Abstract

Boards of directors affect corporate strategy and decision-making through monitoring of management and resource provision. Recently, an increasing number of studies have examined the relationships between board characteristics and corporate social responsibility (CSR). These studies have yielded inconsistent findings. This article therefore reports the results of a study applying meta-analytical techniques to a sample of 82 empirical studies to help clarify the relationships between board characteristics and CSR. Although prior research has tended to apply relatively simplistic models investigating the impact of individual board characteristics independently and only directly, we adopt a more complex perspective to shed new light on the board characteristics–CSR nexus. Specifically, we use a meta-analytic path model that accounts for the potential interplay between board characteristics in determining CSR and tests whether the presence of a CSR committee plays a meditating role. Our findings suggest that board size, board independence, and female board representation are partially interrelated with each other and jointly influence CSR directly as well as indirectly via the presence of a CSR committee. In addition, we find that country-level institutional factors act as moderators and that the relationships differ with regard to the specific dimension of CSR (i.e., social, environmental, or aggregate).

Keywords

The relationships between corporate board characteristics and firm performance are well researched in the strategic management and corporate governance literature. From an agency theory perspective, boards serve a monitoring function to ensure the alignment of managerial actions with shareholder interests (Fama & Jensen, 1983), reducing agency costs that may arise when managers pursue their own interests at the expense of shareholders. Resource dependence theory (RDT) highlights another function of the board, namely, the provision of access to resources, such as knowledge and networks, critical to firms’ success (Hillman et al., 2000; Pfeffer & Salancik, 1978). Hillman and Dalziel (2003) suggest that both monitoring and resource provision determine the association between board characteristics and firm performance.

While most studies concerned with board characteristics and firm performance focus on financial performance, 1 recently several scholars have investigated the association between board characteristics and corporate social responsibility (CSR), a nonfinancial dimension of firm performance (de Villiers et al., 2011; Walls et al., 2012). CSR has become increasingly prevalent and visible within firms as a mechanism to cope with stakeholder demands and to manage societal expectations beyond firms’ financial aims (H. Wang et al., 2016). Evolving from a long-standing debate about firms’ responsibilities toward society and from an enormous body of empirical work concerned with the relationship between CSR and corporate financial performance, the business case perspective increasingly prevails (i.e., the view that CSR enables firms to enhance their competitive advantage and that firms benefit from CSR in terms of financial performance, Carroll & Shabana, 2010). Recent studies (Eccles et al., 2014; Surroca et al., 2010), as well as earlier meta-analyses (Orlitzky et al., 2003), suggest a positive association between CSR and corporate financial performance. CSR is deemed to create firm value by providing better access to valuable resources (Waddock & Graves, 1997), attracting high-quality employees, (Turban & Greening, 1997), increasing customer value of products and services (Peloza & Shang, 2011), and enabling the development of intangible assets (Hull & Rothenberg, 2008). Consequently, CSR can be seen as a strategic imperative and an increasing number of investors consider CSR in their decision-making (Khan et al., 2016). In view of the strategic importance of CSR and given the decisive role that boards play in corporate strategy and decision-making processes (Kassinis & Vafeas, 2002; Tang et al., 2015), it is important to fully consider reliable scientific evidence regarding the board characteristics associated with superior CSR.

However, the available empirical evidence regarding these relationships is difficult to assess for at least three reasons. First, different studies provide conflicting evidence. For example, Walls and colleagues (2012) find a negative relationship between the number of directors and the environmental dimension of CSR and concluded that smaller boards “[. . .] can mitigate detrimental environmental performance more effectively” (p. 901), whereas Post and colleagues (2011) find a positive relationship between the same constructs, leading them to conclude that “[. . .] having more directors provides boards with more information about environmental issues (rather than the opposite argument that board size leads to chaos and inaction) [. . .]” (p. 211). Similarly, Galbreath (2016) reports a negative relationship between CEO–chair duality (i.e., a CEO that also serves as the chairman of the board) and CSR, whereas Ferrero-Ferrero and colleagues (2015) do not find a significant relationship. Such conflicting empirical results undermine the establishment of credible scientific generalizations, impeding advances in managerial practice and regulatory reform. Second, while studies examine various aspects such as board size, the number of outside directors, or CEO–chair duality and their relationships with CSR, most of them examine the board characteristics in isolation. Thus, while theoretically self-evident, little is known about whether, and how, certain board characteristics may interact with each other in their relationships with CSR (Galbreath, 2016; Oh et al., 2018; Rao & Tilt, 2016). In this vein, Jain and Jamali (2016) conclude from their review on corporate governance and CSR that future research needs to “[. . .] rethink CG [corporate governance] mechanisms as bundles rather than piecemeal” (p. 266). Moreover, prior empirical studies employ overly simplistic models that only investigate direct relationships while potential mediating mechanisms have been neglected. Finally, as CSR is becoming increasingly prevalent on a global scale and while several studies have begun to explore relationships between board characteristics and CSR in different institutional settings (Chang et al., 2017; Young & Thyil, 2014), we have limited knowledge about whether different legal and sociocultural contexts determine the focal relationships. Finally, CSR constitutes a multidimensional construct encompassing a range of aspects, such as employee relations, philanthropy, and environmental performance (Walls et al., 2012; H. Wang et al., 2016), which can be grouped into social and environmental dimensions. However, to date, no quantitative review has investigated the (potentially) different relationships between the social versus the environmental dimension of CSR and board characteristics.

To address and shed light on these issues, we draw on meta-analytic methods to further develop and refine the understanding of the relationship between board characteristics and CSR. Based on the available evidence from prior studies, we examine the relationships between CSR and board size, board independence, female board representation, CEO–chair duality, and the existence of a CSR committee. First, we quantitatively synthesize existing empirical research on the relationships between these board characteristics and CSR by means of random-effects meta-analysis. Second, we specify and test a meta-analytic path model to examine the interplay between board characteristics in determining CSR and to investigate whether the presence of a CSR committee plays a meditating role. Third, we explore potential moderating effects by using meta-analytic regression analysis.

Our study aims to make three contributions to the literature. First, in terms of an empirical contribution, we clarify the direction and strength of the relationships between certain board characteristics and CSR, drawing on cumulative data allowing us to provide more definitive answers than those reported in any single primary study. In particular, our analysis is based on 82 studies providing us with correlations based on a total of 167,317 firm-year observations. Thus, first, we resolve the uncertainties raised in the narrative review of Jain and Jamali (2016), by providing aggregated, generalized evidence regarding the relationships between CSR and the most widely empirically examined board characteristics; second, we move beyond Byron and Post’s (2016) focus on women on boards. While we find that board size, board independence, female board representation, and the presence of a CSR committee are positively related to CSR, we do not find a significant relationship between CEO–chair duality and CSR.

Second, we make a theoretical contribution and advance the literature by hypothesizing and testing a model that (a) accounts for the likely interrelatedness of board characteristics and their joint influence on CSR and (b) incorporates the potential mediating role of the presence of a CSR committee. Hence, we add to the recent literature that applies a more holistic approach and seek to uncover more complex relationships that might be at play in promoting CSR (Aguilera et al., 2012; Jain & Jamali, 2016; Oh et al., 2018).

Third, our article also contributes to theory refinement by showing that country-level factors, as well as the specific dimensions of CSR, moderate the focal relationships. In particular, we provide evidence that investor protection strength moderates the relationships between board size and CSR and between board independence and CSR. We ascribe these results to countries’ investor protection substituting for these board-level influences. Moreover, we find that a country’s level of gender parity moderates the relationship between female board representation and CSR, specifically that countries’ gender parity complements (or amplifies) the effect of female board representation on CSR. Those aspects can be hardly explored by primary studies due to data collection constraints (Jeong & Harrison, 2017). Our findings in this regard establish some boundary conditions on the analyzed relationships and highlight the importance of taking into account macro-contextual factors when studying the relationship between board characteristics and CSR. Finally, our results show that the particular dimension of CSR that is examined (i.e., environmental vs. social dimension) influences board characteristics–CSR relationships. Hence, we add to the growing stream of research that acknowledges the multidimensional nature of CSR and thus seeks to provide a more nuanced understanding of organizational commitment to society (H. Wang et al., 2016). In sum, our study is valuable both for advancing the academic discussion on the relationships between board characteristics and CSR, and for informing business and regulatory practice.

