Abstract

This study adds to the emergent stream of work examining the micro-level antecedents of pay dispersion by focusing on how business founders’ personal characteristics influence pay dispersion in their organizations. We leverage stakeholder theory and the motivated information processing perspective to predict pathways between founders’ self- versus other-oriented motivations, their perceptions of employee and shareholder salience, and pay dispersion in their organizations. We test our hypotheses on data from a two-wave survey of founders. We find that a high level of motivation to benefit others on the part of a founder reduces the salience of shareholder concerns in decision-making, which in turn reduces pay dispersion. In contrast, a high level of motivation to benefit oneself heightens the salience of shareholder concerns in decision-making, increasing pay dispersion. Our results inform the debate on pay dispersion by elucidating the role played by founders’ self- versus other-oriented motivations and stakeholder salience perceptions.

Keywords

When the founder of remote social media startup Buffer announced in 2013 that he wanted to equalize pay for his employees, basing it entirely on each employee’s role and cost of hometown living, his employees were surprised as well as relieved. The approach, coupled with other initiatives over the years, has managed to keep pay dispersion in his organization low, despite challenges (Goldberg, 2021). This comes at a time when other organizations, such as Google and Uber, have faced litigation as well as employee and media backlash for alleged unresponsiveness to their growing pay dispersion (Barnard-Bahn, 2020). Such examples are increasingly noted, as the question of how organizations and their leaders affect pay dispersion is garnering considerable attention within industry, academic, policy, and public discourse. Indeed, there is overwhelming evidence that organizational pay dispersion is rising exponentially in developed countries (Cobb & Lin, 2017; Orlitzky et al., 2006), to a substantial extent due to organizational practices—not employee productivity differences (Organisation for Economic Cooperation and Development [OECD], 2021; Piketty & Saez, 2014). In turn, the detrimental outcomes of pay dispersion at the societal level are receiving increasing attention (Bapuji et al., 2020; Doyle & Stiglitz, 2014) and have brought organizations and their leaders’ complicity under the microscope. In North America and Europe, policymakers have already enacted a range of regulations to curb excesses in pay dispersion (Carnegie, 2022; Goldberg, 2021; U.S. Securities and Exchange Commission, 2022). In response, organizations are trying to understand the internal biases that contribute to pay dispersion, so that they can design effective remedies (Barnard-Bahn, 2020). While remedying ingrained levels of pay dispersion can be a daunting task for a mature organization, founders of new organizations have considerable leeway in setting their own pay (Kelley, 2022; Wasserman, 2017), and in setting their organization on a path of low pay dispersion early on, such as in the case of Buffer’s founder. Given that new organizations account for a large part of new job and wealth creation at the societal level (Audretsch et al., 2006; Baumol, 1996) and that founders’ actions can result in societal outcomes ranging from the productive to the destructive (Baumol, 2016), examining their effect on pay dispersion is timely.

Existing literature on organizational leaders and their decision-making process emphasizes the importance of considering stakeholders’ interests and requests when allocating resources within their organization (Berman et al., 1999; Freeman, 1984; Parmar et al., 2010). Indeed, founders and their organizations do not exist in a vacuum but operate within a system of dense social interdependencies with their stakeholders (Mcvea & Freeman, 2005; Saxton et al., 2016). However, stakeholders’ interests and requests in relation to specific value allocation-related decisions do not always align, leaving to the organizational leader the role of committing to one request over another (Agle et al., 1999). This is particularly true in terms of attending to the two primary groups of shareholders and employees, whose interests and actions have been theorized to influence pay dispersion (Bapuji et al., 2020; Bidwell et al., 2013; Cobb, 2016). To theorize how founders’ perception of shareholders and employees’ salience can influence pay dispersion in their organizations, we build on stakeholder theory and the stakeholder salience framework (Berman et al., 1999; Freeman, 1984; Parmar et al., 2010). We claim that the salience of shareholders and employees to founders is integrally connected to their value allocation-related decision-making (Parmar et al., 2010) and to decisions that affect pay and pay dispersion (Bapuji et al., 2018; Bidwell et al., 2013; Cobb, 2016; Davis & Kim, 2015). However, we hypothesize that the salience of these two groups to founders is partly dependent on founders’ micro-level characteristics.

To better explain why and how each founder will attend to one stakeholder group’s interests and requests over another, we take note of a stream of work in stakeholder literature (Agle et al., 1999; Jones et al., 2007; Mitchell et al., 2016; Neville et al., 2011; Weitzner & Deutsch, 2015) that suggests that stakeholder salience will be influenced by leaders’ stable personal biases, especially those related to self- and other-oriented motivation. Furthermore, we turn to work in social psychology that provides concrete evidence that these motivations routinely bias individuals’ assessment of information and their decisions to capture versus distribute wealth (De Dreu, 2006; De Dreu & Nauta, 2009; Liebrand et al., 1986; Meglino & Korsgaard, 2004). Following this stream of work, conceptualized as the “motivated information processing” perspective (De Dreu, 2007), we argue that these motivations will influence founders’ focus, memory and weighting of expected individual versus collective interests, the types of stakeholders that they consider most salient, and ultimately their choices toward different levels of pay dispersion in their organizations. Thus, bringing together the stakeholder salience framework and the motivated information processing perspective, in this study we hypothesize and test the salience of employees and shareholders as mediating the relationships between self- and other-oriented motivations, and pay dispersion.

Findings derived from two waves of original survey data of Finnish founders indicate that shareholder salience is the primary path through which their self- and other-oriented motivations translate into heterogeneity in pay dispersion. Specifically, self-oriented motivation increases pay dispersion through an increased salience of shareholders to the founder, while other-oriented motivation reduces the salience of shareholders, thus mitigating pay dispersion. In contrast, and contrary to our prediction, the positive influence of other-oriented motivation on employee salience does not translate into reduced pay dispersion. Similarly, high self-oriented motivation was not found to affect pay dispersion through reduced employee salience.

Drawing on these findings, we contribute to prior literature in two distinct ways. First, our study responds to calls of organizational researchers (Beal & Astakhova, 2017; Bidwell et al., 2013; Cobb, 2016; Tsui et al., 2018) to examine how the processes underpinning pay dispersion are enacted across organizations. Relatedly, we add to the organizational behavior literature on pay dispersion (Amore & Failla, 2020; Conroy et al., 2014; Shaw, 2014) by paving the way for a greater consideration of the antecedents and micro-level processes of the phenomenon. Second, our work establishes the relevance of the stakeholder salience framework to the theorizing of the links between the individual and organizational levels in the study of pay dispersion. Prior work on socially (ir)responsible behaviors and outcomes in organizations has considered stakeholder management issues as well as individual-level characteristics and perceptions of leaders (Agle et al., 1999; Galbreath, 2010; Tang & Tang, 2018; Weaver et al., 1999). Our study adds to this prior body of work by explicitly connecting the individual-level instrumental and moral consequences of the motivated information processing perspective (De Dreu & Nauta, 2009; Liebrand et al., 1986) and the instrumental as well as moral underpinnings of the stakeholder salience framework (Eesley & Lenox, 2006; Jones et al., 2007; Neville et al., 2011). In this way, our study promotes the integration of these two literatures in relation to socially (ir)responsible decision-making more broadly and to pay dispersion more specifically.

Our study is also informative for practice. Our findings attest to the central role that founders have in keeping in check versus exacerbating pay dispersion. At a time when organizations are increasingly held accountable for gaping levels of pay dispersion, founders that acknowledge that they are primarily self-orientated can more proactively commit to keeping pay dispersion in check. They could do this by, for example, actively questioning how shareholder salience affects their organization’s recruitment and promotion procedures or setting up institutional guardrails to ensure these are equitable and buffered from salient shareholder expectations. Policymakers might also be better able to combat increasing levels of pay dispersion within organizations if they are aware that founders are an early and enduring influence. While policymakers may not be able to directly observe the motivations of founders, they may be able to use indirect measures to identify and reward founders that exhibit behavior that is indicative of other-oriented motivation. Furthermore, one route to influencing the behavior of self-oriented founders is to try to affect shareholder salience for these founders. Policymakers could do this by reducing the salience of shareholders in the programs and discourse that they employ in their interactions with new organizations, and the broader business community.

