Abstract

We examine the relationships among religious governance, especially Islamic governance quality (IGQ), national governance quality (NGQ), and risk management and disclosure practices (RDPs), and consequently ascertain whether NGQ has a moderating influence on the IGQ–RDPs nexus. Using one of the largest data sets relating to Islamic banks from 10 Middle East and North Africa (MENA) countries from 2006 to 2013, our findings are threefold. First, we find that RDPs are higher in banks with higher IGQ. Second, we find that RDPs are higher in banks from countries with higher NGQ. Finally, we find that NGQ has a moderating effect on the IGQ–RDPs nexus. Our findings are robust to alternative RDP measures and estimation techniques. These results imply that the quality of disclosure depends on the nature of the macro-social-level factors, such as religion that have remained largely unexplored in business and society research, and, therefore, have important implications for policy makers.

Keywords

In this article, we seek to make a number of new contributions to the extant literature by (a) examining the extent to which national and religious governance, especially Islamic governance quality influences the level of risk disclosure in Islamic banks; and (b) consequently, ascertaining whether the link between Islamic governance quality (IGQ) and bank risk management and disclosure practices (RDPs) is moderated by national governance quality (NGQ). 1

Meanwhile, RDPs are a significant part of a bank’s long-term financial sustainability and annual reporting. They often include managerial clarifications and commentaries about a bank’s up-to-date state regarding uncertainty and future predictions (Ntim, Lindop, & Thomas, 2013). In fact, regulators and stakeholders have been concerned with RDPs in recent years, especially following the 2007-2008 global banking crisis (Abedifar, Molyneux, & Tarazi, 2013; Barakat & Hussainey, 2013; Basel Committee on Banking Supervision [BCBS], 2015). This notwithstanding, the role of macro-social-level factors, such as religion and national governance in driving business decisions and outcomes, such as RDPs in distinct religious, cultural, and business contexts remains largely unexplored (Du, Jian, Zeng, & Du, 2014; Ullah, Jamali, & Harwood, 2014). Specifically, prior studies investigating the relationships among IGQ, NGQ, and RDPs are rare (Barakat & Hussainey, 2013; Ntim et al., 2013). Similarly, and to the best of our knowledge, there is no extant study examining how NGQ might probably affect the IGQ–RDPs nexus. A number of reasons have often been cited for the lack of empirical research exploring the effect of religion, in particular, in corporate decision making and outcomes, including religion being inherently divisive, sensitive, and inconsistent with the principles underlying business (Tracey, 2012). Nevertheless, another strand of research suggests that religion can be influential in business decisions and operations (Chan-Serafin, Brief, & George, 2013). In this case, previous research has, for example, linked religiosity-based management to the extent of social and environmental disclosures (Al-Bassam & Ntim, 2017; Farook, Kabir Hassan, & Lanis, 2011; Haniffa & Hudaib, 2007; Losoncz, 2011; Rahman & Bukair, 2013), risk-taking (Chircop, Fabrizi, Ipino, & Parbonetti, 2017), earnings management (Elghuweel, Ntim, Opong, & Avison, 2017), and financial reporting irregularities (McGuire, Omer, & Sharp, 2012). The current study, therefore, seeks to address this lacuna within the extant literature by examining the links among IGQ, NGQ, and RDPs. In addition, we explore why and how NGQ may have a moderating influence on the IGQ–RDPs nexus within Middle East and North Africa (MENA) Islamic banks.

RDPs have witnessed substantial developments and interests in recent years (Abdallah, Hassan, & McClelland, 2015). In this case, the prior literature suggests that Islamic banks may commit to increased RDPs for two main theoretical reasons: (a) efficiency/instrumental and (b) legitimation/moral ones. First, and from the efficiency perspective of neo-institutional theory, institutional pressures often originating from coercive, mimetic, and normative forces can compel corporations to commit to standards and regulations that can enhance internal processes, improve efficiency, and thereby gain competitive advantages. In this case, engaging in transparent RDPs may improve economic performance by reducing information asymmetry between management and shareholders (Jensen & Meckling, 1976; Ntim et al., 2013; Safieddine, 2009). Similarly, committing to increased RDPs may send positive signals to prospective investors about management’s willingness to engage in prudent risk management practices, and thereby offer access to cheaper capital (Connelly, Certo, Ireland, & Reutzel, 2011; Ntim et al., 2013). Furthermore, improved RDPs can enhance financial performance and improve economic efficiency by offering Islamic banks’ access to critical resources, such as Islamic bonds (“Sukuk”) and contracts (Al-Bassam, Ntim, Opong, & Downs, 2018; Pfeffer & Salancik, 2003).

Second, the legitimation/moral view of neo-institutional theory predicts that coercive, mimetic, and/or normative institutional forces can compel Islamic banks to conform to expected social behavior. This is because conforming to such expected social behavior can be a strategic approach toward enhancing Islamic banks’ legitimacy and justifying their right to exist (Al-Bassam et al., 2018; Ntim et al., 2013). Thus, compliance with good RDPs, in the form of increased risk disclosures, can facilitate congruence of the goals and norms of Islamic banks with those of the broader society, and thereby improve organizational legitimacy. Similarly, the need to maintain good relationships with various bank stakeholders (Aguilera, Rupp, Williams, & Ganapathi, 2007), and hence improving organizational legitimacy, can serve as a motivation for Islamic banks to engage in, or mimic, accepted social behavior (Al-Bassam et al., 2018). Hence, engagement in RDPs by Islamic banks can strategically enhance their legitimacy by helping to gain the support of powerful stakeholders, such as governments, employees, shareholders, depositors, and investors (Freeman, 1984; Freeman & Reed, 1983). Consequently, and in consideration of the apparent complex nature of the relationship among RDPs, Islamic governance, and national governance in specific settings, such as MENA (Al-Bassam & Ntim, 2017; Elghuweel et al., 2017), there have been increasing calls for research that can explore the determinants of RDPs from theoretical perspectives that have the capacity to capture both efficiency and legitimation motives underlying corporate engagement in RDPs (Judge, Douglas, & Kutan, 2008; Judge, Li, & Pinsker, 2010; Ntim et al., 2013).

Noticeably, the extant research has examined a wide range of motivations and antecedents of RDPs (e.g., Abdallah et al., 2015; Barakat & Hussainey, 2013; Dobler, Lajili, & Zéghal, 2011; Ntim et al., 2013). However, existing research seems to suffer from a number of weaknesses. Despite the significance of increased RDPs and the associated substantial accounting standards (e.g., International Financial Reporting Standards [IFRS] 7 and 9, International Accounting Standards 32 and 39), and corporate governance reforms worldwide (Alnabsha, Abdou, Ntim, & Elamer, 2017; Al-Bassam et al., 2018; Elmagrhi, Ntim, & Wang, 2016), existing RDPs research is largely focused on examining the influence of either firm-level characteristics (Dobler et al., 2011; Linsley & Shrives, 2006) or internal corporate governance mechanisms (Abraham & Cox, 2007; Ntim et al., 2013) on RDPs in nonfinancial firms in developed countries. By contrast, studies investigating why and how religion and other macro-social-level factors may influence the level of RDPs in Islamic banks are rare (Barakat & Hussainey, 2013; Ullah et al., 2014), especially in developing countries (Abdallah et al., 2015). Meanwhile, a number of studies indicate that macro-social-level institutional factors, such as national governance and religion can influence corporate decisions and outcomes (Alon & Dwyer, 2014; Ernstberger & Grüning, 2013). In the case of IGQ and NGQ, for example, it has been argued from a neo-institutional theoretical perspective that they can help in determining how bank executives treat their shareholders, as well as make decisions, including those relating to voluntary disclosures (Essen, Engelen, & Carney, 2013), and thus, can arguably ultimately affect RDPs directly. Also, and despite the growing suggestions that NGQ may be an important driver of bank strategies, behavior, and valuation (Alon & Dwyer, 2014; Ernstberger & Grüning, 2013; Essen et al., 2013; Tunyi & Ntim, 2016), the extant research relating to the impact of NGQ on disclosure quality (e.g., RDPs) has received little attention (Alon & Dwyer, 2014; Cahan, De Villiers, Jeter, Naiker, & Van Staden, 2015; Schiehll, Ahmadjian, & Filatotchev, 2014).

Furthermore, and notwithstanding the lack of evidence relating to the IGQ–RDPs nexus (Aguilera, Filatotchev, Gospel, & Jackson, 2008; Barakat & Hussainey, 2013; Essen et al., 2013; Ntim et al., 2013), to the best of our knowledge, there is no extant research that has examined whether NGQ can moderate the IGQ–RDPs relationship. Meanwhile, Islamic banks in the MENA region provide a unique context for exploring RDPs. Islamic banks operate on the basis of Islamic religious business principles, values, and laws that are drawn from Shariah (Islamic law), and, thus, arguably offer an interesting context to assess the extent to which religion (IGQ) and other macro-social-level factors, such as NGQ may drive RDPs. In particular, the distinctiveness of Islamic banking/finance forms can create unique challenges regarding disclosure and society. For example, it has been suggested that some specific Islamic banking/finance forms, such as “mudarabah” (profit-sharing), “murabaha” (cost plus), “musharakah” (joint venture), “bai-muajjal” (deferred payment sale), “ijarah” (leasing), and “istisna” (processing and manufacturing contracts) may not only be more prune to conventional agency conflicts, such as adverse selection and moral hazard problems, but also can exacerbate nontraditional agency problems by increasing opportunities for managerial expropriation of bank assets (Al-Bassam & Ntim, 2017; Elghuweel et al., 2017; Safieddine, 2009). Furthermore, MENA countries have observably pursued economic, corporate governance, accounting standards, and regulatory reforms (Amico, 2014). These reforms have in the main created an enabling economic and corporate environment within which Islamic banks can maintain successful operations. However, and arguably, the relatively poor NGQ in a majority of MENA countries may affect the trustworthiness of Islamic banks.

Hence, this study seeks to make a number of new contributions to the extant literature by examining the relationship among IGQ, NGQ, and RDPs within such a distinct environment. First, and drawing insights from a neo-institutional perspective, we offer first-time evidence on the impact of IGQ on Islamic banks’ RDPs. Recent studies suggest that Shariah boards play an important role in monitoring Islamic bank’s financial reporting quality (Al-Bassam & Ntim, 2017; Farook et al., 2011; Safieddine, 2009). We extend this nascent research by providing evidence that Islamic governance can serve as an additional governance layer with capacity to closely monitor and scrutinize managerial decisions, including those relating to disclosures. We argue that by highlighting the monitoring, performance, and value maximizing roles of Islamic governance within Islamic banks, our finding may help inform the decisions of the various stakeholders of Islamic banks, such as employees, depositors, investors, government, and regulators. Second, and to the best of our knowledge, our study offers first-time evidence on the effect of NGQ on RDPs. This result may potentially help investors and regulators to better understand and/or evaluate the channels (e.g., the institutional and regulatory setting) through which macro-social-level factors, such as religion and national governance affect disclosure quality, transparency, and accountability within Islamic banks. Finally, previous research indicates that the relation between governance quality and disclosure varies according to the type of business, disclosure, and contexts (Abedifar et al., 2013; Barakat & Hussainey, 2013; Essen et al., 2013; Ntim et al., 2013). We extend this literature by providing first-time evidence that shows that NGQ has a moderating effect on the relationship between IGQ and RDPs.

The rest of this study is organized as follows. The next section outlines the theoretical framework. The following sections review the extant empirical literature and develop research hypotheses, outline the research design, and discuss the empirical results, whereas the final section presents concluding remarks, and discusses implications and recommendations for future research.

Theoretical Framework

The variations in RDPs could be explained through a generalized neo-institutional lens because a generally accepted theory that links RDPs and governance is still elusive (Christopher, 2010; Ntim et al., 2013; Zattoni & Van Ees, 2012). Thus, we employ a generalized neo-institutional perspective as a direct response to the latest calls for innovative alternative theoretical approaches to the ubiquitous agency theory for studying the link between IGQ and RDPs (Abraham & Shrives, 2014; Christopher, 2010; Dobler et al., 2011). One reason is that no single theoretical framework may be able to offer a complete understanding of how Islamic and national governance mechanisms may affect RDPs on their own. By contrast, insights from a generalized neo-institutional perspective may offer unique insights toward interpreting and explaining RDPs within distinctive regulatory and institutional contexts, such as MENA. Also, a neo-institutional perspective may facilitate the examination of the potential interactions among IGQ, NGQ, and RDPs (Ntim et al., 2013; Zattoni & Van Ees, 2012; Haque & Ntim, 2018).

