Abstract

Research on the implementation of corporate social responsibility (CSR) has revealed the critical role of CSR departments vis-à-vis functional departments. While both CSR and functional departments influence CSR implementation, the question of how they work together remains underexamined. We address this question by mobilizing and merging two complementary yet separate perspectives on CSR implementation: “coordination” and “enactment.” Building on a comparative case study involving seven large Swiss financial institutions that have established CSR departments and implemented CSR to varying extents, we inductively derive six courses of actions conducing to CSR implementation, involving both coordination and enactment. We distinguish between four courses of actions in the CSR departments (centralizing, coalescing, orchestrating, and consulting) and two courses of actions in the functional departments (decentralizing and tailoring). As our data suggest that coordination and enactment work in tandem, we capture these insights in a model of CSR implementation as coordinated enactment. Our research contributes to the literature by explaining how CSR departments and functional departments enact and simultaneously coordinate CSR at a particular implementation stage, thus illuminating how and why the variance in CSR implementation occurs.

Keywords

While external demands made by stakeholders are critical drivers of corporate social responsibility (CSR) implementation in companies (Delmas & Toffel, 2008), a profound understanding of CSR implementation requires intraorganizational analysis (Jacqueminet, 2020; Osagie et al., 2019). To emphasize the intraorganizational dimension, we define CSR implementation as the integration of social, environmental, and ethical issues into companies’ “strategies, structures and procedures [. . .] within and across divisions, functions [and] value chains” (Wickert et al., 2016, p. 1170).

In the literature that adopts an intraorganizational perspective on CSR implementation (Acquier et al., 2011; Baumann-Pauly et al., 2013; Delmas & Toffel, 2008), researchers have emphasized the role of CSR departments (Hunoldt et al., 2020; Kok et al., 2019; Risi & Wickert, 2017), which are increasingly being established in large companies to manage CSR implementation (Lindgreen et al., 2009; Wickert & Risi, 2019). CSR departments perform a special function because they “filter” external demands for CSR (Delmas & Toffel, 2008; A. Hoffman, 2001) to a company’s functional departments, which ultimately implement CSR in their operations (Wickert & de Bakker, 2018).

However, functional departments also significantly influence whether and how CSR is implemented. Large companies are usually diversified and structured into different functional departments, each with specific staff (e.g., accounting, human resources, and procurement) and operational tasks (e.g., manufacturing, logistics, and sales; see Greenwood & Hinings, 1996). Prior research has shown that given that CSR affects core business operations, the involvement of functional departments is critical for its implementation (Delmas & Toffel, 2008). Functional departments influence overall internal decision-making about CSR implementation (Crilly et al., 2012) and can independently implement CSR in their respective practices and procedures (Jacqueminet, 2020).

However, while it has been acknowledged that both CSR and functional departments influence CSR implementation, the question of how they work together remains underexamined (Onkila & Siltaoja, 2017; Wickert & de Bakker, 2018). Understanding this is vital because comprehensive implementation implies that CSR is not executed within CSR departments but is instead embedded in a company’s various functional departments (Kok et al., 2019; Wickert et al., 2016). Studying how these departments work together could illuminate their roles in enacting strategic and operational aspects of CSR implementation and how coordination can be achieved for coherent implementation across a company’s various functions. Furthermore, such insights can help to explain variance in how comprehensively companies implement CSR as this may depend on how effectively both types of departments work together during CSR implementation. This is important because although external pressures increasingly require companies to engage in CSR, evidence indicates that companies still vary significantly in how they implement it (Baumann-Pauly et al., 2013; Bondy et al., 2012; Risi, 2020). A closer examination of the intraorganizational dynamics of CSR implementation is thus warranted. Our research question asks,

How do CSR departments and functional departments work together to implement CSR?

To answer this question, we combine two complementary yet separate perspectives on CSR implementation. On the one hand, research has shown that CSR implementation can be understood as enactment, which is defined as “a combination of strategies, processes and structures aimed at promoting first commitment to the practice and then its inclusion in the day-to-day activities” (Vigneau, 2020, p. 12; see also, Bondy et al., 2012; Maon et al., 2009; McNamara et al., 2017; Miska et al., 2016). While the enactment view underscores that CSR must progress from commitment to inclusion, it fails to specify how enactment is shared and distributed among the CSR department and other functional departments. On the other hand, research has shown that CSR implementation involves coordination among those departments tasked with implementing it (Asmussen & Fosfuri, 2019; Durand & Jacqueminet, 2015; Wickert et al., 2016). Given the complexity of CSR implementation, companies need to ensure its proper coordination, which is defined as the “managerial attempts to ensure the efficient and effective operation of the organization’s functions in line with its objectives” related to CSR (Wickert et al., 2016, p. 7). However, research on the coordination of CSR implementation has failed to specify how coordination between the CSR department and functional departments is achieved and depicts coordination activities as relatively stable and disconnected from how advanced CSR implementation is in a given company.

We approached these theoretical limitations via a qualitative multiple-case study of large Swiss financial institutions, each of which has implemented CSR to varying degrees. Our data set includes primary data from interviews with members of CSR and functional departments and secondary data such as CSR reports and internal documents from the case companies.

The analysis of our empirical data shows how CSR departments and functional departments work together to implement CSR and that this varies depending on the stage of implementation a company is at. We present six courses of actions conducive to CSR implementation involving either coordination or enactment. We distinguish between four courses of actions in the CSR department (centralizing, coalescing, orchestrating, and consulting) and two courses of actions in the functional departments (decentralizing and tailoring).

Because our data suggest that coordination and enactment work in tandem, we then capture these insights in a model of CSR implementation as coordinated enactment, which we define as a combination of strategies, processes, and structures aimed at promoting first commitment to CSR and then its inclusion in day-to-day activities to ensure the efficient and effective operation of the organization’s functions in line with its objectives in relation to CSR. Our model suggests that the better the involved departments are able and willing to master a particular course of actions, the more likely they will be to advance to the next stage of CSR implementation, thus illuminating how and why the variance in CSR implementation occurs. In this sense, and in the context of our research, we understand mastery to be a company’s ability to control a particular course of action.

Our model contributes to the CSR implementation literature by unpacking the underinvestigated relationship between the CSR department and functional departments. It shows how these departments enact CSR at a particular stage of CSR implementation and explains the simultaneous coordination between them depending on the respective stage. We also highlight the need to pay closer attention to “non-CSR” functions to understand CSR implementation as prior work has primarily focused on the role of CSR managers and departments (Hunoldt et al., 2020; Osagie et al., 2019; Wickert & de Bakker, 2018) at the expense of non-CSR departments that execute CSR. Our research also contributes to the understanding of internal variance in CSR implementation, which is important in light of the institutionalization of CSR that elicits increasingly uniform and standardized responses by companies.

Theoretical Background

Implementation of Corporate Social Responsibility

Research on CSR implementation has scrutinized the integration of environmental, social, and ethical issues into organizational practices and procedures and typically depicts CSR implementation as a sequence of successive stages (Acquier et al., 2011; Baumann-Pauly et al., 2013; Maon et al., 2010; Mirvis & Googins, 2006). For example, Bondy et al. (2012) examined the various practices and procedures in which companies engage at the different stages of CSR implementation ranging from nascent to intermediate to mature. Similarly, Mirvis and Googins (2006) suggest that companies begin with an elementary understanding of CSR, become more engaged over time, innovate, integrate CSR, and ultimately transform how they do business. More generally, while studies of CSR implementation differ in the exact content, number, and scope of the stages they depict, they tend to share an idealized conception of CSR implementation in which a company progresses, though not necessarily smoothly, through multiple stages toward increasingly mature stages of CSR.

The CSR implementation literature highlights the importance of enactment (McNamara et al., 2017; Miska et al., 2016; Vigneau, 2020). Recently, for example, Vigneau (2020) demonstrated that enactment encompasses a combination of strategies, processes, and structures for initially fostering a commitment to CSR and then incorporating it into daily activities. The enactment perspective emphasizes the processual character of CSR implementation by describing, in sequence, first the commitment to CSR and then the incorporation of this commitment into daily activities (Bondy et al., 2012; Maon et al., 2009). This perspective offers linear frameworks of CSR implementation that cover the arc from a company’s initial lip service to CSR to the homogeneous entrenchment of environmental, social, and ethical aspects across an organization. While such research depicts how CSR homogeneously unfolds once a commitment to implement CSR has been made, it does not capture how enactment is shared and distributed among departments inside a company seeking to implement CSR (Vigneau, 2020).

Another line of research has shown that CSR implementation involves a great deal of coordination (Asmussen & Fosfuri, 2019; Durand & Jacqueminet, 2015; Wickert et al., 2016). The coordination perspective suggests that companies engaged in CSR often face coordination issues when seeking to ensure the coherent and company-wide application of activities to achieve common objectives, and this is particularly relevant for companies that have largely decentralized activities across departments, functions, and value chains (Asmussen & Fosfuri, 2019). However, research that has emphasized the need for coordination in CSR implementation has not shown how coordination between the CSR and functional departments is achieved and has depicted coordination activities as relatively stable and disconnected from how advanced CSR implementation is in a given company (Asmussen & Fosfuri, 2019; Durand & Jacqueminet, 2015; Wickert et al., 2016).

In summary, research shows that both enactment and coordination are relevant to CSR implementation. Nevertheless, the complementarity of these simultaneously occurring and mutually interdependent courses of actions linked to CSR vis-à-vis functional departments remains a significant oversight in the literature and complicates the current understanding of how the CSR department and involved functional departments share the enactment and coordination of CSR at a particular stage of CSR implementation.

The Role of CSR Departments in CSR Implementation

A growing strand of research has focused on CSR managers and their departments (Hunoldt et al., 2020; Kok et al., 2019; Lindgreen et al., 2009; Risi & Wickert, 2017). In many large companies, these departments have been created as separate units and are formally tasked with ensuring the incorporation of a formal CSR commitment into corporate activities and the alignment of a company’s functions and operations with this commitment.

CSR departments perform a critical function by enacting and coordinating CSR internally because they serve as a “filter” or intermediary between external demands for CSR (A. Hoffman, 2001) and a company’s functional departments, which ultimately execute the practices and procedures in line with these demands. For example, Acquier et al. (2011) suggest that CSR departments mediate “between top management, the company’s external environment, and middle managers from the operating divisions,” fostering initial commitment to CSR, incorporating CSR practices into the organization, and ensuring that corporate functions follow the CSR strategy (p. 233). Similarly, Wickert and de Bakker (2018) highlight the importance of relationships between CSR and non-CSR departments in an organization because, after the initial commitment, CSR needs to be incorporated into the operations of functional departments while the CSR department ensures the effectiveness and efficiency of those same operations in line with the CSR strategy.

In conclusion, we know from prior work that CSR departments play a crucial role in initially fostering commitment and ensuring the effectiveness and efficiency of their operations under CSR. However, the literature lacks explicit attention to a company’s non-CSR functions that must respond to the efforts of the CSR department to implement CSR as well as the CSR department’s precise role in shaping CSR vis-à-vis non-CSR departments (Onkila & Siltaoja, 2017; Wickert & de Bakker, 2018). Given that CSR practices and procedures are ultimately executed in functional departments, attention to this oversight is vital.

The Role of Functional Departments in CSR Implementation

The literature recognizes the internal complexity of organizations, describing a “mosaic of groups structured by functional tasks” (Greenwood & Hinings, 1996, p. 1033), including functional departments such as accounting, human resources, and procurement. These functional departments have a critical influence on whether and to what extent their company actually incorporates an initial public CSR commitment into operations.

Functional departments are crucial for CSR implementation because within large organizations, various functional departments have varying degrees of influence on overall internal decision-making about CSR implementation (Crilly et al., 2012). Functional departments influence CSR implementation because they are not “passive recipients of demands for implementation” but “can take initiatives and implement a practice through unique actions or increase their practice implementation extent” (Jacqueminet, 2020, p. 184).

Overall, the limited attention given to how CSR and other functional departments work together in implementation is a critical oversight because implementation that affects the core business and is not a mere symbolic exercise cannot be executed within a standalone CSR department but must be embedded in various functional departments throughout an organization (Wickert et al., 2016). This in turn requires the enactment of the implementation by both types of departments and coordination between them. The current study explores how this is manifested in organizational practices. The following chapter explains our empirical setting and research methods.

