Abstract

The vertical merger of AT&T and Time Warner combined one of the largest multiple video program distributors (MVPDs) in the United States with one of the largest providers of pay-TV programming. This study evaluates the potential competitive effects of the transaction by considering changes in the equity valuations of the respective upstream and downstream competitors to the merging parties when news of their proposed merger became public. Consistent with the government’s central theory of harm, it appears that financial markets expected the proposed transaction to result in Time Warner increasing its carriage fees to AT&T’s and DirecTV’s MVPD rivals. Market reactions to the announcement of AT&T’s commitment to enter into binding arbitration when negotiating future carriage fees for Tuner content provide further support for this inference. The results are difficult to rationalize in terms of the various efficiencies and synergies that AT&T claimed it would realize from the merger.

I. Introduction

In October 2016, AT&T announced its intention to acquire Time Warner for approximately US$85 billion. The relevant antitrust product markets implicated by the merger were the distribution of video programming content to pay-TV consumers and the associated supply of that programming to distributors. AT&T operated as a downstream (“retail”) multi-programming video distributor (“MVPD”) primarily through its ownership of DirecTV, whereas Time Warner was an “upstream content provider” (UCP), that is, a firm that produced and sold upstream video programming content to MVPDs throughout the United States. 1 The proposed transaction therefore represented a “pure” vertical merger as the parties were not significantly involved in each other’s primary lines of business. 2 An extensive public debate formed before and during the district court trial on whether the AT&T/Time Warner merger was likely to benefit or harm pay-TV consumers. 3

The U.S. Department of Justice (“DOJ”) sued to block the merger in the U.S. District Court of Columbia. 4 The district court trial culminated in June 2018 with Judge Richard J. Leon issuing a ruling in favor of the defendants. 5 The court—in unusually strong language—criticized almost every facet of the plaintiff’s affirmative case, placing particular emphasis on the assumptions underlying the government’s Nash bargaining model (used to predict downstream welfare effects); the inputs used to parameterize that model; and the other theories of harm advanced by the DOJ for enjoining the merger. 6 The court also gave significant weight to the parties’ claims of various revenue synergies arising from the combination of their viewership and advertising assets.

The litigation surrounding the proposed merger highlighted several potential challenges in assessing vertical mergers, particularly those associated with measuring various inputs (e.g., diversion ratios or profit margins) required to score postmerger pricing incentives. The trial testimonies of the opposing economic experts also conveyed the sensitivity of each other’s results to seemingly minor changes in the assumptions or data used to derive those inputs. This apparent lack of robustness served as one rationale for Judge Leon’s dismissal of the evidence provided by the government’s merger simulation model, but the court also questioned the general applicability of (Nash) bargaining theory to model or predict postmerger price effects. For example, there was a question of whether unaffiliated MVPDs would view threats of long-term input foreclosure by the merged entity as credible, with Judge Leon concluding they would not. Other issues that received little (if any) attention at trial are probably no less pertinent to evaluating vertical mergers but no less difficult to evaluate. 7

As the practical and conceptual uncertainties noted above may sometimes be unresolvable when conducting ex ante vertical merger evaluations, this paper takes a different approach to assessing the potential competitive effects of the proposed AT&T/Time Warner merger. Specifically, it considers the reactions of the stock market prices pertaining to Time Warner’s upstream competitors and AT&T’s downstream (MVPD) rivals at the time when news of the proposed transaction was made public. This event study methodology has the distinct advantage of measuring “direct effects” on competitors’ equity valuations that do not require the researcher to quantify the (possibly many) individual effects stemming from a vertical merger that might raise or lower prices, nor the various inputs needed to assess those separate effects. The stock market reactions of the merging firms’ rivals can and on average will reflect the overall or net impact of the various counterbalancing effects determining the consequences of a vertical merger on competition. Event studies may thus provide for clearer inferences of the proposed transaction’s likely competitive effects when certain conditions (discussed further herein) are satisfied.

The paper proceeds as follows. Section II provides a broad overview of the potential procompetitive and anticompetitive theories of harm applicable to vertical mergers and the implications for those theories on the stock price reactions of rivals competing in the upstream and downstream segments. Section III outlines the event study methodology and the data used to implement that analysis, while Section IV presents the empirical results. Section V discusses alternative explanations besides anticipated partial foreclosure effects that might rationalize the estimated returns patters, explanations that are found to be unavailing. Section VI then presents several robustness checks that support the earlier inferences. Finally, Section VII concludes.

II. What Stock Market Returns Imply about the Competitive Effects of Vertical Mergers

A. Inferring Competitive Effects from Abnormal Stock Returns

There are several event studies examining whether horizontal mergers are likely to be procompetitive or anticompetitive. 8 Examining whether horizontal mergers are procompetitive or anticompetitive is relatively straightforward. In either case, the merged firms’ stock price should be expected to increase, with the rivals’ stock prices mattering to the conclusion. An anticompetitive horizontal merger would increase the present discounted value of cash flows and therefore the stock prices of rivals. Conversely, transactions that generate efficiencies internalized by the merging parties would lower the returns of rivals.

Event studies that examine vertical mergers are far less common, perhaps because the returns of rivals are less indicative of the procompetitive or anticompetitive nature of a deal. 9 The challenge is that both procompetitive and anticompetitive vertical mergers can benefit the merging firm but harm the rivals. As an example, suppose that a downstream firm acquires an upstream input supplier. In a possible anticompetitive scenario, the merged firm subsequently raises the price of a critical input it supplies to its downstream rivals. The expected profits and thus stock returns of the downstream rivals would then fall since they would be paying higher input prices. 10 In a pro-competitive scenario, the merger would lower the merged firm’s marginal costs (e.g., through the elimination of double marginalization (“EDM”)), which would also reduce the profits and stock returns of the downstream rivals, since they would face a more formidable competitor and have to lower prices. That is, observing a negative pattern in downstream rivals’ returns is consistent with both anticompetitive and procompetitive scenarios.

There are two ways that event studies might provide inferences in vertical mergers given this complication. First, an anticompetitive merger should raise downstream prices, whereas a procompetitive merger should lower them. Both of those outcomes would have obvious implications for the stock prices of (publicly traded) firms that buy the downstream products, and as such, those same effects would provide an indication of the merger’s expected impact on downstream competition. However, this method of inference does not apply here since consumers rather than firms buy from the downstream MVPDs.

Second, to the extent that the merger would result in no or otherwise modest EDM effects or other efficiencies, a decrease in the equity prices of downstream firms competing against the merging parties would tend to reflect foreclosure expectations. 11 In the next sections, we first argue that efficiencies are not likely to be passed on in this merger, and therefore any decrease in the equity prices of MVPD rivals would likely reflect foreclosure effects. 12 Then, we present various theories of competitive effects that may result from vertical mergers and what we would expect the signs of upstream, downstream, and advertising rivals to be under each theory. 13

B. Why Efficiencies Are Not Likely to be Passed on in the MVPD Industry

1 . EDM Efficiencies Were Likely Already Contracted

Neither the U.S. Federal Communications Commission (“FCC”) nor DOJ credited most of the efficiency claims (including those related to EDM) raised by the parties in the earlier and similar Comcast/NBCU merger. 14 With regard to EDM in particular, the DOJ concluded that extant supply contracts between them already allowed most of the associated efficiency effect to be realized premerger. It also appears that the premerger contracts between AT&T and Time Warner also resulted in some, though perhaps not complete, EDM. For example, the government’s expert concluded that the terms governing Time Warner’s provision of “Turner” content to MVPDs “[did] not appear to incentivize [DirecTV] to set its price to maximize the joint profits of Turner and [DirecTV].” 15 However, the premerger negotiated contract between Home Box Office (“HBO”) and DirecTV was based on a two-part tariff, 16 and as such, may have precluded realization of most or all the associated EDM benefits that would otherwise be realized by combining Time Warner with AT&T/DirecTV.

2. The Industry Is Not Conducive to Passing on Efficiencies

Even if there were EDM efficiencies here, we might not expect the vertically integrated firm to pass them on, as highlighted by William P. Rogerson.

17

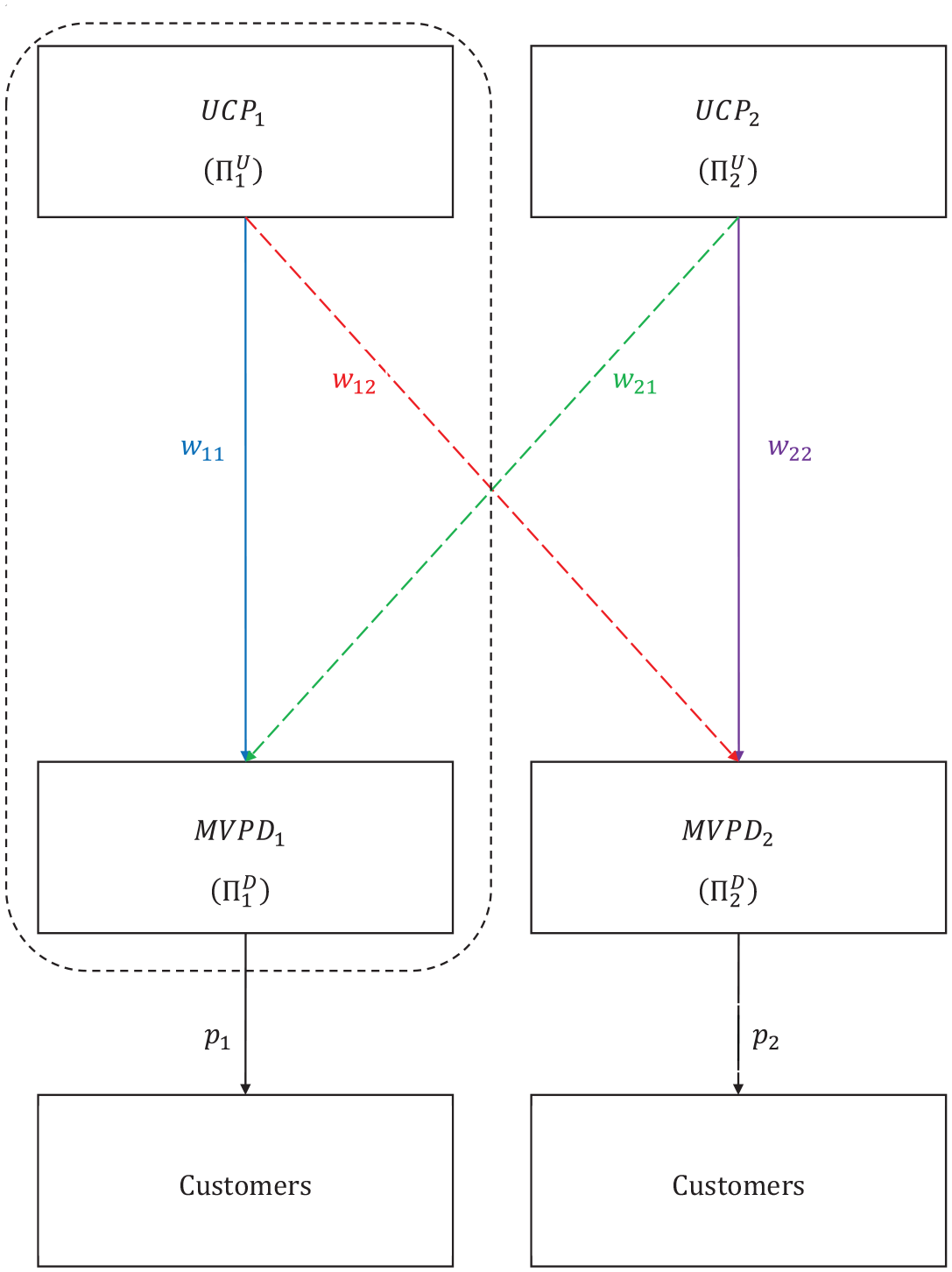

To help frame this argument, consider Figure 1. The figure shows two rival upstream content providers (“UCPs”) who supply television content (channels) to two MVPDs competing in some downstream local distribution market. Both MVPDs purchase programming content from both UCPs, that is, subscribers demand linear programming content (i.e., “channels” or “networks,” which are themselves aggregations of video content) provided by both upstream firms. Assume that

Vertical merger between MVPD and UCP.

