Abstract

This article looks at the competition (or lack thereof) in the U.S. and EU financial service markets and how innovative companies have decided to enter the market. Over the years, many start-ups have ventured into financial services; however, they have faced heavy regulations. These regulations have led these companies to using a “white label” business model. This model has wide competition law implications: some good (e.g., more innovation at different levels of financial services) and some bad (e.g., innovative companies being bought out). These start-ups do not provide the competition first hoped while competition authorities and regulators often lag behind the technology to act and preserve competition before it is too late. This article makes some recommendations how the U.S. and EU competition authorities can learn from each other’s mistakes.

I. Introduction

Since the 1980s, the U.S. and EU economies have seen a decrease of its manufacturing sector and an increase of its service sector. 1 This shift has deeply impacted the economy and society. Many manufacturers relied on outsourcing. 2 Companies had to rely on either outsourcing their whole supply chains or outsourcing specific tasks along their supply chains.

Breaking up the supply chain into smaller pieces is known as “taskification.” 3 Much like manufacturing, services underwent a taskification in recent times. 4 This taskification 5 enables some service providers to outsource some tasks, improve efficiency, 6 and use white label services. 7 White labeling occurs when an entity manufactures a product and sells it to another who then affixes their own label onto the product.

The financial sector has followed similar patterns. The financial industry has expanded in the United States and United Kingdom since the late 1970s and early 1980s. Deregulations in the United States and the European Union boosted this growth: 8 they led to market entry and more competition from within the industry. 9 Deregulations shifted the oversight burden from specialized regulators to the competition laws because policy makers implicitly relied on competition to keep these markets efficient.

White labeling is a form of outsourcing or subcontracting. With this form of subcontracting, the consumers do not know the identity of the producer and suffer from information asymmetries. However, information asymmetry is not the only problem with white labels. This article investigates how white labeling has been used to circumvent financial and competition regulations. This article compares this circumvention in the United States and Europe, with a focus on the United Kingdom because of its large financial service industry.

The circumvention of competition laws can harm customers in the short run because less competition often leads to higher prices. This circumvention can harm financial markets over the long run because financial services may become less innovative. The circumvention of financial regulations will also undermine financial markets. 10

In the financial sector, the chief white label service providers are banks and FinTech companies. FinTech is a portmanteau word combining two words: finance and technology. FinTech companies are companies that provide financial services through technology. 11 Those types of financial services have a long history 12 ; but the Internet and smartphones have enabled the FinTech sector to grow.

FinTech encompasses many activities from payment systems to trading services. 13 But in general, these companies have been disrupting how many financial activities have been carried out—including how regulations are implemented. 14

The business model of FinTech companies varies as much as their offerings. The business model of white label FinTech companies focuses on offering business-to-business (B2B) services; however, some white label FinTech companies have also consumer facing and handling offerings.

Section II discusses how taskification and white label can be used to circumvent regulation (i.e., regulatory arbitrage). White label has the potential to both increase and decrease regulatory compliance. Regulations create barriers to entry; so, a white label opens the door to some potential competition. However, in the FinTech industry, most start-ups have not provided the expected benefits.

Section III focuses on selected issues linked to white labeling of financial services and how white labeling increases the likelihood that companies violate the competition laws. White labeling affects market definition because judges must assess whether generics compete with branded products. Judges have opted to investigate this issue using a case-specific analysis putting the burden on the plaintiff; however, under specific circumstances, a quick rule approach would advance judicial efficiency. FinTech companies tend to operate under these specific circumstances.

White labels have also made market definitions in merger control more difficult. Both the transaction threshold notification approach and the turnover notification approach have their flaws. However, in an innovative industry like FinTech, a dual approach may better ensure that the competition authorities prevent welfare harming mergers.

II. White Label and Regulatory Arbitrage

This section provides some background on taskification in the FinTech industry. In many situations, tasks are regulated—not businesses. So FinTech companies can use white label services to delegate tasks and shift the associated regulatory burden on other entities. This section focuses on how white labeling and delegation affect the principal–agent problems within the FinTech industry. As these problems worsen, these companies become more likely to not take the efficient care level.

A. White Label and Regulatory Arbitrage

Regulatory arbitrage occurs when companies organize their activities to limit their regulatory exposure. 15 For example, oil companies may outsource their oil transport to limit their exposure in case of a spill. 16 Regulatory arbitrage depends on the ability to divide supply chains into tasks, the tasks existing as a standalone service, and the amenability of the regulation.

Regulations can facilitate regulatory arbitrage by limiting liability to the agent carrying out the services. 17 These regulations hold the agent/decision-maker liable but do not extend liability to the company hiring their services.

However, some regulations (e.g., environmental law) have extended liability to the entity that contracts out the service through vicarious liability. For example, the Oil Pollution Act implicitly created a vicarious liability 18 and included the owners and operators of vessels or facilities spilling oil under the “responsible parties.” 19 Without vicarious liability, regulatory arbitrage can benefit contracting parties while creating externalities on third parties.

Other regulations have extended liability from the agent to the principal through joint and several liability of both parties. For example, the Finance Act 2016 made online platforms jointly and severally liable for unpaid VAT of non-UK businesses that use their platform services. 20 Joint and several liability can still benefit the company that is contracting out because it can still receive some contribution from its contractor. 21

Regulatory arbitrage and white labeling often go hand in hand. Like regulatory arbitrage, white labeling allows companies to specialize, which can benefit society through learning by doing or economies of scale. However, white labeling also allows companies to shift the regulatory burden in two possible ways.

First, the seller of white label services may comply with the regulation and saves the purchaser of its services from having to comply with the regulation. For example, moneyinfo provides a white-label RegTech application that allows wealth managers to communicate securely with their clients. 22 Moneyinfo has built its system so as to comply with the General Data Protection Regulation to ensure that their clients do not violate the privacy laws. 23 In case of a breach, the data processor becomes liable, which may differ from the data beneficiary.

Second, the seller of white label services may sell its services as is and shift the regulatory burden on the purchaser of white label services. For example, Uber presents itself as a technology company and “describes the software it provides as a ‘lead generation platform’ that can be used to connect ‘businesses that provide transportation’ with passengers who desire rides.” 24 Through this approach, Uber has classified its drivers as independent contractors. 25 It avoids not only having to pay employment benefits but also having to hold a taxi license.

These regulatory burden shifts create a principal–agent problem because, in both situations, the entity liable for regulatory failure does not take some of the regulatory-impacting decisions. Due to the principal–agent problem, the entities may not take the efficient level of care in complying with regulations. This shift in regulatory burden has started to worry financial regulators. The next section discusses banking as a service and its relationship with regulation.