Determinants of Organizational Pay Dispersion: A Literature Review

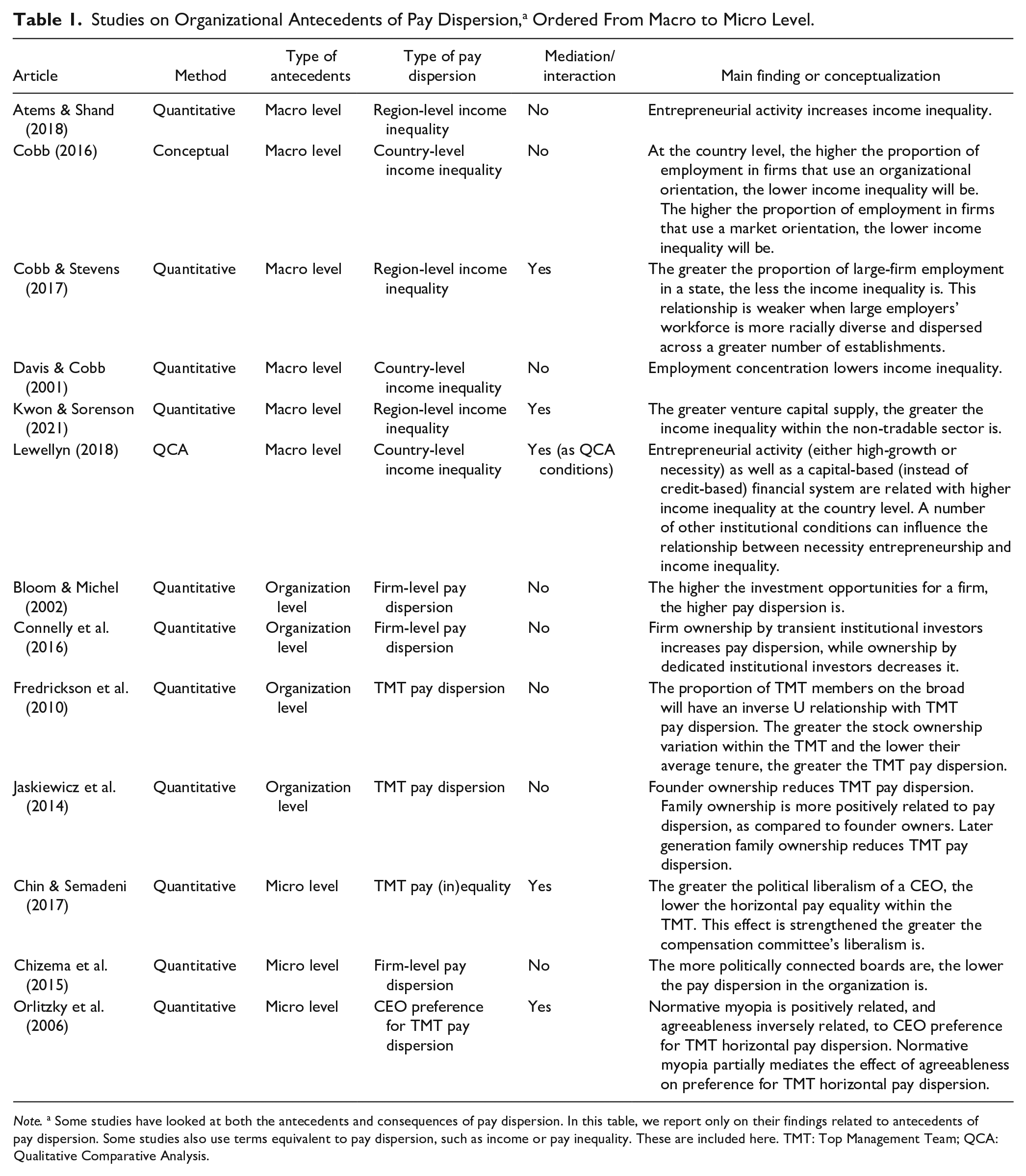

The bulk of existing literature on pay dispersion thus far examines its positive and negative organizational consequences (Li et al., 2021; Shaw, 2014). This work has firmly established that a substantial part of pay dispersion cannot be explained by productivity differentials between employees but is subject to several other influences. Thus, in line with the growing societal concern around pay dispersion, the focus of recent work is shifting toward the societal consequences (Bapuji et al., 2018), as well as antecedents (Bidwell et al., 2013; Cobb, 2016) of pay dispersion. Relatedly, a number of studies have adopted a macro lens to explain the institutional and organizational antecedents of pay dispersion at the country or regional level (see Table 1 for a summary). Nevertheless, scholars contend that a crucial next challenge is to understand “the micro mechanisms that underlie patterns observed at the organizational or field level” (Bidwell et al., 2013, p. 103). Micro-level factors include the characteristics of organizational leaders, who are key allocators of the value their organizations create, and can have considerable freedom and input in setting wages (Beal & Astakhova, 2017; Tsui et al., 2018). Founders in particular are less constrained by the inertia of large organizations (Agle et al., 1999) and can exert a lasting influence on their organizations (Beckman, 2006; Beckman & Burton, 2008).

Studies on Organizational Antecedents of Pay Dispersion,a Ordered From Macro to Micro Level.

Note. a Some studies have looked at both the antecedents and consequences of pay dispersion. In this table, we report only on their findings related to antecedents of pay dispersion. Some studies also use terms equivalent to pay dispersion, such as income or pay inequality. These are included here. TMT: Top Management Team; QCA: Qualitative Comparative Analysis.

As a result, an emergent stream of research has begun looking at the extent and ways that micro-level factors of organizational leaders can bias them in ways that contribute toward, or alternatively reduce, pay dispersion. For example, studies have shown that leaders’ political ideology as well as their agreeableness can affect pay dispersion within the top management team (Chin & Semadeni, 2017; Orlitzky et al., 2006). What this emerging stream of literature reveals is that value-allocation decisions are influenced by organizational leaders’ perceptions of their environment and these perceptions are determined by more stable individual differences. Building on this, we argue that organizational leaders’ perceptions of the environment involve instrumental, pragmatic, and moral considerations of multiple stakeholders that constitute the organization’s system of relationships (Berman et al., 1999; Freeman, 1984; Mcvea & Freeman, 2005; Parmar et al., 2010). Perceptions are in turn biased by those values and motivations that guide organizational leaders in the selection of information that results in the prioritization of wealth allocation interests and requests of specific stakeholder groups (Carnevale & Probst, 1998; De Dreu & Nauta, 2009). We explain our theoretical model next.

Research Model

Building on stakeholder theory (Berman et al., 1999; Freeman, 1984; Parmar et al., 2010) and the motivated information processing perspective (De Dreu, 2007; De Dreu et al., 2006), we develop a model that connects founders’ self- versus other-oriented motivations to organizational pay dispersion via shareholders’ and employees’ salience. Stakeholder theory expects that instrumental and pragmatic considerations, as well as moral considerations, translate into decision makers’ perceptions of the salience of different stakeholders, which can influence their responsiveness to competing stakeholder group interests (Berman et al., 1999; Freeman, 1984; Parmar et al., 2010). The stakeholder salience framework has emerged as the most used means of understanding the translation of multiple factors into the prioritization and accommodation of the interests of stakeholder groups. According to the original framework (Mitchell et al., 1997) and later revisions (Magness, 2008; Neville et al., 2011), stakeholders will become more salient to decision makers—thus prompting a greater accommodation of their interests—the greater their power, and the urgency and moral legitimacy of their claims (Eesley & Lenox, 2006). Stakeholders’ power refers to their ability to control resources, and thus decision makers’ attention. Urgency of the claim exists when there is a pressing call for attention (Magness, 2008; Mitchell et al., 1997). Finally, moral legitimacy is an assessment by the decision maker of the degree that a stakeholder’s claim is desirable or appropriate within personally, organizationally, and socially constructed systems of norms, values, beliefs, and definitions (i.e., moral legitimacy; Neville et al., 2011; Suchman, 1995).

Recent work has drawn connections between the salience of specific stakeholder groups, most notably shareholders and employees, and pay dispersion (Bapuji et al., 2020; Bidwell et al., 2013; Cobb, 2016). According to Bidwell and colleagues (2013), one important factor re-defining the relationship between employers and employees is the increasing power of shareholders to promote their own agendas and to capture an increasing share of the wealth created and distributed by organizations. In contrast, the authors identify employees as overall decreasing in terms of their power, and of their salience to employers, leading to their decreasing ability to capture value created by the organizations they work for. A recent review of the antecedents of pay dispersion equally identified attention to shareholders as the likely culprit for the increasing pay dispersion we are currently witnessing (Bapuji et al., 2020). Cobb (2016, p. 329) provides the most detailed theorization to date, according to which organizations are dominated either by internal considerations such as a “desire for equity” or by “pay and allocation decisions based on external criteria” of the market. These different focal points (internal vs external orientation) correspond to different pay distribution outcomes: lower when the focus lies primarily with internal stakeholders such as employees and higher when the focus lies primarily with shareholders.

The salience of other groups of stakeholders might also be relevant to pay dispersion. For instance, country-level actors such as government and unions (Bidwell et al., 2013) can use their power to mandate lower organizational pay dispersion. Similarly, at the industry level, non-profits could possibly exert pressures to large and visible organizations toward lower pay dispersion. Yet, the effects of regulation and unions, and the rare incidence of activist campaigns for pay equality cannot account for the differences between organizations (Tsui et al., 2018) or for founders’ role in pay dispersion. Moreover, while customers arguably exert a major influence on firms and are an important stakeholder group (Agle et al., 1999), the role of their salience on organizations’ pay dispersion remains unclear. Customer preferences can push organizations toward fair buying practices and certifications, for instance, especially for items produced in developing countries, but organizational pay dispersion is still not transparent to customers in most contexts. It is therefore uncertain at this point why and how customer salience could influence organizations’ pay dispersion. We consequently focus on the two primary groups of shareholders and employees, whose salience has been explicitly theorized in prior literature as relevant to pay dispersion outcomes (Bidwell et al., 2013; Cobb, 2016).

