Abstract

Although populism is an ideologically fluid political vehicle, it is not one that is intrinsically anti-business. Indeed, different varieties of populist parties may encourage business activity for utilitarian ends, but with their own ideas on what businesses should be doing. This reality implies that initiatives not related to national greatness or priorities as defined by the populist leadership may be viewed as redundant. Key among such initiatives would be corporate social responsibility (CSR). In a populist environment, it is possible that firms may divert resources away from broad-based CSR under pressure from populist governments. This article explores the relationship between populist governance and CSR with an econometric examination of over a thousand firms in 13 countries under both pro- and anti-business populist governments at varying times from 2012 to 2020. Using dynamic panel data methods, we find strong evidence that firms substitute away significantly from CSR under populism. This effect grows significantly larger under anti-business populists.

Populism is once again a potent political force. In its simplest form, populism is an ideational concept, separating the world into “us” and “them,” with a pure “people” against a corrupt “elite” (Bennett et al., 2022, using the definition as given by Mudde & Rovira Kaltwasser, 2018). Its uncanny ability to persist as a rhetorical device along these lines, often co-opted by mainstream parties, means that its appeal never really goes away (Hicks, 1931). However, beyond its allure as rallying cry, it is also a way to organize politically, and it is undeniable that populist electoral successes, key to operationalizing populist ideas, have been increasing over the past two decades (Caiani, 2019; Heydarian, 2020; Spicer, 2018). Moreover, populism has expanded its reach into both developed and developing economies, given fertile ground to grow by a succession of financial and economic crises. It has also shown resilience in being able to successfully adapt to local conditions. Instead of a uniform, Latin American–style populism of the 1950s, the world has seen the mutation of the populist virus into a variety of populisms (Devinney & Hartwell, 2020), each one tailored to the local context while gaining strength and knowledge from the variety of contexts in which it has been operating. At the same time, populist parties, having attained power, have concentrated their efforts in retaining it (Chesterley & Roberti, 2018; Hartwell & Devinney, 2021).

This expansion of populist varieties has further challenged our understanding of what populism actually is, as the literature reveals that “populism” is a notoriously difficult concept to grasp. Famously investigated as a “thin ideology” by Stanley (2008), populist parties globally have adopted common approaches to political organizing (relying on a charismatic—or at least vocal—leader), common themes (a virtuous “us” of the people versus a malefic “them” in existing elites), and common policy prescriptions (higher spending and less attention to macroeconomic stability; see Dornbusch & Edwards, 1990). However, while the overall approaches and themes of populism have been consistent across countries, populist attitudes to the private sector have been wildly divergent across its varieties. In the first instance, a populist party’s location on the continuum from left-wing to right-wing, focusing more on redistribution or national greatness, often colors its attitudes toward business. But even these labels sometimes fail to capture the diversity of populisms, which can range from staunchly pro-business but somewhat paradoxically anti-globalization (as in the United States under Donald Trump [Butzbach et al., 2020; Cha, 2016] or in Thailand [Phongpaichit & Baker, 2005]) to anti-business but with an activist, globalist outlook (as in Venezuela or Turkey [Demiryol, 2020]).

In spite of these various mutations, and despite the fact that some populism may be overtly pro-business, populism, in general, generates uncertainty (de Sousa et al., 2021; Hartwell & Devinney, 2021) while at the same time deliberately creating institutional volatility (Hartwell, 2018) in an attempt to change the “rules of the game.” A variety of research has explored the channels by which populism may affect firms, including the effects of protectionism and its disruption of supply chains (Free & Hecimovic, 2021), the ramifications of anti-immigration policies on human resource management in multinational companies (MNCs; Cumming et al., 2020), issues with financing and financial volatility (Stöckl & Rode, 2021), and even overt effects on strategic positioning within the home country (Mbalyohere & Lawton, 2021; Ozawa, 2019). For the most part, the influence of populism is negative overall, although this effect may be evanescent as firms adapt, or, alternatively, the specific effects are highly context-dependent (de Sousa et al., 2021; Hartwell, 2021).

These obvious effects of political risk may be complemented by more subtle, harder-to-discern channels of influence, as firms learn how to deal strategically with an inherently intrusive and active government—one with its own ideas on what a firm should be doing under a populist regime. While some firms may rely on corporate political activity (CPA; Hillman et al., 2004; Lawton et al., 2013; De Villa et al., 2019) to mitigate political risk, these activities may take a long time to work with insulated populist leaders and some populist parties—especially of an actively anti-business bent—may look unkindly on such overt strategies. For smaller firms or those without the ability to generate political connections, firms may instead adopt a number of coping mechanisms (Feldmann & Morgan, 2021), which could include a reorientation of processes away from populist unfriendly or “peripheral” activities.

Paramount among these activities could be corporate social responsibility (CSR). CSR, as is well known, is a strategic orientation that focuses on satisfying broader societal needs as perceived by the company, including environmental protection, community engagement, working conditions and labor relations, and generating public goods (Sheehy, 2015). However, CSR activities are both determined internally by the firm (in terms of its extent of engagement and in what areas) and externally by existing institutional structures (that is, need for CSR comes about because of the manner in which society is already organized). Both of these attributes may, in some way, threaten a populist regime, which has specific expectations of the role of business in society and the way in which society should be ordered (Otjes et al., 2018). This is a specific function of the nature of populism: Whereas CSR is a function of “stakeholder capitalism,” with various stakeholders beyond the business invested in the social aspects of commerce (Carroll, 2021), populism instead demands only one stakeholder, the people, whose interests are represented by the populist regime. While S. Roth and colleagues (2020) may have called for CSR to go beyond economy and society, populism would ensure that CSR would not go beyond politics.

This article conjectures that populism of all stripes could, thus, be bad for CSR, especially if one conceives of CSR in its pure form of developing “social responsibility,” as populists demand firms reorient toward populist-friendly, politically motivated initiatives. This does not mean that CSR as a business activity would grind to a halt, as there are many instances of CSR being utilized as a political activity to insulate a firm from government predation (Blake et al., 2022; Markus, 2012)—indeed, defensive CSR might actually increase as a result of populism. Blake and colleagues (2022) show that particular configurations of CSR, predicated on building the legitimacy of the government and/or targeting specific constituencies of populists, can act as an effective nonmarket strategy to lessen risk. However, we conjecture (and in line with their theory) that broad-based CSR initiatives, ones which did not necessarily generate immediate goodwill or sympathetic stakeholders within the populist governance structure, would likely see a decrease as a result of populist electoral victories. The reason behind this is that the existence of firm-directed CSR implies societal interests outside of the purview of the populist government. This runs directly counter to populist rhetoric, championing the people, and thus firms would be discouraged from such initiatives lest they clash with political ideas of what is good for the people.

These effects and their direction may be conditioned by the variety of populism that has taken root within a country, another point that distinguishes our work from Blake and colleagues (2022) and extends it. For example, under a pro-business, national greatness-style populism, CSR might be seen as tangential to business functioning, as the business of firms would be to generate profits and employment rather than engage in peripheral activities (Maier, 2021). Paradoxically, under an anti-business populism, with redistribution as the order of the day, CSR may be even more threatened, as small, token policies such as CSR will be seen as wholly inadequate (an attempt at “greenwashing”). Indeed, the “societal co-regulation” (Steurer, 2010), which CSR uses as a basis, would be removed by an anti-business populist, and replaced with singular and all-encompassing regulation, coming from the regime and the regime alone. On the contrary, the left-wing orientation of most anti-business populists could also mean that some aspects of CSR are made mandatory, as a way to both achieve policy outcomes and ensure that firms (and business elites) do not stray from the preferred direction of the populists; under such a scenario, CSR may actually increase, but, again, in a way that is tied to (and serves) the populists in power.

Due to the many possible ways in which the many varieties of populism could affect CSR across firms in a country, this article fashions an empirical exercise to explore these multiple possible explanations to see which is supported by the evidence. Amassing a database of 1,434 firms across 13 small- and medium-sized countries that have experienced populism over a 10-year period, and using dynamic panel modeling, our results show that firms operating under populist leadership decisively shift away from aggregated CSR activities. Delving deeper into these effects, we find that the lowering of aggregate CSR activities is especially pronounced in countries that have an anti-business populist regime. Although we cannot say definitively where the resources that firms are withdrawing from CSR are going (an ongoing research question), the reality appears to be that populism in general reduces a firm’s willingness or ability to engage in CSR initiatives overall.

Populism, Its Varieties, and Their Impact on Business

The political science literature (Mudde, 2004; Mudde & Rovira Kaltwasser, 2018) has invested a lot of time and energy in defining just what populism is, calling it a “thin ideology” (Stanley, 2008) and noting that populism can be used as a catch-all label (Collier, 2001). A consensus has been fashioned through rigorous study, however, that populism is characterized by two main facets (Deiwiks, 2009): (a) a rhetorical focus on an ill-defined but all encompassing “people” and (b) opposition to an “elite,” who are often taken to be the diametrical opposite of “the people.” While the “us versus them” rhetoric is prominent in many strands of politics, and especially in left-wing rhetoric (Beldarrain-Durandegui, 2012), populism instead posits the political arena as an existential struggle of the virtuous versus the wicked. In such an arena, compromise is rarely sought after, and, instead, institutional capture is needed to remove “entrenched” or “structural” attributes that tilt the playing field against “the people.”

Populism also has distinct organizational and policy aspects, a fact which should dissuade researchers from focusing solely on its rhetorical flourishes. From the organizational side, populism almost uniformly focuses on building cross-class coalitions for rapid and sometimes radical political change (Rode & Revuelta, 2015). This mobilization generally means bringing marginalized and/or apolitical constituencies together to create new voters, who then elevate populist parties to power to work against the system. Holding the populist party together is normally a charismatic (or at least image savvy) leader, the face of the people who brings the populist message to the masses (Mudde, 2004) and often is the direct channel of influence for populist ideology (more so than the organizational form of the party). Despite disagreement among authors on how this “charisma” should be measured (see especially Van der Brug & Mughan, 2007), there is ample evidence that leadership matters, especially when in reference to the electoral chances of a populist party (Pappas, 2016), again perhaps the only way in which a populist movement can influence the direction of a nation. Finally, from the policy side, and more concerned with governance than getting elected, populism also holds an almost entirely redistributive (left-wing) set of macroeconomic policies (Stankov, 2018), using the power of government to rectify the actual and perceived injustices done to the people. Although recent variants of populism have been more situated on the right wing of the political spectrum, these parties (such as Orbàn in Hungary or Kaczynski in Poland) are not above using the power of the state to meddle in the market, especially if this can further the political goals of social conservatism or national greatness.

Beyond these commonalities, the past 20 years have shown a divergence among several varieties of populism, including with regard to their location on the political spectrum, the countries in which they thrive, their particular style of governance, the political system from which they arise, and, most importantly, in the priorities of various populist leaders. This reality is compounded by the existence of issues that do not sit easily on the left-wing/right-wing axis, such as trade policy—meaning that much of the populism observed globally in recent years also fails to adhere to such a neat formulation related to political ideology (despite the tendency to do so in the popular press). Indeed, the one consistent recent trend across populist regimes has been related to anti-globalization, first and foremost (K. E. Meyer & Li, 2022). This priority has been evidenced in populist leaders from right-wing demagogues such as Donald Trump, riding to power on a wave of protectionist and anti-trade sentiment, to left-wing stalwarts such as Jacinda Ardern in New Zealand, who only became Prime Minister by courting the xenophobic and anti-immigrant “New Zealand First” party of her (future) Deputy Prime Minister Winston Peters (C. Johnson et al., 2005). Moreover, this emphasis on anti-globalization has not been limited to democracies, with “authoritarian populism” also a defining feature of the former Soviet Union (Busygina, 2019; Eke & Kuzio, 2000), including Putin’s Russia (Burrett, 2020; Lassila, 2016; Robinson & Milne, 2017), and present even in the world’s largest autocracy, Communist China (Devinney & Hartwell, 2020; H. Li, 2021). Populists need not be authoritarians, and authoritarians need not be populists, but in practice there is much overlap between the two in methods, if not in message.