B. Banks Providing White Label Services

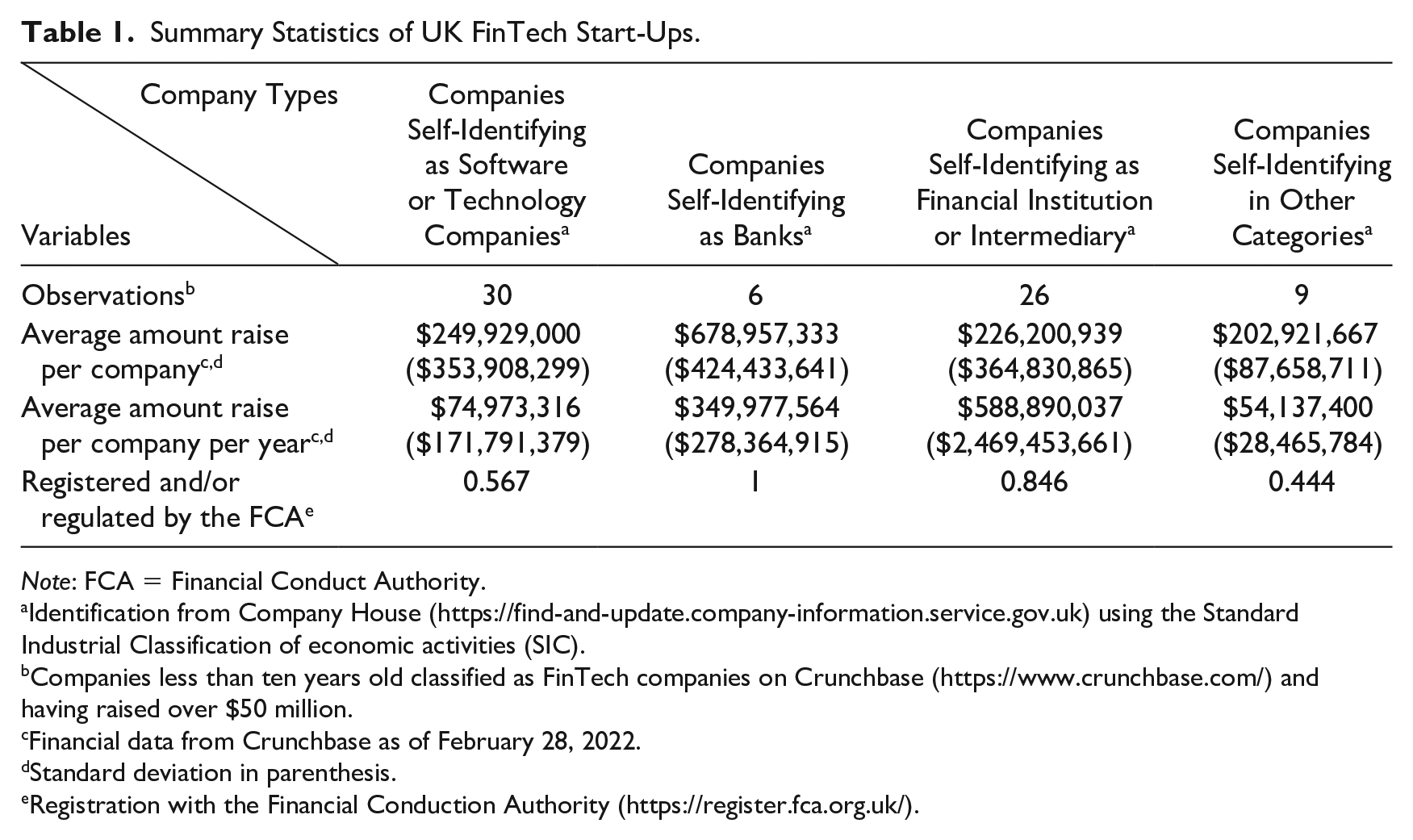

In recent times, the FinTech sector has expanded into areas traditionally reserved for banks. However, to do so, FinTech companies have two options. First, they can obtain a banking license and become banks themselves to comply with the banking regulation. However, this process has been so cumbersome that in the 2012–2022 period only six FinTech became banks in the United Kingdom (see Table 1). For example, Revolut operated an “electronic money” service but did not hold a license. 26 Eventually, Revolut sought a bank license to expand its services. 27

Summary Statistics of UK FinTech Start-Ups.

Note: FCA = Financial Conduct Authority.

Identification from Company House (https://find-and-update.company-information.service.gov.uk) using the Standard Industrial Classification of economic activities (SIC).

Companies less than ten years old classified as FinTech companies on Crunchbase (https://www.crunchbase.com/) and having raised over $50 million.

Financial data from Crunchbase as of February 28, 2022.

Standard deviation in parenthesis.

Registration with the Financial Conduction Authority (https://register.fca.org.uk/).

Second, FinTech companies can enroll the help of existing banks who already comply with the banking regulations. This is what Revolut did for many years:

Funds [were held] in accounts with a tier one UK bank, as per our obligations under the e-money regulations. Plus, all of your card transactions are processed by the Mastercard or Visa network and are protected by Mastercard or Visa rules.

28

The Federal Reserve Board (FRB) categorizes this approach as banking-as-a-service transaction. The FRB defines banking-as-a-service when a bank partners with a FinTech company; the FinTech then interacts with customers and provides banking services (e.g., lending, end-to-end transactions) through the support of the bank. 29 The customer may not know who provides the banking services. In other words, banks offer their white label services to intermediaries who then transact with third parties. The FRB also refers to this as “front-end FinTech partnerships.” 30

For example, Affirm is a U.S. FinTech company that allows consumers to spread out payments for items purchased at participating retailers. 31 Affirm also offers savings accounts. These funds are held with Cross River Bank. 32 Cross River Bank provides the white label services 33 and allows FinTech companies like Affirm to provide their offering while complying with the regulation. 34 Cross River Bank is a FinTech itself and also provides banking services directly to the public. 35

Banking-as-a-service can benefit many unbanked individuals. 36 The FRB hopes that technology can help reach individuals that banks cannot reach. However, banking-as-a-service has also raised some concerns. These services have allowed FinTech companies to provide regulated services without being regulated. For example, some online lenders have offered lending services but have relied on a small bank to underwrite the loan. 37 This approach has allowed these intermediaries to charge interest rate beyond the regulated interest rate limits. 38

The National Consumer Law Center identified a number of small banks that provide such banking-as-a-service offering. 39 They have warned customers against this business model because it can lead to higher rates. Regulations create barriers to entry, whereas white label creates more opacity. The combination means that consumers cannot rely on competition to keep prices low.

Policymakers have to balance regulating these issues against stifling innovation. Empirical studies have showed that regulations in the finance and banking industry have ambiguously impacted innovation. 40 On one hand, regulations may prevent financial institutions to innovate because these institutions have remained compliant with the regulations. On the other hand, regulations can spur innovations to gain a competitive advantage and to find ways to circumvent these regulations.

As compared with the United States, the United Kingdom has taken a different approach. The UK government has given more weight to the stifling of innovation argument. The UK Financial Conduct Authority (FCA) has created a regulatory sandbox where any company can “test” services with real costumers and introduce these services to the market in less time. 41 The FCA changed this sandbox to accommodate FinTech following a review of the FinTech landscape. 42 But this approach gives FinTech companies a competitive advantage over more established financial companies: they face less regulations.

In the United Kingdom, Crunchbase identified 120 UK-based FinTech companies 43 that raised over $50 million before February 2022. Of those companies, seventy-seven were less than ten years old, which could be considered “young” companies. Of those seventy-seven companies, two companies went public, one filed for administration, and three were acquired. Table 1 shows some summary statistics for the remaining 71 companies.

Most of the UK FinTech companies that self-identify as software or technology companies have registered with the FCA and are regulated as payment services or electronic money service providers. By contrast, all banks are fully registered and regulated with the FCA. These FinTech companies have raised more funds. Almost all financial intermediaries are registered and/or regulated.

Much of the development in FinTech has come from B2B markets. 44 This B2B is where much of white labeling occurs. Among the start-ups identified in the table, some companies specify that they provide white label services. For example, Chetwood Financial describes some of its offering as “bank-as-a-service solutions.” 45 As part of its offering, Chetwood Financial provides a wide range of services that can be rebranded. 46 However, third-party entities have used this ability to white label to defraud some consumers: “clone firms” pretend to be or work with the regulated firms to defraud the public. 47 White labeling can lead to more fraud: because Chetwood Financial provides white label support to many companies, consumers may struggle to identify who they support.

To increase its bank-as-a-service offering, Chetwood Financial acquired Yobota. 48 The Chetwood Financial Head of Corporate Development claims that these services can help increase competition and challenge “legacy banks.” 49 As shown in Table 1, the number of new companies being able to provide full-service banking-as-a-service and compete is limited. Instead, most companies tend to specialize as software providers or intermediaries with limited capacity to compete. Therefore, FinTech could be trading a fully integrated vertical monopoly of legacy banks with a vertically disintegrated production chain with a few competition choke points.

C. Banks Using White Labeling Services

As Table 1 shows, more FinTech start-ups self-describe as software or technology companies than they do as full-service banks. Companies may decide to offer white labeling services for many reasons. A rational service provider would do so if they profit more from specializing in software development and spreading their costs over multiple downstream entities than they would from offering their services to the public. These FinTech companies compete for a “task” along the supply chain instead of the supply chain.