The rest of the article is organized as follows. First, we introduce the constructs used in our meta-analytic examinations and draw on theoretical arguments and prior empirical evidence to derive our hypotheses. Subsequently, we describe our procedures for the identification and coding of the primary studies and outline our methods of analysis. After having presented our findings, we discuss them and conclude with a review of contributions, limitations, and directions for future research.

Theoretical Background and Hypotheses

Construct Definitions and Theoretical Overview

Although several theoretical frameworks have been used to posit links between particular board characteristics and CSR, the relationships between board characteristics and CSR that we examine can be theorized using either agency theory–related arguments, resource provision arguments, or a combination of both. For example, although feminist ethics theories (Boulouta, 2013; Slote, 2007) may inform us about the specific characteristics of female directors, ultimately those characteristics constitute resources (including capabilities and perspectives) that female directors bring into the boardroom, and therefore, the influence of female directors on CSR can be argued and explained by referring to resource dependence theory (Jeong & Harrison, 2017). Agency theory posits that directors serve as agents of firms’ shareholders and play a monitoring role to ensure that managers act in the interest of shareholders, as the owners of the firm (Fama & Jensen, 1983). Vigilant directors can reduce agency costs (Hillman & Dalziel, 2003) and ensure appropriate processes of strategy development and formulation (McNulty & Pettigrew, 1999). RDT, however, emphasizes directors’ role in providing firms with access to resources (Pfeffer & Salancik, 1978) such as networks, knowledge and insight, advice and counsel, legitimacy, and communication channels between the firm and external organizations and parties (Hillman & Dalziel, 2003). Furthermore, directors’ expertise and their access to expanded networks provide reputational benefits and legitimacy to firms (Daily & Schwenk, 1996) and can reduce uncertainty (Hillman et al., 2000).

Our reliance on agency- and resource dependence-related arguments corresponds with a recent stream of literature that emphasizes boards’ duties in protecting shareholders’ wealth as well as creating new wealth (Filatotchev, 2007; Zahra et al., 2009). On one hand, boards must minimize downside shareholder risk by monitoring managers, on the other hand, boards should also enable managerial entrepreneurship so that shareholders and other stakeholders benefit from the upside potential of firms (Filatotchev, 2007). This is consistent with Hillman and Dalziel’s (2003) notion of the two main functions of boards—monitoring and resource provision.

CSR can be defined as the integration of social and environmental concerns into firms’ operations and paying attention to stakeholders’ concerns (Carroll, 1979; Cheng et al., 2014; H. Wang et al., 2016). 2 The most prominent stream in CSR research considers whether CSR adds financial value to the firm. This question can be considered settled for two reasons. First, the available meta-analyses all point to a (weak but) significant positive association between CSR and corporate financial performance (Endrikat et al., 2014; Orlitzky et al., 2003). Second, firms increasingly adopt CSR initiatives due to public awareness and pressure from various stakeholder groups (H. Wang et al., 2016; Ioannou & Serafeim, 2015). The recent United Nations Global Compact-Accenture (2019) CEO Survey shows that 94% of the more than 1,000 participating CEOs from around the world believe that CSR issues are important to the future success of their business. Because of the strategic importance of CSR and the fundamental role of boards in strategy development, boards are considered key players in firms’ CSR activities, being directly or indirectly responsible for firms’ CSR strategy and performance and the consequences thereof (Dixon-Fowler et al., 2017; Kassinis & Vafeas, 2002; Rao & Tilt, 2016).

Prior research has examined a variety of board characteristics. Of course, the constructs in any meta-analysis are restricted to the ones examined with some regularity in the prior literature, which is also the case with this study. Board size refers to the number of board members. Board independence refers to the number or proportion of outside directors (i.e., directors that are independent because they are not part of the management team) (Bergh et al., 2016). In line with Post and Byron (2015), we define female board representation as the number, proportion, or presence of women on boards of directors. CEO–chair duality refers to whether the same person jointly holds the titles of chief executive officer and chairperson of the board (Bergh et al., 2016). We define CSR committee as the existence of a board committee specifically responsible for CSR-related matters, and in practice, these committees may also be referred to as “sustainability,” “corporate ethics,” or ‘environmental” committees (Helfaya & Moussa, 2017).

Board Size and CSR

Regarding the monitoring role of boards—the primary focus of agency theory arguments pertaining to boards of directors—it has been argued that larger boards are more actively involved in monitoring and evaluating activities and are less susceptible to managerial domination (Zahra & Pearce, 1989). According to RDT—highlighting the resource provision function of directors—firms should benefit from larger boards, because there are more directors, who can each provide access to resources, such as specialized knowledge and networks (Hillman et al., 2009; Pfeffer, 1972). In particular, the presence of more directors potentially provides more external links and knowledge to secure critical CSR resources, more CSR-related experience, knowledge, advice, and counsel (Dalton et al., 1999; de Villiers et al., 2011). Therefore, we state the following hypothesis:

Board Independence and CSR

From an agency theory viewpoint, outside directors are better monitors of managers, as they are independent of the top management team and the firm (Dalton et al., 1998; J. L. Johnson et al., 1996). Because CSR goes hand in hand with a more long-term orientation of firms (Eccles et al., 2014) and as CSR activities need some time to translate into firm value (Carroll & Shabana, 2010), outside directors may be more likely to foster CSR, because they tend to pursue longer time horizons and thus are more likely to see the long-term potential of investments in environmental and social projects (de Villiers et al., 2011; Post et al., 2011). Also from an RDT perspective, the number of independent directors should relate positively to CSR because they are more likely to have, and provide, access to alternative sources of CSR-related knowledge and networks, than directors who are associated with the firm. Therefore, our second hypothesis is:

Female Board Representation and CSR

Research from multiple disciplines provides evidence that women differ from men with regard to morals and ethics (Borkowski & Ugras, 1998; Jaffee & Hyde, 2000), educational background and expertise (Hillman et al., 2002), and risk preferences (Croson & Gneezy, 2009). In general, women are deemed to be more concerned with social issues (Elm et al., 2001). Moreover, women have different ways of thinking, have superior communication skills, are less prone to suffer from overconfidence, and provide unique resource portfolios, including distinct risk-taking attitudes (Huang & Kisgen, 2013; Jeong & Harrison, 2017), which are likely to predispose them toward a positive attitude toward CSR. A recent meta-analysis—exclusively focusing on women on boards and CSR—found a positive relationship between female directors and CSR (Byron & Post, 2016). However, we deem it meaningful to reexamine this relationship for two reasons. First, we embed this relationship in our meta-analytic path model testing the mediating role of CSR committees. Second, we complement the findings of Byron and Post (2016) by investigating potential differences between the environmental and the social dimension of CSR in our moderator analyses. 3 We state the following hypothesis:

CEO–Chair Duality and CSR

Above, we argued that board independence is likely to be positively related to CSR. One aspect that can undermine a board’s independence is the leadership structure of the board. A CEO that also serves as chair of the board (i.e., CEO–chair duality) may not be trusted by shareholders to effectively monitor his or her own activities as CEO. CEO–chair duality also induces management entrenchment and thus decreases the monitoring effectiveness of the entire board (Finkelstein & Aveni, 1994). In essence, CEO–chair duality increases information asymmetry between the CEO and the board and strengthens managerial power in the boardroom, as a CEO–chair is able to monopolize board meetings and advance his or her own agenda to the detriment of the firm (de Villiers et al., 2011; Finkelstein & Aveni, 1994). In the context of CSR, this would imply that it is easier for short-term-oriented, profit-maximizing CEOs to advance their own agenda at the expense of long-term CSR-related investments if they are also chair of the board (de Villiers et al., 2011). In contrast, separate CEO and chair positions provide further checks and balances and may prevent that a CEO can divert board attention away from CSR activities that are likely to have longer payback periods (Galbreath, 2018a). We therefore propose the following hypothesis:

Mediating Role of the Presence of a CSR Committee

So far, we have followed the majority of the prior literature and provided arguments for direct relationships between CSR and each board characteristic. However, the relationships between board characteristics and CSR might be more complex than most of the existing research suggests. Some recent articles set out that previous models have been overly parsimonious in that they ignore the possibility of interweaving characteristics and overlook mediating factors that may link board characteristics and firm outcomes (Post & Byron, 2015; Post et al., 2015; Pye & Pettigrew, 2005). We build on this line of thought and examine a more advanced model. In particular, we argue that the presence of a CSR committee may partially mediate the relationships between the other board characteristics and CSR. Thus, board size, board independence, female representation on boards, and CEO–chair duality may not only have direct effects on CSR but also indirect effects translated into CSR via the presence of a CSR committee.