However, even the broader anti-globalization trend has been splintered by different emphases on either the flow of goods (Trumpian protectionism), the flow of capital (Brexit and many strands of left-wing populism in Latin America), or the flow of people (anti-immigrant campaigns such as in New Zealand and Poland)—or, in some instances, all three. The reason for this is that, for all policies but for populism especially, context matters, as the priorities of populist parties and, in particular, of their leaders are almost wholly endogenous. That is, they are reactive to the previous policies put in place by the political elite, meaning that the precise make-up of populism is dependent on these previous policies: One cannot spew fiery invectives against mass immigration if the previous mainstream parties actually pursued a fairly restrictive approach to a country’s borders. This reactive stance also means that traditional formulations of left versus right wing mean less when applied to a populist lens, as a traditionally right-wing party, concerned with social conservatism, may become much more like a left-wing party in its reaction to existing elites (and vice versa). In this sense, populist policies are instrumental and not necessarily bound by any rigid ideology; in the words of Pelinka (2013), “populism was (and still is) an instrument open to anybody, any politician, any political party” (p. 9)

The clearest manifestation of populist divergence is thus not along the left-/right-wing axis but in an anti- or pro-business orientation. One may make the argument that this is, in a sense, an imperfect proxy for left versus right wing, as left-wing parties tend to be more anti-business than right-wing ones. On the contrary, one may also make the argument that populism itself is a proxy for left-wing anti-business policies, as, historically, populism has been rooted in left-wing economics, unrelentingly anti-business, and unconcerned with macroeconomic stability (Dornbusch & Edwards, 1990). This variant of populism has persisted to the present day in many forms, with Venezuela as an extreme example: Originally a populist movement led by Hugo Chavez, “Chavismo relie[d] on charismatic linkages between voters and politicians, a relationship largely unmediated by any institutionalised party” (Hawkins, 2003, p. 1137). It was only after Chavez ascended to power that the ideological framework of socialism was erected to support the populist edifice, and even then, governance in Venezuela has seen a mix of populist discourse and policies targeting previous elites and especially foreign investment (Hawkins, 2009).

But populism need not only be extremely anti-business, and it may be better to think of anti-business populism as a continuum from Venezuela at one end and a milder distrust of business or even seeing business as an opportunity at the other. An example of such “distrustful” populism can be seen in the late 1800s and early 1900s in the United States, where President Theodore Roosevelt championed anti-trust legislation and an “emphasis upon the need of governmental regulation of industrial tendencies in the interest of the common man” (Turner, 1920, p. 28). Although these reforms increased the power of the federal government over business, with Roosevelt granting himself sweeping executive authority to influence commerce (and obtaining similarly high levels of discretion to go after specific firms), the overall purpose of these reforms was to strip out the “evil” in corporate combinations rather than to weaken business altogether (A. M. Johnson, 1959).

The continuum of varieties of populism need not stop merely at mildly anti-business populism, however, and, in fact, various populisms may actually be pro-business. Weffort (1966) described populism as a precarious alliance among elements in society that may be normally opposed but are brought together because of intra-elite conflict; in this conception, business may support and be supported by populist leaders, providing legitimacy to the populists, as the populists mediate this class conflict (Barros & Wanderely, 2020). Thus, populists could support business as a key member of their electoral coalition, undermining other established organizations but also generating pro-business policies as a reward. Indeed, while macro-level populist policies may have foundations that are anathema to business, including generating uncertainty and focusing more on left-wing redistributionist policies, the policies pursued at the micro level may be entirely differently framed in terms of their attitude to commerce. Alongside this pro-business attitude would be an element of responsibility for business, as, going beyond the usual right-wing emphasis on economic growth, populists may elevate the economy to a mythic stature, with business tasked with (to use a few populist slogans) “making America great again,” “building back better,” or “achieving the goals and tasks of the great rejuvenation of the Chinese nation.”

In terms of policies that have a pro-business orientation, from a utilitarian point of view, savvy populist regimes are aware that some parts of a country’s private sector are necessary for achieving populist visions. In particular, there is a need for capital to finance works programs or government spending, which then leads to a more laissez-faire approach to the financial sector (Hartwell, 2021). Similarly, under a populist government with an emphasis on “national greatness,” the need for reinvigorating industry and generating jobs may take precedence, with political leaders tolerating or actively encouraging commerce as a means toward national renewal (Chandra & Walton, 2020; Yoshida, 2020). 1 In such a scenario, high-profile sectors such as IT or other advanced service sectors might be seen as a way to “upgrade” an economy and restore national pride, and thus motivated industrial policy, replete with subsidies and government support (as with Putin in Russia and Morawiecki in Poland), could be undertaken to support domestic business (Aiginger & Rodrik, 2020). But even in a populist regime that has embraced anti-globalization, the imperative to “save” domestic industries may be the impetus behind protectionist and anti-globalization policies (Zaslove, 2008), with policymakers attempting to “build a wall” against foreign competition and/or workers (Franzese, 2019).

A final point about the continuum of anti-/pro-business leanings in populism relates to just who exactly the populists actually are, either in their party organization or, more likely, in their personification in a particular leader (another point that distinguishes populism from pure authoritarianism). Although populism more generally claims to speak for “the people,” there is no guarantee that populist policies derive from marginalized and under-represented communities. Indeed, much like the intelligentsia leading the workers in communism, a recent trend in populism has been the prevalence of populist leaders who are elites or oligarchs (one only need think of Silvio Berlusconi in Italy, a billionaire media mogul, or Donald Trump in the United States, as key examples). This phenomenon, named “populist plutocracy” (Lee, 2019; Pierson, 2017), means that these brands of populism are likely going to emphasize supporting domestic businesses (Ruzza & Fella, 2011) and growing the economy as a way to help supporters.

This does not mean that the support of business under populist plutocrats would necessarily be universal; indeed, it has been observed that the “pro-business” policy pursued might simply be pro- the populist’s own business, see work done by Fella and Ruzza (2013) and Doctor (2019). At the same time, countries already disposed to clientelism may see much more targeted favoritism under populism (Lee, 2019); along these lines, sectors where there is little organized opposition and where populist policies may help with electoral success, may also be easy targets for populist policies (as happened in Turkey with the pharmaceutical sector, see Dorlach, 2016). One may then think of “pro-business” as also being context-dependent, influenced by the personalities and people involved (Devinney & Hartwell, 2020), and, most importantly, also represented by a continuum rather than corner solutions.

Taking this all together, it is clear to see that populism places itself in opposition to existing elites and, importantly, existing policies, with recent strains of populism focused on anti-globalization in various forms. Within the anti-elite, anti-globalization populism of recent years, there also exists varying attitudes toward business, separate and distinct from the overarching anti-globalization theme: one can be anti-globalization because they are a staunch supporter of local business, or they can be anti-business across the spectrum. It is this nuanced conception of populism, beyond the simple left-/right-wing dichotomy, which will inform our analysis going forward.

CSR and Its Value in Different Contexts

CSR: A Public or Private Good? Or Neither?

Just as in the case of populism, CSR has a wide variety of definitions (Sheehy, 2015). This is conflated with a growing belief among scholars that CSR is a bit passé, as it fails to encompass broad environmental, social, and governance (ESG) responsibilities of the corporation (Porter & Kramer, 2011). In addition, those that promote variants of the “business case for CSR” (see Crane et al., 2014, for a criticism of the “shared value” logic) try to argue that doing good can lead to doing well (Fatemi et al., 2018; Yoon et al., 2018). This approach implies that firms are not making social versus economic trade-offs and, hence, CSR is little more than another, potentially profitable, facet of business to be exploited (see Devinney, 2009, for a discussion of “doing evil by doing good”).

From our perspective, both narrow and broad definitions of CSR are effective to understand the operations of a firm. In the narrower definition, CSR represents the corporation providing social benefits to society without recourse to their being profitable (Schwartz & Saiia, 2012). In the broader definition, CSR reflects a complex mixture of activities that generate greater profitability (or risk-adjusted return on investment), some of which can involve social activities and investments (Frynas & Stephens, 2015) that, alone, may not appear logical but make sense over the longer term or as a portfolio of investments (perhaps jointly with other firms).

The benefits of these investments may also not appear clearly on the balance sheet and income statement, for example, such as if CSR helps a firm to curry favor with a national government, by demonstrating social responsibility and/or directing investments into favored communities, projects, or areas. This idea of CSR investment as a political tool for both firms and governments has been common for many years (Fooks et al., 2013; Lock & Seele, 2018)—sometimes appearing directly as a firm investment in a specific area and at other times as a philanthropic contribution by an owner or an owner’s private foundation. For example, much is made today of Russian oligarchs and Chinese firms contributing to arts organizations or universities in foreign countries as a way of currying influence via political and social elites (Milam, 2013). From the point of view of government, sometimes CSR is demanded, as in the case of foreign direct investment (FDI) in China in the 1980s and 1990s, which almost invariably involved companies investing in training programs, local schools, and other infrastructure as a quid pro quo for approval. 2 This use of CSR as a lever by government also has been present in Russia, where the Kremlin hijacked CSR for its own gain beginning in the 2000s, making CSR an inherently political activity; rather than a way for firms to curry favor, compliance with government-decided CSR became mandatory, and woe to the firm that did not follow its “business responsibility” (Zueva & Fairbrass, 2021). 3

However, the use of CSR as a political tool from the firm side has been connected with regimes with weaker institutional structures, and where softer, more elite social networks tended to substitute for formal institutions (Adelopo et al., 2015). This invariably involved generating political and social influence that potentially involved both overt CPA and CSR (Zhao, 2012). Such an approach in other environments, especially where formal institutions are strong or where elite networks are insular, would have less of a chance for success or would require substantial investment over time to pay off (Decker, 2011). But where access to the political elite is more difficult or where local business is highly connected to political elites (Wiig & Kolstad, 2010), the adoption of CSR as a tool of influence will likely fail as it comes up against countervailing domestic pressures. And while CSR may mitigate against political risk by creating goodwill in a strong institutional environment (Chatjuthamard et al., 2020), CSR with the goal of political influence may run up against the reality that nongovernmental organizations (NGOs) are more prevalent in policymaking in developed economies, acting as a check against CSR being utilized merely to ingratiate a firm with the government (Doh & Guay, 2006; Rotter et al., 2014). Ironically, however, CSR may also actively court such civil society as a buffer against formal political predations, as Markus (2012) shows in the case of Ukraine pre-Maidan: Manufacturing firm Oleyna was under attack in 2006 from the financial conglomerate Privat Group, which attempted to expropriate the firm using formal political pressure and informal, underhanded (and illegal) means. Oleyna was saved only through the broader stakeholder community it cultivated, including local communities, but, notably, was also protected by the international community, a luxury that most firms under populist governance do not have. 4

Finally, CSR may be less valuable for a firm under certain styles of governance, not because of the lack of benefit in terms of political influence but simply because different regimes may value CSR very differently. In the first instance, CSR can fail if a firm reduces the pluriversal facets of social responsibility to a simplified dimension that does not comport with the worldview of the government (Ehrnström-Fuentes, 2016). As Zhao (2012, p. 441) notes, CSR is a “non-regulatory aspect of the business–state interaction beyond legal compliance,” meaning that informal institutions and compliance rules the day where the state is active. Viewing one aspect of CSR as “important,” where a government’s priorities lay elsewhere, is a recipe for failure, especially if a government is actively working against a firm’s own particular CSR strategies (Idemudia, 2010). Moreover, the very same institutional failings that may make CSR attractive as a tool of political influence may also create rent-seeking behavior and distortionary effects (Lepoutre et al., 2007), with political forces pushing for high-profile CSR and/or (for the government) more lucrative CSR initiatives than those favored by the market (Michael, 2003). As Vishwanathan (2014) shows, when political pressures are intense in a country, the use of CSR is detrimental for a firm’s bottom line, as time is spent dealing with these pressures rather than in creating intangible value for the firm. The governance matrix can thus change immensely the risk/reward payoff for a firm in undertaking CSR.