This “task” approach allows them to externalize the regulatory burden onto the public-facing service provider. For example, Rapyd, a start-up created in 2016, offers a myriad of financial services. 50 Among its offering, Rapyd offers a “white label” model where it “license[s] its technology to other companies.” 51 Different companies can adopt Rapyd’s technology and compete for consumers. Rapyd’s move to offer white label services was prompted because it faced regulatory constraints. 52

Companies like Rapyd offer their services to banks or other institutions that are already regulated. Since these institutions already carry the compliance burden, the white label service providers do not have to duplicate those costs. This decrease of cost duplication could encourage competition because it decreases a barrier to entry at the white label service provider level.

However, without full transparency, service purchasers may not realize that they are responsible for the ultimate compliance. In its 2018 interim report on platforms, the FCA found that compliance with the rules was an issue when using white label services. 53 The FCA, however, did not find it necessary to change its regulatory approach. 54

The FRB labeled banks using FinTech white label services as “operational technology” partnerships. 55 Through these partnerships, banking institutions hire FinTech companies to enhance their processes. 56 In other words, FinTech companies provide white label services to the banks. The FRB warned about the risks associated with these relationships. 57

In 2021, the FRB, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency wrote “Interagency Guidance on Third-Party Relationships” and opened a public consultation. 58 These U.S. agencies have put in place this guidance because reliance on white label services has increased: including “core bank processing, information technology services, accounting, compliance, human resources, and loan servicing.” 59

This increased reliance on outsourcing and white labeling has increased monitoring costs for financial institutions. Because of these increased costs, these agencies seem to worry that these institutions do not conduct due diligence to the expected level. They have found the need to spell out risk management and oversight best practices. 60

In this guidance, these agencies also worry about the impact on competition. They warn that these banking institutions need to evaluate how “strategic business arrangements (such as mergers, acquisitions, divestitures, partnerships, joint ventures, or joint marketing initiatives)” affect their activities. 61

The guidance also warns about carrying out due diligences of their service provider with competing banks. 62 This joint approach would affect competition because the banks who join forces to carry out due diligence would benefit through economies of scale: they would spread the costs of due diligence between them. These banks could refuse that other banks join in their due diligence efforts—effectively raising the relative costs for their competitors.

The guidance also discusses data aggregations. 63 These aggregators raise their own competition concerns. A third-party data aggregator has the opportunity to gather data from multiple banks, which would not otherwise be able to do so. These data aggregators face the risk of acting as hubs where the banks act as spokes: these data aggregators must ensure that they do not use this aggregation to give these banks a competitive advantage that would otherwise be illegal.

The European Commission has already fined companies for facilitating a cartel. 64 The next logical move is for the competition authorities to take a look at data aggregator and their role in cartelization. The European Commission has indicated that it may intervene in such situations. 65 The next section dives into the relationship between competition and white labels.

III. White Labeling and Competition Law

FinTech companies have injected competition in the financial service industry to the great despair of incumbents, who claim that the low regulations created unfair competition and an uneven playing field. 66 While the complaint may be overblown, FinTech has provided some needed competition.

Taskification can increase competition in downstream markets while decreasing competition in the upstream markets. But taskification and white labels can also be used to circumvent competition laws and harm society at large. The following section dives into these issues.

A. Market Definition: White Labeling versus Branding

Brands affect our purchasing decisions of goods and services. When consumers purchase an airline ticket with a legacy airline, they expect a different service than when they purchase a ticket with a low-cost carrier. This section discusses the relationship between white labels and consumer expectations.

Faced with consumption decisions, consumers form a belief system about the probability of the quality of the product or service. Branding can transmit information about the service quality: branding allows consumers to correlate past with future consumption experience. 67 Consumers can perform a less speculative cost–benefit analysis than they perform with generics.

Brand owners can capture some of the information cost savings: consumers are willing to pay more for branded goods to avoid information costs 68 ; so, brand owners can charge higher prices to decrease information asymmetries. 69 But white labels can blur the line between generics and branded services.

In Brooke Group Ltd. v. Brown & Williamson Tobacco Corp., 70 the U.S. Supreme Court contrasted “true generics” which carry no brand against “private label generics” carrying the brand of the ultimate retailer. 71 As the U.S. Supreme Court noted: generics differ from “private label generic,” which this article refers to as white labeling. At the heart of this decision, the U.S. Supreme Court had to decide whether branded products and generic products compete—an exercise that will be repeated in many industries over the years. 72

The necessity to investigate whether a generic or white label compete is inefficient given the jurisprudence. The U.S. Supreme Court should use a quick look rule approach that would not require plaintiffs to have to reprove that generics compete with branding in every case. This presumption would still allow the branded products to present counter evidence. 73

According to this definition, generics are the absence of a brand. 74 Because consumers cannot distinguish between generics, they perform a more speculative expected cost–benefit analysis than they would perform with branded products. 75 White labels can however create confusions. White labeling amounts to the service provider rebranding the service as its own.

Some consumers may be aware of the re-labeling and consider it in their purchasing decision; but others will not realize that the ultimate seller affixed their brand onto of another service provider’s offering. 76 Therefore, consumers may mistakenly associate a re-labeled service with an experience when the correlation between experience and brand breaks down. So, white labeling defeats much of what branding attempts to accomplish.

Branding and trademarks differ. 77 All trademarks are brands; but not all brands are trademarks. The brand owner may decide not to protect its trademark, or the brand may not be protectable under trademark law. But their differences are not central to this article.

Trademarks have three main functions: (1) they disseminate information about the quality of the product; (2) they indicate the origin of the product; and (3) they protect the goodwill of its owners.

First, trademarks help consumers associate an experience or the quality of a product with a brand. Brands help differentiate products through quality. For example, in the United States, trademarks (and service marks) exist to promote fair competition. 78 Trademarks improve information dissemination and reduce consumer search costs and confusion. 79 To that effect, U.S. trademark law prohibits the registration of trademarks that aim “to cause confusion, or to cause mistake, or to deceive.” 80

Second, trademarks also signal the origin of the product and help differentiate the products through its origin (instead of just its quality): trademarks keep producers accountable if a product fails to live to merchantability standards. For example, in the European Union, in Adam Opel v Autec, 81 the European Court of Justice (ECJ) had to decide whether replica toys displaying the Opel logo infringed on the Opel trademark. The ECJ held that the replica did not infringe if “the relevant public does not perceive the sign identical to the Opel logo . . . as an indication that those products come from Adam Opel.” 82 In other words, the ECJ ruled that trademark also functions as a marker of origin. Geographical indicators can perform that function on a broader scale (at the regional level instead of entity level). Some markers of origins can also evolve into a product themselves. For example, many luxury brands act as status symbols. 83

Finally, trademarks also help decrease the negative impact on companies from others pretending to sell their products. They encourage brand holders to monitor the market for poor-quality pretenders. For example, in the United Kingdom, the common law passing-off and malicious falsehood causes of action preceded trademark laws but accomplished many of the same aims. 84

White labeling affects all three functions of trademarks. First, if consumers are aware that the service is provided by contractors, they may no longer trust the trademarks. They may worry that even if the label remains the same, the experience or quality often differs when the supplier changes. Without more transparency, they may no longer trust the market. White labeling creates information asymmetries, and the consumers will fall back into evaluating their consumption decisions as they did with generics.

However, even if the quality is equivalent to the previous supplier (i.e., seller acting as quality control instead of service provider), white labeling affects the other functions of trademarks. A trademark cannot fulfill its origin function because the origin is not ascertainable. Some consumers assign utility and disutility with certain service providers. To avoid any disutility, the consumers now have to ensure that the service provider cannot delegate their duties. This non-delegation increases negotiation and transaction costs.

For example, some consumers may object to a company for moral or ethical reasons. But white labeling makes the supply chain opaque. This opacity can affect how consumers enjoy their goods or services. 85 For example, many consumers object to Amazon’s business methods, its anti-tax lobbying, and the working conditions of their employees to the point that some have called for boycotts. 86 However, these same consumers may not realize that many web-based service providers use Amazon services. 87 More specifically, Netflix uses Amazon Web Services (AWS). 88 While one might argue that what they do not know do not hurt them, consumers are unknowingly contributing to Amazon’s hegemony.