The variable

Now consider the standard argument for how a vertical merger can be efficient even if it reduces the profit of downstream rivals. Following Rogerson,

18

assume that both UCPs hold their carriage fees constant postmerger (i.e., abstract from any possible foreclosure effects). Note that the vertically integrated provider (VIP) will not view

We would expect

Contrary to the standard argument, the reason why we might not expect efficiencies to be passed on in this industry is as follows. As emphasized by Rogerson,

20

the above scenario fails to account for two important institutional characteristics of the pay-TV industry: (1) almost all households subscribe to some form of MVPD service; and (2) MVPDs (particularly “traditional” ones) often carry programming content from each upstream content provider. That is, the upstream firm stands to gain little in terms of new business by lowering price. In the context of Figure 1, if some new subscribers to

The upstream profits

C. Vertical Theories and Their Expected Pattern of Returns

1. Foreclosure of Critical Upstream Inputs to Unaffiliated Downstream Firms

A VIP may have the ability and incentive postmerger to restrict or otherwise make more costly (i.e., “foreclose”) the inputs that it provides to its unaffiliated downstream rivals relative to the premerger situation. Such strategies would tend to increase the (quality-adjusted) relative price of the downstream rivals’ retail offerings, thereby causing their customers to substitute toward the VIP’s downstream affiliate. In the extreme case, the VIP simply refuses to sell inputs to unaffiliated downstream rivals altogether, so-called total foreclosure. This foreclosure strategy is potentially quite costly as it forces the VIP to forgo all of the profits associated with supplying the input to its downstream rivals.

A VIP might instead adopt relatively less costly partial foreclosure strategies. In the present context, a partial foreclosure strategy will refer to any effort by the VIP to raise the input price and/or degrade the quality of the input(s) sold to unaffiliated downstream firms. If, in the context of Figure 1, all prices are expressed implicitly in quality-adjusted terms, a partial foreclosure strategy corresponds to an increase in

If equity markets anticipate that the VIP will successfully implement an input foreclosure strategy postmerger, then one would expect

2. Foreclosure of the Affiliated Downstream Firm to Rival Upstream Input Suppliers

Vertical mergers may also result in the downstream affiliate of the merged firm forgoing the purchase of inputs that it acquired (or could have acquired) from unaffiliated upstream firms premerger (i.e., so-called customer foreclosure). To illustrate in the context of Figure 1,

The DOJ’s affirmative case did not allege that the proposed merger would lead to softened competition upstream or downstream via customer foreclosure effects. But customer foreclosure concerns have been raised in previous reviews of vertical mergers between content providers and distributors. 27 We therefore consider this theory of harm as a potential consequence of AT&T’s acquisition of Time Warner.

3. Facilitation of Collusion in the Upstream or Downstream Segments

Vertical mergers may facilitate collusion or other forms of coordinated behavior in the upstream

28

or downstream

29

segments through acquisition of a maverick or disruptive downstream firm that (premerger) helped to deter collusion in the relevant segment. For example, upstream collusion may result from a wholesaler vertically integrating with a retailer or distributor that holds a relatively large market share in the downstream segment if that share is indicative of buyer power.

30

The anticipation of sustainable upstream collusion via the acquisition of such a downstream firm would, of course, be exemplified by

In a similar vein, downstream collusion may be easier to sustain postmerger if a VIP can weaken a rival downstream maverick by totally foreclosing its access to the input or raising the input’s price. Such behavior might imply a negative price reaction for the rival downstream maverick but positive reactions for all other downstream firms. The impact on upstream rivals could be negative assuming the effect of the downstream collusion is to decrease aggregate retail demand and thus the derived demand for the upstream inputs. 32 Another possibility is that the VIP threatens is rival upstream competitors with customer foreclosure (i.e., to the integrated downstream affiliate) if they do not (also) increase their input prices to the rival downstream maverick. 33 If downstream collusion is successfully implemented using this strategy, one would expect a positive price reaction for rival downstream firms (save perhaps for the maverick) and a negative price reaction for rival upstream firms.

In the present context, there was little evidence that any of the rival UCPs or MVPDs competed as a maverick against AT&T or Time Warner. Again, while vMVPDs frequently offered lower-priced alternatives relative to traditional MVPD service, they did so primarily by offering smaller bundles of video content. As discussed below, the coordinated effects theory of harm advanced by the DOJ relied instead on a structural argument that vertically integrated providers would more easily reach and maintain a collusive agreement.

4. Facilitation of Collusion among Vertically Integrated Suppliers

The ability of rival firms to reach and sustain a collusive agreement is likely mitigated to the extent they are not similarly “situated” as competitors. For example, differences across firms measured in terms of product portfolios; technology (cost structure); capacity; demand conditions; buyer characteristics; market shares; and so on will generally work to make reaching, monitoring, and punishing defections from the collusive agreement more difficult, thereby reducing the likelihood and/or extent of collusive behavior. 34 Vertical mergers or vertical contractual integrations might be mechanisms by which rival firms can make themselves more symmetric, and there could be a concern that the acquisition of Time Warner by AT&T might facilitate coordination between the merged entity and other similar, integrated firms. Indeed, the DOJ alleged that: “[T]he merger would facilitate coordination between AT&T and Comcast . . . the only major vertically integrated distributors.” 35 This coordination would allegedly target virtual MVPDs (vMVPDs) in order to slow or their growth or deter their entry as a competitive alternative to traditional (“facilities-based”) MVPD service.

The DOJ argued that Time Warner and NBCU programming constituted “two of the most important network groups for Virtual MVPDs.”

36

If vMVPDs, therefore, were (totally) foreclosed from accessing that content, their preferred business model (i.e., offering so-called “skinny bundles” at a lower price point relative to traditional MVPD service) could not be implemented, thereby limiting their potential to serve as disruptive entrants. The DOJ also argued that market conditions were conducive to facilitating such coordination against vMVPDs to the benefit of traditional MVPDs.

37

To the extent that the hypothetical merger in Figure 1 facilitates such coordination, one would expect

The defendants pointed to an important structural asymmetry between AT&T and Comcast that would persist postmerger and potentially limit their ability and incentive to reach and sustain a collusive agreement. AT&T is one of the largest wireless telephony and data providers in the United States, whereas Comcast holds only a de minimis wireless position. AT&T argued that it possesses strong incentives to maximize usage of its wireless broadband network. Withholding Time Warner content to those vMVPDs whose offerings are accessed through AT&T wireless handsets would clearly make it more difficult to achieve that objective. Moreover, as wireless devices grow in their tendency to be the primary medium through which subscribers access media, AT&T’s incentives to supply rival vMVPDs could grow even stronger. AT&T also claimed that it wanted “Turner content to be included in this growing sector of the video ecosystem . . . to encourage consumers to continue to use network-based distribution options rather than turning to Netflix and similar alternatives.” 38

5. A Procompetitive Theory of Increased Advertising Competition

AT&T and Time Warner placed great emphasis on the potential for their combination to generate revenue synergies, especially those related to the provision of online/digital advertisements. More specifically, they claimed the merged firm would obtain the ability to develop new targeted advertising platforms by combining information on DirecTV’s customers’ viewing patterns with Time Warner’s. These platforms would allegedly benefit both digital advertising purchasers (who could better tailor ads to specific customers) and pay-TV customers (who would receive fewer superfluous ads). The defendants also argued that they would increase competition in the digital advertising space by introducing a new competitor to incumbents (in particular, Facebook and Google) while also creating a new profit center for the merged entity. 39

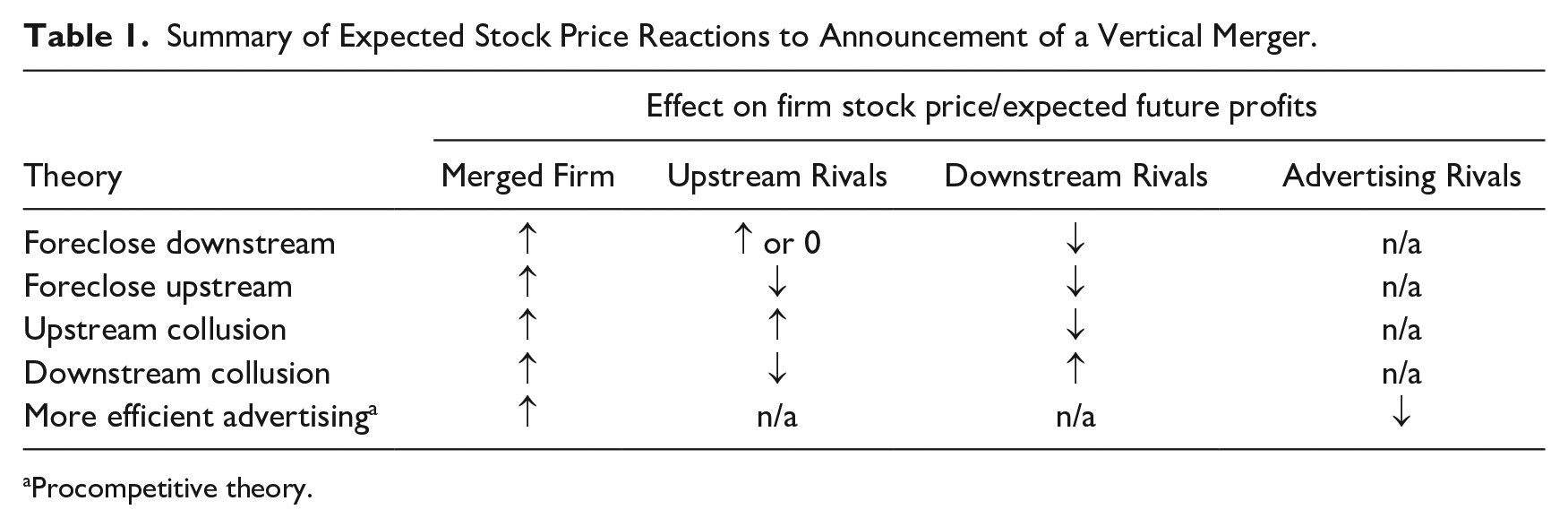

6. Summary of Expected Stock Market Returns across Posed Vertical Theories

Table 1 summarizes the expected stock market reactions for each of the vertical theories posited in this section.

Summary of Expected Stock Price Reactions to Announcement of a Vertical Merger.

Procompetitive theory.

III. Data and Event Study Methodology

We estimate a standard event study that measures the abnormal returns of potentially affected stocks. The literature defines the abnormal return of a security as the return in excess of what would be expected from some pricing model. 40 In our case, we use the capital asset pricing model (“CAPM”).