Briefly, a generalized neo-institutional theory incorporates both efficiency/instrumental perspective, and legitimation/moral view of Islamic banks operating in an institutional environment rather than examining the incidence of particular institutional isomorphisms directly (e.g., coercive, mimetic, and/or normative institutional pressures). In this case, and on one hand, efficiency/instrumental perspective of the generalized neo-institutional theory suggests that effective mechanisms relating to bank- and national-level governance quality may lead to more transparent risk disclosures. Consequently, increased risk disclosure can mitigate agency conflicts and reduce the information asymmetry between management and shareholders (Abraham & Cox, 2007; Jensen & Meckling, 1976; Safieddine, 2009). Efficiency/instrumental motive further suggests that economic actors principally tend to maximize their self-interests by competing for critical resources.

On the other hand, sociology theorists consider institutions to be beyond not only delivering economic efficiency but also as social institutions with some symbolic value (Meyer & Rowan, 1977). Hence, the sociological neo-institutionalism theorists suggest that individuals and firms not only compete for critical resources but also endeavor to gain social acceptance (“organisational legitimacy”; Zattoni & Cuomo, 2008). In this respect, legitimation is driven by the different values and ethics of economic actors, which may direct an Islamic bank, for example, to adopt some practices with no instant or clear economic benefits (e.g., interest-free loans or “Qard Hassan”).

Specifically, Scott (2001) theorized that neo-institutional framework contains three levels of analysis: social (country) institutions, governance arrangements, and firms as economic actors. Social (country) level institutions provide a formal and informal platforms that provide legitimate models and standards of acceptable social behavior (Judge et al., 2008; Judge et al., 2010). In this case, social (country) level institutions may interact to shape, facilitate, and/or limit the diffusion and/or imposition of structures and actions at lower levels. Thus, it suggests that Islamic banks are more likely to seek to conform to societal norms and expectations, and as such, may engage in increased risk disclosures, as a way of conforming to such expectations (Ntim et al., 2013; Ntim & Soobaroyen, 2013). These pressures tend to arise from Islamic banks’ external and internal forces, and may lead to institutionalization and organizations’ isomorphic behavior (DiMaggio & Powell, 1983; Ntim et al., 2013). Hence, a key principal assumption within a generalized neo-institutional theory’s perspective is that the firms are not only seeking “legitimacy” and social acceptance but also competing for critical resources (“efficiency”).

A generalized neo-institutional theory has rarely been employed at the organizational level of analysis relating to Islamic governance–RDPs nexus, and this is principally relevant with respect to the rapid global growth of Islamic banking over the past decades. Debatably, there is opportunity to extend our understanding of the institutional antecedents and justifications of RDPs beyond Islamic banks. Hence, complying with Basel Accords and IFRS through increased RDPs can enhance the legitimacy of bank generally. Similarly, voluntarily engaging in RDPs can help Islamic banks to gain organizational legitimacy by fairly balancing the diverse, and often conflicting, demands of their different influential stakeholders, such as investors, shareholders, governments, and depositors (Freeman, 1984; Freeman & Reed, 1983). Furthermore, increased commitment to RDPs can send a credible signal to current and prospective investors of the quality of a bank’s governance structures, and, by extension, its positive current and future prospects (Connelly et al., 2011; Ntim et al., 2013). This can enhance economic efficiency by granting access to critical resources, such as cheaper capital.

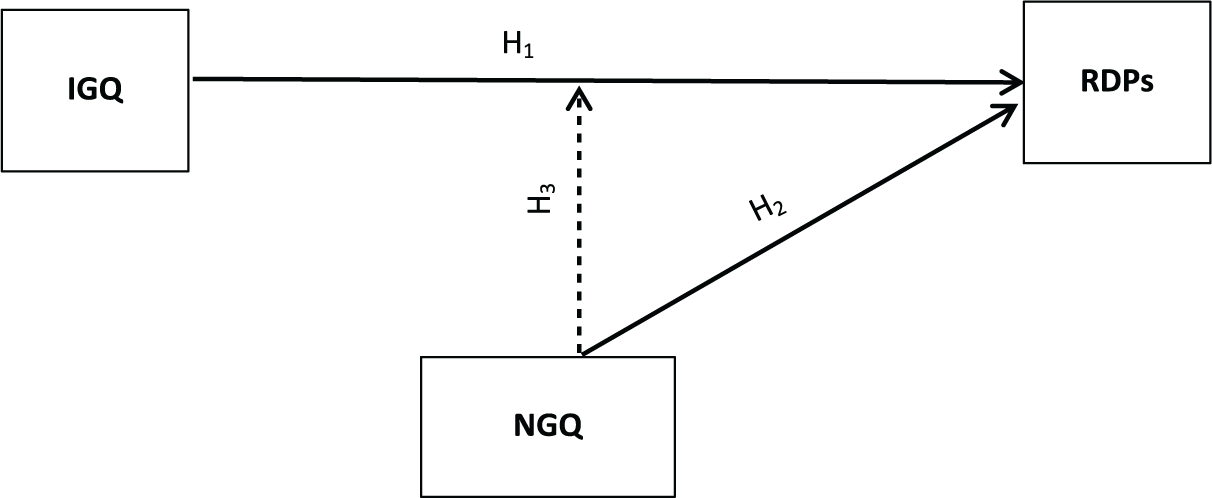

This study, therefore, seeks to enhance these neo-institutional motives by drawing insights from all of them together (i.e., efficiency and legitimacy perspectives) in examining and understanding the associations among Islamic governance, national governance, and bank risk disclosures. To add further theoretical nuance to our neo-institutional lens, we cogitate how NGQ and further effects, such as ethical and religious values of the MENA region (i.e., IGQ) may influence RDPs, as presented in Figure 1.

Proposed empirical model.

Related Literature and Research Hypotheses Development

Most prior literature on RDPs focuses on firm-specific factors (e.g., Dobler et al., 2011; Ntim, Soobaroyen, & Broad, 2017). However, the focus has recently shifted from firm-specific factors to firm’s internal corporate governance mechanisms following unprecedented malfeasance and bank failures (Ntim et al., 2013). Conversely, there is no consistent evidence on the relationship between corporate governance mechanisms and disclosure quality in banks (Abraham & Cox, 2007; Ntim et al., 2013). Moreover, the role of religion and other macro-social-level factors in influencing RDPs has not been explored. Specifically, most prior RDPs studies rely on single governance-level analytical approach, while often being inattentive to the potential influence of religion and national governance-level factors (Barakat & Hussainey, 2013). Consequently, this study seeks to examine the impact of IGQ on the level of RDPs. In addition, this study investigates the effect of NGQ on the level of RDPs. Finally, it explores why and how NGQ may have a moderating influence on the IGQ–RDPs nexus in MENA Islamic banks.

Islamic Governance Quality and Risk Management and Disclosure Practices

It can be argued that Islamic banks’ activities are likely to be consistent with the shareholders, stakeholders, and society’ expectations because of their explicit incorporation of Islamic values and laws (Shariah) into their operations (Abu-Tapanjeh, 2009; Elghuweel et al., 2017). These include the prohibition of interest charges (“riba” or “usury”) and Shariah supervisory boards in Islamic banks that are responsible for assessing whether Islamic banks’ transactions meet the requirements of Islamic law and values. 2 Thus, it can be conjectured that Islamic governance may play an important role in Islamic banks’ decision making, including those relating to RDPs. For example, prudential supervision and principles regarding Islamic governance may place a better emphasis on committing to more transparent disclosure practices for a number of theoretical considerations (Al-Bassam & Ntim, 2017; Farook et al., 2011). From an efficiency/instrumental perspective (Aguilera et al., 2007; Chen & Roberts, 2010), neo-institutional theory suggests that Islamic governance is likely to convey additional monitoring requirements to Islamic banks due to further rules, experience, and knowledge needed to be Shariah compliant (Al-Bassam & Ntim, 2017; Elghuweel et al., 2017). In particular, Islamic governance rooted in Islamic religious values and principles may offer opportunities to engage in greater RDPs through certifying whether Islamic banks have complied with Shariah and related risks, and thus, mitigating the level of information asymmetry between managers and Islamic banks’ stakeholders (Al-Bassam & Ntim, 2017; Farook et al., 2011; Jensen & Meckling, 1976; Safieddine, 2009). The legitimation/moral view of neo-institutional theory predicts that Islamic governance may offer incentives to engage in greater RDPs to enhance their legitimacy within the broader society (Al-Bassam et al., 2018; Haniffa & Hudaib, 2007; Ntim et al., 2013; Pittroff, 2014). Furthermore, Islamic governance may offer incentives to engage in greater RDPs, especially practices linked to complying with Shariah and related risks due to coercive and societal pressures, arising from MENA Islamic banks’ external settings, as well as institutional pressures within the banks (Chandler & Hwang, 2015; DiMaggio & Powell, 1983; Ntim & Soobaroyen, 2013).

A number of current qualitative studies have explored the nature of Islamic governance and ethics in Islamic banks (Ullah et al., 2014). For example, Haniffa and Hudaib (2007) examined the ethical identity of Islamic banks using annual reports data from seven Islamic banks in four Gulf countries from 2002 to 2004. They found that Islamic banks disclose further information relating to Shariah supervisory boards as a way of creating ethically and socially responsible identity for Islamic banks. Ullah and colleagues (2014) have also reported similar findings for Shariah departments relating to socially responsible investments. Furthermore, Safieddine (2009) explored corporate governance practices using a survey of 43 questions from 40 Islamic banks in five Gulf countries. The results of Safieddine indicate that Islamic banks have well-established Shariah supervisory boards, which operate as good proxies for Islamic governance based on an evaluation of their independence, structure, education, and power.

Prior quantitative studies have also found a strong evidence supporting the view that the quality of Islamic governance has a positive impact on social responsibility disclosures within Islamic banks (Farook et al., 2011; Haniffa & Hudaib, 2007; Rahman & Bukair, 2013). For instance, using data from 47 Islamic banks in 14 countries, Farook and colleagues (2011) found that Islamic governance quality, including the presence of a Shariah supervisory board has a positive impact on the level of social responsibility disclosures. Similarly, prior literature has examined the relationship between Islamic governance quality and disclosure quality. For instance, using data from 75 firms listed on the Saudi market from 2004 to 2010, Al-Bassam and Ntim (2017) found that Shariah supervisory board characteristics have a positive effect on the level of voluntary corporate governance disclosure. Similarly, and using a sample of 116 Omani firms from 2001 to 2011, Elghuweel and colleagues (2017) reported that IGQ has a negative effect on earnings management. Notably, to the best of our knowledge, no prior study has examined the impact of IGQ on RDPs to date, thus providing genuine opportunity to make a new contribution to the literature by examining this association. Accordingly, we hypothesize the following:

National Governance Quality and RDPs

Effective national governance may place further emphasis on RDPs (Barakat & Hussainey, 2013; Essen et al., 2013; Kaufmann, Kraay, & Mastruzzi, 2011). Efficiency/instrumental perspective of neo-institutional theory suggests that banks in countries with improved national governance quality may provide additional monitoring level that can mitigate information asymmetries, and hence serve as a motivation to engage in greater RDPs (Aguilera et al., 2008; Barakat & Hussainey, 2013; Beltratti & Stulz, 2012). Similarly, the legitimation/moral view of neo-institutional theory suggests that NGQ may offer Islamic banks incentives to engage in greater RDPs to gain the legitimacy to exist and carry out their operations from the broader society (Barakat & Hussainey, 2013; Haniffa & Hudaib, 2007; Ntim et al., 2013; Pittroff, 2014). Also, NGQ may offer incentives to engage in greater RDPs due to coercive and societal pressures arising from banks’ external settings, such as government, professional, and regulatory bodies (Aguilera et al., 2008; Barakat & Hussainey, 2013; Chandler & Hwang, 2015; DiMaggio & Powell, 1983; Ntim & Soobaroyen, 2013). Finally, effective national governance may offer motivations and pressures to engage in greater RDPs to offer Islamic banks’ access to required resources, such as Sukuk (Alon & Dwyer, 2014; Barakat & Hussainey, 2013; Ntim et al., 2013; Pfeffer & Salancik, 2003).

