producer in an industry. We also controlled for industry munificence, measured by the regression slope coefficient of a given industry’s sales at the four-digit industry level in a 5-year window prior to the focal year (Keats & Hitt, 1988). This variable reflects the extent to which the industry environment can support firm growth (Dess & Beard, 1984). Firms in a more munificent environment have additional resources to engage in political action. Information for the two variables was obtained from the Industrial Statistical Survey Database constructed by the National Bureau of Statistics of China, which has been widely used in previous studies (Chang & Xu, 2008; Park et al., 2006; Tian et al., 2009). Finally, we fixed the industry effects at the two-digit level and the period effect by including a set of year dummy variables.

Statistical Methods

A common problem with our data is the nonrandomness of treatments. 14 Firms with political ties (treatment group) may systematically differ from those without political ties (control group), raising endogeneity concerns. We thus used propensity score matching (PSM) to generate a control group that has characteristics similar to those of the treatment group. PSM is a procedure that matches firms based on comparable characteristics in archival data instead of randomized experiments (Blevins et al., 2019; Haleblian et al., 2017; Hu et al., 2021). Specifically, our matching procedure used the dichotomous comparison of firms with any political connections (instead of the number of politically connected corporate leaders) to those without political connections. We used STATA 15’s “teffects psmatch” command to create propensity scores based on firm size, firm age, firm profitability, firm slack, state ownership, industry munificence, and industry concentration. We matched each firm in the treatment group with a firm in the control group with the closest propensity scores. We discarded unmatched observations in the control group. 15 According to Rosenbaum and Rubin (1983), such matching may asymptotically balance the observed covariates, mitigating biases conditional on these covariates. We evaluated average treatment effects (Blevins et al., 2019; Haleblian et al., 2017; Hu et al., 2021), that is, how regulatory standards-making is affected by political ties. Formally, average treatment effects were calculated as the difference (D) in expected standards-making in two similar Firms, A and B, with observable attributes Xa and Xb, whose probabilities of establishing political ties are about equal, as follows:

where

Building on the matched sample, given that our dependent variable is a dichotomous measure, we used logit regressions to estimate the results. In our panel data, the same firms were repeatedly observed for different years. The multiple observations of each firm may not be mutually independent. We recognized that the fixed-effects approach can be used to address such an issue. According to prior studies (Crossland et al., 2014; Henderson et al., 2006; Hillman et al., 2007), however, this approach did not seem to be a good fit for our data. A fixed-effects approach is generally inappropriate if within-firm variation is minimal over time. In our sample, approximately 75% of regulatory standards-making activities (i.e., dependent variable) did not vary over time. That is, 1,183 out of 1,536 firms did not make regulatory standards in our observation window. Thus, we employed robust standard errors clustered by firm IDs to avoid any biased estimations that result from the interdependence of observations (Greene, 2000).

Following prior research (Crossland et al., 2014; Gamache et al., 2020), we utilized a generalized estimating equation (GEE) to estimate the correlation structure of the error terms (Liang & Zeger, 1986). In GEE, the data are clustered within firms, allowing for the analysis of within- and between-firm variations (Liang & Zeger, 1986). GEE does not require the assumption that unobserved firm-specific error terms are fixed over time for each firm. In contrast to a random effects approach, GEE does not require the strong assumption that unobserved firm-specific effects are uncorrelated with the regressors (Liang & Zeger, 1986). Thus, GEE represents a generalized linear model that considers within-firm correlations, correcting for violating the assumptions that unobserved firm-specific characteristics are uncorrelated (Stata Manual, 2003). Relaxing these assumptions allows the choice of multiple correlation-matrix structures that best match the data (Liang & Zeger, 1986). We estimated our results using the maximum likelihood estimation of the logit regressions with GEE stratification, using STATA 15.

