Abstract

This article reflects on the way in which the new initiatives to regulate powerful online platforms in the European Union, the United States, the United Kingdom, and Germany challenge well-established fundamentals of modern antitrust and thereby reshape the future of competition law. It shows that the new platform regulations set in motion a profound transformation of modern antitrust law that operates along four parameters. First, the new platform regulations unsettle the long-standing baseline assumption that the maximization of consumer welfare constitutes competition law’s core mission. Second, the new instruments repudiate the orthodox understanding of error costs that advocates under-enforcement as the optimal standard of intervention in innovation-driven markets. Third, by relying primarily on rule-like presumptions as legal commands to regulate digital competition, the new platform regulations reverse the trend toward an increasingly inductive mode of analysis that characterized modern antitrust under the “more economic” or “effects-based” approach. Fourth, the new platform regulations also fundamentally diverge from a purely probabilistic standard of proof which requires the showing that impugned conduct is more likely than not to cause anticompetitive harm. The reconfiguration of modern antitrust along these four vectors, the article concludes, foreshadows a new, more inclusive model of innovation and growth in digital markets.

Keywords

I. Introduction

Antitrust law is set to undergo a period of tectonic shifts as policymakers in Europe and the United States are rushing toward the adoption of new regulations to tame the unprecedented economic power of digital platforms (hereinafter “new platform regulations”). While the current antitrust debate focuses primarily on the specific substantive and procedural rules, as well as the institutional design of these new regulatory tools, this contribution takes a slightly different, at the same time forward- and backward-looking angle. It approaches the new platform regulations not only as the heralds of a new era in antitrust law. Rather, as these new platform regulations considerably depart from the status quo of conventional antitrust enforcement, they also constitute a mirror that throws into relief and, thereby, allows us to better understand the basic economic and normative predispositions that shaped modern antitrust law over the last four decades. In unpacking how the new platform regulations reconfigure these predispositions, the article inquires into the broader implications that the new platform regulations may entail for the future of antitrust law. The paper argues that these new initiatives to regulate digital competition mark a “paradigm adjustment” of modern antitrust along four fault lines.

First, being geared toward promoting fairness, contestability, and non-economic values such as privacy, the new platform regulations openly reject the long-standing dogma that consumer welfare constitutes the only rational and legitimate goal of competition law. Instead, they emphasize that the protection of competition, as the key mission of competition law, extends beyond promoting consumer welfare and is capable of embracing other values.

Second, the new platform regulations also challenge the conventional wisdom that false positives of competition law enforcement are more costly than false negatives. Instead, the new platform regulations embody a recalibration of the error-cost framework which recognizes that the probability and magnitude of anticompetitive harm in digital markets may be greater than usually assumed by conventional antitrust literature.

Third, this recalibration of the error-cost framework becomes apparent in the reliance of the new platform regulations on a broad set of ex ante rules that introduce presumptions of illegality for specific types of platform conduct. By forging rule-like legal presumptions as legal commands to regulate the conduct of digital platforms, the new regulations depart from the “effects-based” analysis as the default mode of assessment of the “more economic approach.” Instead of endorsing an inductive case-by-case approach, the new platform regulations highlight the value of economically informed rebuttable presumptions in antitrust analysis.

A fourth distinctive feature of the new platform regulations that also reflects the recalibration of the conventional error-cost framework is their recourse to a probabilistically de-weighted or bounded standard of proof. Instead of requiring the showing of actual or likely anticompetitive effects, the new platform regulations compel antitrust intervention on the mere basis that specific forms of conduct by powerful platforms may result in potential anticompetitive harm of significant scale. This bounded probabilism of the new platform regulations thus marks an important departure from the increasing trend in conventional antitrust analysis to make the finding of unlawful conduct conditional on the showing that anticompetitive effects are more likely than not.

Against the backdrop of this recalibration of the goals, error-cost framework, legal commands, and standard of proof, the article concludes that the new platform regulations epitomize a fundamental rethink of innovation in digital markets. In fact, the new platform regulations openly discard the Schumpeterian conception of innovation that has shaped mainstream antitrust enforcement in dynamic, high-tech markets. Instead of being concerned about the ability of large-scale incumbents to appropriate and recoup their investments in the development of innovative technology, products, and services, the new platform regulations aim to ensure market openness and contestability and preserve smaller business users’ and rivals’ sunk investments in digital innovation.

To illustrate how the new platform regulations disrupt and evolve competition law in readjusting the predispositions of modern antitrust, the remainder of the paper is organized as follows. Section II provides an overview of the new regulations adopted or currently discussed in Germany, the European Union (E.U.), the United Kingdom (U.K.), and the United States (U.S.) to reign in the economic power of digital platforms. Section III describes how the new platform regulations depart from the conventional, monolithic, and consumer welfare-based understanding of competition law which assumes that the ultimate mission of competition law consists of securing that consumers get a better deal in terms of lower prices, greater quality, new products, or broader choice. Section IV traces how the new platform regulations bring about a recalibration of the conventional error-cost framework of antitrust law. Section V shows how this recalibration of the error-cost framework feeds through into the reliance of the new platform regulations on form-based, rebuttable presumptions. Section VI sheds light on how the recalibration of the error-cost framework translates into a lowered, probabilistically de-weighted or bounded standard of proof. Section VII concludes in putting this evolution into a broader context by exploring how the new platform regulations foreshadow a new model of digital innovation and growth.

II. The New Platform Regulations—An Overview

Over the last years, experts and policy makers across the world have pondered over how competition law could be reformed to tackle the challenges that the rise of digital markets poses to competition law. This process culminated in the adoption of the 10th amendment of the Competition Act in Germany, 1 as well as the proposals of a Digital Markets Act (DMA) in the E.U., 2 a New Pro-Competition Regime for Digital Markets (“SMS regime”) in the U.K., 3 and several legislative bills in the U.S.. 4 All initiatives have as their common aim to address growing concerns over the increasingly entrenched economic power that a handful of powerful digital platforms have amassed over the last decade.