White labeling also affects goodwill and perceived reputation. When AWS suffered an outage, consumers blamed Netflix. 89 Netflix can respond by switching its service provider; but the harm is already done: consumers already blame Netflix (instead of AWS). In the case of Netflix, the company has limited choice for their service providers. 90

In this situation, the white label relationship creates a principal–agent problem. The B2B service providers control the quality whereas the business-to-consumer service seller faces the reputational impact. In other words, the service provider externalizes some costs of poor services onto the service seller. These externalities distort the incentives of white label service sellers and purchasers and affect the functioning of trademarks.

From a competition law standpoint, the branding of generic products (i.e., white labeling) is “an example of the power of brand advertising to bamboozle the public and thereby promote monopoly.” 91 These trademarks can create consumer deception and waste resources. 92

In the case of Amazon, they have a further distorted incentive because they also compete with Netflix in the streaming service sector. This competition might incentivize them to prioritize reestablishing their Prime services after an outage.

In FinTech, Chetwood Financial follows a similar business model: they offer their banking services as white labels for others to affix their brand and they offer services direct to consumers. This position as service providers upstream and retail competitor downstream raises competition concerns discussed in the next section.

B. White Labels and Vertical Relationship

A FinTech company that operates both at the wholesale and at the retail levels raises some red flags. However, it is not uncommon for companies to change their business models and offerings.

First, if a vertically integrated company (that offered its own retail brand) introduced a white label wholesale service, such a company would cannibalize itself. 93 This company would slow down its potential penetration in the downstream markets by making it easier for downstream retailers to compete. So, introducing a white label could reveal that the company gave up competing in the downstream market while its comparative advantage remains at the wholesale level.

Second, if a FinTech company started at the retail level and decided to start providing white label services at the wholesale level, this sequence of events can have diverging explanations. On one hand, some explanations can be competition neutral. For example, the company may have started at the retail level and may have been unable to enter the wholesale level because it lacked funds or the technology to operate at both levels. Many start-ups face budget constraint at the beginning of their lifecycle. 94

On the other hand, some explanations may be rooted in an intent to decrease competition. For example, the retailer may create a wholesale entity to coordinate with its competitors at the retail level. This approach amounts to a hub-and-spoke with a horizontal element. The horizontal element could be viewed as an anticompetitive price fixing business model. 95

Vertical business arrangements do not tend to raise as many issues as horizontal business arrangements. In 2022, the European Commission reiterated its vertical block exemptions to deal with e-commerce 96 : vertical agreements that do not exceed 30 percent of the market 97 and do not contain hardcore restrictions 98 are exempt from antitrust scrutiny. It discusses “online intermediation” and classified them as vertical agreements—when these agreement “facilitate the initiation of direct transactions between undertakings, as well as those that facilitate the initiation of direct transactions between undertakings and final consumers.” 99

The European Commission addressed what it refers to dual distributions “where a supplier sells goods or services not only at the upstream level but also at the downstream level, thereby competing with its independent distributors.” 100 The Commission considers that these agreements without hardcore restriction would also fall under this exemption because “the competitive relationship between the supplier and the buyer at the downstream level is less important than the potential positive impact of the vertical agreement on competition in general at the upstream or downstream level.” 101

However, the Commission worries about the exchange of information because this dual distribution “may raise horizontal concerns” and the Commission limits the information that can be shared to the information necessary to the vertical agreement and to the improvement of the production or distribution of the services. 102 But, if the dual distributor is an online intermediary, then the exemption would not apply. 103

Third, if a FinTech company started as a wholesale white label service provider before entering the retail market, this sequence of events can also raise some anticompetitive concerns. For example, a FinTech company may have decided to enter the retail market to price squeeze downstream players and increase its revenues over the long term. Price squeeze refers to a practice when “a vertically integrated firm sells inputs at wholesale and also sells finished goods or services at retail” and because of its market power in the input level, it increases input prices to reduce the profit margins of retail-level competitors. 104

The U.S. Supreme Court has viewed price squeeze as combining two causes of actions. First, price squeeze can be viewed as a form of predatory pricing: the firm uses the input market profits to subsidize its predation in the retail market. 105 Second, price squeeze can be viewed as a form of refusal to deal: the firm charges downstream competitors the retail price. 106 The U.S. Supreme Court has rejected price squeeze as a valid antitrust cause of action. 107 Many scholars agree with the U.S. Supreme Court’s decision. 108

However, EU courts have viewed price squeeze as an abuse of dominant position.

109

Price squeeze is referred as “margin squeeze” in the European Union. Margin squeeze occurs when

the difference between the retail prices charged by a dominant undertaking and the wholesale prices it charges its competitors for comparable services is negative, or insufficient to cover the product-specific costs to the dominant operator of providing its own retail services to end-users.

110

The different approaches between the United States and the European Union could be attributed to different views on the responsibilities of entities with market powers against the limit of freedom of contracting. The debate about the two approaches rages on. 111 A clear answer may not arise because different model parameters lead to different consumer welfare impacts. Deciphering the intent of a white labeler may be impossible; but context provides sufficient clues that they should trigger more scrutiny. Specifically, competition authority may pay more attention to how companies grew and developed instead of the current object and effect of their behavior. The next section focuses on another type of business model: the platform. Platforms are often combined with dual distribution as discussed next.

C. White Labels and Platforms

FinTech companies offer financial services relying on modern technologies to decrease transaction costs. These offerings take many forms, but two main trends have emerged: (1) FinTech relying on existing platforms like smartphones and (2) FinTech becoming platforms.

First, FinTech companies rely on technology like smartphones to delivery financial services. Websites, smartphones, and applications are platforms where consumers meet service providers—including FinTech. However, many FinTech companies use existing platforms like smartphone to offer their services. For example, Venmo is a social media-style peer-to-peer payment system funded in 2011 and acquired by PayPal, another FinTech, in 2013. 112 Venmo has become a dominant player in the mobile payment application space in the United States. 113

For these FinTech to thrive, they require access to these platforms. However, established platforms may not want to grant them access. For example, the European Commission has sent a statement of objection to Apple over its Apple Pay practices. 114 Previous companies have complained about Apple and the openness of its iPhone technology to other companies. 115 These issues with access to platforms could explain why some companies have decided to opt to provide white label services instead of competing with incumbents.

What Apple allegedly carried out amounts to a refusal to deal under an essential facility theory of harm. Apple is the platform provider (iPhone) but it is also a competitor and FinTech through its Apple Pay application. The U.S. Supreme Court rejected this theory of harm in Verizon v. Trinko 116 because the court did not want to impose a duty to deal 117 —particularly when the industry is regulated. However, it is unclear whether the U.S. Supreme Court would view financial services regulated like telephone services. Instead of refusing access, these platforms could use different strategies (discussed in section III B) to impede competition.

By contrast, in the European Union, policymakers have been worried about the power of these platforms. The European Commission has created the concept of “gatekeeper” in the Digital Market Act. 118 A gatekeeper is any platform that (1) “has a significant impact on the internal market”; (2) “serves as an important gateway for business users to reach end users”; and (3) has “an entrenched and durable position” in the market. 119 The Digital Market Act provides more specific definitions and bestows on these gatekeepers duties toward market participants—including FinTech start-ups.

Based on cursory observations, companies like Apple (with its iPhone and Apple Store) and Google (with its Android Operating System and Google Play) would qualify as gatekeepers. Therefore, they would not be able to restrict access to their platforms without reasons. 120 Under the Digital Market Act, Apple would have to grant access to FinTech companies to its platform or iPhone capabilities such as its payment system capabilities. 121

Second, many FinTech companies have adopted a platform model. Platform models vary almost as much as they are companies. For example, some FinTech like LendingClub 122 have adopted a matching platform model or “marketplace” model. 123 On these kinds of platforms, supply meets demand: on LendingClub, fund providers meet fund demanders.