Our general approach to drawing inferences proceeds in two parts. First, we calculate the daily abnormal returns for each security separately around the date of the proposed merger’s announcement. Second, we reduce the noisiness in the individual daily abnormal returns by applying the portfolio method of Jeffrey Jaffe 41 as a robustness check on the results obtained from the individual securities. 42 That is, we look at the daily abnormal returns for certain portfolios of securities, where each portfolio is the simple average return for related companies. As markets may not respond instantaneously to new information (including merger announcements), we examine the abnormal returns over several days after the event day. We also consider cumulative abnormal returns over several days.

The estimation method for the first method (i.e., at the individual security level) is as follows. Let

We estimate

The cumulative average abnormal return after the announcement is given by

where

The portfolio method averages the securities in group

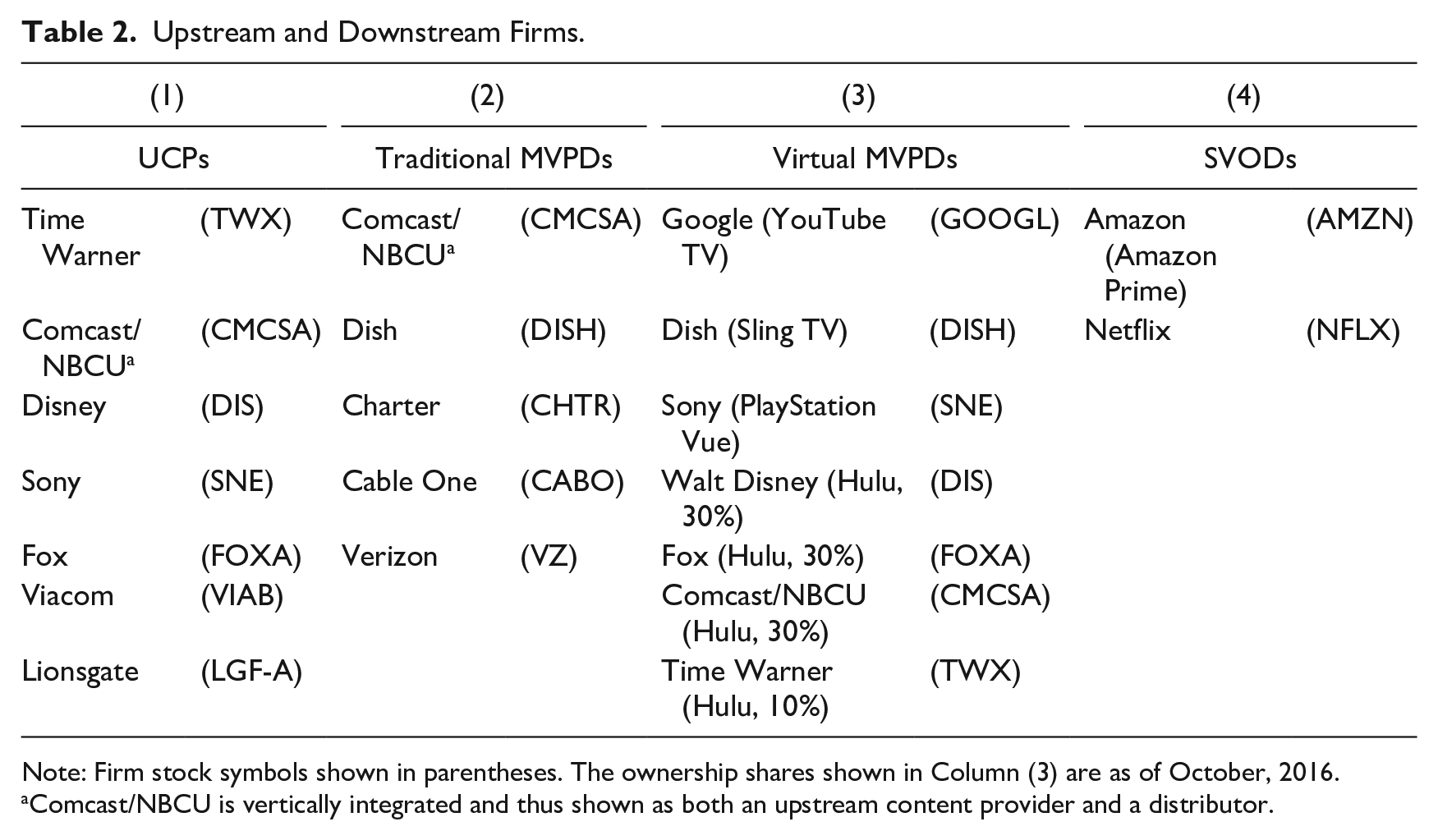

Table 2 summarizes the various publicly traded companies considered in the event study analysis and their ownership structures as of the date of the AT&T/Time Warner merger announcement. These entities are grouped according to whether they are (1) an upstream content provider; (2) a traditional MVPD (which includes satellite-based distributors); (3) a vMVPD; and/or (4) a subscription video on demand (“SVOD”) provider. Note that these classifications are not always mutually exclusive. For example, DISH operates both as a (traditional) satellite-based MVPD and as a vMVPD (through Sling TV). Sony is both an upstream content provider and a vMVPD (through its “PlayStation Vue” offering). Hulu, a vMVPD, is a joint venture between Disney, Comcast/NBCU, Time Warner, and Fox. Where applicable, Table 2 also reports the ownership share of each entity in such joint ventures (e.g., Disney owns 30 percent of Hulu) at the time of the proposed acquisition. Despite the fact that some firms are involved with more than one category, in most (if not all) instances the size of a given entity’s primary line of business is appreciably larger than that associated with any ancillary video distribution activity. Thus, one might expect any abnormal returns accruing to, say, Disney to be more reflective of its position as a major upstream content provider rather than its comparatively small position as a vMVPD (i.e., through its partial ownership share of Hulu).

Upstream and Downstream Firms.

Note: Firm stock symbols shown in parentheses. The ownership shares shown in Column (3) are as of October, 2016.

Comcast/NBCU is vertically integrated and thus shown as both an upstream content provider and a distributor.

IV. Results

Media reports mentioning AT&T’s intention to acquire Time Warner were leaked to the press and first published on Thursday, October 20, 2016. These initial reports, however, were somewhat tentative in their coverage, with an article by Ed Hammond, Alex Sherman, and Scott Moritz 44 serving as the basis for most. A substantially larger number of more definitive reports were published the following day, October 21, 2016. 45 The official announcement by the parties of their intention to merger was made on October 22, 2016.

Given the aforementioned events, the ensuing discussion treats October 20, 2016 as the “effective” announcement date of the proposed merger and focuses on it and the following day to assess the impacts of the merger’s announcement on the stock returns of upstream and downstream rivals. Let

A. Traditional MVPDs

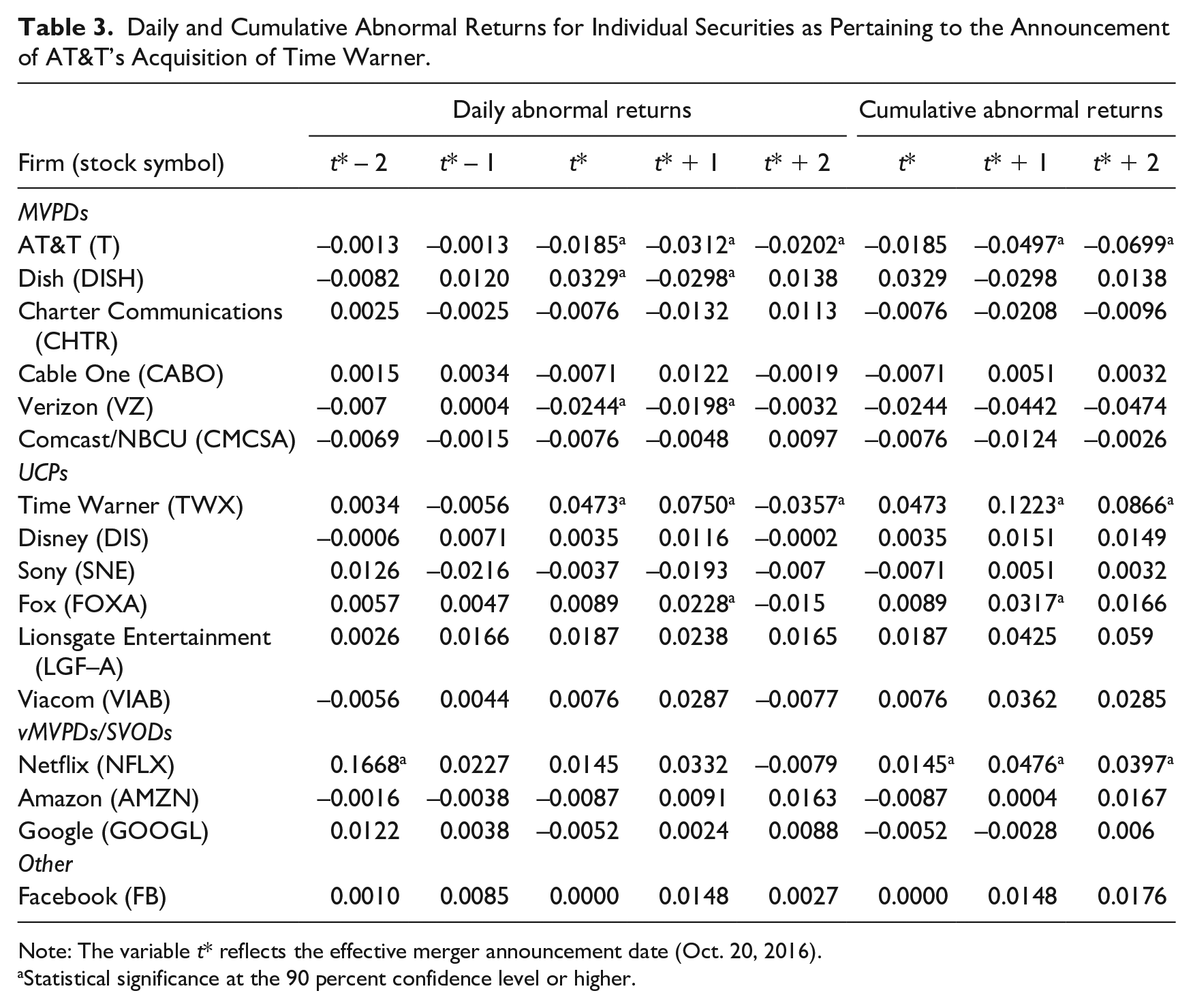

Table 3 presents the results of estimating the aforementioned daily and cumulative abnormal returns. First consider the pattern of daily abnormal returns accruing to the rival MVPDs.

Daily and Cumulative Abnormal Returns for Individual Securities as Pertaining to the Announcement of AT&T’s Acquisition of Time Warner.

Note: The variable t* reflects the effective merger announcement date (Oct. 20, 2016).

Statistical significance at the 90 percent confidence level or higher.

The abnormal returns for Verizon right after the announcement are negative and statistically significant on both

Charter, a cable-based MVPD, also experienced negative daily abnormal returns for days

Another cable-based distributor, Cable One, experienced a positive daily abnormal return on date

Finally, the largest cable-based MVPD, Comcast, experienced an appreciable drop in its estimated daily abnormal return between days

The preponderance of the negative estimated abnormal returns for Comcast does not support the DOJ’s theory that the proposed merger would lead to a successful (tacitly) collusive postmerger agreement between Comcast and AT&T. Moreover, the mixed evidence suggesting an adverse impact on Comcast’s future profitability (presumably via future partial foreclosure) may reflect the firm’s position as a vertically integrated content provider/distributor, which might in turn impose offsetting impacts on the firm’s expected performance. As discussed below, it appears that the announcement of the proposed merger had positive effects on the abnormal returns realized by Time Warner’s upstream rivals. Comcast’s pattern of returns might therefore reflect the combined expectations of a decease (i.e., through higher postmerger carriage fees paid for Time Warner content) and increase (i.e., due to owning and operating NBCU) in its future cash flow. Put differently, the firm’s upstream operations might temper any harm its downstream MVPD operations might suffer due to paying higher postmerger carriage fees to AT&T.