Specific committees as subgroups of the board have long been neglected by empirical research, but have recently attracted growing attention (S. G. Johnson et al., 2013; Kolev et al., 2019; Neville et al., 2019). These committees, with narrowly defined objectives, such as audit or compensation committees, are deemed to be of significant importance, as many of the critical processes and decisions of boards with regard to a firm’s policy and strategy, may derive from them (Dalton et al., 1998; Dixon-Fowler et al., 2017). Board committees serve a management support function as they enable directors to cope with the limited time that they have available and to deal with the complexity of information (Lorsch & MacIver, 1989). Moreover, equipped with specialized responsibilities and authorities, board committees also serve a monitoring function (Dixon-Fowler et al., 2017; Harrison, 1987).

While firms began to adopt committees focusing on social and environmental issues during the 1970s (Harrison, 1987), recent studies document an increasing number of firms establishing CSR committees (Institute of Business Ethics, 2016; Spitzeck, 2009). The typical activities carried out by CSR committees comprise the creation, implementation, and updating of environmental and social policies, the assessment of a firm’s resource allocation decisions, and the coordination and monitoring of CSR-related issues (Gennari & Salvioni, 2019). That is, CSR committees oversee a firm’s impact on different stakeholders, such as communities, the environment, or employees, but also the specific interests of these groups, and thus can develop opportunities that may generate and protect shareholder value and also serve as a high-level control mechanism preventing downside risk from irresponsible firm behavior (Burke et al., 2019). Paine (2014) illustrates how Nike benefited from its CSR committee, and was transformed from being attacked by labor activists and non-governmental organizations (NGOs) to pioneering responsibility toward social and environmental issues. In addition, the presence of a CSR committee is a signal of a firm’s commitment and orientation toward CSR for both external stakeholders and organizational members (Mallin & Michelon, 2011; Walls et al., 2012).

We argue that the presence of a CSR committee is likely to mediate the relationships between the other board characteristics and CSR. Thus, board size, board independence, female representation on boards, and CEO–chair duality may have not only direct effects on CSR but also indirect effects translated into CSR via the presence of a CSR committee. The establishment of a CSR committee is a voluntary and deliberate decision. Unlike compensation and audit committees, which are often mandated (e.g., in the United States), CSR committees are purely voluntary (Dixon-Fowler et al., 2017). Thus, the establishment of a CSR committee can be seen as a conscious strategic decision to actively foster social and environmental responsibility and to explicitly take responsibility for nonshareholding stakeholders’ interests (Eccles et al., 2014). Or in other words, the formation of a CSR committee is a way to institutionalize CSR in a firm (Gennari & Salvioni, 2019). Moreover, several researchers suggest that board committees influence firm outcomes in a more meaningful way than the board as a whole (Daily & Schwenk, 1996; Dalton et al., 1998; Dixon-Fowler et al., 2017). That is because the most important board decisions are taken in a specialized committee rather than at the more general board level (Kesner, 1988). Moreover, by means of a CSR committee, firms explicitly assign responsibility to specific individuals and hold them accountable, also to specific stakeholder groups (Burke et al., 2019). For example, while a higher proportion of females on the board may generally provide the impetus for a proactive CSR strategy, a CSR committee that coordinates and reviews CSR-related activities and proposed investments are more likely to effectively translate general intentions into CSR outcomes. A CSR committee can also serve as a buffer, mitigating potential negative effects of CEO–chair duality on CSR activities. Therefore, we hypothesize the following:

Moderators of Board Characteristics–CSR Relationships

Meta-analysis not only determines the overall strength and direction of a relationship but also allows for an examination of potential moderating effects. In this sense, meta-analysis allows the identification of boundary conditions that cannot be explored by primary studies that rely on data within these boundaries. We next hypothesize possible moderators of the focal board characteristics–CSR relationships.

An emerging stream of literature highlights the importance of country-level institutional factors in determining firm strategies and practices (Carney et al., 2011; Heugens et al., 2009). CSR practices and activities have also been shown to be contingent upon institutional settings, such as the legal and political systems, regulatory stringency, and culture (Jain & Jamali, 2016). CSR activities usually affect firm outcomes indirectly via stakeholders’ reactions (H. Wang et al., 2016). Given that stakeholder attitudes vary across countries (Matten & Moon, 2008), it is not surprising that CSR-related relationships vary by country (Ioannou & Serafeim, 2012).

Moreover, previous research has shown that both formal and informal institutional mechanisms significantly determine corporate governance practices and characteristics of the boards of directors (Aguilera & Jackson, 2010; Grosvold, 2011; J. Li & Harrison, 2008). In fact, scholars argue that the mixed empirical findings in corporate governance studies may be due to the neglect of contextual issues (Aguilera et al., 2012; Filatotchev, 2008). In particular, it is argued that certain country-level governance systems, such as corporate ownership structures, the legal system, and corporate law, significantly determine the effectiveness of corporate governance. This implies that these country-level factors could substitute or complement corporate governance aspects. Mechanisms are substitutes when an increase in one mechanism directly replaces a portion of the other (i.e., functional replacement); in contrast, two mechanisms are complements when an increase in one leads to an increasing effect of the other mechanism (i.e., synergistic effect) (Aguilera et al., 2012). For example, long-term bank-firm relationships, which are typical for Germany and Japan, may effectively substitute for an active market of control (Filatotchev, 2007). Or high levels of blockholder ownership may partially substitute for board independence (Aguilera et al., 2012; Oh et al. (2018)).

One of the key institutional factors affecting corporate governance choices is shareholder protection (La Porta et al., 2000; Leuz et al., 2003). Strong and well enforced legal protection of shareholder rights limits expropriation risks and may decrease the need for boards of directors to monitor and avoids managerial discretion (Villarón-Peramato et al., 2018). Thus, strong shareholder protection might effectively substitute for the monitoring role of corporate boards implying weaker effects of board characteristics on CSR.

However, an alternative argument has been brought forward by Post and Byron (2015). They propose that stronger shareholder protection may provide increased motivation to corporate boards to strive for and take into account the multiple perspectives of board members and to integrate the divergent expertise and values held by different board members (Byron & Post, 2016; Post and Byron, 2015). Hence, shareholder protection is likely to motivate boards to more effectively capitalize on their CSR resources, suggesting that shareholder protection could complement—instead of substitute for—boards characteristics’ impact on CSR. Given the two competing perspectives, we offer a nondirectional hypothesis: 4

Post and Byron’s (2015) meta-analysis on the relationship between female board representation and firm financial performance finds that a country’s level of gender parity significantly moderates the relationship. Byron and Post (2016) show that this country-level factor also moderates the relationship between female board representation and CSR. In contexts with greater gender parity (i.e., contexts in which men and women are more similar in terms of education, economic participation, health, and political empowerment), the distribution of power between male and female board members will be more balanced and thus women will be more likely to be heard and considered in decision-making processes (Byron and Post, 2016). In other words, a country’s level of gender parity may complement the positive effect of female board representation on CSR. Because our sample of studies differs from those of Byron and Post (2016) in that we include more recent studies—in particular, studies published after the year 2015, which is the last year covered by Byron and Post (2016)—we deem it necessary to revisit these relationships. We hypothesize the following: 5

CSR is a multidimensional construct (Rowley & Berman, 2000; H. Wang et al., 2016). Different studies use different measures of overall CSR performance and/or different measures of specific dimensions of CSR. Aggregate measures of CSR subsume dimensions that are not necessarily related to each other, such as environmental performance and social performance (H. Wang et al., 2016). The environmental and social aspects of CSR differ substantially, because environmental issues tend to be more systemic, affect multiple organizational and operational functions, and involve factors that are internally focused (Dixon-Fowler et al., 2017; Russo & Fouts, 1997). Therefore, it is likely that the relationships between board characteristics and CSR systematically differ depending on whether an aggregate measure of CSR is used or whether a measure explicitly focusing on the environmental or the social dimension of CSR is applied in primary studies. Hence, acknowledging the importance of unpacking the dimensions of CSR and to provide a more fine-grained analysis, our final hypothesis is:

Method

Identification of Studies

We employed three complementary procedures to identify prior empirical studies. First, we conducted a key word search in the following databases: Business Source Complete, Science Direct, JSTOR, and Wiley Online Library, using the following search string: (“board” OR “CEO” OR “corporate governance”) AND (“CSR” OR “corporate social” OR “environmental performance” OR “environmental responsibility” OR “sustainability”). Second, we searched for unpublished manuscripts in the Social Science Research Network database. Third, we employed an ancestry approach (Aguinis et al., 2011) and searched through the reference lists of the studies identified in the preceding steps and in the narrative review of Jain and Jamali (2016) and the meta-analysis of Byron and Post (2016).