Results

Overall Results

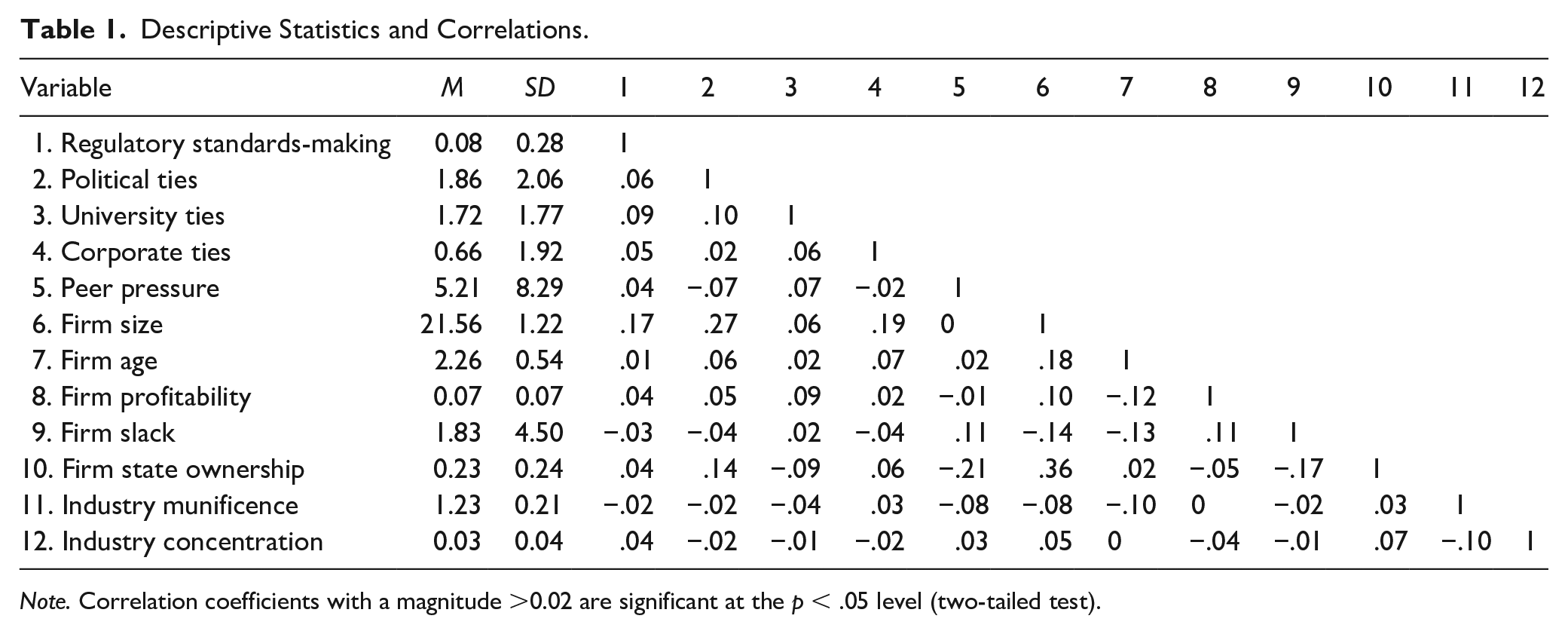

Table 1 presents descriptive statistics and correlations for all analyzed variables. To address the potential problem of multicollinearity between the component and interaction terms, we ran the analysis after all component variables were centered on the means. The variance inflation factor (VIF) for each predictor variable was calculated to check for multicollinearity. The VIFs of all variables were <1.27, indicating that multicollinearity was not a problem in our regression analyses (Hair et al., 1998). For ease of data interpretation, all variables in Table 1 are reported prior to their transformation.

Descriptive Statistics and Correlations.

Note. Correlation coefficients with a magnitude >0.02 are significant at the p < .05 level (two-tailed test).