A. The Entry-Point: The Designation of Platforms with Entrenched Substantial Market Power

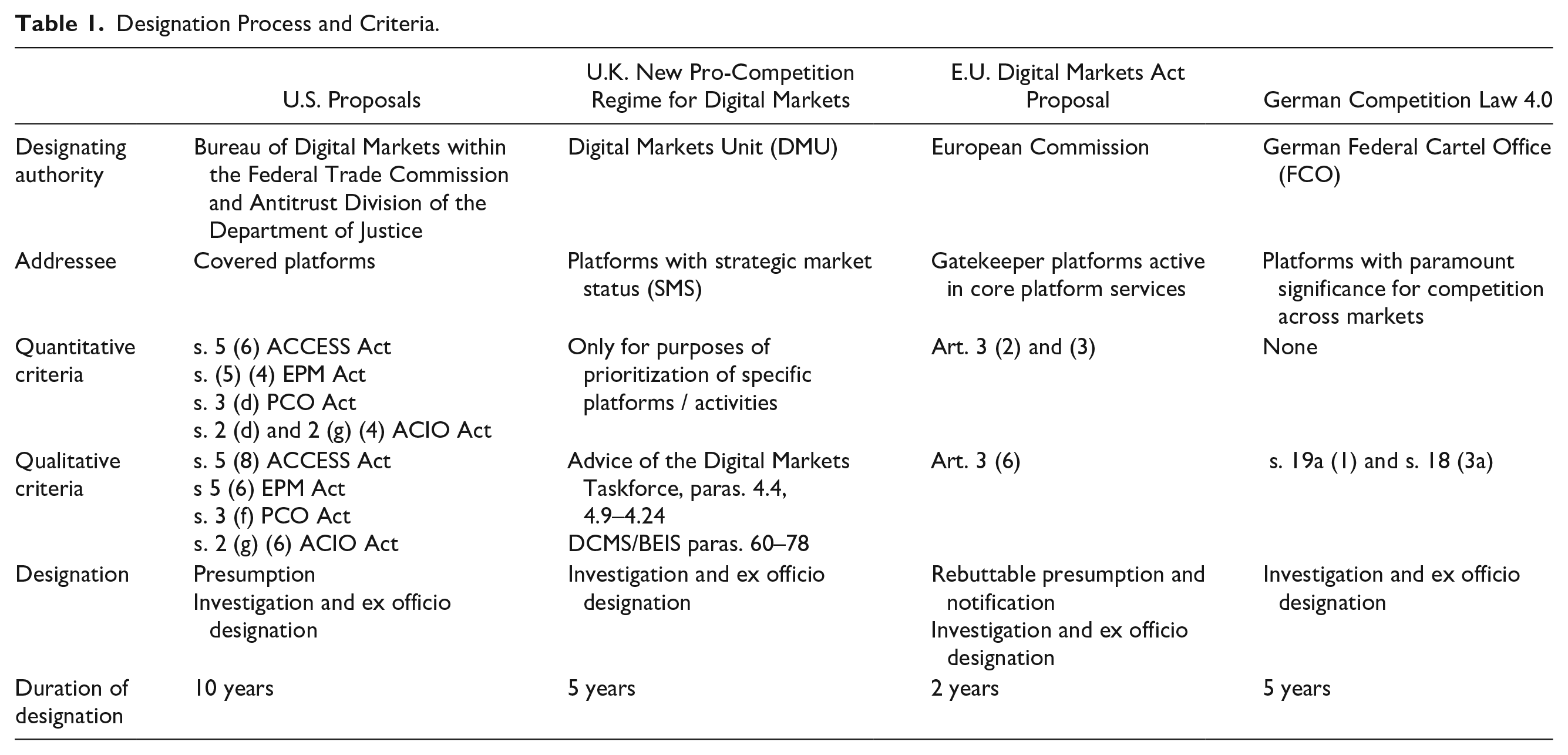

Although these new platform regulations come along in different forms and shapes, 5 they have many features in common. All new instruments revolve around a designation process that ensures that the new platform regulations only apply to the most powerful digital platforms (see Table 1). Depending on the jurisdiction at hand, these regulated platforms are referred to as “gatekeeper” platforms, 6 platforms with “strategic market status” (SMS), 7 “covered platform,” 8 or “multi-sided platforms and networks holding a position of paramount significance for competition across markets.” 9 In terms of their material scope, the new regulations apply to sectors or activities for which digital technology constitutes a core element of their functioning and business model. Whereas some of the new regulations only require that the regulated platforms be active in loosely defined digital markets or sectors, 10 others exclusively apply to platforms that operate a specific subset of clearly delineated digital activities. 11

Designation Process and Criteria.

The designation of regulated platforms proceeds through two main channels. Regulated platforms are designated

either on the basis of specific quantitative thresholds—such as annual turnover, number of end users and business users, market capitalization—that provide proxies for their size, competitive impact, and market power;

or based on qualitative criteria—such as entry barriers, network effects, barriers to switching, dominance—which are indicative of their substantial and enduring market power.

Some jurisdictions, such as the E.U. and the U.S., rely on a combination of both quantitative and qualitative scoping criteria. The U.K. and Germany only use qualitative criteria to designate regulated platforms. Whereas in Germany and the U.K. platforms are called in by competition authorities/regulators ex officio after a case-specific analysis, the quantitative criteria in the E.U. DMA trigger a rebuttable presumption that a platform holds gatekeeper status. 12 Accordingly, a provider of a core platform service that meets the quantitative thresholds set out in the DMA is presumed to qualify as a designated platform and must notify the Commission about its status, unless it puts forward countervailing evidence showing that it does not possess gatekeeper power. 13 The U.S. proposals provide for a similar presumption for platforms that meet the primarily quantitative designation criteria. 14 Designated platforms are subject to the new platform regulations for a duration between 2 (E.U.), 5 (Germany and the U.K), and 10 (the U.S.) years.

The designation process of platforms under the new platform regulations importantly differs from traditional antitrust analysis in two respects. First, although the designation process requires competition authorities to identify specific industries in which the platforms are active, they are no longer under a formal obligation to define relevant antitrust markets. Second, while the scoping criteria are geared toward identifying platforms with substantial and enduring market power, competition authorities no longer need to make any formal finding that the platforms hold a dominant or monopoly position. Though there might be an overlap between the status of designated platforms and dominance/monopoly power, they do not always have to be congruent. This becomes, for instance, apparent in the fact that the DMA and the German Competition Law 4.0 also apply to platforms that have not yet reached a dominant position. 15 This extension of the regulation of unilateral conduct beyond dominance/monopoly power is testament to the growing concern that the traditional concepts of “dominance” or “monopoly” fail to account for the fact that digital platforms may wield important “intermediation power” allowing them to harm competition, even though they do not hold a dominant position in a clearly defined relevant product market. 16

B. Ex Ante Conduct and Merger Rules

A second common feature of the new platform regulations is that they subject designated platforms to a broad set of ex ante rules and obligations. The peculiarity of these rules is that they are—at least to a certain degree—self-executing. This means that these rules are designed in a way that reduces the need for any further specification to a minimum. Instead, most of the ex ante rules are directly applicable and binding on the designated platforms.

The specific content and design of the ex ante rules differ across the various new instruments. Whereas the E.U., U.S., and German platform regulations crafted a set of ex ante rules that apply to all designated platforms across the board, the new U.K. regime for SMS platforms envisages a more bespoke approach that lays down legally binding codes of conduct for individual designated platforms. These codes blend some ex ante rules that apply to all designated platforms with more tailored rules that are negotiated with the designated platforms on an individual basis. 17

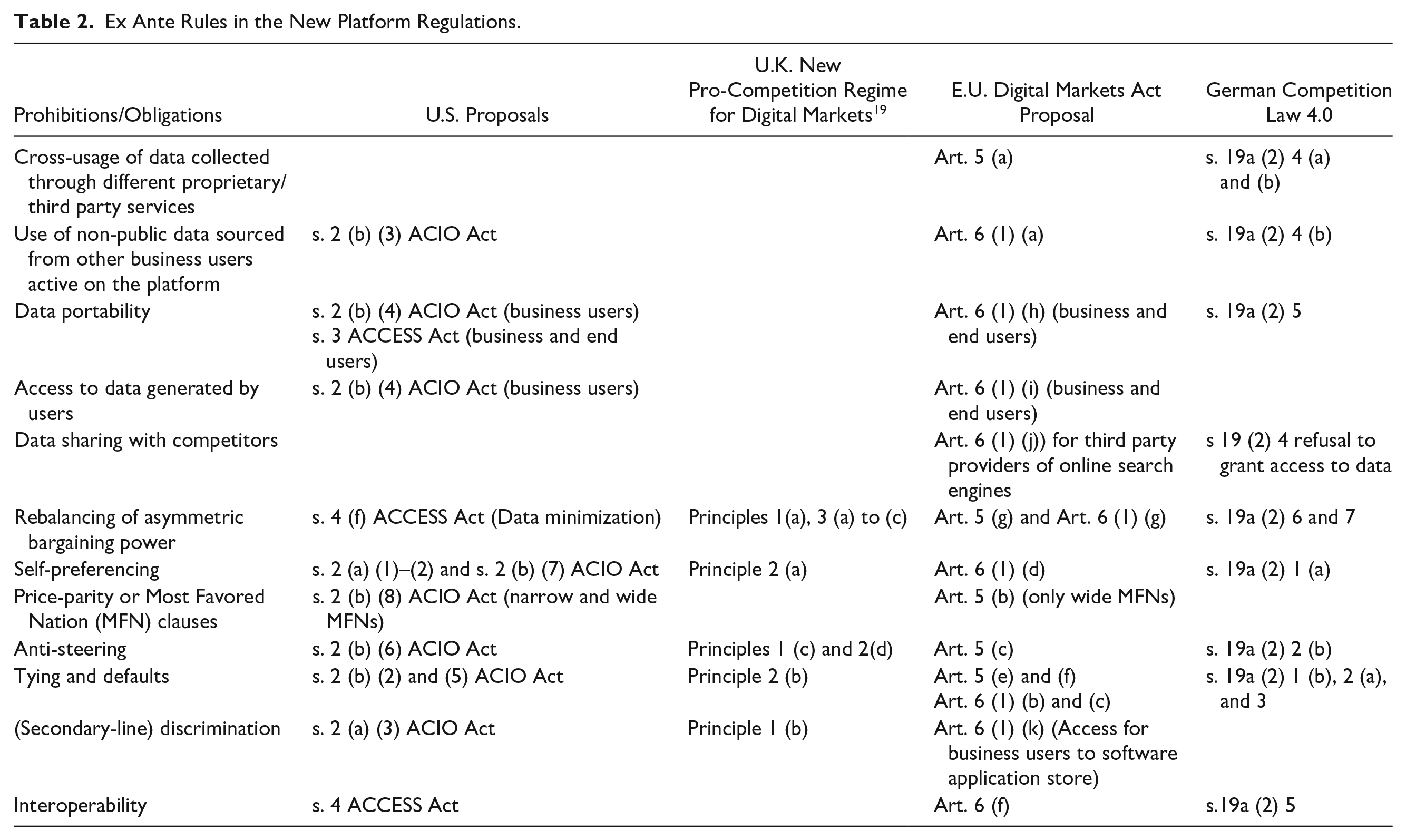

Despite these differences in their design, all platform regulations share a preventative approach in so far as they seek to bar designated platforms from engaging in certain forms of conduct by outlawing them ex ante. There is also some considerable overlap in terms of the substantive content of these ex ante rules across the different platform regulations (see Table 2):

Data: All platform regulations provide for rules that regulate the extent to which regulated platforms can make use of and must provide third-party access to data. Most platform regulations restrict the ways in which designated platforms can combine data sourced from their different services or make use of non-public data of business users to gain a competitive edge over the latter. They also contain obligations to enable and/or prohibitions to impede data portability for end users and/or business users. Moreover, they mandate designated platforms to ensure that business users can access data generated by them or their end users on the platform. The DMA even goes one step further by imposing an obligation on gatekeeper platforms operating search engines to give competing search engine operators access to their data. 18

Interoperability and switching: Prohibitions to restrict and obligations to ensure interoperability between the designated platform’s products or services and the products and services provided by third parties are also present in all new platform regulations. Furthermore, the new platform regulations lay down rules that promote switching and multi-homing.