A Theoretical Examination of CSR Under Populism

This realization that the value of CSR to a firm is highly context-dependent brings us to the situation where CSR is being implemented under a populist regime. As noted above, populist regimes, in their governance, are an odd phenomenon: In the first instance, as Ware (2002) noted, the goal of populism is generally to be elected, whereas the goal in power is to retain power (Devinney & Hartwell, 2020). In this, populism’s style and tenor are derivative of democracy: a type of democracy that is grounded on representation and the constitution; that uses elections along with, occasionally, direct forms of popular vote, such as the referendum and the plebiscite; and whose political arena is made of issue-based associations and partisan affiliations, not solely individual actors and elections. (Urbinati, 2019, p. 113)

But with its focus on being on the outside of elite governance, populism thus works more as an electioneering style (Barr, 2018) than a coherent philosophy of governance itself (although there is evidence that this is mainly true at the national level, as Drápalová & Wegrich, 2021, find evidence that a sort of technocratic populism can be prevalent at municipal levels).

When it is in power, however, populism appears to exist somewhere between fascist or totalitarian and Athenian democratic styles of governance (Eatwell, 2017; Weyland, 2018), with a much more expansive and activist state than in even the most social democratic countries but stopping short of complete centralization and repression as in authoritarianism. It may even encourage local participatory governance as a mean to continue its relationship with “the people,” but for the most part, national-level governance is predicated on what is good for the populists rather than the people (Rhodes-Purdy, 2015).

This emphasis on an activist state (an institutional apparatus that should be in service of the populist party) colors populism’s relationship with business and especially business incentives for strategy and operations. Across populist regimes, there often is an expectation for firms to engage in ways that support the political regime and, by extension, the people. Unlike other forms of authoritarian governance, which serve “the nation” or “the state,” populism has an underlying expectation that business activities support “the people,” conveniently identified as the populist party and/or its leader (Katsambekis, 2022). Practically, this translates to corporate responsibility redefined as serving the goals of the ruling elite (Blake et al., 2022) and away from a nebulous “social” entity of various “stakeholders.” Indeed, in a populist regime, the set of relevant stakeholders is collapsed to just one, the ruling populist party (or, in extreme cases, even just the leader him or herself). Rather than having a firm attempt to curry to various and diverse stakeholders with differing needs, populists have redefined themselves as the only stakeholder through which the one true “people” speak, acting as a political manifestation of a benevolent and progressive people.

Extending this school of thought to CSR is thus just a step away, as it implies that CSR at the firm level is redundant in its emphasis on stakeholder management. Put another way, if firms were able to satisfy their business responsibilities and aid the populist regime, they would be satisfying their social responsibilities, as the populists are the people made manifest in a political sense. There would be no need for additional environmental, community, or labor engagement because these areas would all be satisfied by a variety of populist programs. With populism seeking to co-opt established institutions to serve populist ends (Hartwell & Devinney, 2021), CSR becomes another casualty, with a myriad of stakeholders routed instead through the political organizations and/or leadership of populists.

Indeed, as CSR is, at its heart a liberal, idea (Kinderman, 2017), allowing a firm to choose the way it attempts to please its various stakeholders, populists—as a more authoritarian and centralized political approach—would naturally be opposed to such an approach as they view themselves as the representatives of the most important stakeholder group, “the people.” As Bainbridge (2020, p. 543) noted, “Populists historically have viewed corporate directors and managers as elites opposed to the best interests of the people,” and thus they would not have the best interests of the people at heart. Rather than a messy, uncoordinated, and disparate tangle of individual initiatives, CSR would then be reduced to “support of the populist regime”—the only responsibility that a firm needs to undertake in terms of its relationship with society—with the rest of a firm’s social obligations filtered through populist governance and policies. This is very different than other types of governance styles across the spectrum, where predatory states may ignore CSR altogether and welfare states may impose CSR requirements of firms (Brejnholt et al., 2021). Instead, populism demands CSR on its own terms, through its own devices, and oriented toward one all-encompassing stakeholder. CSR goes from being an informal and firm-level institutional mechanism to being a formal, coordinated political mechanism under the purview of the populist elite and against the wishes of the existing business elite. The only agency which may be allowed for businesses in choosing CSR initiatives would thus be CSR that supports the regime itself (Blake et al., 2022).

An example of this transfer of CSR from firms to populist governments is the increasing proliferation of local content requirements. A staple of 1950s and 1960s development approaches, they were wiped away by international organizations such as the World Trade Organization and vehicles such as bilateral investment treaties (BITs). Although these modern mechanisms prohibit the use of local content requirements, there is no prohibition against voluntary local content requirements, and many firms use these as a way to engage in CSR (Gilberthorpe & Banks, 2012; Pang et al., 2018). However, in a series of populist countries over the past decade, local content requirements have come back in vogue as a mandatory attribute of doing business, with populist governments wresting agency from firms and placing it back under the purview of an activist and populist state (Buckler, 2021).

Similarly, whereas many firms have undertaken specific CSR activities, populist governance may eschew such initiatives in pursuit of broader social goals and other types of CSR that favor the regime. The example of the oil industry in Venezuela is instructive, as the ascendance of Hugo Chávez meant that the state oil company PDVSA began to spend massive amounts on social programs and projects: According to Utting and Ives (2006), in 2005, they spent over four billion dollars (equal to 6% of previous year revenues) on such social projects. At the same time that this bonanza was directed toward “the people,” PDVSA jettisoned any remaining environmental CSR it may have had and has become a notorious polluter, transgressing all manner of environmental norms and regulations, including spills, occupational disasters, and corruption (Contreras-Pacheco, 2021).

The variety of populism adhered to (anti- or pro-business) would further define the possible ways in which populist governments interact with firms undertaking CSR. From the pro-business side, there is much diversity in the tolerance of a firm to undertake CSR quasi-independently from the government. At one end of the spectrum are governments that are concerned with enlarging the economic pie, as in Joko Widodo’s administration in Indonesia (Chacko & Jayasuriya, 2018; Wicaksana, 2022), which might see successful business dealings (leading to growth and increased employment) as satisfying populist responsibilities and thus allowing a longer leash for additional initiatives. On the other hand, regimes concerned more with the distribution of the pie would be less likely to allow for independent-minded CSR (as in Russia or Venezuela), even if there was ostensibly a pro-business orientation of the ruling party. Thus, simply being classified as “pro-business” is not enough to say in which direction the influence may go, as it may come down to the specific variety of populism in a particular country—and that populist regime’s perception of where firms should be concentrating their energies. It would also depend on how connected the previous elite, which populism sets itself up in opposition to, was connected to existing CSR or business initiatives.

On the contrary, anti-business populism is likely to be more clear-cut in its effects on CSR investment. Leaders such as Evo Morales in Bolivia or Jacinda Ardern’s first administration in New Zealand (as noted, supported by populist Deputy PM Winston Peters) are far more likely to have much higher expectations for firms in their dealings with the state, being already ideologically predisposed to a lack of trust in the private sector; this lack of trust will mean narrowly circumscribing firms’ individual agency to undertake CSR, as it is not believed that firms can actually satisfy social responsibilities on their own. In fact, anti-business stance populists, due to their ideological priors, could make CSR a net negative for a firm, as the anti-elite rhetoric (and policies) of populism would perceive firm CSR investments only as an attempt to attain positive political and social public relations (so-called “greenwashing”). Under such a regime, firms that also attempted to utilize CSR as a subtle form of CPA could find such a strategy backfiring, losing both influence and bringing unwanted attention to their activities from the ruling regime.

Empirical Model and Results

To examine the effects of populism on CSR, we undertake an empirical exercise using firm-level data from countries that have transitioned to or away from populism. In line with our points noted above, we believe that firms under populism, facing new demands and expectations from the government, will withdraw from “peripheral” activities such as CSR to either refocus on their core business or to shift resources to more regime-friendly activities.

The formal model expressing this relationship is thus:

where y is the change in the CSR activities of a firm (j) in a country (i) at time t + 1 versus time t. As we are concerned with the behavioral effects, rather than the level of CSR, we utilize change in CSR to see what occurs to a firm’s preexisting CSR rating when populists come into power. This approach also allows us to account for noncontemporaneous effects, as we can observe how a firm’s CSR involvement is altered in response to a change in government. To proxy for these CSR activities, we utilize a firm’s overall “CSR rating” as given by the CSRHub database as the left-hand variable. The “CSR rating” is defined as a summation of over 5,000 data elements (including S&P Global, MSCI, and others) per firm per year in 12 subcategories of CSR performance, resulting in a number on a 0 to 100 scale (with higher numbers indicating more CSR involvement and performance). Given that firms are rated annually over such a wide variety of metrics, there is the possibility of substantial annual variation in CSR performance, making this a plausible proxy for firm dedication to CSR year on year.

The right-hand side variable of interest is the first term, Populism, a simple dummy taking the value of 1 for each year that a country had a populist leader and 0 otherwise. To classify a leader as populist or not, we use several commonly accepted metrics from the political science literature and especially relied on Timbro (2019), Grzymala-Busse and McFaul (2020), and Norris (2020) to classify a leader as “populist” or not. In addition to this binary approach, and delving deeper into the issue of the different varieties of populism, we also have an alternate populism measure included, namely, Varieties of Populism, coded as a −1 if the leader is an anti-business populist, 0 if neutral or no populist in power, and +1 if the leader is a pro-business populist. 5 We expect that countries that have populists in power should have less CSR overall, meaning a negative correlation between populism and the change in a firm’s CSR rating. For the variety of populism, the theoretical link is more ambiguous; it is likely that firms under anti-business populism will be focused on survival and keeping their heads down, so CSR will not be undertaken. On the contrary, firms may be trying to ingratiate themselves with the anti-business rulers and thus undertaking CSR might be a way to curry favor. Similarly, pro-business populists might be in favor of all business activities, so long as the business is serving national greatness, and thus CSR might not be actively discouraged; however, as noted above, CSR might be seen precisely as a peripheral activity and pro-business populists might push for more corporate political responsibility in the form of profit-maximization rather than firm-determined CSR.

The other terms in Equation 1 are used to isolate nonpolitical environment effects, with the first a set of firm controls derived from the literature. These include a company’s (log) operating revenues, (log) total assets, profit/loss (P/L) before tax, profit margin, return on equity, and its solvency ratio, with the theory being that firms not concerned with survival (i.e., profitable) have more assets or funds to dedicate to CSR activities (W. Li & Zhang, 2010). Similarly, we include a set of macroeconomic covariates of the country in which a firm is located to proxy for business cycle effects, including annual inflation, annual GDP growth, gross capital formation (as a percentage of GDP), trade as a percentage of GDP, and domestic credit to the private sector. The inclusion of these controls will also determine to some extent the space that a particular firm has to undertake CSR initiatives, independent of the political environment (Al Hawaj & Buallay, 2021).

