Abstract

The elimination of double marginalization has been an important consideration in recent updates to the U.S. Horizontal and Vertical Merger Guidelines, in particular, and the evaluation of whether vertical mergers are pro- or anticompetitive, in general. This article extends frameworks for analyzing the effects of eliminating double marginalization on prices from situations with upstream and downstream monopolies to encompass Cournot oligopolies both upstream and downstream.

I. Introduction

In 2020, the United States Department of Justice (DOJ) and Federal Trade Commission (FTC)—the U.S. competition agencies—withdrew their 1984 guidelines (DOJ) and replaced them with new Vertical Merger Guidelines (DOJ and FTC). 1 During the almost four decades the old guidelines were in effect, the competition agencies had litigated only one merger to completion—the 2018 AT&T/Time Warner merger, 2 consistent with the possibility that unlike horizontal mergers, which have the potential to increase prices by lessening competition (absent offsetting efficiencies), vertical mergers can result in lower prices due to elimination of double marginalization.3,4

In response to these developments, Alderman and Blair addressed the trade off between the procompetitive effects of eliminating double marginalization and the reduction of potential downstream competition. 5 In particular, Alderman and Blair extended the textbook analysis of successive upstream and downstream monopolies 6 to address downstream duopolies. This article further extends that framework to include general results for Cournot oligopolies both upstream and downstream. This more general framework is consistent with the recently issued Merger Guidelines. In particular, the guidelines explain that the structures of both upstream and downstream markets are relevant in evaluating mergers. 7

The remainder of this article is organized as follows. Section II presents the solutions for the upstream price, downstream price, and quantities for Cournot oligopolies. Section III derives those solutions. Section IV presents illustrative results and Section V summarizes the findings.

II. General Results

The framework consists of the following:

Inverse linear demand curve: Pd = A – b Q, where Pd is the downstream price and Q is the quantity of the final output.

Cournot competition among m upstream firms supplying an input for downstream firms, each with marginal cost MCui (possibly unequal) and no fixed costs.

Cournot competition among n downstream firms producing the final output, each with a marginal cost MCdj (possibly unequal) in addition to the price of the upstream input and no fixed costs.

The following three equations describe the general solution:

where

The framework represented by the three equations encompasses the range from (1) upstream/downstream monopolies (n = m = 1) 8 ; (2) upstream monopoly/downstream Cournot oligopoly (m = 1; 1 > n < ∞) 9 ; (3) upstream monopoly/downstream perfect competition or equivalently, vertical integration, or Bertrand competition (m = 1; n large); and (4) upstream and downstream oligopolies (m > 1; n > 1).

The price equations have the following properties. First, the upstream price (Pu) stays the same as the number of downstream firms increase. Upstream profits increase as downstream competition intensifies, due the greater sales of the input at a positive margin over marginal cost. Second, the downstream price depends on the sum of the upstream and downstream marginal costs (

III. Derivation

The derivation of equations (1)–(3) starts with the general formula for the equilibrium price for a Cournot oligopoly with N firms 12 :

where N is the number of firms and

The upstream price (equation (1)) follows from the inverse derived demand for the input, 13 which is derived from equation (3):

In particular, equating the right-hand sides of equations (2) and (5) produces the following:

This equation can be rearranged to produce:

That is, the intercept of the derived inverse demand curve for the input is

Applying equation (4) to the inverse demand curve shown in equation (7) (with A’ =

IV. Illustrative Examples

This section extends the results presented in Alderman and Blair.

14

Their examples are based on an inverse demand curve of Pd = 150 – 0.1 × Q, an upstream monopolist with MCu = 50 and one (monopoly) or two (duopoly) downstream firms, with MCd = 10. Alderman and Blair also present results for vertical integration of the upstream and downstream monopolies (m = 1; n large number) and for a competitive outcome (Pd =

Prices and Outputs for Upstream Monopoly and Downstream Oligopoly.

The third through fifth columns extend the results to downstream oligopolies of three, four, and five firms. While the increased downstream competition results in lower prices and greater output, the outcomes are inferior to vertical integration, which is equivalent to perfect downstream competition.