Tying: Designated platforms are also prohibited from using contractual or technical ties, and in certain circumstances default settings, to give their own service a competitive edge over those of competing third parties.

Self-preferencing: All new platform regulations outlaw self-preferencing of different sorts, whereby a vertically integrated platform affords preferential treatment, visibility, or ranking to its own services, while placing competing rivals at a competitive disadvantage.

Discrimination: Other forms of discrimination against third-party business users are also addressed by most platform regulations. Designated platforms thus are—at least to a certain degree—subject to a public-utility like obligation to guarantee fair, reasonable and non-discriminatory access to third parties on their platforms. Whereas the E.U., U.K., and German regulations translate this non-discrimination principle primarily through narrowly defined prohibitions and obligations, the U.S. proposals also stipulate broadly phrased general prohibitions of discriminatory conduct. 20

Anti-steering provisions and Most Favored Nation (MFN) clauses: A majority of the new platform regulations also prohibit contractual or technical anti-steering provisions and, albeit to a lesser extent, wide and narrow MFN clauses. They thereby seek to prevent designated platforms from restricing the ability of third-party business users to reach end users through alternative sales channels.

Bargaining power: In addition, most new platform regulations also contain a number of rules that seek to address the bargaining power of designated platforms, for instance, by promoting greater price and service transparency for business and end users, notably in opaque markets such as the online advertising sector. 21

Ex Ante Rules in the New Platform Regulations.

Unlike in regular antitrust cases, designated platforms have only limited possibilities to obtain an exemption from or justify violations of these obligations. The U.S. proposals, DMA proposal, and German Competition Law 4.0 do not provide for any explicit efficiency defense. Instead, designated platforms can only advance a narrowly construed “affirmative defense,” 22 “objective justifications,” 23 “economic viability,” 24 or “public policy” 25 grounds to excuse any non-compliance with the newly designed rules. Only the U.K. framework explicitly recognizes the possibility for firms to plead an efficiency defense to excuse conduct that otherwise violates the code of conduct. 26

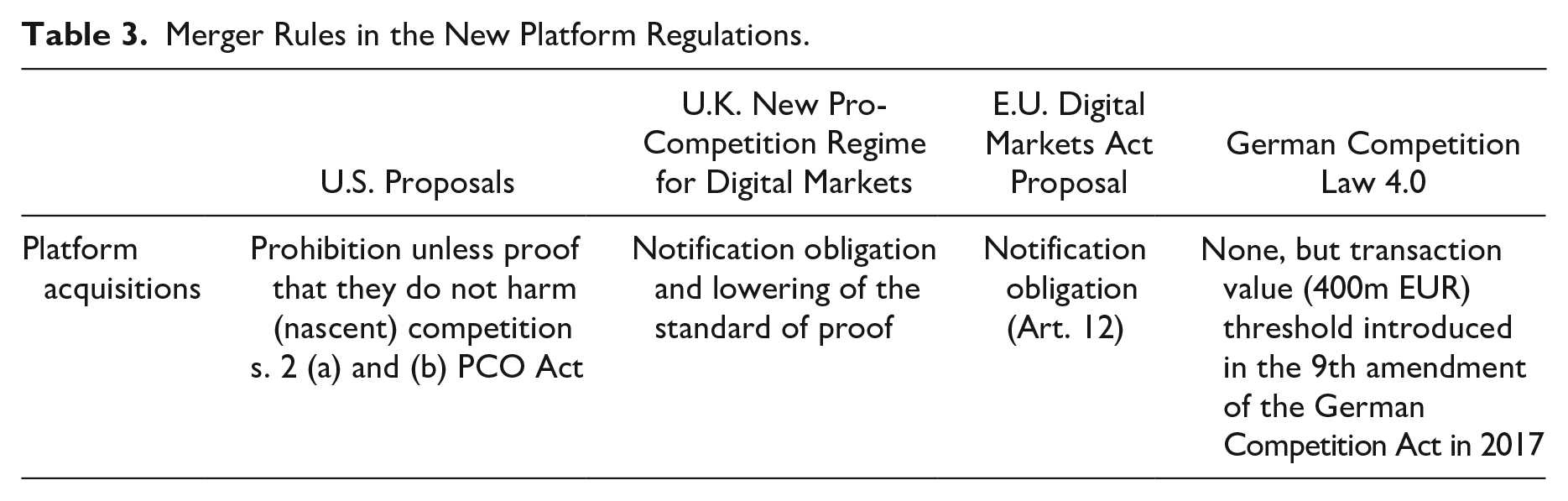

Alongside ex ante rules relating to unilateral conduct of powerful platforms, new platform regulations also contain provisions that seek to empower competition authorities to scrutinize start-up acquisitions by powerful platforms (see Table 3). While the DMA only imposes a new obligation on gatekeeper platforms to notify any acquisition to the European Commission, 27 the new U.K. SMS regime also envisages a lowering of the standard of proof for the competitive assessment of mergers by designated digital platforms. When reviewing acquisitions by platforms with SMS status in phase II, the Competition and Markets Authority (CMA) would no longer have to establish that the merger will lead on a “balance of probabilities” to a substantial lessening of competition (SLC) as is the case for regular mergers. Instead, it could rely on the lower “realistic prospect” standard, normally reserved for the phase I assessment of mergers. Unter this lower standard, it only needs to demonstrate that the merger gives rise to a realistic prospect of a SLC. 28

Merger Rules in the New Platform Regulations.

The U.S. proposals go even further in altering the assessment of mergers by powerful digital platforms. They envisage a presumption of unlawfulness against acquisitions by designated platforms. Under the new platform rules, designated platforms will be prohibited from acquiring other firms unless they advance “clear and convincing evidence” showing that the merger would not adversely affect competition. 29

The German Competition Law 4.0 does not provide for specific rules on start-up acquisitions. However, already back in 2017, the 9th Amendment to the German Competition Act had introduced a new transaction value threshold (s. 35(1a) 3) to enable the Federal Cartel Office to review start-up acquisitions that otherwise would fly under the radar of the jurisdictional turnover thresholds. 30