Other platforms like Visa, Master Card, and American Express may not have started as FinTech but compete with FinTech companies. In many respects, they are becoming FinTech companies themselves. These companies mainly function as payment platform 124 where they match billing and paying needs.

Platforms have baffled many courts and challenged many established antitrust principles in general 125 and in the FinTech industry in particular. For example, in Ohio v. American Express Co., 126 the U.S. Supreme Court had to address two-sided payment platforms and decided that the product market was the payment services. The Court found that the plaintiffs failed to carry their burden of proof. In this case, the Court demonstrated a lack of understanding of the platform models. 127

By contrast, the ECJ recognized three different product markets. In MasterCard and Others v European Commission, 128 the European Commission argued that three markets existed: (1) upstream market for the business of banks; (2) downstream market for the business of card holders; and (3) downstream market for the business of merchants. 129 The European Commission rejected the American Express approach that only one market existed. 130 The ECJ agreed 131 and found that MasterCard abused its dominant position. 132

The U.S. approach focuses on an ex-post approach to card issuance, whereas the EU approach uses an ex-ante approach view to these platforms. The EU approach is more complete and in line with rational behavior that the U.S. Supreme Court has repeatedly embraced where ex-post actions affect ex-ante behavior. According to rational expectation theory, individuals form rational expectations about the future based on perfect information. 133 Thus, payment service platform clients ought to know how much each service they use costs, and this cost affects which card they obtain.

However, if information is partial, then the theory breaks down. Instead, when an individual gathers new information, they change their expectations. So, if a client does not have the most optimal card to make a purchase in a store because of imperfect information (e.g., learns about card fees), they can return to the card market to obtain the optimal card before they need to make another payment.

The U.S. approach has many problems. Viewing platforms as “one market for transaction” fails to recognize that clients have repeated interactions with their payment service providers and merchants and that individuals learn by doing. The U.S. approach is not more (judicially) efficient because the parties still have to present evidence about which market they would believe the platforms are operating.

Similarly, the EU approach, while more complete, fails to consider that payment service uses multi-home, 134 that is “many merchants accept both American Express and Visa; furthermore, some consumers have both Amex and Visa cards in their pockets.” 135 Thus, another market exists at the transaction level, which allows the car user to decide based on the situation which card is more optimal.

The U.S. and EU competition authorities (and scholars) are learning everyday about new business models. The courts should embrace the challenge instead of trying to retrofit old rules to new business models. FinTech companies have been innovating constantly and the use of white label platform will challenge established theories. The competition authorities should ensure that this innovation is protected. 136 The next section discusses how white labels can enhance innovation.

D. White Labels and Innovation

White labels may have helped FinTech innovations through taskification and vertical disintegration. Vertical (dis)integration and competition have a U-shaped relationship: more vertical integration occurs at opposite end of the competition spectrum. 137 So, taskification and white labeling could be correlated with the middle of the competition spectrum. And this middle of the spectrum is correlated with more innovations. Competition and innovation also have a U-shaped relationship: 138 less innovation occurs at opposite end of the competition spectrum. In other words, vertical disintegration that comes with white labels 139 could benefit consumers in the long run through more innovation.

Legislators and regulators have had many conversations about the need to foster innovation through competition laws; 140 but little has been done. The FinTech ecosystem has led to many innovations but remains fragile. White labeling could improve the likelihood of seeing innovations.

White label and FinTech innovations can help the competition laws by removing the need for certain exemptions. For example, the insurance industry suffers from many market failures including information asymmetries. In the United States, insurance companies are exempt from Federal antitrust laws 141 under the McCarran-Ferguson Act. 142 Based on this exemption, insurance companies were able to share information. This information sharing could have benefited consumers because no insurance companies had enough information (at the time) to efficiently price their insurance products. 143

A modern FinTech company decreases the need to have such exemptions. These companies have access to big data and can calculate the probably of accident without having to information-share. They can also use white labeling to increase their economies of scale and gather that information on their own. For example, Insuritas is a consumer facing white label insurance company founded in 1999. 144 Insuritas is an innovative insurance FinTech. 145 Insuritas has allowed banks like Incommons Banks to offer insurance services to their clients. 146 Insuritas provides the insurance products and the banks use their network of customers to sell the product. Insuritas can use the information it gains from a broader pool of insured than it would have otherwise in the insurance market to ensure products are price properly.

Through white labeling, this insurance company may gain a critical mass of information to price its product in a competitive manner and to have enough clients to spread the cost of insurance over the pool of clients. The insurance company may even enter the retail market once ready. So white labeling might help competition policy in this case 147 and make the insurance exemption unnecessary. The next section discusses how competition authority should ensure that innovation and white labels reach their potential and delivery on the promises of FinTech.

E. White Labels and Merger Control

White labeling gives merging parties an opportunity to circumvent merger notification. Most jurisdictions have implemented one of two kinds of threshold: (1) a turnover threshold and (2) a value threshold. First, the European Commission uses a turnover threshold: if the merging entities have a combined turnover of over €5 billion and an EU-wide turnover for at least two of the firms over €250 million each, then they must notify the European Commission of their impending merger. 148

Through regulatory arbitrage, companies can structure their organization to fall below these thresholds. For example, Uber classifies its drivers as independent contractors. This classification allows companies like Uber to avoid labor regulation (e.g., paid leave). However, it also allows companies like Uber to avoid some competition laws regulation. For example, when Didi and Uber merged in China, they did not report the merger because it allegedly fell below the reporting threshold: 149 the revenues of both companies were hard to identify because of the subsidies and because it was unclear whether the passenger-to-driver transaction should be part of Uber’s revenue. 150 In other words, outsourcing makes calculating turnover ratios difficult. 151

White labeling can also be used to structure a company so as to decrease its turnover value. If each task is carried out by a different entity, then each entity will have a relatively smaller turnover (as compared with the value of the full supply chain). For example, CurrencyCloud provides its services to banks and other financial institutions making international payments. 152 CurrencyCloud had reported turnover of around £27 million in 2019 and £36 million in 2020. 153 Thus, the 2021 merger with Visa would fall outside the EU merger review threshold. 154

However, because Visa acquired CurrencyCloud for £700 million, 155 this acquisition would have triggered a merger review in the United States. In the United States, the requirement is linked to the value of the asset acquired—not to the turnover of the companies. If entities acquire another’s assets (through a merger or acquisition) above the regulatory thresholds, these entities must notify the authority before consummating the transaction. In 2022, the U.S. threshold increased from $92 million to $101 million. 156

This threshold explains how the Department of Justice was notified and opposed Visa’s acquisition of Plaid “an innovative and nascent competitor.” 157 Visa wanted to acquire Plaid on “strategic, not financial” grounds because Visa viewed Plaid as a future potential competitor. 158 This kind of mergers has been referred as killer acquisition. 159

The issue of “killer acquisition” (or “catch-and-kill”) is not unique to FinTech. 160 Many start-ups are acquired before they can become a competitor to the incumbent. The digital space is littered with such examples. For example, the UK Competition Market Authority ordered an ex-post analysis of some merger decisions. 161 The review found that “[t]he decisions taken in Facebook/Instagram and Google/Waze may have represented missed opportunities for the emergence of challengers to the market incumbents but have also likely resulted in efficiencies.” 162

Plaid’s turnover would not have triggered a notification to the European Commission.

163

But Plaid was turning an “essential” white label service provider:

Plaid already supports over 2,600 fintech apps, including 80% of the largest such apps in the United States, and has a network of more than 11,000 U.S. financial institutions. Plaid also connects to over 200 million consumer bank accounts through its existing services.

164

If Plaid were to be acquired, it would have devasting effects on the competitive landscape in the payment industry. The services that Plaid, a FinTech itself, provides are white label services to FinTech companies like Wise and Venmo. 165

Both threshold approaches have some benefits. If the competition authorities had to rely on a sole test, the value threshold test may be preferable when dealing with FinTech and other innovative companies who can act as rise to the potential of competitors to established incumbents.

For many years, merger control focused on “static” competition. One view of merger control is that at best it can only maintain the status quo. The review threshold in Europe reflects that view because it focuses on how large the companies are at the time of merger.