National governance structures are designed and employed to address agency problems (Aguilera, 2005; La Porta, Lopez-de-Silanes, Shleifer, & Vishny, 2000). They consist of formal constraints (e.g., regulations and laws, economic and political regulations and procedures, and other clear restrictions on bank behavior), and informal rules containing unwritten, but relatively important, social norms, conventions, codes of ethics, and values (Kaufmann et al., 2011; Schiehll et al., 2014; Yoshikawa, Zhu, & Wang, 2014). Thus, national governance structures can serve as motivation for economic actors to comply with laws and regulations. Prior research suggests that national governance structures can protect stockholders from being expropriated by the company’s managers, and safeguards minority shareholder rights (Aslan & Kumar, 2014; La Porta et al., 2000; Schiehll et al., 2014; Yoshikawa et al., 2014). Hence, rigorous national governance structures tend to demand mandatory information disclosure and regulate market intermediaries, thereby alleviating information asymmetries. Also, they place the board of directors and managers under larger pressure to implement their regulatory responsibility (Yoshikawa et al., 2014). Collectively, rigorous national governance structures can serve as a valuable external governance instrument to protect shareholders and influence accountability and disclosure quality. Thus, banks’ incentive to offer higher RDPs tends to be higher in countries with strong national governance structures.

The findings of previous empirical studies largely suggest that NGQ may be an important driver of bank strategies, behavior, and valuation (Alon & Dwyer, 2014; Ernstberger & Grüning, 2013; Essen et al., 2013; Tunyi & Ntim, 2016). However, empirical evidence regarding the impact of NGQ on disclosure quality, including RDPs is almost nonexistent. For instance, using 85 banks from 20 European countries, Barakat and Hussainey (2013) found that countries with stronger NGQ (i.e., the rule of law [ROL]) are associated with an increase in the level of operational risk disclosures. However, using data from 71 nations, Alon and Dwyer (2014) found that countries with poor NGQ are more likely to adopt IFRS early in comparison with their counterparts with strong NGQ, with the aim of allowing them to gain access to critical resources, such as foreign direct investments. To the best of our knowledge, no prior study has examined the impact of NGQ on RDPs to date, and, therefore, this study offers genuine opportunities to contribute to the extant literature by examining the effect of NGQ on RDPs. Accordingly, we hypothesize the following:

IGQ and RDPs: The Moderating Effect of NGQ

Inconsistent results about the sign and significance of the governance quality–RDPs nexus has triggered a number of studies to explore them further (Abraham & Shrives, 2014; Aguilera et al., 2008; Barakat & Hussainey, 2013; Essen et al., 2013; Ntim et al., 2013; Zattoni & Van Ees, 2012). On one hand, a number of studies indicate that different methodological approaches can lead to inconsistent results (Al-Bassam et al., 2018; Barakat & Hussainey, 2013; Ntim et al., 2013). For instance, endogeneity problems (Barakat & Hussainey, 2013; Ntim et al., 2013), time frame differences (Abraham & Cox, 2007; Ntim et al., 2013), and different risk disclosure measures (Ntim et al., 2013) can affect the research findings. On the other hand, others suggest that the mixed results relating to the governance–RDPs nexus can be addressed by concentrating on how probable theory-driven variables moderate such a relationship (Aguilera, 2005; Aguilera et al., 2008; Alon & Dwyer, 2014; Cahan et al., 2015; Ernstberger & Grüning, 2013; Essen et al., 2013).

La Porta and colleagues (1997, 2000) suggested that NGQ (e.g., legal rules and enforcement quality) might enhance investor protection, as well as the efficiency of governance structures (e.g., corporate governance mechanisms, external finance type, and, more important, disclosure quality). Hence, La Porta and colleagues (1997, 2000) suggested that NGQ may have a moderating role on the existing agency problems. Thus, Islamic banks might be motivated by coercive, mimetic, and normative national pressures, particularly for those operating in strongly governed countries to engage in increased RDPs with the purpose of signaling their good performance and bright future prospects to their current and future stakeholders, such as employees, investors, and depositors.

Empirically, Ernstberger and Grüning (2013) reported that NGQ has a complementary or substitutive influence on the governance–disclosure nexus using a sample of 1,044 European companies. Specifically, Ernstberger and Grüning’s (2013) results suggest that NGQ can serve as an alternative to firm-level governance quality in terms of its impact on corporate disclosure quality. Hence, we assume that the IGQ–RDPs relationship may be highly sensitive to the institutional environment, as characterized by the extent of NGQ. Accordingly, we hypothesize the following:

All the earlier hypothesized relations are shown in Figure 1.

Research Design

Sample Selection and Data Sources

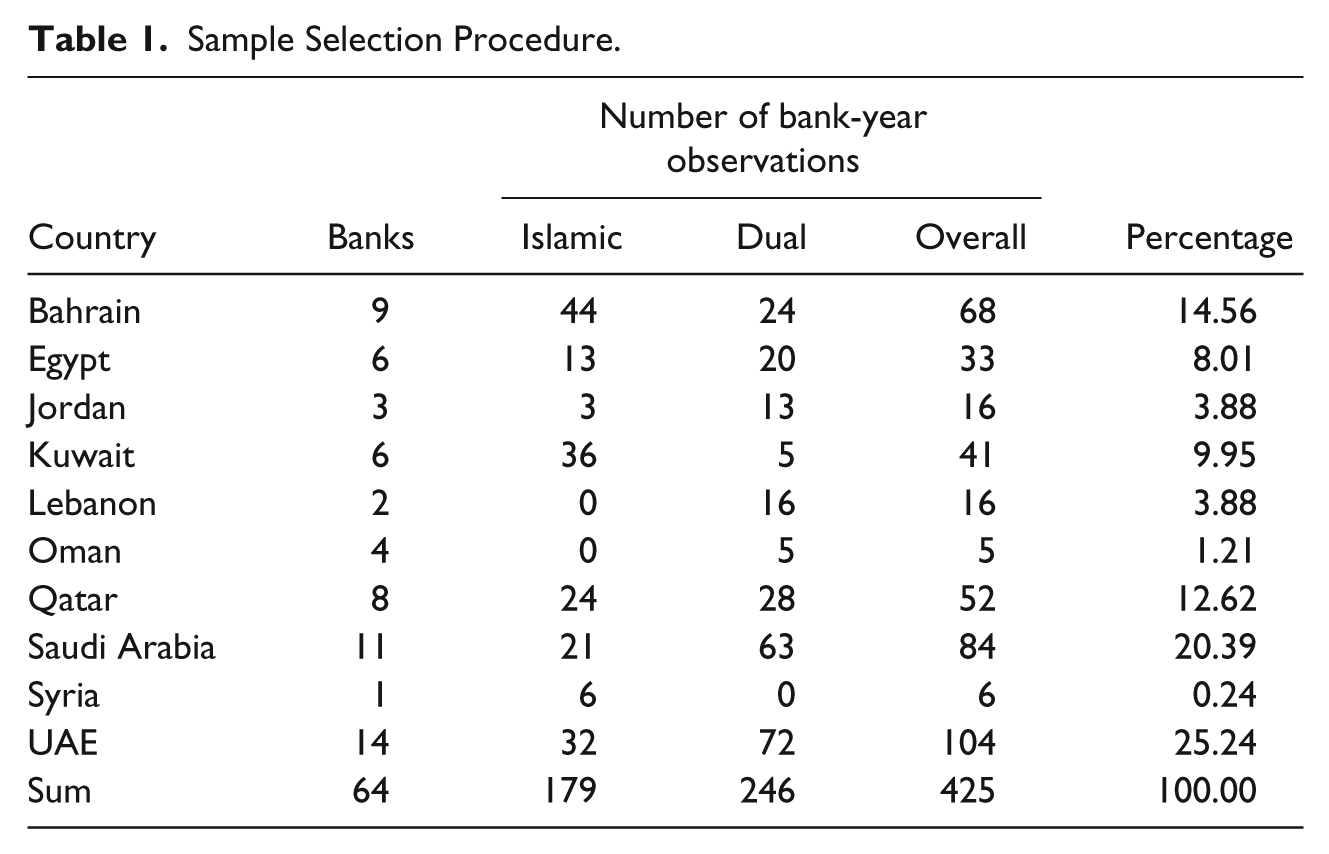

Our sample is based on all listed Islamic and dual banks (ISBs) located in 10 countries in the Arab MENA region, namely, Bahrain, Egypt, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, and UAE. We generate our sample based on the Bankscope database as shown in Table 1, from 2006 to 2013, covering pre-, during, and post-2007-2008 banking crisis period. In addition, the sample begins in 2006 because Basel II came into effect from mid-2005, as well as the fact that data before 2006 relating to the vast majority of our sample being unavailable. This results in a final sample of 64 banks over 8 years from 2006 to 2013. This generated a total of 425 bank-year observations for our empirical analyses.

Sample Selection Procedure.

We collected the data from three different sources. First, we collected RDPs and governance variables from annual reports, which we obtained mainly from the Perfect Information database and the sampled Islamic banks’ websites, where available. Second, financial data were obtained from the Bankscope database and the Islmaic banks’ annual reports. Finally, national macroeconomic statistics and national governance quality (NGQ) data were obtained from the World Bank’s databases.

Definition of Variables

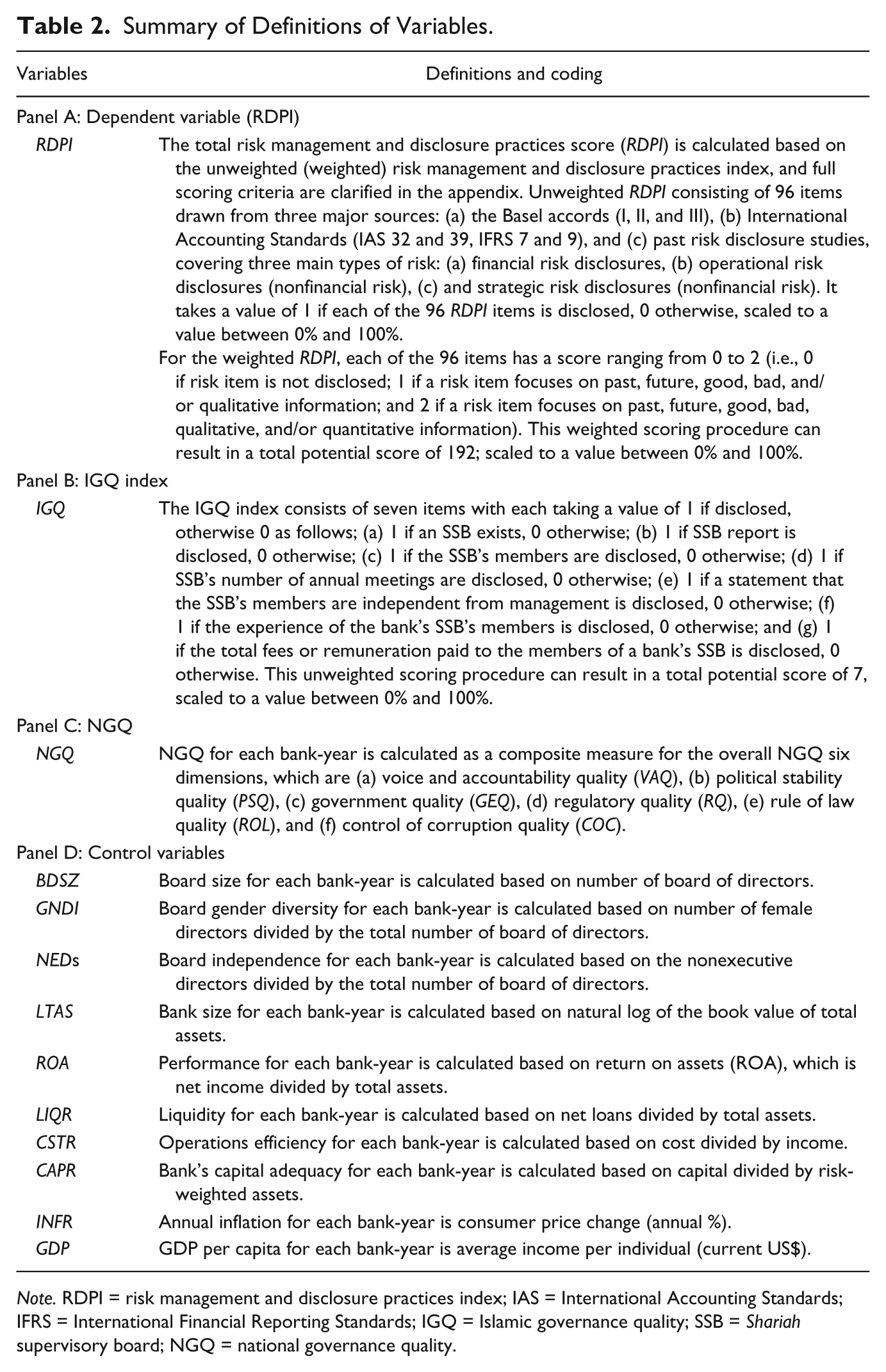

The study’s variables are categorized into four main types and Table 2 presents the full definitions of all the variables used in this study.

Summary of Definitions of Variables.