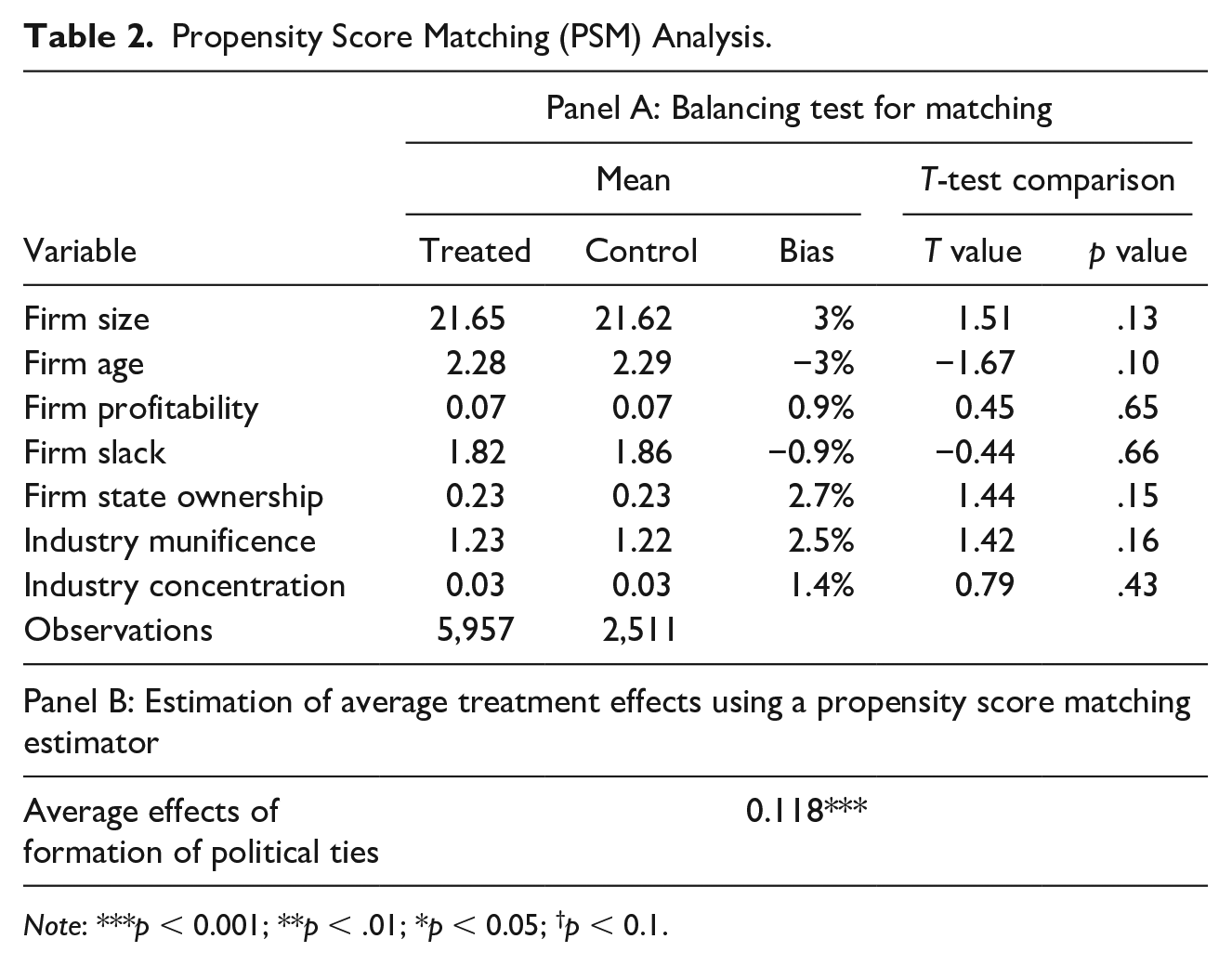

Table 2 presents the results of the propensity score analysis. Specifically, the table presents the balancing diagnostics, the differences in covariates of the treatment and control groups, and the results when we test whether the covariates are independent of treatment assignments. We used t-tests to determine whether the treatment and control groups are statistically different (Blevins et al., 2019) and found that the pairwise differences between the treatment and control groups are statistically insignificant for all covariates of interest (all p ≥ .10), demonstrating the balancing property and indicating the matching effectiveness. The propensity score analysis also estimates average treatment effects (i.e., the effects of political ties on regulatory standards-making). The results indicate that the average treatment effect is positive (β = .118, p < .00).

Propensity Score Matching (PSM) Analysis.

Note: ***p < 0.001; **p < .01; *p < 0.05; †p < 0.1.

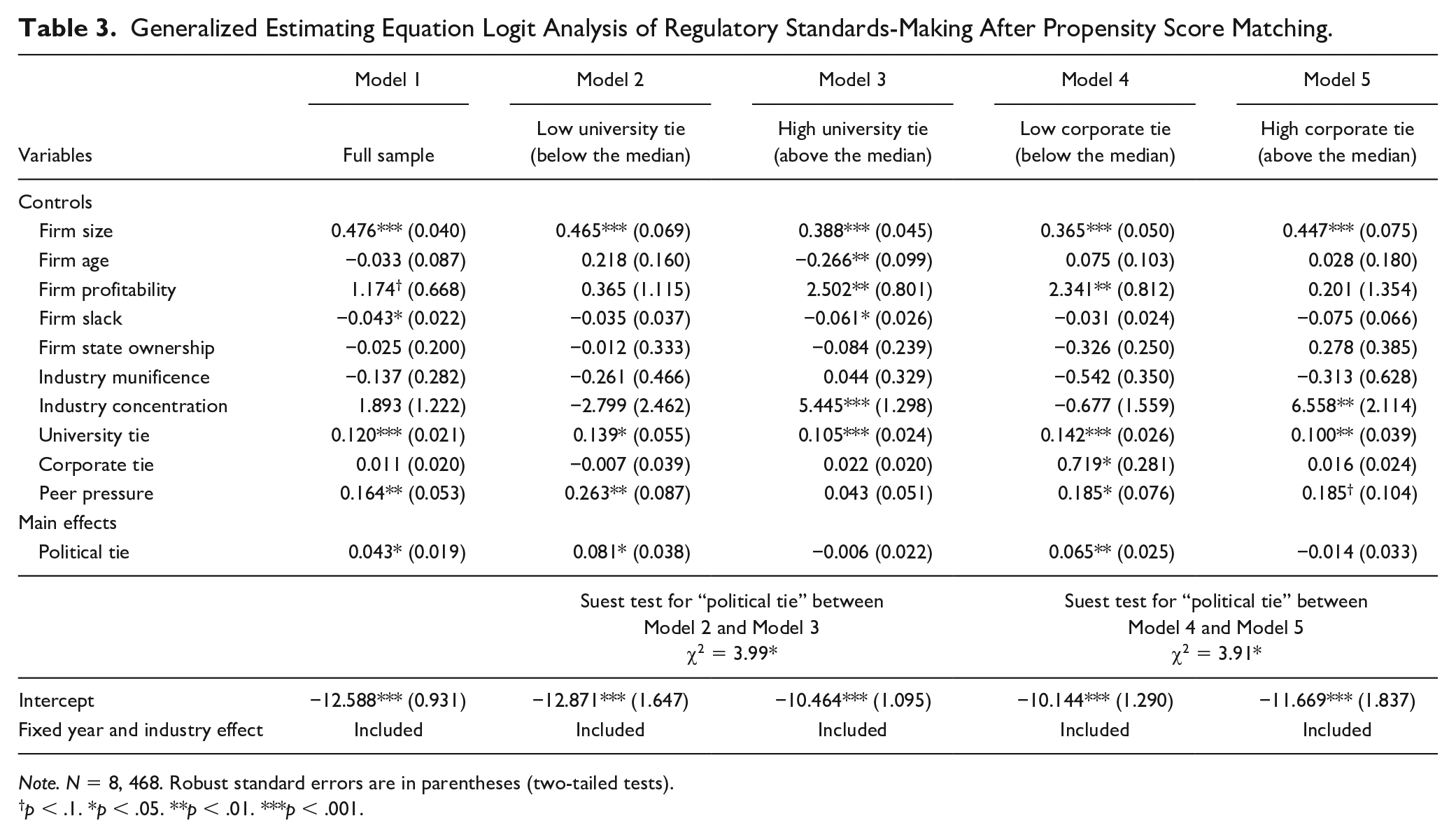

Table 3 presents the results of GEE logit regression models for the propensity score matched sample. Model 1 tests the main effect of political ties. Because the interpretation of interaction terms for moderating hypotheses in nonlinear models is complicated (Jeong et al., 2020), we split the sample to test the moderating effects of university ties and corporate ties. Models 2 and 3 split the sample into two subsamples by using the median of university ties to test the moderating effect of university ties on the relationship between political ties and regulatory standards-making. Models 4 and 5 split the sample into two subsamples by using the median of corporate ties to test the moderating effect of corporate ties.

