Abstract

Scholars have long suggested that CEOs can benefit from corporate philanthropy. However, little is known about this relationship in contexts of authoritarian capitalism such as China, where the state not only uses its control of economic entities to pursue social goals but also plays a key role in CEOs’ careers. We theorize how corporate philanthropy among state-controlled firms increases the CEO’s likelihood of receiving career benefits from the state in the form of outside directorships. Outside directorships represent an important form of social capital in the Chinese context, and corporate philanthropy is an important mechanism through which social capital can be acquired. In addition, we theorize how two factors—the degree of state ownership and the number of independent directors on the CEO’s board—moderate this relationship. Analyzing a 12-year panel of state-controlled, publicly-listed firms in China comprising 6,594 firm-year observations, we find general support for our ideas. In so doing, we contribute to scholarship on the business–society relationship and corporate governance in the context of authoritarian capitalism.

Recent business and society research have begun to explore the consequences of authoritarian capitalism (Hofman et al., 2017; Sallai & Schnyder, 2021; Situ et al., 2020), a system in which older governance structures serving the interest of the state (such as intervention, and state control) persist alongside new governance structures aimed at a market economy (such as liberalization). This has led to a new class of firms that are publicly listed but still controlled by the state and therefore subject to a mix of different and potentially conflicting interests. Such firms are pervasive in many economies, accounting for instance for 62% and 38% of total stock market capitalization in Russia and Brazil, respectively (The Economist, 2012). Authoritarian capitalism is thus a topic within the wider domain of how political structures continue to affect business aims, performance, and governance.

Governments under authoritarian capitalism often use their control of economic entities to pursue social goals and thus play a key role in steering the corporate social responsibility (CSR) agenda of their firms (Dentchev et al., 2017; Y. Xu & Zeng, 2021). Authoritarian capitalism is associated with a long history of encouraging state-controlled firms to sacrifice profits to shoulder certain social burdens, such as taking on redundant workers, absorbing price distortions, and curtailing excessive executive compensation (J. Y. Lin & Tan, 1999; Markóczy et al., 2013). More recently, the Chinese government—a leading practitioner of authoritarian capitalism—has begun to encourage firms to make social contributions through CSR activities such as corporate philanthropy as a way to promote social benefit (See, 2009; Sun et al., 2021; Zhao, 2012).

The traditional (Western) agency lens frames CSR in general, and corporate philanthropy in particular, as self-serving behavior by executives at the shareholders’ expense (Barman, 2017). Yet under authoritarian capitalism, the state as the controlling shareholder often encourages such activities (Levine, 2008; Marquis & Qian, 2014; Situ et al., 2020), and thus the traditional agency perspective may not apply (Young et al., 2008). This is particularly relevant given that investigations into corporate philanthropy’s financial implications for shareholders have led to mixed results (W. O. Brown et al., 2006; Cuypers et al., 2016; Masulis & Reza, 2015). In contrast, prior research is relatively clear in showing that serving the state’s objectives can generate private benefits for executives (Firth et al., 2006; Perotti et al., 1999). Accordingly, it can be expected that the government in an authoritarian capitalism context may reward CEOs at state-controlled firms for pursuing corporate philanthropy because doing so helps the government achieve its social goals.

But how are CEOs in authoritarian capitalism rewarded for leading their firms to engage in corporate philanthropy? Because managerial compensation in firms under state control is low (Peng et al., 2015), rewards are typically non-pecuniary, such as more spacious housing, more perquisites, and greater social recognition (Firth et al., 2006; Markóczy et al., 2013; Perotti et al., 1999). In our article, we propose that an additional—and previously underexplored—way in which the state rewards CEOs for engaging in corporate philanthropy is through appointment as outside directors on the boards of other firms. Outside directors have an important corporate governance function in terms of monitoring, bringing in knowledge and expertise, and accessing resources (Mutlu et al., 2018; Peng, 2004; Shropshire, 2010). Outside directorships are also seen as a reflection of the CEO’s social standing (Belliveau et al., 1996; Flickinger et al., 2016; Sauerwald et al., 2016).

In China, where social standing and relationships are important (Jin et al., 2011; Peng & Luo, 2000; Zhu & Yoshikawa, 2016), outside directorships are considered a key component of CEO prestige and associated with more perks and power (Ting & Huang, 2018; Yan et al., 2019). Importantly, under authoritarian capitalism, the state as controlling shareholder has a key role in the appointment of outside directors (Z. Chen & Keefe, 2018). Thus, we hypothesize that by engaging in corporate philanthropy and helping the Chinese government to achieve its social objectives, CEOs of state-controlled firms curry government favor, thereby increasing the likelihood that they will be appointed as outside directors at other state-controlled firms.

In addition, we propose two factors that moderate this relationship. First, we hypothesize that the relationship between corporate philanthropy and CEO outside directorships is amplified when the state owns a larger percentage of the firm’s shares. Because a higher degree of state ownership signals greater alignment of interests between the state and the CEO (J. C. Wang et al., 2022), under these conditions the state is more likely to perceive corporate philanthropy as motivated by a desire to serve the state’s interests (as opposed to other considerations) and will reward the CEO accordingly. Second, we hypothesize that the relationship between corporate philanthropy and CEO outside directorships is attenuated when a higher number of independent directors sits on the focal CEO’s board. Because independent directors in China are expected to serve as monitors of the CEO and a counterweight to the controlling shareholder (Z. Chen & Keefe, 2018), they may be skeptical of the CEO being rewarded for currying favor by engaging in corporate philanthropy, as opposed to more “legitimate” performance reasons. As a consequence, they may be less likely to support a CEO actively engaged in corporate philanthropy.

To test these hypotheses, we analyze corporate philanthropy by publicly listed firms in China that have the state as the ultimate controlling entity. Most listed firms in China are state-controlled (Chizema et al., 2015; Mutlu et al., 2018; Peng, 2004; J. C. Wang et al., 2022). In such firms, low salaries and the corresponding focus on nonpecuniary rewards make connections to other firms particularly important to CEOs (Conyon et al., 2015; Jin et al., 2011). Outside directorships are considered a key component of CEO prestige in China and are associated with enjoying more perks and power (Ting & Huang, 2018; Yan et al., 2019). Using a 12-year sample (2003–2014) and a two-stage methodology in which we first generate a predicted value for corporate philanthropy and then test its effects on the number of CEO outside directorships, we find general support for our arguments.

Our study contributes to business and society research in two ways. First, we explore the relationship between corporate philanthropy and CEO-specific benefits in terms of outside directorships. While the Western-oriented corporate philanthropy literature focuses primarily on benefits to the firm and sees personal benefits to the CEO more in the form of warm glow or pet charities, authoritarian capitalism provides a context in which the CEOs of state-controlled firms can be rewarded for corporate philanthropy with career-related benefits. Second, we shed light on the relationship between the controlling shareholder, the firm, and the monitoring of independent directors in the context of authoritarian capitalism. Specifically, not only does greater alignment between the controlling shareholder and the CEO enhance the likelihood of the CEO reaping such rewards, but our study also shows that more independent directors on the focal CEO’s board increase that likelihood as well, when their important monitoring and dissenting function would predict otherwise. Overall, our study helps to contextualize our thinking about corporate governance (Tihanyi et al., 2014) and CSR (H. Wang et al., 2016) and reveals another potential “dark side” of authoritarian capitalism (Cheung et al., 2010).

China Under Authoritarian Capitalism

Authoritarian capitalism is a system in which concentrated government power is imposed on firms (Hofman et al., 2017; Sallai & Schnyder, 2021; Situ et al., 2020). Such power is especially strong in state-controlled firms—our focus in this article. China is a key example of authoritarian capitalism (McGregor, 2019). Corporate governance under authoritarian capitalism involves a mix of modes, whereby formerly wholly state-owned enterprises are partially privatized through listing on stock markets (Bruton et al., 2015; Peng et al., 2016). As such, older governance structures serving the interests of the state (as controlling shareholder) persist alongside new governance structures intended to protect minority shareholders (Hua et al., 2006; Peng, 2004; Young et al., 2008). In this context, independent directors have an important monitoring and dissenting function (Z. Chen & Keefe, 2018; Ma & Khanna, 2016), but their appointment is formalized by the controlling shareholder and influenced by management, leading to concerns about their independence.