Finally, we look at Dish, which according to trial testimony was likely DirecTV’s closest rival. Contrary to expectations, the day-of-announcement (i.e.,

This ambiguous pattern might be explained by DirecTV’s announcement on October 19, 2016 (i.e., at

In that sense, equity markets might have viewed this announcement as an indication that DirecTV was repositioning its business away from traditional satellite service in favor of a vMVPD internet platform, thereby weakening the competitive constraint exerted on Dish. The problem with this explanation is that the other MVPDs discussed above did tend to experience a drop in equity prices, which seems inconsistent with an expected softening of downstream competition. Moreover, since Sling is a vMVPD owned by Dish, one could argue that DirecTV was becoming more of a competitor for Dish as a result of introducing DirecTV Now.

There may be other explanations for the positive daily abnormal return realized by Dish on the day of announcement. First, Dish’s Sling TV offering at the time was rather differentiated from DirecTV’s anticipated vMVPD offering; that is, DirecTV Now was not (initially) envisioned as a low-priced or “skinny” bundle of content, whereas Sling TV was. Second, the market may have viewed Direct TV’s announcement of providing a vMVPD service as giving credibility to the vMVPD strategy, which could benefit Dish. Overall, all these factors might have been hard for the market to immediately digest, perhaps explaining a two-day delay between the announcement and Dish’s negative

B. vMVPDs/SVODs

Now consider the non-traditional video distributors. Again, the fact that all of the vMVPD providers in the sample are themselves owned and operated by large firms operating primarily in some other line of business makes it difficult (if not impossible) to ascribe any change in their estimated abnormal returns specifically to their vMVPD operations. Rather, any estimated changes are more likely than not to reflect some effect on their primary line of business operations. Google, for example, operates as a vMVPD through its YouTube TV service, but the revenues associated with that offering pale in comparison to those generated from selling online advertisements. This latter fact provides a rationale to evaluate Google’s abnormal returns nonetheless (recall that the parties argued that the merger would allow them to enter the online advertising space through the development of new targeted advertising platforms). 54

If consummation of the proposed merger would in fact make AT&T a stronger competitor against Google for online advertising dollars, one would expect Google to realize a negative abnormal return on or immediately after the effective announcement date. While Google’s estimated abnormal return at

AT&T and Time Warner also alleged that the merged entity would compete more effectively against content-integrated SVODs postmerger. More specifically, the parties claimed that Time Warner could also use AT&T’s subscriber data to produce content that was better aligned with subscriber viewing habits, an advantage that content-integrated SVODs like Amazon and Netflix already possessed. 55 Another potential impact of the proposed transaction on SVODs involves input quality degradation. Some commenters alleged that AT&T—through its role as a supplier of both high-speed broadband and Internet backbone services—could engage in partial foreclosure by deteriorating the quality of streaming service provided to Amazon and Netflix (and possibly vMVPDs as well). 56 In response, customers of those SVODs might be incentivized to substitute toward DirecTV’s or AT&T’s pay-TV offerings, thereby increasing the latter firms’ profitability at the expense of SVODs. Again, to the extent that such non-price discrimination was expected to arise postmerger, Netflix and Amazon would realize a negative abnormal return on or after the effective announcement date (all else equal).

Contrary to the latter hypothesis, Table 3 shows that Netflix’s estimated daily abnormal return is positive on both

Evaluating Facebook’s pattern of abnormal returns provides further evidence that the merged entity was unlikely to become (or at least not expected to become) a disruptive competitor in the online advertising space. As shown at the bottom of Table 3, Facebook’s estimated daily abnormal return at

C. UCPs

Now consider the estimated daily abnormal returns for Time Warner and its upstream competitors reported in Table 3. Four of these five entities realized positive estimated daily abnormal returns on day

As noted earlier, Comcast’s estimated abnormal return pattern likely reflects a mixture of its upstream and downstream operations. The UCP results discussed above suggest that the negative

Finally, note that the positive upstream abnormal returns discussed above are consistent with the earlier inferences regarding negative downstream effects via postmerger partial foreclosure of Time Warner content to rival MVPDs. Janusz A. Ordover, Garth Saloner, and Steven C. Salop (“OSS”) have shown that vertical foreclosure can arise in equilibrium under oligopolistic price-setting (Bertrand) behavior in both the upstream and downstream segments. 60 OSS also find (relative to the premerger equilibrium) that vertical foreclosure generally leads to lower equilibrium profits for downstream rivals but higher equilibrium profits upstream—i.e., higher profits for both the upstream division of the VIP and its upstream rival. 61

The same intuition driving those results applies in the present case. UCPs are effectively price-setting firms competing in differentiated products (where prices are the carriage fees assessed to downstream MVPDs and the variable fees assessed to advertisers). Assume that a vertical merger between one of the UCPs and one of the MVPDs leads the merged entity to partially foreclose its downstream rivals by raising the price of the content it supplies to them. This increase in the integrated firm’s input price causes rival UCPs to unilaterally increase their carriage fees in response since prices are strategic complements in differentiated Bertrand competition. In other words, the unaffiliated UCPs partially accommodate the merged firm’s input price increase (even if they do not fully match that increase). 62 The input price increases imposed by the outside UCPs then cause the profits of the MVPDs to fall even further, thus enhancing the downstream impacts of the merged firm’s partial foreclosure strategy. The divergent foreclosure effects on the respective equilibrium profits realized by upstream vs. downstream firms discovered by OSS are thus consistent with the respective abnormal return patterns reported in Table 3.

D. Economic Significance of Estimated Effects

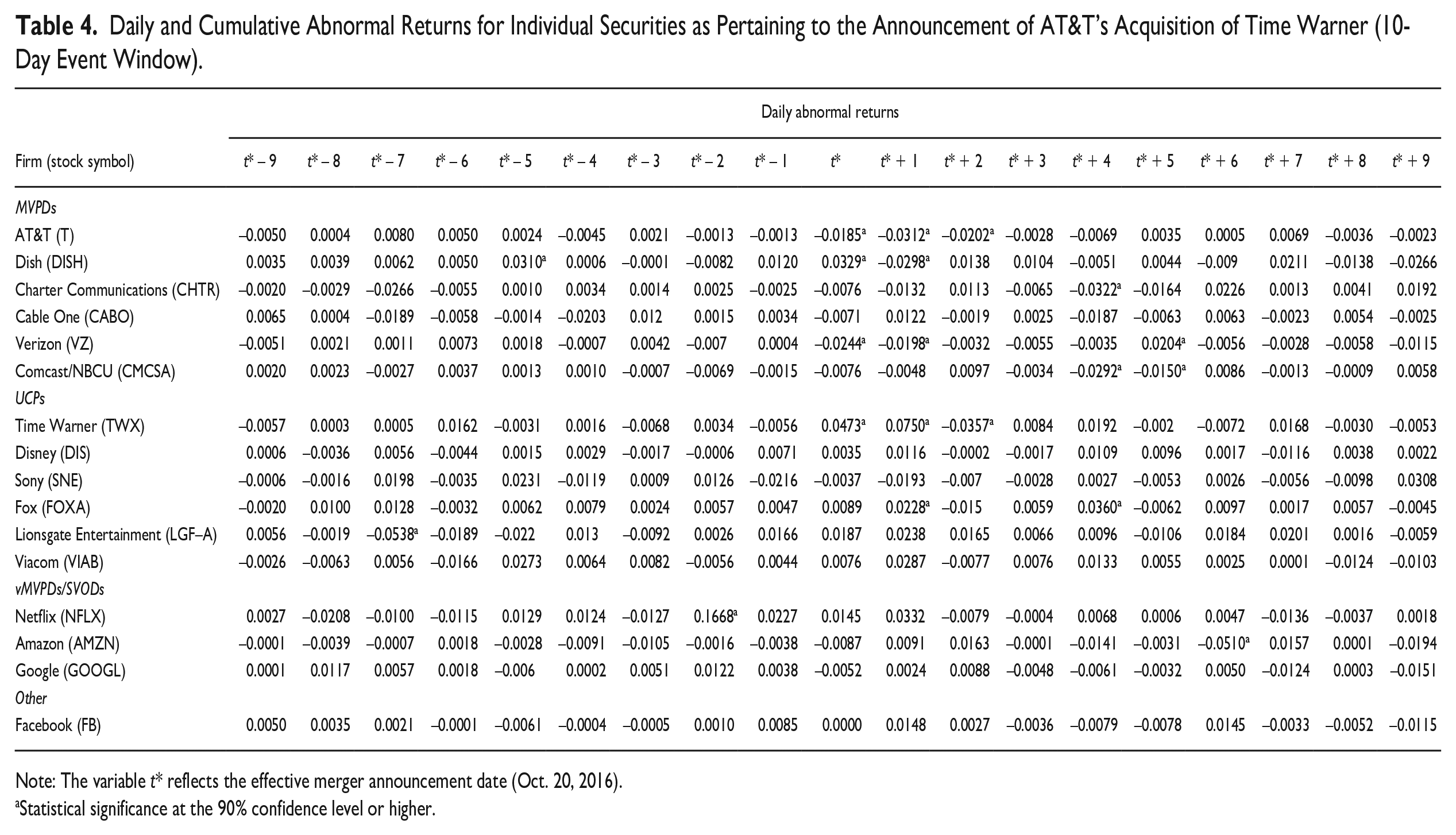

Table 4 presents results from an analogous event study model but using a ten-day event window. This is a way to examine the economic significance of the measured abnormal returns as a longer event window does not change the values of the estimated abnormal returns on days

Daily and Cumulative Abnormal Returns for Individual Securities as Pertaining to the Announcement of AT&T’s Acquisition of Time Warner (10-Day Event Window).

Note: The variable t* reflects the effective merger announcement date (Oct. 20, 2016).

Statistical significance at the 90% confidence level or higher.