To be included in our analysis, studies needed to report a bivariate correlation between our focal board characteristic constructs and a measure of CSR (i.e., a measure of aggregate CSR or the environmental or the social dimension of CSR). The constructs from which correlations are reported did not have to be the main focus of the study (Dalton & Dalton, 2005). This procedure is in line with general meta-analytic practice (Geyskens et al., 2009) and potentially decreases the risk of biased meta-analytic results due to publication bias—the fact that statistically significant results are more likely to have been published (Post & Byron, 2015).

The final set of studies included in our analyses consists of 82 primary studies representing a total of 167,713 observations. These studies were published between the years 1991 and 2019 with a clear trend toward more studies being published in more recent years. The references of the studies used for the meta-analytic calculations are included in the supplemental file available online.

Coding of Studies

We coded the effect sizes of the focal relationships (i.e., the relationships between board characteristics and CSR), the effect sizes of the relationships between the board characteristics, because we need them for our meta-analytic path models, as well as information needed for our analyses of potential moderating effects. We initially coded a set of studies to establish and validate the coding rules, resolving ambiguous cases and differences in coding through discussion, before reaching consensus (Sleesman et al., 2012). Next, the first author of this study completed the rest of the coding. Finally, to ensure the accuracy and reliability of the coding, we had an independent rater (postgraduate in management) that coded approximately one quarter (k = 20) of the studies (Carpenter & Berry, 2017). Apart from some minor discrepancies that were resolved through communicative validation (Kvale, 1995), the overall agreement was high and the calculated Cohen’s Kappa (.92) suggests almost perfect reliability (Landis & Koch, 1977).

Studies in our sample measured board size as the number of board members. In one study (Bai, 2013), the number of directors was scaled by the size of the organizations. Board independence was measured by means of the number or proportion of outside directors. In cases where studies measured the number, proportion, or ratio of inside directors, we converted the sign of the correlation. The primary studies measured female board representation in different ways. In the majority of studies, the number or proportion of women on boards was used as a measure. Two studies (Jia & Zhang, 2012; Post et al., 2011) used a critical mass measure, which equals 1 if the board consists at least of three women. CEO–chair duality was either measured as binary variable equaling 1 if the CEO also serves as chairperson of the board or in a reverse manner (i.e., a variable that equals 1 if the CEO is not the chairman) (Surroca & Tribó, 2009). In the latter case we converted the sign of the correlation. With regard to the presence of a CSR committee, we conformed to the existing literature (Dixon-Fowler et al., 2017; Mallin & Michelon, 2011) and regarded “environmental committees,” “sustainability committees,” or “corporate ethics committees” as CSR committees. Our focal dependent construct, CSR, was measured in a variety of ways, reflecting its multidimensional nature. Most of the studies in our sample use aggregate measures of CSR combining different environmental and social aspects (e.g., aggregate indices based on the items of the Kinder, Lydenberg, and Domini [KLD] database). For our moderator analysis, we were primarily interested in potential differences between the environmental and social dimensions of CSR (Bansal et al., 2014). Therefore, we sought to keep these dimensions apart whenever it was possible. In particular, we built composites in the case of studies using different subdimensions of the social dimension of CSR (e.g., community-related CSR measures and employee-related CSR measures) as well as in the case of studies using multiple subdimensions of the environmental dimension of CSR (e.g., measures of waste and measures of toxic waste). 6 Apart from the moderator analysis pertaining to the specific dimension of CSR, we included both effect sizes in our analyses when a study reported correlations for both the environmental and the social dimension. This procedure is in line with other recent meta-analyses (Lander & Heugens, 2017; Mutlu et al., 2018) and is deemed to outperform procedures using only a single effect size according to Bijmolt and Pieters (2001). In cases where studies measured corporate social irresponsibility, such as environmental lawsuits (Kassinis & Vafeas, 2002) or the amount of carbon emissions (Haque, 2017), we converted the sign of the correlation.

Apart from the distinction between the environmental and the social dimension of CSR, we examine two country-level institutional factors as potential moderators. First, with regard to all relationships between board characteristics and CSR, we explore the influence of shareholder protection strength. Therefore, we coded each study using the value of the investor protection index provided by the World Economic Forum (Schwab, 2018). The index ranges from 0 to 10, with higher index values indicating better shareholder protection, and comprises of three dimensions: (a) the extent to which there is transparency of related-party transactions, (b) the extent to which directors are held liable for self-dealing, and (c) the ease with which shareholders can sue for director misconduct. For single-country studies, we coded the index associated with that country. For studies covering multiple countries (i.e., six or fewer countries), we calculated the average index for those countries. Studies using large multicountry samples were excluded from this moderation analysis. This procedure follows Post and Byron (2015). With regard to the relationship between female representation on boards and CSR, we explore the potential moderating effect of a country-level measure of gender parity. We coded each study using the World Economic Forum’s (2018) gender gap index. This index ranges from 0 to 1 with higher index values indicating greater gender equality in terms of economic participation, educational attainment, health and survival, and political empowerment. In cases of multicountry samples, we follow the same procedure as we did for the shareholder protection index.

Meta-Analytic Procedures

We used the software Meta-essentials (Suurmond et al., 2017) and calculated random-effects models assuming the variability between effect sizes is due to sampling error in addition to the variability in the population (Lee et al., 2017; Lipsey & Wilson, 2001). In line with prior meta-analyses (Jeong & Harrison, 2017; Lee et al., 2017; Lee & Madhavan, 2010) and following Hedges and Vevea (1998), correlations were first transformed using Fisher’s z transformation, because the sample correlation r is not an unbiased estimator of the population r (Dalton & Dalton, 2005; Hunter & Schmidt, 2004). Z-transformed correlations have statistical properties of being approximately normally distributed. Furthermore, according to Geyskens and colleagues (2009), this procedure ensures an optimal weighting of effect sizes as the sample variance depends only on sample size and not on the population itself. We computed 95% confidence intervals to assess the significance of the mean effect sizes. A confidence interval that does not include zero indicates that the mean effect size is statistically significant (Lipsey & Wilson, 2001). To test the homogeneity of the effect size distributions, we used Q statistics and I2 statistics. The Q statistic represents total dispersion in effect sizes and reflects the need to test moderators when it is significant (Allan et al., 2018; Lipsey & Wilson, 2001). The I2 statistic refers to the amount of observed variance that is due to true differences among the studies, rather than error (Allan et al., 2018). Significant heterogeneity suggesting the presence of moderating effects is indicated when the Q statistic is significant and the I2 statistic suggests that there is a significant amount of variance attributed to true differences (i.e., I2 greater than 75%) (Allan et al., 2018).

One potential problem of meta-analysis is the file drawer problem, also called publication bias, which refers to circumstances in which “the research that appears in the published literature is systematically unrepresentative of the population of completed studies” (Rothstein et al., 2005, p. 1). This might occur when the decision to submit or publish studies is influenced by the magnitude, direction, or significance of the study’s findings in such a way that findings that, for instance, are not statistically significant are less likely to be published (Geyskens et al., 2009). We addressed this issue by calculating the fail-safe N that provides an estimate of the number of null-effect studies that would be needed to render the mean effect insignificant (Rosenthal, 1979).