Governments under authoritarian capitalism typically pursue a “double bottom line” policy, requiring state-controlled firms to shoulder social burdens alongside profitability demands (Kamal, 2010). In many Central and Eastern European economies, for example, state-controlled firms are still used to achieve social objectives such as job security (Glaser, 2019; Uhlenbruck & de Castro, 2000). More recently, authoritarian capitalist governments have begun to extend this double bottom line policy to include socially motivated investments such as corporate philanthropy in an effort to shift some of the burdens of public goods provision onto the corporate sphere (See, 2009; Zhao, 2012). For instance, the Chinese government, as part of its philosophy of fostering a “harmonious society” in which economic, social, and environmental demands are balanced, encourages state-controlled firms to “take responsibility for stakeholders and the environment” (Levine, 2008, p. 52) while subjecting them to close monitoring of cash flow and nonoperating expenses (Guo, 2009).

While state control means that firms are expected to contribute to the achievement of state objectives, it is important to note that the state only provides general guidelines on how those objectives should be achieved (Marquis & Qian, 2014). Thus, the state in China adopts a position of “endorsing” (as opposed to “mandating”) CSR activities such as corporate philanthropy (Situ et al., 2020) such that no explicit guidance is given as to which objectives should have primacy over others. To complicate matters further, state interests are themselves diverse and fragmented, representing multiple (and at times conflicting) objectives (Clarke, 2003; Globerman et al., 2011; Jia & Zhang, 2013). For instance, state-controlled firms are typically subject to demands made from different levels of government (Cheung et al., 2010; Tihanyi et al., 2019). As such, state control does not automatically imply that firms will engage in more corporate philanthropy (H. Wang & Qian, 2011).

State-controlled firms may not benefit directly from heeding the state’s calls to achieve social objectives because they already enjoy the benefits of state ownership (R. Zhang et al., 2010). Instead, heeding the state’s call for corporate philanthropy may lead to private benefits for the executive directly (Hung et al., 2012). In China, where informal elements of social standing such as status and relationships are important and pecuniary incentives weak, executives value prestigious positions in the pyramidal management hierarchy, such as outside directorships (You & Du, 2012). Because boards and board interlocks represent important conduits for influence and exchange (Conyon et al., 2015; Davis, 1996; He & Huang, 2011; Sauerwald et al., 2016; Westphal & Khanna, 2003), positions as an outside director on the board of other firms afford the CEO more influence. Moreover, the increased market competition that characterizes economic transition under authoritarian capitalism makes managers with influential positions particularly respected and valued (Peng et al., 2015; Tihanyi et al., 2019; Yan et al., 2019). In sum, outside directorships are an important means by which the state can reward CEOs for helping achieve its social goals.

Hypothesis Development

Corporate Philanthropy and CEOs

Outside the Chinese context, several studies have considered ways in which corporate philanthropy can generate benefits for CEOs (Barnard, 1997; Barnea & Rubin, 2010; Bartkus et al., 2002). Specifically, charitable causes may serve CEOs’ personal “pet interests” at shareholders’ expense, and corporate philanthropy can enhance CEOs’ entrenchment within their firms (Marquis & Lee, 2013). Yet other studies have focused more on external visibility to highlight the social recognition and admiration that philanthropic CEOs can enjoy (Petrenko et al., 2016). Indirectly, this research implies that corporate philanthropy can strengthen observers’ perceptions of CEOs’ social standing (Piazza & Castellucci, 2014). In China, there is evidence that both the public and the government see corporate philanthropy as a moral imperative and will publicly shame CEOs of less philanthropic firms for failing to exhibit social solidarity (X. R. Luo et al., 2016).

Corporate philanthropy is a valued activity in society because people generally appreciate empathic concerns and willingness to help others (Jia et al., 2019; Marquis & Qian, 2014; O’Brien & Kassirer, 2019). While individual donation decisions can be made at different levels within an organization, the firm’s overall philanthropic profile is typically ascribed to the CEO (Barnard, 1997; Muller et al., 2014; Navarro, 1988; Petrenko et al., 2016). Accordingly, given that the social approval generated through philanthropy is directed at the individual perceived as responsible for the decision (Bekkers & Wiepking, 2011), CEOs benefit in particular from the warm glow associated with corporate philanthropy (Su et al., 2016; Willer, 2009). Moreover, this approval can be expected to increase with the level of resources committed (Glazer & Konrad, 1996; Harbaugh, 1998; Olsen et al., 2003). Therefore, corporate philanthropy can be seen as a process by which the CEO commits organizational resources—“valued goods in society” (N. Lin, 1999, p. 467)—and receives admiration and respect in return (Barman, 2017). These benefits can be leveraged for positions associated with prestige and deference, such as outside directorships (Sauerwald et al., 2016).

Corporate Philanthropy and CEO Outside Directorships

In China, board appointments in state-controlled firms are the purview of the state. Appointing CEOs as outside directors may benefit the appointing firm because of the novel experiences, knowledge, and expertise that the CEO brings (Shropshire, 2010). However, the benefits of having a CEO as an outside director remain unclear (Chu & Davis, 2016; Westphal & Stern, 2006) as do the benefits to the CEO’s focal firm (V. Z. Chen et al., 2011; Ma & Khanna, 2016). Thus, director appointments are commonly made based on subjective criteria (Stern & Westphal, 2010). Because social relationships, deference, and social control are essential elements of board functioning (He & Huang, 2011; Westphal & Khanna, 2003; Withers et al., 2012), perceptions of embeddedness and influence in social networks affect the appointment of outside directors (Sauerwald et al., 2016; Stern & Westphal, 2010; Westphal & Stern, 2007).

This is particularly the case in China, where executives’ standing and influence in the pyramidal management hierarchy are critical for their ability to contribute resources (D. Chen et al., 2018; Zhong et al., 2017). Moreover, recent processes of market reform have led to increased demand for managers with such influence in the management hierarchy (Mutlu et al., 2018; Peng, 2004; Peng et al., 2015; Yan et al., 2019). Although outside directorships carry opportunity costs and are poorly compensated (Z. Chen & Keefe, 2018; Fahlenbrach et al., 2010), CEOs in China value such positions because they elevate CEOs’ standing in the managerial hierarchy, affording them more prestige, more extensive social relationships, and greater influence. Accordingly, CEOs seek ways in which to curry the favor of the controlling shareholder for the sake of perks such as career advancement (J. Chen et al., 2016). As such, prestige and influence in corporate networks may be particularly valuable to executives in authoritarian capitalist states such as China, and executives with prestige and influence are particularly valuable to state-controlled firms.

One way in which CEOs seek to curry favor and gain prestige is through corporate philanthropy. Because corporate philanthropy is both valued by the state and associated with perceptions of social embeddedness and deference (Galaskiewicz, 1989; Marquis et al., 2007), rewarding philanthropic CEOs with outside directorships makes sense because philanthropic CEOs can be expected to leverage higher quality and more extensive relationships in ways that can add value in a board setting (S. Brown & Taylor, 2015). In sum, rewarding a philanthropic CEO of a state-controlled firm with outside directorships enhances the prestige and standing of the CEO in the management hierarchy and, in so doing, enhances that of the appointing firm (Zhong et al., 2017). Therefore:

The Moderating Effect of the Degree of State Ownership

In the context of authoritarian capitalism, the state remains the ultimate controlling entity of many firms (Huang et al., 2017). However, because many such firms are also publicly listed, their shares are held to varying degrees by private investors as well. As such, the degree of state ownership of state-controlled firms averages around 40% (K. J. Lin et al., 2020). The state thus has varying degrees in the amount of say it has in state-controlled firm outcomes and its expectations of management in terms of the guidelines the firm should follow (Bruton et al., 2015; Genin et al., 2021; J. C. Wang et al., 2022). Greater state ownership implies that the firm is more dependent on the state for resources and thus that the state’s interests are more salient to firm decision makers. This is particularly the case because CEOs of state-controlled firms are employed by the state and thus their career prospects are in the hands of the state. Hence, greater state ownership signals a greater degree of interest alignment between the controlling shareholder and management (J. C. Wang et al., 2022). This creates a horizontal agency problem that is distinct from the vertical agency problem typically studied in Western countries (F. Jiang & Kim, 2020).