Method

To understand how CSR departments and functional departments work together to implement CSR, we applied an inductive multiple-case study approach (Yin, 2017). For the data analysis, we drew on grounded theorizing (Gioia et al., 2013; Glaser & Strauss, 1998). This method was appropriate for our research interest because it has proven helpful in researching multiple cases (Chandra, 2017) and is oriented toward inductive theory building (Risi & Wickert, 2017).

Sampling Strategy and Research Context

We selected seven large companies in the Swiss financial services industry (each company had at least 1,700 employees). We chose large companies because they are more likely to be functionally differentiated (Blau, 1970; Williamson, 1967) and have a CSR department. All of the companies selected for this study had a standalone CSR department, and each leadership team had made a commitment to implement CSR throughout their organization.

The Swiss context was an appropriate setting for our research because many companies headquartered in Switzerland have or are set to develop a broad portfolio of CSR-related organizational practices (Baumann-Pauly et al., 2013). Several Swiss financial services companies are considered to have achieved advanced CSR implementation, as evidenced by various rankings. However, not all companies in the industry are equally advanced, and research has indicated significant heterogeneity in stages of CSR implementation among Swiss banks and insurance companies (Risi, 2020).

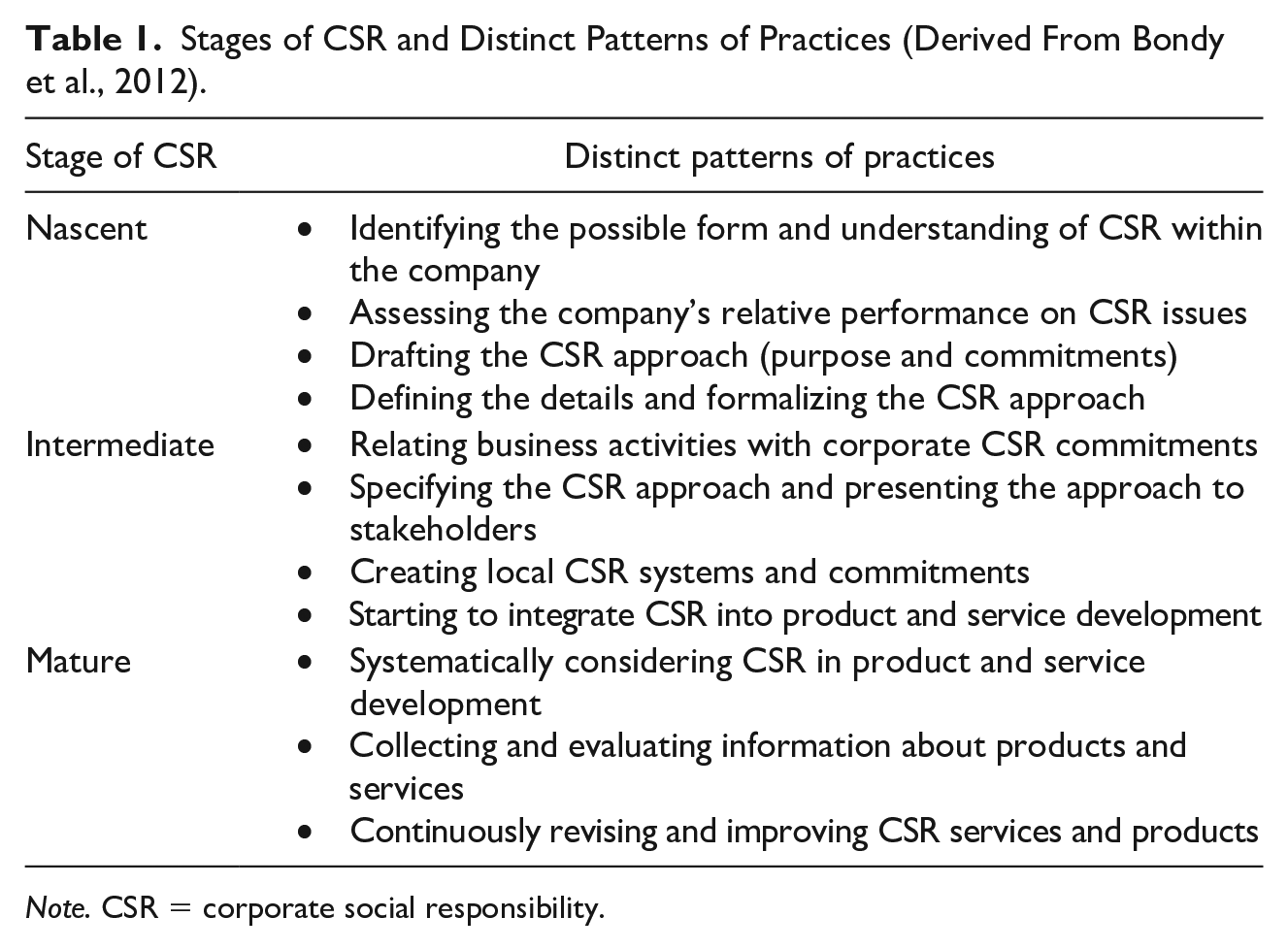

To answer our research question, our sampling strategy needed to ensure that we study both companies that had already developed CSR practices in several functional departments and others that had just established a structurally separated subunit in charge of CSR (i.e., a CSR department). This is because, following insights from some preliminary and informal interviews with field experts before this research project, we expected that how the CSR and functional departments worked together was likely to vary depending on the implementation stage. To capture and compare such variance in our sample, we consulted publicly available sources of potential case companies (including annual reports, CSR reports, codes of conduct, and corporate websites) and mirrored our preliminary insights into CSR stages against established CSR implementation frameworks given our knowledge of the literature. Next, we based the selection of actual case companies on prior research that has described CSR implementation as a sequence of successive stages (Acquier et al., 2011; Baumann-Pauly et al., 2013; Bondy et al., 2012; Maon et al., 2009). Here, we specifically drew on the work of Bondy et al. (2012), who offer a comprehensive implementation framework based on distinct patterns of activities that span from nascent to intermediate to mature CSR implementation (see Table 1).

Stages of CSR and Distinct Patterns of Practices (Derived From Bondy et al., 2012).

Note. CSR = corporate social responsibility.

Accordingly, in our study, we distinguish between nascent, intermediate, and mature CSR. At the nascent stage, the company identifies what CSR means and which of its activities are related to CSR and compares its own CSR record to that of its competitors. Furthermore, the company designs its CSR approach, defines the form its commitments will take, and compiles information about how it will meet those commitments. Once these steps have been taken, a company might move to an intermediate stage during which the company creates and adjusts relationships between its business activities and commitments, specifies the CSR approach based on the previously formulated commitments, and presents the specified approach to selected stakeholders. Furthermore, the company creates local CSR systems and commitments and begins taking CSR into account when developing services and products. Some companies then move to a more mature stage at which they have mostly integrated CSR issues into the development and provision of their products and services. Furthermore, at the mature stage, a company gathers information about the performance of those products and services and analyzes this information. In addition, the company continually revises its CSR-compliant services and products by incorporating the results of past analyses into the next cycle of improvement (see Bondy et al., 2012).

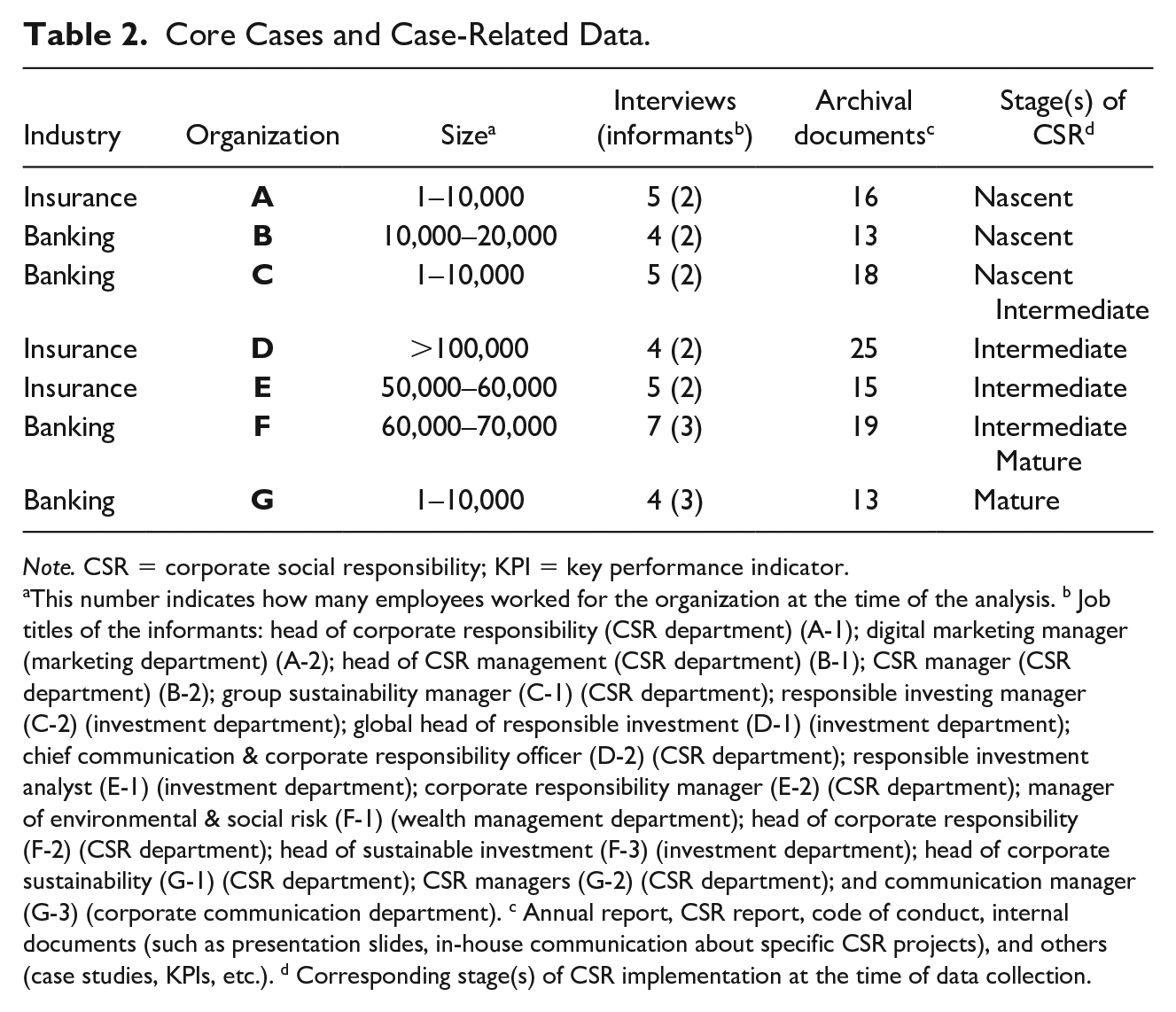

We sampled the case companies to capture variance in all three stages of CSR (Table 2 indicates the stage(s) each company had reached at the time of data collection). As it takes many years or even a decade for a large company to progress through all stages of CSR implementation (Baumann-Pauly et al., 2013; Vigneau, 2020), we selected companies to allow for at least two cases per stage and identify constraints preventing a company from moving from one stage to the next (see Table 2). While this allowed for cross-stage comparison, we could also rely on cross-case triangulation as there was more than one company in every CSR stage. Two companies in our sample even moved from one stage to the next during our observation period (i.e., Company C moved from nascent to intermediate and Company F from intermediate to mature; see Table 2), which enabled us to investigate conditions enabling this shift. Table 2 provides an overview of the core cases and the collected data.

Core Cases and Case-Related Data.

Note. CSR = corporate social responsibility; KPI = key performance indicator.