We used the meta-analytically derived mean correlations between board characteristics and CSR, as well as the intercorrelations among the board characteristics, to conduct meta-analytic path analysis (Bergh et al., 2016; Viswesvaran & Ones, 1995). For this purpose, we used the meta-analytic correlation matrix as input for MPlus 8.2. Consistent with prior studies, we used the harmonic mean sample size from the correlation matrix as the sample size for our analysis (Allan et al., 2018; Jeong & Harrison, 2017). Meta-analytic path modeling allows us to examine simultaneously the relationships among the board characteristics and with CSR. Moreover, it enables us to test H6 about the (partial) mediation of the presence of a CSR committee.

For examining our hypotheses regarding potential moderating effects, we used random-effects meta-regression analyses (Jeong & Harrison, 2017; Lipsey & Wilson, 2001), in which the dependent variable is the meta-analytically derived mean correlation for a certain relationship and the independent variables are the suggested moderators. A significant beta coefficient suggests that the examined factor moderates the focal relationship.

Results

Bivariate Analyses of the Relationships Between Board Characteristics and CSR

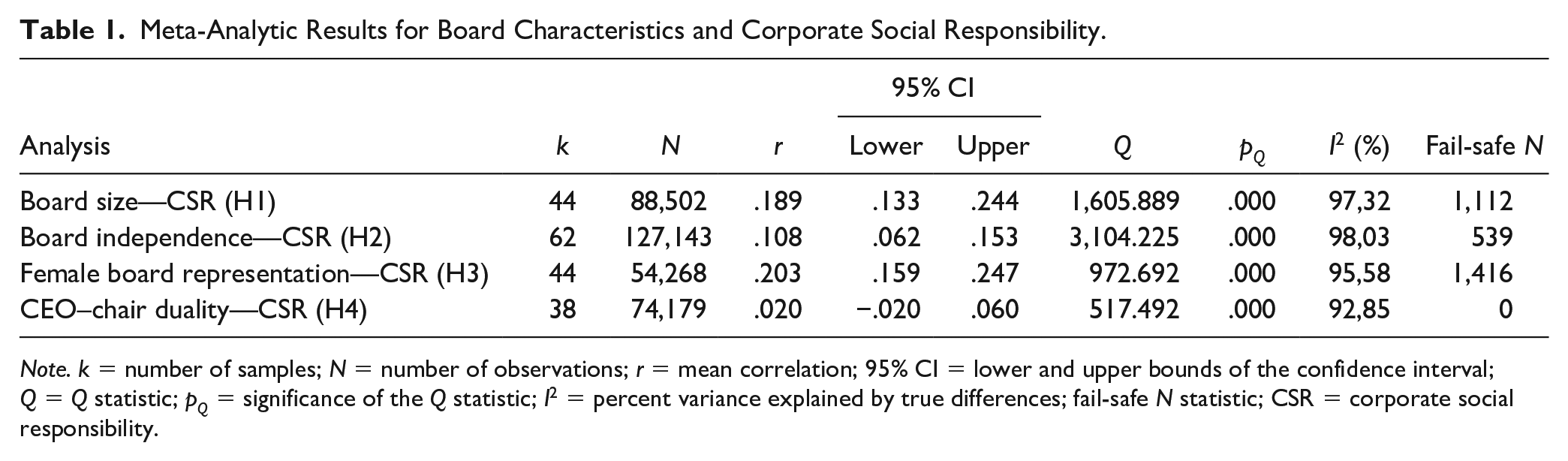

Table 1 presents the results of the meta-analyses for the different relationships between board characteristics and CSR.

Meta-Analytic Results for Board Characteristics and Corporate Social Responsibility.

Note. k = number of samples; N = number of observations; r = mean correlation; 95% CI = lower and upper bounds of the confidence interval; Q = Q statistic; pQ = significance of the Q statistic; I2 = percent variance explained by true differences; fail-safe N statistic; CSR = corporate social responsibility.

For the relationship between board size and CSR, we find a positive and significant mean correlation (r = .189; 95% CI = [.133, .244]), lending support for H1. In H2, we predicted a positive relationship between board independence and CSR. The meta-analytic effect size is positive and statistically significant (r = .108; 95% CI = [.062, .153]), thus supporting H2. Also H3, predicting a positive relationship between female board representation and CSR, receives empirical support (r = .203; 95% CI = [.159, .247]). Regarding the relationship between CEO–chair duality and CSR (H4), we suggested a negative relationship. The small and non-significant mean correlation (r = .020; 95% CI = [−.020, .060]) does not support this hypothesis.

For all significant relationships, the calculated fail-safe N suggests robustness of our findings in terms of a bias against the publication of null findings. The number of null-effect findings that would be needed to overturn the relationships are all above the tolerance level suggested by Rosenthal (1979). 7

The Q statistics and the I2 statistics reject the assumption of homogeneity for hypotheses H1 to H4. Thus, moderator analyses are warranted for all of these board characteristics–CSR relationships.

Meta-Analytic Path Model Results

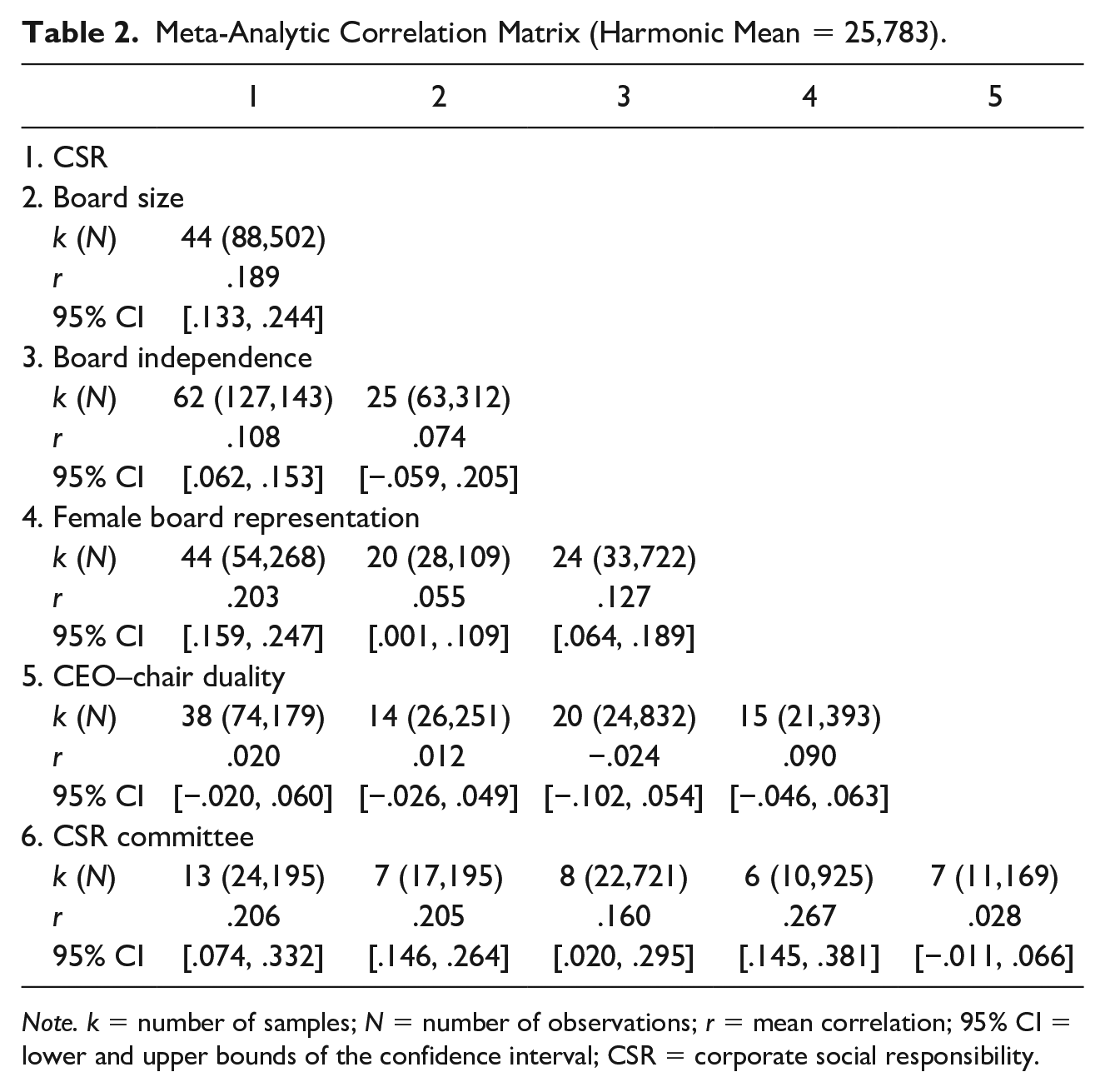

Table 2 shows the meta-analytic correlation matrix used as input to test our meta-analytic path model.