Note. RDPI = risk management and disclosure practices index; IAS = International Accounting Standards; IFRS = International Financial Reporting Standards; IGQ = Islamic governance quality; SSB = Shariah supervisory board; NGQ = national governance quality.

First, and to test Hypothesis 1 to Hypothesis 3, we employ RDPs scores, as the dependent variable, which seek to measure the level of RDPs.

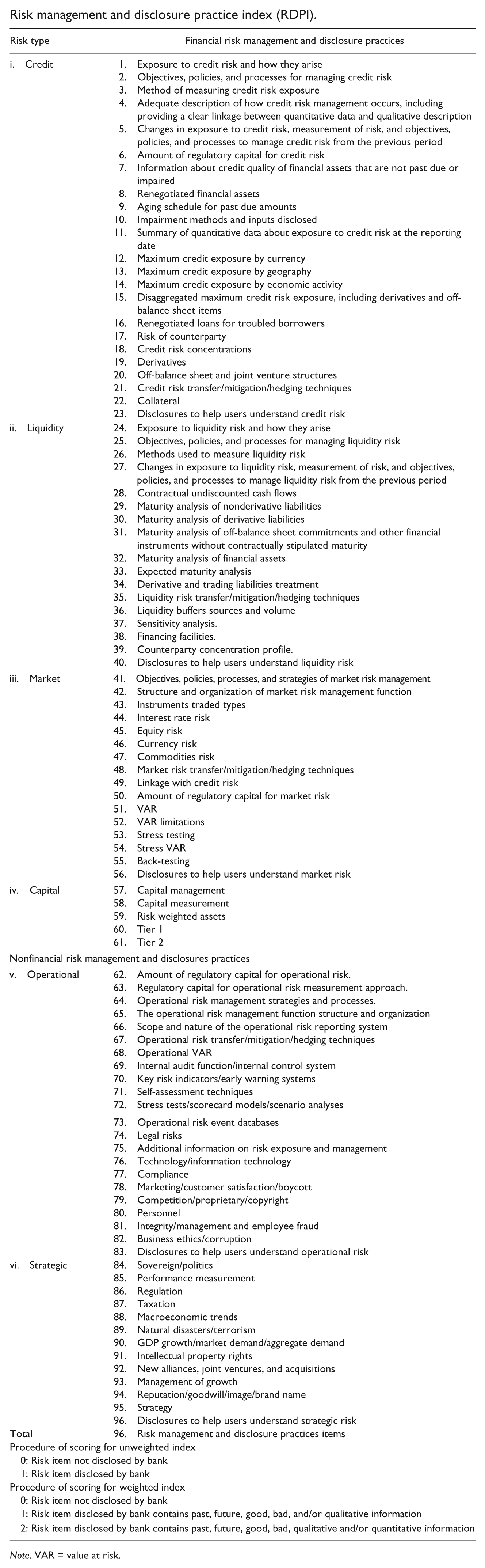

We measured RDPs variable using risk management and disclosure practices index (RDPI) based on six broad subsections and total of 96 individual items drawn from several sources. Particularly, the individual items were drawn from the (a) Basel accords (I, II, and III), (b) International Accounting Standards (IAS 32 and 39, IFRS 7 and 9), and (c) other risk disclosure items that have been employed previously in closely related studies (Barakat & Hussainey, 2013; Ntim et al., 2013). Hence, the RDPI contains 96 items classified as follows: (a) bank financial RDPs, consisting of (i) credit, (ii) liquidity, (iii) market, and (iv) capital RDPs; and (b) bank nonfinancial RDPs, consisting of (i) operational and (ii) strategic RDPs. The appendix displays the definitions and scoring procedure of all 96 items included in the RDPI.

We use RDPI measurement approach instead of other quantitative measures (e.g., word, sentence, paragraph, and page counts) because indices measurement approach employed has the ability to measure RDPs more precisely (Barakat & Hussainey, 2013; Ntim, 2016). More specifically, RDPI measurement approach has the capacity to capture the comparative weights of different risk categories. In addition, alternative quantitative measures, such as word, sentence, paragraph, and page counts, have been repeatedly criticized for the increased probability of capturing non-RDPs (Beattie, McInnes, & Fearnley, 2004; Ntim, 2016); and, there is no broad agreement with respect to a set of predefined words or sentences that can fully reflect RDPs in annual reports. As a result of these limitations, we employ the index approach in coding our RDPs. However, the index measurement approach is also often criticized for being inherently subjective (Marston & Shrives, 1991). Therefore, to reduce subjectivity, we followed the following steps.

First, two independent coders coded a sample of 10 annual reports independently and their results were compared. Evidently, no main variances occurred, with high agreement coefficient (.83), which is higher than the acceptable level in the social science (reliability threshold ranges from .70 to .80; Beattie et al., 2004; Krippendorff, 2004; Marston & Shrives, 1991). Second, and subsequently, a single coder (the main coder) completed the coding of the rest of the RDPI. Third, the main coder recoded a sample of five annual reports randomly, and the results were compared with his previous original coding results. Apparently, no significant variances occurred, with high agreement coefficient (.95). Finally, we use Cronbach’s alpha to assess the internal consistency of the RDPI. The Cronbach’s alpha was sufficiently high at 83.50%, noting that the cutoff level for Cronbach’s alpha is 70% (Elghuweel et al., 2017).

Second, and to test the first hypothesis, our independent variable is the Islamic governance quality index (IGQ). It covers seven IGQ best practices, including broad areas of Islamic governance and business principles. The detailed items are contained in Table 2. The IGQ seeks to measure the extent to which Islamic banks voluntarily and clearly incorporate Islamic governance and business principles into their operations, and subsequently, disclosed in their annual reports. We selected these provisions based on three criteria. First, we conducted extensive exploration of the previous research that explores governance from an Islamic viewpoint and sourced Islamic governance quality variables used in those studies (Abu-Tapanjeh, 2009; Al-Bassam & Ntim, 2017; Elghuweel et al., 2017; Farook et al., 2011; Rahman & Bukair, 2013; Safieddine, 2009). Second, we sourced relevant Islamic governance provisions contained in the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) standard on independence of Shariah supervisory board. Finally, we supplemented these with Islamic governance variables that were identified in a preliminary exploration of a sample of the sampled banks’ annual reports.

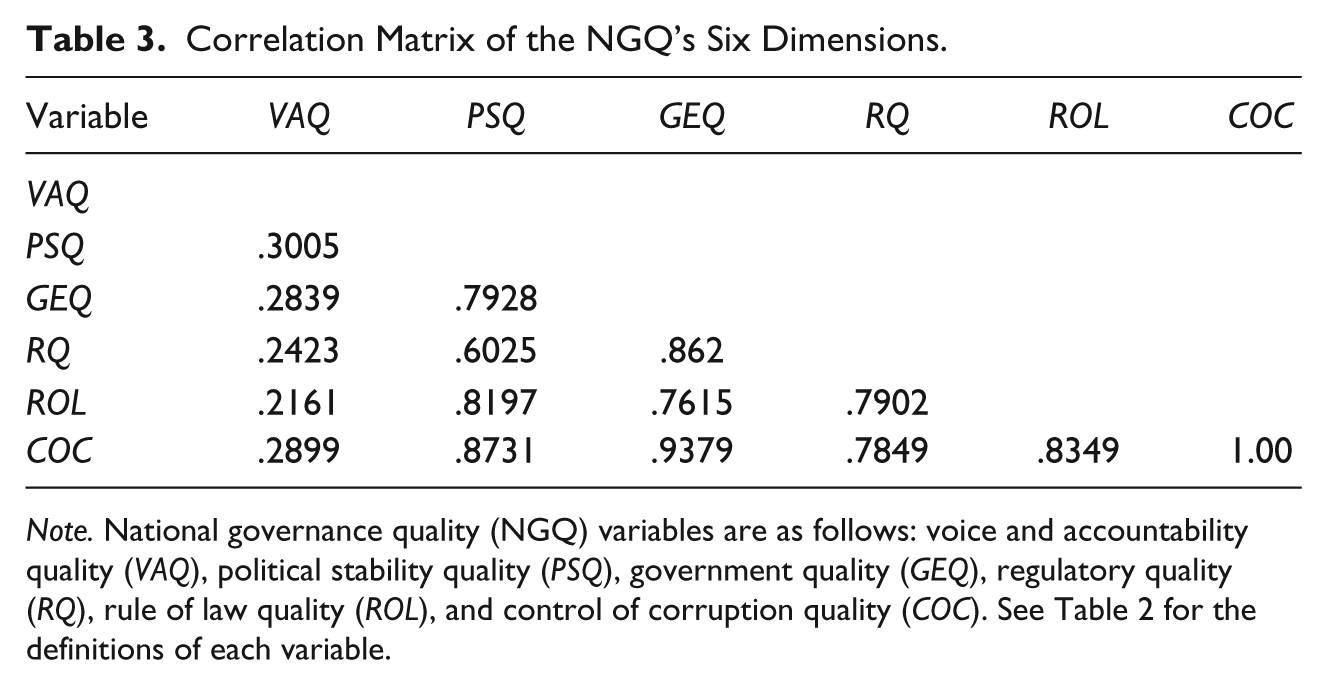

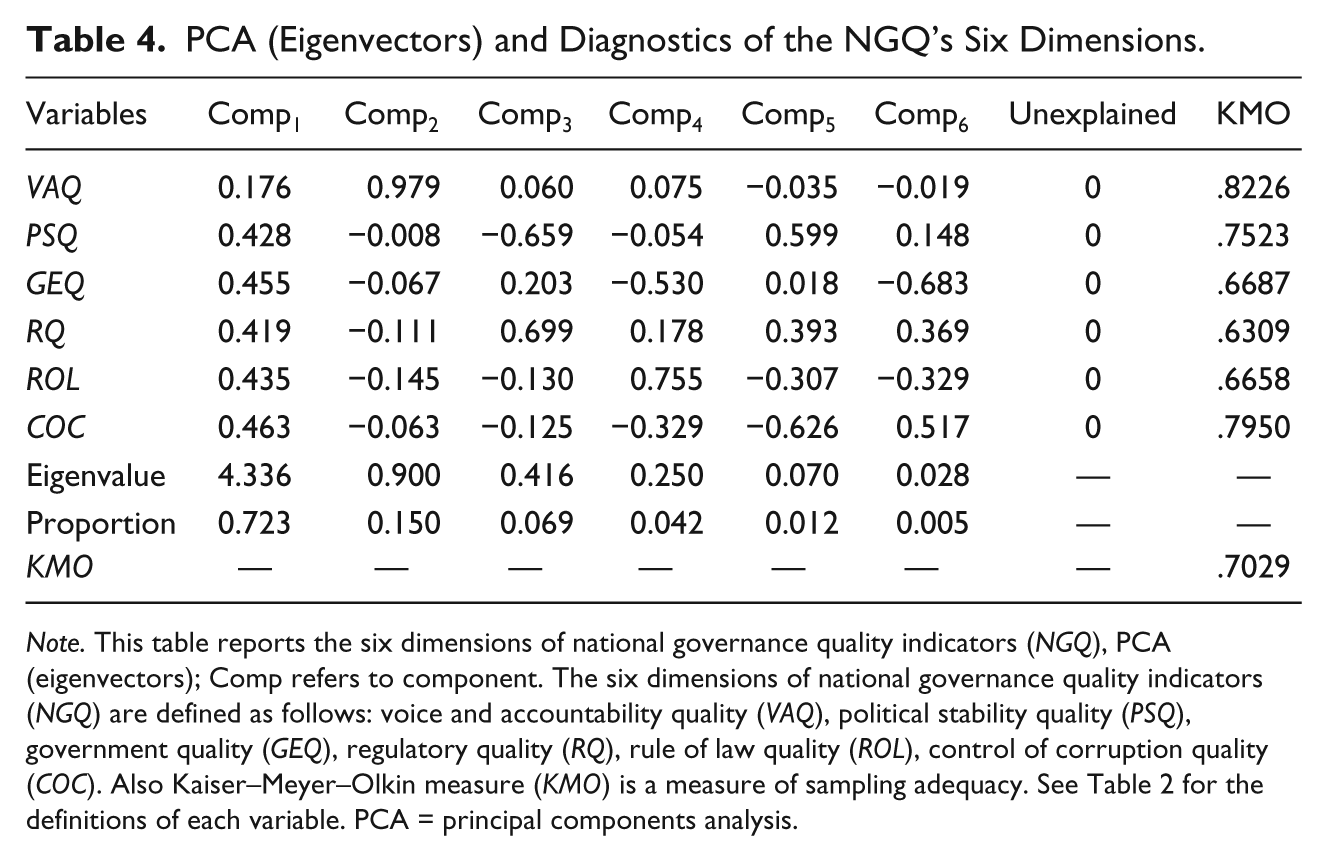

Third, because several studies suggest that NGQ can affect the quality of disclosure (Barakat & Hussainey, 2013; Essen et al., 2013; Kaufmann et al., 2011; Zattoni & Van Ees, 2012), we collected data on NGQ. This study employed the Worldwide Governance Indicators developed by the World Bank to measure national governance quality (NGQ). Kaufmann and colleagues (2011) identified six dimensions of NGQ: (a) voice and accountability quality (VAQ), (b) political stability quality (PSQ), (c) government effectiveness quality (GEQ), (d) regulatory quality (RQ), (e) ROL, and (f) control of corruption (COC). Correlation matrix in Table 3 shows that there are high intercorrelations among the six NGQ dimensions, which are consistent with the findings of prior studies (Alon & Dwyer, 2014). Therefore, and following prior research (Dikova & Van Witteloostuijn, 2007; Tunyi & Ntim, 2016), we conducted a principal components analysis (PCA) to create a composite measure for the overall NGQ dimensions. Table 4 shows the PCA (eigenvectors) and diagnostics of NGQ dimensions. The overall Kaiser–Meyer–Olkin (KMO), which we use as a measure of sampling adequacy is .7029, which is higher than the recommended minimum PCA value of .50 (Tunyi & Ntim, 2016).