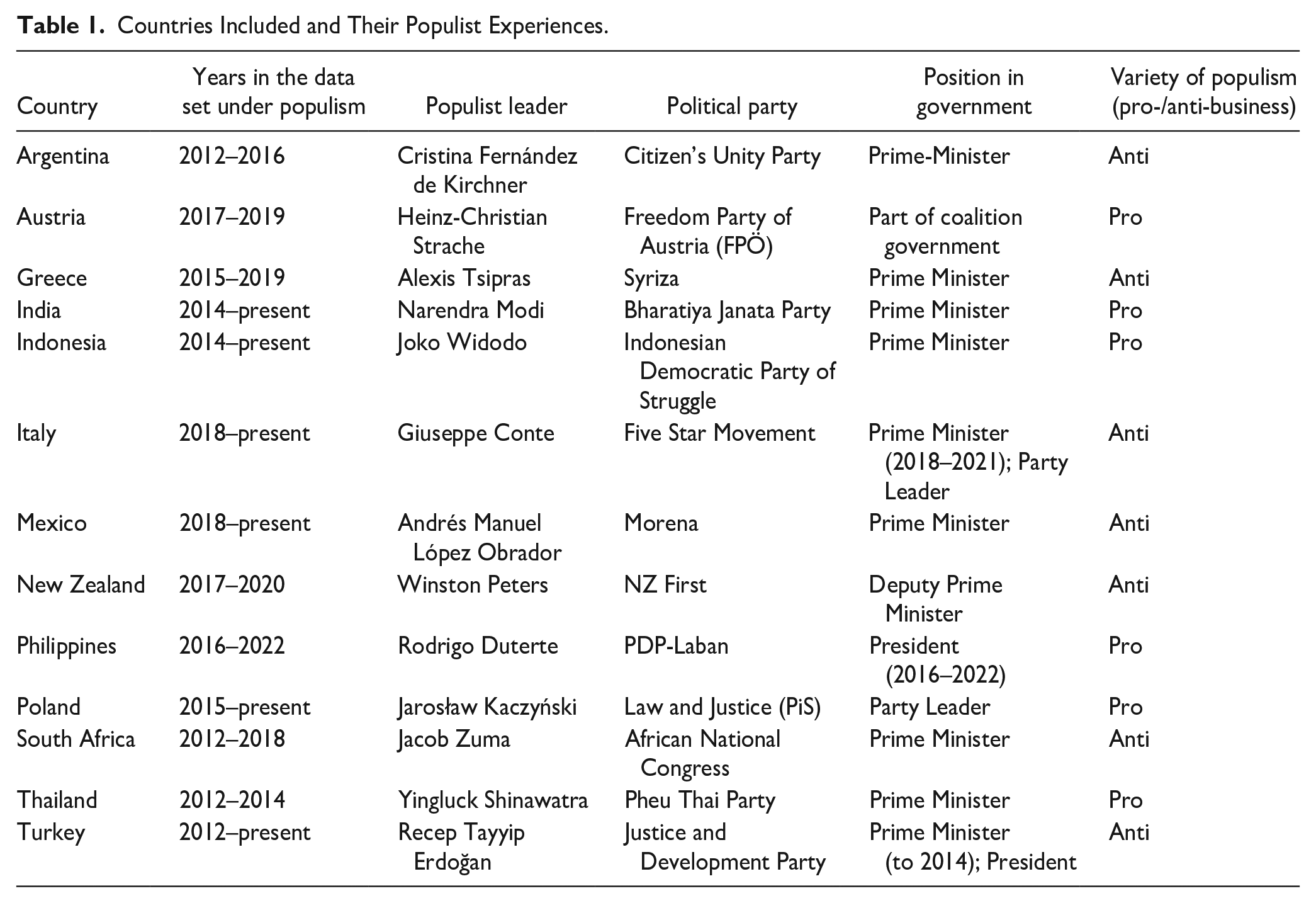

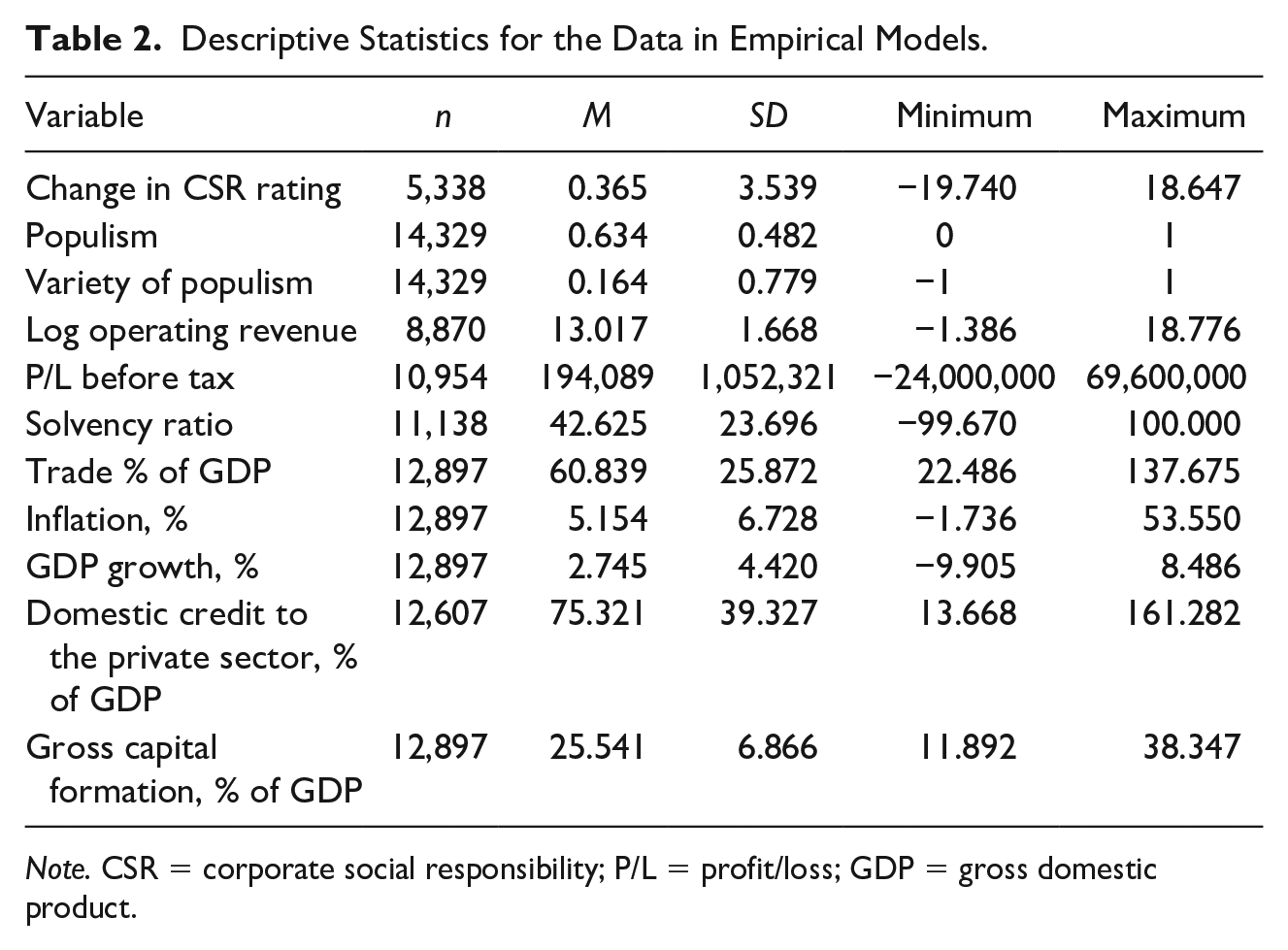

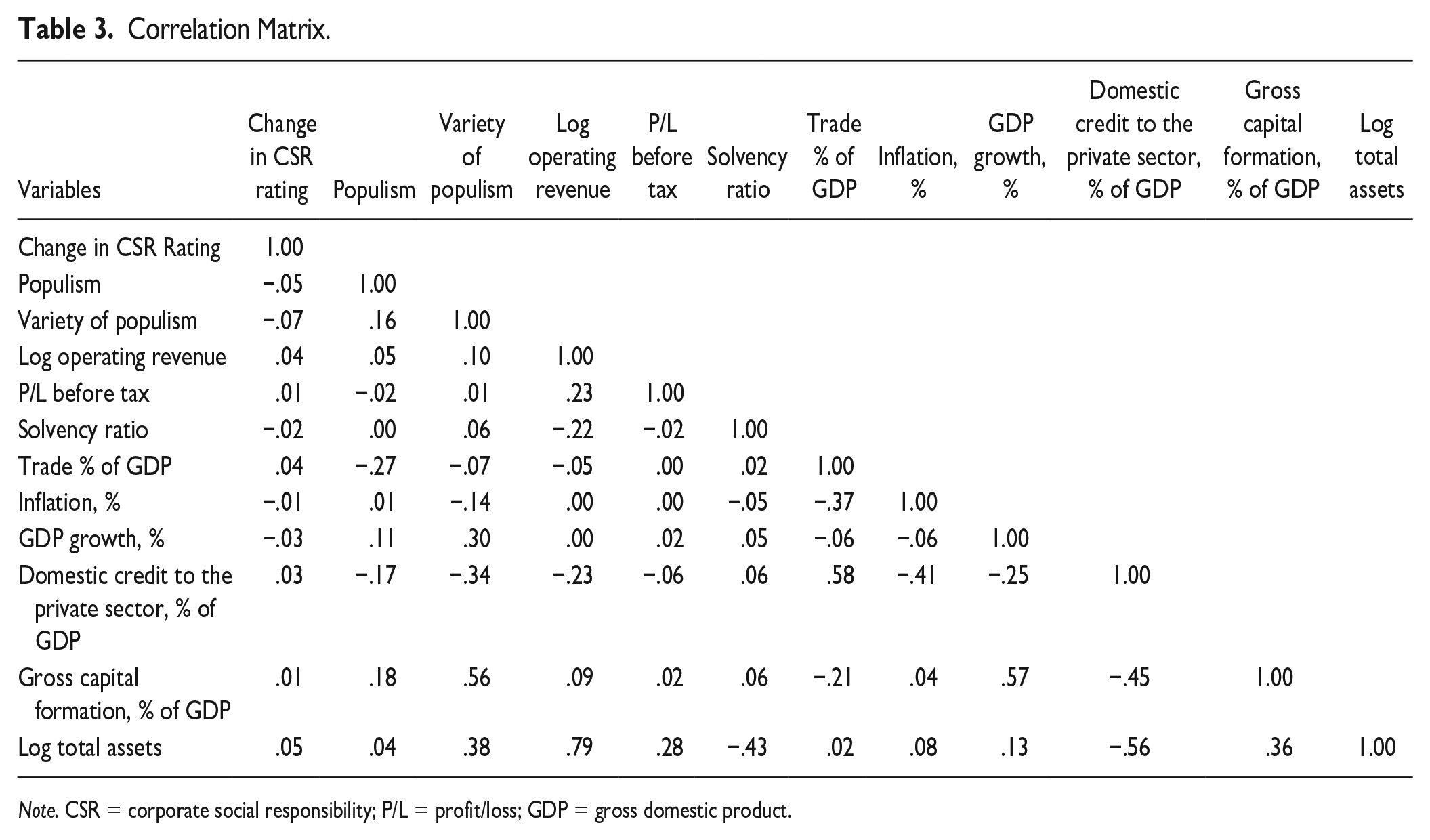

To populate this model, we have amassed a database of 1,434 firms across 13 small- and medium-sized countries that have experienced populism from 2012 to 2020, with a collection of both pro- and anti-business variants. 6 The CSR rating’s provenance has already been noted but given the lack of a CSR rating for all firms in all years, we are left with approximately 2,000 to 3,000 observations per model. Firm financials are taken from the Orbis database and matched up with the companies in CSRHub, whereas macroeconomic controls come from the World Bank World Development Indicators. As noted above, for our variable of interest, coding whether or not a leader or party in government was populist was done by the authors based on a series of populism databases, including the Timbro (2019) Authoritarian Populist Dataset, Norris (2020), and the “Votes for Populists” database (Grzymala-Busse & McFaul, 2020)—a more precise coding of the countries (and the varieties of populism) included in the database is shown in Table 1. Table 2 offers some descriptive statistics of the data and Table 3 shows pairwise correlations.

Countries Included and Their Populist Experiences.

Descriptive Statistics for the Data in Empirical Models.

Note. CSR = corporate social responsibility; P/L = profit/loss; GDP = gross domestic product.