Meta-Analytic Correlation Matrix (Harmonic Mean = 25,783).

Note. k = number of samples; N = number of observations; r = mean correlation; 95% CI = lower and upper bounds of the confidence interval; CSR = corporate social responsibility.

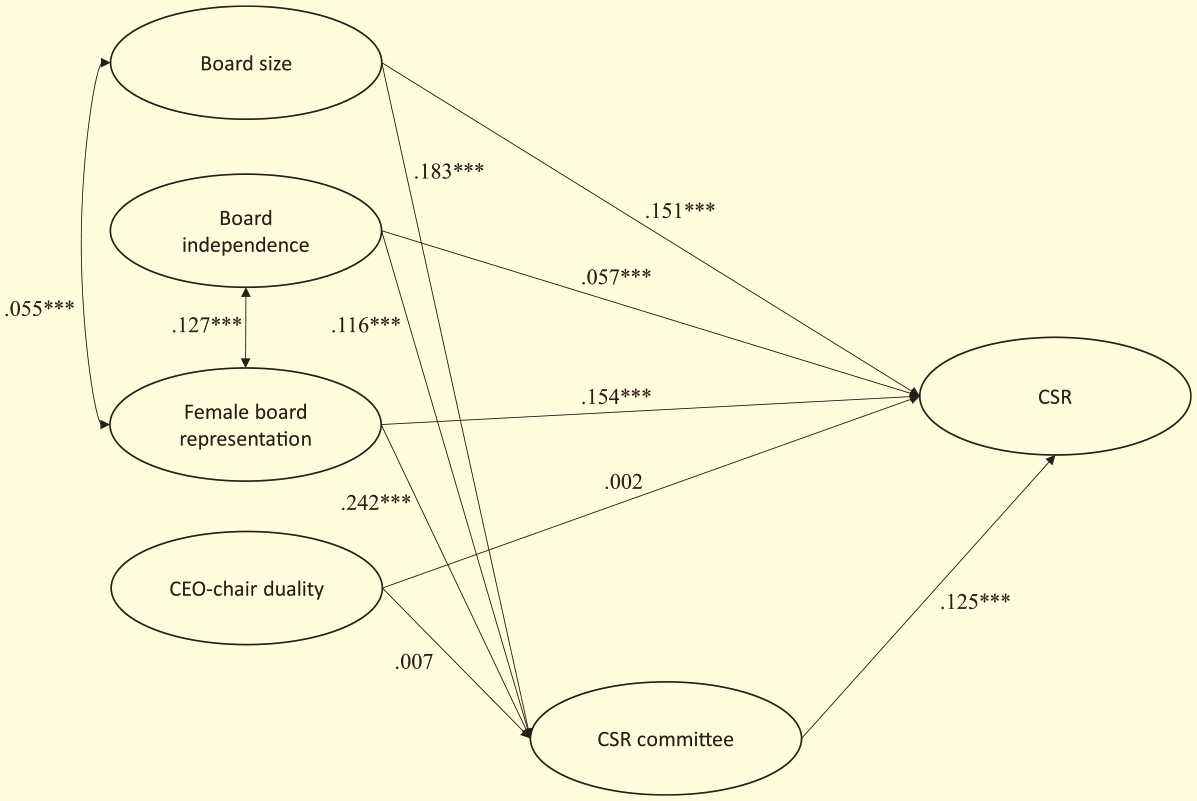

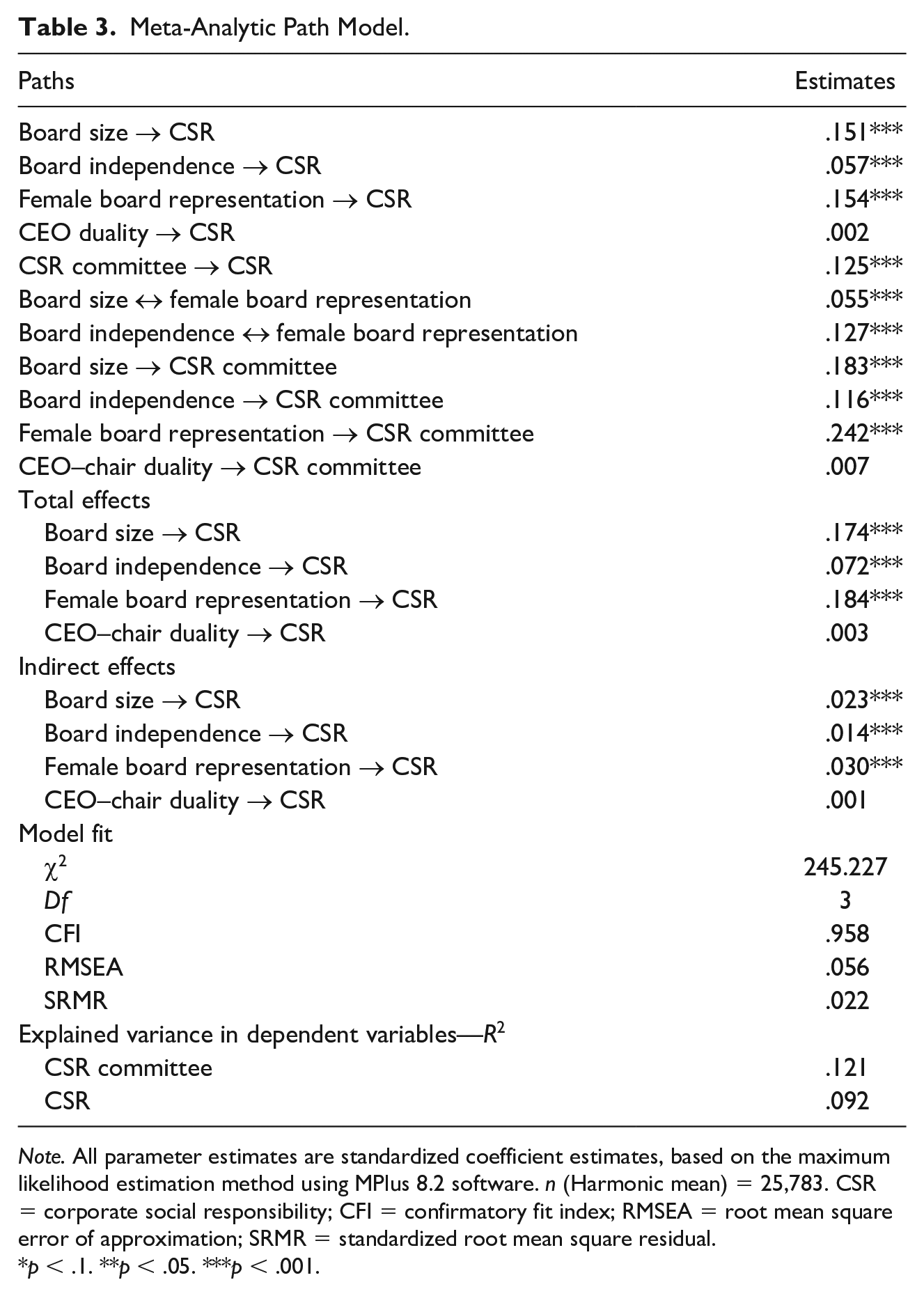

We test a model (displayed in Figure 1) in which the presence of a CSR committee partially mediates the relationships between CSR and the other board characteristics: board size, board independence, female representation on boards, and CEO–chair duality. We allow those board characteristics, which displayed significant mean correlations in the meta-analytic correlation matrix (Table 2), to covary with each other. As reported in Table 3, the model fits the data in an acceptable manner (comparative fit index [CFI] = .958, root mean square error of approximation [RMSEA] = .056, standardized root mean square residual [SRMR] = .022) and all paths are significant, except the path linking CEO–chair duality to CSR directly and the path linking CEO–chair duality to the presence of a CSR committee. The indirect effects on CSR that are channeled through the presence of a CSR committee are significant for board size (β = .023; p < .001), board independence (β = .014; p < .001), and female board representation (β = .030; p < .001). Thus, H5 is supported suggesting a partial mediation of the presence of a CSR committee, except for CEO–chair duality, which is neither directly (β = .002; p = .708) nor indirectly related to CSR (β = .001; p = .242) and is also not significantly related to the presence of a CSR committee (β = .007; p = .241). Thus, our meta-analytic path model results further corroborate the findings from our bivariate analyses and supports H1, H2, and H3. 8