The value threshold reflects a “dynamic” competition. Merger valuation usually transfers some of the (expected) gains from the acquirer to the acquiree: the larger the deals, the larger the (expected) gains and the more the acquiring company expects to extract from consumers. 166 In some cases, this extraction comes from new offering; but in other cases, it comes from consumer surplus being transferred. If the competition authorities worry about foreclosing future competition, the value threshold will be superior in most cases to the turnover threshold.

Although it does not have the history of other tech giants, 167 Visa has invested or acquired many start-ups. 168 These investments demonstrate either an inability to innovate internally or a desire to stifle competition before they occur. Either way, this approach needs more scrutiny.

IV. Conclusion

At its core, financial service clients should care about money—whether their gains in capital markets or their liability exposure in the insurance market. Money is the most fungible assets; so, financial market should be as close to perfectly competitive as a market can be. To address the common solution to cutthroat Bertrand style competition, companies usually resort either to cartelization or to product differentiation.

Financial service companies have used both strategies to increase their profits. First, banks have cartelized to increase profits. For example, banks were found guilty of coordinating and manipulating the London Inter-Bank Offered Rate 169 and led to the ultimate demise of this rate. Second, financial institutions have also relied on branding to sway clients. 170 So, it makes the introduction of white labels that much more puzzling; or it could signal that FinTech companies have identified that entry was easier at the wholesale level. 171 Nonetheless, this approach has left them at the mercy of downstream companies.

The presence of white labels may signal that an industry has an upstream market more competitive than a downstream market. This competition may occur at the upstream market because of the barriers to entry in the downstream market. However, the evolution of the industry could reveal that white labels have an anticompetitive intent. In the case of FinTech companies, regulations have created barriers to entry and innovative companies may have found it easier to use white labels than enter downstream—through outsourcing the regulation to others. However, when large incumbents start offering white labels, the competition authorities should stand up and pay attention. Context is everything.

Footnotes

Acknowledgements

I would like to thank Guofang Xue for her excellent research assistant work in collecting and compiling the FinTech data and Claudia Lemus Pineros for her comments and editorial suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

1.

See e.g., Kerwin Kofi Charles et al., The Transformation of Manufacturing and the Decline in US Employment, 33

2.

See e.g., Christian Berggren & Lars Bengtsson, Rethinking Outsourcing in Manufacturing: A Tale of Two Telecom Firms, 22

3.

“Taskification refers to piecemealing (slicing) work activity into smaller activities.” Seppo Poutanen et al., Digital Work Economy in the Platform, in

4.

See e.g., Rainer Lanz & Andreas Maurer, Services and Global Value Chains: Servicification of Manufacturing and Services Networks, 6

5.

I have discussed and modelled in a previous article how breaking up services that were previously provided together can be used to increase profits. See Garry A. Gabison, Harmful Unbundling, 39

6.

Almas Heshmati, Productivity Growth, Efficiency and Outsourcing in Manufacturing and Service Industries, 17

7.

For example, in the merger between Marriott and Starwood, the European Commission identified three business models: (1) a hotel owned and operated by main entity; (2) owned by the main entity while operated by a “white label” management company; and (3) a franchise where the owner of a hotel contracts with the main entity to be able to use the brand and chooses either to manage their hotel under business model (1) or (2).

8.

Improvement in telecommunication also led to some outsourcing. See e.g., M. Hossein Safizadeh et al., Sourcing Practices and Boundaries of the Firm in the Financial Services Industry, 29

9.

See e.g., Hilary Ingham & Steve Thompson, Structural Deregulation and Market Entry: The Case of Financial Services, 14

10.

See e.g., Daniel Haberly & Dariusz Wójcik, Culprits or Bystanders? Offshore Jurisdictions and the Global Financial Crisis, 3

11.

Thomas Puschmann, Fintech, 59

12.

Id.

13.

Some FinTech companies also specialize in regulatory compliance. These companies are also referred as RegTech companies, a portmanteau word combining Regulation and Technology; however, the difference between FinTech and RegTech companies is not germane to this article.

14.

See e.g., Conf. of State Bank v. Office of Comptroller, 313 F. Supp. 3d 285, 296 (D.D.C. 2018)(granting a motion to dismiss in favor of the Office of the Comptroller of the Currency, which decided that it could grant bank chatters for FinTech companies that do not accept deposits, against a nationwide organization of financial regulators who believed “chartering of a Fintech would diminish a state’s ‘ability to continue [its] existing regulation’ and will make it marginally more difficult to detect ‘unlicensed activity.”)

15.

Elizabeth Pollman, Tech, Regulatory Arbitrage, and Limits, 20

16.

Richard R. W. Brooks, Liability and Organizational Choice, 45

17.

For the purpose of this discussion, I limit the regulatory arbitrage to outsourcing activities to non-separately owned entity. Using subsidiary does not fall under this discussion. As such, piercing the veil is not discussed below.

18.

Garry A. Gabison, Limited Solution to a Dangerous Problem: The Future of the Oil Pollution Act, 18

19.

Oil Pollution Act of 1990, as amended through P.L. 106-580, Dec. 29, 2000, § 1001 (32).

20.

Finance Act 2016, § 77B Joint and several liability: operators of online marketplaces.

21.

The opportunity for contribution exists regardless of the regulatory regime because companies can negotiate a contribution in case of regulatory failure.

23.

24.

O’Connor v. Uber Technologies, Inc., 82 F. Supp. 3d 1133, 1137 (ND Cal. 2015)

25.

Sanjukta M. Paul, Uber as For-Profit Hiring Hall: A Price-Fixing Paradox and Its Implications, 38

26.

27.

Revolut obtained a license in Europe. Chad West, We Got a Banking Licence, ![]() (accessed Feb. 10, 2022). At the time of writing, Revolut was close to obtaining a license in the United Kingdom. Siddharth Venkataramakrishnan in Chennai and Jyoti Mann and Stephen Morris in London, Revolut Chief Hopes for UK Banking Licence by Start of 2022, Financial Times (

(accessed Feb. 10, 2022). At the time of writing, Revolut was close to obtaining a license in the United Kingdom. Siddharth Venkataramakrishnan in Chennai and Jyoti Mann and Stephen Morris in London, Revolut Chief Hopes for UK Banking Licence by Start of 2022, Financial Times (

28.

Hiraki, supra note 26.

29.

30.

Id.

36.

FRB White Paper, supra 29, at 7.

37.

38.

Id.

40.

Knut Blind, The Impact of Regulation on Innovation, in

42.

Id.

43.

“For Financial Services we include the following leading industries: Banking, Insurance (InsurTech), Lending, Payments (Mobile payments), Personal Finance, and Wealth Management.” “All Financial Services Industries Accounting, Angel Investment, Asset Management, Auto Insurance, Banking, Bitcoin, Commercial Insurance, Commercial Lending, Consumer Lending, Credit, Credit Bureau, Credit Cards, Crowdfunding, Cryptocurrency, Debit Cards, Debt Collections, Finance, Financial Exchanges, Financial Services, Fintech, Fraud Detection, Funding Platform, Gift Card, Health Insurance, Hedge Funds, Impact Investing, Incubators, Insurance, InsurTech, Leasing, Lending, Life Insurance, Micro Lending, Mobile Payments, Payments, Personal Finance, Prediction Markets, Property Insurance, Real Estate Investment, Stock Exchanges, Trading Platform, Transaction Processing, Venture Capital, Virtual Currency, Wealth Management.” For more details, see Crunchbase Industry Spotlight: Fintech, ![]() (last accessed Apr. 25, 2022).

(last accessed Apr. 25, 2022).

44.

46.

“We can provide full ongoing servicing, complaints management, customer contact and collections on your behalf, whitelabelled as your brand. We provide built in automated communications as well as real-time functionality for Customer Services representatives through live chat or on the phone.” Id.

47.

48.

49.

51.

52.

Id.

53.

54.

Id.

55.