Correlation Matrix.

Note. CSR = corporate social responsibility; P/L = profit/loss; GDP = gross domestic product.

Finally, given the exigencies of the data and the reality that many of the firm, political, and macroeconomic variables are highly dependent upon each other, we utilize a system-GMM estimator to account for the endogeneity in the system. 7 The benefit of system-GMM is that it allows for the capture of a multiplicity of fixed effects while also instrumenting the variables in the equation with their own lags; in practice, most of the macroeconomic variables were utilized as standard instrument variables while firm-specific attributes utilized GMM-type instruments. Moreover, this data set, consisting of “large n” and “small t” is precisely the sort of data that system-GMM was designed for. Taken together, these facts make system-GMM the preferred estimator, and the models shown below have both dynamic stability and satisfy the commonly utilized criterion for model fit, including rejecting the presence of autocorrelation of order AR(2) in first differences and not rejecting the null of the Hansen test statistic (i.e., that the overidentifying restrictions are valid).

Results

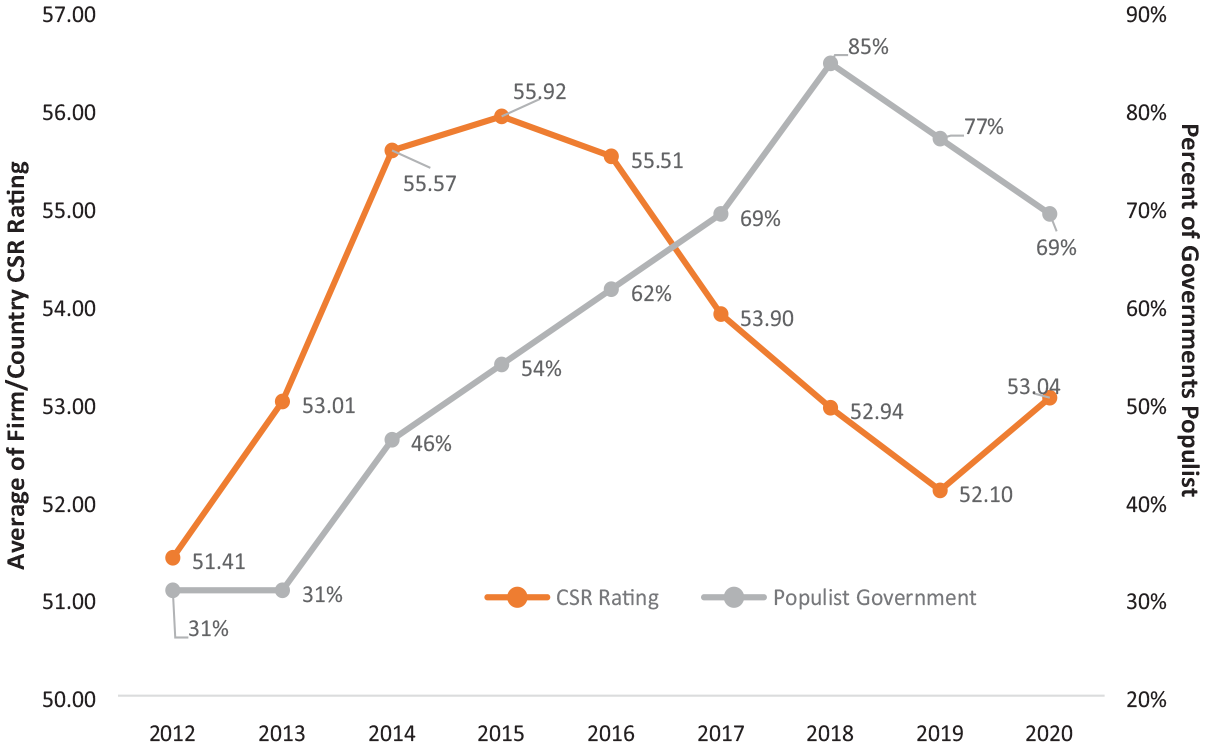

The first quick results we can point to are simply based on an examination of the raw data. Figure 1 presents average CSR ratings (0–100) of the firms in the sample by year/country and the percent of the countries in the sample that had a populist government in that year. What is seen is that the CSR ratings overall peak in 2015 and reverse through 2019, whereas the percent of governments in our sample that are populist peak 3 years later. As one would not expect contemporaneous effects, there is potentially some cursory information that the effect has a lag as firms adjust to the new political reality. However, what it reveals is that there is sufficient variation of both the dependent variable (CSR) and the key independent variable (populism) over the sample and study period.

Average Firm CSR Rating by Country/Year and Percent of Countries With Populist Government.