C. New Enforcement Tools

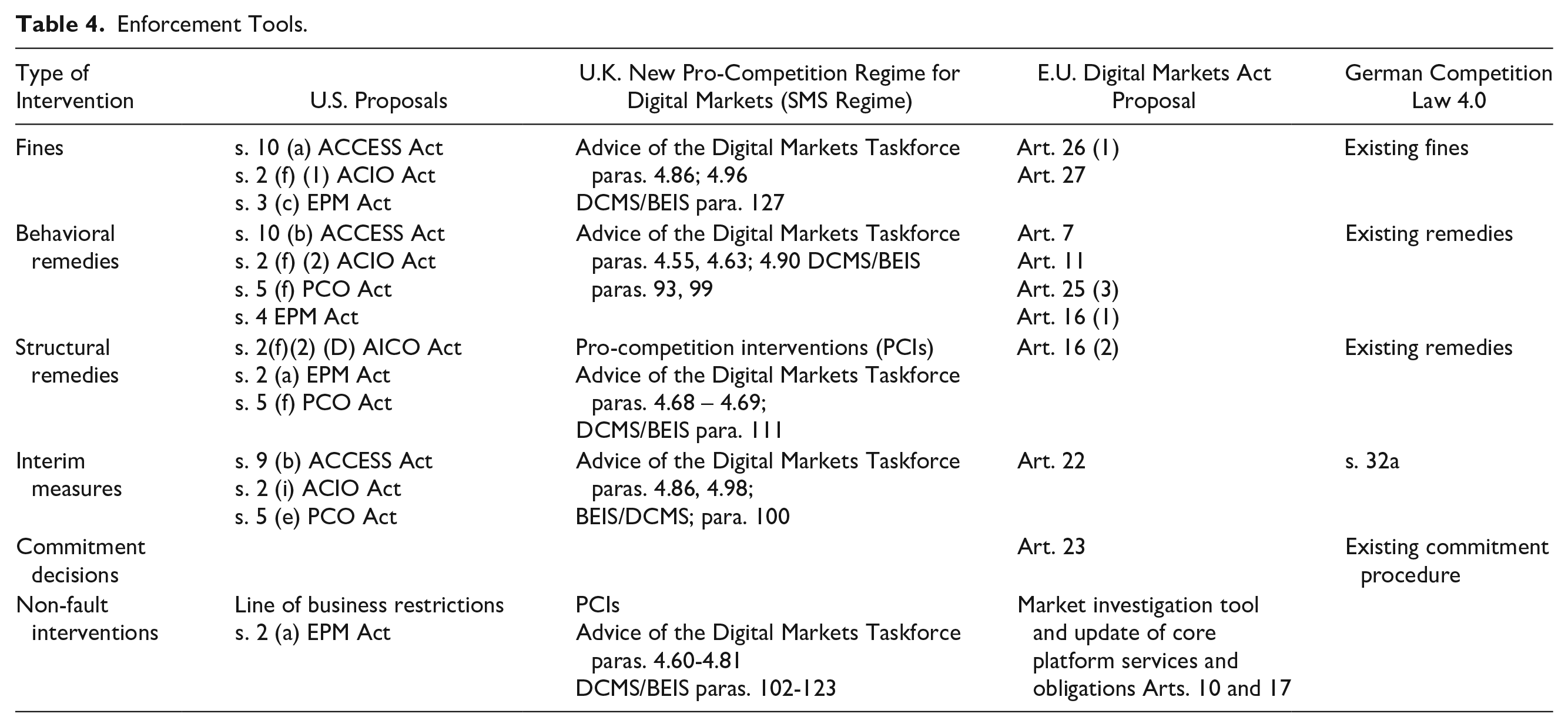

A third feature which all new platform regulations have in common is that they empower competition authorities with a broad range of enforcement tools and remedies to ensure compliance with the new obligations and enhance competition in digital markets (Table 4). All platform regulations provide for interim or emergency relief measures aimed at speeding up enforcement in digital markets. In the event of non-compliance, designated platforms will face substantial fines. The self-executing nature of most prohibitions and rules in the new platform regulations also entails that they clearly indicate a specific behavioral remedy that platforms have to adopt in order to bring an infringement to an end. Alongside behavioral remedies, the new platform regulations also provide for a broad range of structural remedies. They, however, differ in the way in which they blend and escalate these different remedies.

Enforcement Tools.

The U.S. proposals, for instance, go as far as envisaging lines of business restrictions that prohibit platforms from operating lines of business through which they provide services or sell goods via their platform. Designated platforms may also be required to divest existing lines of business if they create conflicts of interest. These structural remedies may apply to designated platforms even in the absence of any concrete breach of the new platform regulations. The U.S. proposals thus create a non-fault antitrust liability for designated platforms that exposes them to structural interventions in markets whose characteristics make systemic competition issues more likely. 31

The U.K. SMS framework also introduces a similar non-fault liability regime for designated digital platforms. The SMS regime, on one hand, provides for the imposition of remedies to address non-compliance with the new codes of conduct. On the other, it also empowers the newly created Digital Markets Unit (DMU) to adopt pro-competition interventions (PCIs) that impose behavioral and structural remedies on designated platforms with a view to enhancing the contestability of digital markets. These PCIs can be mandated regardless of whether a SMS platform has breached its code of conduct. Instead, they are explicitly aimed at eliminating the root causes of the entrenched market power of SMS platforms. 32

Similarly, the DMA proposal gives the Commission at hand a new market investigation tool which empowers it to go beyond the enforcement of the rules and obligations laid down in the DMA. Instead, the Commission can use the market investigation tool to identify new digital sectors in which markets are not sufficiently contestable or determine new practices that unfairly hinder competition or dampen contestability. 33 These markets or practices can then be added to the list of “core platform services” regulated 34 and of blacklisted practices outlawed by the DMA. 35 In a similar vein as the non-fault liability regimes in the U.S. and U.K. proposals, the market investigation tool enables the Commission to intervene in markets and impose obligations on digital platforms that are not geared toward remedying specific breaches of existing competition and platform rules but—in their final consequence—seek to reduce entrenched market concentration as such.

In sum, the new platform regulations in Germany, the E.U., the U.K., and the U.S. bring about a fundamental reconfiguration of the regulation of competition in the digital economy. Despite some differences in their institutional and substantive design, all regulatory initiatives display a number of common features (Tables 1 to 4). In terms of material scope, all four have in common that they apply to multi-sided platforms in digital markets. For a digital platform to fall within the scope of the new regulations it has to hold some form of durable, significant market power with respect to digital markets that play a crucial role as access points for businesses to reach end consumers. Platforms with substantial and durable market power will be identified on the basis of quantitative (E.U., the U.S.) and qualitative (Germany, E.U., the U.S., the U.K.) factors. Competition authorities are, however, under no obligation to define standard antitrust markets to determine the market power of digital platforms. Moreover, platforms may become subject to the new regulatory framework even if their market power falls short of conventional dominance or monopolization thresholds. All four new platform regulations also have in common that they lay down a number of ex ante rules that prohibit specific forms of conduct deemed to undermine the contestability of digital markets and/or amount to unfair conduct toward business or end users. Most new platform regulations also strengthen the ability of competition authorities to scrutinize mergers by designated platforms. Beyond that, the new frameworks confer upon competition authorities far-reaching powers to ensure compliance with these newly created rules and intervene in digital markets without finding concrete unlawful behavior.

D. The Economic Rationale Underpinning the New Platform Regulations

This reconfiguration of competition law envisaged by the new platform regulations in Germany, the E.U., the U.K., and the U.S. constitutes in the first place a response to the specific features of digital markets. The most distinctive characteristic of these markets is the presence of firms that operate multi-sided online platforms. The business model of these multi-sided platforms consists of reducing transaction costs by bringing together and matching the supply and demand of end user and business user groups which value each other. 36 Owing to the importance of multi-sided platforms acting as intermediaries between different customer groups, digital markets are characterized by significant direct and indirect network effects. 37 The direct and (cross-platform) indirect network effects are further compounded by the role data play in the business model of online platforms. 38 As the ability of a platform to collect data and optimize its intermediation services increases with the size of its end user base, data tend to further reinforce the direct and indirect network effects on both sides of the platform. The role of data thus amplifies already existing direct and indirect network effects because access to a broad scale and scope of data enables platforms to offer better targeted and more bespoke products and services to end and business users.

This prevalence of direct, indirect, as well as data-driven network effects has three implications for competition in digital markets. First, digital markets are often characterized by extreme economies of and returns on scale and scope. In order to be attractive for business and end users and be able to compete effectively, new platform entrants must achieve a minimum efficient scale in terms of the size and scope of their customer base, data sets, and network effects. User- and data-driven network effects thus often constitute important barriers to entry for new platform competitors. Digital markets may, therefore, only accommodate a limited number of players large enough to operate at a minimum efficient scale. 39 Second, data- and non-data-driven network effects may generate important lock-in effects if they make it more costly for end and business users to switch to competing platforms. This is particularly the case if network-effects-driven switching costs limit or prevent multi-homing. 40 Third, by virtue of the important role of network and lock-in effects, digital markets may reach a point where the entire demand “tips” toward a single winner that attracts so many users that it will virtually become the sole viable system in the market. A player who succeeds in achieving scale and harnessing network effects may thus be able to tilt the market on a lasting basis in its favor. 41 The market position of the successful survivor of this “winner takes most” competition is often difficult to challenge and dislodge by new entrants or residual competitors. The combined effect of these extreme economies of scale and scope, network effects, and market tipping is an important driver of market concentration and decreasing contestability of digital markets. Numerous digital markets are, therefore, showing signs of increasing consolidation and concentration of economic power in the hands of a few large-scale incumbents who managed to entrench their market position.

A third distinctive feature of digital markets is the prevalence of vertical integration and the emergence of conglomerate “ecosystems.” 42 Many digital platforms integrate vertically or “diagonally” by providing up-stream, down-stream, or complementary services and expanding their presence into neighboring markets. As a consequence, digital platforms often rely on a hybrid business model. 43 On one hand, they operate a marketplace facilitating the interaction between business users and end users. In providing this marketplace function, digital platforms control an important “input” or “bottleneck” 44 that business users have to access to reach end users. On the other hand, digital platforms often also operate a “sales function” through which they distribute their own complementary products or services on their marketplace. 45

These three structural features of digital markets—namely, the (1) importance of multi-sided intermediary platforms, the (2) prevalence of extreme economies of scale and scope, network effects and market tipping, and (3) the presence of vertical/diagonal integration—importantly shape the incentives of incumbent digital platforms both with respect to their horizontal relationship with other (competing) platforms and with respect to their non-horizontal relationship with business users.