Results of meta-analytic path modeling.

Meta-Analytic Path Model.

Note. All parameter estimates are standardized coefficient estimates, based on the maximum likelihood estimation method using MPlus 8.2 software. n (Harmonic mean) = 25,783. CSR = corporate social responsibility; CFI = confirmatory fit index; RMSEA = root mean square error of approximation; SRMR = standardized root mean square residual.

p < .1. **p < .05. ***p < .001.

Meta-Regression Results

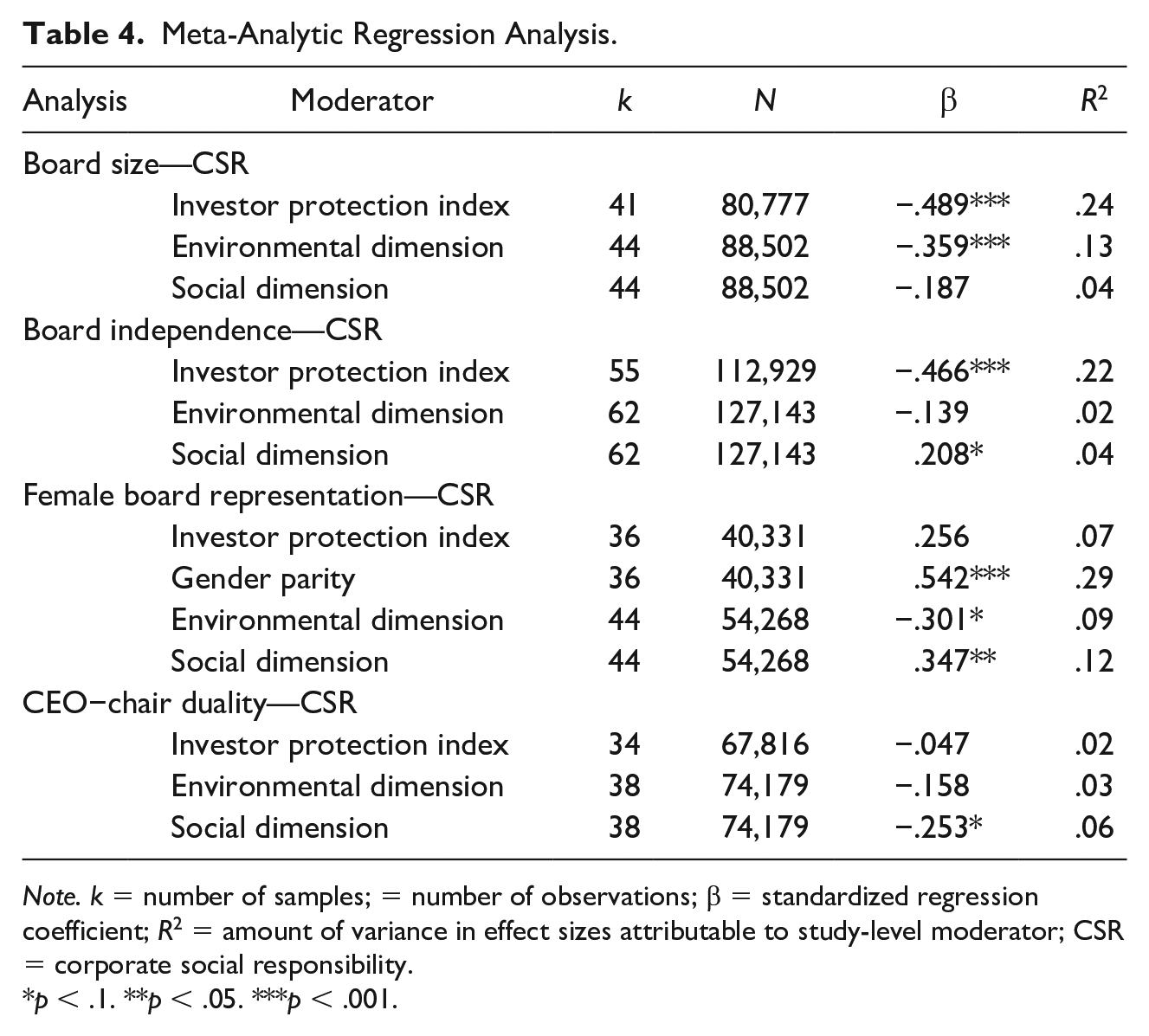

To test our hypotheses concerning potentially moderating effects, we estimated random-effects meta-regression models. Table 4 reports the results. Regarding H6, concerning the influence of countries’ shareholder protection strength, we find significantly negative effects regarding the relationships between board size (β = −.489; p < .001) and CSR and board independence and CSR (β = −.466; p < .001) (i.e., the positive relationships are significantly weaker in countries with stronger levels of shareholder protection). 9

Meta-Analytic Regression Analysis.

Note. k = number of samples; = number of observations; β = standardized regression coefficient; R2 = amount of variance in effect sizes attributable to study-level moderator; CSR = corporate social responsibility.

p < .1. **p < .05. ***p < .001.

In H7, we hypothesized that countries’ level of gender parity moderates the relationship between female board representation and CSR. Our results show a significantly positive effect (β = .542; p < .001), providing evidence that the relationship between female board representation and CSR is more positive for firms in countries with greater gender parity. This result is in line with the finding of Byron and Post (2016).

Our hypothesis H8 was about possible differences in the relationships depending on whether the environmental or the social dimension of CSR is examined. To test this hypothesis, we included dummy variables in the regression models taking the value of 1 when the measurement of CSR in the study focused on the environmental dimension of CSR (or social dimension respectively) and 0 in the case of aggregate CSR measures. 10 We find that an exclusive focus on the environmental dimension significantly weakens the relationship between board size and CSR (β = −.359; p = .002) and the relationship between female board representation and CSR (β = −.301; p = .054). We also find that an exclusive focus on the social dimension significantly strengthens the relationship between board independence and CSR (β = .208; p = .073), and the relationship between female board representation and CSR (β = .347; p = .013), but weakens the relationship between CEO–chair duality and CSR (β = −.253; p = .051). However, given that we found that the CEO–chair duality—CSR relationship is not significant, this finding should be interpreted with caution.

Discussion

The relationships between board characteristics and CSR are examined by many empirical studies, often yielding conflicting results and raising further questions. In addition, prior research typically relied on simple models that fail to account for possible interrelationships between different board characteristics and ignore mediating mechanisms that might be at play. Finally, very little attention has as yet been paid to potential boundary conditions of the relationships. Our meta-analytic study clarifies several of those issues.