Correlation Matrix of the NGQ’s Six Dimensions.

Note. National governance quality (NGQ) variables are as follows: voice and accountability quality (VAQ), political stability quality (PSQ), government quality (GEQ), regulatory quality (RQ), rule of law quality (ROL), and control of corruption quality (COC). See Table 2 for the definitions of each variable.

PCA (Eigenvectors) and Diagnostics of the NGQ’s Six Dimensions.

Note. This table reports the six dimensions of national governance quality indicators (NGQ), PCA (eigenvectors); Comp refers to component. The six dimensions of national governance quality indicators (NGQ) are defined as follows: voice and accountability quality (VAQ), political stability quality (PSQ), government quality (GEQ), regulatory quality (RQ), rule of law quality (ROL), control of corruption quality (COC). Also Kaiser–Meyer–Olkin measure (KMO) is a measure of sampling adequacy. See Table 2 for the definitions of each variable. PCA = principal components analysis.

Finally, we included a wide range of bank-level governance mechanisms, bank-level characteristics, and country-level factors, as control variables. These include (a) bank-level governance mechanisms, such as board size (BDSZ), board gender diversity (GNDI), and nonexecutive directors (NEDs); (b) bank-level characteristics, such as bank size (LTAS), performance (ROA), liquidity (LIQR), operations efficiency (CSTR), and capital adequacy ratio (CAPR); and (c) country-level variables, such as annual inflation (INFR), and annual GDP per capita (GDPC). We do not develop direct theoretical links between these variables and RDPI for brevity, but the findings of a number of prior studies suggest that they can influence the level of the RDPI (Abdallah et al., 2015; Barakat & Hussainey, 2013; Farook et al., 2011; Ntim et al., 2013).

Model Specification

We use fixed-effects regression analysis (Ntim et al., 2013) to investigate the moderating effect of NGQ on the relationship between IGQ and RDPs in MENA Islamic banks. Therefore, our main regression model to be considered is identified as follows:

where RDPI is a proxy of risk management and disclosure practices level for bank i during year t. IGQ refers to Islamic governance quality (IGQ). NGQ refers to national governance quality. CONTROLS refers to (a) bank-level governance mechanism, including board size (BDSZ), gender diversity (GNDI), and nonexecutive directors (NEDs); (b) bank-level characteristics, namely, bank size (LTAS), performance (ROA), liquidity (LIQR), operations efficiency (CSTR), and capital adequacy (CAPR); and (c) country-level control variables including, annual inflation (INFR), and annual GDP per capita (GDPC). δ is the bank-year–specific fixed effects, and ε is the white noise error term.

We present the empirical analyses, including the descriptive statistics, bivariate correlations, and multivariate regression analyses in the following sections.

Empirical Results and Discussion

Descriptive Statistics and Bivariate Analyses

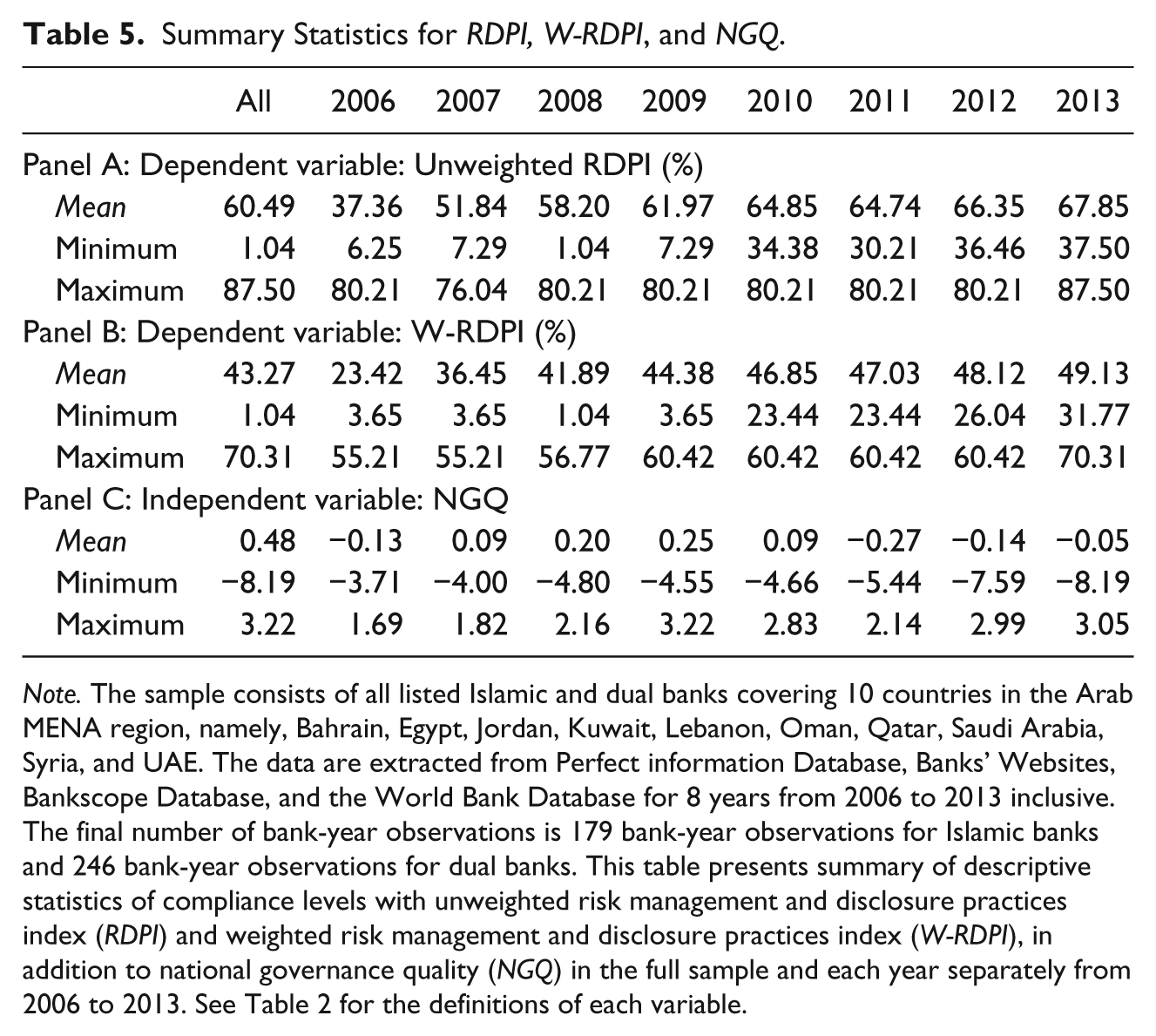

Table 5 presents descriptive statistics for the main indices (i.e., the unweighted risk management and disclosure practices index—RDPI), the weighted risk management and disclosure practices index (W-RDPI), and national governance quality (NGQ) for the full data set, as well as for each of the eight bank-years examined, respectively. On average, the distribution of the RDPI differs considerably, ranging from 1.04% (one out of 96 items disclosed) to 87.50% (84 out of 96) with a mean of 60.49%. Also, Table 5 reports that the RDPI improved over time. For instance, the mean of the RDPI improved steadily from 37.36% in 2006 to 67.85% in 2013. The steady improvement in the RDPI suggests that the implementation of the Basel Accords (Basel I, II, and III), International Accounting Standards (IAS 32, 9; IFRS 7 and 9) and national corporate governance (CG) codes (e.g., Egypt, Oman, and Saudi CG codes) appear to have helped in improving the level of RDPs among MENA banks. This seems to reflect the importance that has been attached to RDPs and good national governance, particularly during and after, the 2007-2008 credit crunch (Barakat & Hussainey, 2013; Essen et al., 2013; Ntim et al., 2013). Similarly, the distribution of the W-RDPI depicts a similar pattern to the distribution of the RDPI. By contrast, the distribution of the NGQ fluctuates substantially, ranging from −8.19 to 3.22 with the mean of 0.48. Also, Table 5 reports that NGQ has been fluctuating over time. Continuous fluctuations in NGQ reflect the nature of MENA context. In particular, MENA countries have experienced considerable political instability, especially in the form of the “Arab Spring,” as well as the impact of the 2007-2008 credit crunch in the MENA region (Beltratti & Stulz, 2012; Hasan & Dridi, 2010).

Summary Statistics for RDPI, W-RDPI, and NGQ.

Note. The sample consists of all listed Islamic and dual banks covering 10 countries in the Arab MENA region, namely, Bahrain, Egypt, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, and UAE. The data are extracted from Perfect information Database, Banks’ Websites, Bankscope Database, and the World Bank Database for 8 years from 2006 to 2013 inclusive. The final number of bank-year observations is 179 bank-year observations for Islamic banks and 246 bank-year observations for dual banks. This table presents summary of descriptive statistics of compliance levels with unweighted risk management and disclosure practices index (RDPI) and weighted risk management and disclosure practices index (W-RDPI), in addition to national governance quality (NGQ) in the full sample and each year separately from 2006 to 2013. See Table 2 for the definitions of each variable.