Although state owners do not monitor executives closely, there is still a vertical agency problem in the sense that the state as controlling shareholder is not necessarily focused on minority investors’ interests and has the tendency to use firm resources to serve its own ends and rewards executives for doing so (Young et al., 2008). Accordingly, state ownership is often associated with a host of negative outcomes, such as weaker financial performance, heavier social burdens, and more dubious loans (Bruton et al., 2015; Peng et al., 2016). This means that the state is not only concerned with effective firm financial performance but is also motivated by a range of interests, including engagement in CSR activities such as corporate philanthropy (See, 2008; Zhao, 2012). However, this engagement is more “endorsed” than “mandated” (Situ et al., 2020) such that executives retain considerable discretion in the extent to which they accommodate the state in this regard. As such, because interests are better aligned when the state’s ownership share is greater, the state is more likely to perceive the firm’s corporate philanthropy as an expression of the CEO acting in the interest of the state, as opposed to being motivated by other considerations, such as social approval or reputation gains. Consequently, CEOs are more likely to curry favor with the state through corporate philanthropy and thus be rewarded with outside directorships, when the state’s degree of ownership is high. Therefore:

The Moderating Effect of Independent Directors on the CEO’s Board

Independent directors on the CEO’s board are commonly argued to be more effective monitors than inside directors, given independent directors’ ostensibly unbiased view of the firm (Helland & Sykuta, 2005; Mutlu et al., 2018). However, this assumption is questionable, as the empirical evidence that independent directors add value to shareholders is weak, whether in China (J. Chen et al., 2011; Ma & Khanna, 2016; Peng, 2004; van Essen et al., 2012; Zhu & Yoshikawa, 2016), the rest of Asia (van Essen et al., 2012), or the United States (Dalton et al., 1998). Some scholars have even argued that monitoring is not necessarily the independent directors’ primary objective (Masulis & Mobbs, 2014). Instead, such directors are often motivated by the desire to preserve and enhance their reputations (Fama & Jensen, 1983).

Although all board members may be considered corporate elites (Johnson et al., 2011), status differences exist among board members, and board functioning is sensitive to those differences (Belliveau et al., 1996). Boards of directors have been described as a “conduit for social influences” (Davis, 1996, p. 154) in which social orderings play an important role (He & Huang, 2011; Westphal & Khanna, 2003). Independent directors are sought after because they are typically higher in the hierarchy of executives than insider board members (Johnson et al., 2011), and their presence on the board enhances the prestige of the board as a whole and the firm itself. At the same time, independent directors can exert considerable influence, for instance, by acting as a brake on the CEO. Independent directors may have an especially important monitoring function in the Chinese context (Z. Chen & Keefe, 2018), where dissenting is important for their reputation as “decision experts” (W. Jiang et al., 2016; Ma & Khanna, 2016).

Status theory suggests that higher status others may resist the “status decrements” that come with status enhancement to lower status peers (Podolny, 2005). Higher status individuals tend to hold “zero sum beliefs”—that is, an increase in status afforded to a lower-status other undermines the level of status attributed to the self (Wilkins et al., 2015). Accordingly, higher status individuals are more likely to believe that the status quo is legitimate and respond negatively to status challenges from peers (Porath et al., 2008). This is particularly the case when any such enhancements are perceived as undeserved and therefore illegitimate or not a reflection of true quality (Cao & Smith, 2021; Magee & Galinsky, 2008). In the context of our theorizing, where the status hierarchy is particularly important, independent directors may see the prospect of status-enhancing rewards to their CEOs based on actions unrelated to firm performance, such as currying favor with the state through corporate philanthropy, as a threat to their (and the firm’s) status, especially as such rewards may be detrimental to firm performance in China (F. Jiang & Kim, 2020). Therefore, independent directors in China may exert “social influences” (Davis, 1996; Sauerwald et al., 2016) through their board ties to other firms, and their connections to the controlling shareholder who appointed them, to discourage the state’s appointment of the CEO as an outside director at another firm when that reward may be seen in relation to corporate philanthropy. Specifically:

Method

Sample and Data

We test our hypotheses on a set of firms listed on the Shanghai and Shenzhen Stock Exchanges from 2003 to 2014 (inclusive). Specifically, we focus on firms with the state as the ultimate controlling entity, which form the majority of listed firms in China (Peng, 2004; D. Xu et al., 2014). This setting is particularly relevant for our study not only because prestige is important in China generally (Jin et al., 2011; Zhu & Yoshikawa, 2016) but also because executive compensation in our sampled firms is typically low (Chizema et al., 2015; Peng et al., 2015). For example, Peng and colleagues (2015, p. 129) report that in 2008 (the approximate mid-point of our sample period), the average CEO compensation (cash only) in listed firms in China was only US$52,591. However, the non-pecuniary benefits associated with prestigious positions such as outside directorships are high (Firth et al., 2006; Markóczy et al., 2013; Perotti et al., 1999).

For all state-controlled firms listed on the two exchanges during the 2003–2014 period (inclusive—11,220 firm-year observations), we searched for their total annual corporate philanthropy contributions and CEO outside directorships from annual reports and other media sources. Financial variables were drawn from the China Stock Market and Accounting Research (CSMAR) database (Z. J. Lin et al., 2009; Markóczy et al., 2013; Marquis & Qian, 2014). Missing values reduced our initial sample to 9,276 firm-year observations. Incorporating 1-year lags in our models reduced the number of potential firm-year observations to 8,002.

Dependent Variable

Following Belliveau and colleagues (1996) and Flickinger and colleagues (2016), we identified the number of outside directorships the CEO holds as reported in firms’ annual reports. CEO outside directorships is a count variable taken at the end of each calendar year (Belliveau et al., 1996). The measure took a mean of 0.9, with a standard deviation (SD) of 2.0. These values are comparable to those found in other contexts, such as an average of 1.6 directorships (SD 1.6) in the United States (Geletkanycz & Boyd, 2011) and 0.9 (SD 0.7) in Germany (Flickinger et al., 2016).

Independent Variable and Moderators

Corporate Philanthropy

To test Hypothesis 1, we searched firms’ annual reports to obtain their total amount of charitable contributions during a specific year. Because the variable is skewed, ranging from 0 to 625 million yuan (US$100 million), we took the natural logarithm of the total annual amount (+1) in accordance with prior studies (Adams & Hardwick, 1998). Research has suggested that the effects of corporate philanthropy on observers’ perceptions are a function of the absolute magnitude of giving as opposed to its relative magnitude (Glazer & Konrad, 1996; Harbaugh, 1998; Olsen et al., 2003). However, as a robustness check, we also calculated an industry-adjusted corporate philanthropy measure to account for the possibility that the industry forms a frame of reference for between-firm comparisons of corporate philanthropy amounts. The industry-adjusted measure generates results that are fully consistent with those reported here.

Degree of State Ownership

To test Hypothesis 2, we measured degree of state ownership as the percentage of shares owned by the state and its entities. This measure took a mean value of 39.5% and an SD of 15.3%.

Number of Independent Directors on the Focal CEO’s Board

To test Hypothesis 3, we measured the number of independent directors as the number of directors on the focal CEO’s board who are employed by other organizations (S. Li et al., 2015; Mutlu et al., 2018; Peng, 2004). This variable took an average value of 3.37, with a standard deviation of 0.77.