This number indicates how many employees worked for the organization at the time of the analysis. b Job titles of the informants: head of corporate responsibility (CSR department) (A-1); digital marketing manager (marketing department) (A-2); head of CSR management (CSR department) (B-1); CSR manager (CSR department) (B-2); group sustainability manager (C-1) (CSR department); responsible investing manager (C-2) (investment department); global head of responsible investment (D-1) (investment department); chief communication & corporate responsibility officer (D-2) (CSR department); responsible investment analyst (E-1) (investment department); corporate responsibility manager (E-2) (CSR department); manager of environmental & social risk (F-1) (wealth management department); head of corporate responsibility (F-2) (CSR department); head of sustainable investment (F-3) (investment department); head of corporate sustainability (G-1) (CSR department); CSR managers (G-2) (CSR department); and communication manager (G-3) (corporate communication department). c Annual report, CSR report, code of conduct, internal documents (such as presentation slides, in-house communication about specific CSR projects), and others (case studies, KPIs, etc.). d Corresponding stage(s) of CSR implementation at the time of data collection.

Data Collection

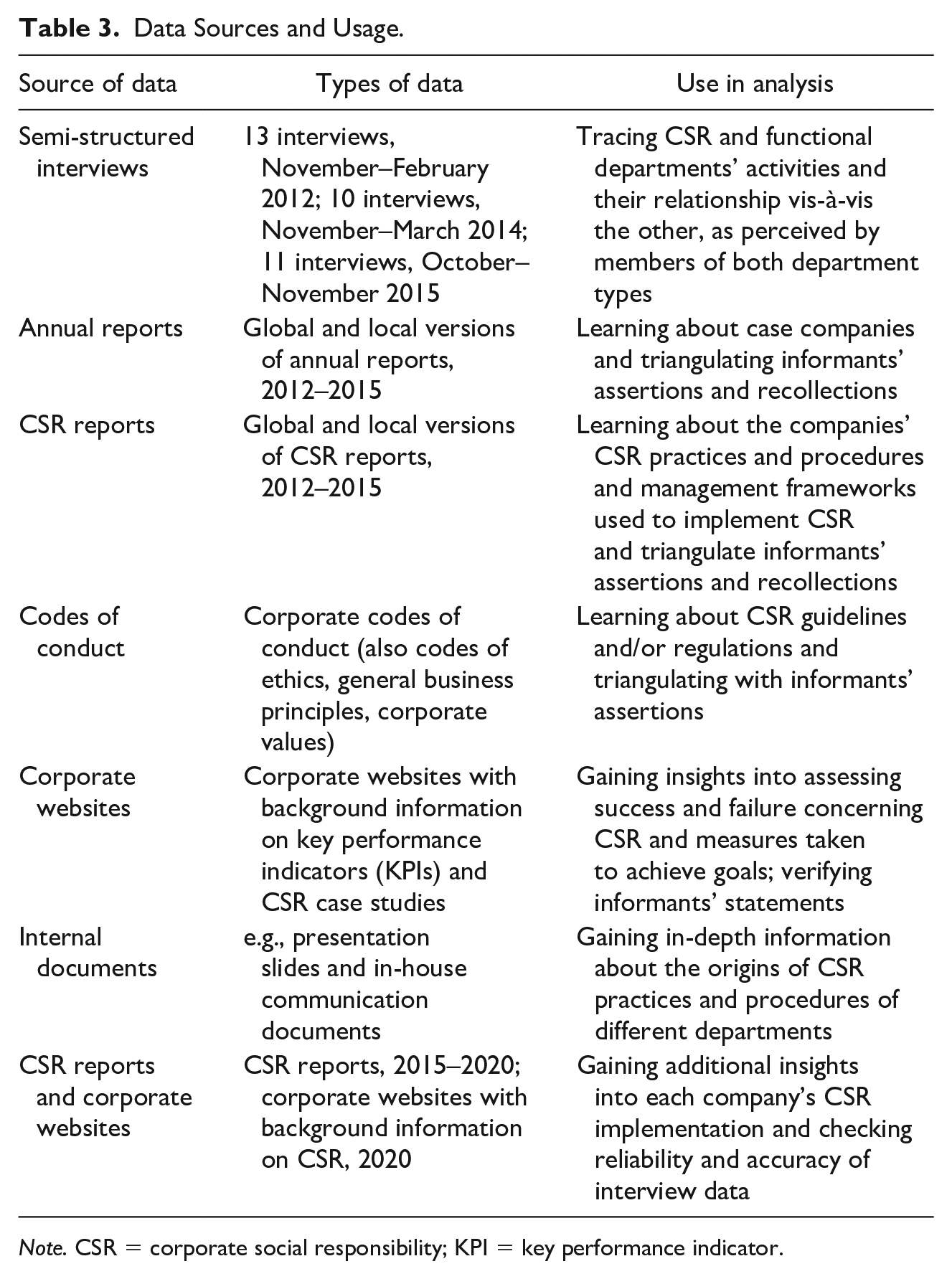

Our primary source of information was semi-structured interviews, which we combined with archival data as secondary sources. We interviewed people from different functional departments (see Table 2) to include both “overhead” functions (marketing and corporate communications) and “value-creating” functions (investment and wealth management), which allowed triangulation between them. Overall, we conducted 34 semi-structured interviews, each performed in German and lasting approximately 40 min. All interviews were recorded, resulting in nearly 1,000 min of audio data, and subsequently replayed and fully or partially transcribed. We also collected data from secondary sources such as CSR reports, annual reports, codes of conduct, press releases, corporate websites, and internal documents. We collected 118 archival documents comprising 6,120 pages of text. Table 3 outlines our data sources and how we used them in the analysis.

Data Sources and Usage.

Note. CSR = corporate social responsibility; KPI = key performance indicator.

The main data collection occurred in three phases coded (a), (b), and (c) between 2012 and 2015. In 2012, we interviewed 13 representatives from functional departments who had working relationships with the CSR department and CSR managers of all the companies we had selected (see Table 2 for an overview of the informants). In this first phase, our interviews were intended to develop a broad overview of how the CSR and functional departments worked together in each case company as it implemented CSR.

Building on these preliminary insights, in late 2014, we approached our case companies again (phase b) to collect archival and interview data to deepen our understanding of (i) the activities run by the CSR and functional departments, (ii) how these activities varied across companies given their stage of CSR implementation, and (iii) how CSR and functional departments interacted in each company. In this phase, we interviewed five informants from CSR departments and five from functional departments. This enabled us to obtain detailed information about differences and similarities in CSR implementation across our case companies.

In our last phase of data collection (c), which we conducted in 2015, we interviewed eight informants from CSR departments and three from functional departments to develop a dynamic understanding of the aforementioned differences. Hence, we adapted our interview protocol to determine whether and how the role of functional and CSR departments had changed in each of the case companies as they implemented CSR.

We classified all answers by coding responses with a distinct company code (A–G), the number of the informant (1–3), and the phases of data collection (a–c), creating a combined code such as “B-1-a.”

Early in 2020, we collected additional CSR reports published between 2015 and 2020 and information from corporate websites to gain retrospective data on CSR implementation in the seven case companies. This publicly available data allowed us to triangulate our previous insights and check the reliability and accuracy of the previously collected information.

Data Analysis

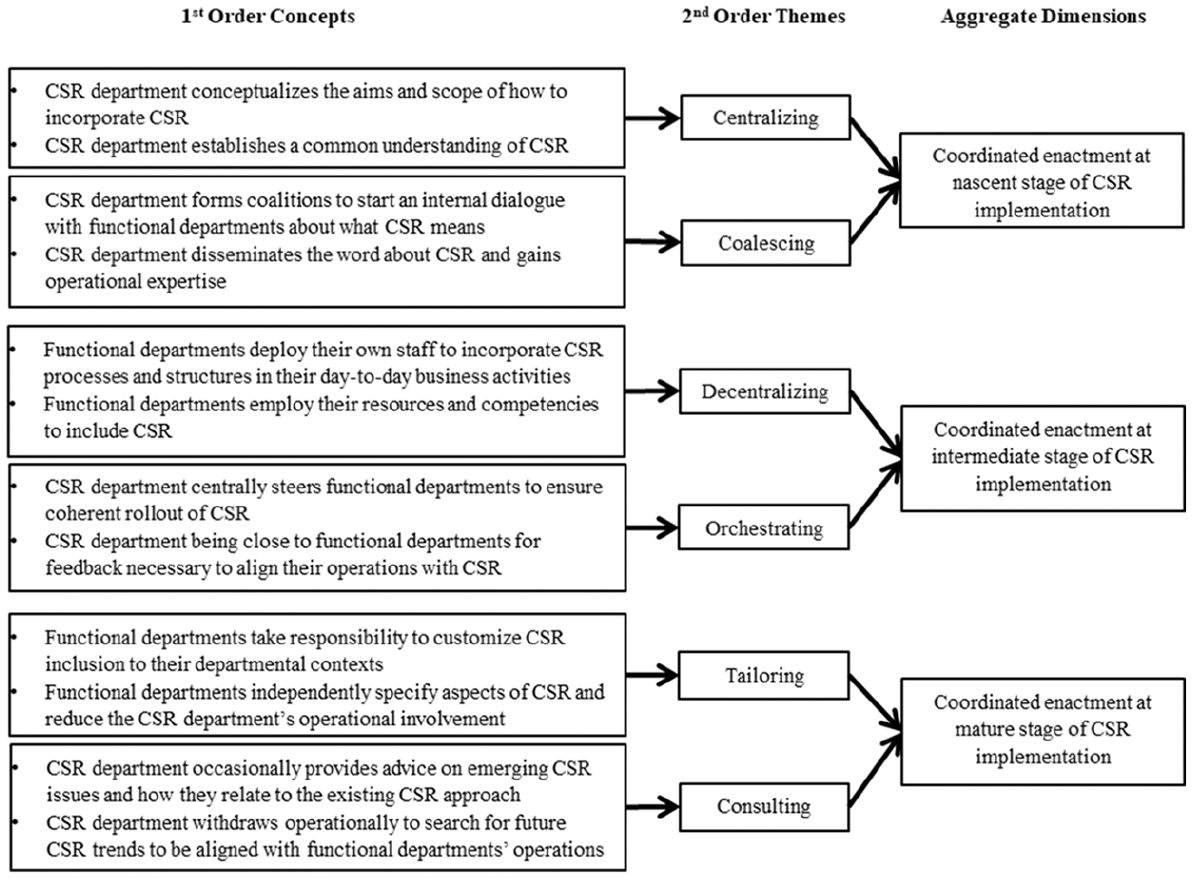

To analyze our data, we employed a grounded theorizing approach oriented toward inductive theory building (Gioia et al., 2013; Glaser & Strauss, 1998). In a first-order analysis, we processed the raw data to identify an initial set of codes and classified the descriptions of those codes into different groups. This brought to light a range of individual actions conducive to CSR implementation conducted by CSR and functional departments, which present our first-order concepts.

To understand how and why different actions of the CSR department and the functional departments influenced implementation, we also focused on the exchange of CSR-related expertise between different departments. We assessed the relative degree of influence of each CSR department on its company’s overall approach by considering the proportion of the organization’s entire staff employed in the department. Tracing resources such as staff, budgets, and the frequency of top managers’ interactions with both the CSR department and functional departments is in line with prior research that has shown that a dedicated budget, staff, top management support, and internal influence assist organizational departments with CSR implementation (Chandler, 2014).

Based on these preliminary insights, we began the second-order analysis. We further analyzed the data and studied the literature to move from descriptive insights toward more theoretical explanations. Previous research helped us interpret the actions of the CSR department and functional departments we had identified and allowed us to group them into corresponding courses of actions conducive to CSR implementation and constituting our second-order themes.

Up until this point, our insights were purely grounded in the data. However, we realized that those courses of actions were associated with what the CSR implementation literature characterizes as “enactment” (Bondy et al., 2012) vis-à-vis “coordination” (Asmussen & Fosfuri, 2019). Following common standards in grounded theorizing, we thus entered what Gioia and colleagues (2013, p. 20) have described as the “theoretical realm,” iterating between the insights from our data and the literature. While some courses of actions aimed to promote an initial CSR commitment and the subsequent inclusion of this commitment in a company’s daily operations (i.e., enactment), others ensured the alignment between CSR commitment and daily operations (i.e., coordination). This analysis resulted in a set of courses of actions reflecting coordination and conducted by CSR departments (coalescing, orchestrating, and consulting), one course of action reflecting enactment and conducted by the CSR department (centralizing), and two courses of actions reflecting enactment and conducted by functional departments (decentralizing and tailoring).