When it comes to the horizontal relationship between platforms, the importance of extreme returns to scale and scope and network effects increases the incentives of incumbent digital platforms to tip markets on a lasting or even irreversible basis. Once a market has pivoted in its favor, a digital platform can entrench its market power and generate monopoly profits through various monetization channels without having to fear that it will be challenged by new or competing platforms. The propensity of digital markets to tip also heightens the incentive of incumbents to defend their entrenched market position by nipping competitive threats of nascent platforms or entrants in the bud. The payoffs that an incumbent who successfully unlevels the market in its favor derives from securing a lasting monopoly position oftentimes exceed those for competitors to enter. Due to these “asymmetric stakes,” an incumbent platform may indeed be inclined to to spend more (or to sacrifice more profits) to insulate its monopoly profits from potential competition than competitors or entrants may be willing to invest in order to remain operational or achieve a viable competitive position. 46 Incumbent platforms may therefore have a heightened incentive to eliminate horizontal competitors or competitive threats by engaging in exclusionary conduct or acquiring them.

In terms of the vertical relationship between platforms and business users, the hybrid business model of operating a “marketplace” and “sales function” often exposes digital platforms to a conflict of interest. Hybrid platforms provide business users with an important input, while at the same time competing with them downstream in selling complements to end users. Digital platforms thus face a continuous trade-off between wholesale profits that they earn by charging business users for their marketplace function and the cannibalization of the margins of their retail sales function. 47 On one hand, the more business users they serve with intermediary services, the higher their wholesale profits (wholesale margin effect). On the other hand, the more business users populate their platforms, the greater the downstream competition that “cannibalises” the profitability of their retail sales function (cannibalization effect). If the cannibalization effect outweighs the wholesale margin effect, platforms have an incentive to raise business users’ (i.e., their downstream rivals’) costs, for instance, by designing the rules of their market function in a way which places competing business users at a disadvantage or by leveraging their market power from the marketplace into the sales function.

These horizontal and vertical effects do not operate in isolation but often interact and reinforce each other. The various platform regulations adopted or currently envisaged by policy makers across the globe seek to address and channel the complex incentive structure of digital platforms shaped by the three effects outlined above. All types of ex ante rules and interventions foreseen in the German, E.U., U.K., and U.S. frameworks for platforms can be categorized as either (1) seeking to preserve or inject horizontal inter-platform competition and advance contestability, or (2) guarantee intra-platform competition by protecting business users or end users which are dependent on a platform’s marketplace function from opportunistic behavior, or (3) both. The regulatory rationale of the new platform regulations thus mirrors the multi-dimensional harms that may derive from the horizontal and vertical incentive structure digital platforms are subject to. On one hand, by promoting contestability the platform regulations seek primarily to reduce structural factors that facilitate the entrenchment of incumbents’ market power and mute their incentives to impair horizontal competition by foreclosing or acquiring competitors. On the other, by ensuring fairness and equality of opportunity, the platform regulations seek to reduce the vertical competition issues arising from the hybrid role of integrated platforms that operate a simultaneous marketplace and sales function. To this end, the various platform regulations lay down a number of—primarily negative—obligations that are geared toward tempering the incentives of platforms to raise the costs of business users that act as third-party sellers competing with their own sales function on their platform.

III. Goals Reconsidered

The fact that the new platform regulations pursue the goals of enhancing contestability and fairness is a first point in which they radically divert from the baseline approach of modern antitrust. The new platform regulations indeed depart from the fundamental prior of modern antitrust that competition law has as its primary or even exclusive mission the enhancement of consumer welfare in the form of lower prices, greater choice, quality, or innovation. 48

A. The Multi-Value Approach of the New Platform Regulations

Instead of focusing on consumer welfare as their primary or exclusive goal, the new platform regulations identify several policy goals. By way of example, the proposed DMA pursues the twin goal of ensuring the contestability 49 of digital markets and fairness and equality of opportunity 50 by reducing “significant dependencies” 51 of business users on powerful platforms and redressing power imbalances. 52 Along similar lines, the U.S. proposals pursue the goal of enhancing fairness, 53 business opportunities, 54 choice, and innovation 55 in digital markets. The U.K. framework, too, deviates from a purely consumer welfare approach, as it seeks to address the adverse economic but also societal implications of the accumulation of market power by a small number of large-scale platforms. 56 The objectives of limiting and securing the contestability of economic power of digital platforms and at the same time guaranteeing fair and equal competitive opportunities for rivals and business users who are dependent on platform services also lie at the heart of the new German Competition Law 4.0. 57

The prominent role of contestability and fairness as goals of the new platform regulations marks a significant move away from the single-edged understanding of competition law advocated by the proponents of the consumer welfare standard. This becomes most apparent in the fact that the new platform regulations draw up ex ante rules that seek to prevent platforms from foreclosing competitors or business users regardless of their efficiency. The new platform regulations allow competition authorities to intervene in digital markets without being required to carry out an “as-efficient competitor test” which has been widely endorsed in modern U.S. 58 and E.U. 59 antitrust as the ultimate touchstone to determine when impugned unilateral conduct harms consumer welfare and therefore falls afoul of competition rules. The new platform regulations hence clearly depart from the fundamental of modern antitrust that unilateral conduct by dominant firms is only objectionable if it forecloses an “as-efficient” or equally efficient competitor. 60

The new platform regulations thus enable competition authorities to protect a competitive market structure and the economic opportunity and liberty of smaller competitors and business users regardless of their efficiency and immediate contribution to consumer welfare. They thereby implicitly challenge the truism of modern antitrust that competition law protects “competition, not competitors.” 61 In so doing, they vindicate the long-standing insight that competition, at least in the medium-to-long-run, “requires the existence of competitors, in the plural.” 62 This suggests that for competition to exist and thrive, competitors must at least be protected to some extent. For without competitors, there is no competition.

B. Toward a More Holistic Understanding of Consumer Welfare

Does this mean that the new platform regulations discard the consumer welfare standard? Not necessarily. Their focus on limiting economic power, securing a contestable and rivalrous market structure, and fairness in digital markets does not mean that consumer interests are irrelevant for the new platform regulations. On the contrary, the new platform regulations rest on the assumption that greater structural rivalry and equality of opportunity at the level of inter-platform and intra-platform competition will ultimately result in greater innovation and consumer welfare in the medium-to-long run. They thereby operationalize the Arrovian assumption that greater rivalry will foster innovation efforts. 63

The new platform regulations thus stand for the proposition that more rivalry in digital markets, fostered by greater contestability and equality of opportunity, will benefit consumers in the medium-to-long run in the form of enhanced innovation, service quality, choice, and privacy. 64 Implicit in this proposition is the assumption that the interests of smaller innovative competitors, business users, and end users are largely aligned. It also implies that increased contestability and rivalry might enable or compel firms to differentiate themselves from incumbent platforms, for instance, by providing less privacy-intrusive products and services. Moreover, greater contestability and equality of opportunity among rivals are also thought to lead to lower prices for consumers because business users will be able to operate on lower costs and will pass on these lower costs to end users.

The new platform regulations thus embrace a more open, holistic and, arguably, more accurate understanding of consumer welfare that comprises alongside lower prices also non-price parameters such as quality, innovation, choice, and privacy. This holistic understanding of consumer welfare pays heed to the fact that many digital markets are zero-price markets on which firms compete for customer goodwill on the basis of non-price parameters. Most importantly, this holistic understanding of consumer welfare is cognizant of the fact that consumers also value things that are difficult to quantify in monetary terms, such as privacy or the option to flexibly change their preferences in the future should the so far preferred choice prove no longer attractive or “turn rogue.” 65

C. The Implications of the Multi-Value Approach: Managing Value Conflicts

Despite the continuous importance of consumer interests, the new platform regulations fundamentally diverge from the consumer welfare standard of conventional antitrust in so far as consumer interests are no longer considered the exclusive or primary goal that, in case of conflict, trumps all other considerations. This raises the central question of whether the various goals pursued by the new platform regulations always prove complementary to the extent their architects seem to assume. This is anything but certain. The history of the U.S. Robinson-Patman Act, 66 for instance, constitutes a prominent example of how antitrust statutes which pursue multiple, at times conflicting, objectives may easily run into difficulties and turn into an anti-consumer welfare policy. 67 The claim that competition law when pursuing a “hotchpotch” of various goals inevitably results in inconsistent outcomes was a central element of the Chicago School critique. 68 It also explains the breath-taking success of the consumer welfare standard which allowed modern antitrust to avoid goal conflicts by reducing the normative content of competition law to the single goal of consumer welfare. 69

The prospect of potential conflicts between the multiple policy goals pursued by the platform regulations invite three reflections. First, more empirical research is necessary to understand under which circumstances specific goals of the new platform regulations cease to be complementary and start pulling in opposite directions. Narrowing down these instances might enable legislators and enforcers to reduce goal conflicts to a minimum. Second, mechanisms should be devised that allow for a transparent prioritization and trading-off of various objectives in those remaining, hopefully rare but inevitable, occasions of goal conflicts. Third, instead of seeking to fully eradicate value conflicts, legislators and enforcers should endorse them pragmatically. Such value conflicts are, in fact, inevitable and coexistent with the indeterminacy of legal rules. 70 Attempts to define conflicts away by proclaiming that competition law should only pursue consumer welfare are therefore intellectually unsatisfactory and doomed to fail. They are also misleading because the adoption of the consumer welfare standard by modern antitrust constitutes nothing else than a political choice that seeks to settle value conflicts by declaring certain considerations irrelevant for deciding antitrust cases. Instead of sweeping them under the rug, legislators and enforcers should candidly address those value conflicts and clearly articulate and justify the political choices they make to settle them. As long as these choices are the results of a good-faith attempt to trace the interests of all relevant stakeholders and remain contestable through legal and political channels, they should be considered legitimate both in legal and democratic terms.