The results in Table 4 demonstrate such a pattern. Consider, for example, the median (absolute) return taken across the five

V. Alternative Hypotheses

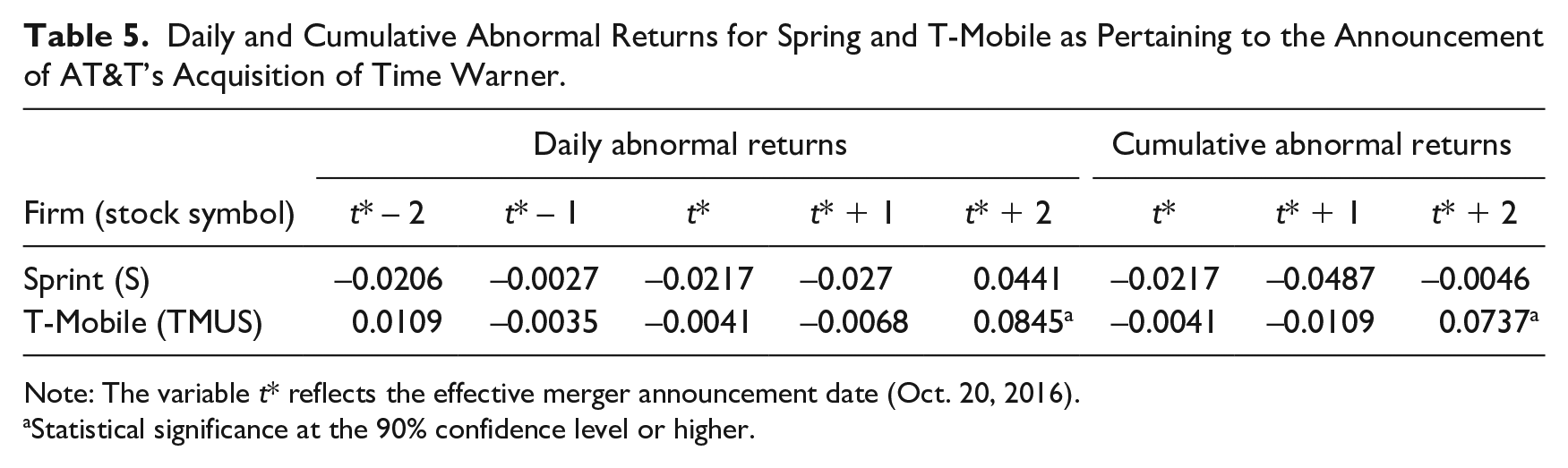

We now consider other possible explanations for some of the abnormal returns patterns discussed previously. Recall that Verizon experienced negative daily abnormal returns on the effective announcement date and on the day after. Rather than indicating anticipated foreclosure effects, one might conjecture that these results are ascribable to (1) Verizon’s position (similar to AT&T’s) as a major provider in the growing U.S. mobile telephony industry; and/or (2) certain efficiencies generated by the proposed merger expected to affect that position.

As discussed earlier, AT&T argued that its integration with Time Warner would give it the ability to offer targeted advertising to its subscribers, including those who view Time Warner content on AT&T handsets. If some Verizon wireless subscribers who watch video content on their mobile devices prefer (or even value) such advertising, then they might view AT&T’s service as being relatively more attractive postmerger and switch to AT&T in response. 64 Verizon’s expected profitability would likely fall and AT&T’s would likely rise, all else equal, should equity markets expect the number of such switching customers to be sufficiently large.

The results in Table 3 appear inconsistent with this hypothesis. Note that AT&T realized a negative and statistically significant daily abnormal return at date

We consider a falsification test to further explore this issue. Suppose AT&T’s future targeted advertising platforms would increase the perceived value (or profitability) of its own wireless (and possibly other) offerings. Verizon and all other unaffiliated wireless carriers should then experience negative abnormal returns on or just after the effective announcement date. If only Verizon is affected in this manner, then it is less likely that its negative returns reflect anticipated output expansion by the merged entity (i.e., as resulting from efficiency or synergy effects) relative to anticipated foreclosure effects (i.e., from paying higher prices for Time Warner content postmerger).

We implement the above test by considering the stock market reactions of the other major U.S. wireless carriers, T-Mobile and Sprint, to the (effective) announcement of AT&T’s intention to acquire Time Warner. As shown in Table 5, while T-Mobile (respectively, Sprint) experienced a negative daily abnormal return on

Daily and Cumulative Abnormal Returns for Spring and T-Mobile as Pertaining to the Announcement of AT&T’s Acquisition of Time Warner.

Note: The variable t* reflects the effective merger announcement date (Oct. 20, 2016).

Statistical significance at the 90% confidence level or higher.

Recall that the positive estimated returns at

Several strands of qualitative evidence cut against this possibility. There was little consensus among financial analysts and industry executives as to whether the proposed merger (when it was publicly announced) would lead to any further consolidations among media providers. For example, Ben Levisohn 66 cites to a Bernstein analyst report stating: “Some believe [the proposed acquisition of Time Warner by AT&T] will stimulate more M&A. We doubt it because we don’t see the buyers (where were the competitive bids for Time Warner?) and we don’t see the industrial logic.”

Similarly, Ryan Faughnider and Meg James characterize Wall Street’s reception to the proposed deal as ambivalent, a reception they further portray as “illustrating sharply divergent views on whether the blockbuster deal will usher in a new era of media consolidation” while also noting that “[a]nalysts were split on whether AT&T’s move would spur other companies to combine.” 67 Brooks Barnes and Emily Steel report a similar reaction among senior entertainment executives, leading them to answer the question “Will a line of major media consolidation dominoes—involving titans like Disney, Fox and Comcast—begin to fall?” with the response “Not likely.” 68 And according to an RBC Capital Markets report: “If content companies are key acquisition targets, then [Time Warner] is unique in being both heavily focused on owned content and . . . a single-class equity share structure that has no financial considerations.” 69 In other words, Time Warner may have been a distinctively attractive target relative to rival UCPs, implying that there may have been no effective “acquisition demand” for the latter firms at the time of the proposed transaction’s (effective) announcement.

Other organizational or financial characteristics specific to those UCPs other than Time Warner likely limited their attractiveness to potential buyers. Disney, with a market capitalization of almost US$150 billion, was likely too costly a target for most other media providers, save perhaps for Amazon and Google. 70 Moreover, according to Barnes and Steel: “Disney, which has a singular corporate culture . . . has made it clear that it sees itself as the predator and not the prey when it comes to technology related deal making.” 71

Two other unaffiliated UCPs, Fox and Viacom, were effectively owned and controlled by respective private families that held a majority of their outstanding equity shares. Some commentators argued that those families were unlikely to sacrifice their ownership interests even in light of the proposed merger between AT&T and Time Warner. 72 Note also that Viacom was already in negotiations to reverse its split-up with CBS, a move that was viewed as occurring at the behest of Viacom’s controlling interests. According to Todd Spangler, “If they [i.e., Viacom’s familial holders] weren’t forcing the issue, both companies [i.e., Viacom and CBS] would be seen as prime M&A targets.” 73 And while Disney declared its intention to purchase Fox just two months after the official announcement of the AT&T/Time Warner merger, this ex post action does not detract from the relevant ex ante perceptions that Fox was not a viable acquisition target. 74

To the extent that announcement of the proposed merger led to any expectations of future acquisitions involving media-involved firms, those anticipated deals appear to have implicated SVODs, wireless carriers, and other types of content producers more so than Time Warner’s rivals in the upstream segment. For example, one analyst considered whether Comcast might acquire T-Mobile; another raised the possibility of Disney purchasing Netflix. 75 But given Disney’s then-recent US$1 billion purchase of another online streaming company (BamTech), even the latter possibility was tenuous. 76 Finally, Cynthia Littleton and Todd Spangler conjecture that smaller content producers such as Discovery Communications and AMC Networks were more likely to become potential targets, but that same prediction was made for only one unaffiliated UCP (namely, Lionsgate). 77

In short, the qualitative evidence considered above does not suggest that announcement of the proposed merger lead equity markets to regard the unaffiliated UCPs are more attractive acquisition targets. A comparison of the abnormal returns patterns across those entities supports this conclusion. Recall that the estimated announcement effects for Lionsgate were appreciably smaller than they were for the other unaffiliated UCPs. These findings may reflect the fact that Lionsgate, while being a major producer of one-off television series and movies, is less geared toward the provisioning of linear programming channels (or networks) to MVPDs (thereby earning revenues through negotiated carriage fees), at least when compared with Disney, Fox, or Viacom. Lionsgate’s operations in the latter regard are largely confined to its “STARZ” networks, which consist of a series of premium channels similar to HBO or Showtime in their programming focus. Accordingly, relative to Lionsgate, one would expect any increase in postmerger carriage fees to have a proportionately greater (positive) impact on the future profitability of Disney, Fox, and Viacom. The results in Table 3 are consistent with this hypothesis.

Still other alternative explanations for the estimated return patterns presented herein may be antipodal to our conclusions regarding anticipated foreclosure effects. One might argue, for example, that the various direct and indirect relationships between advertisers, content providers, distributors, and subscribers may permit vertical mergers in the pay-TV industry to achieve any number of other efficiencies/synergies beyond those considered so far. Examples include reducing transactions costs; internalizing indirect network externalities; mitigating moral hazard effects; and facilitating knowledge transfers, all of which might lead to lower relative prices being assessed by the merged entity and/or its provisioning of new and improved products. AT&T’s downstream rivals would likely lose customers to DirecTV/U-verse as a result of these effects, but that outcome, of course, would be procompetitive. The question, then, is whether the latter efficiency-based explanations are more likely to explain the pattern of results relative to our inferences of anticipated foreclosure effects. The answer is “No.”

As a threshold matter, given the historical significance and controversy surrounding AT&T/Time Warner, the defendants clearly had strong incentives to advance any plausibly cognizable efficiencies that would flow from the transaction as justification for allowing the merger. But even a cursory examination of litigant’s filings and trial transcripts readily demonstrates that the parties’ efficiency arguments are almost exclusively confined to the advertising-related revenue synergies noted above and a handful of “routine” assertions (e.g., eliminating redundant business functions, achieving scale economies in procurement, etc.). As there is no evidence that incumbent online advertising suppliers would be adversely affected by the merger, it is highly unlikely that those same revenue synergies could then explain the negative returns accruing to traditional MVPDs (who would be less directly affected). Accordingly, the latter results would need to be justified in terms of various efficiencies/synergies for which neither the parties nor the government (in terms of preemptive argument) ever raised in making their respective cases. A more likely explanation for this absence of argument, of course, is simply that neither party regarded such efficiencies/synergies to result from the proposed transaction.

VI. Robustness Checks

This section considers the robustness of our inferences regarding anticipated foreclosure effects with regard to (1) abnormal returns on portfolios of related media securities and (2) the announcement of AT&T’s commitment to enter into binding arbitration to resolve carriage fee disputes with MVPDs.