Cross-case and within-case comparisons further validated our interpretations of the six courses of actions and their correspondence with the stages of CSR implementation. Importantly, this analysis also suggests that not all companies mastered each course of action with equal effectiveness. Some had already advanced to more mature stages of CSR implementation than others (see Table 2). Our data thus suggest that variance in the stage of CSR implementation in a given company is influenced by how effectively the involved departments in that company manage the courses of actions we identified.

At the highest level of analysis, which leads to aggregate dimensions, we triangulated the interview data with secondary sources such as publicly available and internal documents on CSR and consulted the literature again (Bondy et al., 2012; Vigneau, 2020; Wickert et al., 2016). This combination of further analysis of the data and study of the literature provided insights into the six courses of actions and, most importantly, allowed us to identify the links between them and, because of their interdependent nature, pair them into “tandems” of enactment vis-à-vis coordination with each tandem occurring at one of the three stages of implementation (particularly Bondy et al., 2012; see also Table 1).

We assigned centralizing and coalescing by the CSR department to the aggregate dimension of “coordinated enactment at nascent CSR implementation,” at which stage, as our data suggest, CSR implementation is exclusively driven by the CSR department. We then assigned orchestrating by the CSR department and decentralizing by the functional departments to the aggregate dimension of “coordinated enactment at intermediate CSR implementation” and consulting by the CSR department and tailoring by the functional departments to the aggregate dimension of “coordinated enactment at mature CSR implementation.” This final step of the analysis then served as the basis for the subsequent development of a model of CSR implementation as coordinated enactment, which we present after illustrating our findings in detail. Figure 1 shows our data structure.

Data structure.

Findings

Below, we illustrate how CSR and functional departments work together to implement CSR. As widely acknowledged in the literature (Acquier et al., 2011; Wickert & de Bakker, 2018), CSR implementation typically follows top management’s initial public commitment to CSR and the establishment of a CSR department. This commitment is essential because it emphasizes the broader objective of the company-wide integration of CSR in core business practices and procedures. It therefore speaks to the requirement that all functional departments across the company are tasked with implementing CSR. For example, the CSR report of Company E, published in 2012, opens with the following commitment: For us, CSR is to be implemented in every business activity and serves as an incentive to always reflect critically on the effects of our activities on customers, business partners, employees, the environment, and society.

The implementation of CSR thus begins after an initial commitment to CSR. In this phase, the CSR department is primarily in charge of initiating implementation, while functional departments are not yet proactively engaged in either coordination or enactment of CSR.

At Nascent-Stage Implementation, CSR Departments Enact and Coordinate CSR

Two courses of actions, which we label “centralizing” and “coalescing,” occur at the nascent stage of CSR implementation, and both are characteristic of what the CSR department does. At the same time, other functional departments do not (yet) play a central role in CSR implementation.

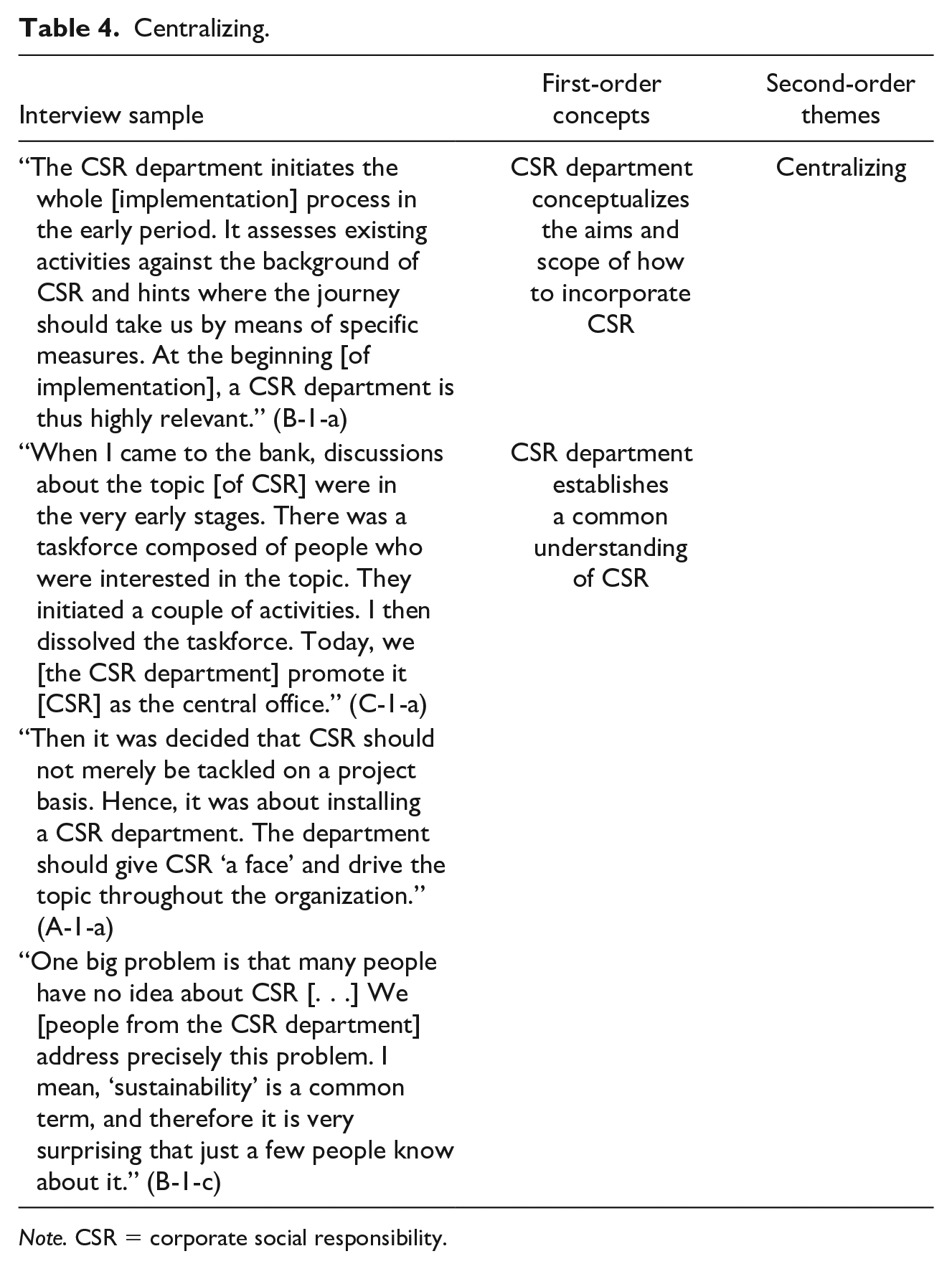

Centralizing

In the case of nascent implementation, CSR is centralized within the CSR department because this department bears the primary responsibility for initiating implementation and in doing so develops strategies, processes, and structures aimed at promoting the commitment to CSR and then ensures their inclusion in the organization’s day-to-day activities. “Centralizing” describes how the CSR department—formally established and equipped with a budget, staff, and expertise—conceptualizes the aims and scope of how to incorporate CSR. For instance, in its 2011 annual report (p. 40), Company B describes both its goal and starting point as follows: “CSR should be incorporated into as many operational areas and processes as possible. To this end, [Company B] set up the CSR department in autumn 2010.” Similarly, Company A initially created a CSR department in 2012. This consisted of one full-time position (A-1) in charge of initiating the inclusion of CSR in daily operational activities.

The CSR department establishes a common understanding of CSR and the associated areas of action regarding the inclusion of CSR issues. For example, in Company A’s 2014 CSR report (p. 9), the head of CSR mentions that at the beginning of implementation, “it is [. . .] important to determine the essential fields of CSR activities.” Company A’s 2019 annual report (p. 14) describes the main activities during the 3 years following the creation of the CSR department (i.e., 2013–2016) as follows: We [i.e., the CSR department] identified 15 potentially relevant aspects of CSR for [Company A]. We then analyzed the recognized national and international sustainability and industry standards, checked the feedback on the previous materiality matrix, and screened our most important stakeholder groups and their concerns.

Thus, at the nascent stage, a CSR department is instrumental in identifying relevant CSR issues and developing the necessary competencies and procedures to subsequently incorporate them into operations. In 2015, the department mentioned above was busy initiating activities and instruments to promote CSR, such as creating a new supply-chain responsibility policy and developing environmental guidelines with company-wide relevance. These initiatives were supported by a 50% increase in the CSR department’s budget and staff. As shown by the example above, centralizing responsibilities for implementation to a CSR department encourages this department to focus entirely on promoting CSR commitment and initiating company-wide inclusion of CSR in operational activities. For example, the digital marketing manager (A-2-a), who is a member of the marketing department, reports that nascent-stage CSR at Company A manifests itself precisely because “there is a central CSR team [. . .] responsible for this [CSR] strategy,” while the marketing department does not yet devote substantial resources or attention to CSR.

However, when the different strategies, processes, and structures associated with CSR are understood, and the necessary skills and resources to manage it are developed, members of the CSR department can reach out to other groups in the organization to secure the necessary buy-in of those ultimately responsible for including CSR in their daily activities. For example, in Company A’s 2014 CSR report (p. 9), the head of CSR mentions that in the beginning, “it is [. . .] important to determine the essential fields of CSR activities.” Once the CSR department has reached a consensus on the objectives, values, and strategic planning related to CSR, it can then begin to coordinate “the further development of existing activities and the implementation of new projects” (CSR report 2014 of Company A, p. 9). Table 4 provides some additional quotations about centralizing.

Centralizing.

Note. CSR = corporate social responsibility.

Coalescing

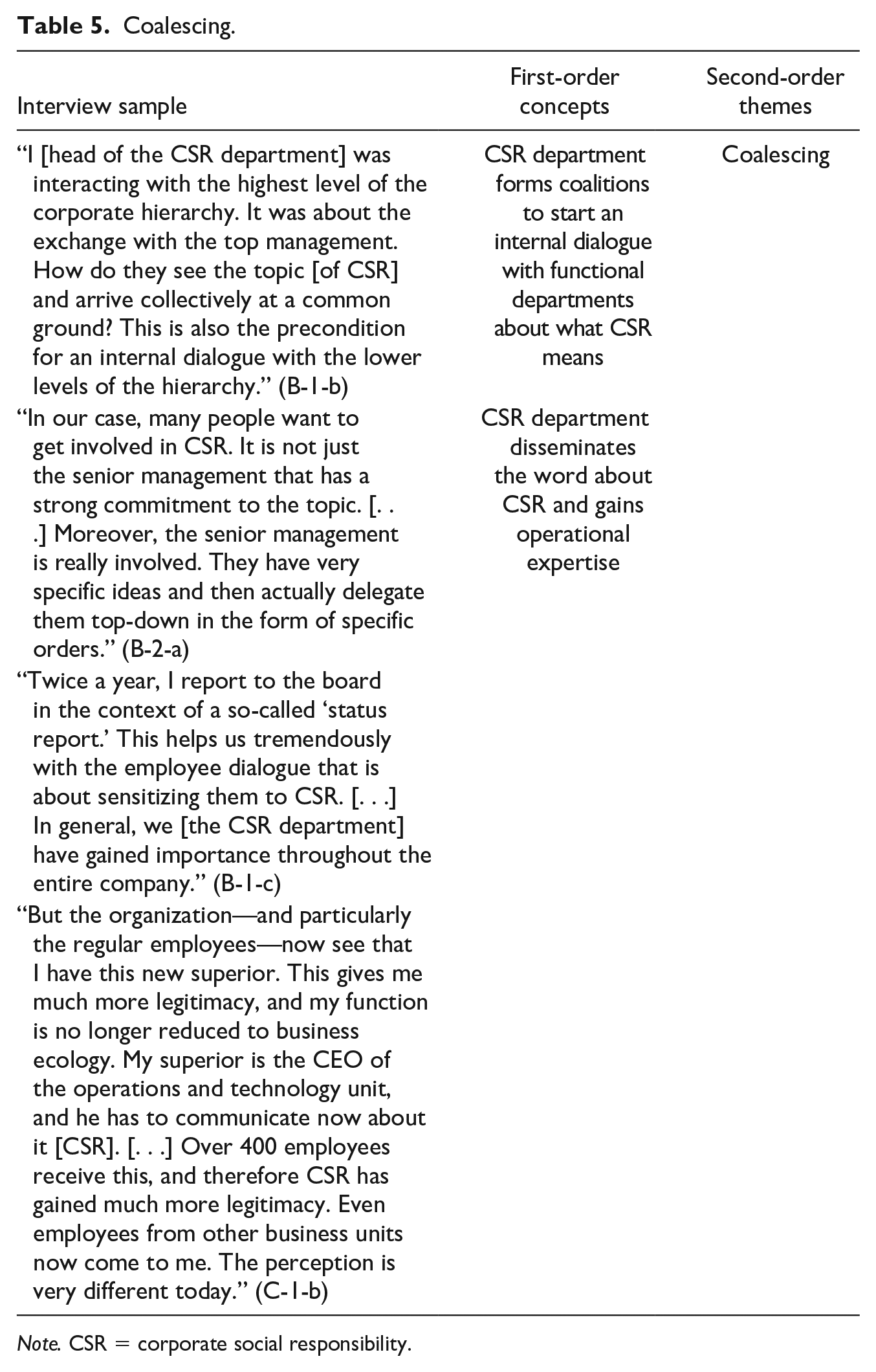

While the CSR department centrally develops the goals and scope of a company’s CSR engagement to be subsequently included in day-to-day activities, it also seeks functional departments’ support for aligning their operations with CSR. In doing so, the CSR department aims to ensure that the operation of the company’s functions is in line with its CSR-related objectives, which we refer to as “coalescing.”