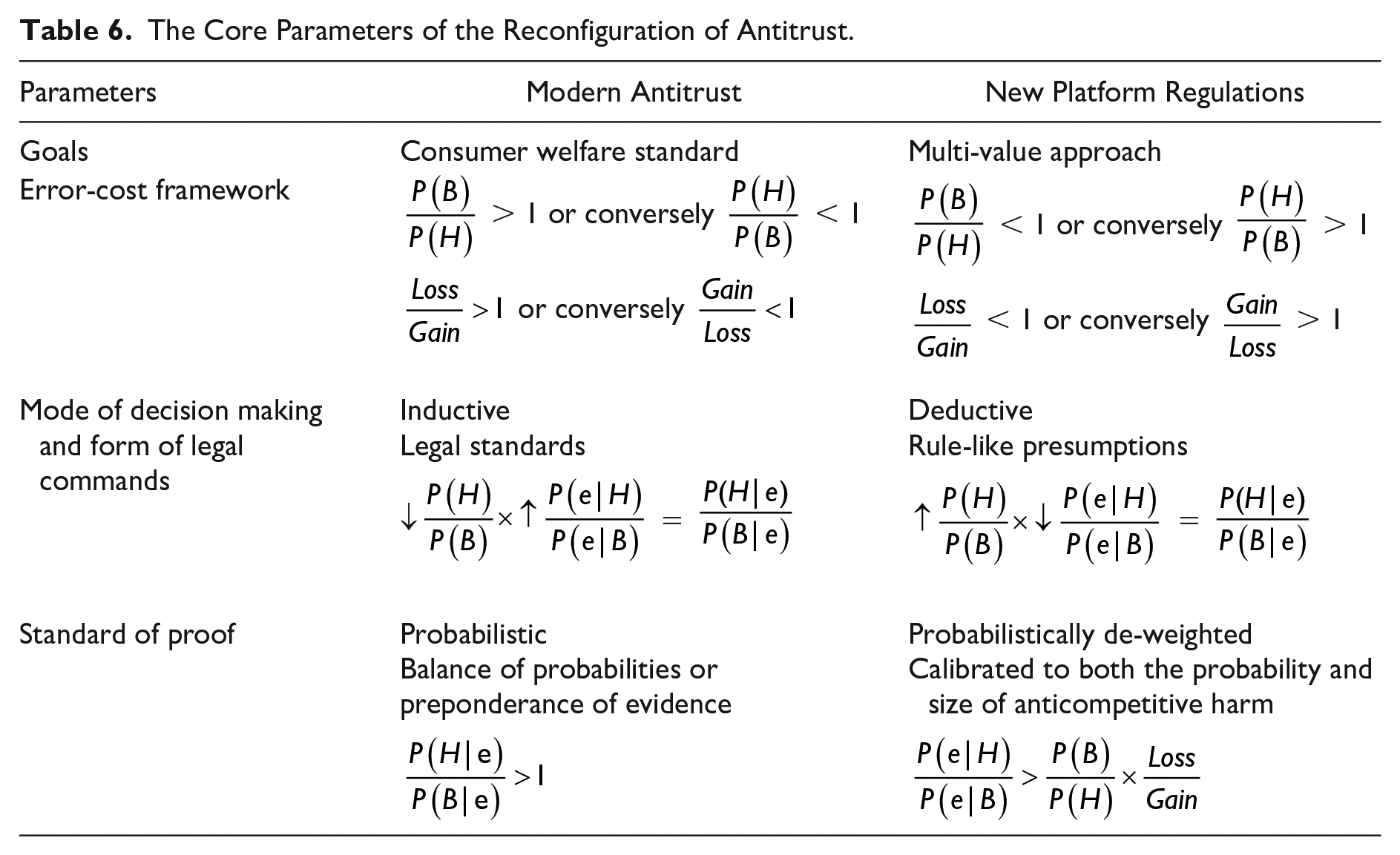

IV. The Recalibration of the Error-Cost Framework

A second significant reconfiguration brought about by the new platform regulations is the recalibration of the baseline assumptions of modern antitrust regarding the costs and benefits of competition law intervention. Antitrust orthodoxy for a long time adhered to the view, initially coined by Chicago scholars, 71 that as a matter of principle erroneous antitrust intervention tends to be more costly than erroneous non-intervention.

A. The Axioms of the Conventional Error-Cost Framework

This skewed understanding of error costs of modern antitrust rests on two axioms. First, it assumes that the probability of specific business conduct resulting in anticompetitive effects tends to be low. 72 In other words, the orthodox error-cost framework is predicated on the belief that the prior probability of firm conduct being beneficial (P (B)) always exceeds the prior probability of it being harmful (P (H)), that is,

This in turn means that the odds ratio of the prior probability of business conduct being beneficial (P (B)) relative to it being harmful (P(H)) is always greater than 1,

Second, the conventional error-cost framework also turns on the proposition that judicial errors are rarely corrected. Chicago scholars highlighted that erroneous convictions (i.e., type 1 errors or false positives) prevent not only efficiency-enhancing conduct in a single wrongly decided case but also deter procompetitive conduct by other firms in the future. This “judicial deterrence effect” is hence thought to amplify the costs of type 1 errors across time. Type 2 errors resulting from erroneous acquittals or non-intervention, by contrast, are presumed to be easily corrected by market forces. For, at least in the long run, monopoly profits will attract new entry that will erode market power. The preference of type 2 over type 1 errors encoded in the conventional error-cost framework thus embodies the belief that markets are robust and tend to self-correct. 74

This postulate of the disparate weight of error costs not only implies that the probability of conduct being truly anticompetitive is much lower than it being procompetitive, but it also suggests that the costs of erroneous antitrust intervention (Loss) often outweigh the accuracy benefits of antitrust intervention resulting from correctly averted or remedied antitrust harm (Gain), that is,

The skewed orthodox error-cost framework thus assumes that the ratio between the social losses created by the costs of false positives and the benefits resulting from accurate antitrust intervention that successfully averts or remedies truly harmful conduct always exceeds 1, that is,

It directly follows from this slanted understanding of error costs that under-enforcement (that means excess type 2 errors) constitutes the optimal standard of intervention or deterrence. This is because type 1 errors are more likely (as the likelihood of pro-competitive conduct exceeds that of anticompetitive conduct (

B. From Under- to Over-Enforcement as the Optimal Policy Standard

The orthodox concern that over-enforcement would unduly deter pro-competitive firm conduct for a long time dominated the academic and policy debate about the appropriate role of antitrust law, notably in innovation-driven digital markets. Market power or large market shares, it was often argued, were short-lived in digital markets as incumbents would remain constrained by dynamic, potential competition “for the market.” 76 The importance of innovation and dynamic efficiencies in the digital sector further added to the costs the conventional error-cost framework associates with “judicial over-deterrence.” It was feared that type 1 errors would not only deter other firms from engaging in conduct that maximizes static efficiencies but also dampen their incentives to innovate and generate dynamic efficiencies. Antitrust scholars and courts relied on a Schumpeterian 77 understanding of innovation, which posits that the prospect of temporary monopoly profits operates as an important incentive for firms to innovate, 78 to support the claim that heavy-handed competition law intervention against large incumbents in innovation-driven markets would inevitably harm innovation. 79

The new platform regulations fundamentally challenge this orthodox understanding of error costs and, with it, the widely held opposition to interventionist antitrust policy in technology-enabled markets. By subjecting digital platforms to ex ante rules and expanding the intervention toolkit of competition enforcers in digital markets, the new platform regulations instead stand for the proposition that the welfare costs of under-enforcement of traditional competition rules (type 2 errors) in digital markets outweigh the potential error costs caused by the over-enforcement of more or less broadly construed ex ante rules (type 1 errors). The new platform regulations thus openly challenge the assumption of orthodox antitrust that under-enforcement is the optimal standard of intervention in innovation-driven markets. At the same time, they also call into question the “contestable market hypothesis” 80 which posits that market power in digital markets is short-lived, as incumbents remain constrained by dynamic, potential competition “for the market.” The new platform regulations, instead, suggest that in the case of doubt competition law enforcement in digital markets should err on the side of intervention and type 1 errors. The platform regulations hence embody the proposition that over-enforcement constitutes the optimal intervention standard for competition law in digital markets.