A. Portfolios of Securities

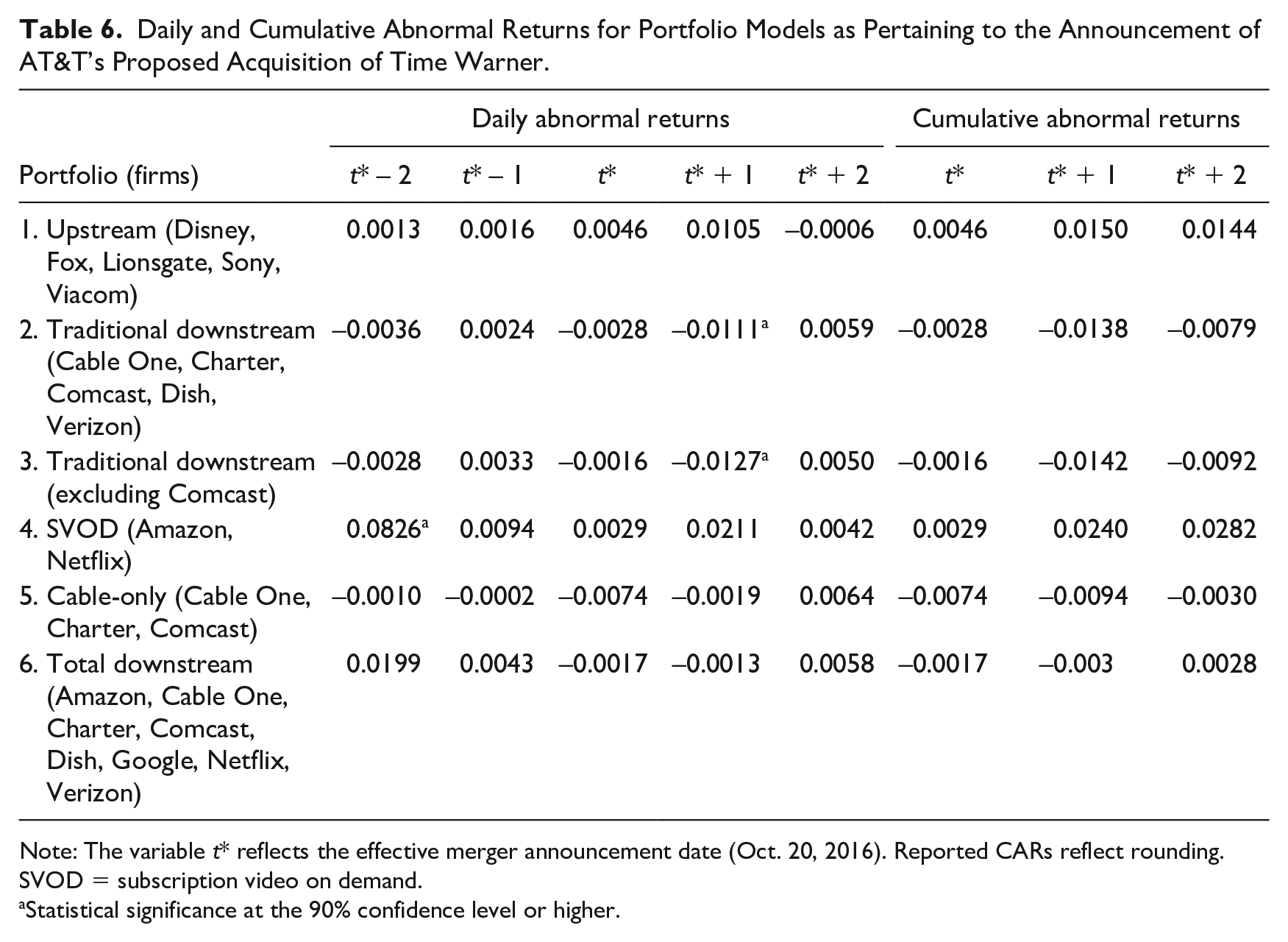

The magnitude and/or precision of the firm-specific results presented in the previous section may be affected by either idiosyncratic, firm-specific shocks that bias a given entity’s estimated abnormal return pattern (e.g., the potentially confounding influence of DirecTV’s announced vMVPD offering on Dish’s estimated abnormal returns on the event day) or random sampling error. Combining the observed returns across firms into a “portfolio” of equities may help to alleviate such issues to the extent that idiosyncratic shocks average out across firms and/or periods. It may also be of interest to consider various aggregations of entities—in particular, downstream and upstream firms—in order to gauge the average (response) effect imparted by the (effective) announcement of the proposed merger on a particular grouping of entities.

We consider the following groupings of securities: (1) an “upstream” portfolio consisting of Disney, Sony, Fox, Lionsgate, and Viacom; (2) a “traditional downstream” portfolio consisting of Dish, Charter, Cable One, Verizon, and Comcast; (3) the same traditional downstream portfolio as in (2) but excluding Comcast (given the vertically integrated nature of that firm); (4) an “SVOD” portfolio consisting of Netflix and Amazon; and (5) a “cable-only” portfolio consisting only of Comcast, Cable One, and Charter. Finally, we also consider (6) a “total downstream” portfolio consisting of all the firms in (1) and (2) as well as Google.

As shown in Table 6, the inferences obtained from the various portfolios discussed above closely mirror those obtained from estimating the individual firms’ daily returns. With regard to the upstream portfolio, the daily abnormal return at

Daily and Cumulative Abnormal Returns for Portfolio Models as Pertaining to the Announcement of AT&T’s Proposed Acquisition of Time Warner.

Note: The variable t* reflects the effective merger announcement date (Oct. 20, 2016). Reported CARs reflect rounding. SVOD = subscription video on demand.

Statistical significance at the 90% confidence level or higher.

There is some evidence of a negative market reaction with respect to the traditional downstream portfolio on the effective announcement date. The estimated abnormal return for this group goes from 0.0024 on day

The estimated daily abnormal returns pertaining to the SVOD portfolio do not suggest any adverse impacts on the future profitability of the SVOD providers. Indeed, all of the estimated daily returns and positive. These results are also inconsistent with the defendants’ claim that the proposed merger would make AT&T’s traditional MVPD or vMVPD offerings more attractive relative to SVOD services.

The cable-only portfolio also suggests that traditional, cable-based MVPDs would be harmed by the proposed transaction. The estimated

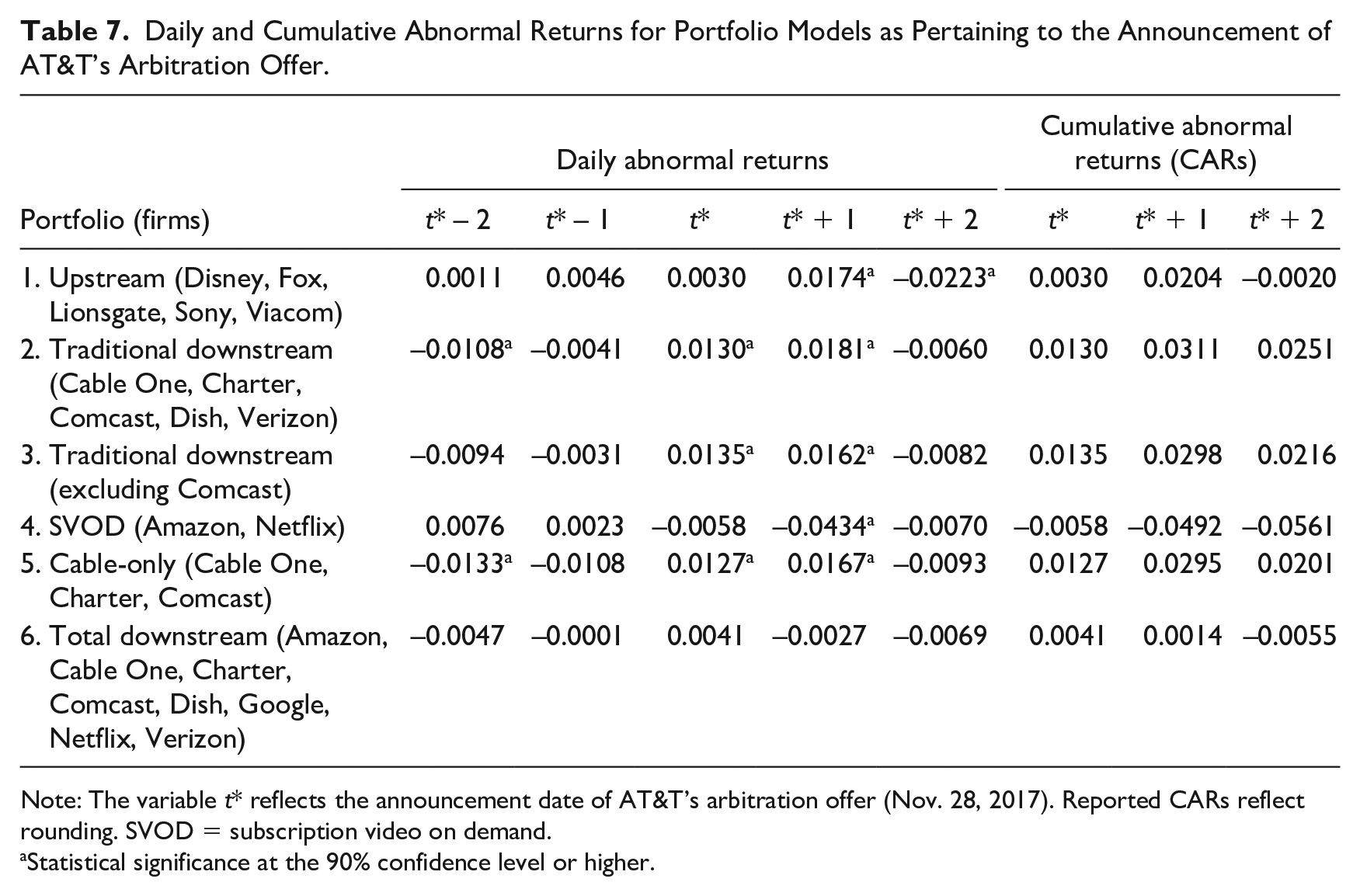

B. AT&T’s Arbitration Commitment

In late November 2017 (i.e., prior to the initiation of the district court trial), AT&T announced that it would commit to the use of binding third-party (“baseball-style” final offer) arbitration to resolve carriage fee disputes (renegotiations) with rival MVPDs. 78 A key provision of this measure was AT&T’s guarantee that it would not blackout Time Warner’s Turner programming while those arbitration proceedings were taking place. As AT&T could no longer use the threat of such blackouts as bargaining leverage for the purpose of extracting higher carriage fees from rival MVPDs, this remedy would presumably mitigate the government’s concerns regarding postmerger partial foreclosure effects.

The (unexpected) announcement of AT&T’s arbitration offer provides an important event for assessing our previous inferences regarding the anticipated foreclosure effects of the proposed transaction. 79 Given Judge Leon’s adoption of a similar remedy as a central basis for his approving the earlier Comcast/NBCU merger and the value MVPD subscribers appear to place on Turner content, it is likely that equity markets would have viewed the offer as: (1) significantly increasing the likelihood that the AT&T/Time Warner merger would be approved (or else consummated due to a settlement outcome with the government); but (2) leaving AT&T with no ability (at least in the immediate future) to withhold the Turner network stations to its downstream rivals (and thus effectively no additional bargaining leverage by which a partial foreclosure strategy for such content could be effectuated against them). Accordingly, to the extent the proposed merger was in fact expected to result in (net) efficiency effects (which are the effects that would tend to dominate as a result of the binding arbitration offer), rival MVPDs should have realized negative abnormal returns on or just after the arbitration provision’s announcement. Conversely, if—consistent with our earlier inferences—the merger (absent the arbitration commitment) was expected to result in the partial foreclosure of AT&T’s MVPD rivals, then those firms should have realized positive abnormal returns on the aforementioned dates as equity markets responded to this new information. 80

Table 7 shows the daily and cumulative abnormal returns associated with each of the portfolio models shown in Table 6 but now estimated with respect to the announcement of AT&T’s binding arbitration offer.

81

Each specification reflecting (in part) the estimated abnormal returns accruing to AT&T’s traditional downstream rivals ((2), (3), (5), and (6)) shows a positive and, in most cases, economically significant abnormal return on the arbitration announcement date (

Daily and Cumulative Abnormal Returns for Portfolio Models as Pertaining to the Announcement of AT&T’s Arbitration Offer.

Note: The variable t* reflects the announcement date of AT&T’s arbitration offer (Nov. 28, 2017). Reported CARs reflect rounding. SVOD = subscription video on demand.

Statistical significance at the 90% confidence level or higher.

Finally, while the estimated

VII. Concluding Remarks

We employ a financial event study to prospectively evaluate the potential competitive effects of the then-proposed AT&T/Time Warner merger. Models estimated on both individual firm securities and portfolios of firm securities at the upstream or downstream levels suggest that, in general, MVPDs competing downstream against AT&T incurred a reduced equity valuation at the time of the (effective) announcement of the proposed merger. Conversely, the valuations of those MVPD rivals appear to have increased with respect to the announcement of AT&T’s arbitration commitment, which also suggests that equity markets expected the merger (without imposition of a remedy) to lead to increased bargaining leverage by Time Warner and higher negotiated programming fees for its content. These and other results appear to align closely with the DOJ’s central theory of harm in challenging the proposed merger.