Our data show that the CSR department forms coalitions to start an internal dialogue with functional departments about what CSR means. In this sense, coalescing is instrumental to achieving two related objectives: first, to spread knowledge and acceptance of what CSR means based on internal conversations with functional departments, and second, to enable the CSR department to gain valuable information about functional departments’ key characteristics and identify “focal points” of contact with them. This in turn helps the CSR department master centralizing more effectively.

For example, under the heading “Identification and prioritization of areas for action,” Company A’s 2012 CSR report states (on p. 11), “We [the CSR department] weighted the focal points in dialog with the top management team and discussed them with a small team consisting of internal and external experts.” As suggested by this report, preferred coalition partners are top managers who commit to CSR. The head of corporate responsibility at Company A explained, In terms of CSR, we are lucky because in management and on the advisory board, many members are thinking in the long term [. . .] They [board members] are more amenable to CSR, and this helps us enormously. (A-1-a)

The CSR department disseminates the word about CSR and gains operational expertise by exploiting top managers’ status to legitimize CSR without imposing the alignment of functional departments’ operations with the CSR strategy on those departments. For example, on Company A’s corporate website in 2013, a member of the executive board who was also head of the human resources department openly endorsed the focus on aligning the company’s core business with its CSR objectives.

Allies from the top management team such as this executive board member not only legitimize CSR in the company but also help the CSR department engage in conversations with functional departments to discuss emerging issues and gather further contextualized knowledge to ascertain the effective operation of functional departments in line with CSR. For example, Company B’s 2011 annual report (p. 40) highlights that the executive board and the CSR board, including the chief executive officer and the heads of eight functional departments, endorsed the CSR department’s objective of aligning functional departments’ operations with CSR throughout the company. Backed by the support of the top management team, the head of CSR management mentioned that in addition to affording better access to various company representatives, this would also help to identify the different ways of working, departmental subcultures, and mindsets of the various functional areas to which CSR could then be introduced: Today, I report to another corporate secretary who is the head of the bank’s service division. After three years, this change has definitely been an advantage for the area [of CSR], as it has opened up a new network of many influential people. Overall, I have better access to people from other business areas. [. . .] It is easier for me to figure out how people actually do business there. I just go over and ask about the technical aspects of their work. Today, there is much better access to knowledge and people. (B-1-c)

CSR departments considered it necessary to become acquainted with how the various functional departments work because a better understanding of these departments’ characteristics helps them analyze which existing business operations might be aligned with CSR and then customize them to functional departments. For example, in connection with “a stable working group” (informant A-1-c) that regularly meets to discuss the state of CSR implementation, among other things, the head of corporate responsibility at Company A mentioned the importance of good relationships with functional departments as well as up-to-date knowledge about “how things work” there.

This insight shows why a CSR department in a company currently in nascent-stage CSR engages in coalescing. For example, Company A’s digital marketing manager (A-2-a), who is located in the marketing department and interested in CSR, reported that in companies that “still have the potential for [CSR] optimization,” the CSR department “tries to focus responsibility [for CSR implementation] more on the individual line function.” At a nascent stage of CSR, the CSR department supports functional departments in aligning their conventional activities with CSR.

Finally, and as illustrated by the quote above (i.e., B-1-c), coalescing in companies such as Company B fed back into centralizing because knowledge about the expectations and priorities of relevant functional departments where CSR is to be executed allowed the CSR department to steer the implementation of CSR such that different needs, priorities, and expectations of functional departments were considered. Table 5 provides further evidence of coalescing.

Coalescing.

Note. CSR = corporate social responsibility.

At Intermediate-Stage Implementation, Functional Departments Enact CSR, and CSR Departments Coordinate

Functional departments enact CSR at an intermediate stage by including relevant strategies, processes, and structures in their day-to-day activities. However, this requires the CSR department to coordinate functional departments’ operations to ensure their alignment with overall CSR objectives. For example, between 2012 and 2015, Company C transitioned from the nascent to the intermediate stage of implementation. As evidenced in Company C’s 2019 CSR report (pp. 6–7), traditional private banking and investment banking departments had been tasked with including CSR in their activities once the CSR department had set the objectives and made them understandable to and acceptable for those departments. As this example illustrates, the intermediate stage is thus characterized by two courses of actions for implementing CSR: “decentralizing” by functional departments and “orchestrating” by the CSR department. We detail these courses of actions below.

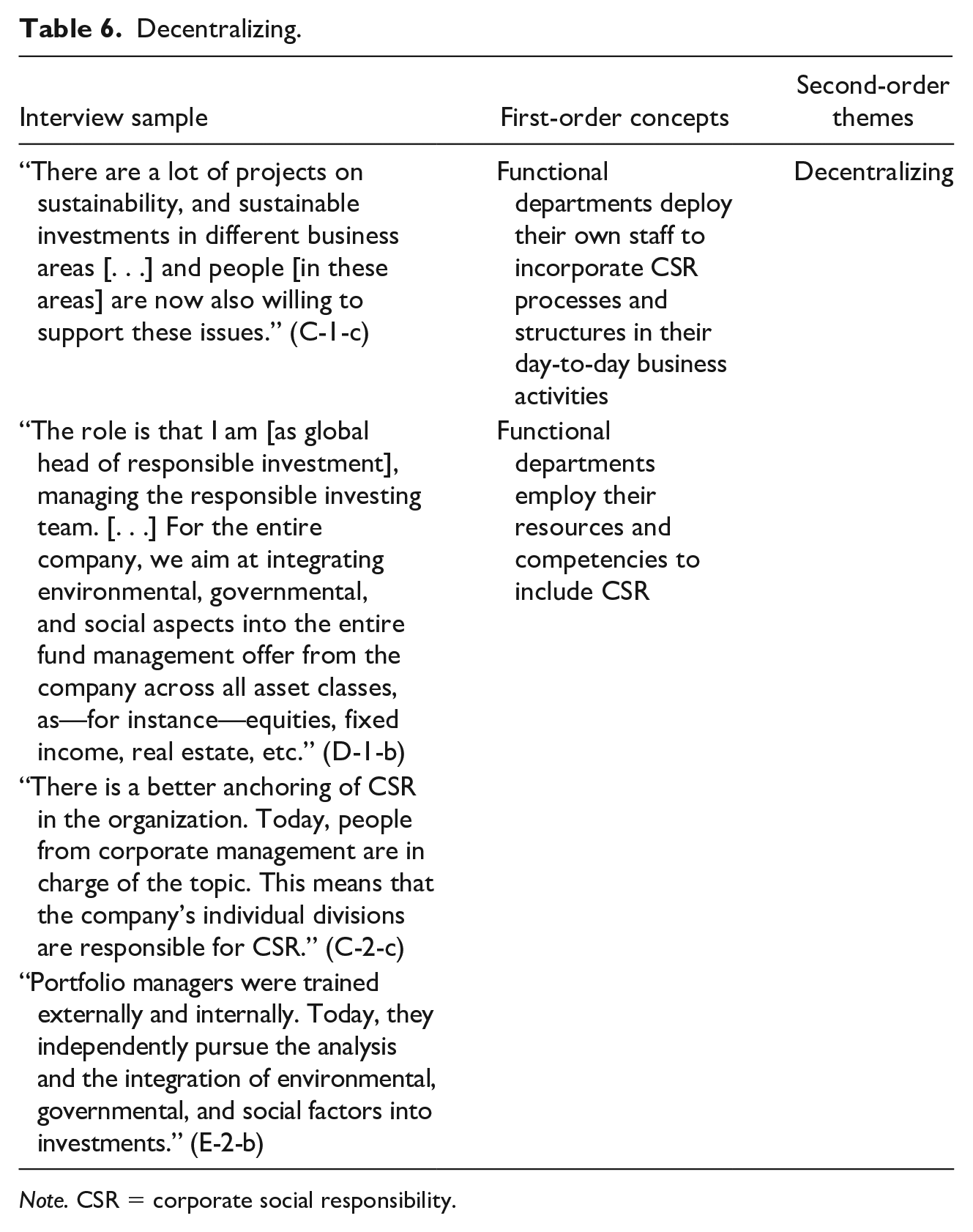

Decentralizing

Taking the overall CSR strategy as a reference point, functional departments deploy their own staff to incorporate CSR processes and structures in their day-to-day business activities. As the responsible investing manager of Company C explained, When there is better anchoring of CSR in the organization, people from corporate management are in charge of the topic. This means that the company’s individual divisions become responsible for CSR.(C-2-c)

“Decentralizing” implies that the CSR department no longer enacts CSR; rather, the various functional departments of Company C work on the inclusion of CSR in their day-to-day activities. The chief communication and corporate responsibility officer at Company D explained this shift of responsibilities as reflected in the number of staff tasked with managing CSR as part of their job profile, saying, I do not need two or three more people [in the CSR department]. In each area of work, for instance, procurement, underwriting, etc., they all have to bear CSR in mind. (D-2-b)

Following this shift in responsibilities, functional departments employ their resources and competencies to include CSR and in this way develop a better understanding of how to implement CSR in their specific operational activities. Because functional departments increasingly take over CSR enactment at the intermediate stage, CSR departments face a relative reduction in staff or budget. The group sustainability manager of Company C explained, Today [at the end of 2015], we are a team of two, while in 2013, I was alone. I am sure that the size of our team won’t be extended. We have the know-how, we can push certain topics, but the business units bear the responsibility. (C-1-c)

At this point, staff with CSR expertise are based in functional departments rather than CSR departments. They exploit resources to adapt CSR activities to the specific operational activities run by each functional department in line with the overall CSR strategy set by the CSR department. For instance, in a 2013 in-house publication, Company D’s asset management department explained that it was devoting resources to the inclusion of CSR in day-to-day activities and announced, within the frame of a so-called “sustainable investing initiative,” an investment of over US$160 million in various social funds and environmental projects. Providing two further examples, Company F’s head of corporate responsibility explained that functional departments allocated new resources to CSR initiatives after taking over responsibility for managing these issues. In this way, functional departments began to enact CSR given their resources and specificities: The CSR team has remained the same. However, we increasingly count on resources from others. [. . .] In the case of communicating [on CSR], we rely on experts from corporate communications. Another example would be our topical event on ecology that was planned and executed by people from risk management and environmental management. (F-2-b)

Functional departments such as communication and risk management now enact CSR by including it in their daily activities. A responsible investment analyst at Company E explained that this shift in executive responsibility was vital for bringing CSR “into the business units” and developing CSR activities that could fit the specificities of each functional department in view of the company’s overall CSR strategy: It is about breaking down the focal points [of CSR] into the business units. In concrete terms, what has to change in the business units. For instance, one can invest everything in sustainable funds, or one invests in the training of customer consultants. (E-1-c)

While enabling a more customized and company-specific implementation of CSR, decentralizing also enables a better understanding of CSR and how to adapt it to the different functional departments’ specificities. For instance, a corporate responsibility manager (E-2-b) for Company E explained that the finance department strives to “work on the importance of responsible investing.” Because of this course of actions, CSR “is now more deeply implemented [. . .] and people [in Company E] understand what sustainability in investing means.” In summary, decentralizing implies that the enactment of CSR no longer happens in the CSR department but rather in various functional departments. These departments enact CSR in their practices and activities based on their departments’ resources. Table 6 provides further evidence of decentralizing.