FRB White Paper, supra note 29, at 3. The FRB White Paper labeled banks using FinTech white label services as “operational technology” partnerships or as “customer-oriented” partnership. FRB White Paper, supra note 29, at 5. In customer-oriented partnerships, the FinTech companies interact with the customer but still serve the banking institution. In this setup, the FinTech may interact with the customers using their own brand. For example, Visa and MasterCard put their brands on debit and credit cards provided to bank customers. So, the customers may be able to distinguish the services provided by the FinTech and by the banks; thus, this type of partnership is not central to the discussion in this article.

56.

Id. at 3-5.

57.

Id. at 4 & 6.

58.

86 FR 38182.

59.

Id. at 38183.

60.

Id. at 38187-91.

61.

Id. at 38189.

62.

Id. fn. 7. at 38186; fn. 15 at 38189; fn. 10-11 at 38189; and discussion at 38199-200.

63.

Id. at 38197.

64.

Brian N. Hartnett & Will Sparks, The Service Provider as Cartel Facilitator: Assessing ‘Third Party’ Liability Under Article 101 TFEU, 1

65.

In the draft version of the Digital Market Act, the European Commission has indicated that data aggregation creates an unfair advantage. December 2020 draft version available here: https://ec.europa.eu/info/sites/default/files/proposal-regulation-single-market-digital-services-digital-services-act_en.pdf (last accessed May 24, 2022). In 2022, the European Commission proposed a new legislation called the Data Act that would facilitate data sharing. The draft version of the act is available here: ![]() (last accessed May 24, 2022).

(last accessed May 24, 2022).

66.

67.

William M. Landes & Richard A. Posner, Trademark Law: An Economic Perspective, 30

68.

Id. at 271.

69.

Id. at 274.

70.

509 US 209 (1993).

71.

Id. at 213.

72.

For example, in the pharmaceutical industry, some US Courts have had to analyze whether the generics compete with the branded product—even though they have identical chemical compositions—because of consumer perception. See e.g., Geneva Pharmaceuticals Technology Corp. v. Barr Labs. Inc., 386 F. 3d 485, 496-499 (2nd Cir. 2004)(considering whether generics constitute a separate market). The European Court of Justice has gone through this exercise. For example, the General Court of Justice investigated whether generics compete directly with branded products in the Perindopril (Servier) brought up by the European commission (Case AT.39612). Case T-691/14 123-40. The General Court assessed whether the same products were used for the same treatments. It also considered whether the market definition should also include drugs offering therapeutic treatment for similar ailment.

73.

For a discussion of the quick look rule see e.g., Garry A. Gabison, Juries Can Quick Look Too, 10 Seton

74.

Black’s Law Dictionary defines generic as “An item marketed with no brand name, trademark, or other distinguishing feature. Nothing separates it from other similar items except for its market name. Part of a certain general class, or genus, of items.”

75.

In his seminal paper, George A. Akerlof, The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism, 84

76.

White labeling or this “rebranding” could have dire consequences in many other settings. For example, a student would be accused of cheating for affixing their name on another student’s work. It would amount to fraud or misrepresentation. This would definite the signaling value of education (see e.g., Michael Spence, Job Market Signaling, 87

77.

See e.g., Tudor Nistorescu et al., Trademark vs Brand: A Conceptual Approach, 11

78.

Sondra Levine, The Origins of the Lanham Act, 19

79.

Mark P. McKenna, The Normative Foundations of Trademark Law, 82

80.

15 U.S. Code § 1052 (d).

81.

C-48/05.

82.

24.

83.

See e.g., Jacqueline K. Eastman et al., Status Consumption in Consumer Behavior: Scale Development and Validation, 7

84.

David Brainbridge, Intellectual Property, 534-35 (10th ed. 2018).

85.

See e.g., Shinichi Kitano et al., The Impact of Information Asymmetry on Animal Welfare-Friendly Consumption: Evidence From Milk Market in Japan, 191

86.

See e.g., Angela Giuffrida, Italians Urged to Boycott Amazon to Support Day of Strikes, ![]() (last accessed Mar. 9, 2022).

(last accessed Mar. 9, 2022).

87.

88.

See e.g., Matt O’Brien & Frank Bajak, Explainer: What Caused Amazon’s Outage? Will There Be More? ![]() (last accessed Feb. 14, 2022).

(last accessed Feb. 14, 2022).

89.

Id.

90.

Id.

91.

Id. at 274.

92.

Id. at 274-75.

93.

John Quelch and David Harding, Brands Versus Private Labels: Fighting to Win,

94.

See e.g., Nick Wilson et al., The Equity Gap and Knowledge-Based Firms, 50

95.

The horizontal elements of such arrange can lead to a violation of the antitrust laws. For example, in the e-book case, Apple (the hub) colluded with publishers (the spokes) to increase prices in the e-book market. See e.g., US v. Apple Inc., 952 F. Supp. 2d 638 (SDNY 2013).

96.

Commission Regulation (EU) 2022/720 of May 10, 2022 on the application of Article 101(3) of the Treaty on the Functioning of the European Union to categories of vertical agreements and concerted practices.

97.

Id. at Art. 3.

98.

Id. at Art. 4.

99.

(11)

100.

(12)

101.

Id.

102.

(13)

103.

(14)

104.

Pacific Bell Telephone v. Linkline Comm., 129 S. Ct. 1109, 1115 (2009).

105.

Id. at 1118.

106.

Id. at 1119.

107.

Id. at 1123 (stating that the plaintiffs “have not stated a duty-to-deal claim under Trinko and have not stated a predatory pricing claim under Brooke Group. They have nonetheless tried to join a wholesale claim that cannot succeed with a retail claim that cannot succeed, and alchemize them into a new form of antitrust liability never before recognized by this Court.”)

108.

See e.g., Gregory J. Sidak, Abolishing the Price Squeeze as a Theory of Antitrust Liability, 4

109.

In Konkurrensverket v. TeliaSonera Sverige AB, Case C-52/09 [2011] “A margin squeeze [. . .] is in itself capable of constituting an abuse within the meaning of Article 102 TFEU.”¶ 31.

110.

Deutsche Telekom AG v European Commission, Case C-280/08 P [2010] 142. See also, Case COMP/C-1/37.451, 37.578, 37.579 Deutsche Telekom [2003], affirmed in Case T-271/03 Deutsche Telekom AG v Commission of the European Communities [2008] ECR II-477 and Case C-280/08P Deutsche Telekom v European Commission [2010] ECR I-9555.

111.

For example, Kennedy argues that price squeeze in the United States should move away from a predatory pricing approach and align more with its EU cause of action. Kennedy argues that price squeeze should be reviewed under a quick look rule where the defendant would have an opportunity to rebut the antitrust presumption. Patrick Kennedy, Squeezing LinkLine: Rethinking Recoupment in Price Squeeze Cases, 57

112.

113.

114.

115.

116.

540 U.S. 398 (2004).

117.

Id. at 415.

118.

119.

Id. Art. 3.

120.

The obligations of gatekeepers are described in Art. 5-6 and the exemptions are described in Art. 9, which are limited to reasons of public interests: morality, healthy, and security.

121.

Art. 6 § (f) specifies that the gatekeeper must “allow business users and providers of ancillary services access to and interoperability with the same operating system, hardware or software features that are available or used in the provision by the gatekeeper of any ancillary services;”

123.

For a discussion of platform taxonomy, see e.g., Thomas Derave et al., Comparing Digital Platform Types in the Platform Economy,

124.

Similar to the Apple Pay case discussed above, the European Commission has found that Visa had restricted access to its platform to third party in case COMP/D1/37860 Morgan Stanley/Visa International and Visa Europe. In this case, Visa refused that Morgan Stanley issued Visa cards.

125.

For example, in Apple Inc. v. Pepper, 139 S. Ct. 1514 (2019) the US Supreme Court had to consider who were the direct purchasers (i.e., App consumers) on a marketplace platform like Apple’s App Store because Illinois Brick Co. v. Illinois, 431 US 720 (1977) established that only direct purchaser had standing. The Court decided that the iPhone purchasers had standing to sue but avoid the question of whether some other individuals (i.e., App producers) may have standing as well.

126.

138 S. Ct. 2274 (2018).

127.