Generalized Estimating Equation Logit Analysis of Regulatory Standards-Making After Propensity Score Matching.

Note. N = 8, 468. Robust standard errors are in parentheses (two-tailed tests).

p < .1. *p < .05. **p < .01. ***p < .001.

H1 predicts a positive association between political ties and regulatory standards-making. The coefficient for political ties is positive and significant (β = 0.043, p < .05) in Model 1. Regarding effect size, for each additional political tie, the odds of making new national standards increases 4.42%. Hence, H1 is supported.

H2a and H2b posit that university ties and corporate ties, respectively, weaken the effects of political ties on a firm’s regulatory standards-making activities. Model 2 provides results for the subsample with low university ties; the coefficient of political ties is positive and significant (β = 0.081, p < .05). Model 3 presents regression results for the subsample with high university ties; the coefficient of political ties is insignificant. The Hausman test, using the “suest” command, reveals that the coefficients of political ties are significantly different between Models 2 and 3 (χ2 = 3.99, p < .05), supporting H2a. Model 4 provides results for the subsample with low corporate ties; the coefficient of political ties is positive and significant (β = 0.065, p < .01). Model 5 presents regression results for the subsample with high corporate ties; the coefficient of political ties is insignificant. The Hausman test shows that the coefficients of political ties are significantly different between Models 4 and 5 (χ2 = 3.91, p < .05), supporting H2b.

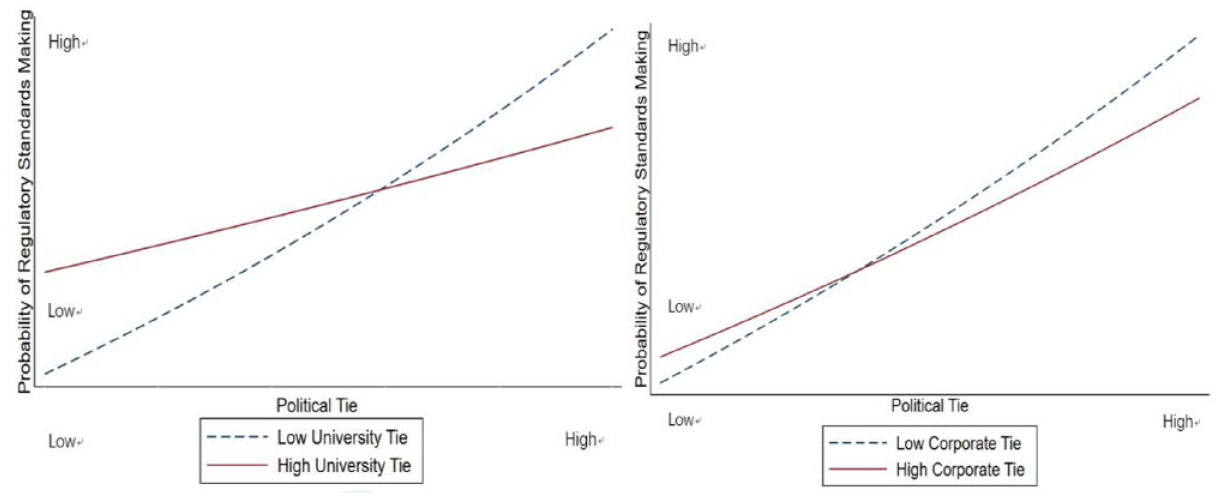

We further illustrate the moderating effects of university ties and corporate ties in Figure 1, in which “high” and “low” are defined as one standard deviation above and below the mean, respectively. The figure shows that the positive effect of political ties on the firms’ propensity to set regulatory standards is weaker for firms with more university ties and stronger for firms with fewer university ties. The figure also shows that the positive effect of political ties on the firms’ propensity to set regulatory standards is weaker for firms with more corporate ties and stronger for firms with fewer corporate ties. These results further confirm our findings.

Two-Way Interactions Between Political Ties and University Ties and Between Political Ties and Corporate Ties.

Robustness Tests

A Generalized Method of Moment Approach

An alternative approach to address endogeneity is to use the generalized method of moments (GMM) model. 16 Following prior studies (J. Li et al., 2021; Wintoki et al., 2012), we use the STATA “xtabond2” command to generate the GMM estimator for a dynamic panel model and find a positive and significant coefficient for political ties (β = 1.086, p < .01). The results for the subsample analyses at different levels of university ties show that the coefficient of political ties is positive and significant in the subsample of low university ties and insignificant in the subsample of high university ties. Similarly, the results reveal that the coefficient of political ties is positive and significant in the subsample of low corporate ties and insignificant in the subsample of high corporate ties. The Hausman test, using the “suest” command, further supports significant differences of coefficients between subsamples. We thus obtain regression results that are largely consistent with those reported by the GEE.