Decentralizing.

Note. CSR = corporate social responsibility.

Orchestrating

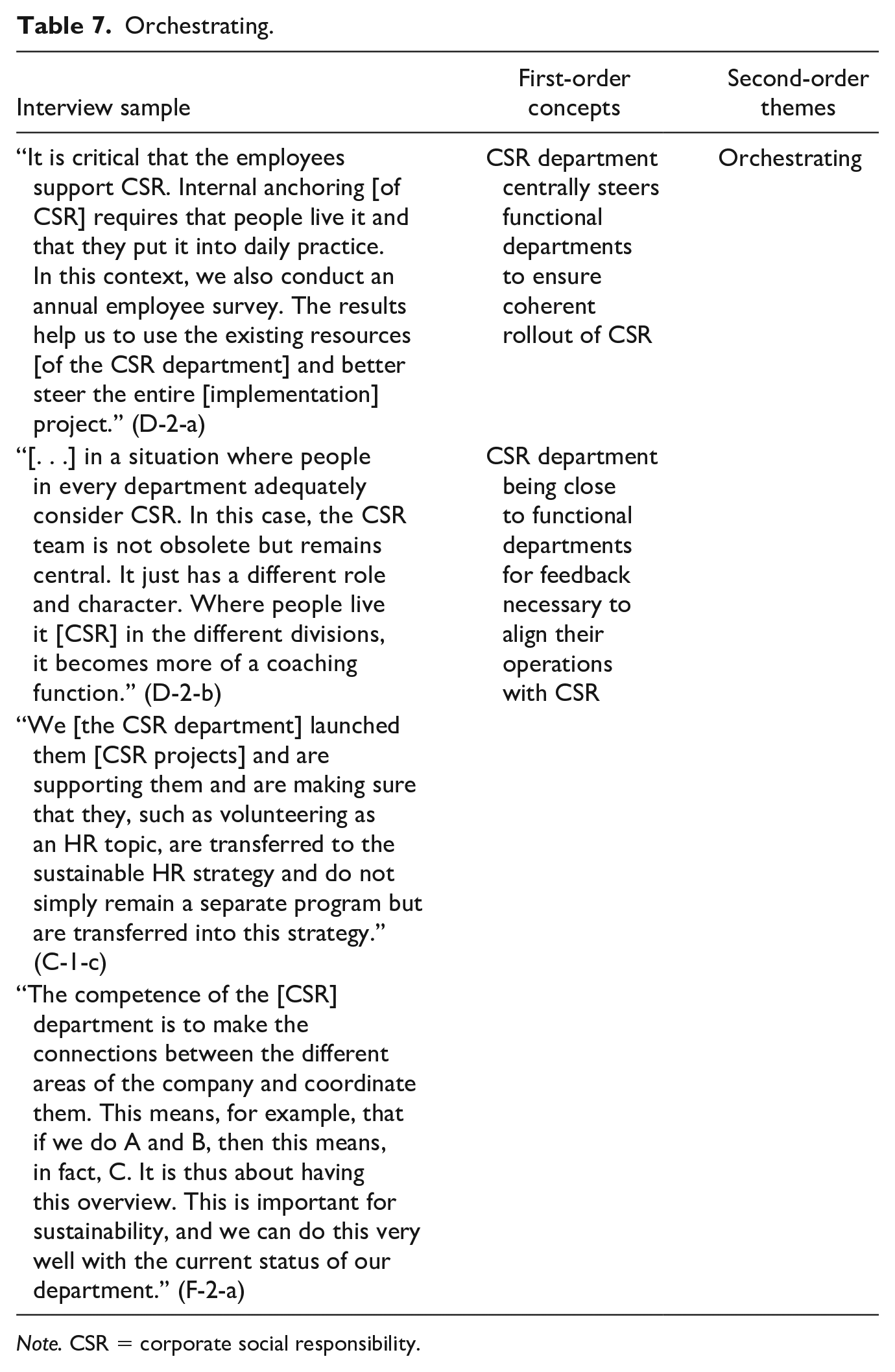

While at the intermediate stage, functional departments are busy enacting CSR, the responsibility for coordinating these decentralized activities and ensuring that they are in line with the company’s overall CSR objectives lies with the CSR department. We refer to this course of actions as “orchestrating.” As the “control center,” the CSR department centrally steers functional departments to ensure a coherent rollout of CSR, as the chief communication and corporate responsibility officer of Company D explained: We do not lose sight of CSR, as we [the CSR department] really want to push social and environmental aspects forward company-wide, too. This is a real change. CSR is going more and more into the core business. [. . .] The CSR department is thus the control center. (D-2-c)

A responsible investment analyst of Company E further clarified that orchestrating CSR “from headquarters” goes along with CSR departments’ proactive yielding of organizational influence, favoring the effective operation of functional departments in line with CSR: Responsible investing has to be addressed in the investment department. Diversity has to be managed by HR [human resources], etc. In our current structure, we [the CSR department] only coordinate these different activities from headquarters. (E-1-a)

In addition to the CSR department being less present in the enactment of CSR concerning core business activities, orchestrating involves the CSR department being close to functional departments for feedback necessary to align their operations with CSR. For instance, a manager of environmental and social risk at Company F explained the importance of orchestrating different functional departments: First, as shown, the CSR department must “work closely” with the functional departments, as it requires information on the extent to which functional departments’ CSR execution is consistent with the CSR program and where the CSR department may need to take corrective action. [. . .] it is not primarily our responsibility anymore for the bank to reduce its energy use or CO2. However, instead, this department has taken responsibility for the implementation. We merely support it and ensure that its activities match our overall [environmental] strategy. (F-1-a)

Under the heading of “Environmental Strategy,” Company F’s 2013 website confirms the manager’s statement: “The [functional] divisions bear full responsibility for identifying and developing market opportunities offered by environmental issues.” However, with its small team, Company F’s CSR department oversaw the environmental strategy rollout and maintained access to functional departments to ensure that their operations were coherent with the CSR strategy. Such access is essential because, in its orchestrating role, the CSR department also provides functional departments with expertise and procedures to align their operations with the company’s CSR commitment. Company C’s 2015–2016 CSR report (p. 9) mentions that the CSR department provides target group-oriented measures such as “web-based training, classroom training, information events or information conveyed via the intranet, e-mail, information monitors or posters.” These measures help the CSR department coordinate the enactment of CSR by the functional departments, suggesting a shared responsibility for CSR implementation at the intermediate stage.

The importance of orchestrating at the intermediate stage of CSR implementation is underscored by Company D. For example, its chief communication and corporate responsibility officer (D-2-a) stated, “There are people in all areas and departments who wear the ‘CSR hat’ and who support us [the CSR department] in implementing these CSR measures.” However, the informant explained, “We [the members of the CSR department] have to coordinate the whole thing [CSR implementation]; we drive it, we coach, we support, we inform. That’s our job. But the people outside [of the CSR department] have to do it.” Table 7 provides additional illustrative quotations about orchestrating.

Orchestrating.

Note. CSR = corporate social responsibility.

At Mature-Stage Implementation, Functional Departments Enact CSR, and CSR Departments Coordinate

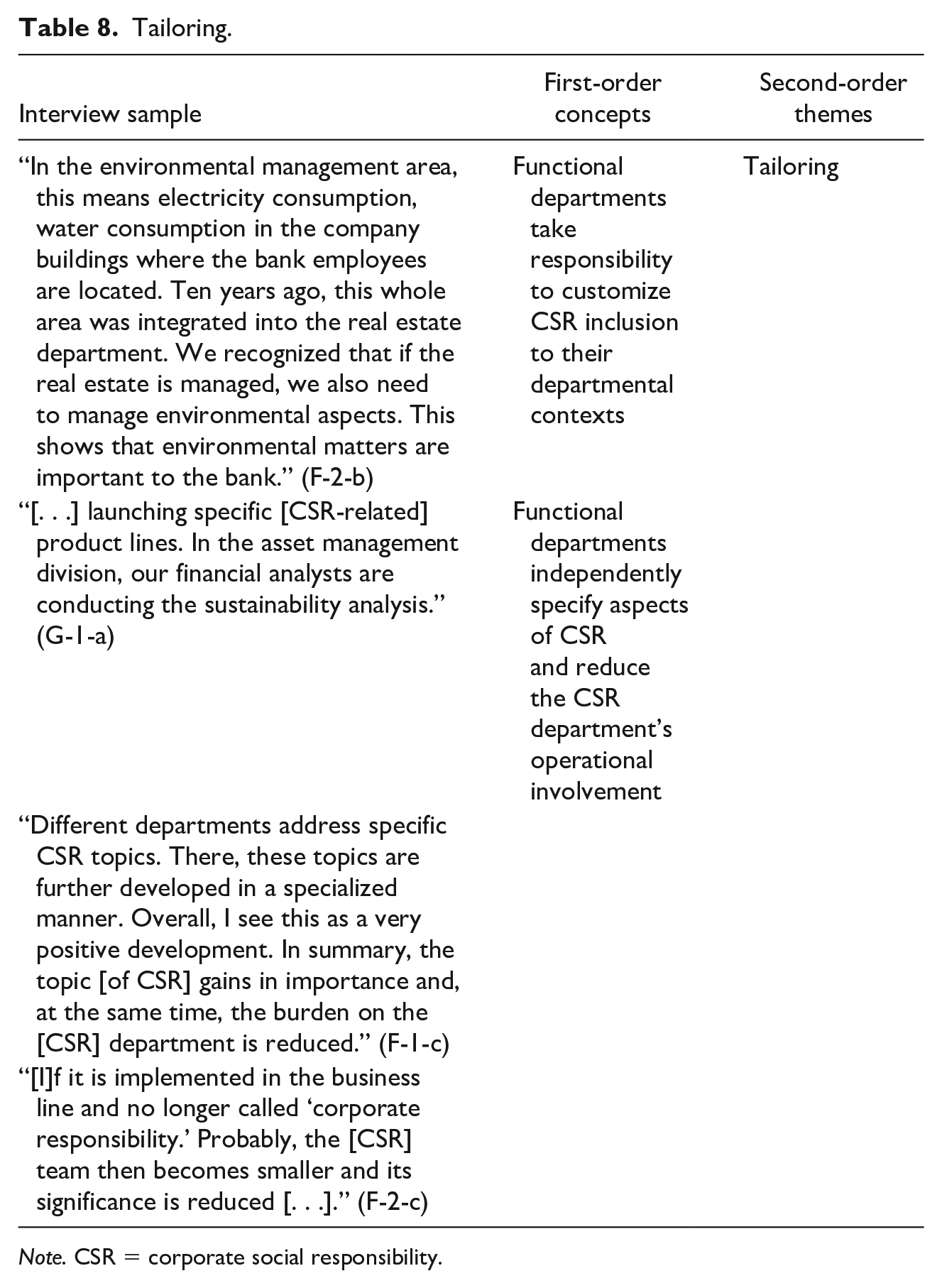

We found two courses of actions occurring at the stage of mature CSR implementation. We label these “tailoring” and “consulting.” “Tailoring” describes how functional departments contextualize the inclusion of CSR in their activities through their specific capabilities and needs. “Consulting” refers to how the CSR department provides advisory support to functional departments to ensure that they are up to date regarding emerging CSR trends.

Tailoring

When tailoring, functional departments take responsibility to customize CSR inclusion to their departmental contexts, while previously, they tended to follow the instructions of the CSR department. Tailoring implies that functional departments are more autonomous in specializing in relevant and context-sensitive CSR issues with less of the CSR department’s previous control. The head of corporate responsibility of Company F illustrated this by saying, This goes along with the specialization that is in the nature of things. This means that, ultimately, customer-specific things are taken over by the customer services area of the bank, environmental and social risks are analyzed in the risk management division, etc. (F-2-b)

Tailoring differs from decentralizing in that functional departments still enact CSR within the company’s initial CSR commitment but primarily tailor the inclusion of CSR to their own capabilities and needs and thus enact CSR without the strong involvement of the CSR department. The functional departments can do so because they now “assume. . . [CSR in their respective] business area” (G-1-b) and in doing so develop their own CSR initiatives and working groups rather than “only” executing what the CSR department had previously instructed them to do.