Control Variables

In all our models we accounted for a number of firm-specific factors. In line with prior research, we controlled for size, measured as the natural logarithm of total assets (K. Li et al., 2011), as well as capital intensity, measured as the ratio of total assets to total sales, to account for size and investment effects on the likelihood of CEO board appointments (Lungeanu et al., 2018). For instance, CEOs of large firms might be perceived as more skilled directors because of the size of the firms they oversee (Ferris et al., 2003). We also controlled for R&D intensity, measured as the ratio of R&D expenditure to total sales; and advertising intensity, measured as the ratio of selling, general, and administrative expenses to total sales (H. Wang & Qian, 2011), because both dimensions reflect aspects of firm strategy on which the CEO might obtain insights through board connections (Lungeanu & Weber, 2021). We winsorized both measures at the 1% level to account for extreme values. We also controlled for management ownership share, measured as the proportion of shares held by management, because the opportunity costs associated with being a director elsewhere could be higher if management is more vested in the firm.

We also controlled for firm performance as return on assets (ROA), winsorized at the 2% level to account for outliers. ROA is generally one of the most important metrics for capturing attributions of CEOs’ performance (Fitza, 2014, 2017; Quigley & Graffin, 2017) and particularly in China (Hu & Leung, 2012; Peng & Luo, 2000). Next, we controlled for leverage, measured as the ratio of total debt to total assets, to account for the firm’s risk-taking; firm age, measured as the number of years since going public (H. Wang & Qian, 2011), because the opportunity costs of directorships may be lower for CEOs of more mature firms (Fahlenbrach et al., 2010); and the firm’s overall visibility, measured as the total number of news articles per year in which the firm was referenced, because this reflects the level of social approval of the firm and its managers (Lungeanu & Weber, 2021). We did not account for tone (Zavyalova et al., 2012) because media coverage of firms, particularly those subject to state control, is rarely negative in China (You et al., 2017).

We also accounted for a number of CEO-specific factors. In the outside directorship models, we controlled for CEO duality, coded as 1 if the CEO was chair of the board (Lungeanu et al., 2018; Peng, 2004) and CEO politically connected (H. Wang & Qian, 2011; J. Zhang et al., 2016) based on CEO background information provided in annual reports. Following Fan and colleagues (2007), we considered the CEO to be politically connected if he or she was formerly an official in the government or military. We also controlled for CEO age and CEO tenure, measured in years at year-end. CEOs of above-average age or tenure are less likely to be considered for more high-status positions such as outside directorships in China (Fee et al., 2018; X. Luo et al., 2014).

We then controlled for the CEO’s corporate philanthropy media profile as a factor that may affect the CEO’s general level of admiration and approval (Petrenko et al., 2016). We calculated this measure as the number of news articles that explicitly referred to both the CEO and the corporate philanthropy divided by the total number of news items that referred to the company in the same year. Here too, we did not control for tone (Zavyalova et al., 2012). Alternately, we specified models including the raw number of news articles (not weighted for total news coverage) and found virtually identical results. We note that this measure correlates highly with the firm’s overall visibility measure and that our results are robust to the exclusion of either or both measures.

Analytical Strategy

As we are interested in explaining within-firm variance over time, we adopted fixed-effects specifications with year controls. This choice was substantiated by Hausman test results (χ2 = 50.09, p = .009). However, we also implemented the hybrid approach advocated by Certo and colleagues (2017) by which the data are separated into its within-firm and between-firm components, to allow us to more directly test whether our within-firm theorizing is applicable. In addition, in our data, endogeneity is a potential concern due to simultaneity as well as omitted factors that may affect corporate philanthropy amounts or CEO outside directorships (Semadeni et al., 2014). We addressed these concerns in part by adopting 1-year lags in all specifications and also firm fixed effects with time dummies allow us to control for time-variant and time-invariant factors that may drive the results.

However, to more robustly account for these concerns, we employed a two-stage approach in which we used a Tobit model to generate a predicted corporate philanthropy measure as our input variable for the subsequent analyses and recalculated the variance-covariance matrix to ensure that standard errors were correctly estimated (Cameron & Trivedi, 2005). A Tobit model is relevant here, given the incidence of zero values for the corporate philanthropy measure. As we aimed to address endogeneity, we needed an identification variable that is correlated with corporate philanthropy but not with the error term of outside directorships, the dependent variable in our subsequent models. We used the dummy variable state control at the local level as our identification variable. All firms in our sample are subject to a mix of ownership but are ultimately controlled by the state (D. Xu et al., 2014). However, state control can be held by government bureaus at the central, provincial, or local (municipal) level in China (Huang et al., 2017; J. C. Wang et al., 2022).

Because local ties are known to be highly important for corporate philanthropy (Crampton & Patten, 2008; Marquis et al., 2007), state control at the local level may be expected to correlate with higher levels of giving, but it is not expected to directly affect outside directorships. Given the stratification of the political hierarchy in China, although there is vertical competition within the hierarchy, each stratum has its own dynamic (D. Chen et al., 2018; Huang et al., 2017; J. C. Wang et al., 2022). Thus, there is no evidence that the market for outside directorships for firms controlled at the local level functions any differently than it does for firms controlled at the central level (Ting & Huang, 2018). Moreover, Stock-Yogo tests of instrument strength returned an F statistic of 37.88 for the outside directorship model, which is well above the 10% Wald test threshold for the relative bias in the case of limited information maximum likelihood models (F statistic 3.58). Overall, these results provide sufficient support for the strength of state control at the local level as an instrument in our analysis.

First-Stage Controls

In addition, we control for a number of factors known to predict corporate philanthropy. Leveraging Brammer and Millington (2005) and Fry and colleagues (1982), we controlled for size, measured as the natural logarithm of total assets (K. Li et al., 2011). Following Petrenko and colleagues (2016), we controlled for capital intensity by taking the ratio of total assets to total sales. We also controlled for R&D intensity, measured as the ratio of R&D expenditure to total sales; and advertising intensity, measured as the ratio of selling, general, and administrative expenses to total sales, because both have been shown to correlate with corporate philanthropy in China (H. Wang & Qian, 2011). We winsorized both measures at the 1% level to account for extreme values.

We also controlled for leverage, measured as the ratio of total debt to total assets; firm age, measured as the number of years since going public (H. Wang & Qian, 2011); slack resources, measured as the ratio of total cash flow from operations, financing, and investing activities divided by total assets (S. Li et al., 2015); and cash ratio, measured as the ratio of cash holdings to total assets. Following H. Wang and colleagues (2008) and H. Wang and Qian (2011), we controlled for firm performance as ROA, winsorized at the two-percent level to account for outliers, because profitability is an important driver of corporate philanthropy budgets. We also included a control for market performance, measured as Tobin’s Q, as an alternate measure of performance, given its links to corporate philanthropy (W. O. Brown et al., 2006).

Next, we controlled for the overall tendency to engage in corporate philanthropy. First, we accounted for the firm’s overall visibility, measured as the total number of news articles per year in which the firm was referenced, to proxy societal pressure on the firm to demonstrate social engagement. In addition, we controlled for the firm’s overall social engagement given that firms’ social endeavors need not be restricted to philanthropy alone. As no reliable, valid, established measure for social engagement exists in the Chinese context, we adopted a measure based on the “social burden” borne by the firm. Specifically, the Chinese government has a long history of encouraging—but not mandating—firms to shoulder certain social burdens in the interest of social harmonies, such as taking on redundant workers (J. Y. Lin & Tan, 1999; Markóczy et al., 2013). We operationalized overall social engagement as surplus labor, measured as the number of employees per unit asset above its industry average over the previous 2 years (Bai et al., 2006), winsorized at the 2% level.

Finally, generating a predicted variable manually as an input for our second-stage regressions offers considerable flexibility compared with existing statistical commands. However, when conducting two-stage regressions manually, it is necessary to recalculate the variance–covariance matrix to account for the unobserved nature of the predicted variable to ensure that the standard errors are correct. We followed established practices to do this (Baum, 2010; Cameron & Trivedi, 2005).