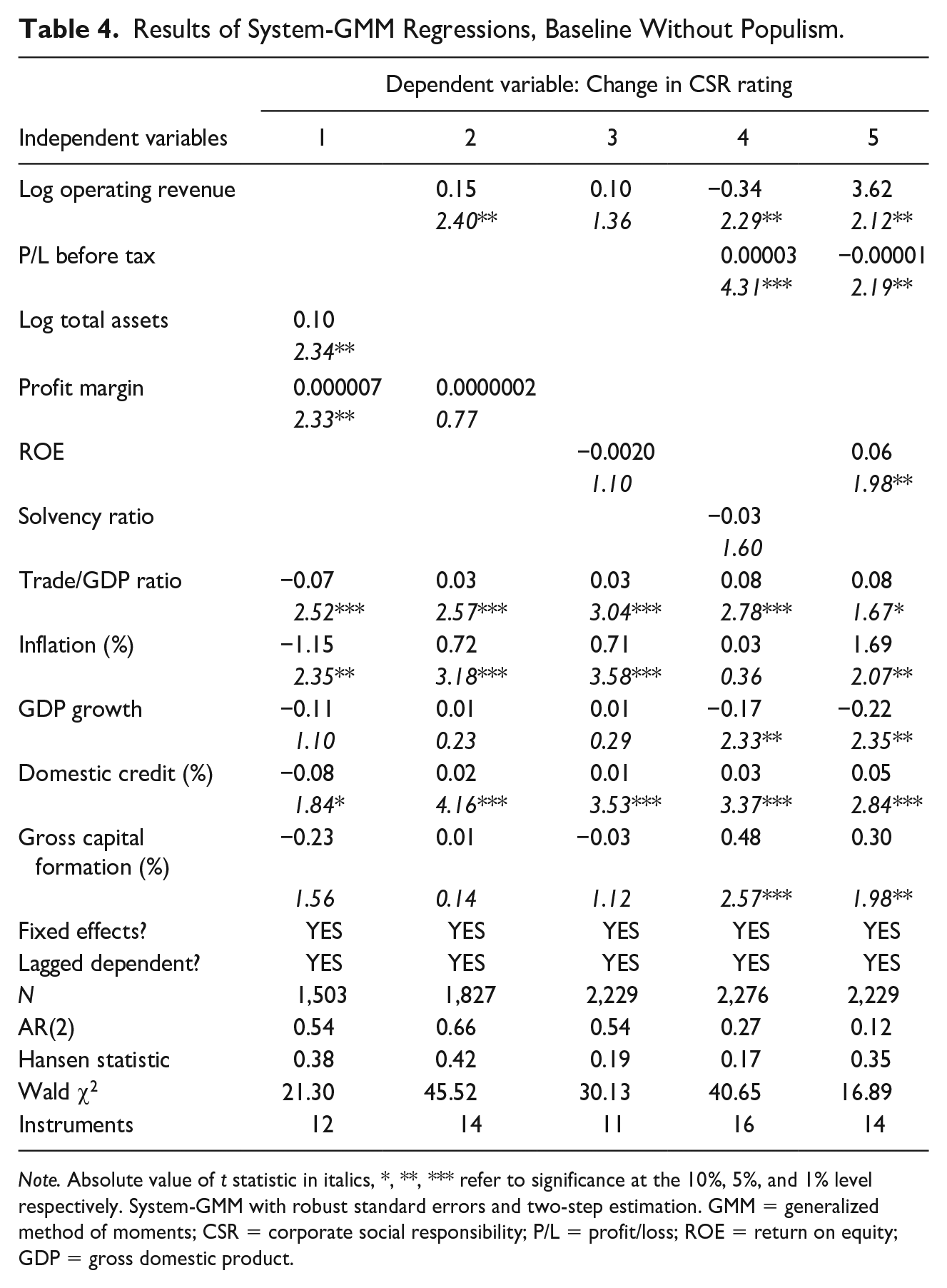

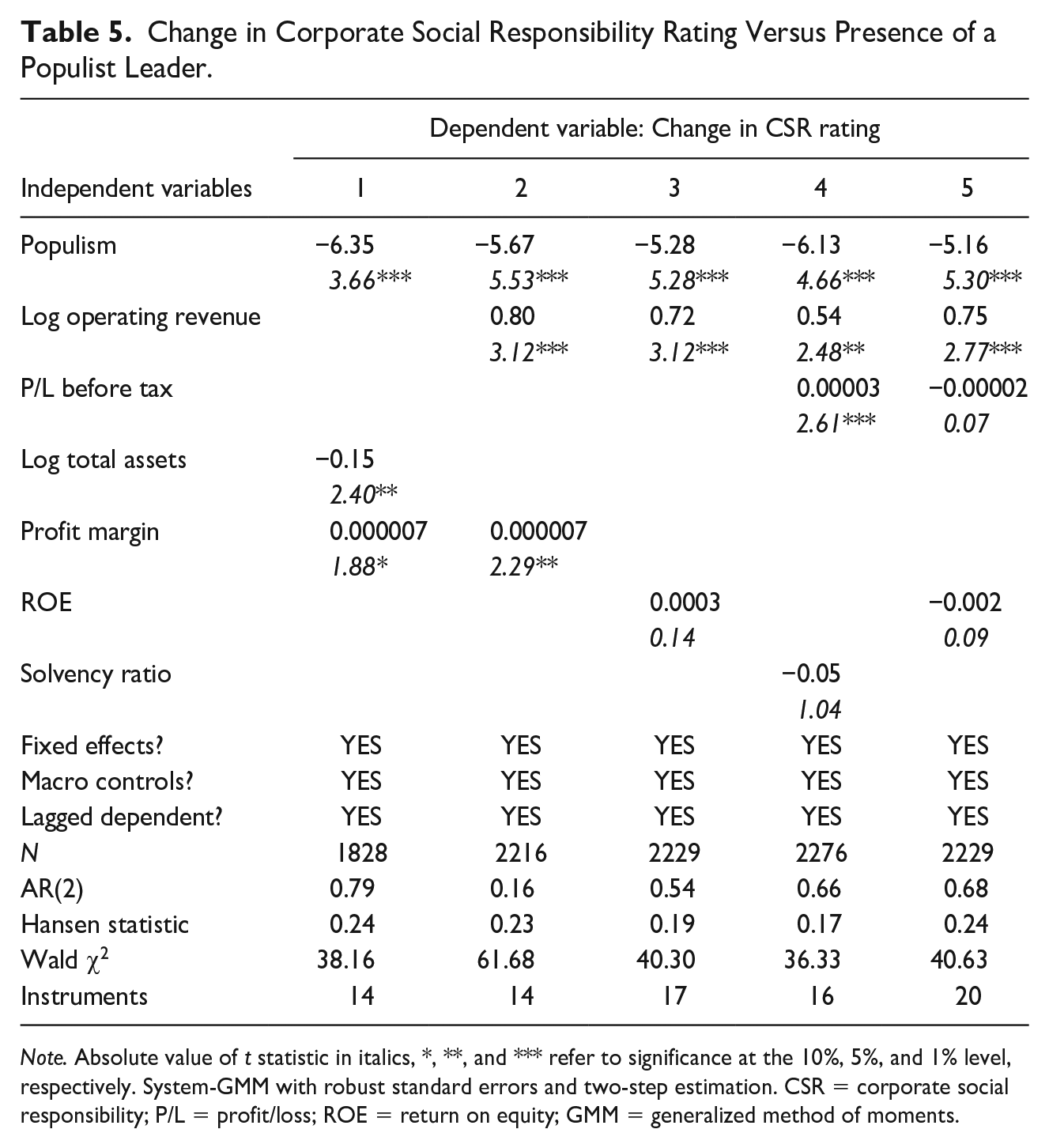

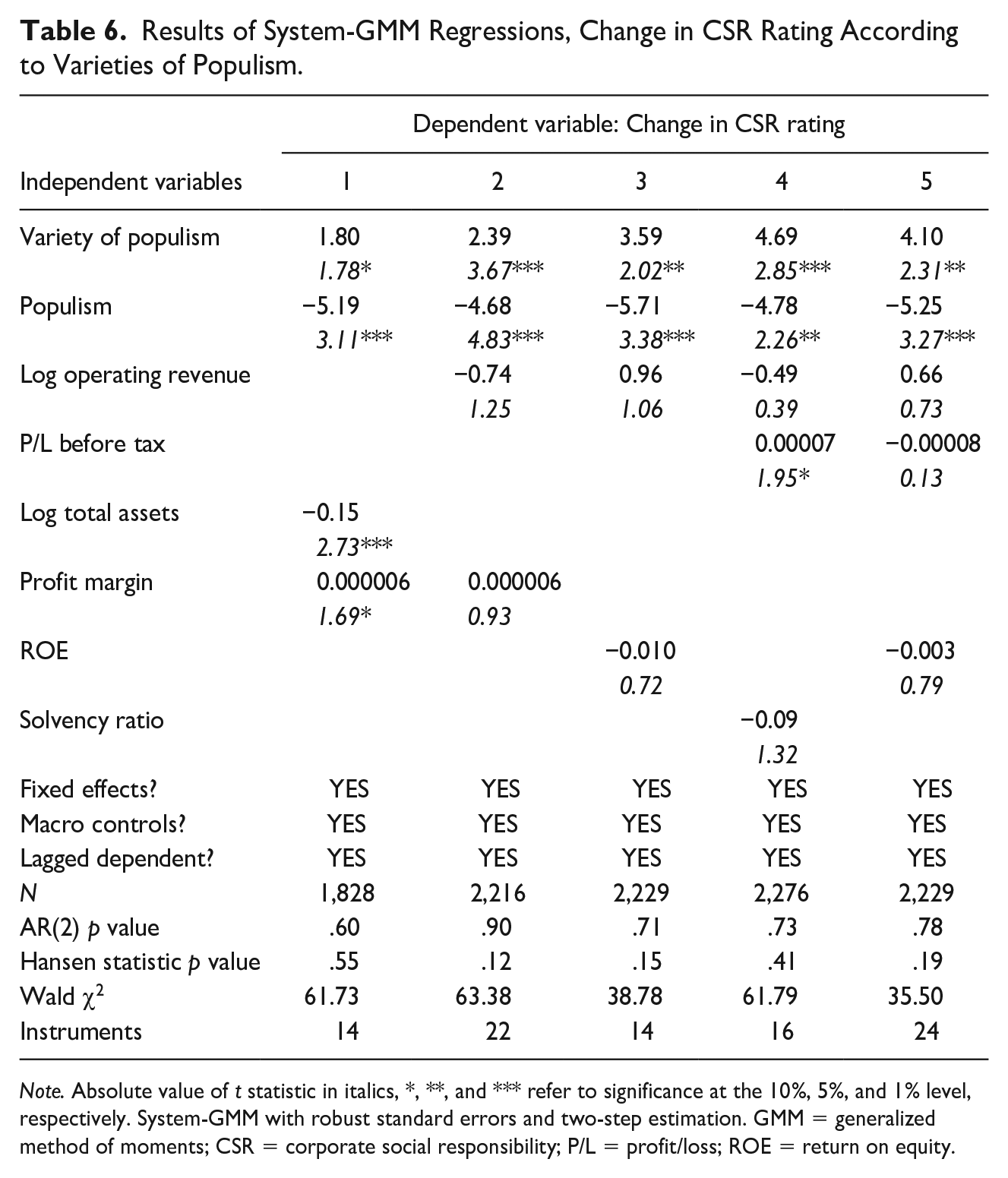

Looking more rigorously at these relationships, the results of the GMM models are shown in Tables 4 through 7. Table 4 provides baseline models without populism as a covariate, which helps to understand whether populism, from an econometric standpoint, improves the fit of the model. Comparing the models with populism (Table 5) and varieties of populism (Table 6) with the controls only models (Table 4), we see that there is a significant improvement in fit for all models except Model 4 in Table 5. Hence, populism, however measured, is picking up a significant part of the effect of a change in CSR rating across the firms/countries/years.

Results of System-GMM Regressions, Baseline Without Populism.

Note. Absolute value of t statistic in italics, *, **, *** refer to significance at the 10%, 5%, and 1% level respectively. System-GMM with robust standard errors and two-step estimation. GMM = generalized method of moments; CSR = corporate social responsibility; P/L = profit/loss; ROE = return on equity; GDP = gross domestic product.

Change in Corporate Social Responsibility Rating Versus Presence of a Populist Leader.

Note. Absolute value of t statistic in italics, *, **, and *** refer to significance at the 10%, 5%, and 1% level, respectively. System-GMM with robust standard errors and two-step estimation. CSR = corporate social responsibility; P/L = profit/loss; ROE = return on equity; GMM = generalized method of moments.

Results of System-GMM Regressions, Change in CSR Rating According to Varieties of Populism.

Note. Absolute value of t statistic in italics, *, **, and *** refer to significance at the 10%, 5%, and 1% level, respectively. System-GMM with robust standard errors and two-step estimation. GMM = generalized method of moments; CSR = corporate social responsibility; P/L = profit/loss; ROE = return on equity.

For the first populism model (Table 5), we investigate the relationship of CSR rating changes in firms when any stripe of populism is in power versus when there is a nonpopulist government. The results are consistent across various combinations of control variables: Populism unequivocally is associated with a decrease in firm CSR ratings. As Table 5 shows, the coefficient for populism is negative and highly significant (ranging between −5.16 and −6.35). In practical terms, the CSR rating of a firm changes little from year to year, with a mean change of 0.365 on a measure that varies from 0 to 100 (see Table 3), implying an effect size of approximately 1.7 to 2.3 CSR ratings points. In other words, the presence of a populist leader, on average, corresponds with an approximately 5% lower firm CSR rating year-on-year, with the magnitude depending slightly on which covariates are used control for heterogeneity.

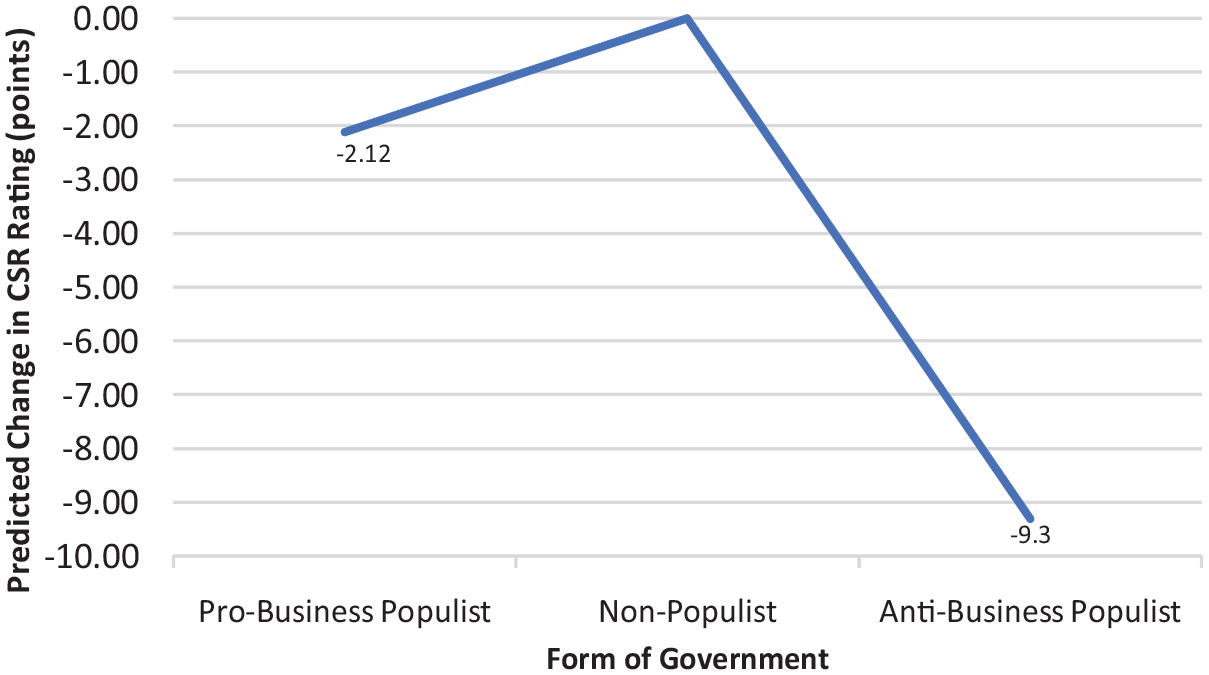

Turning to the varieties of populism (Table 6), we see some very interesting results emerge. In the first instance, the presence of a populist in power continues to be associated negatively with CSR engagement, with similar effects in the model including revenue and profit margin and revenue, P/L, and solvency (Column 4), with coefficients of −4.69 (p = .000) and −4.78 (p = .024), respectively. More interesting is the behavior of the varieties of populism variable, which is across-the-board positively related to CSR ratings. The interpretation of this is that pro-business populists seem to demand less of firms, leaving them free to pursue CSR in any way that they wish. Alternatively, it is possible that pro-business populists have less of a deleterious effect on the macroeconomic environment, meaning that firms are better situated to thrive and then do as they please with their success (remember these are all conditional effects). However, this is something not measurable in the model as specified. The impact of looking at the varieties of populism, versus populism generally, can be seen Figure 2, which uses Model 3 to estimate the effects of (a) populism versus no populism and (b) the form of populism. Under a baseline of no populism, the marginal effect is −2.12 in the pro-business populism case and rises fourfold to −9.30 in the anti-business case. Hence, the general conclusion is that anti-business populism crowds out more CSR activity than pro-business populism.

Marginal Effects, in Change in CSR Rating, by Variety of Populism.