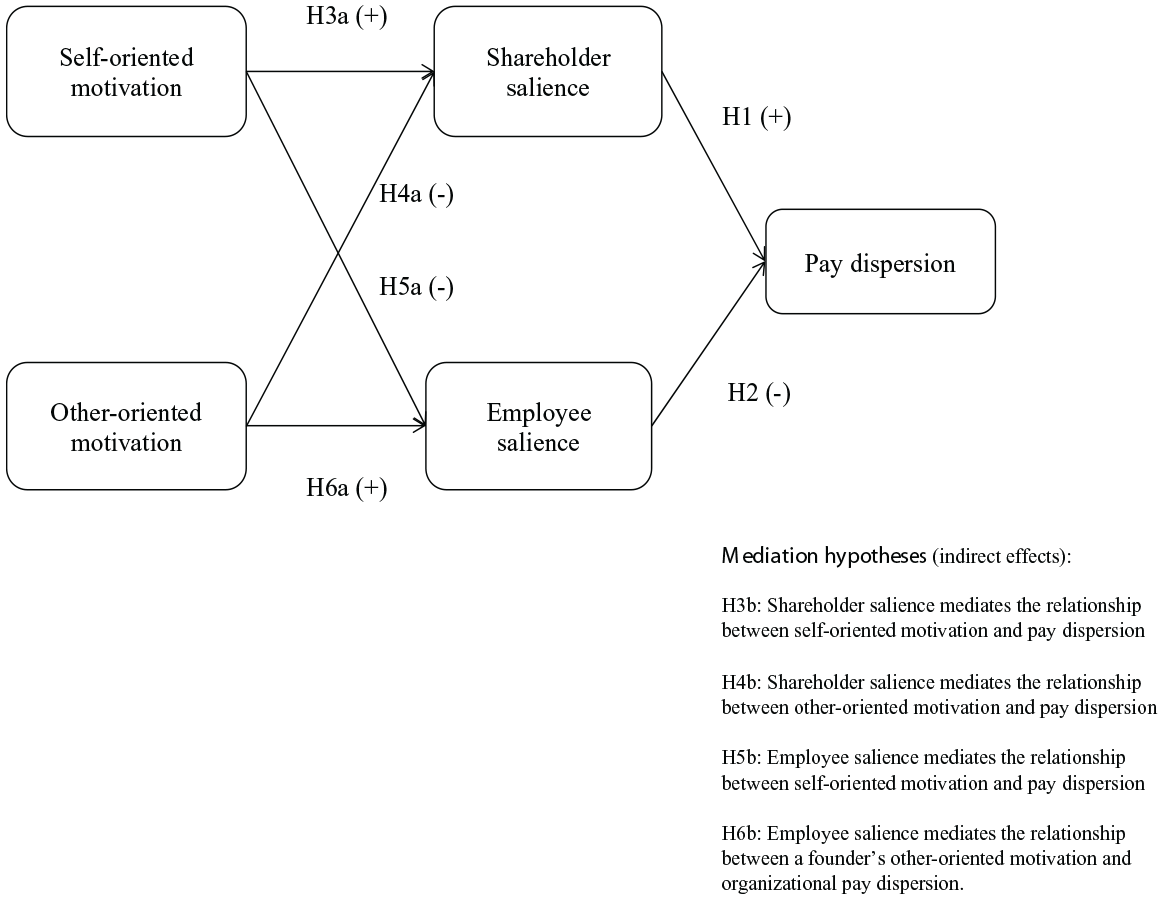

Building on the stakeholder salience theoretical framework, we argue that shareholders’ and employees’ interests in pay allocation decisions are both salient in the eyes of organizational founders. However, we hypothesize that the perceptions of power of these two groups of stakeholders, and the urgency and moral legitimacy of their claims lead to differential effects on pay dispersion (Hypotheses 1 and 2). We subsequently elaborate on the motivated information processing perspective (De Dreu, 2007; De Dreu et al., 2006) to argue that founders’ motivations help resolve this tension by influencing the perceptions of shareholders’ and employees’ salience (Hypotheses 3a, 4a, 5a, and 6a), and through these, organizational pay dispersion (Hypotheses 3b, 4b, 5b, and 6b). We summarize our hypotheses in Figure 1 and explain the rationale behind them in the following sections.

Theorized Model.

Shareholder Salience and Pay Dispersion

Shareholders are primarily concerned with growth and financial performance and represent a market logic that has been increasingly taken-for-granted in recent decades (Amis et al., 2020; Davis & Kim, 2015). According to a market logic, pay can be a tool that founders and employers more broadly can use to help shareholders achieve the highest possible growth and performance (Bidwell et al., 2013; Jaskiewicz et al., 2014). Accordingly, founders’ decisions on pay dispersion are influenced by their consideration of shareholders’ power as well as the urgency and moral legitimacy of their claim. Their strategic choices can have implications for shareholders’ return causing considerable financial harm to them and the organization (Berman et al., 1999).

Shareholders control resources they seek to mobilize by shifting the terms of the employment relationship in accordance with their own agendas, capturing increasing value for themselves versus other stakeholders in the short term (Bidwell et al., 2013). For example, shareholders exercise their power to counteract employee concerns for equal pay, promoting the application of external market rules in pay allocation decisions. In general, shareholders’ preference is reflected in an external market orientation that is aligned with market principles of highly differentiated pay (Bidwell, 2011; Cobb, 2016). Shareholders tend to favor a short-term, competitive point of view (Jacoby, 2018), according to which high pay is needed to quickly acquire talent from the market, as well as to motivate internal and external talent to exceptional performance (Bidwell, 2011; Connelly et al., 2016). This “shorter-term orientation discourages employers from bearing market risks on behalf of their workers and encourages them to use employment practices that lower costs and increase flexibility” (Cobb, 2016, p. 329; Kalleberg, 2013). A side-effect of this tendency is the reduction of wage premiums, particularly for less skilled employees, which in turn results in greater pay distribution across the organization (Cobb, 2016).

To signal the urgency of their request, shareholders exercise short-term pressure in regular intervals that results in the increasing rationalization of production, affecting how employee pay is set (Bidwell et al., 2013). Under this pressure, founders feel that internal organizational standards are less relevant criteria for employee pay, while market-based assessments become the main factor driving it (Cobb, 2016). For instance, to attract a new employee from the external market, pay will on average be set higher than for a similarly qualified employee who is already part of the organization due to information asymmetries between employers and employees in the job market (Bidwell, 2011; Dreher & Cox, 2000). In addition, founders attend to shareholders’ influence toward highly differentiated pay because they recognize the moral legitimacy of their request. Shareholder wealth maximization without constraints has become an institutional norm or “myth” that has departed from earlier conceptions of responsible capitalism and has become ingrained in modern culture (Amis et al., 2020; Bapuji et al., 2020). Thus, founders might see shareholders’ claim for highly differentiated pay as intrinsically right and proper (Neville et al., 2011).

By considering the power, urgency, and moral legitimacy of shareholders and their claim for growth and higher financial performance, founders perceive shareholders as highly salient and may resort to a greater extent to external market principles characterized by highly differentiated pay distributions when determining employee pay. Hence, we posit that:

Employee Salience and Pay Dispersion

Employees are frequently concerned with equal pay and fair treatment within the organization (Christie & Barling, 2010; Wade et al., 2006). They claim that pay allocation is a signal founders can use to show an organization’s attitude toward its employees (Bidwell et al., 2013; Tao et al., 2020). Accordingly, founders’ decisions on pay dispersion are influenced by their consideration of employees’ power as well as the urgency and moral legitimacy of their claim. Founders’ strategic choices can have implications for employees’ attitudes and behaviors, with important consequences for the organization (Berman et al., 1999).

Employees represent the most valuable intangible asset within the organization because with their efficiency and talent they can influence the survival, growth, and financial performance of their organization (Bidwell et al., 2013). Aware of their role within the organization, employees can exercise their power by modifying their attitudes and behaviors to impact participation and productivity. For example, when pay inequality is perceived, employees can try to eliminate or reduce perceived injustice by withdrawing work efforts, requesting pay increase, sabotaging other’s efforts, or leaving the organization (Nickerson & Zenger, 2008). These behaviors can be easily implemented by employees in their everyday job, reflecting the urgency of their request for equal pay. In addition, employees can exercise pressure on founders to address their claim by organizing strikes and turning to trade unions that can support them with financial resources to sustain their living expenses (Eesley & Lenox, 2006). To control employees’ power and reduce the pressure of their request for equal pay, founders can apply an internal market orientation, according to which internal criteria related to the organization function as guideposts for important decisions, including pay, while shielding employees from market pressures to a certain extent (Cobb, 2016). According to this long-term view, an internal orientation results in greater opportunities for the training and development of existing employees, more opportunities for internal promotions, and reduced pay dispersion.

Moreover, founders can consider applying an internal market orientation to determine pay allocation also because they embrace the moral legitimacy of employees’ claim. First, founders might attend to employees’ requests because they perceive that this is the right thing to do. While founders are primarily interested in organizational performance, they cannot overlook their leadership role and their influence in establishing an organizational culture that protects employees (Jones et al., 2007). Thus, we expect that after considering the power, urgency, and moral legitimacy of employees and their claim, founders are more likely to see this stakeholder group as highly salient. This perception contributes toward greater equalization in salaries (i.e., a decrease in pay dispersion) within an organization. Hence, we posit that:

Motivations and Shareholder Salience

Stakeholder theorists have for some time posited that one important antecedent to the salience of stakeholders, and accordingly, to organizational leaders’ decisions benefiting one stakeholder over another, are organizational leaders’ self- versus other-oriented motivations (Casson & Pavelin, 2016; Jones et al., 2007; Lewellyn, 2018; Mitchell et al., 2016). This stream of work has implied that leaders who are self-oriented might be more attentive to financial issues rather than issues of equality and social welfare, and vice versa for those who are primarily other-oriented. Yet, scholars have rarely tested these predictions nor examined the processes through which they should work (for an exception, see Agle et al., 1999). Nevertheless, social psychologists following the motivated information processing perspective have generated a rich stream of insights on how individual differences, in particular self- and other-oriented motivations, bias the ways that individuals process information and make decisions on wealth allocation and other value distribution tasks (Carnevale & Probst, 1998; De Dreu & Nauta, 2009). While several combinations of self- and other-oriented motivation could be possible for an individual, social psychologists have observed that in practice the majority of people are either primarily self-oriented or primarily other-oriented (Liebrand et al., 1986). Furthermore, the effects of such motivations have been proven to be separable from situational factors and manifest in individuals’ “stable preferences for certain patterns of outcome distributions to oneself and others in situations of social interdependence” (Carnevale & Probst, 1998, p. 1304). Both self- and other-oriented motivation work through affecting memory (Carnevale & Probst, 1998; De Dreu & Boles, 1998), focusing attention (De Dreu & Nauta, 2009; Grant & Berry, 2011), skewing the weighing of benefits and costs related to different distributions (T. Miller et al., 2012), and even by producing neural discomfort when individuals deviate from their stable preference (Van Dijk & De Dreu, 2021).