An Alternative Measure of Regulatory Standards-Making

We calculated the count dependent variable by counting the number of GB standards developed by each firm in each year. Building on the matched sample, we considered Poisson regressions to estimate the results, given that the number of GB standards is a count measure that takes integer values from zero upward. As the distribution of our dependent variable exhibited an overdispersion, we chose a negative binomial model to analyze the data, relaxing the Poisson assumption of an equal mean and variance (Cameron & Trivedi, 2013; Greene, 2000). We estimated our results using the maximum likelihood estimation of negative binomial regressions with GEE stratification. Moreover, the count dependent variable is zero-inflated, as many firms did not develop regulatory standards in our observation window. We therefore performed zero-inflated negative binomial regression analyses as well. In addition, we conducted linear probability analyses. 17 Tables A1, A2, and A3 in the appendix present the regression results for the GEE negative binomial models, the zero-inflated negative binomial models, and the linear probability estimation models. We found largely consistent regression results by using the alternative dependent variable and regression models.

An Alternative Measure of University Ties

We counted the number of professors who served as independent directors on a firm’s board each year and found robust results. Table A4 in the appendix presents the regression results for this alternative measure. The results based on the subsample analyses between different levels of university ties show that the coefficient of political ties is positive and significant in the subsample of low university ties and insignificant in the subsample of high university ties. The Hausman test shows that the coefficients of political ties are significantly different between the two subsamples (χ2 = 4.06, p < .05).

Potential Contingency Condition: A Post Hoc Analysis

We introduce peer pressure as a potential contingency under which the negative moderating effect of nonpolitical ties on the relationship between political ties and corporate participation in regulation-making diminishes. When peer firms frequently produce new regulatory standards, peer pressure and the lockout effect are stronger. In other words, setting such standards challenges incumbents with established standards (Garud et al., 2002) and threatens the operations 18 (Lipton & Abrams, 2016) of industry firms that cannot meet or beat the new regulatory standards due to the technological lock-out effect (Schilling, 1998). As a response, industry rivals tend to match each other’s actions, such as making political donations (Hersch & McDougall, 2000), to control the regulation-making process to reduce external pressure (Buchanan et al., 1980; X. Deng et al., 2010; Shaffer, 1995).

Moreover, under greater peer pressure, firms may downplay the divergent opinions from nonpolitical stakeholders (university professors and interlocking directors), thereby mitigating the constraint of nonpolitical ties for better “exploiting firm-specific political resources” (Frynas et al., 2006, p. 322). As political connections provide “intelligence and cognitive maps about nonmarket environments” (Boddewyn & Brewer, 1994, p. 136), firms with such connections may leverage the intellectual capital derived from university ties to gain government approval (Nahapiet & Ghoshal, 1998). University ties may help to redress concerns regarding technological viability and allow government officials to more favorably evaluate a firm’s competence to make a regulatory industry standard (Higgins & Gulati, 2003). Furthermore, firms with political ties also may leverage corporate ties to gain industry information that is important for standards-making (Shapiro & Varian, 1999; Waguespack & Fleming, 2009). Thus, under great peer pressure, the negative moderating effect of nonpolitical ties on the relationship between political ties and regulatory standards setting may diminish to a certain degree because firms are under greater urgency to participate in regulation-making in response to peer pressure.