We find little support for the notion that the results reflect anticipated efficiency effects—whether cost-based (e.g., EDM) or otherwise—accruing to the merged entity. The results are also inconsistent with the merging parties’ assertions that their combination would enhance their ability to become a competitively significant supplier of targeted advertising platforms postmerger. Nor is there evidence that the merger was likely to increase the likelihood that AT&T and Comcast would successfully coordinate against unaffiliated (v)MVPDs.

The above inferences appear consistent with several postmerger actions taken by AT&T. For example, the company imposed an across-the-board US$10/month price increase on DirecTV Now legacy packages just two weeks after winning its appellate case 84 despite its claims that “[c]ertain merger efficiencies will begin exerting downward pressure on consumer prices almost immediately.” 85 The company also announced that it would discontinue offering those legacy packages to new subscribers and instead offer them a choice between two new packages with subscription rates starting from US$50 to US$70/month (whereas legacy packages were priced between US$40 and US$75 on a monthly basis). While those new packages included HBO, they would no longer include many other popular channels including A&E, Discovery, and Nickelodeon. 86 It is thus unclear whether this change in product mix made consumers better off on a quality-adjusted basis.

To be sure, the annually increasing costs of content incurred by MVPDs may partially explain the price increases noted above and those imposed on certain DirecTV and U-verse services following AT&T’s acquisition of Time Warner. 87 But there is also reason to believe that some of these increases might be attributable to softened downstream competition (or the anticipation thereof) following the merger. For example, Netflix’s imposition of a 13 to 18 percent increase in its monthly subscription fees in April 2019—the first price increase imposed by the company since 2017 and also the single largest increase in its history 88 —is at least consistent with the latter possibility. 89 AT&T’s price increases for its traditional pay-TV offerings also belie its earlier claims that its acquisition of Time Warner would increase competition and lead to lower customer subscription fees for those services. 90

Another notable postmerger development was AT&T’s blackout of HBO and Cinemax to Dish (arguably DirecTV’s closest competitor) that lasted from November 2018 until late July 2021. Recall that Judge Leon’s central basis for permitting the AT&T/Time Warner merger was his determination that long-term or permanent blackouts were unlikely to be regarded as credible threats in negotiations between content providers and distributors. By extension, the court concluded that long-term blackouts of popular Time Warner programming options (including the Turner channels and HBO) would rarely (if ever) occur in the course of future carriage (re)negotiations. 91 But the duration of the blackout—which was also the first blackout of HBO in its 43-year history 92 —is at least suggestive of increased bargaining power accruing to Time Warner due to its acquisition by AT&T. 93 That is, postmerger AT&T was more willing to incur the costs associated with foreclosing Time Warner programming (i.e., relative to Time Warner operating on its own) because it possessed the ability capture some of the lost sales (subscribers) realized by the targets of such outages. It appears therefore that integrated content providers-distributors can credibly threaten to blackout content even on a relatively “long term” (though perhaps not “permanent”) basis in some instances.

Finally, in a remarkable epilogue to this narrative, AT&T ultimately decided to divest both DirecTV and Time Warner. While some commenters have argued that this development indicates that the government’s theory of harm was incorrect, 94 the same could said regarding the various efficiencies and synergies that AT&T, its retained economic expert, and Judge Leon himself repeatedly pointed to as procompetitive justifications for the merger. After all, presumably a firm would not voluntarily sell off assets that result in cost savings and/or lead to new product innovations that only serve to increase profits.

But irrespective of whether foreclosure or efficiency effects would have ultimately prevailed postmerger, there is still an open question of why AT&T chose to divest the assets. One straightforward explanation may be paramount: AT&T simply made a business mistake by severely underestimating the extent of near-term household cord cutting and cord shaving. Once the likely diminishment (or slower growth) in AT&T’s carriage fees, subscriber fees, and/or advertising receipts resulting from such actions became transparent, AT&T may have no longer perceived the DirecTV/Time Warner assets as providing a sufficiently high future return on investment even assuming it could successfully implement a partial foreclosure strategy postmerger. In other words, the opportunity cost of maintaining or expanding capital in those divisions became (or was expected to become) so high that AT&T decided to reallocate its investment and refocus its efforts toward its core wireline and wireless assets.

Footnotes

Acknowledgements

We thank David Schmidt for helpful comments.

Authors’ Note

The views expressed in this article are those of the authors and do not necessarily reflect those of the U.S. Federal Trade Commission.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

1.

MVPDs distribute linear television programming, that is, content aired on specific channels at specific times. As employed herein, the term ‘traditional MVPDs’ applies to facilities-based cable (e.g., Comcast) and telecom (e.g., Verizon) companies as well as satellite-based providers (e.g., DirecTV) that supply linear pay-TV programming to consumers (end users). A virtual MVPD (e.g., Sling TV and Hulu) refers to any firm that distributes linear programming over the Internet without also providing the physical data path (be it land-, satellite-, or wireless-based) over which content is delivered to consumers. Other Internet-based distribution platforms known as ‘subscription video on demand services’ (“SVODs”) offer libraries of content that can be streamed by the consumer. As such, consumers can start watching content at the time of their choosing and are not otherwise limited by a linear programming schedule. Relatedly, subscription video on demand services do not generally offer live video programming including, for example, sports events or concerts. Examples of these distributors include Netflix and Amazon Prime.

2.

Nor was there any substantive indication that the parties intended to compete against one another by respectively integrating into the adjacent vertical segment.

3.

Articles suggesting benefits include Larry Downes, Why Mergers Like the AT&T-Time Warner Deal Should Go Through, ![]() ) Judge Leon’s ruling. Two amicus briefs filed in the appellate case and authored by a host of veteran antitrust scholars/practitioners are themselves important contributions to this post-trial discourse. Brief of 27 Antitrust Scholars as Amici Curiae in Support of Neither Party, United States v. AT&T Inc., No. 18-5214 (D.C. Cir. Aug. 21, 2018); Brief Amici Curiae of 37 Economists, Antitrust Scholars, and Former Government Antitrust Officials in Support of Appellees and Supporting Affirmance, United States v. AT&T Inc., No. 18-5214 (D.C. Cir. Sept. 26, 2018).

) Judge Leon’s ruling. Two amicus briefs filed in the appellate case and authored by a host of veteran antitrust scholars/practitioners are themselves important contributions to this post-trial discourse. Brief of 27 Antitrust Scholars as Amici Curiae in Support of Neither Party, United States v. AT&T Inc., No. 18-5214 (D.C. Cir. Aug. 21, 2018); Brief Amici Curiae of 37 Economists, Antitrust Scholars, and Former Government Antitrust Officials in Support of Appellees and Supporting Affirmance, United States v. AT&T Inc., No. 18-5214 (D.C. Cir. Sept. 26, 2018).

4.

Complaint, United States v. AT&T Inc., No. 1:17-cv-2511 (D.D.C. Nov. 20, 2017).

5.

United States v. AT&T Inc., 310 F. Supp. 3d 161 (D.D.C. 2018).

6.

The DOJ appealed the district court’s decision to the U.S. Court of Appeals for the District of Columbia. Motion of the United States to Expedite Consideration of the Appeal, United States v. AT&T Inc., No. 18-5214 (D.D.C. July 18, 2018). In February 2019 the appeals court sided with the defendants, thereby upholding Judge Leon’s decision. United States v. AT&T, Inc., 916 F.3d 1029 (D.C. Cir. 2019). The DOJ announced shortly thereafter that it would not appeal the appellate court’s decision to the U.S. Supreme Court.

7.

For instance, competitive responses by upstream rivals (here, content providers) to attempted input foreclosure by the merged entity might significantly temper any harm realized by consumers or unaffiliated downstream rivals (here, MVPDs). Such responses would tend to maintain the latter firms’ threat values in their negotiations with the merged entity.

8.

See, for example, B. Espen Eckbo, Horizontal Mergers, Collusion, and Stockholder Wealth, 11

9.

Examples include Eric S. Rosengren & James W. Meehan, Empirical Evidence on Vertical Foreclosure, 32

10.

This argument assumes that financial markets would on average correctly anticipate and price in this behavior, which is the standard assumption made under the Efficient Markets Hypothesis.

11.

We do note that this no-efficiency argument allows us to identify harm from the stock returns. Were there efficiencies, a negative return of downstream rivals would have ambiguous implications for anticompetitive effects because harm can occur even with efficiencies.

12.

Rivals might realize positive stock market reactions even where there are expectations of (appreciable) efficiency effects. Such a result might imply, for example, that the merger would facilitate collusion in the relevant segment(s), the effects of which would dominate any tendency for rivals to lose customers due to EDM realized by the merged entity.

13.

These subsections draw heavily from Steve C. Salop & Daniel P. Culley, Revising the US Vertical Merger Guidelines: Policy Issues and an Interim Guide for Practitioners, 4

14.

See Memorandum Opinion and Order, In the Matter of Applications of Comcast Corporation, General Electric Company and NBC Universal Inc. for Consent to Assign Licenses and Transfer Control of Licensees, Federal Communications Commission MB Docket No. 10-56 (2011) and Complaint, United States v. Comcast Corp, No. 1:11-cv-00106 (D.D.C. Jan. 18, 2011), respectively. See also Steven C. Salop, Invigorating Vertical Merger Enforcement, 127

15.

Expert Report of Carl Shapiro, United States v. AT&T Inc., No. 18-5214 (D.D.C. Feb. 2, 2018). Jonathan B. Baker, Nancy L. Rose, Steven C. Salop & Fiona Scott Morton, Five Principles of Vertical Merger Enforcement, 33

16.

Expert Report of Carl Shapiro, supra note 15, at note 230.

17.

William P. Rogerson, Economic Analysis of the Competitive Harms of the Proposed Comcast-NBCU Transaction, In the Matter of Applications for Consent to the Transfer of Control and Licenses, General Electric Co. Transferor, to Comcast Corporation, Transferee, Federal Communications Commission MB Docket No 10-56 (June 21, 2010).

18.

Id.

19.

As this scenario does not consider the VIP changing

20.

Rogerson, supra note 17.

21.

More generally, letting

22.

According to the government’s expert, this same result constituted “one critical reason why the vertical merger between AT&T and Time Warner is more problematic than many other vertical mergers.” Expert Report of Carl Shapiro, supra note 15, at 63; see also Trial Brief of the United States, United States v. AT&T Inc., No. 18-5214 (D.D.C. Mar. 9, 2018) at 35 (“[T]he [EDM] effect in this case would be much smaller than the effect seen in vertical mergers in some other industries. It would be much too small to offset the competitive harm.”); Proposed Findings of Fact of the United States, United States v. AT&T Inc., No. 18-5214 (D.D.C. May 8, 2018) at 85 (“Although AT&T’s cost for the Turner content will decrease, resulting in lower prices . . . [it will] pass through only a relatively small portion of its cost decrease, around 22 percent on average.”); Carl Shapiro, Vertical Mergers and Input Foreclosure: Lessons From the AT&T/Time Warner Case, 59

23.

Salop, supra note 14, at 1971.

24.

Salop & Culley, supra note 13, note that the merger may instead provide the upstream suppliers with an incentive to raise input prices through coordinated action. Such an effect would lead to the same prediction on the stock price reactions of upstream rivals. There is some reason to believe that any observed stock market reactions in the pay-TV industry are more likely to reflect unilateral foreclosure effects rather than any expectation of postmerger collusive behavior (as discussed further below).

25.

This effect might be ameliorated to the extent that the

26.

Note that this prediction is likely to hold even if

27.

28.

See, for example, Volker Nocke & Lucy White, Do Vertical Mergers Facilitate Upstream Collusion? 97

29.