While the mechanisms underlying each motivation are similar, the attention and wealth distribution outcomes each one promotes can diverge widely. Individual self- versus other-oriented motivations can limit founders’ perceptions because they act as a filter through which they may select and interpret information (Kunda, 1990). Self-oriented motivation has been found to stimulate information scanning for, and processing of, individual-level attributes and self-relevant consequences, leading to prioritization of a competitive mindset and wealth distribution (De Dreu & Nauta, 2009; Grant, 2008). In contrast, other-oriented motivation information facilitates scanning for and processing of group-level attributes, social cues, and other relevant consequences, leading to prioritization of cooperation and wealth distribution benefiting mostly others (De Dreu & Nauta, 2009; Grant, 2008). On the basis of the above, we argue that founders’ self- and other-oriented motivations can be relevant to wealth distribution decisions, including employee pay.

Building on this argument, we theorize that founders who are high in self-oriented motivation might have more reasons to be highly attentive to shareholder expectations. A high self-oriented motivation “stimulates the individual to consider personal characteristics and qualities (e.g., competency needs, need for autonomy), personal inputs and outcomes, and personal success” (De Dreu & Nauta, 2009, p. 914). Furthermore, individuals high in self-oriented motivation primarily focus on “information about competitive tactics, about the effectiveness of competitive tactics, and about the counterpart’s lack of trustworthiness” (De Dreu et al., 2006, p. 929). A search in such individuals’ memories and existing mental sets therefore results in the more frequent recollection of experiences where a competitive and firm stance was necessary and in the selection of competitive, “zero-sum game” heuristics (Carnevale & Probst, 1998; De Dreu & Boles, 1998).

A competitive stance can also result in founders attending primarily to shareholder expectations and pressures in the case of wealth allocation problems and solutions. This is because the recollection of zero-sum game heuristics, cues, and incidents can steer founders’ focus toward “mighty” stakeholders (De Dreu & Boles, 1998) such as shareholders, who are aligned with a competitive, short-term, profit-oriented approach (Agle et al., 1999; Jacoby, 2018; Kalleberg, 2013). Self-oriented founders are thus likely to perceive, in line with shareholders, material incentives and threats as tools toward achieving profits (Weitzner & Deutsch, 2015), and furthering their personal interests. Accordingly, scholars have argued that self-oriented motivation is ethically more closely aligned to a market morality that attends to shareholders over other stakeholders (Jones et al., 2007; Neville et al., 2011). Concerns over relationships, fairness, justice, and rights, and “the larger social system” become tempered as one narrows the focus to shareholders (Agle et al., 1999; Wood, 1994), whose financial interests are largely aligned with those of founders’. Consequently, self-oriented motivation tends to result—on average—in shareholder’s power, urgency, and the moral legitimacy of their claim being perceived as more relevant for the success of the organization, which in the case of founders is directly connected with personal success (Arthurs & Busenitz, 2003; Jaskiewicz et al., 2014). We therefore expect founders high in self-oriented motivation to consider shareholders as highly salient. If this is the case, while, as argued in H1, shareholder salience positively affects pay dispersion, then shareholder salience should act as mediator between a founder’s self-oriented motivation and pay dispersion in their organizations. Based on the above, we posit that:

In contrast, founders who are high in other-oriented motivation might have fewer reasons to be highly attentive to shareholder expectations. These individuals are more likely to be more attuned to social, normative, and ethical cues and considerations than to instrumental ones (De Dreu & Nauta, 2009; Jones et al., 2007; Meglino & Korsgaard, 2007). Such considerations induce a sense of care and responsibility toward stakeholders who, although perhaps less powerful and more vulnerable, are nevertheless—or even because of this (Weitzner & Deutsch, 2015)—perceived as highly legitimate. Concurrently, such other-oriented considerations can lower the salience of shareholders based on their power, urgency, and the moral legitimacy of their claim to use pay allocation decisions as a tool toward achieving their objectives of growth and financial performance. Therefore, individuals who are high in other-oriented motivation are, when approaching situations where wealth needs to be allocated among stakeholder groups, less likely to recall competitive beliefs and the use of competitive heuristics (De Dreu et al., 2006). As a result, we expect that shareholder salience is reduced in the case of a founder high in other-oriented motivation. This would further imply that, if shareholder salience positively affects pay dispersion, as argued in H1, it should act as mediator between a founder’s other-oriented motivation and pay dispersion in their organization. Hence, we posit that:

Motivations and Employee Salience

According to the motivated information processing approach, information search and processing will be focused on the group with which one is in close contact and will incorporate the social cues related to and the consequences of any actions for this group (De Dreu & Nauta, 2009). In organizations, the most proximal group of reference is the group of employees. We expect a founder’s self-oriented motivation to dampen the salience of employees. Self-oriented motivation tends to result in employees’ claims being seen as less relevant to the success of an organization as compared with shareholders’ claims (Jones et al., 2007). Self-oriented motivation taken to the extreme can, through the evocation of competitive beliefs and heuristics, result in “arm’s length transacting, zero-sum bargaining, highly specified contracting, litigation of contract disputes and ambiguities, opportunistic exploitation of contracting failures, and aggressive exploitation of power imbalances”; it can also lead to employees being approached in a manner that reduces salary costs (Jones et al., 2007, p. 147) and overcompensates the highest performers. Thus, we propose that employees might overall be less salient to founders who are high in self-oriented motivation. Furthermore, if employee salience negatively affects pay dispersion, as argued in H2, then it should act as mediator between a founder’s self-oriented motivation and pay dispersion in their organizations. Hence, we posit that:

Conversely, we expect founders’ other-oriented motivation to stimulate the salience of employees. Other-oriented motivation induces the individual to “consider collective (group or organization) characteristics and qualities (e.g., relatedness), joint inputs and outcomes, and collective success” (De Dreu & Nauta, 2009, p. 1247). When faced with problems or decisions that relate to employees, individuals high in other-oriented motivation are able to retrieve from their memory beliefs and experiences that are more collaborative and inspire trust in joint undertakings and “win-win” solutions (De Dreu et al., 2006). Therefore, pay decisions are approached as an opportunity to attend to employees and foster their well-being and, through this, the well-being of the organization.

Furthermore, it has been shown that other-oriented motivation is closely connected to changes in the cost–benefit analysis that individuals mentally conduct, by increasing the perceived benefits of attending to others’ interests, while decreasing the perceived costs of doing so (Grant & Berry, 2011; T. Miller et al., 2012). As employees’ interest in equal pay allocation contrasts with shareholders’ pressure for higher pay dispersion, the other-oriented cost–benefit analysis will attach greater importance to the morality of decisions affecting employees (Neville et al., 2011). Other-oriented individuals are therefore “more likely to internalize, adhere to, and enforce societal norms even if doing so is personally costly” (Meglino & Korsgaard, 2007, p. 60). Therefore, both moral considerations and genuine concern for others will tend to take precedence over market-based considerations (Jones et al., 2007) for these founders, making them more attuned to equalizing pay decisions for their employees to protect them from the wide pay distributions dictated by market pressures. Employee salience should therefore increase for founders with higher other-oriented motivation. In turn, if employee salience negatively affects pay dispersion, as argued in H2, then employee salience should act as mediator between a founder’s other-oriented motivation and pay dispersion in their organization. Hence, we posit that:

Method

Data Collection

We tested our hypotheses on two waves of survey data on founders of 119 Finnish small and medium organizations. Finland was chosen because response rates tend to be high (Harzing, 1997), including for organizational leader samples and multiple waves of data collection (Hyytinen et al., 2015; Van Gelderen et al., 2015). Moreover, a culture of societal trust and individual honesty (Delhey & Newton, 2005; Helkama & Portman, 2019) increases confidence in reported answers on sensitive topics, such as pay dispersion. Finland is also a context where income inequality has increased markedly in the last years, despite traditionally low overall pay dispersion rates (Cobb, 2016).

To construct the sample, we started by extracting from Bureau van Dijk’s Orbis database the names and contact details of the entire population of businesses founded in Finland between 2005 and 2016. Founders exert substantial long-term influence on their organizations in comparison to hired managers that are constrained by the “vast inertia” of established organizational practices (Agle et al., 1999, p. 511; Finkelstein & Hambrick, 1988; McKelvie et al., 2011), and founders are easiest to access and research within the context of young organizations. The survey instruments were designed in English and translated into Finnish with the help of a local research agency specialized in survey research. Translations were double-checked by a management academic who is fluent in both languages.

The sample was narrowed down to 1,453 organizations that had a majority shareholding founder, allowing us to focus on individual founders rather than founding teams. All of these organizations were contacted by the research agency by telephone, to identify the majority shareholding founder, ensure that the person is still active in the organization, and then ask that person to participate in the survey. Upon receiving permission, the research agency sent an e-mail link to an online survey, which resulted in 409 responses (28% response rate). The Wave-1 survey measured individual motivations and the salience of the two stakeholder groups (i.e., shareholders and employees) in organizational decision-making. Six months after the completion of Wave 1, the local agency started to contact as many participants from Wave 1 as possible for a follow-up survey. Wave 2 concluded within 2 months with 119 participants (29% response rate). Because we sampled the entire population of Finnish businesses founded between 2005 and 2016, the businesses in the analytic sample represent a broad range of industrial sectors: 48% services, 19% construction, 15% manufacturing, 12% retail, 4% transportation, and 2% agriculture. In addition to these primary survey data, we also use financial data on the same organizations extracted from the Orbis database.