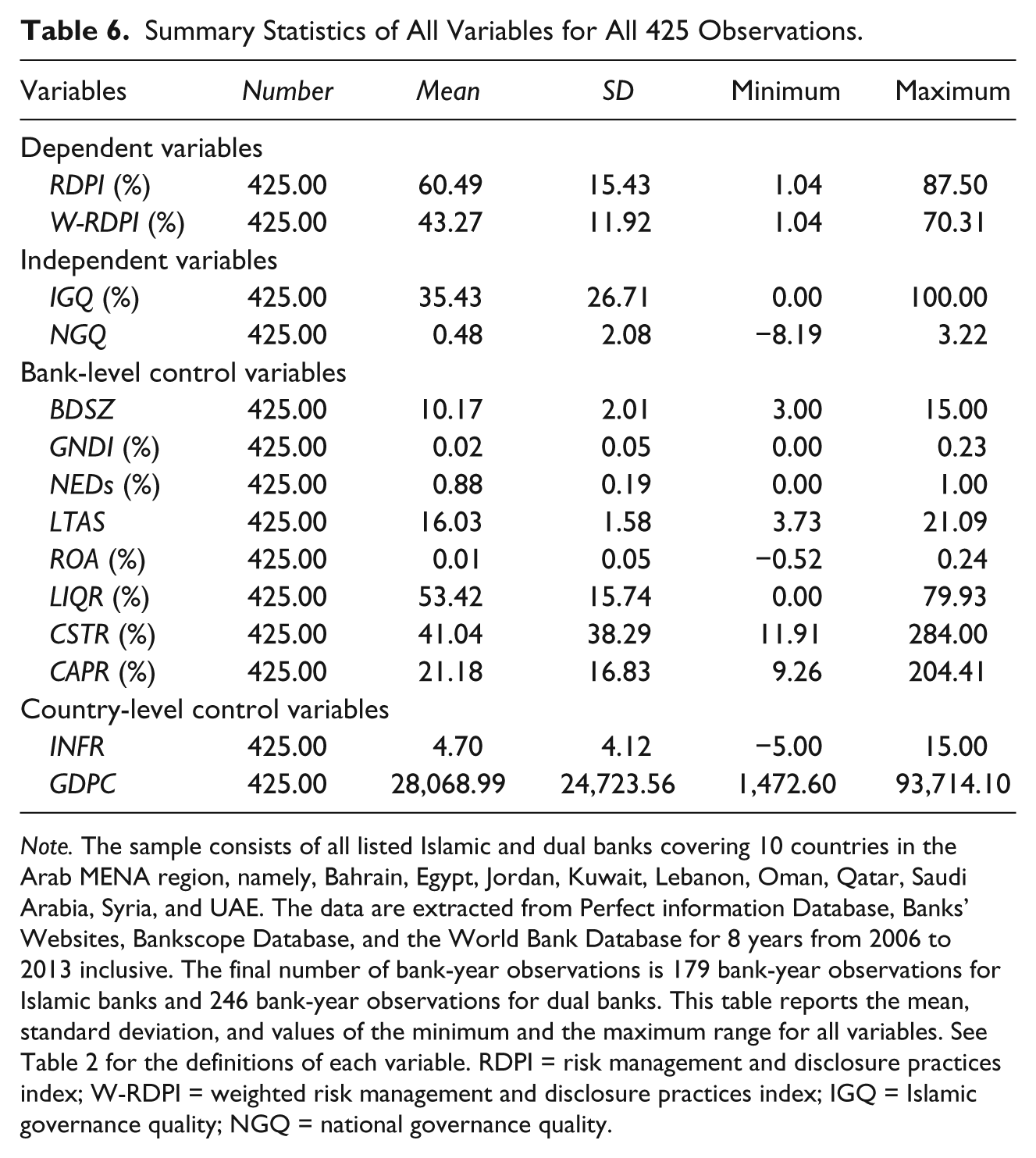

Table 6 shows summary statistics for all variables. Similar to the RDPI, all the independent and control variables distributions generally show widespread variations. For instance, Islamic governance (ISQ) ranges from 0.00% to 100.00% with a mean of 35.43%. Also, board size (BDSZ) ranges from 3.00 to 15.00 with a mean of 10 board members. These results are in line with previous related studies in the banking sector (e.g., Hasan & Dridi, 2010; Rosman, Wahab, & Zainol, 2014). Finally, the values of other variables reported in Table 6 suggest widespread variations in our sample, hence decreasing the possibilities of any sample selection bias.

Summary Statistics of All Variables for All 425 Observations.

Note. The sample consists of all listed Islamic and dual banks covering 10 countries in the Arab MENA region, namely, Bahrain, Egypt, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, and UAE. The data are extracted from Perfect information Database, Banks’ Websites, Bankscope Database, and the World Bank Database for 8 years from 2006 to 2013 inclusive. The final number of bank-year observations is 179 bank-year observations for Islamic banks and 246 bank-year observations for dual banks. This table reports the mean, standard deviation, and values of the minimum and the maximum range for all variables. See Table 2 for the definitions of each variable. RDPI = risk management and disclosure practices index; W-RDPI = weighted risk management and disclosure practices index; IGQ = Islamic governance quality; NGQ = national governance quality.

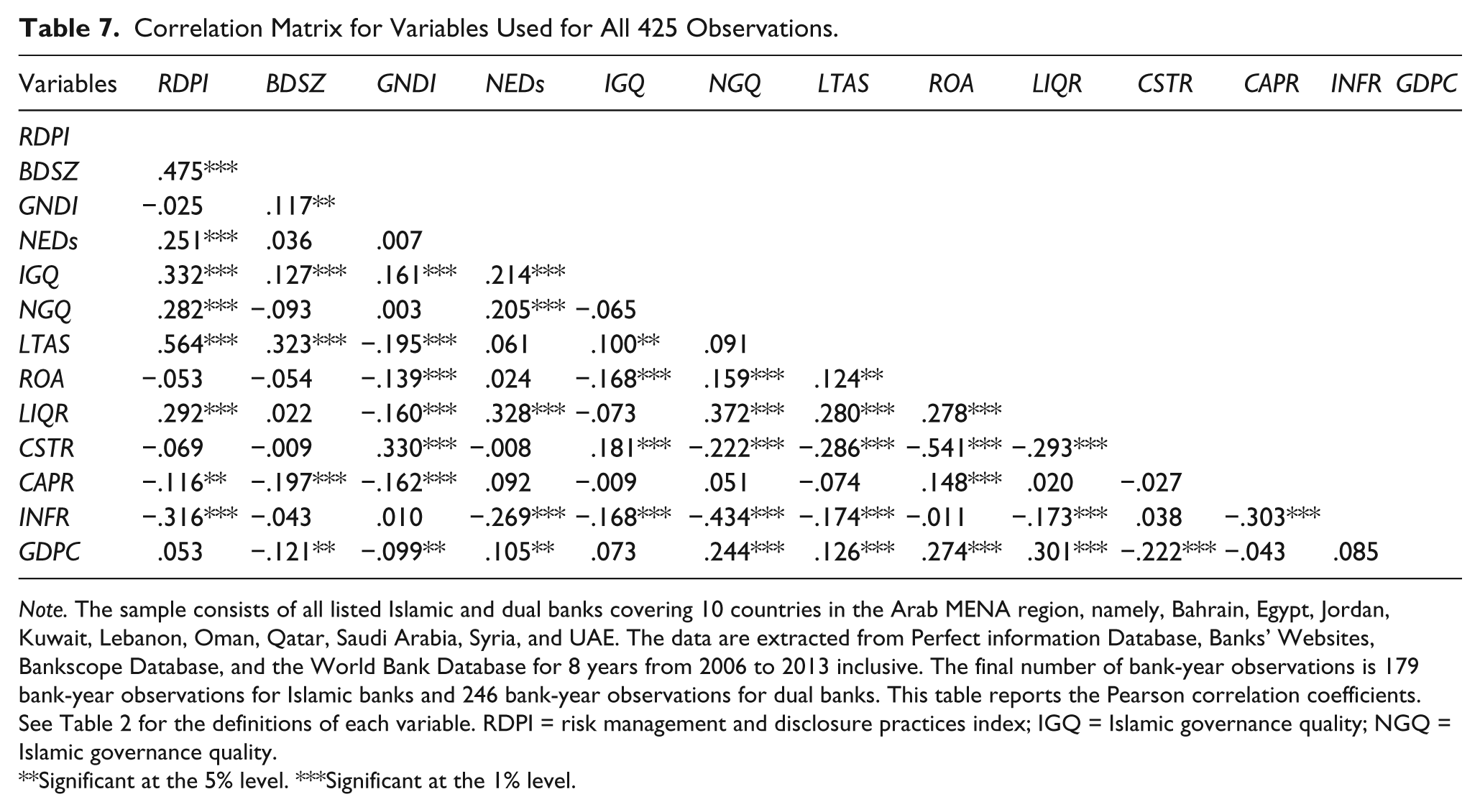

Table 7 reports the correlation matrix of Pearson’s parametric coefficients for all variables to test for multicollinearities relating to the regression analysis. Evidently, low correlation coefficients among the variables presented in Table 7 indicate absence of any serious multicollinearity problems. In addition, Table 7 shows statistically significant correlation between the RDPI and the other variables. For instance, BDSZ, NEDs, IGQ, NGQ, LTAS, and LIQR are positively related to the RDPI, whereas CAPR and INFR are negatively associated with the RDPI.

Correlation Matrix for Variables Used for All 425 Observations.

Note. The sample consists of all listed Islamic and dual banks covering 10 countries in the Arab MENA region, namely, Bahrain, Egypt, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, and UAE. The data are extracted from Perfect information Database, Banks’ Websites, Bankscope Database, and the World Bank Database for 8 years from 2006 to 2013 inclusive. The final number of bank-year observations is 179 bank-year observations for Islamic banks and 246 bank-year observations for dual banks. This table reports the Pearson correlation coefficients. See Table 2 for the definitions of each variable. RDPI = risk management and disclosure practices index; IGQ = Islamic governance quality; NGQ = Islamic governance quality.

Significant at the 5% level. ***Significant at the 1% level.

Regression Analyses and Discussion

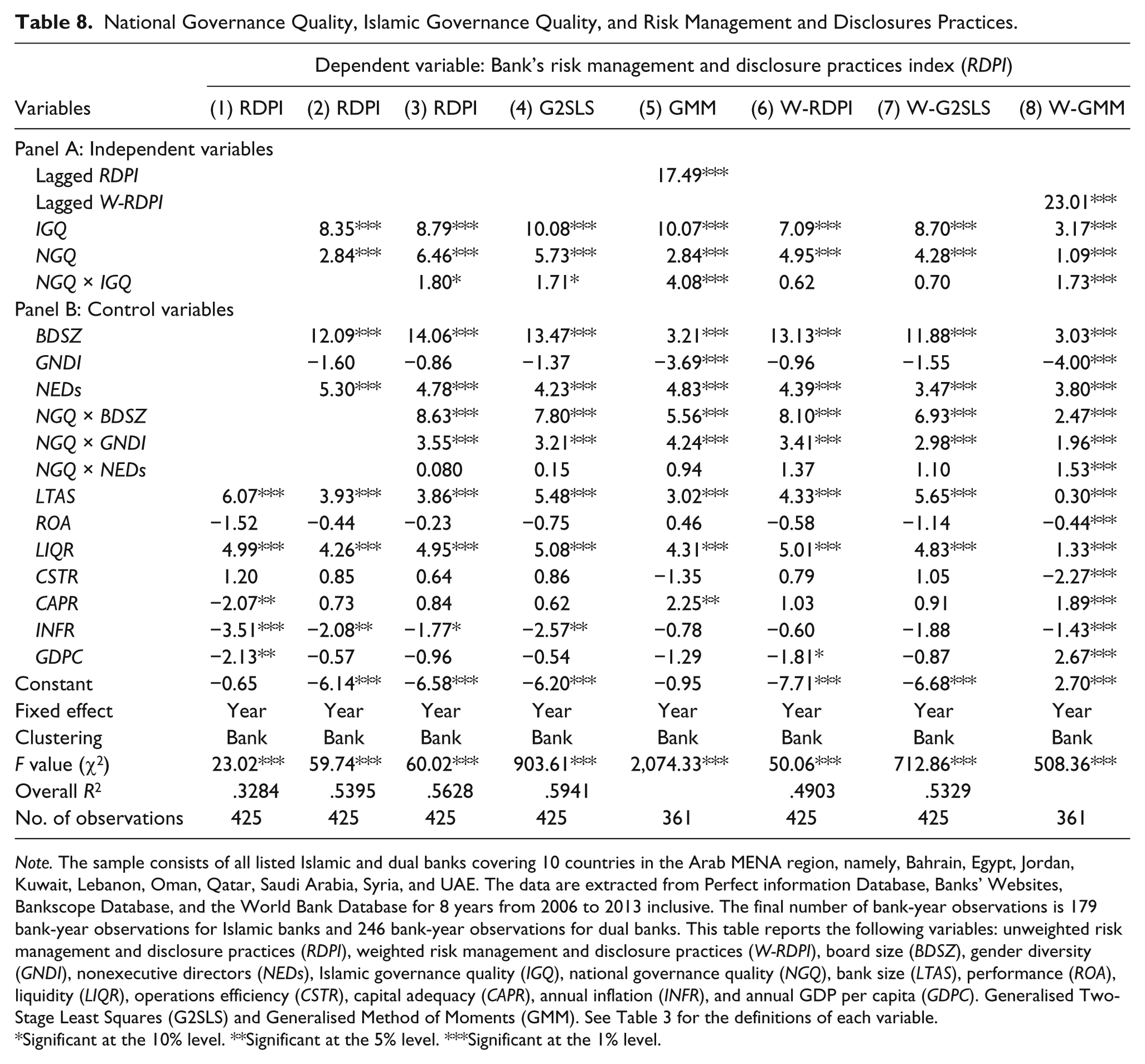

Table 8 reports the fixed-effects regression results of the relationship among national governance quality (NGQ), Islamic governance quality (IGQ), and risk disclosures (RDPs). The findings of Models 1, 2, and 3 indicate that IGQ and NGQ are important in explaining observable differences in RDPs as follows. First, we examine whether IGQ affect the level of RDPI. The coefficients of the IGQ in Models 2 and 3 of Table 8 are positive (t = 8.35, p < .001 and t = 8.79, p < .001, respectively), thus providing empirical support for Hypothesis 1. Specifically, this offers new evidence, which suggests that better governed Islamic banks are more transparent about their risk management and disclosure practices than their poorly governed counterparts. To the best of our knowledge, this is the first study to examine the impact of IGQ on the level of RDPs. This evidence is largely in line with previous studies that suggest that Islamic governance can improve general voluntary disclosure quality (Al-Bassam & Ntim, 2017; Farook et al., 2011; Haniffa & Hudaib, 2007). This evidence is also consistent with the expectations of our neo-institutional framework presented in Figure 1, which suggests that effective Islamic governance conveys additional monitoring and accountability requirements on Islamic banks, thereby encouraging them to engage in greater RDPs (Al-Bassam & Ntim, 2017; Elghuweel et al., 2017; Jensen & Meckling, 1976). Similarly, enhanced RDPs, due to coercive, normative, and mimetic pressures can lead to higher levels of risk disclosures to gain legitimacy from the broader society, which can facilitate access to critical resources, such as finance (Chandler & Hwang, 2015; Connelly et al., 2011; Haniffa & Hudaib, 2007; Pittroff, 2014). All together, the result reveals that religiosity (i.e., Islamic governance) can serve as a motivating force for managers to commit to greater levels of accountability and transparency through increased RDPs, and thereby improve both the efficiency and legitimacy of Islamic banks’ operations (Al-Bassam & Ntim, 2017; Farook et al., 2011; Haniffa & Hudaib, 2007).