C. The Reasons for a Recalibrated Understanding of Error Costs

What explains this recalibration of the error-cost framework? The departure from the orthodox error-cost framework is representative of a broader reckoning that its preference for type 2 errors is grounded in very strong assumptions about the self-healing forces of markets and the costs of state intervention. 81 There is hence a growing awareness that the orthodox error-cost framework is all too often rooted in inherently political value judgments and beliefs—namely, a strong ideological aversion against state intervention and preference for laissez-faire, laissez-aller—rather than in market realities.

Post-Chicago scholarship has notably shown that the Chicago School analysis on which the orthodox error-cost framework is premised underestimated the frequency at which unilateral conduct by powerful firms may result in anticompetitive harm.

82

This reconsideration of the probability distribution of anticompetitive conduct has been further compounded by the specific features of digital markets. The presence of extreme economies of scale and scope, network effects, and rising levels of industry concentration is believed to make digital markets more prone to anticompetitive outcomes than other industries.

83

Recent economic scholarship thus questions the fundamental premise of the orthodox error-cost framework that firm conduct always tends to be more likely to be beneficial than harmful. Instead of assuming that the prior odds ratio of pro-competitive effects always exceeds 1 (

The recalibration of the error-cost framework underpinning the new platform regulation is, however, not only informed by the recognition that anticompetitive outcomes occur in digital markets more frequently than it was believed by the orthodox error-cost framework. The revisited assessment of error costs also gives currency to the view that anticompetitive conduct by powerful digital platforms tends to result in harm of substantial magnitude. 84 First, owing to their size and importance as gateways to online markets and customer groups, anticompetitive conduct by powerful platforms is likely to affect a vast number of transactions by end and business users. Second, the propensity of digital markets to tip on a lasting basis in favor of the predominant incumbent further amplifies the harm of anticompetitive conduct by rendering it irreversible (or at least prohibitively costly to reverse). 85 As network effects might tilt digital markets on a lasting basis, market mechanisms are less likely to readily self-correct any type 2 errors than the orthodox error-cost framework assumes. Given the low degree of contestability, once a digital market has pivoted in favor of a powerful incumbent, competing alternative innovation paths and technological solutions may be forever lost.

The magnitude of harm of anticompetitive outcomes in digital markets has, therefore, an important inter-temporal dimension. If markets by reason of the presence of strong network effects and limited contestability are unlikely to rapidly eradicate anticompetitive outcomes, the magnitude of anticompetitive harm increases the longer it takes competition authorities or courts to intervene. The magnitude of anticompetitive harm, in other words, is positively correlated with the size and importance of digital platforms as gateways and negatively correlated with market contestability, reversibility of anticompetitive harm, and the speed of competition law intervention.

This growing awareness of the significant scale of the costs of false negatives inverts the ratio between the losses and gains of antitrust intervention. The revised error-cost framework underpinning the new platform regulations posits that, at least in digital markets, the gains of antitrust intervention often outweigh its losses. Instead of assuming that the ratio between losses and gains of antitrust intervention always exceeds 1 (

The revised error-cost framework underpinning the new platform regulations thus epitomizes not only a reconsideration of the probability distribution of anti- and procompetitive effects but also evinces greater awareness for the magnitude of harm that anticompetitive conduct may bring about in digital markets. Anticompetitive harm in digital markets tends to be of particularly sizeable scale if antitrust intervention and market mechanisms are slow in correcting anticompetitive outcomes and/or innovation is irreversibly lost as a consequence of it. The orthodox error-cost framework was grounded in the apprehension that judicial errors will stay uncorrected and procompetitive conduct will be forever deterred and lost. The recalibrated error-cost framework of the new platform regulations turns this assumption upside down. It recognizes that by reason of network effects and the tendency of markets to tip on a lasting basis in favor of the incumbent, anticompetitive harm may stay forever uncorrected. In the presence of a higher frequency of anticompetitive and potentially irreversible harm of substantial magnitude, over- rather than under-deterrence becomes the optimal standard of intervention. Instead of preferring type 2 errors, it suddenly makes economic sense to err on the side of type 1 errors. 86

V. A Reconfiguration of the Modus Operandi of Modern Antitrust

The recalibration of the error-cost framework envisaged by the new platform regulations finds its direct and most significant expression in a third major shift, namely the reconfiguration of the modus operandi of modern antitrust. The new platform regulations curtail the extent to which antitrust enforcers are required to rely on case-specific information or evidence to make a legal determination of the (il)legality of specific conduct. All new platform regulations thereby fundamentally depart from the incremental shift of modern antitrust toward a more inductive competition law analysis. Instead, they resurrect a more deductive mode of decision making that relies on strong priors to infer anticompetitive harm from the economic and legal form of specific platform conduct. To illustrate this transformation, this section proposes a basic model of antitrust decision making (A) before describing how the new platform regulations will alter this mode of decision making (B) and considering the implications of this development (C).

A. A Basic Model of Antitrust Decision Making

The decision making of competition authorities and judges in antitrust cases can be modeled by Bayesian decision theory. In competition proceedings, the basic task of the factfinder consists of deciding whether impugned conduct will create anticompetitive harm (H) or will be competitively neutral/beneficial (B or non-harm). Bayes’ theorem, which forms the basis of subjectivist approaches to epistemology and theories of evidence, 87 describes how such a determination of the anticompetitive nature of specific impugned conduct can be formed. This decision-making process can be expressed in the following formula:

Bayes’ theorem outlines how a factfinder can form probability estimates by updating prior beliefs with further evidence. To this end, the factfinder will build a hypothesis about the impugned conduct’s impact on competition by first forming a prior probability opinion. This prior probability estimate

The prior probability estimate

By combining the prior probability

The above expression of the Bayesian theorem hints at two alternative, albeit complementary, modes of decision making competition authorities and courts can use to make determinations about the lawfulness of specific conduct. 89 The first mode of decision making is deductive in nature. Under this deductive mode, a factfinder can primarily rely on prior probability estimates of the impugned conduct entailing anticompetitive harm. This prior can take the form of legal rules or presumptions that indicate the legality of specific types of conduct without requiring the factfinder to account for a broad range of additional assessment criteria. Rules or presumptions operate as analytical shortcuts or heuristic devices which enable a factfinder to infer fact B from the showing of another fact A. 90 They thus allow a factfinder to infer a certain legal fact or conclusion, such as the anticompetitive nature or illegality of specific conduct, from a limited set of specific facts without engaging in a fully-fledged analysis of case-specific evidence. 91 Instead of proving the anticompetitive nature of the impugned conduct on the basis of case-specific evidence showing that it is actually or likely causing anticompetitive harm, a competition authority or court can deduce the anticompetitive harm from the way in which its legal or economic form relates to a specific rule or presumption.

The respective weight of this presumption (prior) and additional evidence e can vary. The presumption can be neutral (i.e., equal 1) if the competition authority starts from the premise that the respective probabilities of the conduct being anticompetitive or not are on par with each other (

The strength of a legal presumption thus regulates the amount of information a competition authority is required to account for and produce in order to make a legal qualification of the impugned conduct. It operates as a multiplier that affects the weight of additional evidence or information a factfinder needs to consider to assess the legality of the conduct. At the same time, it also determines the height of the evidentiary burden a defendant has to meet to rebut a presumption of anticompetitiveness operating against its impugned conduct. 92 The higher (lower) the prior odds ratio, the stronger the additional evidence must be to offset (confirm) the initial presumption of anticompetitive harm. A legal presumption thus puts the “thumb on the scale” as it tilts the decision making toward the finding of anticompetitive harm (or non-harm). 93

The second mode of antitrust decision making is inductive in nature. It consists of a careful and casuistic inquiry into the actual or likely effects of the impugned conduct on competition. This inductive mode of decision making fundamentally differs from a deductive analysis where the prior carries significant weight as the factfinder relies on hard-and-fast rules or strong presumptions and infers the legality of specific conduct from its economic and legal form. The inductive method, instead, requires the factfinder to consider additional assessment criteria and case-specific evidence to form an opinion as to whether the conduct has actual or likely anticompetitive effects. The importance of this case-specific evidence is negatively correlated to the strength of the prior. The weaker the prior, the more case-specific information the factfinder has to rely on to establish the anticompetitive nature of impugned conduct. When the factfinder starts from the prior that the conduct is competitively neutral (

Most of the time, antitrust decision making will not take the pure form of either deductive or inductive analysis. Rather, both modes describe ideal types that lie at the two extremes of a continuum of more or less differentiated modes of analysis and rules. 94 Real-life decision making will often be a mix of and thus sit somewhere in between these two extremes. Whether decision making gravitates more to the deductive or the inductive approach depends on the exact weight of the prior and the case-specific evidence in the formation of the posterior probability estimate.