Alderman and Blair (2022, 46) also explain that entry could occur upstream, rather than (or addition to) downstream. Table 2 presents parallel results that compare vertical integration and the concomitant elimination of double marginalization with potential upstream entry. As explained above, with the same inverse demand curve and upstream and downstream marginal costs, downstream prices and outputs are the same as in Table 1. The reduction in upstream prices resulting from greater upstream competition is exactly offset by the larger monopoly (relative to oligopoly) downstream mark-ups.

Prices and Outputs for Downstream Monopoly and Upstream Oligopoly.

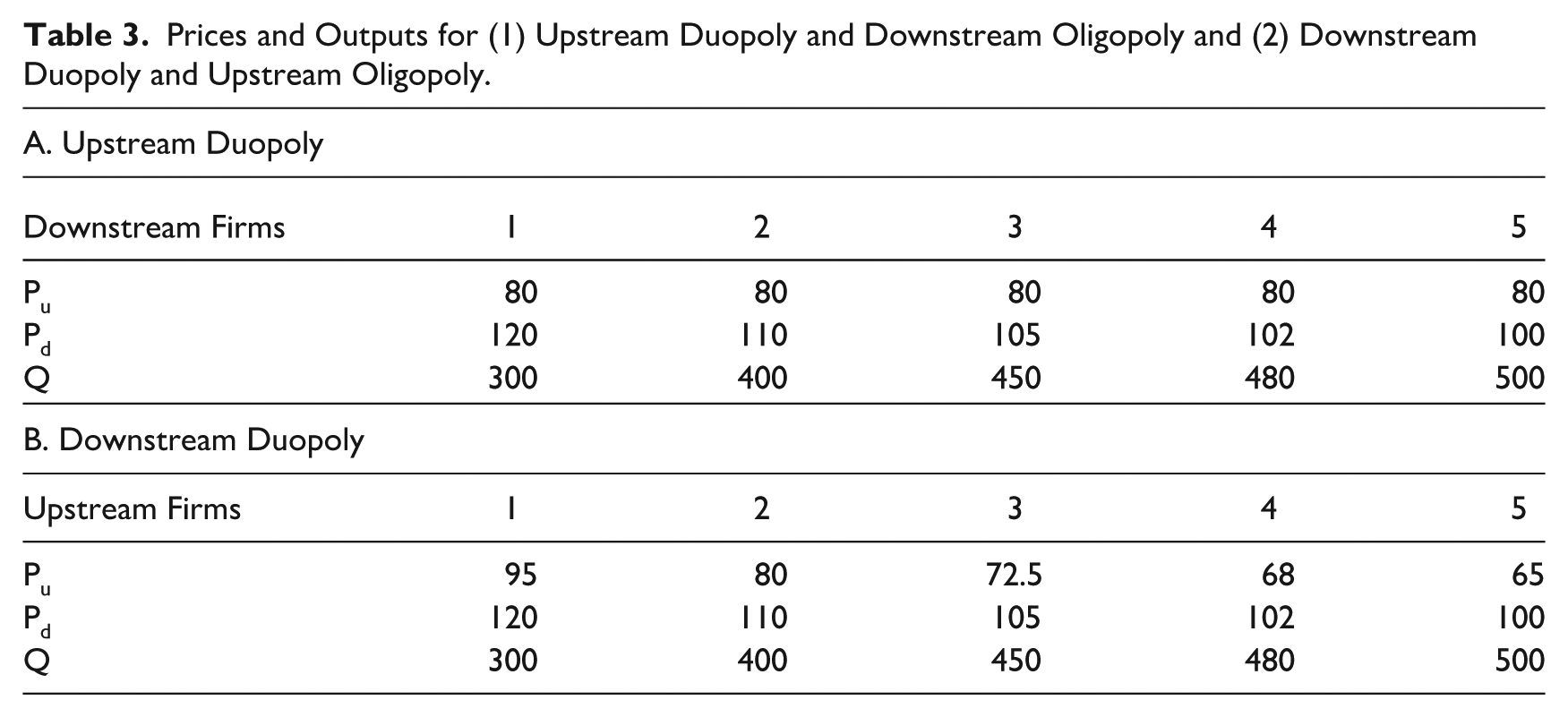

Finally, Table 3 demonstrates the general result that an oligopoly with j firms upstream and k firms downstream produces the same downstream prices as and oligopolies with k upstream and j downstream firms, again given common inverse demand curves and upstream and downstream marginal costs. In particular, the table compares the results for an upstream duopoly with the parallel results for a downstream duopoly.