We examined potential nonresponse bias by comparing the 409 participants in Wave 1 with those 2,359 businesses that were part of the population but did not participate in this study (Rogelberg & Stanton, 2007). We performed mean comparisons based on variables derived from the Orbis database: organization size (total assets and number of employees), liquidity (current ratio), and performance (Return on Equity [ROE] before tax).The participants and non-participants did not differ significantly (p < .10) in terms of liquidity or performance. However, the organizations that responded are smaller on average than those that did not participate in the study. To control for size bias, we included organization size as a control variable in our analysis. Furthermore, we used the same variables to control for attrition bias between survey Waves 1 and 2. The businesses that participated in both waves did not differ significantly (p < .10) from those that only participated in Wave 1.

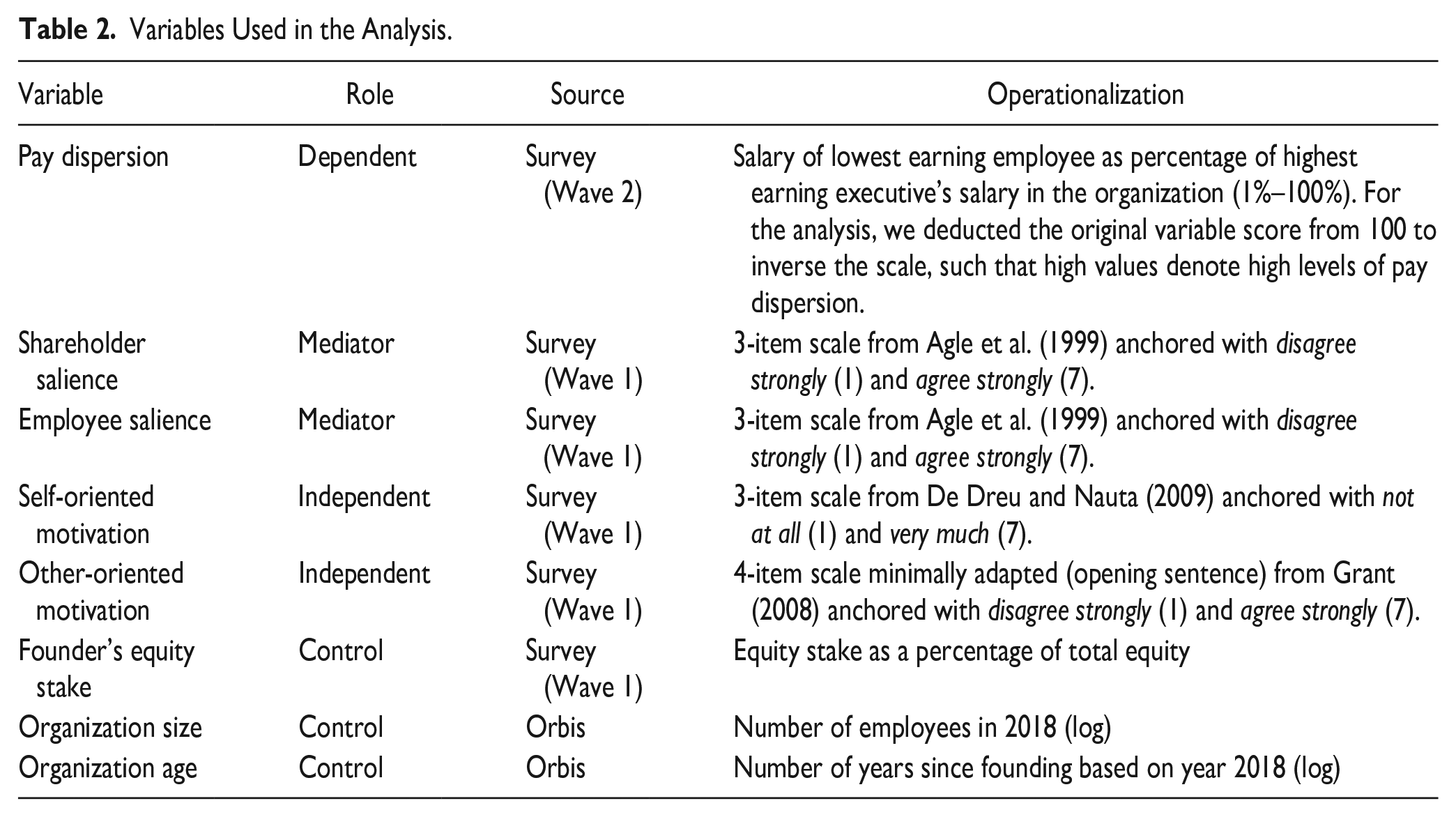

Variables

The variables used in this study as well as the sources from which they were drawn are summarized in Table 2.

Variables Used in the Analysis.

Obtaining pay data can be challenging (Shaw, 2014), especially so from younger and smaller organizations, which are not required to make pay data publicly available. We, therefore, chose a ratio measure of pay dispersion to enable respondents to be more candid in their answers and to limit possible social desirability bias. Given the small size of the organizations involved in our sample, it should not be difficult for founders to recall information about maximum and minimum pay. Ratios of salaries between the highest and lowest levels of pay dispersion are frequently used for operationalizing pay dispersion (Connelly et al., 2016; Yang & Klaas, 2011). To measure the dependent variable, we asked the founders in survey Wave 2 to report the ratio of the salary of the lowest earning employee of their organization as a percentage of the highest earning executive’s salary. This measure reflects pay dispersion at the organizational level. For analysis, we inverted the variable by subtracting its values from 100. This way, high values stand for high levels of pay dispersion.

We used validated rating scales in survey Wave 1 to measure our two independent variables, self-oriented motivation and other-oriented motivation at the level of the individual founder. To measure self-oriented motivation, we used De Dreu and Nauta’s (2009) three-item measure of self-concern with a 7-point rating scale anchored at not at all and very much. A sample item is: “At work, my personal goals and aspirations are important to me.” Cronbach’s alpha coefficient for this scale is .85. Bolino and Grant (2016) argue that other-oriented motivation and prosocial motivation scales are different operationalizations of the same construct. Accordingly, we measured other-oriented motivation with the frequently used four-item prosocial motivation scale developed by Grant (2008). The 7-point scale was anchored at disagree strongly and agree strongly. A sample item is: “I want to have positive impact on others through my work.” Cronbach’s alpha for this scale is .91.

To measure the two mediating variables of our model—shareholder salience and employee salience—we used the rating scales developed by Agle and colleagues (1999) in survey Wave 1. These scales measure salience at the individual level of the decision maker. The scales consist of three items for each group, measured on a 7-point rating scale anchored at disagree strongly and agree strongly. Respondents were asked to report salience based on their recollections over the past month, so as to mitigate post-rationalization bias, as in Agle and colleagues (1999). A sample item reads: “Satisfying the claims of this group was important to our management team.” Cronbach’s alpha for shareholder salience was .92 and for employee salience .89.

Our first control variable is the founder’s own equity stake, as this can influence pay distribution choices (Wasserman, 2017). The variable was measured as the founder’s equity stake as a percentage of total equity. In addition, we used data extracted from the Orbis database to control for each organization’s size and age. Organizational size has been found to have an overall negative relationship with pay dispersion (Cobb & Stevens, 2017). We operationalized size as the log of the number of full-time employees in the organization. The age of the organization can limit the ability of founders to exercise control over their organizations’ decisions due to the emergence of bureaucratic structures (Agle et al., 1999; McKelvie et al., 2011), including decisions related to pay distribution. We measure it as years since the founding year.

Confirmatory Factor Analysis and Common Method Bias

Before computing composite indices for use in a path model, we subjected the four multi-item scales to confirmatory factor analysis (CFA). The model specification where all items load on their intended factors shows a good fit with the data (Hu & Bentler, 1999): the root mean square error of approximation (RMSEA) score of 0.048 is below the recommended threshold of 0.06 and the value for the standardized root mean square residual (SRMR) of 0.043 is clearly below the threshold of 0.08, while the comparative fit index score of 0.985 exceeds the threshold of 0.95. We compared this specification with alternative specifications, such as both salience and motivation scales loading on single factors. In each case, the specification where the items load on their intended factors shows superior fit with the data. For further evidence on discriminant validity, we compared the average variance extracted (AVE) scores with the squared correlations between the latent variables. The AVE scores range from 0.70 to 0.80, whereas the squared correlations are between .00 and .11, signaling good discriminant validity (Fornell & Larcker, 1981).

We designed the study so as to mitigate common method bias concerns (Podsakoff et al., 2003). Even though data on the main variables are derived from reports by the same founder, there was a considerable time gap between the measurement of the dependent and all other variables. Furthermore, different instruments (multi-item rating scales and a ratio measure) were used to collect the primary data. Finally, we combined primary data with archival data drawn from the Orbis database for our control variables.

Analysis Strategy

We chose path analysis as the most appropriate statistical technique. It allows testing all of our hypotheses in a single model, and it is also well suited for examining mediation effects (Williams et al., 2009). Furthermore, it is better suited for analyzing our relatively small sample of 119 observations than structural equation modeling because it requires fewer parameters to be estimated and thus maximizes the power of the model. The analysis was performed using the software package Stata 15.