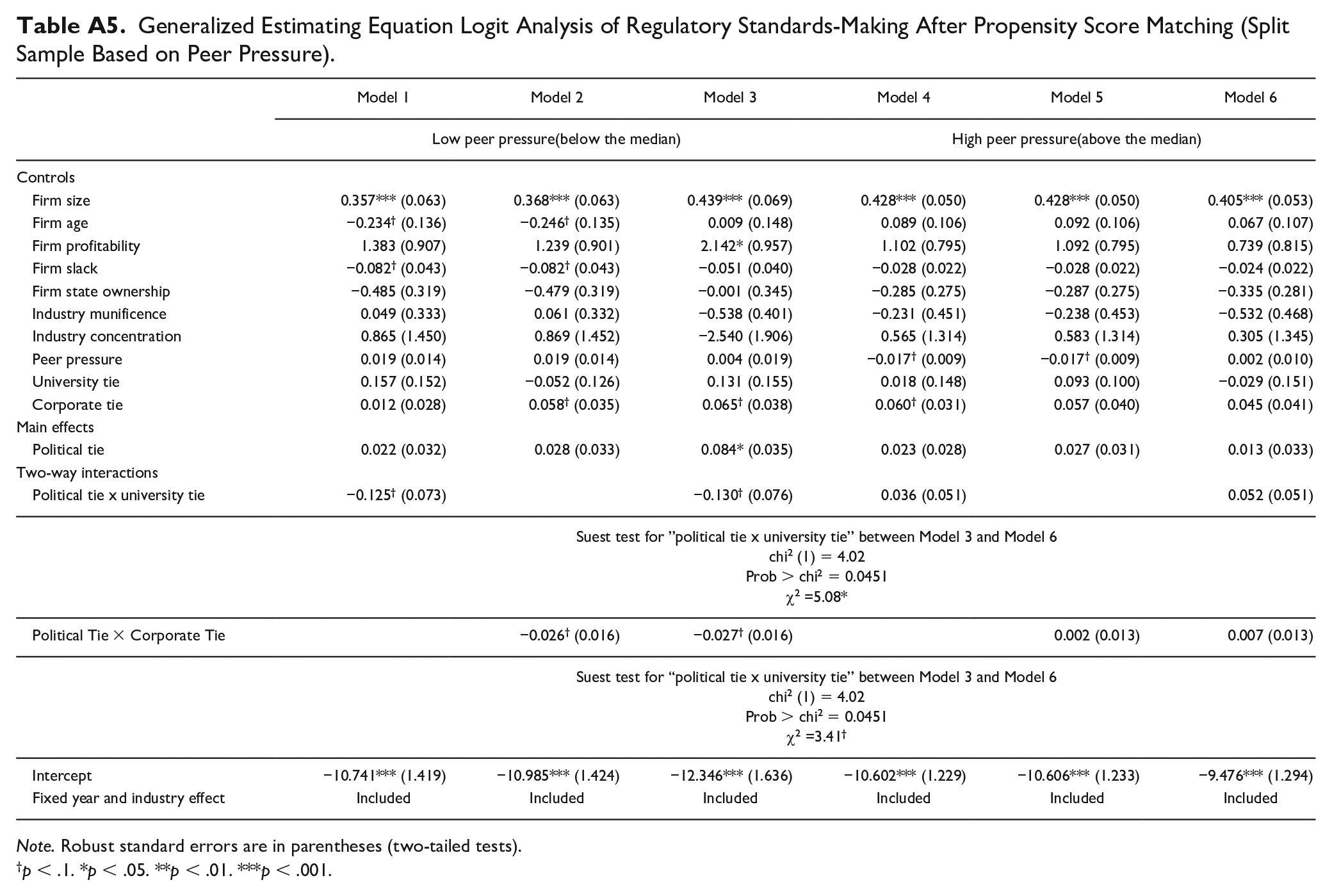

To examine the moderating role of peer pressure, we split the sample into two subsamples using the median of peer pressure. Table A5 in the appendix presents the regression results. We find that, in the subsample of low peer pressure, the coefficient of interaction between political ties and university ties is negative and marginally significant (β = −0.130, p < .10), and the coefficient of interaction between political ties and corporate ties is also negative and marginally significant (β = −0.027, p < .10). In the subsample with high peer pressure, the coefficients of the interaction between political ties and university ties and the interaction between political ties and corporate ties are insignificant. The Hausman test, using the “suest” command, shows that the coefficients of the interaction between political ties and university ties are significantly different between the two subsamples (χ2 = 5.08, p < .05), and the coefficients of the interaction between political ties and corporate ties are marginally significantly different between the two subsamples (χ2 = 3.41, p < .10). The regression results are largely consistent with our predictions.

Discussion

This study addresses the extent to which political and nonpolitical ties jointly affect corporate participation in regulation-making. Our findings suggest that political ties drive regulatory standards setting. When firms have more nonpolitical (university and corporate) ties, however, the effect of political ties is weaker. Intuitively, political and nonpolitical ties can be complementary. Political stakeholders, however, draw a firm’s attention to political solutions, whereas nonpolitical stakeholders tend to drive political participation by following professional norms or reciprocal firm benefits. As shown in our study, organizations may be difficult to balance as satisfying the opinions of one type of stakeholder may disregard the opinions of another type of stakeholder. Given that our knowledge of how individual firms gain government approval to create industry regulations is limited (for reviews, see Dal Bó, 2006; Hillman et al., 2004; Lux et al., 2011), our study takes an important step in addressing the gap in the literature, which has important theoretical and practical implications.

Our research contributes to the organization literature by identifying regulatory standards setting as a nonmarket strategy by which firms influence government regulations (Lawrence & Suddaby, 2006). Although nearly 75 years ago, Selznick (1949) noted that organizations can gain external support through co-optation in the form of interfirm alliances, joint projects, or special committees (Gargiulo, 1993), most studies have focused on co-optation between organizations rather than regulatory capture. As firms are actively involved in regulation-making, regulatory capture by corporations increases (Marsden et al., 2009) to influence and create new regulations (Dal Bó, 2006; Hillman et al., 2004).

Our theoretical framework and findings extend regulatory capture theory by examining the joint effect of political and nonpolitical ties on corporate regulation-making. A stream of research has emphasized political actions through campaign donations or lobbying used by firms to establish a competitive advantage over rivals (Gale & Buchholz, 1987; Leone, 1986; McWilliams et al., 2002; Shaffer, 1995). These studies, however, have focused on political actions through the capture of legislators or government agencies (D. Carpenter & Moss, 2013; Etzioni, 2009), whereas our study focuses on the direct capture of regulations, which is supported by the regulator. Our study shows that the idea of regulatory capture developed in political economics can help to enrich strategy research (Jia et al., 2022). Moreover, our findings support the notion that it is useful to study complex relationships among multiple ties to enrich the theoretical approach (Davenport & Skandera, 2003; Gould, 2003; Lim, 2010).

Although our study also complements the literature on standards wars (Stango, 2004), defined as “battles for market dominance between incompatible technologies” (Shapiro & Varian, 1999, p. 8), that has documented numerous historical episodes of such wars, including the competition among Apple’s iPhone, Motorola’s Droid, RIM’s Blackberry, and Palm’s Pre in the smartphone market (Q. Wang & Xie, 2011), empirical studies are rare. This literature emphasizes the mechanism of competition among industry firms through which “the winner takes all” (e.g., Microsoft in desktop operating systems and the Video Home System format in home Version Control Systems), as standards incompatibility eliminates competitors (Giessmann & Stanoevska-Slabeva, 2012) and thereby motivates firms to proactively promote their own standards as de facto. Once a firm’s technical standard wins the battle, it leads to a single, winner-take-all outcome (Stango, 2004). In this regard, standards wars essentially reflect market competition without much state intervention (Porter & Strategy, 1980). Our study shows that standards wars can be transformed into political competition among industry firms to influence the regulator. When the government attempts to regulate industry standards, firms may capture the process.