First-Stage Analysis

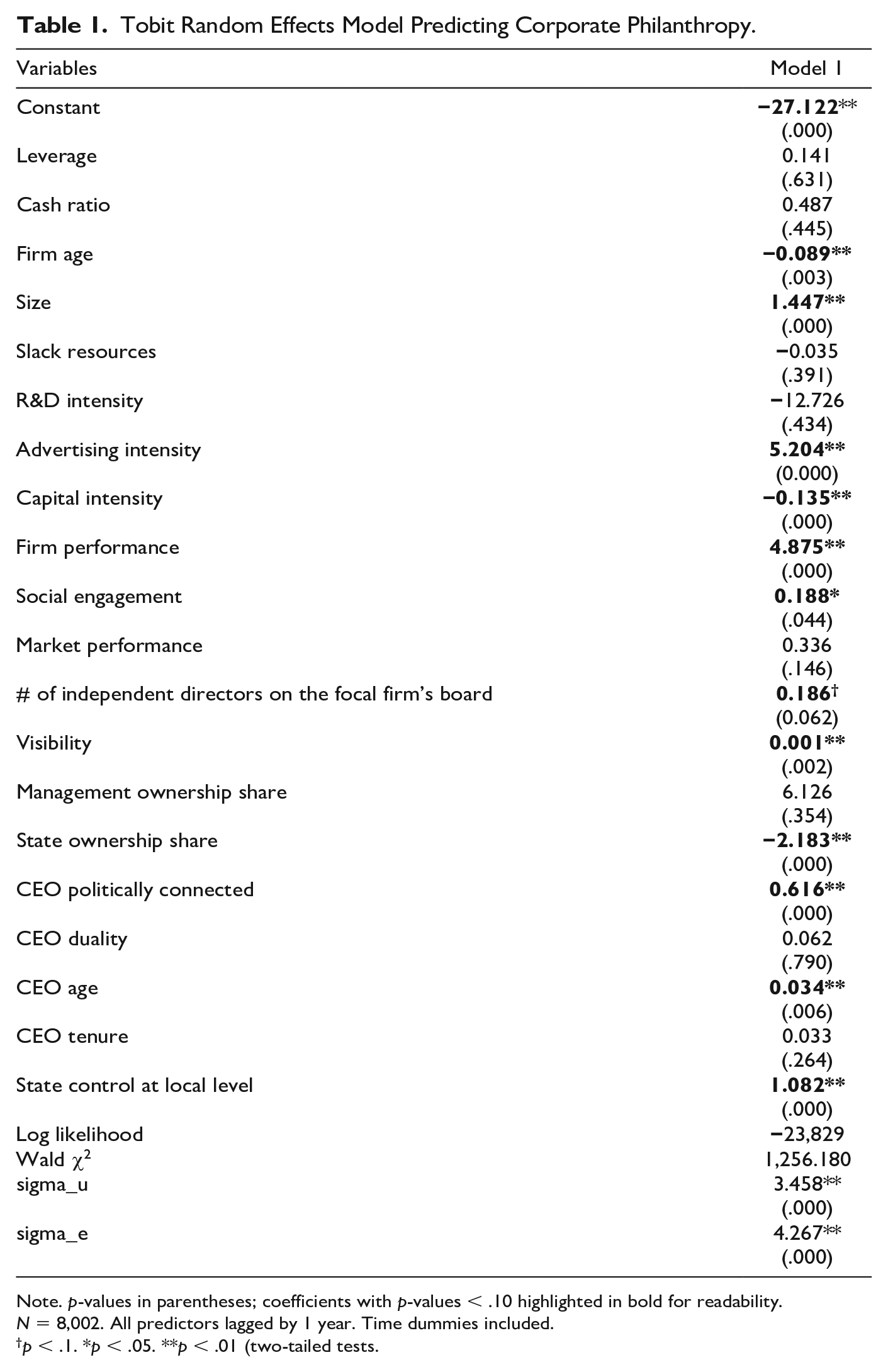

We report the results of our first-stage Tobit regression in Table 1. In addition to addressing endogeneity through a large number of controls, firm fixed effects, and 1-year lags in our models, we also examined the potential for omitted variable bias when generating our predicted corporate philanthropy measure by testing for the impact threshold of a confounding variable (ITCV). The user-generated ITCV test “-konfound-” in Stata calculates how large the impact of an omitted variable must be to affect the results (Gamache et al., 2019; Hubbard et al., 2017). To invalidate the inference of the effect of state control at the local level on corporate philanthropy, such a variable would have to correlate at 0.127 with both state control at the local level on corporate philanthropy (impact = 0.016). Alternatively, 42.9% of the estimate would have to be due to bias such that the “true” effect of 3,349 cases was actually zero.

Tobit Random Effects Model Predicting Corporate Philanthropy.

Note. p-values in parentheses; coefficients with p-values < .10 highlighted in bold for readability.

N = 8,002. All predictors lagged by 1 year. Time dummies included.

p < .1. *p < .05. **p < .01 (two-tailed tests.

In addition, we examined the partial impact of all other significant predictors in Table 1. If we consider size, for example, as the predictor with the highest impact, the ITCV test showed that for an omitted variable to invalidate its effects, such a variable would have to have an impact in excess of [0.019]. For comparison, the second highest partial impact in the ITCV analysis was [0.011] (market performance), and the third-highest partial impact in the model is <0.01 (CEO politically connected). Given the large number of controls in our model, we consider it highly unlikely that an omitted variable of such magnitude exists.