Descriptive Statistics

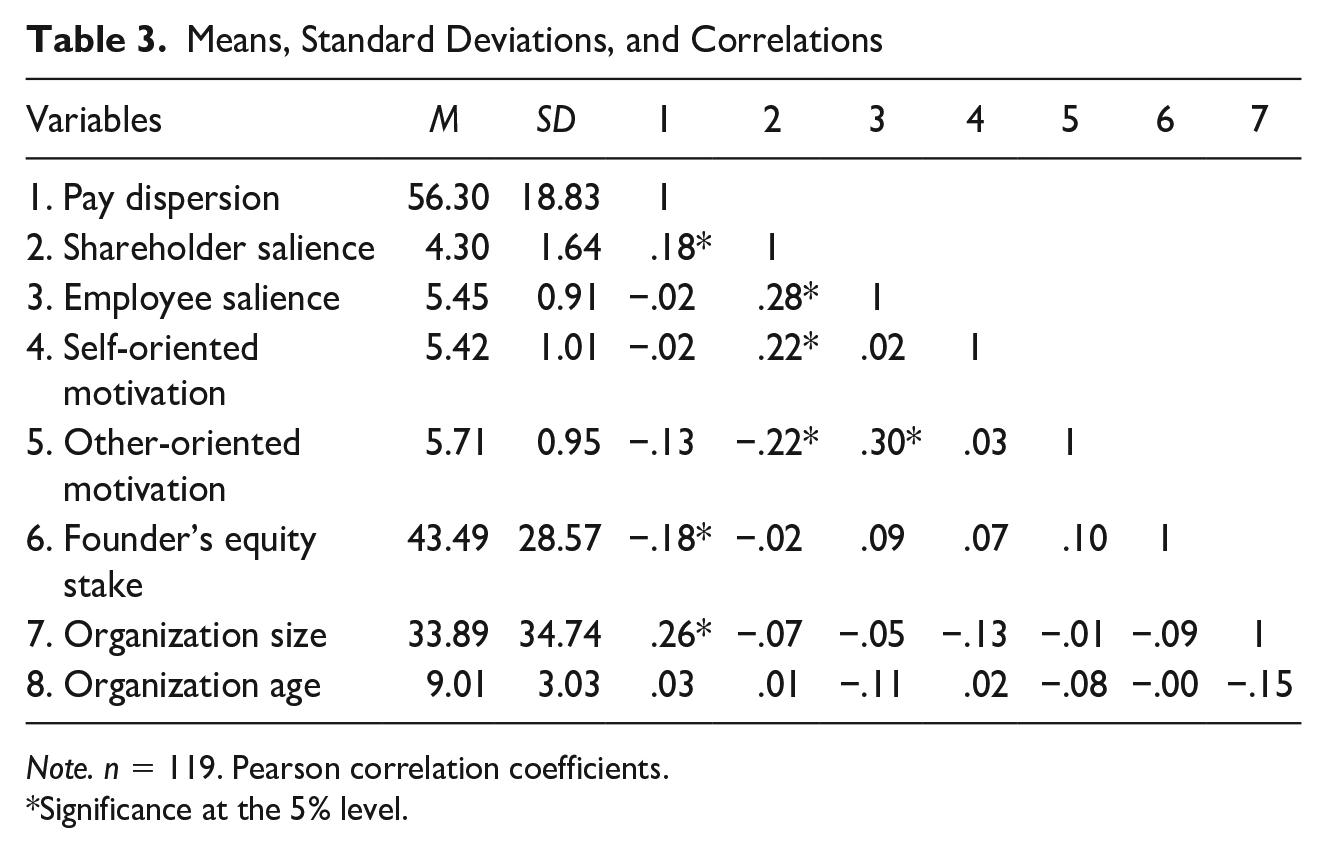

Table 3 presents the means, standard deviations, and intercorrelations of all variables included in the analysis. The correlations are moderate with the highest Pearson coefficient being .30. This suggests that multicollinearity is unlikely to be a major concern in our model.

Means, Standard Deviations, and Correlations

Note. n = 119. Pearson correlation coefficients.

Significance at the 5% level.

Results

Hypothesis Tests

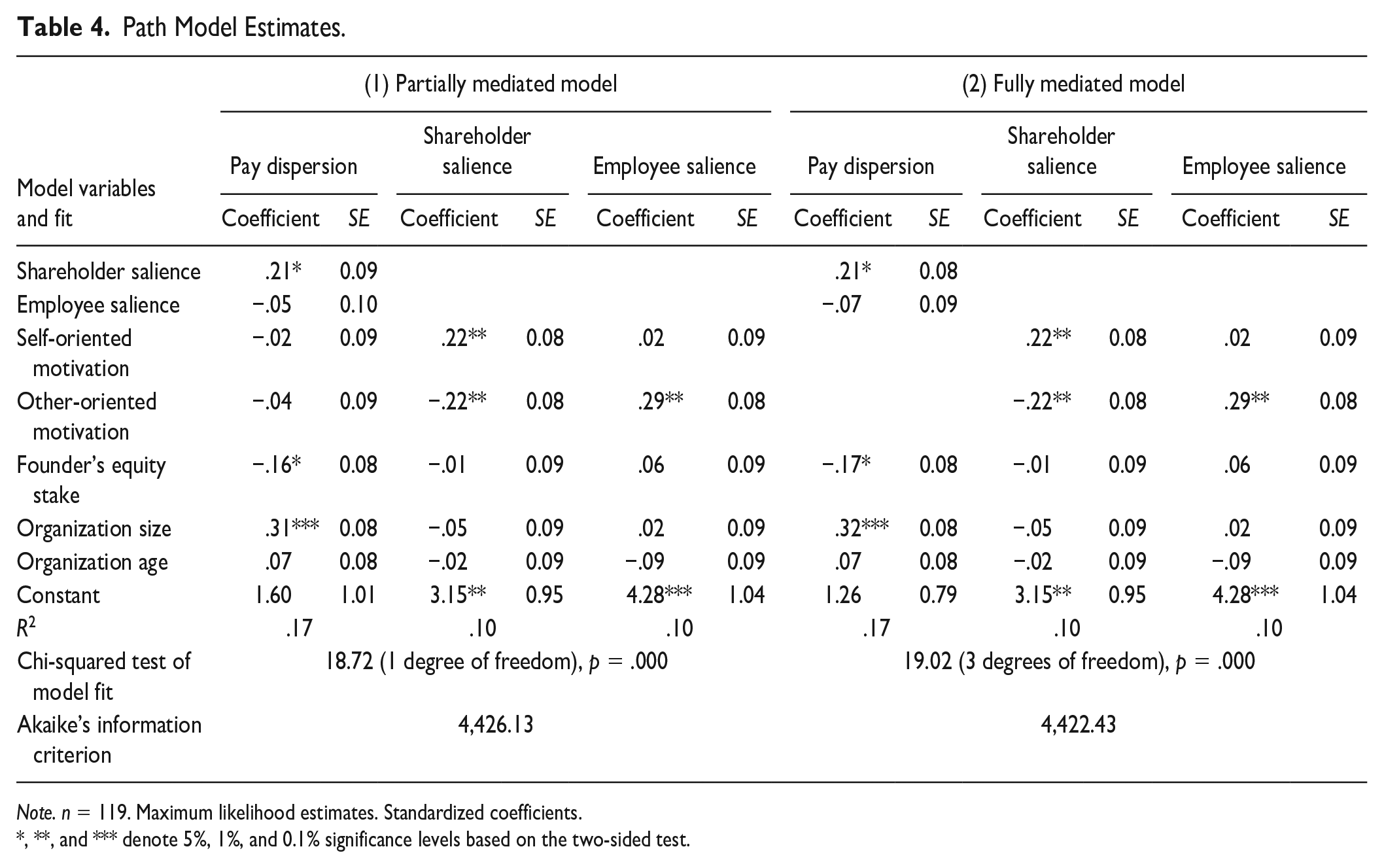

Table 4 displays the results of our path model analysis for a partially mediated model (Model 1) and a fully mediated model (Model 2). The partially mediated model includes direct paths from self- and other-oriented motivations to pay dispersion even though we hypothesize these effects to be fully mediated by shareholder and employee salience; these paths are not included in the fully mediated model. The chi-square test of model fit for the partially mediated model is 18.72 with one degree of freedom and the Akaike’s information criterion (AIC) is 4,426.13. The chi-square test score for the fully mediated model is 19.02 with three degrees of freedom and the AIC is 4,422.43. The chi-square difference test for these models is thus 0.30 with two degrees of freedom, which results in a p-value of .86. Thus, the partially and fully mediated models are not significantly different from each other. This being the case, we prefer the more parsimonious model, which is the fully mediated one. This choice is supported by the fully mediated model having more degrees of freedom and a smaller AIC score.

Path Model Estimates.

Note. n = 119. Maximum likelihood estimates. Standardized coefficients.

, **, and *** denote 5%, 1%, and 0.1% significance levels based on the two-sided test.

As such, the chi-square test score being significant indicates unsatisfactory model fit. We investigated the reason for this and found that—due to the correlation between the measures of shareholder and employee salience—there should be a path between them for the model as a whole to have a good fit. However, as our analytic interest is not in testing whether the model as a whole fits well, but instead in testing individual relationships within the model, we did not include a theoretically unfounded structural path between shareholder and employee salience. Nevertheless, we ran a robustness test with a path from employee salience to shareholder salience to see whether improving the model fit artificially (with an untheorized path) affects the analytic outcomes. The substantive results in this model were the same as in Model 2 in Table 4. Thus, we felt confident to proceed with the analysis using the specification reported in Model 2.