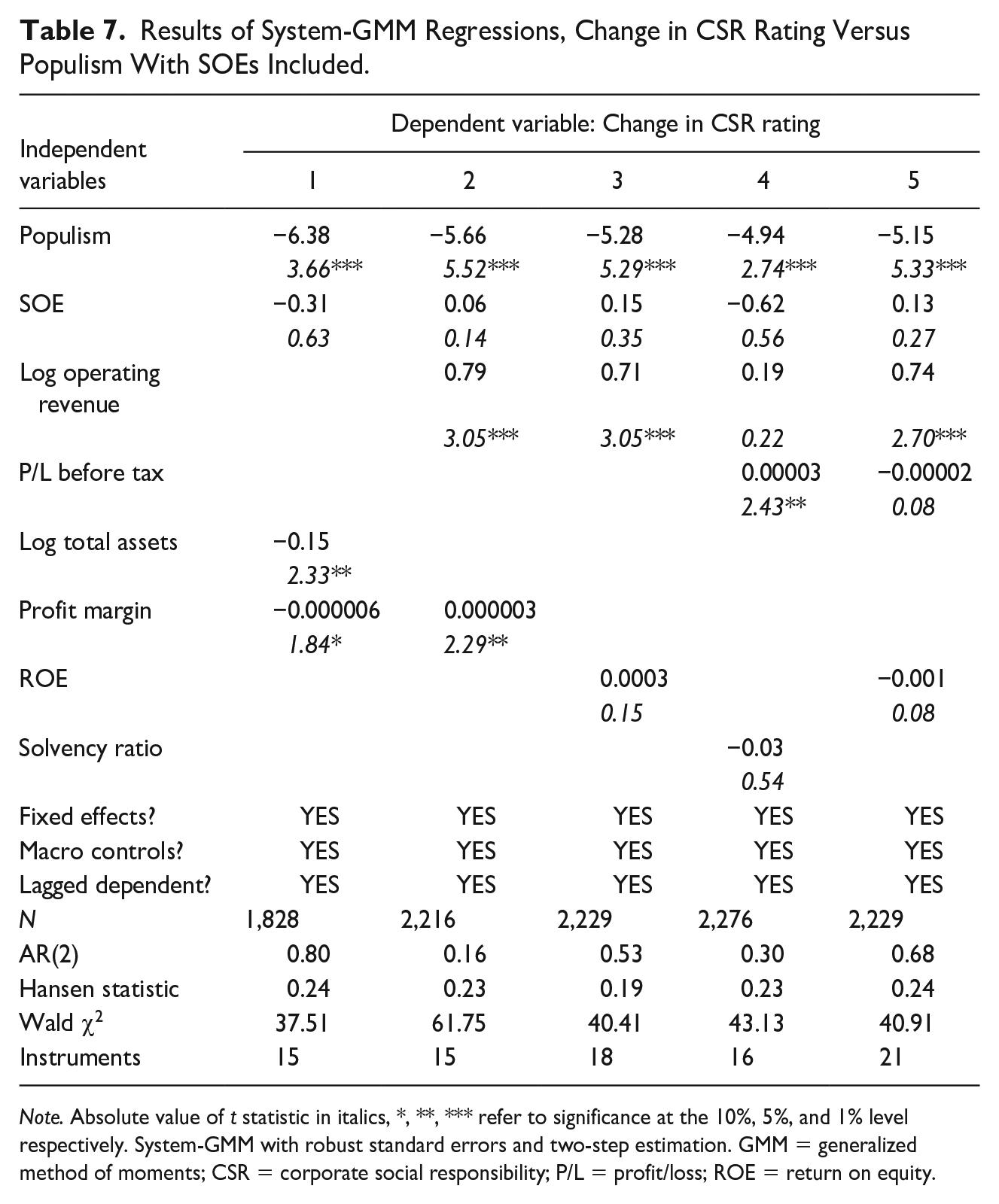

Results of System-GMM Regressions, Change in CSR Rating Versus Populism With SOEs Included.

Note. Absolute value of t statistic in italics, *, **, *** refer to significance at the 10%, 5%, and 1% level respectively. System-GMM with robust standard errors and two-step estimation. GMM = generalized method of moments; CSR = corporate social responsibility; P/L = profit/loss; ROE = return on equity.

Finally, Table 7 is included as a robustness test. Many papers have noted (W. Li & Zhang, 2010) that ownership structure is a key determinant of CSR performance, and indeed many of the countries we examine here have substantial state-owned sectors. To account for this, we delve back into the data and code firms as state-owned if they have national government ownership of 50.1%, leaving them as a 0 if otherwise. Including this dummy for SOEs we rerun the analysis of Table 4 to find that a firm being an SOE has very little effect (either economically or statistically) in its overall CSR performance. Populism, however, continues to pull down firm CSR activities at even higher levels of significance, suggesting that overall, populism’s demands on firms has a decided effect in reducing firm corporate social responsibility.

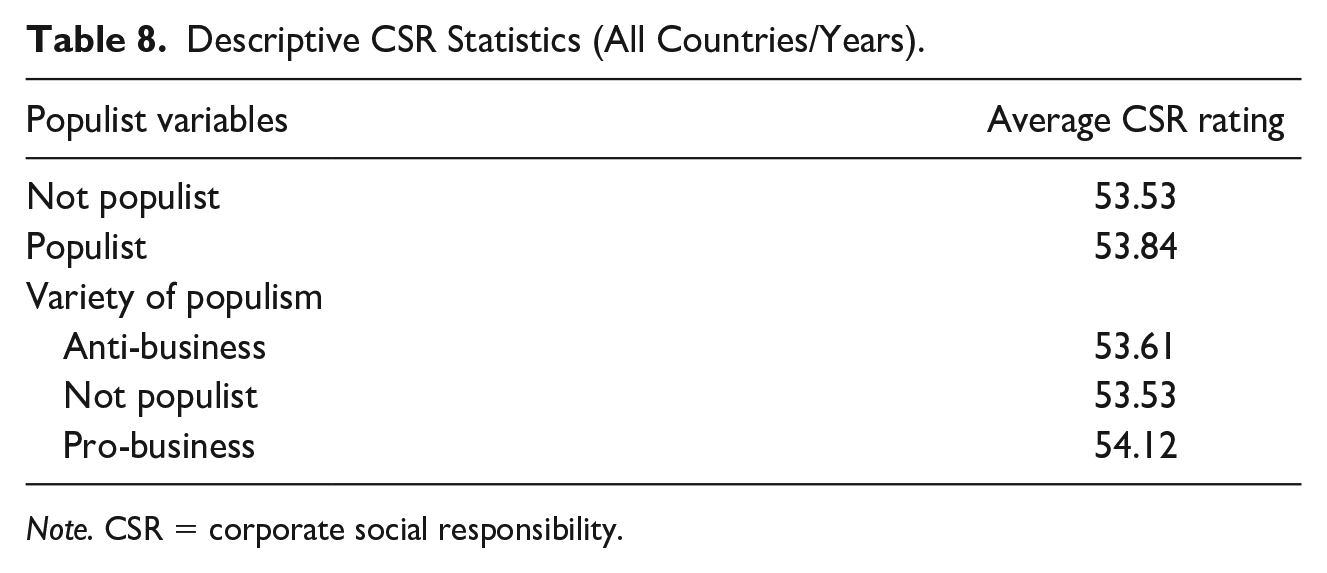

Overall, the statistical results show clearly that populism overall is correlated with fewer CSR activities, in the sense that it attenuates any trend of growth in CSR activities that occurred prior to a populist victory. It is most negative at the margin (Figure 2 and Table 5) when the populist government takes an anti-business stance. One can get a more nuanced view of what is happening by looking at the 13 countries studied individually. As Figure 1 showed, there is clearly a time-related effect in the sample. And over the 13 countries studied and the range of years, the aggregate data do hide quite a lot. Table 8 shows that when compared with a nonpopulist government, the CSR rating is lower, but the differences are not really material. Part of this relates to the fact that from 2012 through 2015, both populism and CSR ratings both increased; in this case, the pro-business populist governments seem to exhibit a more attenuation effect (on average, there is no real change). From 2016 through 2018, CSR ratings declined on average while populism marched on.

Descriptive CSR Statistics (All Countries/Years).

Note. CSR = corporate social responsibility.

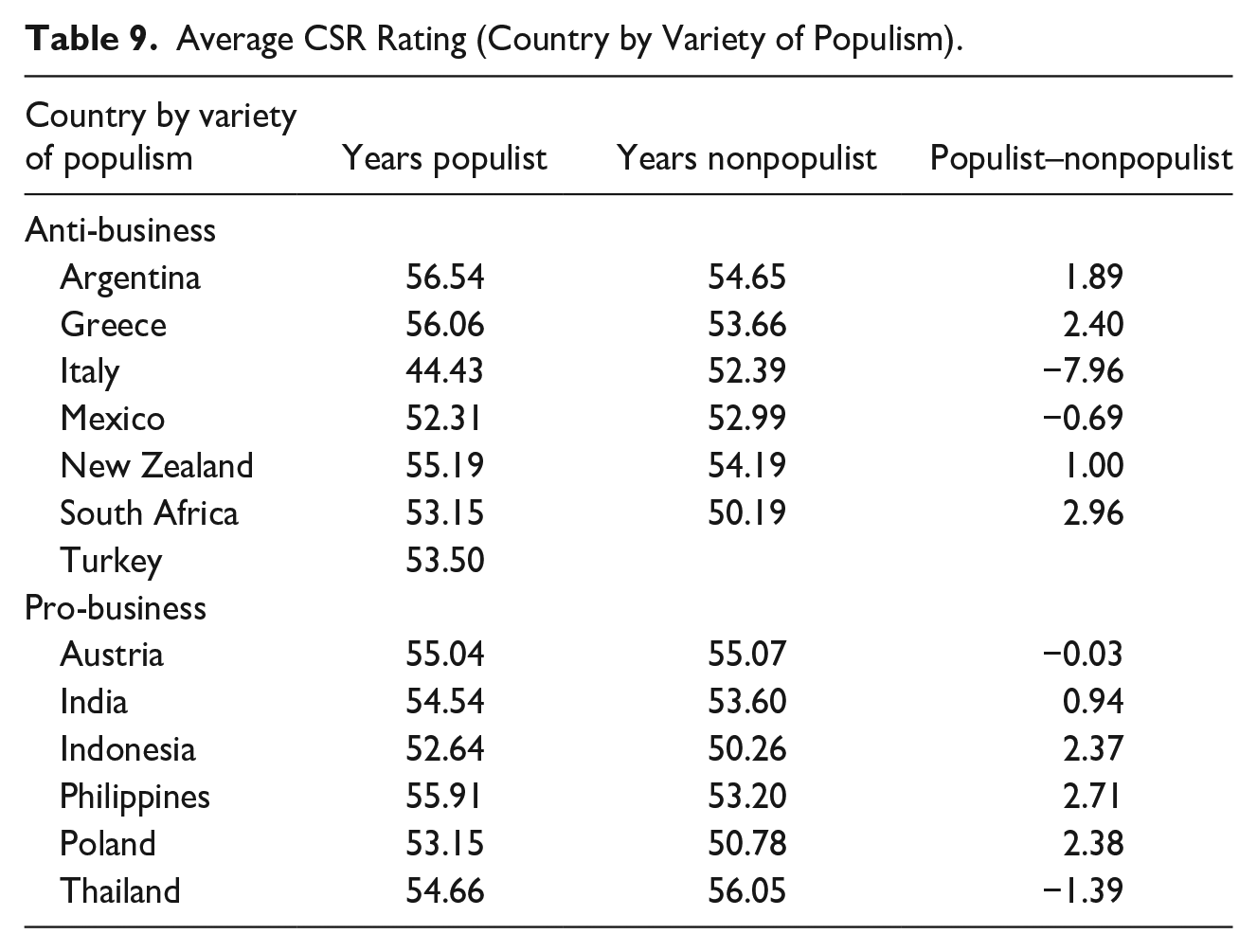

What we can see in Tables 9 and 10 is that the effects are highly variable by country (which can reflect industry mix, macroeconomic and other factors we included as controls). If we look at countries that elected anti-business populists, we see that Italy saw a large drop in the CSR ratings of its firms, but firms in South Africa and Greece showed material increases. In the case of pro-business populist countries, Indonesia, the Philippines, and Poland showed an increase, whereas Thailand (admittedly moving away from pro-business populism during this timeframe) had a slight decrease. Hence, there is considerable variability to explain, and our GMM models hopefully account for a great deal of this heterogeneity.

Average CSR Rating (Country by Variety of Populism).