Tailoring also means that functional departments independently specify aspects of CSR and reduce the CSR department’s operational involvement. The CSR department’s reduced involvement in the functional departments’ enactment of CSR is evidenced by a reallocation of budget from the CSR department to the functional departments. The following statement from Company G’s head of corporate sustainability illustrates this: [T]here is a general trend of diminishing CSR managers [. . .] However, the issue of CSR is not neglected at all. In fact, it is the opposite. A large number of initiatives and taskforces are driving it and are specializing in certain [CSR] areas. My job has been reduced to a 50% position. In this context, the top management has clearly stated that the job of the CSR manager is not assumed by a new CSR manager but goes into the business area instead. The remaining 50% is for people who focus on CSR in these other areas. (G-1-b)

Company G’s 2015 CSR report (p. 11) exemplifies how asset management responds to increasing client demand for sustainable investing through tailoring: In regular sustainability meetings, analysts and portfolio managers discuss current ESG [environmental, social, and corporate governance] evaluations and let the result flow into the investment process.

While functional departments in Company G deliberately customized their daily practices and procedures within the boundaries of the overall CSR strategy—for instance, asset management integrates ESG criteria in investments—the CSR department experienced a 50% staff reduction. The other 50% of the budget was then reallocated to functional departments, which invested in developing specific CSR-related services and products such as sustainable investments.

Tailoring means that CSR is “taken over” by functional departments, which now interpret, execute, and develop specific CSR aspects independent of the CSR department, thereby helping to stabilize the enactment of CSR at a mature implementation stage. An internal document from 2013 that defines the resources and responsibilities involved in implementing CSR in Company F highlights the presence of tailoring: “[T]he financial means for implementing CSR issues is part of each functional department’s budget, according to its responsibilities.” Accordingly, through tailoring, a company can consolidate a mature stage of CSR implementation. In response to the question of what is relevant for achieving this stage, the head of corporate sustainability of Company G (G-1-a), for instance, referred to the asset management department to indicate the relevance of functional departments’ contextualizing of CSR to their daily activities: “It [CSR] is now strongly integrated. For example, we have the global equity team in asset management, where sustainability analysis is now part of their daily work.”

In summary, our data show that tailoring describes functional departments’ contextualized inclusion of CSR in their daily activities and thereby shows how CSR is enacted at a mature stage of implementation. As underscored by changes in budget and staff, this means, in essence, that the role of the functional departments vis-à-vis the CSR department has been upgraded from passive to much more active. Notwithstanding this, we found that functional departments still need the CSR department’s consultative support to ensure that their operations align with the company’s overall CSR objectives. We explain this course of action in the following section. Table 8 provides further evidence of tailoring.

Tailoring.

Note. CSR = corporate social responsibility.

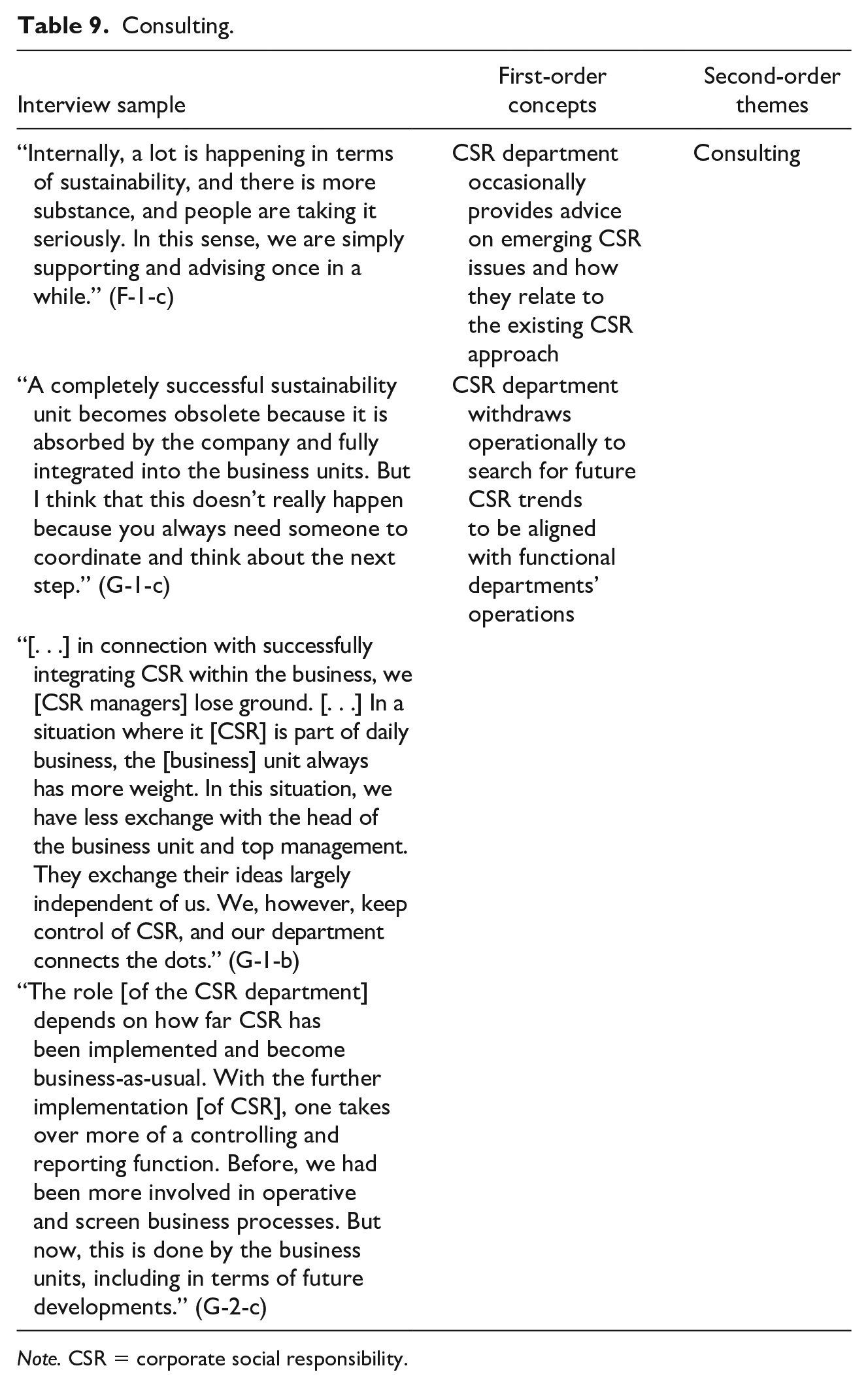

Consulting

Consulting complements tailoring at a mature implementation stage but indicates a shift in the CSR department’s role vis-à-vis the functional departments. Orchestrating implies a more proactive approach and close coordination of functional departments’ daily activities by the CSR department to ensure that the functional departments execute CSR in line with the company’s overall objectives. In contrast, consulting implies that if approached by functional departments, the CSR department occasionally provides advice on emerging CSR issues and how they relate to the existing CSR approach. Hence, the role of the CSR department is downgraded to that of a sporadic adviser that, unlike in its previous role as central orchestrator, largely stays out of the day-to-day business of the functional departments and only coordinates the company-wide uptake of new CSR topics.

An internal document from 2013 concerning the resources, roles, and responsibilities involved in Company F’s CSR implementation elaborates on the CSR department’s consulting function: The CSR department should only offer support in case of urgent matters as ownership of enacting CSR now lies within functional departments such as the wealth management and investment divisions. Such urgent matters are usually about emerging CSR issues and concomitant field-level trends, regarding which the CSR department acts as a consulting expert. Company F’s 2016 annual report (p. 273) provides further evidence of this as functional departments demand expertise from the CSR department about “the main topic” of the Sustainable Development Goals of the United Nations.

Consulting manifests in fewer interactions between the CSR department and functional departments. In Company F, for example, the CSR department had less access to operational knowledge about socially responsible investing because the functional department involved had begun to develop the corresponding procedures and performance indicators on its own. The head of corporate responsibility explained how the CSR department has become an occasional consultant when functional departments have taken over CSR, saying, In some cases, we see that CSR has shifted to the specialist departments. This is because we are no longer the only ones who are in charge of that [i.e., CSR]. The business case of CSR or sustainable investing is recognized in certain departments, and we [the CSR department] are only consulted as experts or specialists. (F-2-b)

The CSR department withdraws operationally to search for future CSR trends to be aligned with functional departments’ operations. CSR managers explained that once they had been able to withdraw from their central orchestrating function, their staff was able to engage more closely with developments related to CSR in their broader market environment that might become relevant for the company in the future. Hence, the CSR department consults on CSR, “thinks about the next step” (G-1-c), and coordinates how new trends reach the relevant functional departments.

Consulting allows the CSR department to focus on future CSR trends to be aligned with functional departments’ operations, which corresponds with the CSR department’s reduced organizational influence and top management access. A CSR manager in Company G explained, It is the case that CSR managers are, generally speaking, losing influence, but then again, the CSR manager is just taking on a new consulting role, so it’s not so much that one does a certain project from start to finish. Instead, that is done by line management, and they also implement it. [. . .] That is why we are talking about less influence, as it is just another function [of the CSR manager]. However, regarding the topic [CSR], most people [CSR managers] who are working on it have no problem with that. They welcome the fact that CSR is strongly embedded. (G-2-c)

This statement illustrates that because functional departments are now fully responsible for enacting specific CSR processes and structures, as the CSR manager explained, the CSR department has actively worked to reduce its organizational influence in favor of the consolidation of CSR in the functional departments’ operations. This is in line with the above statement of Company G’s head of corporate sustainability (informant G-1-b), who referred to reducing the headcount in the CSR department while further consolidating CSR implementation. Accordingly, consulting by the CSR department helps to consolidate mature-stage CSR implementation. As the head of corporate sustainability (G-1-c) of Company G explained, “there is a wide range of [CSR] initiatives and departments that are pushing forward and are specializing in certain [CSR] topics.” To ensure such specialization, the CSR department provides advisory support to functional departments to ensure that they are up to date about emerging CSR trends: Here, of course, the business has greater ownership. The relevant business units are responsible for their products and simply seek expert input from me when it comes to further development. For example, I continue to provide the sustainable investment universe based on the information we receive from external research partners. (G-1-c)

In summary, consulting implies that once at a mature implementation stage, CSR departments focus on consulting with functional departments about emerging trends while coordinating to ensure that these trends are addressed internally in a coherent manner. Table 9 provides further evidence of consulting.

Consulting.

Note. CSR = corporate social responsibility.

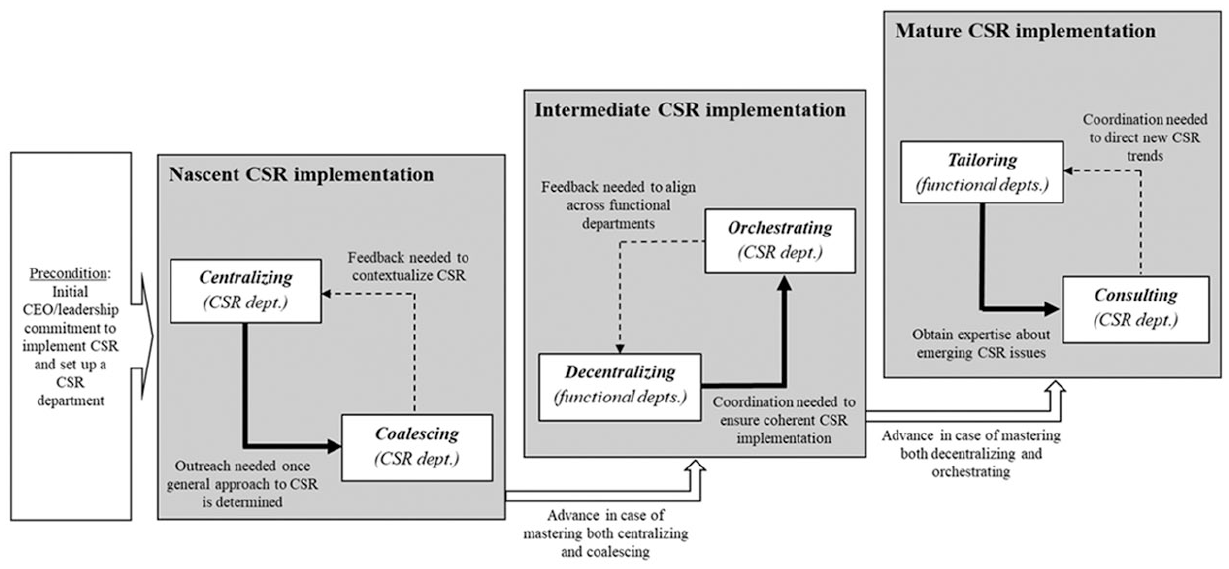

A Model of CSR Implementation as Coordinated Enactment

The previous chapter illustrated how CSR departments and functional departments work together to implement CSR, including coordination and enactment among all parties. We now consolidate our findings into a model of CSR implementation as coordinated enactment. While CSR departments engage in coordination at all three stages of implementation by coalescing, orchestrating, and consulting, these departments only show enactment at a nascent stage via centralizing. In contrast, at the intermediate and mature stages, CSR is enacted by functional departments via decentralizing and tailoring. Figure 2 illustrates our model, which we explain in detail below.