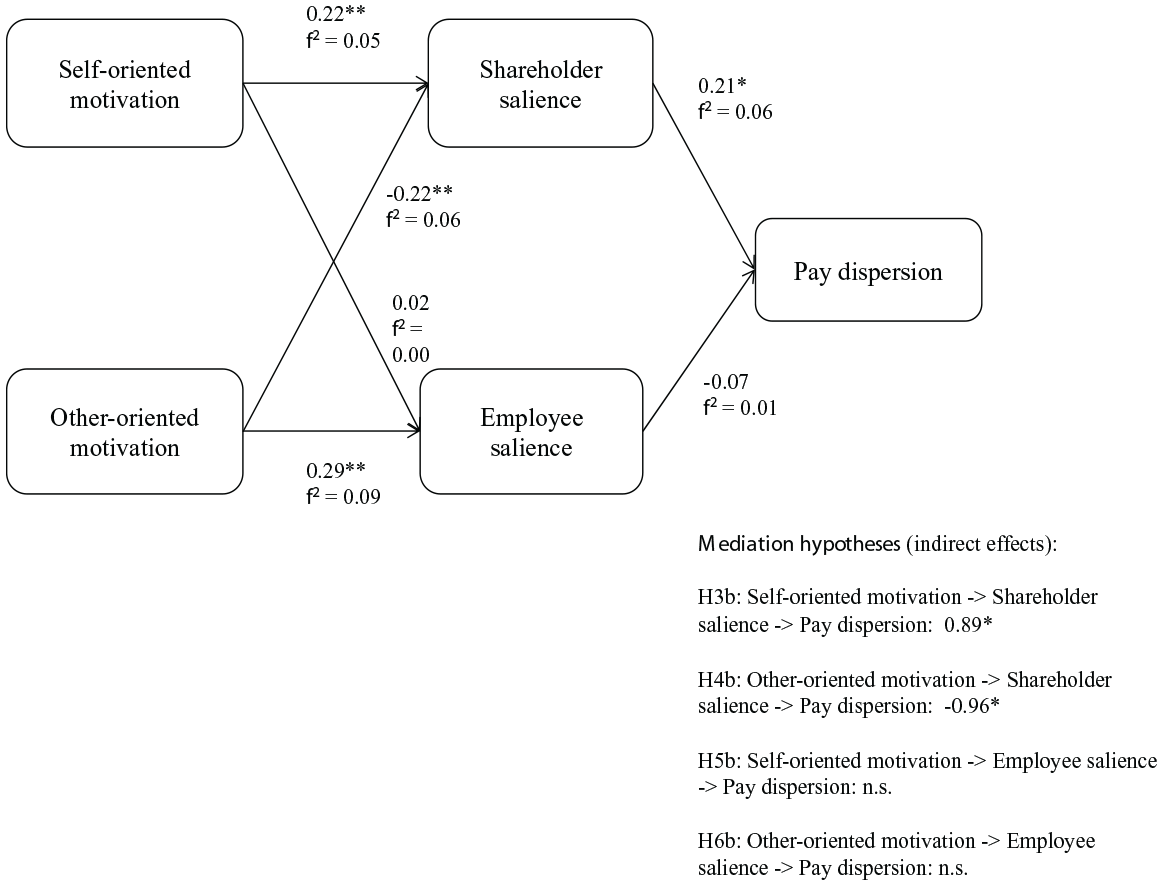

Figure 2 provides a graphical summary of the principal results in the fully mediated model (Model 2 in Table 3) and also presents Cohen’s (1988) f2 effect size measures (f2 < 0.02 indicates a weak, f2 > 0.15 moderate, and f2 > 0.35 strong effect).

Summary of Main Results.

Hypotheses 1 and 2 predicted shareholder salience to be positively and employee salience to be negatively associated with the level of pay dispersion in an organization. Shareholder salience has a positive and statistically significant (p = .012) relationship with pay dispersion. This relationship has a moderate-to-weak effect size of 0.06. The relationship between employee salience and pay dispersion is not significant (p = .441) and the effect size is also below the threshold for weak effect. Hence, we find support for Hypothesis 1 but not for Hypothesis 2.

Hypotheses H3a, H4a, H5a, and H6a outlined the expected relationships between self- and other-oriented motivations and shareholder and employee salience. The results show that a founder’s self-oriented motivation increases the salience of shareholders (H3a), while a founder’s other-oriented motivation both reduces shareholder salience (H4a) and increases employee salience (H6a). However, we did not find support for H5a, which stipulated a negative relation between a founder’s self-oriented motivation and employee salience.

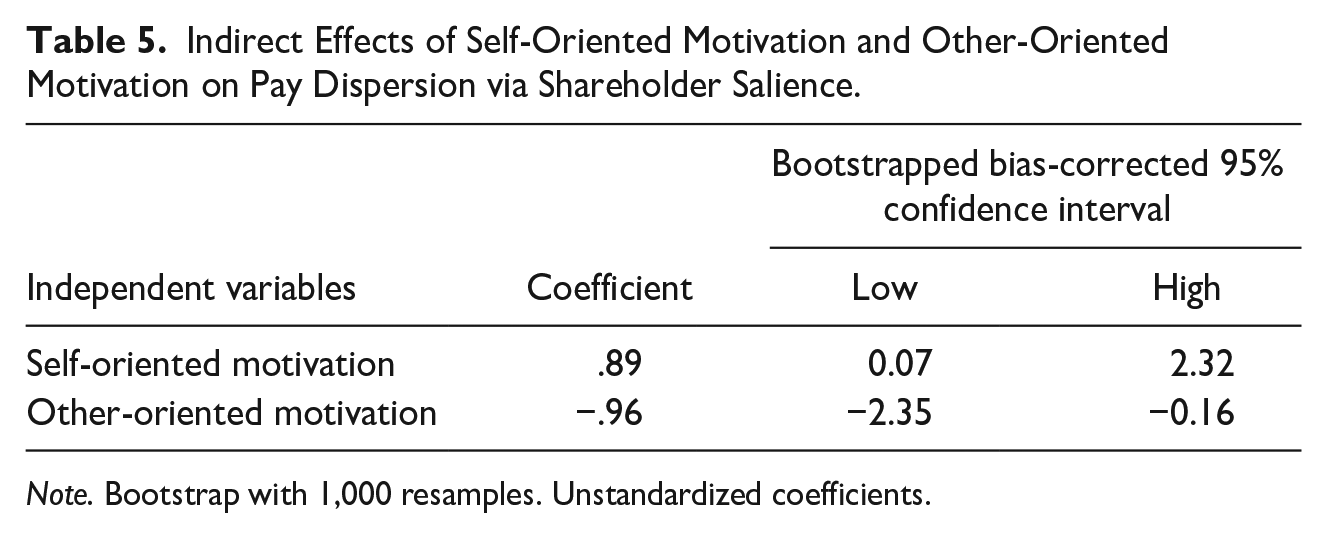

The remaining four hypotheses (H3b, H4b, H5b, H6b) proposed mediation effects, which are best tested by examining the indirect effect of the independent variable on the dependent variable via the mediator (Williams et al., 2009). Because employee salience is not significantly associated with pay dispersion, it cannot mediate the motivational effects outlined in Hypotheses 5b and 6b. Thus, we can conclude that those two hypotheses are not supported. However, Hypotheses 3b and 4b warrant further attention because not only is shareholder salience positively associated with pay dispersion, but both self- and other-oriented motivations show significant (p = .009 and p = .008, respectively) and moderate-to-weak effects on shareholder salience. Thus, the basic requirements of mediation are met.

The indirect effects required to test for mediation are reported in Table 5. In addition to the coefficient estimates, we report bias-corrected 95% confidence intervals as an appropriate test of significance for mediation hypotheses when power is a more pressing concern than Type I error (Hayes & Scharkow, 2013). For both self- and other-oriented motivation, zero is not within the range of the confidence interval, which suggests that the mediation effects are significant at the 5% level. Therefore, we conclude that shareholder salience mediates the effects of self- and other-oriented motivation on pay dispersion, as predicted in Hypotheses 3b and 4b.

Indirect Effects of Self-Oriented Motivation and Other-Oriented Motivation on Pay Dispersion via Shareholder Salience.

Note. Bootstrap with 1,000 resamples. Unstandardized coefficients.

In summary, we find support for Hypotheses 1, 3a, 3b, 4a, 4b, and 6a, while we reject Hypotheses 2, 5a, 5b, and 6b.

Post Hoc Tests

We acknowledge that pay dispersion is subject to many different influences. While we kept the main model parsimonious to enhance the statistical power of the analysis, we also ran different specifications of the model with additional control variables to rule out endogeneity caused by omitted variable bias. We started by including industry fixed effects as overall control of industry-level effects. While some of the industry effects were significant on pay dispersion, the results relating to the hypothesized relationships remained intact.

Next, we added further predictors to the model. We included up to three new variables at a time to preserve the statistical power of the model given the small sample. We started with several variables from our primary survey data: the founder’s age and gender, the number of hierarchical levels in the organization (do hierarchical organizations exhibit more pay dispersion than flat organization structures?), and an index of industry maturity (do firms in mature industries report more or less pay dispersion than firms in young industries?).

Furthermore, we used the financial statement data from Orbis to examine the effect of the cost of employees relative to operating revenue to see whether pay dispersion is different in human-capital-intensive firms. Also, we obtained industry-level pay dispersion data from Statistics Finland and used their recommended ratio of the 9th to the 1st decile of total earnings as an indicator of dispersion. We ran a multilevel specification of our model to test this variable because it only varies at the level of the 11 industries included in our sample. Finally, we explored the effects of several performance indicators (ROE, current ratio, profit margin) derived from the financial statement data in Orbis to see if well or poorly performing firms are more likely to have large salary differentials.

The conclusion of these tests is that none of the additional control variables has a significant effect (p < .10) on our dependent variable. Also, their inclusion in the model does not change the outcomes of the hypothesis tests.