National Governance Quality, Islamic Governance Quality, and Risk Management and Disclosures Practices.

Note. The sample consists of all listed Islamic and dual banks covering 10 countries in the Arab MENA region, namely, Bahrain, Egypt, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, and UAE. The data are extracted from Perfect information Database, Banks’ Websites, Bankscope Database, and the World Bank Database for 8 years from 2006 to 2013 inclusive. The final number of bank-year observations is 179 bank-year observations for Islamic banks and 246 bank-year observations for dual banks. This table reports the following variables: unweighted risk management and disclosure practices (RDPI), weighted risk management and disclosure practices (W-RDPI), board size (BDSZ), gender diversity (GNDI), nonexecutive directors (NEDs), Islamic governance quality (IGQ), national governance quality (NGQ), bank size (LTAS), performance (ROA), liquidity (LIQR), operations efficiency (CSTR), capital adequacy (CAPR), annual inflation (INFR), and annual GDP per capita (GDPC). Generalised Two-Stage Least Squares (G2SLS) and Generalised Method of Moments (GMM). See Table 3 for the definitions of each variable.

Significant at the 10% level. **Significant at the 5% level. ***Significant at the 1% level.

Second, our results show that cross-sectional differences in the RDPI level can largely be explained by NGQ. Specifically, the coefficient of the NGQ in Models 2 and 3 of Table 8 is positive (t = 2.84, p < .005, and t = 6.46, p < .000, respectively), and thus providing empirical support for Hypothesis 2. In particular, this offers a new evidence to suggest that banks in better governed countries engage in greater RDPs compared with their poorly governed counterparts. To the best of our knowledge, this is the first empirical evidence to examine the impact of NGQ on RDPs, although this finding offers further empirical support for the findings of prior studies that suggest that NGQ has a positive effect on general voluntary disclosures (Barakat & Hussainey, 2013; Cahan et al., 2015). This evidence is also consistent with the expectations of our neo-institutional theoretical perspective, which suggests that improved NGQ can provide additional layer of monitoring that can help mitigate the level of information asymmetry, hence offering bank executives greater motivation to commit to increased risk disclosures. Collectively, the NGQ results in Tables 8 and 9 are consistent with the notion that NGQ has a positive effect on bank executives’ commitment to accountability and transparency in the form of increased RDPs.

National Governance Quality, Islamic Governance Quality, and Risk Management and Disclosures Practices: Islamic Versus Dual Banks.

Note. The sample consists of all listed Islamic and dual banks covering 10 countries in the Arab MENA region, namely, Bahrain, Egypt, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, and UAE. The data are extracted from Perfect information Database, Banks’ Websites, Bankscope Database, and the World Bank Database for 8 years from 2006 to 2013 inclusive. The final number of bank-year observations is 179 bank-year observations for Islamic banks and 246 bank-year observations for dual banks. This table reports the following variables: unweighted risk management and disclosure practices (RDPI), weighted risk management and disclosure practices (W-RDPI), board size (BDSZ), gender diversity (GNDI), nonexecutive directors (NEDs), Islamic governance (IGQ), national governance quality (NGQ), bank size (LTAS), performance (ROA), liquidity (LIQR), operations efficiency (CSTR), capital adequacy (CAPR), annual inflation (INFR), and annual GDP per capita (GDPC). Generalised Two-Stage Least Squares (G2SLS) and Generalised Method of Moments (GMM). See Table 3 for the definitions of each variable.

Significant at the 10% level. **Significant at the 5% level. ***Significant at the 1% level.

Finally, to ascertain whether the IGQ–RDPI relationship can be moderated by NGQ (to test Hypothesis 3), we create interaction variables between the IGQ and NGQ variables (i.e., NGQ × IGQ) in Model 3 of Table 8. 3 Our estimation is based on the emerging theoretical and empirical evidence (Aguilera, 2005; Aguilera et al., 2008; Alon & Dwyer, 2014; Cahan et al., 2015; Ernstberger & Grüning, 2013; Essen et al., 2013), which suggests that the impact of the IGQ on RDPs can be enhanced in countries with higher NGQ. Observably, the respective coefficient of NGQ × IGQ on the RDPI in Model 3 of Table 8 (t = 1.80, p < .072) is positive, thus providing original evidence, which supports Hypothesis 3. That is, this contributes to the literature by offering new evidence, which suggests that the IGQ–RDPI relationship is significantly and positively improved by NGQ. Thus, this result offers further evidence of the influence that NGQ has on the IGQ–RDPI relationship. Specifically, our evidence indicates that Islamic bank managers operating in better governed countries are more likely to coercive, mimetic, and normative pressures from national institutions, such as accounting regulators, business and treasury ministries, and stock exchanges. This appears to compel Islamic bank executives to commit to increased risk disclosures as a way of gaining legitimacy from the broader society, thereby securing access to critical resources, such as finance.

Additional Analyses

We perform a number of further analyses to determine the robustness of our results. First, as a robustness check, we reproduce our analysis in Model 3 of Table 8 by replacing our unweighted RDPI with the weighted RDPI (W-RDPI), and the results are presented in Model 6 of Table 8. These results are similar to those reported in Model 3 of Table 8, implying that our results seem to be robust to the use of a weighted or an unweighted disclosure index. Second, following extant research (Ntim et al., 2013), we address potential endogeneities that may be affected by omitted variable bias by estimating two-stage least squares using generalized panel-data estimators (G2SLS). First, we predict instruments by estimating a model for IGQ. Second, we check correlations with error terms, and then, we use the predicted values as instruments. Thus, in the second stage, we use the instrumented variables of the IGQ and rerun in Equation 1 as follows:

where in Equation 2, everything else remains unaffected as stated in Equation 1, except that we use the instrumented part of the IGQ, and other bank-level governance variables. The results are presented in Model 4 of Table 8. These results are also similar to those reported in Model 3 of Table 8, implying that our results appear to be robust to potential endogeneities that may be caused by omitted variables bias.

Third, to ascertain the assumption underlying our fixed-panel regression model that all the unobserved heterogeneities may affect the correlation between the Islamic governance variables and the error term is invariable over time, we calculate a dynamic panel GMM estimator as proposed by Wintoki, Linck, and Netter (2012). Dynamic GMM estimators have the unique ability to control for a number of endogeneity problems, including reverse causality, unobservable firm-specific factors, dynamic endogenous regressors, possible omitted variables bias, heteroscedasticity, and simultaneity by allowing all the explanatory variables (e.g., the Islamic governance and all control variables) to be considered as endogenous (Ammann, Oesch, & Schmid, 2011; Arellano & Bond, 1991; Arellano & Bover, 1995; Wintoki et al., 2012). Consequently, in the dynamic GMM model, we employ Equation 3 as follows:

where RDPI is a proxy of risk management and disclosure practices level for bank i during year t.