How CSR departments and functional departments work together to implement CSR.

The fundamental prerequisite and thus boundary condition of our model are the initial CEO and leadership commitment to implementing CSR and setting up a CSR department. After that, coordinated enactment manifests differently depending on the stage of implementation. First, in a nascent stage, implementation comprises two courses of actions aimed at enacting and coordinating CSR, namely, centralizing and coalescing. Given the emergent character of CSR at this stage, both enactment and coordination are interrelated because the CSR department conducts them simultaneously. The CSR department enacts CSR by centralizing the setup and outline of strategies and relevant processes and structures, while other functional departments are not yet involved. However, while CSR strategies, processes, and structures clarify the meaning, scope, and goals of CSR, outreach to other departments starts with and must be coordinated by the CSR department (bold arrow in Figure 2). This is referred to as coalescing.

Coalescing allows the CSR department to form internal coalitions that support CSR implementation. Coalescing implies coordination by the CSR department and feeds back into its task of centralizing because coalescing facilitates access to operational expertise relevant to contextualizing CSR for different functional departments (dotted arrow in Figure 2). Coalescing thus facilitates enactment because it provides the basis for spreading expertise to functional departments and coordinating internal support for formalizing CSR in overarching organizational strategies, processes, and structures. The better a company masters both centralizing and coalescing in terms of having clarified the aims and scope of CSR and put this into a strategy and corresponding policies and having achieved sufficient acceptance of CSR by the company’s functional departments, the more likely it is that the company will be able to advance to the subsequent intermediate stage of CSR implementation (framed arrow in Figure 2).

At an intermediate stage, CSR implementation comprises courses of actions aimed at enacting and coordinating, namely, decentralizing and orchestrating. The critical difference in the nascent implementation stage is that functional departments now begin to play a role in CSR implementation. By decentralizing, these departments enact the CSR strategy in relevant operational processes and structures in line with the company’s overall CSR objectives. Decentralizing shows that once functional departments have accepted the general aims and scope of CSR, they can enact relevant issues in their core business activities and day-to-day operations.

Again, coordination and enactment are interrelated. Decentralized enactment of CSR in functional departments requires the company-wide coordination of these efforts by CSR departments to ensure coherence between processes and structures and overall goals (bold arrow in Figure 2). This course of actions by the CSR departments is captured by what we describe as orchestrating. Orchestrating is critical because it provides a feedback loop to functional departments about how their decentralized enactment of CSR aligns with the overall strategy, which allows them to adjust where necessary (dotted arrow in Figure 2). Furthermore, orchestrating ensures that CSR is enacted in a way that accounts for the specific requirements of functional departments and provides the basis for shifting ownership to these departments, both of which are relevant for their increasingly independent enactment of CSR. Similar to the advancement from the nascent to the intermediate stage, the better a company masters both decentralizing and orchestrating, the more likely it is that the company will be able to advance to the subsequent mature stage of CSR implementation (framed arrow in Figure 2). In this stage, mastering means that functional departments develop the knowledge and resources to operationalize CSR autonomously and the CSR department perceives the operationalization of CSR to be aligned with the company’s overall CSR objectives.

At the mature stage, CSR implementation comprises courses of actions aimed at enacting and coordinating, namely, tailoring and consulting. While at the previous stage functional departments were busy enacting the strategy set by the CSR department, at this stage functional departments have taken full ownership. As a result, they can tailor CSR to their own context and objectives. Moreover, coordination and enactment are interrelated at this stage because functional departments continue to engage with the CSR department to obtain expertise about emerging issues (bold arrow in Figure 2). However, functional departments strive for such expertise more sporadically and are driven by concrete needs. CSR departments are no longer involved in the day-to-day operations of the functional departments and restrict their involvement to consulting on new trends (dotted arrow in Figure 2). The role of CSR departments is reduced to coordinating to ensure functional departments stay up-to-date on new and emerging issues.

Discussion

Our research question asks how CSR departments and functional departments work together to implement CSR. To answer this question, we mobilized two complementary yet separate perspectives on CSR implementation: enactment and coordination. Our main contribution to the literature is to offer a model of CSR implementation as coordinated enactment, which is defined as a combination of strategies, processes, and structures aimed at promoting first commitment to CSR and then its inclusion in the company’s day-to-day activities to ensure the efficient and effective operation of the company’s functions in line with its CSR objectives. In brief, our model disentangles the roles of the CSR department vis-à-vis the functional departments in CSR implementation and, by viewing CSR implementation as coordinated enactment, shows how the simultaneous courses of actions are distributed internally depending on the stage of implementation. The examination of how these types of departments interact provides essential insights into which departments enact strategic and operational aspects of CSR implementation and how coordination among departments is achieved for this purpose. Distinguishing the activities of the CSR and functional departments is critical because it helps to balance current views that locate responsibility for implementation primarily with CSR departments and downplay the significant and underappreciated role of functional departments (Hunoldt et al., 2020; Osagie et al., 2019; Wickert & de Bakker, 2018).

Conceptualizing CSR implementation as a combination of coordination and enactment overcomes significant limitations in research that has emphasized the importance of both enactment and coordination without explaining their interplay. First, while the enactment view underscores that CSR must progress from commitment to inclusion, it is limited in its examination of how enactment is shared and distributed between the CSR department and other functional departments (Bondy et al., 2012; Maon et al., 2009; McNamara et al., 2017; Miska et al., 2016; Vigneau, 2020). We have addressed this limitation and shown how the various departments enact CSR at particular stages of implementation.

Second, we have also addressed an essential limitation of the research on coordination in CSR implementation, which has tended to depict coordination activities as relatively stable and disconnected from the stage of implementation (Asmussen & Fosfuri, 2019; Durand & Jacqueminet, 2015; Wickert et al., 2016). By detailing how coordination between the CSR and other functional departments is achieved, we have conceptualized it as dynamic and dependent on the stage of implementation. In doing so, we have expanded research on CSR implementation that has highlighted the importance of but not yet fully conceptualized the interactions between the CSR and functional departments (Hunoldt et al., 2020; Kok et al., 2019; Lindgreen et al., 2009). Our findings underscore that understanding CSR implementation requires paying more attention to “non-CSR” functions as prior work has primarily focused on the role of CSR managers and departments (Hunoldt et al., 2020; Osagie et al., 2019; Wickert & de Bakker, 2018) at the expense of other organizational functions that actually enact CSR. Overall, combining the enactment and coordination views provides a more granular understanding that attributes specific courses of actions to specific departments at particular stages of implementation and how these departments work together to implement CSR.

Our model also shows how the implementation is distributed within companies and thus expands earlier work that has attributed a pivotal role to companies’ departments rather than organizations more generally as the focal unit of analysis regarding whether and to what extent a company implements CSR (Chandler, 2014; Delmas & Toffel, 2008; Jacqueminet, 2020). While CSR departments have a central role at the nascent stage and are responsible for both enactment and coordination, functional departments take over the enactment once an intermediate or mature stage has been reached, while CSR departments focus on coordination. This insight is vital in light of inconsistent findings in prior work. Some research has shown that the organizational influence of CSR departments and their managers’ status is positively associated with more mature stages of implementation (W. M. Hoffman et al., 2008; J. Weber & Wasieleski, 2013). However, more recent work suggests that the decreasing importance of the CSR department signals mature implementation, whereas the high importance of the CSR department signals the beginning and thus a nascent stage (Risi & Wickert, 2017; Strand, 2014). In fact, research has indicated that CSR departments might even become superfluous once their objectives (i.e., consolidating mature CSR implementation in a given company) have been fulfilled (Risi & Wickert, 2017). Our findings are consistent with the latter observation, and we further clarify this perspective by outlining the activities shaping the type and level of departmental involvement in CSR implementation.

Finally, a better understanding of the interdepartmental dynamics of CSR implementation also helps explain variance in how companies engage in CSR. This is important because while companies often face increasingly uniform institutional pressures for social and environmental responsibility through standards and (self-)regulatory frameworks (Kourula et al., 2019; Shabana et al., 2017), research shows that there still is significant variance in how comprehensively they implement CSR (Baumann-Pauly et al., 2013; Bondy et al., 2012; Risi, 2020). As our model suggests, CSR implementation follows successive steps of coordinated enactment that manifest in the courses of actions we have highlighted. We have found evidence that not every company is equally effective in enforcing those courses of actions, which suggests that mastering them is critical for advancing CSR implementation. Our research thereby refines prior work that has emphasized the importance of an organization’s willingness and ability to implement CSR (see Durand et al., 2019). We specify this prior work by explaining that a company needs to be willing and able to master different courses of actions if it strives to advance its CSR performance.

Limitations and Implications for Future Research

Our model is not without limitations. As previously argued, a commonly emphasized precondition of our model is an initial CEO and leadership commitment to establishing a CSR department to take charge of implementation, which is an issue widely documented in the literature and reflected in our data (Kok et al., 2019; Risi & Wickert, 2017; Wickert & de Bakker, 2018). In addition, due to the focus on companies in which the top management has installed a CSR department, our model is limited in capturing actors at lower hierarchical levels that may also exert bottom-up influence to promote implementation. Accordingly, the pace and effectiveness of coordinated enactment may be due to a variety of factors, including the fact that the implementation of new strategies such as CSR is highly uncertain and political (Waeger & Weber, 2019; K. Weber & Waeger, 2017). Future research should also enrich the boundary conditions of our model such as those linked to industry, geography, regulatory context, and intensity of external demands for CSR alongside features of organizational structure such as company size, all of which may either accelerate or hinder implementation (Endenich et al., 2022).

Our analysis suggests that viewing CSR implementation as coordinated enactment based on the different courses of actions is analytically helpful for disentangling the different roles of the departments. Important future research could thus examine how gradually a company may transition from one stage to the next and to what extent this is influenced by the interplay of the top-down and bottom-up dynamics of CSR implementation. For instance, even if companies show (elements of) coordinated enactment, they might become trapped at a particular stage, deliberately stop a course of actions, or abandon CSR altogether if various internal stakeholders resist it. In this regard, our model of CSR implementation as coordinated enactment could be enriched with a focus on values. Such a focus promises further development of the model as values shed light on a company’s CSR actions and interactions with its various stakeholders (Risi et al., 2022) and support the development of insights relevant to both CSR research and practice (Risi, 2022).

Future research could further disentangle the time and resources (i.e., staff and budget) that are required for CSR implementation and which must first be secured by the relevant departments and then effectively employed. Such research may expand on previous insights that engaging in coordinated enactment depends on the willingness and ability of both the CSR department and the functional departments to fulfill their objectives (Durand et al., 2019) and, in doing so, strengthen our ability to explain variance in CSR implementation.

Footnotes

Acknowledgements

The authors thank Associate Editor Thomas Roulet for his excellent guidance during the review process and three anonymous reviewers for their constructive feedback. Our research also very much benefited from comments on earlier versions of this article by Sean Buchanan, Stefano Brusoni, David Chandler, Jennifer Howard-Grenville, Geoffrey M Kistruck, David Kroon, Shenghui Ma, Emilio Marti, Dirk Matten, Kathleen Rehbein, Anselm Schneider, Michael Smets, Mike Valente, and Peter Walgenbach.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Author Biographies