Discussion

As organizational pay dispersion and its antecedents are becoming a phenomenon that captures increasing societal and academic attention as well as concern (Bapuji et al., 2018, 2020) calls to expand our understanding of the micro-level factors that contribute to it are multiplying (Beal & Astakhova, 2017; Bidwell et al., 2013; Cobb & Stevens, 2017). To this end, in this study we focus on the role of founders’ self- and other-oriented motivations as well as shareholder and employee salience perceptions as antecedents of pay dispersion in their organizations. As theorized, we find that self-oriented motivation positively influences pay dispersion at the organizational level through the higher salience of shareholders to founders. Correspondingly, we find that other-oriented motivation results in a lower salience of shareholders to founders and in turn in reduced pay dispersion at the organizational level. In contrast, our predictions that the level of salience of employees to founders is influenced by founders’ motivations, and, in turn, influences pay dispersion did not receive empirical support. Other-oriented motivation was found to increase the salience of employees, yet this increased salience failed to translate into reduced pay dispersion. This finding could imply that, in practice, for founders, employee salience is overshadowed by shareholder salience in pay dispersion decisions. This could potentially be attributed to founders’ financial and emotional goals that are strongly tied to the organization and its growth and financial performance (Arthurs & Busenitz, 2003; D. Miller et al., 2007). This identification could make founders more aligned with shareholders’ interests and thus form their perceptions of events and situations so that they consider the consequences of their decisions primarily starting from such alignment. This speculation could be further examined in future research.

The lack of empirical support for the mediating role of employee salience in the relationship between founders’ motivations and pay dispersion also offers an opportunity to reflect on employee power within organizations. While employee power could be underrepresented in young organizations, the situation can change as companies expand. A growing number of employees could translate into growing employee power, and thus salience. However, organizations that increase in size also increase their internal formal processes that make the relationship between founders’ characteristics and organizational outcomes more distant and complex. Future research could investigate the dynamism of the relationship between founders’ decision-making and pay dispersion as organizations age and grow.

Theoretical Implications

Taken together, our findings hold theoretical promise vis-à-vis several literature streams. First, our study informs work on pay dispersion conducted within the realm of organizational behavior studies. An extensive and sophisticated body of work has accumulated that finely nuances the consequences of organizational pay dispersion (for reviews, see Conroy et al., 2014; Shaw, 2014). This body of work has concluded that pay dispersion cannot be treated as conclusively positive or negative per se and has added granularity to our understanding of the conditions under which pay dispersion results in valued organizational outcomes (Amore & Failla, 2020; Li et al., 2021; Shaw, 2014). Yet, scholars increasingly acknowledge that pay dispersion can also have negative societal implications that are important in their own right and are calling for the direct examination of the antecedents and mechanisms that underpin pay distribution decisions (Bapuji et al., 2020; Cobb, 2016; Tsui et al., 2018). Our study is a step in that direction, contributing to a better understanding of pay dispersion, which, we find, is partly determined by founders themselves. Accordingly, our study establishes the founder as a consequential figure and unit of analysis in studies and discussions of pay dispersion. It suggests that soft, micro-level attributes, such as shareholder orientation, and self- and other-oriented motivations, have sufficient gravity to justify their examination in related work in the future.

Second, we identify stakeholder salience as a critical mediator that connects individual- and organizational-level constructs of interest. A long literature has treated stakeholder salience and other stakeholder-related considerations as consequential for corporate action related to social responsibility activities (Agle et al., 1999; Eesley & Lenox, 2006; Galbreath, 2010; Tang & Tang, 2018). We extend this work by showing that pay dispersion, an outcome that also carries social responsibility implications, is similarly affected by the heterogeneous strength of shareholder salience. Our findings suggest that discussions of the perception of salience need to also incorporate organizational leaders’ characteristics, such as their personal motivations, thereby answering calls by the original proponents of the stakeholder salience framework (Mitchell et al., 1997) and stakeholder theorists more broadly (Berman et al., 1999). Relatedly, our study points to the possibly productive cross-fertilization between stakeholder theory and the motivated information processing perspective for the future study of organizational phenomena more generally. So far, this stream of work within social psychology has been employed mostly in experimental settings and in relation to individual decisions of resource allocation between two persons (De Dreu & Nauta, 2009; Liebrand et al., 1986; Van Dijk & De Dreu, 2021). Yet, its theoretical claims closely mirror preoccupations of stakeholder theory, such as those related to the subjective formation of perceptions of power, urgency, and moral legitimacy of claims in the stakeholder salience framework. With this study, we attempt to more explicitly connect these two theoretical perspectives, a task that can inform future conceptualizations of pay dispersion as well as other corporate responsibility-related outcomes.

Practical Implications

Current debates in industry, policy, academia, and public discourse attest to the practical importance of understanding the antecedents of pay dispersion. Yet it is difficult to provide definitive solutions to rectifying pay dispersion that is unexplained by productivity differentials, as research on its micro-level antecedents is still nascent. The emerging regulatory demands for pay transparency, whereby organizational leaders are required to justify pay dispersion by means of economic rationality, or asked to publicize salary data, have created a wave of concern among organizations and spurred the emergence of specialized consulting companies that promise to help them remedy growing pay dispersion (Barnard-Bahn, 2020; Goldberg, 2021). One realization from these increasing efforts is that reducing pay dispersion is hard even when having good intentions, as the story of Buffer (in the opening of this article) suggests.

Another realization is that a considerable part of pay dispersion is attributable to unconscious biases of human beings—leaders and employees alike (Goldberg, 2021). Our study highlights that in the case of founders, their self- and other-oriented motivations and the salience of employees and shareholders to them can be important sources of unexplained pay dispersion. This finding is particularly relevant in light of the greater leeway that founders have in exerting influence on their organizations’ direction (McKelvie et al., 2011), also over the long-term (Beckman, 2006; Beckman & Burton, 2008), and of the substantial contribution that young organizations have on economic wealth and job creation (Audretsch et al., 2006; Baumol, 1996). Namely, setting an organization on a path of low pay dispersion early on should be much easier and more consequential than rectifying pay dispersion in a large and established organization. This suggests that founders themselves have a unique opportunity to consider and influence pay dispersion in their organizations. While few organizational leaders consciously think about their self- versus other-orientations, or their shareholder orientation, the scales measuring these constructs are rigorously tested and readily accessible. As such, consulting companies specializing in pay dispersion, as well as founders themselves, could easily use these scales to determine possible biases and compare them to the levels and direction of pay dispersion within an organization. While self- and other-oriented motivations are hard to drastically change, reflexivity has been found to improve cooperative outcomes (De Dreu, 2007), and shareholder orientation should be amenable to manipulation when there is awareness of it. Furthermore, depending on whether their personal motivations and shareholder orientation are conducive or not to pay dispersion, founders could decide whether to get actively involved in pay decisions, or, alternatively, to defer such authority exclusively to HR professionals, even early on.

At the societal level, both civil society and policymakers can intervene to influence the legitimacy of shareholders’ claims and thus alter founders’ perception of shareholder salience that in turn influences pay dispersion. For example, social movements could increase media attention to income inequality and shape public discourse (Gaby & Caren, 2016), thus pressuring founders to re-evaluate the salience of shareholders’ claims against societal concerns. Policymakers’ initiatives could also contribute to a reduction in the salience of shareholders. For example, they could offer clear governmental support to the discourse against income inequality and keep this stance in their interactions with new organizations and the business community. Policymakers could also put together programs that aim to stimulate or reward founders’ other-oriented behavior. For example, they could focus or extend their salary transparency demands to young organizations, or reward founders that exhibit behavior that is indicative of other-oriented motivations, given our finding that founders have a significant influence on their organizations’ pay dispersion levels.

In sum, our research suggests that founders should be aware that self- and other-motivations and salience of shareholders can bias them toward different levels of pay dispersion in their organizations; if pay dispersion becomes a problem, founders could try to temper the attention they place on shareholders or take other actions that could counter-balance their personal biases. In turn, third parties such as policymakers, and consulting firms, can use our findings alongside research on other biases affecting pay dispersion (e.g., gender, ethnic), to better understand the phenomenon and decide where and how to target relevant interventions and discourse.

Limitations and Future Research

This study is not without limitations. First, our sample is relatively small and consists mostly of male participants (reflecting the skewed gender distribution among founders). Second, the Finnish context is characterized by a high level of employee protection based on provisions in the labor law and a relatively high level of trade union membership (59.4% in 2017) (Ahtiainen, 2019). These factors might have influenced our ability to detect effects of employee salience on organizational pay dispersion, as in a context of high protections and overall low pay dispersion external factors might overshadow this relationship. Nevertheless, as Tsui and colleagues (2018, p. 165) suggest, “social and institutional norms at the society level may explain country differences but cannot explain the variance across companies within a country.” Relatedly, our single-context design controls for country level effects, providing confidence in the supported hypotheses. Third, while we examine self- and other-oriented motivations and control for certain situational factors, additional variables could be relevant for organizational pay dispersion. One such factor, political ideology, is attracting increasing attention in terms of its effects on top management team pay dispersion (Chin & Semadeni, 2017) and could be possibly relevant to organizational pay dispersion.

Future studies could address these limitations by examining the interactions between self- and other-oriented motivations, gender, and political ideology, in relation to their effects on organizational pay dispersion, and by replicating our study across countries, in relation to a greater number of stakeholder groups, to clarify the boundary conditions of our findings. We hope that our study as well as cumulative future work spur further interest on the micro-processes underlying pay dispersion, a phenomenon of critical importance for organizations and societies at large.

Footnotes

Acknowledgements

We would like to thank Business & Society Editor Christian Voegtlin and the three anonymous reviewers for their very useful comments and suggestions throughout the review process.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We want to acknowledge Aalto University’s HSE Foundation, the Jenny and Antti Wihuri Foundation, Liikesivistysrahaston (LSR) Foundation, and the Society for the Advancement of Management (SAMS) for kindly supporting this study.