Results

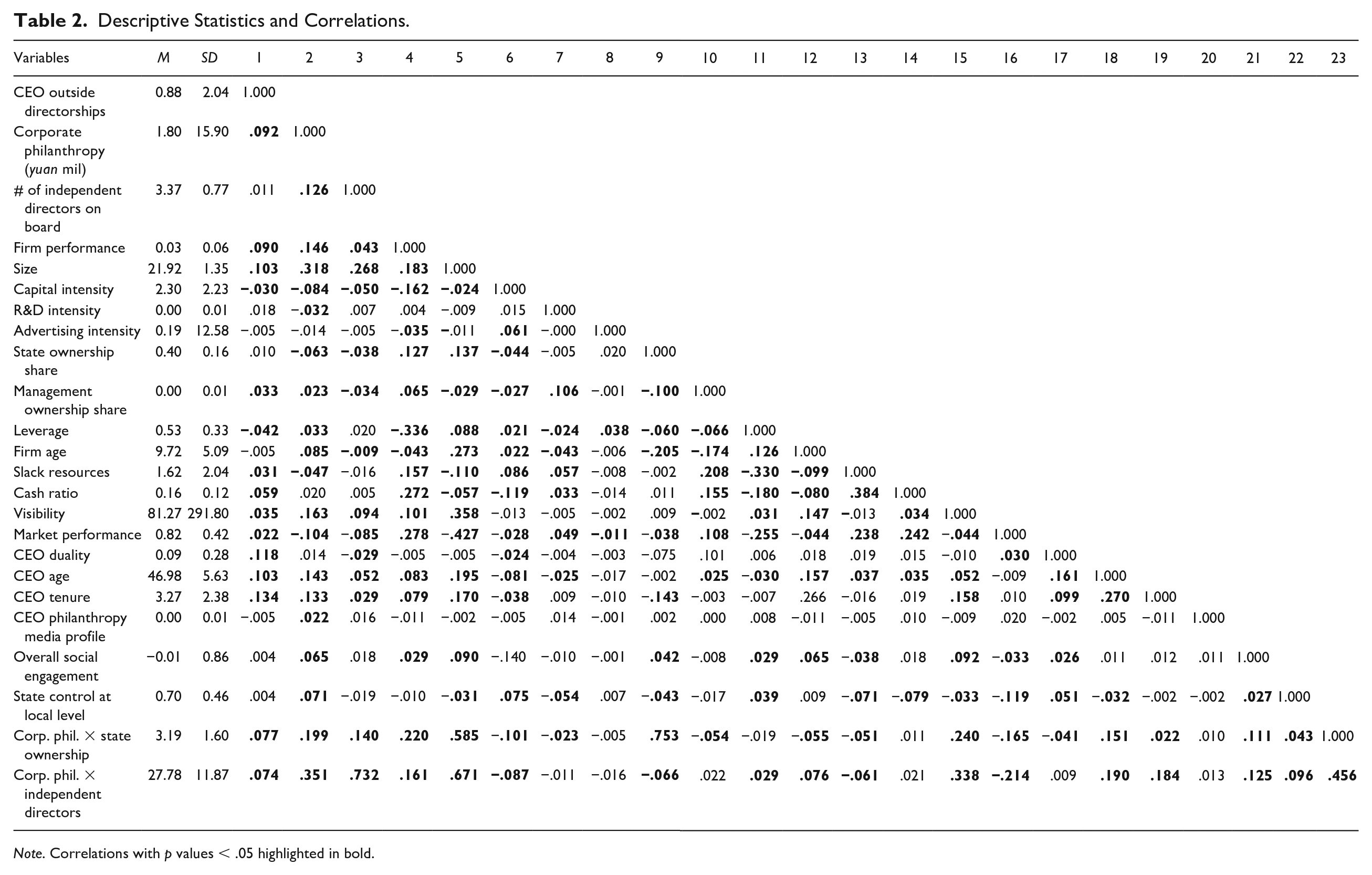

To analyze the effect of our predicted corporate philanthropy variable on CEO outside directorships, we used negative binomial regression models with firm fixed effects (xtnbreg in Stata). Negative binomial regression models are well suited to count dependent variables with potential overdispersion. Descriptive statistics and correlations are presented in Table 2.

Descriptive Statistics and Correlations.

Note. Correlations with p values < .05 highlighted in bold.

Firm Fixed-Effects Models

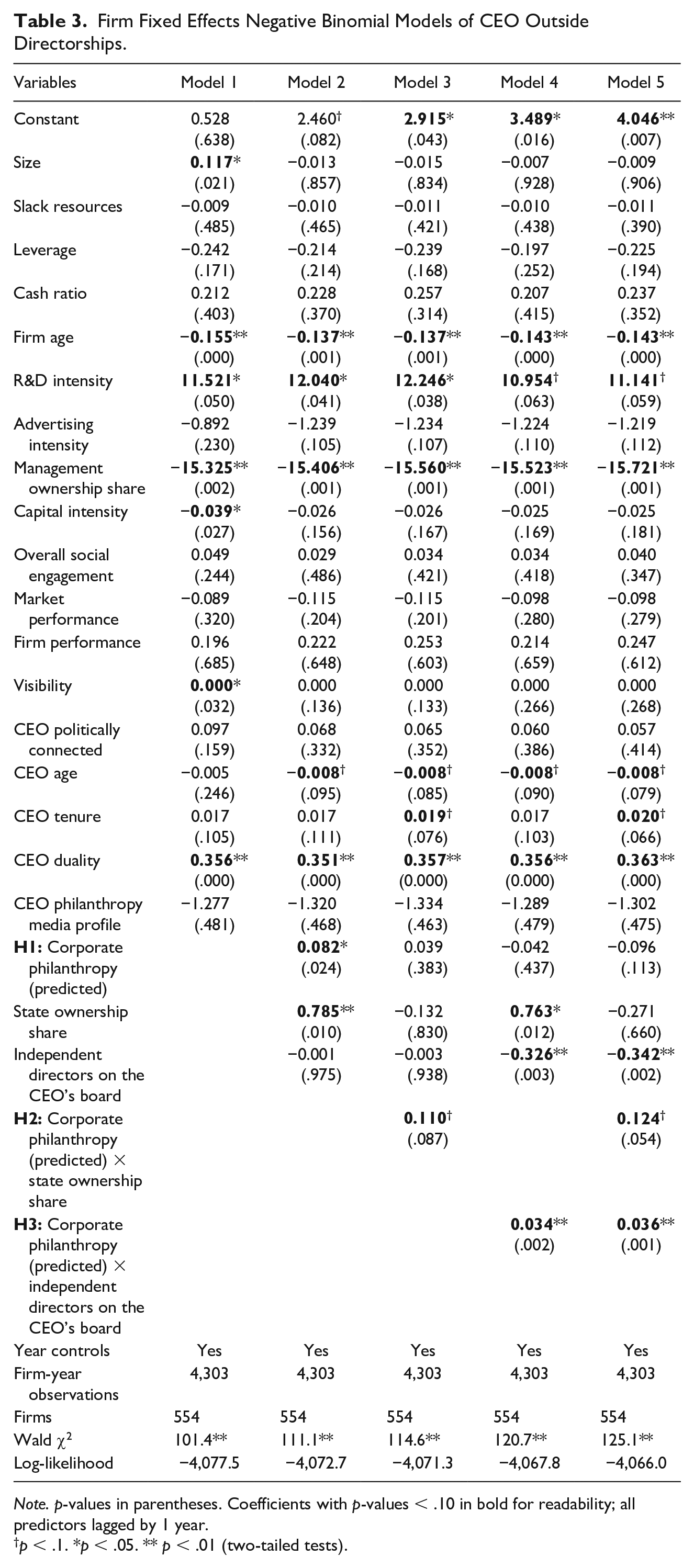

Table 3 presents the results of our negative binomial regressions with firm fixed effects and year controls. We report the effects of our controls in Model 1 (including additional controls from our first-stage model). Model 2 illustrates the main effects of corporate philanthropy and our two moderators, followed by Models 3 and 4, which incorporate the two interactions. Model 5 presents our full model. First, in Model 2, we observe a positive main effect of corporate philanthropy on the CEO’s number of outside directorships (B = 0.082, p = .024), in support of Hypothesis 1. Looking at the full model, Model 5 shows that the interaction between corporate philanthropy and the degree of state ownership is positive and marginally significant (B = 0.124, p = .054), offering some support for Hypothesis 2. Finally, Model 5 shows that corporate philanthropy’s effects on the CEO’s outside directorships are indeed contingent upon the number of independent directors (B = 0.036, p = .001). However, this result is in contrast to what we argued in Hypothesis 3. That is, we hypothesized a negative interaction between corporate philanthropy and the number of independent directors on the focal CEO’s board but find a positive relationship instead.

Firm Fixed Effects Negative Binomial Models of CEO Outside Directorships.

Note. p-values in parentheses. Coefficients with p-values < .10 in bold for readability; all predictors lagged by 1 year.

p < .1. *p < .05. ** p < .01 (two-tailed tests).

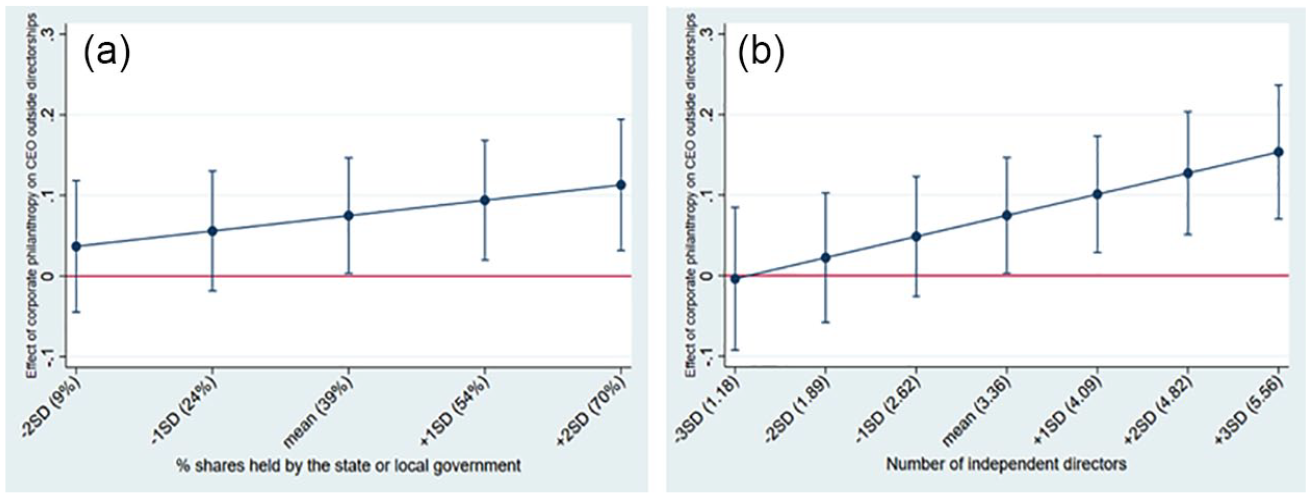

To explore these interactions more carefully, we calculated the marginal effect of corporate philanthropy on the CEO’s outside directorships across a range of values of both moderators (Busenbark et al., 2021). As there is often confusion surrounding the interpretation of interaction effects in relation to main effects, this approach helps to elucidate the values at which a moderator’s effects are significant, at the mean value of the predictor. Figure 1A and B show that the mean value of corporate philanthropy significantly affects the number of CEO outside directorships at above-average values of both moderators.