Our findings have important implications for both firm managers and regulators. As Lester and colleagues (2008, p. 1000) noted, “nearly every aspect of business is shaped by government regulation, which can significantly modify firms’ opportunity sets.” Corporate regulation-making is a joint effort between regulated firms and the regulator, which can be viewed as a type of techno-political action to standardize firm practices. Regulations are not written in a vacuum but, rather, rely upon expertise as a sine qua non in the face of complex issues. This situation leads the regulator to depend on firms to leverage their expertise to provide solutions, thereby tailoring regulations to the industry spectrum (Ayres & Braithwaite, 1992).

As the required expertise is provided by individual firms, it opens up the potential for regulatory capture that allows certain firms to influence regulation that creates standards for other firms to follow. Political ties are viewed as relevant determinants of a firm in gaining state approval (Shaffer, 1995). In emerging economies, individual-based political connections that are widely deemed as corporate elites, assemble, along with political elites, a prestigious group (Walder, 2003) to participate in political events and public affairs (X. Deng et al., 2010; Jia, 2014; Pfeffer & Salancik, 1978). Given that political and nonpolitical stakeholders often have diverging preferences, opinions, and expectations, firms may manage them appropriately to reduce internal conflict.

For regulators, government agents often enjoy considerable autonomy in regulating firms. Regulators are expected to promote the public interest when regulating firms, but they are capacity-constrained due to insufficient information on business operations (Stigler, 1971; Yackee & Yackee, 2006). Interoperable standards are essential for stabilizing resource exchanges among firms, industries, and countries. The regulator must provide adequate guidance to protect consumers by using a single standard to reduce switching costs (Greenstein, 1992) to facilitate exchange and international trade and to enhance technological advancement. In addition, new regulatory standards change the competitive landscape (Getz, 1997; Mahon et al., 1989). The lack of transparency is critical to understanding the outcomes of regulatory capture (Dal Bó, 2006). An effective regulator can avoid or reduce negative outcomes by using more transparent procedures for all regulated players (D. Carpenter & Moss, 2013). Broader input by public notice may also help to prevent negative outcomes (Ayres & Braithwaite, 1992; Thaw, 2013).

The limitations of our study suggest future research directions. First, examining our theoretical framework in a single context (i.e., China) raises concerns regarding the generalizability of our findings. It is worth noting that compared to many other countries, China has a notably higher prevalence of politically connected firms (Faccio, 2006). First, as the Chinese government controls substantial national resources, firms may actively seek to establish ties with government agencies for resources (J. Jiang & Zhang, 2020). Observations show that government officials are often appointed as executives and board directors (Liu et al., 2019). Second, as the regulatory environment in China frequently requires government approvals for various business activities, firms with political connections may gain an advantage in obtaining permits and navigating bureaucratic hurdles (Y. Chen et al., 2020). Finally, although the country has experienced a period of reform from a planned economy to a market one, the government has still maintained a significant level of involvement in economic activities (Zhang, 2022). Given the context-specific test, we must interpret our findings with caution. We encourage future research to examine our theoretical framework in different contexts as attempts by a government to regulate firm practices and operations vary across countries (Garcia, 1992; Gibson, 2007).

Second, our study focuses on how the political ties of corporate leaders affect regulatory industry standards; future studies could also consider how their nonpolitical ties may affect nonmarket actions because these corporate leaders are more subject to the influence of different mechanisms. Among various nonpolitical stakeholders, we focused on a firm’s university and corporate connections to test our theory. As many nonpolitical stakeholders exist, however, future research may consider the potential impact of other nonpolitical stakeholders, such as trade associations or nongovernmental organizations (NGOs), to broaden our knowledge. A trade association often represents the shared interest of its members in a specific industry (Lawton et al., 2018). A firm as a member of a trade association may consider other members’ interests in the association when making regulatory standards. Industry members, however, may also compete for making regulatory standards. Thus, future research could explore whether firms with such nonpolitical connections may leverage political ties to pursue collective interests or individual firms’ competitive advantage. This research direction may shed light on whether trade associations promote collective actions or individual firms’ nonmarket actions.

Moreover, NGOs have played an essential role in changing societal expectations of business by influencing the attention of firms and the public interests (Nelson, 2007). Under the pressure of NGOs, firm nonmarket actions need to take the public interest into consideration. We know little about how NGO pressures and political forces jointly affect regulatory standards setting. Future research on this subject could help clarify the role of NGOs in shaping nonmarket actions. In addition, we study the joint effect of political and nonpolitical ties on corporate regulation-making at the firm level. Future research may explore how individual differences associated with each tie within a firm affect nonmarket action. For example, individual differences of interlocking directors within the same firm, such as their motivation, experience, and status, might shape their preferences for nonmarket actions (Shropshire, 2010).