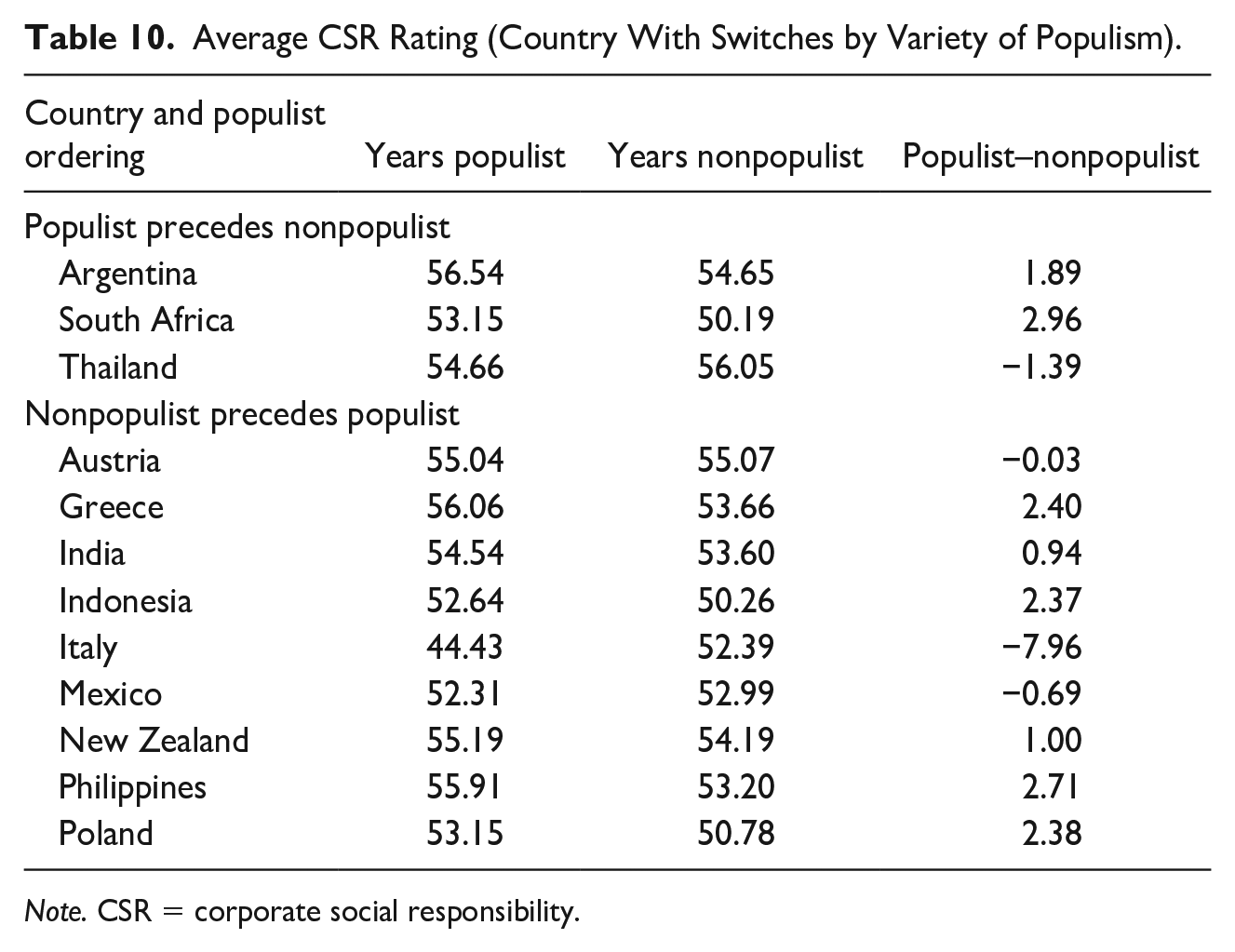

Average CSR Rating (Country With Switches by Variety of Populism).

Note. CSR = corporate social responsibility.

One last point that may matter is the directionality of the populist acquisition (or loss) of power. In three countries, populists were ousted during our sample period—Argentina, South Africa, and Thailand—while in most of the others, populists replaced a nonpopulist government (and were in power in 2020). Only one, Turkey, had a populist government for the entire sample period. One question that we do not address—and which the information in Table 10 may imply—is that the actions that a populist government requires may not be undone by their nonpopulist successor. However, without more data this is difficult to address.

Discussion

This empirical exercise is robust across specifications and suggests that, indeed, firms under populism are expected to perform in ways in which they might not under a less intrusive, less populist government. While we believe that these results support our theoretical suppositions, there are of course many limitations. In the first instance, we are unfortunately only to see half of the influence of populism; that is, we believe, and the evidence appears to show, that an increase in populism will lead to an increase in other regime-friendly activities and thus a reduction in other activities such as CSR. However, our results only show that the presence of populism does in fact result in a reduction of CSR; it does not show the reallocation of effort elsewhere or the activities that might replace CSR under populism. Thus, additional work needs to be done at the firm level so as to determine whether populism implies less CSR and whether there is also an increase in other activities consistent with populist ideals.

An additional criticism that can be made of this exercise regards the CSR measure itself, which is somewhat subjective. Despite being based on thousands of data sources, it would be preferable perhaps to see the actual allocation of firm resources to CSR—and how it changes during populist administrations—to better understand the effect that populism has on specific countries. Such an in-depth look within a country, using textual analysis as in Zueva and Fairbrass (2021), will necessarily narrow the scope of the analysis away from the broader, exploratory examination we have done here, requiring more knowledge of a specific country context. However, such an approach may also help us to understanding the distribution of CSR within a country better, and if it is being done in response to populism as a political action or defense mechanism (generating more stakeholders as a buffer, as shown in Markus, 2012) or if it is a reallocation of CSR funding. This would also help to detail the effect that the various varieties of populism have a little better, in understanding how pro-business populism encourages activities which lead to a higher CSR rating. Moreover, even if we accept that this CSR rating is flawed but is overall a good indicator of CSR commitment by a firm (albeit at an aggregated level), we also may explore the data further and look at the various subcomponents (some of which include environment, governance, community development, and human rights) and see which specific channels populism is operating through.

Finally, a criticism that might be leveled refers to the choice of countries included here. We have focused only on countries that have seen populist electoral successes, to see what the change in CSR was around these particular events. A point could be made that countries where populists have contested the vote but not found success could also be interesting, if only to see the difference between populist ideas and populism in power. While this is an interesting question, our theoretical basis (as with Blake et al., 2022) is that it is precisely populism in power that can threaten CSR activities, and so we restrict ourselves to countries where populism has succeeded. 8 In addition, as noted above, the CSR data that were utilized has incredibly full and rich data for several countries, but realistically, the most CSR data that are available comes from both the United States and China. However, this reality would have meant that the inclusion of these two massive economic superpowers would have swamped the data set, making the effects observed simply driven by activities of the United States and China alone rather than of Turkey, Poland, and other, smaller countries. These superpowers were omitted from the database for just this reason, as we felt the work would have given us more China- or U.S.-specific results rather than trends that are generalizable across countries. At the same time, the mere fact that CSR data were better in the United States and China than in, say, Poland, would have induced some measure of selection bias into the empirics. We thus believe that future work should be done concentrating on these same effects in the United States and/or China alone, so as to not overwhelm any cross-country comparisons.

But even with these limitations, the empirical work that we have undertaken provides strong evidence that there is an impact on firm CSR orientation as a result of the ascendance of populism in specific regimes. Whether or not such an effect persists over time in a populist world (or, more likely, worsens) is a question for future research.

Conclusion

Corporate social responsibility takes as its basis the reality that there are many stakeholders as a party to business, and thus firms must be sensitive to their broader environment. Under a populist government, however, this myriad of stakeholders is reduced to one, the political elite of a country, who purport to speak for the people. As under other governance structures, a populist government may not (and likely does not) have the best interests of the firm at heart. Instead, populist leaders will have their own ideas on the appropriate role of business in society, including on how firms should be focusing their energies. Any broader-based stakeholder management could be seen as peripheral, including and especially CSR.

This article has examined the relationship between CSR and populism via a novel empirical examination of 13 countries who have been under populist governments. To our knowledge, this article represents the first attempt to quantify the effects of populism on CSR, and the results were consistent across models: Populism leads to changes in CSR independent of firm characteristics or underlying trends, with more populism correlated with less CSR. Even more striking, from the point of view of the varieties of populism debate, populist regimes which we classified as anti-business saw much greater declines than those which were pro-business, meaning the marriage of traditional left-wing politics and populist advocacy can (perhaps paradoxically) result in less CSR.

While we have discussed the limitations of the empirical examination above, there are additional theoretical limitations of this work that we are beginning to explore. The most pronounced is that not every type of populist government fits neatly into the definitions shown here: Assuming that the assertion by Tang (2016) and others (Perry, 2015; Zang, 2010 or K. Roth, 2017) is correct, and that China is now under a populist regime (or at least utilizing elements of populism in governance and even among the populace, see Zhang, 2020), is Xi Jinping pro-business or anti-business? Additional dimensions to our empirical definitions of populism need to be added to flesh out the continuum better, such as degree of centralization (germane for Russia and China) or ideology (one can be right-wing and anti-business, or even left-wing and pro-business). Moreover, this empirical exercise lays a beginning basis for understanding firm political responsibilities under populism, but more empiricism is both necessary and supplementary (and, it should be noted, also underway by the current authors).

Perhaps more interesting than the limitations of this work are the ramifications, which should give pause to those who support populism on the belief that it gives voice to the powerless and can help overcome “business as usual.” On the contrary, if CSR initiatives are a public good that can help to both democratize business activities and improve society, the existence of a populist party claiming to speak for the people can actually retard such development. This reality also means that firms need to be able to retool their own risk management in a populist world to understand which CSR may be threatened under populism or, alternatively (and following from Markus, 2012), which may help a firm be insulated in the event of a populist electoral victory. Indeed, as Feldmann and Morgan (2021) note, a firm might even fight back against populist pressure, defiantly maintaining some CSR activities or channeling their efforts into CPA to build a larger stakeholder base and force capitulation (if not outright regime change). Follow-on work should then also concentrate on the ways in which firms are able to circumvent populist pressure and make their CSR initiatives more impervious in a populist political environment. Given the extreme context-dependence of populist governance, it may be sufficient to provide a broader toolbox of ways in which to mitigate this new political risk. And, as noted above, we should also expand our empirical knowledge to exploring this relationship in the United States and China (as noted above). In any event, as a first attempt to understand the constraints facing firms under populism and how it translates into firm strategy, the evidence shown here regarding CSR is indicative of the issues that firms will continue to face into the future.

Finally, there are considerable implications for business decision-makers from our work. One of the most obvious implications brings up the question as to whether going with the herd (i.e., reducing traditional CSR activities and replacing them with activities more in line with populist demands) is the correct way to go. In the United States, the election of Donald Trump in 2016 led to considerable bifurcation in terms of the political activities of firms, as they became caught up in the culture wars that were a hallmark of his tenure (and continue into Biden’s). According to Edgecliff-Johnson (2022), “[b]usiness leaders increasingly find themselves in . . . unwinnable positions, caught between two sides on topics they never wanted to be debating,” but having to nonetheless come up with responses that are meaningful to their customers, shareholders, employees, and others. There are two sides to this. One is to become considerably more activist politically. For the most part this is a nonstarter with most companies, since to do so will automatically immerse it more deeply into fractious and distracting public conflicts that they are ill-suited to fight and have little chance of winning (e.g., as seen with Disney and the Florida Governor Ron DeSantis). The second is to become more “purposeful” in the sense that a company develops a more internalized and meaningful set of values that are defensible across a variety of stakeholders and is reflected in the governance of the firm (C. Meyer, 2021). The integration of purpose into the corporate structure has the benefit of being mostly a pro-active strategic act that drives decision-making, rather than a tactical reactive political move that is driven as a response to outside influences. In this sense, it reflects a need on the part of the corporation to determine what values it wants to internalize and to which it makes a public precommitment. Ultimately, the major implication would be that the firm would be choosing which side of the political equation it wants to sit, and hence its decisions become less expedient. However, in an environment of sociopolitical uncertainty, what may matter more is the ability to keep to a specific and strategic path than the ability to chop-and-change with the political winds. This would imply a diminution of the effect we see, as a firm’s CSR investments and CPA investments could be more strategic and long-term. The question is whether or not such a strategy would survive a populist government.

Footnotes

Acknowledgements

The authors wish to thank the Editors, the Special Issue Editors, and three anonymous reviewers for their encouragement and helpful comments.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.