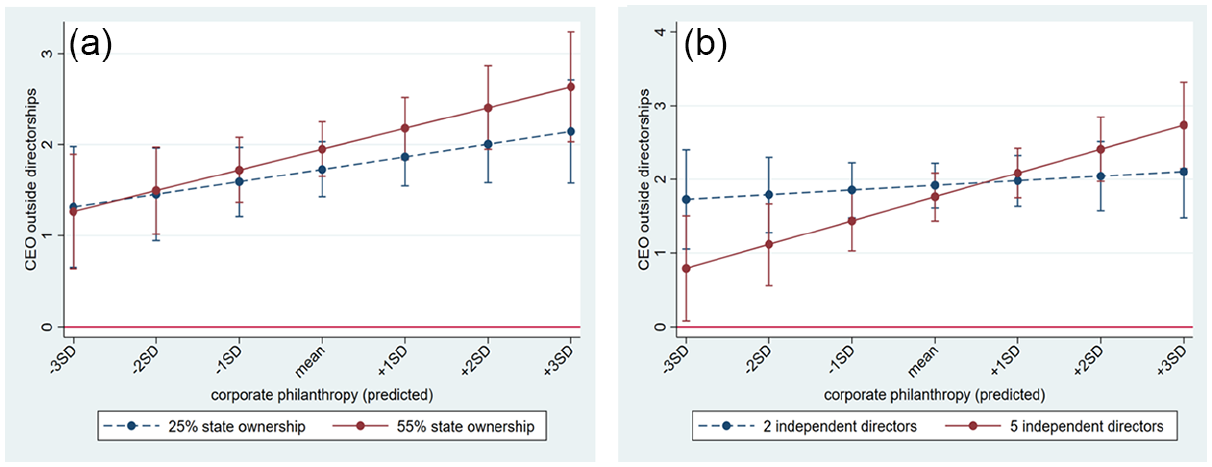

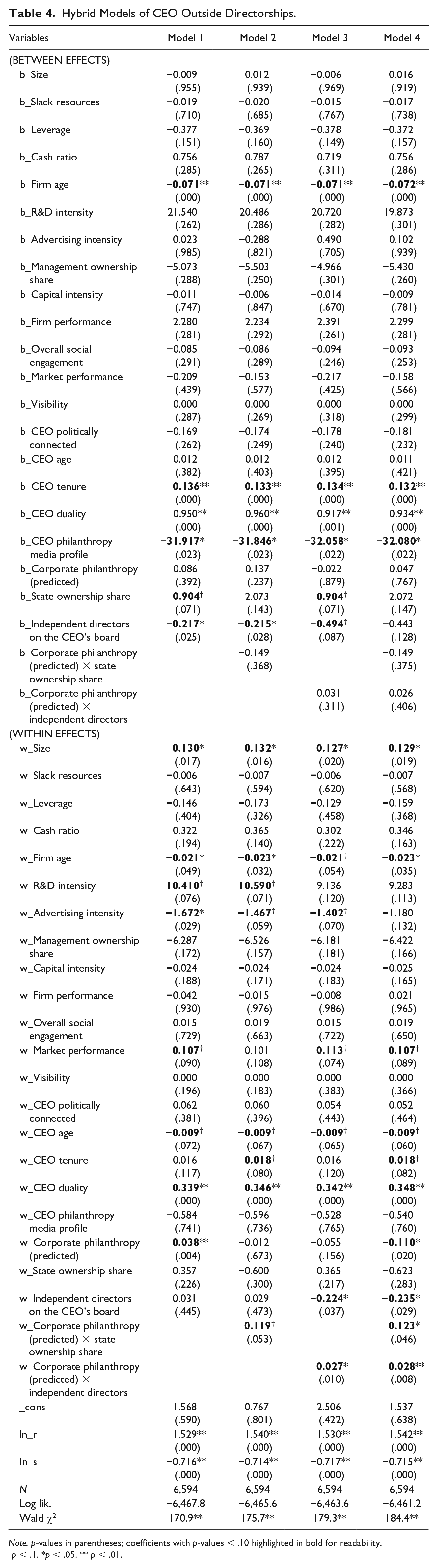

Marginal Effects of Corporate Philanthropy on CEO Outside Directorships. (A) At Varying Levels of State Ownership. (B) At varying numbers of Independent Directors on the CEO’s Board.

However, it is also important to consider the effects of the moderator across the range of values of the main predictor. Therefore, we also used the –mchange– command (Long & Freese, 2014) to generate the predicted number of outside directorships at high and low combinations of corporate philanthropy and (a) the degree of state ownership and (b) the number of independent directors with all other variables held at their means.

Consistent with Hypothesis 2, the positive interaction between corporate philanthropy and state ownership means that increasing corporate philanthropy is associated with more outside directorships, but only at above-average degrees of state ownership. Specifically, at a low degree of state ownership (−1SD), the predicted number of outside directorships at low levels (−1SD) of corporate philanthropy is 1.59, as opposed to 1.86 at high levels (+1SD) of corporate philanthropy. In other words, at low degrees of state ownership, a 1SD change in corporate philanthropy does not significantly affect the CEO’s number of outside directorships (p = .132). When the degree of state ownership is high (+1SD), however, the predicted number of outside directorships at low levels (−1SD) of corporate philanthropy is 1.72, and at high levels (+1SD) of corporate philanthropy 2.18. These values are statistically different, such that at a high degree of state ownership, a 1SD change in corporate philanthropy significantly affects the CEO’s number of outside directorships (p = .013). This is consistent with the ramifications of Figure 1A.

Similarly, the positive interaction between corporate philanthropy and the number of independent directors on the focal CEO’s board means that corporate philanthropy’s effects on the number of outside directorships hold only at values of the moderator above the mean. In other words, when the number of independent directors is low, the predicted number of outside directorships at high (+1SD) levels of corporate philanthropy (= 1.85) is not statistically different from the number of outside directorships at low (−1SD) levels of corporate philanthropy (= 1.98). That is, at low numbers of independent directors, a 1SD change in corporate philanthropy is statistically non-significant (p = .518). However, at high (+1SD) numbers of independent directors on the focal CEO’s board, the predicted number of outside directorships at low levels of corporate philanthropy is 1.44, versus 2.09 at high levels of corporate philanthropy. In other words, at high numbers of independent directors on the focal CEO’s board, a 1SD change in corporate philanthropy is statistically significant (p = .002). To illustrate these effects, we plot the predicted values for our dependent variable across the range of corporate philanthropy, at high and low values of the moderators, in Figure 2A and B.

Moderation of Corporate Philanthropy’s Effects on CEO Outside Directorships. (A) At High and Low Degrees of State Ownership. (B) At High and Low Numbers of Independent Directors on the CEO’s Board.