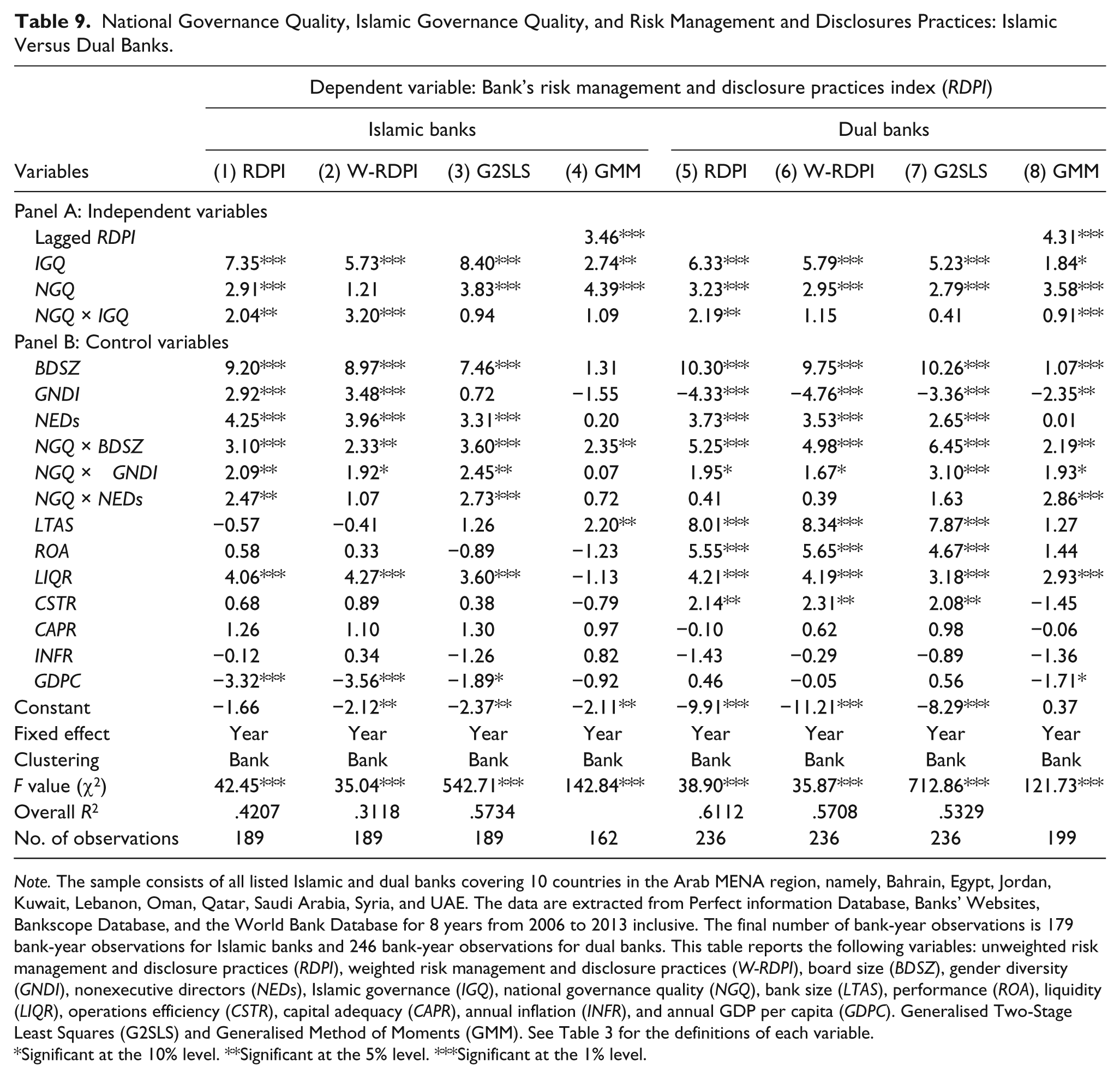

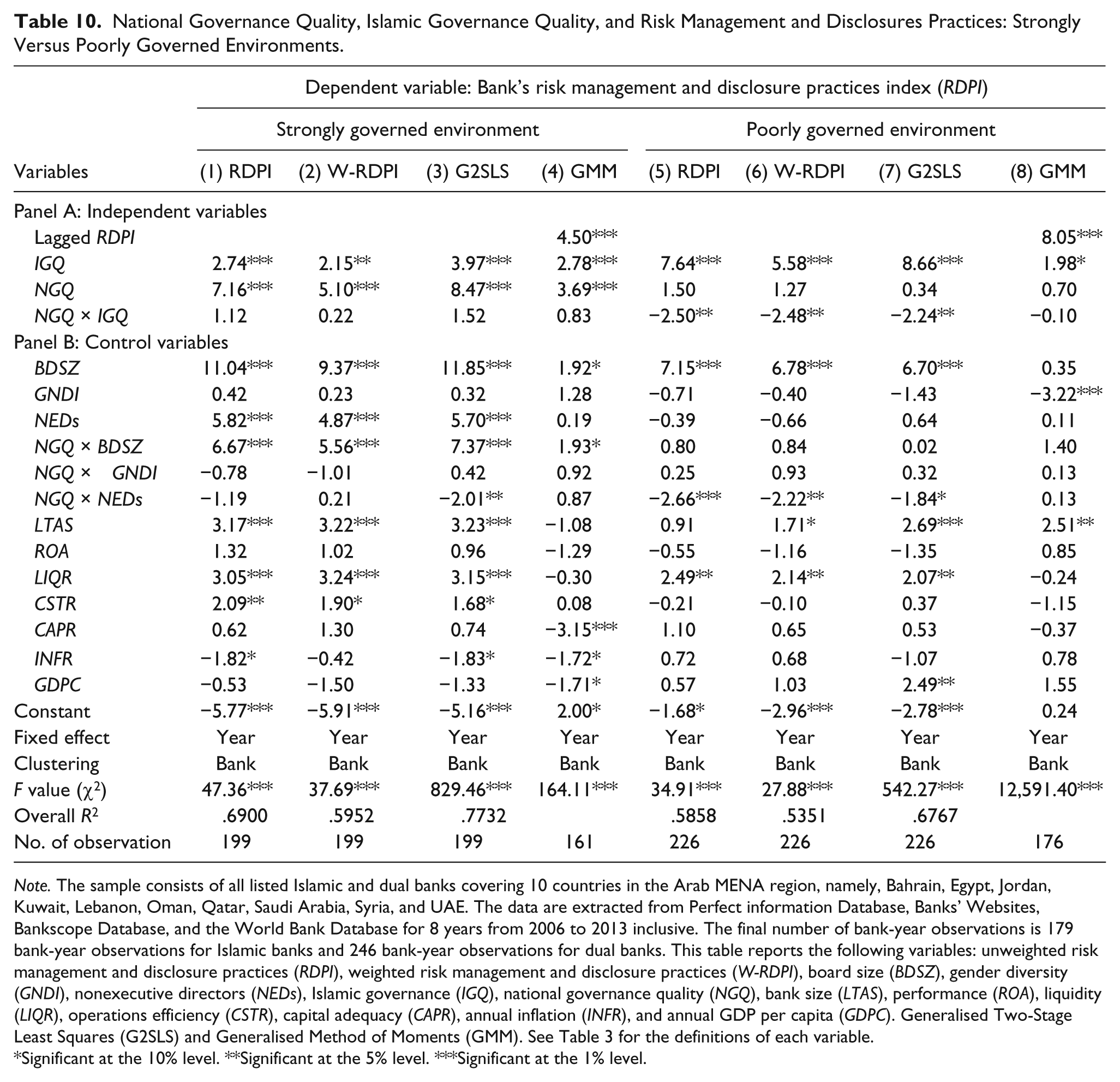

Fourth, we consider the robustness of our results to subsamples: Islamic banks and dual banks by rerunning Equations 1, 2, and 3, and the results are reported in Table 9. Apart from a few sensitivities (such as GNDI being now statistically significant), the results in Table 9 are similar to those reported in Table 8, thereby implying that our results seem to be fairly robust to the use of subsamples. Finally, Table 10 reports the results of the variables that influence banks to commit to greater risk disclosures, and how those variables work among banks operating in strongly governed and poorly governed environments. Table 10 reveals that IGQ and NGQ have a significant impact on RDPs in banks that operate in strongly governed environments compared with their counterparts that operate in countries with poorly governed national environments. Similarly, we found that gender diversity has a positive effect on RDPs in banks that operate in strongly governed environments compared with their counterparts operating in poorly governed countries, although this relationship is not statistically significant. Overall, the results support our hypothesis that NGQ has a moderating effect on the relationship between IGQ and bank risk disclosures.

National Governance Quality, Islamic Governance Quality, and Risk Management and Disclosures Practices: Strongly Versus Poorly Governed Environments.

Note. The sample consists of all listed Islamic and dual banks covering 10 countries in the Arab MENA region, namely, Bahrain, Egypt, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, and UAE. The data are extracted from Perfect information Database, Banks’ Websites, Bankscope Database, and the World Bank Database for 8 years from 2006 to 2013 inclusive. The final number of bank-year observations is 179 bank-year observations for Islamic banks and 246 bank-year observations for dual banks. This table reports the following variables: unweighted risk management and disclosure practices (RDPI), weighted risk management and disclosure practices (W-RDPI), board size (BDSZ), gender diversity (GNDI), nonexecutive directors (NEDs), Islamic governance (IGQ), national governance quality (NGQ), bank size (LTAS), performance (ROA), liquidity (LIQR), operations efficiency (CSTR), capital adequacy (CAPR), annual inflation (INFR), and annual GDP per capita (GDPC). Generalised Two-Stage Least Squares (G2SLS) and Generalised Method of Moments (GMM). See Table 3 for the definitions of each variable.

Significant at the 10% level. **Significant at the 5% level. ***Significant at the 1% level.

Conclusion and Areas for Future Research

Although the effects of business-level factors on the level of corporate risk management and disclosure practices (RDPs) have been fairly documented, the role of religion and macro-social-level factors, such as Islamic and national governance quality on RDPs are rare. Therefore, this article has sought to make a number of new contributions to the extant literature by (a) examining the associations among religious governance, especially Islamic governance quality (IGQ), national governance quality (NGQ), and RDPs; and (b) consequently, ascertaining whether the link between IGQ and RDPs can be moderated by NGQ.

Using one of the largest data sets to date from MENA Islamic banks over the 2006 to 2013 period, our study reveals several interesting findings. Our results suggest that Islamic and national governance quality has a significant effect on the level of bank risk disclosures. Specifically, our results indicate that risk disclosures are high in banks with high IGQ and NGQ. In addition, our results indicate that NGQ moderates the association between IGQ and RDPs. This implies that banks that depict greater commitment toward incorporating Islamic governance into their operations through high Islamic governance index score, and located in better governed countries, engage in higher risk disclosures than those that are not. These results are consistent with the predictions of our neo-institutional framework that incorporates both efficiency/instrumental and legitimation/moral views of neo-institutional theory.

This study makes a number of new contributions to the extant literature. First, and to the best of our knowledge, our study offers a first-time evidence on the effect of national governance quality on bank risk management and disclosure practices using a neo-institutional framework. Second, we offer evidence on the impact of Islamic governance quality on bank risk management and disclosure practices. Finally, we provide evidence relating to the moderating effect of national governance quality on the relationship between Islamic governance quality and bank risk management and disclosure practices for the first time. The success of our generalized neo-institutional framework in explaining the variations and drivers of bank risk disclosures reflects, in part, its ability to integrate complexity. The diverse variations of institutionalism within our research context make it doable to cogitate the contextual embeddedness of the intersections between religion and country governance, as macro-social-level forces operating within the context of Islamic banks.

Consequently, our results have a number of implications for regulators, banks, and investors, especially in emerging markets. Our results suggest that better governed banks at bank or national level have higher tendency to commit to increased level of risk disclosures. These results offer regulators extra incentive to pursue internal CG reforms jointly with national-level governance reforms. Regarding banks, our results suggest that better Islamic governance is expected to be associated with better risk disclosures. These results offer shareholders of banks additional incentive to enhance their banks’ board structure (e.g., board size and board independence) and pay attention to Islamic governance arrangements in particular. These results also bring to bear the importance of Islamic governance in mitigating traditional agency problems, such as information asymmetry, thereby enhancing bank efficiency and legitimacy within the broader society. Thus, our study also has practical implications. Specifically, banks that voluntarily incorporate prudential Islamic governance into their operations are more likely to be more transparent about their RDPs and, hence, offer new crucial insights on Islamic governance and their impact on disclosure quality. Overall, our results highlight the role that religion and national governance, as major macrosocial forces, can play in traditional rational business decision making, such as disclosure and transparency.

Finally, although our evidence is significant and robust, there are a number of limitations that need to be explicitly acknowledged. Such as all archival and quantitative studies of this nature, our governance and disclosure proxies may or may not reflect actual managerial practice. In this case, additional insights may be offered by future studies that may employ qualitative approaches using, for example, interviews, case studies, and observations that may offer a more nuanced and in-depth insight regarding these relationships. Furthermore, researchers might investigate the impact of further governance mechanisms (e.g., risk committee and remuneration committee) on risk disclosures, and might also be extended to the use of nonparametric statistical techniques, such as neural networks to test the robustness of their findings.

Footnotes

Appendix

Risk management and disclosure practice index (RDPI).

| Risk type | Financial risk management and disclosure practices |

|---|---|

| i. Credit | 1. Exposure to credit risk and how they arise 2. Objectives, policies, and processes for managing credit risk 3. Method of measuring credit risk exposure 4. Adequate description of how credit risk management occurs, including providing a clear linkage between quantitative data and qualitative description 5. Changes in exposure to credit risk, measurement of risk, and objectives, policies, and processes to manage credit risk from the previous period 6. Amount of regulatory capital for credit risk 7. Information about credit quality of financial assets that are not past due or impaired 8. Renegotiated financial assets 9. Aging schedule for past due amounts 10. Impairment methods and inputs disclosed 11. Summary of quantitative data about exposure to credit risk at the reporting date 12. Maximum credit exposure by currency 13. Maximum credit exposure by geography 14. Maximum credit exposure by economic activity 15. Disaggregated maximum credit risk exposure, including derivatives and off-balance sheet items 16. Renegotiated loans for troubled borrowers 17. Risk of counterparty 18. Credit risk concentrations 19. Derivatives 20. Off-balance sheet and joint venture structures 21. Credit risk transfer/mitigation/hedging techniques 22. Collateral 23. Disclosures to help users understand credit risk |

| Risk type | Financial risk management and disclosure practices |

| ii. Liquidity | 24. Exposure to liquidity risk and how they arise 25. Objectives, policies, and processes for managing liquidity risk 26. Methods used to measure liquidity risk 27. Changes in exposure to liquidity risk, measurement of risk, and objectives, policies, and processes to manage liquidity risk from the previous period 28. Contractual undiscounted cash flows 29. Maturity analysis of nonderivative liabilities 30. Maturity analysis of derivative liabilities 31. Maturity analysis of off-balance sheet commitments and other financial instruments without contractually stipulated maturity 32. Maturity analysis of financial assets 33. Expected maturity analysis 34. Derivative and trading liabilities treatment 35. Liquidity risk transfer/mitigation/hedging techniques 36. Liquidity buffers sources and volume 37. Sensitivity analysis. 38. Financing facilities. 39. Counterparty concentration profile. 40. Disclosures to help users understand liquidity risk |

| iii. Market | 41. Objectives, policies, processes, and strategies of market risk management 42. Structure and organization of market risk management function 43. Instruments traded types 44. Interest rate risk 45. Equity risk 46. Currency risk 47. Commodities risk 48. Market risk transfer/mitigation/hedging techniques 49. Linkage with credit risk 50. Amount of regulatory capital for market risk 51. VAR 52. VAR limitations 53. Stress testing 54. Stress VAR 55. Back-testing 56. Disclosures to help users understand market risk |

| iv. Capital | 57. Capital management 58. Capital measurement 59. Risk weighted assets 60. Tier 1 61. Tier 2 |

| Nonfinancial risk management and disclosures practices | |

| v. Operational | 62. Amount of regulatory capital for operational risk. 63. Regulatory capital for operational risk measurement approach. 64. Operational risk management strategies and processes. 65. The operational risk management function structure and organization 66. Scope and nature of the operational risk reporting system 67. Operational risk transfer/mitigation/hedging techniques 68. Operational VAR 69. Internal audit function/internal control system 70. Key risk indicators/early warning systems 71. Self-assessment techniques 72. Stress tests/scorecard models/scenario analyses |

| Risk type | Financial risk management and disclosure practices |

| 73. Operational risk event databases |

|

| vi. Strategic | 84. Sovereign/politics |

| Total | 96. Risk management and disclosure practices items |

| Procedure of scoring for unweighted index | |

| 0: Risk item not disclosed by bank | |

| 1: Risk item disclosed by bank | |

| Procedure of scoring for weighted index | |

| 0: Risk item not disclosed by bank | |

| 1: Risk item disclosed by bank contains past, future, good, bad, and/or qualitative information | |

| 2: Risk item disclosed by bank contains past, future, good, bad, qualitative and/or quantitative information | |

Note. VAR = value at risk.

Acknowledgements

We would like to thank the editors (Professor Harry Van Buren, Professor Jawad Syed, and Dr Raza Mir) and three anonymous referees for very helpful comments and suggestions. We would also like to acknowledge constructive and useful comments received from the participants at the 2017 Business & Society Manuscript Development Workshop at Brigham Young University, Provo, Utah, United States, and 2017 British Accounting and Finance Association Annual Conference in Edinburgh, United Kingdom.

Authors’ Note

Any remaining errors are the responsibility of the authors.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.