Many of the findings in this decision are odd. For a more in-depth discussion of the case, see Garry A. Gabison, A Platform Paradox: Two Sides, Three Markets, 17

128.

T-111/08 (appeals on cases COMP/34.579 — MasterCard, COMP/36.518 — EuroCommerce, COMP/38.580 — Commercial Cards).

129.

Id. at 21.

130.

Id. at 23.

131.

Id. at 173-78.

132.

The European Commission made a similar case against Visa in Case AT.39398. Visa agreed to cap some of its fees as part of the case resolution in Decision C/2019/3034. MasterCard agreed to similar caps in Case AT.40049.

133.

For a discussion of rational expectation, see e.g., Ronald A. Heiner, Rational Expectations When Agents Imperfectly Use Information, 8 J

134.

Jean-Charles Rochet & Jean Tirole, Platform Competition in Two-Sided Markets, 1

135.

Id. at 992.

136.

A study by London Economics commissioned by the Financial Conduct Authority in 2014 found that the payment service found that the competition was limited in payment services and that incumbents had limited incentive to innovate. Paula Ramada & Patrice Muller, Competition and Collaboration in UK Payment Systems, ![]() (last accessed May 24, 2022).

(last accessed May 24, 2022).

137.

Philippe Aghion et al., Vertical Integration and Competition, 96

138.

Philippe Aghion et al., Competition and Innovation: An Inverted-U Relationship, 120

139.

See e.g., Srinivasan Balakrishnan & Birger Wernerfelt, Technical Change, Competition and Vertical Integration, 7

140.

For example, the Financial Conduction Authority has discussed as part of its competition mandate the need to consider the impact on innovation. Financial Conduct Authority, The FCA’s Approach to Advancing Its Objectives 2015, ![]() (last accessed May 23, 2021).

(last accessed May 23, 2021).

141.

15 U.S.C. § 1012.

142.

15 U.S.C. §§ 1011-1015.

143.

The exemption might also have limited competition—which we cannot know without a more complicated counterfactual. The Herfindahl-Hirschman Index (HHI) for the life insurance industry is around 300, whereas the HHI for car insurance is around 1300. This indicates that these industries are competitive. However, it is unclear whether competition would not improve if insurance companies were not exempt. Based on the author’s calculation, the HHI of the top 25 companies amounts to an HHI of 292 for a total market share of 71.56 percent of the premium collected in the United States for Life Insurance as reported by the National Association of Insurance Commissioners. So, the maximum HHI for life insurance would be around 332. National Association of Insurance Commissioners, Life and Fraternal Insurance Industry, 2021 Top 25 Groups and Companies by Countrywide Premium, NAIC.ORG (2022), ![]() (last accessed May 23, 2022). Based on the author’s calculation, the HHI of the top 25 companies amount to an HHI of 1284 for a total market share of 90.37 percent of the premium collected in the United States for Life Insurance as reported by the National Association of Insurance Commissioners. So, the maximum HHI for life insurance would be around 1294. National Association of Insurance Commissioners, Life and Fraternal Insurance Industry, 2021 Top 25 Groups And Companies By Countrywide Premium.

(last accessed May 23, 2022). Based on the author’s calculation, the HHI of the top 25 companies amount to an HHI of 1284 for a total market share of 90.37 percent of the premium collected in the United States for Life Insurance as reported by the National Association of Insurance Commissioners. So, the maximum HHI for life insurance would be around 1294. National Association of Insurance Commissioners, Life and Fraternal Insurance Industry, 2021 Top 25 Groups And Companies By Countrywide Premium.

145.

146.

147.

Many other FinTech companies have innovated in a way that increased competition. Some other FinTech companies have focused on other insurance market failures such as the barrier to entry linked to necessary funds. For example, PremFina is a FinTech start-up founded in 2015 that provides software and financing for insurance brokers. PremFina, ![]() (last accessed Nov. 12, 2021). So, this FinTech company allows brokers to compete with the underwriting insurance companies (or wholesalers) and to defeat the budget constraint of brokers. PremFina is not the white labeler but enables white labelling: different brokers could be offering the same insurance product from a white label underwriter at different prices. PremFina provides matching services between brokers and underwriters. This innovation decreases transaction costs. Insurance underwriters are often also players in the insurance retail market; so, they compete with the brokers. Because the underwriters operate at the wholesale and retail levels, this dual distribution business model also raises issues discussed above and can affect PremFina’s business model because PremFina is at the mercy of these upstream or downstream companies.

(last accessed Nov. 12, 2021). So, this FinTech company allows brokers to compete with the underwriting insurance companies (or wholesalers) and to defeat the budget constraint of brokers. PremFina is not the white labeler but enables white labelling: different brokers could be offering the same insurance product from a white label underwriter at different prices. PremFina provides matching services between brokers and underwriters. This innovation decreases transaction costs. Insurance underwriters are often also players in the insurance retail market; so, they compete with the brokers. Because the underwriters operate at the wholesale and retail levels, this dual distribution business model also raises issues discussed above and can affect PremFina’s business model because PremFina is at the mercy of these upstream or downstream companies.

148.

Article 1 § 2 of Council Regulation (EC) No 139/2004 of January 20, 2004 on the control of concentrations between undertakings (the EC Merger Regulation). For simplicity, I do not discuss Article 1 § 3 where companies must file a notification of merger if their turnover exceed €2.5 billion, if the merging parties have combined turnover of €100 million in at least three Member States, and the turnover of at least two entities exceed €25 million in at least three Member States.

149.

Jingmeng Cai, The Sharing Economy and China’s Antimonopoly Law: from the Didi Case to Regulatory Challenges, 28

150.

Fengliang Jin, The Challenges of Applying Turnover Threshold to the Sharing Economy for Control of Concentrations Between Undertakings in China, 35

151.

153.

As reported in FAME - Bureau Van Dijk database.

154.

155.

156.

157.

158.

159.

160.

Colleen Cunningham et al., Killer Acquisitions, 129

161.

162.

Id. at II.268.

163.

While this merger did not involve European-based companies, the turnover of Plaid would have been below the European Commission notification threshold: “Plaid’s revenues have been growing rapidly and were almost $100 million in 2019.” US v. Visa Inc. & Plaid Inc., Case 3:20-cv-07810 Complaint, 7 (May 22, 2020), ![]() (last accessed Mar. 4, 2022).

(last accessed Mar. 4, 2022).

164.

Id. at 11.

166.

Ioannis Kokkoris, A Practical Application of Event Studies in Merger Assessment: Successes and Failures, 3

167.

The American Antitrust Institute estimated that each of Amazon, Apple, Google, Facebook, and Microsoft acquired an average over 100 companies since 2010. Diana Moss & David Hummel, Anticipating the Next Generation of Powerful Digital Players: Implications for Competition Policy, ![]() (last accessed May 26, 2022).

(last accessed May 26, 2022).

168.

Visa has a long history of acquiring or investing into FinTech. Visa has acquired 15 FinTech companies. According to CrunchBase, Visa acquired: Cybersource in 2010; Fundamo and PlaySpan in 2011; TrialPay and Visa Europe in 2015; Cardinal in 2016; Fraedom and Earthport in 2018; Bell ID, Rambus, Verifi, Payworks in 2019; YellowPepper in 2020; and Currencycloud and Tink in 2021. It also invested in 78 start-ups during the same period.

169.

See e.g., Rosa M. Abrantes-Metz & D. Daniel Sokol, The Lessons from Libor for Detection and Deterrence of Cartel Wrongdoing, 3

170.

For example, consumers often pay too much attention to brands that differentiate homogenous services—instead of the underlying services. Richard Schmalensee, Product Differentiation Advantages of Pioneering Brands, 72 ![]() (last accessed May 23, 2021).

(last accessed May 23, 2021).

171.

Many FinTech business models (e.g., e-payment system) have many parallels with other digital markets like search engines or social media. Specifically, these business models rely on network effects and feedback loops. Thus, they have raised issues that companies “compete for the market” instead of “in the market”. See e.g., Ramada & Muller, supra note 136, at 11-16.