As Figure 2A implies, the slope of the graph at a high degree of state ownership is statistically different from zero, while the slope of the graph at a low degree of state ownership is not. Figure 2B shows similar relationships. However, we reiterate that we hypothesized a negative interaction between corporate philanthropy and the number of independent directors on the focal CEO’s board. The results presented earlier suggest a different dynamic: At high levels of corporate philanthropy, having many independent directors on the board is conducive to the CEO’s chances of obtaining outside directorships. At low levels of corporate philanthropy, many independent directors on the board have the opposite effect. This suggests that instead of acting as a brake on the state’s ability to reward the CEO for donating generously to help the state achieve its social objectives, independent directors endorse such rewards.

At the same time, the predicted number of outside directorships (= 1.44) is lowest when corporate philanthropy levels are low and the number of independent directors is high. This suggests in fact that more independent directors only act as a brake on the CEO’s ability to gain rewards for corporate philanthropy when CEOs give too little. Therefore, in contrast to our hypothesized countereffects, the results presented here indicate that the state as controlling shareholder and the independent directors on the board operate in concert, by rewarding CEOs who engage in high levels of corporate philanthropy, and punishing CEOs who do not. As such, our findings suggest that independent directors as a part of the bundle of corporate governance mechanisms in China may not be conducive to the monitoring of managers and controlling shareholders (Mutlu et al., 2018; Yoshikawa et al., 2014).

Hybrid Approach

We use firm fixed-effects models in our regressions to isolate within-firm effects over time. However, the data—given the incorporation of interaction terms—also contain meaningful information on between-firm differences. To examine these effects in isolation in a simultaneous analysis, we adopted the hybrid approach recommended by Certo and colleagues (2017) to identify whether the effects hypothesized are truly within-firm. The hybrid approach splits each value of each independent variable per firm into two variables: (a) a centered variable (

Hybrid Models of CEO Outside Directorships.

Note. p-values in parentheses; coefficients with p-values < .10 highlighted in bold for readability.

p < .1. *p < .05. ** p < .01.

Discussion

In the context of China’s authoritarian capitalism, we make and substantiate the case that corporate philanthropy helps CEOs secure outside directorships. Moreover, we show that these effects are contingent upon the number of independent directors on the focal CEO’s board, but not upon the firm’s financial performance.

Contributions

Overall, two contributions emerge. First, we contribute to an understanding of the relationship between CSR activities such as corporate philanthropy and CEO-specific benefits in the context of authoritarian capitalism (Hofman et al., 2017; Sallai & Schnyder, 2021; Situ et al., 2020). Specifically, we establish how corporate philanthropy by CEOs of state-controlled firms can generate CEO-specific career benefits in the form of outside directorships. Given the pervasive government influence in authoritarian capitalism (Glaser, 2019; McGregor, 2019), we find that corporate philanthropy, as a socially valued activity that is encouraged by the controlling shareholder, enhances the likelihood of CEOs of state-controlled firms attaining outside directorships. The notion of CEO-specific benefits is particularly important in contexts where financial compensation is weak but non-pecuniary perks are pervasive (Markóczy et al., 2013; Perotti et al., 1999). Our article thus extends the notion that corporate philanthropy leads to tangible private benefits for CEOs (Barman, 2017; Barnard, 1997; Galaskiewicz, 1989) to include professional benefits such as outside directorships. In so doing, we contribute to the debate on executive patronage in business and society research (Leutert, 2018), and broaden our view on the effects of political intervention on the relationship between business and society.

Second, we contribute to research on corporate governance under authoritarian capitalism. China remains on the threshold between old and new systems such that older governance structures designed to serve the interests of the state and its agents persist alongside new governance structures intended to protect shareholders (Hu & Sun, 2019; Hua et al., 2006; Mutlu et al., 2018; J. C. Wang et al., 2022; Young et al., 2008). Where the controlling shareholder “endorses” CSR activities such as corporate philanthropy (Situ et al., 2020) that in the Western context are positioned as agency risks (W. O. Brown et al., 2006; Masulis & Reza, 2015), we show how this endorsement can affect the configuration of corporate governance of state-controlled firms (Yoshikawa et al., 2014). As CEOs in China accumulate outside directorships, this changes the nature of board interlocks and information flows between firms (Shropshire, 2010), and therefore can have real and tangible consequences for firms specifically as well as for the business–society nexus more generally (Dentchev et al., 2017; Hofman et al., 2017; B. Li et al., 2022; Sallai & Schnyder, 2021; Zaman et al., 2022). Overall, our findings reveal a horizontal agency problem that reflects a novel “dark side” of authoritarian capitalism (Cheung et al., 2005, 2010).

Managerial and Policy Implications

In terms of managerial implications, first, our results substantiate the long-asserted but underexplored claim that corporate philanthropy leads to CEO-specific career outcomes. In the context of authoritarian capitalism, we show that when state-controlled firms have a greater percentage of state ownership and a greater number of independent directors on the board, CEOs are better able to leverage their higher levels of giving to obtain outside directorships. For CEOs at state-controlled firms, it seems reasonable to expect that their endeavors to promote corporate philanthropy (and potentially other CSR activities) would be rewarded by more outside directorships. To the extent that CSR activities are to be encouraged by governments in authoritarian capitalism, then such a link would be widely practiced.

However, for a given CEO, the number of outside directorships cannot be too large (Chu & Davis, 2016). A CEO eager to maximize the number of outside directorships can become distracted from the core tasks of effectively managing the focal firm. Also, firms appointing such a CEO as an outside director may end up having an individual who is “over-boarded,” not doing adequate “homework” before coming to meetings, and not delivering the value that the appointing firms expect. Given the tendency of CEOs to be interested in acquiring outside directorships, a useful piece of policy advice is to limit the number of outside directorships a CEO at a state-controlled firm can hold.

Future Research Directions

How firms function under authoritarian capitalism is a relatively underexplored topic in business and society research (Hofman et al., 2017; Sallai & Schnyder, 2021; Situ et al., 2020; J. C. Wang et al., 2022). Future research can investigate how specific features of corporate philanthropy or economic contexts matter to the relationships we investigate here. The form corporate philanthropy takes—such as employee volunteering versus goods in-kind (Muller et al., 2014), or the channel through which it is distributed, such as a corporate foundation (Petrovits, 2006)—may affect whether it generates benefits to the CEO. Scholars can explore whether the share of donations made to government-affiliated charities affects the likelihood of outside directorships differently from donations to non-affiliated charities (J. Zhang et al., 2016). Similarly, additional CEO-specific characteristics may matter beyond those incorporated in our analysis (Lungeanu & Weber, 2021). For instance, expressions of passion have been shown to lead to conferrals of prestige (Jachimowicz et al., 2019), and thus future research can examine how CEOs who are passionate about their firms’ corporate philanthropy engagement may attain even more outside directorships. Finally, we look at China only, and how our findings can be generalized to other contexts of authoritarian capitalism and beyond remains to be explored. Given the pervasive and increasing tendency for the state to mix with business around the world more generally, our research suggests a broader investigation of the dynamics studied here is warranted.

Conclusion

Corporate philanthropy is one of the least understood mechanisms through which CEOs can obtain professional career-related benefits. Our findings reveal that in the context of authoritarian capitalism, corporate philanthropy—as a manifestation of currying favor with the state—can improve CEOs’ chances in attaining more outside directorships. The state as a controlling shareholder endorses corporate philanthropy and is in a position to reward ingratiating and generous CEOs, and independent directors on the focal CEO’s board appear to sanction such rewards. Corporate philanthropy under authoritarian capitalism, therefore, has important ramifications for the director labor market, for corporate governance, and for the business-society interface.

Footnotes

Acknowledgements

We would like to thank Flore Bridoux, In-Mu Haw, Ilir Haxhi, Jordi Surroca, Wenming Wang, and Yang Yi for helpful comments and suggestions on earlier versions of the manuscript. We are also grateful to Yunhao Dai, Yang Yi, and Weijie Zhao for helping with data collection. We also acknowledge funding of this research provided by Hong Kong Baptist University.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.