Joint Effects of Board Characteristics on CSR and Mediating Role of the Presence of a CSR Committee

Our results show that board size, board independence, female board representation, and the presence of a CSR committee are positively related to CSR. Thus, we find empirical support for our arguments based on a combination of agency theory and resource dependence theory, suggesting that boards influence CSR by way of their monitoring function and their resource provision function (Hillman & Dalziel, 2003). Furthermore, our meta-analytic path model suggests that board size, board independence, female board representation, and the presence of a CSR committee are partially interrelated with each other (i.e., board size with female board representation and board independence with female board representation) and jointly influence CSR (i.e., operate in conjunction, Jain & Jamali, 2016). Hence, our results contribute to the literature by suggesting the need for future studies to use more complex models that acknowledge these joint effects. Studies that fail to account for the interrelatedness of board characteristics risk to provide inaccurate estimates and erroneous inferences about the relationships under study. Therefore, we strongly encourage research to take a more holistic approach and to examine how board characteristics operate as a complex nexus or a bundle of complements and substitutes. Although this “bundle of governance mechanisms” perspective harks back to Rediker and Seth (1995), to our best knowledge, only Oh and colleagues (2018) have applied this insight in a CSR context. In terms of methodology, qualitative comparative analysis can be a meaningful approach, which has recently been applied by Misangyi and Acharya (2014). This approach would allow disentangling possible manifestations of board characteristics that combine effectively with each other (Misangyi and Acharya, 2014).

Furthermore, our research adds to the literature that suggests that board committees may be more meaningful predictors of firm outcomes than the board characteristics themselves (Daily, 1994; Dalton et al., 1998; Dixon-Fowler et al., 2017). Our evidence that the presence of a CSR committee channels the impacts of board size, board independence, and female board representation on CSR show the importance of board committees in general and CSR committees in particular. Many critical board processes and decisions take place in committees (Dalton et al., 1998; Kesner, 1988). Especially where specialized knowledge and complex decisions are involved, such as CSR, dedicated committees enable boards to function more effectively (Dixon-Fowler et al., 2017). Therefore, in line with Neville and colleagues (2019) for instance, we contend that a more explicit focus on characteristics at the committee-level, instead of the board-level, may provide a more nuanced understanding. In sum, future research should further disentangle the interplay between board characteristics, board committees, and CSR.

Insignificant Relationship of CEO–Chair Duality

Our finding of an insignificant relationship between CEO–chair duality and CSR suggests that CEO–chair duality per se neither fosters nor undermines CSR. Thus, while CEO–chair duality is among the most widely examined aspects in corporate governance research and is of continuing interest to shareholder activists and institutional investors (Dalton & Dalton, 2011; Dalton et al., 1998), we find no generalizable evidence for an effect on CSR. CEO–chairs with positive attitudes toward social and environmental issues may use their power to promote CSR, while CEOs who do not regard CSR as important or who lack CSR expertise may undermine CSR. Thus, our study may encourage future research to go beyond the coarse-grained duality construct and examine more specific CEO attributes, such as education, experience, or values and beliefs, and whether the CEO–chairs are founders, heirs, or professional managers (Aguinis & Glavas, 2012; Siegel, 2014; Tang et al., 2015, 2018).

Moderating Effects in the Relationships Between Board Characteristics and CSR

Our study also sheds light on potential boundary conditions that may alter the relationships between board characteristics and CSR. First, we show that a country’s shareholder protection strength weakens the positive effects of board size and board independence on CSR (i.e., in contexts associated with higher levels of accountability and liability of the board), CSR is well managed by most companies, and therefore, board characteristics do not have a major impact. These findings suggest that high levels of legal and regulatory shareholder protection can substitute for positive board-level impacts on CSR, which is in line with the literature that emphasizes the need to consider the role of the institutional context in corporate governance research (Aguilera et al., 2012; Yoshikawa et al., 2014). Future research that examines this substitution hypothesis more comprehensively would be a worthy pursuit.

We also investigated gender parity as a country-level moderator and our finding confirms previous meta-analytic evidence (Byron & Post, 2016; Post & Byron, 2015). Our findings show that a country’s level of gender parity reinforces or complements the positive effect that women on boards have on CSR (i.e., women on boards can best accomplish higher levels of CSR in countries where they enjoy greater equality in terms of economic participation, educational attainment, or political empowerment). Future research may seek to explore how much of the positive effect of female board representation is due to the superior resources (i.e., knowledge and experience) that women may bring in countries with greater gender equality, compared with other contexts; how much is due to their different values and beliefs; and how much is due to the fact that women, even those on boards, may be less powerful in countries with greater inequality.

Finally, our moderator analysis reveals that the board characteristic relationships are stronger for the social dimension of CSR and weaker for the environmental dimension. Environmental issues are often more technical than social matters and thus require firms to focus on science and to implement technological solutions to production processes (Bansal et al., 2014). These technical solutions to environmental concerns often rely on internal processes, whereas approaches regarding social concerns tend to be more dependent on the actions of external stakeholders (Bansal et al., 2014). Thus, the CSR-related resource provision role of directors via larger boards and specific committees may be more conducive to the social dimension of CSR than the environmental dimension. The stronger relationship between female directors and the social dimension compared with the environmental dimension might be explained by a generally stronger propensity of women to focus on social issues that can be seen as “soft issues” in contrast to environmental issues that tend to be more technical in nature (Rao & Tilt, 2016). Acknowledging that both broad and specific theories and insights are desirable (Edwards, 2001; Weick, 1979), we encourage researchers to use both aggregated and disaggregated measures to provide further insights.

Limitations and Additional Future Research Directions

In common with all studies, there are several limitations that should be noted and which potentially indicate future research opportunities. First, our reliance on meta-analytic path modeling does not allow us to explore the interrelatedness of board characteristics by introducing interaction terms or using conditional correlation approaches. We encourage primary studies to explore these interactions.

Second, different studies use different measures for CSR. The environmental dimension is sometimes measured at a very specific operational level (e.g., by means of data from the Toxic Release Inventory of the Environmental Protection Agency, or by water productivity measures), and at other times in generic terms based on ratings, such as the MSCI KLD database. Similarly, the social dimension is measured in diverse ways, sometimes using MSCI KLD data, or at other times philanthropic activities outside the firm, such as charitable contributions. We were unable to analyze the effects of different measures in detail, which might be a fruitful avenue for further research.

Finally, meta-analyses are inherently limited in testing causality (Jeong & Harrison, 2017). Should primary studies employ time lags between the dependent and independent variables, a meta-analysis could—to some extent—infer causality (Endrikat et al., 2014). However, this is not the case for our sample of primary studies. As it is likely that certain board characteristics manifest their effects on CSR only after a certain period of time, addressing temporal effects could be a fruitful avenue for future research.

Conclusion

This meta-analysis addresses the current state of research concerning the relationships between board characteristics and CSR. We show that board size, board independence, female board representation, and the presence of a CSR committee positively relate to CSR. As regards the relationship between CEO–chair duality and CSR, we do not find a significant effect. Thus, our study helps to reconcile mixed evidence provided by primary studies. Moreover, we provide evidence consistent with the views that (a) board size, board independence, and female board representation jointly determine CSR and (b) the presence of a CSR committee mediates these relationships. In this regard, our study adds to the recent literature promoting more holistic approaches in studying board characteristics. Finally, we highlight important boundary conditions that alter the focal relationships. Our results suggest that macro-contextual factors such as countries’ investor protection strength and gender parity act as moderators. In particular, we find that stronger shareholder protection in a country weakens the positive effects of board size and board independence on CSR—consistent with the view that countries’ investor protection mechanisms substitute for these board characteristics—and that greater gender parity at the country level strengthens the positive relationship between female board representation and CSR—consistent with the view that countries’ gender parity complement females on boards’ positive impact on CSR. Moreover, our findings show that the relationships depend upon the specific CSR dimension examined (i.e., social vs. environmental dimension). Specifically, the relationships are more positive with regard to the social dimension of CSR (i.e., for board independence and for female board representation) and weaker for the environmental dimension (i.e., for board size, for female board representation, and for the presence of a CSR committee). By providing evidence on these boundary conditions, our study also contributes to theory development.

Supplemental Material

BoD_CSR_meta_appendix – Supplemental material for Board Characteristics and Corporate Social Responsibility: A Meta-Analytic Investigation

Supplemental material, BoD_CSR_meta_appendix for Board Characteristics and Corporate Social Responsibility: A Meta-Analytic Investigation by Jan Endrikat, Charl de Villiers, Thomas W. Guenther and Edeltraud M. Guenther in Business & Society

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.