Third, our findings suggest that corporate leaders with political and nonpolitical ties conflict in affecting firm participation in regulation-making and raise the question of why they might coexist in a firm. If the effectiveness of political connections is reduced in the presence of nonpolitical stakeholders, firms with nonpolitical stakeholders should be less likely to acquire political connections in the first place and vice versa. Addressing this issue involves the antecedents of whether corporate leaders with political and nonpolitical ties may coexist in a firm, which goes beyond the scope of our research, given that our study aims to understand the consequences of such coexistence. Thus, it is a worthwhile avenue for future research.

Fourth, our study draws on regulatory capture theory to explain the effect of relational ties. Future research may apply other theoretical perspectives, such as signaling theory, as relational ties also may signal a firm’s quality to government agencies (Spence, 2002). For example, although political connections signal a quality such as trustworthiness, nonpolitical connections signal a quality such as credibility in ways that allow the firm to engage in political action. Identifying different theoretical mechanisms is also a promising direction for future research. In addition, regulatory capture can take a variety of forms, which may affect policy-making (Hillman & Keim, 1995) in terms of technology standards (Narayanan & Chen, 2012). Future research may explain and predict the role of firms in making regulations in various institutional settings. Moreover, our study focuses only on a nonmarket action (i.e., participation in regulatory standards setting). Future research may examine how market and nonmarket actions can coexist.

Finally, our analysis emphasizes corporate participation in regulatory making as an outcome variable. Scholars have emphasized financial performance as an outcome of corporate political strategies (Hillman et al., 2004; Lux et al., 2011). These two types of outcomes may not always be consistent. For example, Oster (1982) found that a firm might encourage the passage of an industry regulation that can damage its rivals to gain a greater market share, even if the new regulation actually increases the overall costs of the entire industry. A dominant standard in a field may not necessarily be the technically “best” standard for a range of institutional and social reasons (Guilloux et al., 2013; Schilling, 1998; Suarez, 2004). Thus, future studies should consider different outcomes to advance our knowledge.

Footnotes

Appendix

Generalized Estimating Equation Logit Analysis of Regulatory Standards-Making After Propensity Score Matching (Split Sample Based on Peer Pressure).

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | |

|---|---|---|---|---|---|---|

| Low peer pressure(below the median) | High peer pressure(above the median) | |||||

| Controls | ||||||

| Firm size | 0.357*** (0.063) | 0.368*** (0.063) | 0.439*** (0.069) | 0.428*** (0.050) | 0.428*** (0.050) | 0.405*** (0.053) |

| Firm age | −0.234 † (0.136) | −0.246 † (0.135) | 0.009 (0.148) | 0.089 (0.106) | 0.092 (0.106) | 0.067 (0.107) |

| Firm profitability | 1.383 (0.907) | 1.239 (0.901) | 2.142* (0.957) | 1.102 (0.795) | 1.092 (0.795) | 0.739 (0.815) |

| Firm slack | −0.082 † (0.043) | −0.082 † (0.043) | −0.051 (0.040) | −0.028 (0.022) | −0.028 (0.022) | −0.024 (0.022) |

| Firm state ownership | −0.485 (0.319) | −0.479 (0.319) | −0.001 (0.345) | −0.285 (0.275) | −0.287 (0.275) | −0.335 (0.281) |

| Industry munificence | 0.049 (0.333) | 0.061 (0.332) | −0.538 (0.401) | −0.231 (0.451) | −0.238 (0.453) | −0.532 (0.468) |

| Industry concentration | 0.865 (1.450) | 0.869 (1.452) | −2.540 (1.906) | 0.565 (1.314) | 0.583 (1.314) | 0.305 (1.345) |

| Peer pressure | 0.019 (0.014) | 0.019 (0.014) | 0.004 (0.019) | −0.017 † (0.009) | −0.017 † (0.009) | 0.002 (0.010) |

| University tie | 0.157 (0.152) | −0.052 (0.126) | 0.131 (0.155) | 0.018 (0.148) | 0.093 (0.100) | −0.029 (0.151) |

| Corporate tie | 0.012 (0.028) | 0.058 † (0.035) | 0.065 † (0.038) | 0.060 † (0.031) | 0.057 (0.040) | 0.045 (0.041) |

| Main effects | ||||||

| Political tie | 0.022 (0.032) | 0.028 (0.033) | 0.084* (0.035) | 0.023 (0.028) | 0.027 (0.031) | 0.013 (0.033) |

| Two-way interactions | ||||||

| Political tie x university tie | −0.125 † (0.073) | −0.130 † (0.076) | 0.036 (0.051) | 0.052 (0.051) | ||

| Suest test for ”political tie x university tie” between Model 3 and Model 6 |

||||||

| Political Tie × Corporate Tie | −0.026 † (0.016) | −0.027 † (0.016) | 0.002 (0.013) | 0.007 (0.013) | ||

| Suest test for “political tie x university tie” between Model 3 and Model 6 |

||||||

| Intercept | −10.741*** (1.419) | −10.985*** (1.424) | −12.346*** (1.636) | −10.602*** (1.229) | −10.606*** (1.233) | −9.476*** (1.294) |

| Fixed year and industry effect | Included | Included | Included | Included | Included | Included |

Note. Robust standard errors are in parentheses (two-tailed tests).

p < .1. *p < .05. **p < .01. ***p < .001.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Dr. Lin wishes to recognize the financial support of Natural Science Foundation of Guangdong Province (2020A1515011227), and Fundamental Research Funds for the Central Universities (23JNULH05).