See, for example, Sara Biancini & David Ettinger, Vertical Integration and Downstream Collusion, 53

30.

Assume that the other conditions required for reaching and sustaining a collusive agreement, such as low monitoring costs and a mechanism to credibly punish defectors, are met. In other words, but for the behavior of the maverick a collusive equilibrium would obtain.

31.

Another possibility is that the forward integration of an upstream supplier into the downstream segment makes it easier for the upstream firm to monitor competitors’ input prices in order to facilitate upstream collusion. For example, in the present context AT&T’s video distribution businesses negotiate contracts with a number of competing upstream content providers. Postmerger, AT&T could share information on the prices and terms negotiated with unaffiliated programmers with its upstream Time Warner affiliate, thereby providing the latter with insight into the pricing of its competitors not otherwise available but for the merger. Such information exchanges could be used to monitor rivals’ compliance with a collusive agreement. Michael H. Riordan & Steven C. Salop, Evaluating Vertical Mergers: A Post-Chicago Approach, 63 ![]() . The second condition does not generally apply to the U.S. video production and distribution industries.

. The second condition does not generally apply to the U.S. video production and distribution industries.

32.

Of course, the operative assumption in this case is that the increased profits to the VIP from its downstream affiliate more than offset the losses to its upstream affiliate from selling fewer inputs.

33.

Salop & Culley, supra note 13, at 29.

34.

See, for example, Kai-Uwe Kuhn & Massimo Motta, The Economics of Joint Dominance (1999) (unpublished manuscript); Olivier Compte, Frederic Jenny & Patrick Rey, Capacity Constraints, Mergers and Collusion, 46

35.

Trial Brief of the United States, supra note 22, at 41.

36.

Id.

37.

Id. at 43–8. Note that the DOJ did not dismiss the possibility that the merged entity would also have a unilateral incentive to foreclose content to vMVPDs. See, for example, Post-Trial Brief of the United States, United States v. AT&T Inc., No. 18-5214 (D.C.C. May 8, 2018) at 107–12. Rather, it argued that coordination with Comcast would probably be even more profitable. Trial Brief of the United States, supra note 22, at 43. The DOJ emphasized that, postmerger, AT&T and Comcast would have “unprecedented insight into each other’s dealings with key programmers” and that “MFNs and similar contractual provisions could amplify the effect by giving AT&T and Comcast further insight into each other’s terms with virtual MVPDs.” Post-Trial Brief of the United States at 117.

38.

Pretrial Brief of Defendants AT&T Inc., DirecTV Group Holdings, LLC, and Time Warner Inc., United States v. AT&T Inc., No. 18-5214 (D.D.C. Mar. 9, 2018) at 58.

39.

Note that absent strong consumer preferences for targeted advertisements (coupled with the assumption that those advertisements would be exclusively offered on AT&T’s pay-TV services), it is unclear whether the deployment of the aforementioned platforms would materially affect the expected future profitability of AT&T’s MVPD rivals (with the possible exception of Verizon, as discussed later on).

40.

We subtract the risk-free return, that is, U.S. Treasury interest rates, from the benchmark’s and the security’s returns to adjust for the fact that the stock market responds to interest rates.

41.

Jeffrey Jaffe, Special Information and Insider Trading, 47

42.

John Y. Campbell et al., The Econometrics of Financial Markets 167 (1997) also discuss this method.

43.

An alternative to the portfolio method would be to calculate the average cumulative abnormal return

44.

Ed Hammond, Alex Sherman & Scott Moritz, AT&T Discussed Idea of Takeover in Time Warner Meetings, ![]() ].

].

45.

See, for example, Keach Hagey, Amol Sharma, Dana Cimilluca & Thomas Gryta, AT&T Is in Advanced Talks to Acquire Time Warner, ![]() ].

].

46.

Note that

47.

In what follows, we treat a firm’s cumulative abnormal return at date

48.

Proposed Findings of Fact of the United States, supra note 22, at note 6.

49.

Mike Farrell, Cable One to Become Sparklight in Summer 2019, ![]() ].

].

50.

Thomas Gryta, AT&T Seeks to Shake Up Pay TV, ![]() ].

].

51.

Id. (noting that AT&T was reportedly under pressure to “deliver gains from the [$50 billion] DirecTV deal.”). The introduction of DirecTV Now may have been viewed as an effort by the company to refocus DirecTV’s offering away from its already declining satellite business by offering a new product that would be viewed as more desirable by cord cutters while leveraging the strength of the DirecTV brand.

52.

Eighteenth Report, In the Matter of the Annual Assessment of the Status of Competition in the Market for the Delivery of Video Programming, Federal Communications Commission MB Docket No. 16-247 (Jan. 17, 2017) at 21.

53.

The DOJ also presented evidence suggesting that AT&T recognized a potential for DirecTV Now to cannibalize its higher-margin (albeit already declining) satellite-based DirecTV service. In turn, AT&T reportedly discussed “where to draw the line on the features/benefits for [DirecTV Now] such that we don’t aggressively cannibalize DBS . . .” (Post-Trial Brief of the United States, supra note 37, at 112) in order to retain (or at least mitigate the attrition from) its legacy DirecTV offerings, which also suggests its desire to distinguish DirecTV Now from traditional DirecTV service. At the same time, it also appears that AT&T wished to differentiate DirecTV Now from competing vMVPD providers by offering a larger bundle of programming. In other words, DirecTV Now appears to have been situated somewhere ‘in-between’ a traditional, satellite-based package and a ‘skinny bundle’ normally offered through vMVPD service.

54.

See, for example, Pretrial Brief of Defendants AT&T Inc., DirecTV Group Holdings, LLC, and Time Warner Inc., supra note 38, at 20 (“Turner networks are increasingly disadvantaged in competing against dominant digital advertisers such as Facebook and Google for advertising revenues, which are essential to Turner’s dual-revenue-stream business model and essential to preventing additional upward pricing pressure on consumer subscription prices.”).

55.

Id. at 20–1. This same argument, of course, is not necessarily restricted to SVODs. If, say, the merger would allow AT&T to provide higher-valued content (possibly containing higher-valued targeted advertising as well) and AT&T could restrict that content to its own pay-TV customers (or price it relatively less than what competitors could profitably charge for it), then the expected future profitability of both SVODs and other types of MVPDs might decrease.

56.

See, for example, Caffarra, Crawford & Weeds, supra note 27; Patel, supra note 3.

57.

The question of whether SVOD service is a substitute or complement to traditional MVPD service was not resolved in the trial proceedings. If they are complements, then an increase in the price of a rival’s traditional MVPD service through partial foreclosure should lower the demand for SVOD service, which in the present context should translate to a negative abnormal return for SVOD providers around the proposed merger’s effective announcement date, all else equal. The opposite would hold true if they are substitutes. Of course, it is also possible that SVOD and traditional MVPD service are, for the average customer, independent in demand. The relatively small changes in the day-to-day abnormal returns for both Netflix and Amazon found here coupled with Amazon’s considerable operations outside of video distribution would seem to preclude drawing an inference on the substitutability versus complementarity question, though this issue will obviously be an important one for future investigations of the video distribution segment.

58.

These results also cut against the notion that the negative post-announcement returns of the traditional MVPDs reflect expectations that the merged entity would offer content better aligned with customer viewing preferences. If that were the case, one would expect to observe significant negative returns accruing to both those distributors and SVODs at the same time. The Netflix and Amazon estimations can in this sense also be regarded as ‘falsification tests’ supporting the partial foreclosure hypothesis as it pertains to the traditional MVPDs.

59.

Post-Trial Brief of the United States, supra note 37, at 129–34.

60.

Janusz A. Ordover, Garth Saloner & Steven C. Salop, Equilibrium Vertical Foreclosure, 80

61.

Id.

62.

Baker, Rose, Salop & Scott Morton, supra note 15.

63.

Large abnormal returns might sometimes occur on days further away from the event date due to other news that impacts a firm’s expected profitability. That said, one would still expect the ‘typical’ (absolute) abnormal returns measured across several ‘distant’ days in the event window (particularly the pre-event window) to be smaller than the (absolute) average abnormal return associated with a smaller window measured around the event date itself.

64.

Of course, one might expect this tendency to be increasing in the extent of video watching that subscribers make over their handsets in lieu of other devices.

65.

Note also that the

66.

Ben Levisohn, AT&T: The King of Dying Businesses? ![]() ].

].

67.

Ryan Faughnider & Meg James, If AT&T Swallows Time Warner, Who Might be Gobbled Up Next? ![]() ].

].

68.

Brooks Barnes & Emily Steel, A Chilly Reaction to AT&T-Time Warner Deal, ![]() ].

].

69.

Todd Spangler, AT&T + Time Warner: 3 Reasons a Merger Makes Sense and 3 Hurdles, ![]() ]. Spangler also cites a Credit Suisse analyst as stating: “Control over a leading film TV studio, plus valuable sports and drama networks, [makes Time Warner] the partner of choice if any consolidation is to take place in U.S. media in our view.” Id. (emphasis added).

]. Spangler also cites a Credit Suisse analyst as stating: “Control over a leading film TV studio, plus valuable sports and drama networks, [makes Time Warner] the partner of choice if any consolidation is to take place in U.S. media in our view.” Id. (emphasis added).

70.

Antoine Gara, What AT&T’s Over $80 Billion Takeover Of Time Warner Means For Media Stocks, ![]() do not indicate any substantive impacts on the abnormal returns of Amazon or Google, which one would expect if equity markets anticipated their intention to acquire Disney.

do not indicate any substantive impacts on the abnormal returns of Amazon or Google, which one would expect if equity markets anticipated their intention to acquire Disney.

71.

Barnes & Steel, supra note 68.

72.

See, for example, Faughnider & James, supra note 67; Gara, supra note 70; Spangler, supra note 69.

73.

Spangler, supra note 69.

74.

See, for example, Barnes & Steel, supra note 68 (“The Murdochs have ownership control, and nobody thinks they would be sellers.”). The same argument pertains for Comcast’s (eventually abandoned) competing bid to acquire Fox.

75.

Id.

76.

Note also that in May 2019 Disney purchased Comcast’s equity stake in Hulu, giving Disney full control of the streaming service.

77.

78.

This arbitration offer would be available to rival MVPDs for seven years following the proposed merger’s consummation.

79.

80.

Note that this result does not depend on the post-arbitration carriage rates being lower than the pre-arbitration rates—it only requires that the post-arbitration rates would not be as high as the rates that would have prevailed absent the arbitration agreement.

81.

These portfolios models were also estimated using the alternative a ten-day event window. We also estimated the associated abnormal returns for each individual firm using two- and ten-day event windows. For the sake of brevity these results are not presented here, but they are available upon request.

82.

For example, on Nov. 29, 2017 Disney announced that it would be paying a semi-annual cash dividend to its shareholders. The Walt Disney Company, The Walt Disney Company Announces Semi-Annual Cash Dividend of $0.84 Per Share, Nov. 29, 2017, https://thewaltdisneycompany.com/walt-disney-company-announces-semi-annual-cash-dividend-0-84-per-share/. Moreover, on that same day Viacom announced the appointment of a new senior executive who would be spearheading the company’s “transformative agenda.” Viacom Appoints Jose Tolosa as Chief Transformation Officer, ![]() .

.

83.

See Akane Otani, Selloff Pauses 2017’s Tech-Stock Surge,

84.

Todd Spangler, AT&T Confirms DirecTV Now Price Hikes, Launches New ‘Slimmer’ Bundles With HBO That Omit Many Cable Channels, ![]() ].

].

85.