Prices and Outputs for (1) Upstream Duopoly and Downstream Oligopoly and (2) Downstream Duopoly and Upstream Oligopoly.

The results in Table 3 mirror those in Tables 1 and 2, for example, the downstream price and quantity for an upstream duopoly (j = 2) and a downstream oligopoly with four firms (k = 4) are the same as for a downstream duopoly (k = 2) and an upstream four-firm oligopoly (j = 4). Table 3 also demonstrates the increased price constraint duopoly competition has relative to monopoly, for example, an upstream duopoly with a three-firm downstream oligopoly results in the same downstream price and quantity as an upstream monopoly with perfect downstream competition. 16

V. Summary

Consistent with the recently-released Merger Guidelines’ explanation that the structures of both upstream and downstream markets are relevant in evaluating vertical mergers, this article extends previous analyses of mergers of upstream monopolies and downstream monopolies or duopolies to upstream and downstream oligopolies with one or more firms. Based on upstream and downstream Cournot competition and linear inverse demand curves, upstream prices and downstream prices have the properties that (1) while the upstream price depends on the number of upstream competitors, it is independent of the number of downstream firms, (2) the downstream price is a function of the sum of upstream and downstream marginal costs, but not on how these costs are distributed upstream and downstream, and (3) downstream prices and outputs are symmetric in the sense that the price and output for a j-firm upstream oligopoly providing inputs to a k-firm downstream oligopoly is the same as the price and output for a k-firm upstream oligopoly providing inputs to a j-firm downstream oligopoly.

Footnotes

Acknowledgements

This article is based on the author’s experience as the instructor in Northeastern University’s Econ 4680 course, Competition Policy and Regulation. Thanks to David Sappington, co-author of the text used for the course, for ongoing email communications.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

1.

U.S. Department of Justice, DOJ and FTC announce draft vertical merger guidelines for public comment, ![]() .

.

2.

Dennis W. Carlton et al., Evaluating a Theory of Harm in a Vertical Merger: AT&T/Time Warner. in

3.

Id. at 92.

4.

The 2020 Vertical Merger Guidelines describes double marginalization as follows:

Due to the elimination of double marginalization, mergers of vertically related firms will often result in the merged firm’s incurring lower costs for the upstream input than the downstream firm would have paid absent the merger. This is because the merged firm will have access to the upstream input at cost, whereas often the downstream firm would have paid a price that included a markup. The elimination of double marginalization. . .arises directly from the alignment of economic incentives between the merging firms.

5.

Brianna L. Alderman & Roger D. Blair, Preserving Potential Competition Is Not the Holy Grail of Vertical Merger Enforcement, 36

6.

W. Kip Viscusi et al., Economics of Regulation and Antitrust 262–65 (5th ed. MIT Press 2018).

7.

DOJ & FTC, 2023, supra note 1, at 15–16. The new guidelines include vertical mergers in a broader category of mergers that may limit access to products and services that rivals use to compete. Id. at 13–18. Under the Merger Guidelines framework, the upstream market that provides the product or service corresponds to the Merger Guidelines’ related market and the downstream market to the Merger Guidelines’ relevant market.

8.

Viscusi et al., supra note 6, at 262–265.

9.

Alderman & Blair, supra note 5.

11.

Inserting the formula for the upstream price from equation (1) into ![]() and simplifying results in:

and simplifying results in:

For given upstream and downstream marginal costs, this formula produces the same downstream price when m = j and n= k and when m = k and n = j.

12.

Timothy J. Tardiff, Efficiency Metrics for Competition Policy in Network Industries, 6

13.

15.

The corresponding results from applying equations (1)–(![]() ) to

) to