Nonetheless, historically competition law analysis on both sides of the Atlantic increasingly drifted under the banner of the “more economic” or “effects-based” approach toward a more inductive mode of decision making. 95 The primary channel through which this shift toward the inductive, effects-based approach took shape was the reconfiguration of the type of “legal commands” 96 competition law chooses to lay down proscriptions and obligations; in short, the manner in which competition law formulates propositions of normative desiderata. 97 With the rise of the so-called “more economic approach” under the auspices of the Chicago School, flexible legal standards that call for a casuistic and inductive analysis of “demonstrable economic effects” 98 became the preferred default mode of modern antitrust analysis. The reliance of U.S. and E.U. competition law on self-executing rules or broadly construed legal presumptions was increasingly disavowed as outdated “formalistic line drawing” 99 that led to economically illiterate outcomes. Modern antitrust thus increasingly opted for more differentiated and complex legal commands, taking the form of flexible standards that require competition authorities to account for additional, case-specific assessment criteria (i.e., greater amounts of evidence e) to enhance the precision of antitrust analysis in telling apart truly harmful from truly beneficial conduct. 100

Modern antitrust’s preference for an inductive method relying on “flexible” standards rather than “rigid” rules was the immediate result of the rise of the orthodox error-cost framework and its aversion against type 1 errors. As long as the axiom of the orthodox error-cost framework that, as a matter of principle, business conduct is most of the time pro-competitive—that is,

B. From Standards to Rule-Like Presumptions

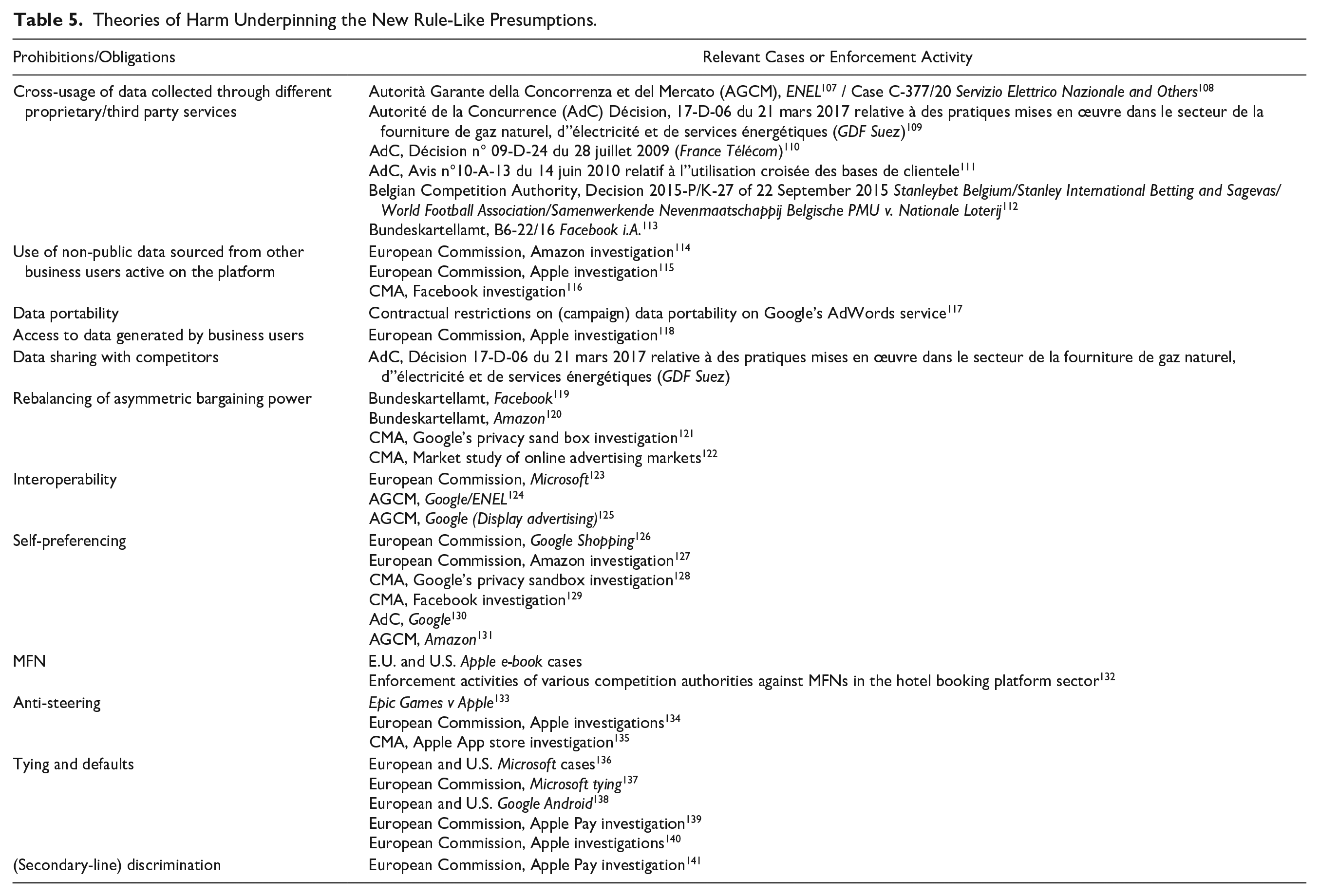

The new platform regulations mark a significant rupture in what appeared an inexorable progress toward a more inductive, effects-based approach and a greater differentiation of legal commands in competition law. Some of the new platform regulations rely on rebuttable 102 presumptions to identify firms that qualify as designated platforms. 103 All new platform regulations also introduce novel self-executing, rule-like presumptions of anticompetitiveness for specific forms of unilateral platform conduct 104 or mergers 105 (see Tables 2 and 3). They thus establish ex ante bans preventing designated platforms from engaging in different forms of “blacklisted” conduct that are deemed to be “particularly unfair or harmful” to competitors and/or reduce the contestability of markets. 106 Most of these presumptions codify a number of theories of harm that lay at the core of recent antitrust cases and investigations against powerful online platforms (see Table 5).

Theories of Harm Underpinning the New Rule-Like Presumptions.

By codifying existing or novel theories of harm into rule-like presumptions, the new platform regulations assign increased weight to priors in the determination of anticompetitive conduct in digital markets. Consequently, they importantly depart from the preference of modern antitrust for flexible legal standards and an ever more inductive, casuistic analysis of anticompetitive effects. The new platform regulations bring about a partial roll-back of the inductive “effects-based” approach and more differentiated legal standards to the benefit of a more deductive “form-based” approach and less differentiated rules.

142

They are thus suggestive of a transition from an equilibrium characterized by the decreasing weight of priors

This greater role of rule-like presumptions not only reduces the amount of information competition authorities have to process before they can qualify platform conduct as unlawful, but it also substantially heightens the evidentiary burden for defendants. All new platform regulations indeed attribute considerable weight to the newly crafted presumptions by limiting the degree to which they can be rebutted by designated platforms. The presumptions established in arts. 5 and 6 of the DMA arguably carry the most important weight. Although they remain rebuttable, the DMA sets a particularly demanding standard for defendants to reverse them. The DMA does not recognize any form of efficiency defense that defendants could advance to justify blacklisted conduct. Rather, designated platforms can only defeat the presumptions by putting forth offsetting evidence showing that the conduct is exempted under public interest grounds 143 or temporarily necessary to secure the viability of their business. 144

The U.S. proposals also set a high evidentiary burden for the rebuttal of presumptions of illegality for unilateral platform conduct or platform acquisitions. Unlike conventional antitrust law, the new proposals do not provide for a clear-cut efficiency defense. Instead, designated platforms can merely rely on an “affirmative defense” to rebut presumptions of illegality. 145 Under the proposed rules for platform mergers, designated platforms can also obtain an “exemption” from the prohibition against platform acquisitions if they demonstrate that the proposed merger does not have any adverse effect on actual, potential, or nascent competition. 146 To rebut these presumptions, designated platforms must, however, meet an exacting evidentiary burden. They have to produce “clear and convincing evidence” 147 suggesting that the conduct or merger is with a strong probability—of 75 percent or more 148 —competitively neutral or pro-competitive.

The presumptions listed in s. 19a GWB carry considerable weight, too. Yet, designated platforms appear to have to surmount a less important evidentiary hurdle to overturn them. Although s. 19a does not provide for any explicit efficiency defense or other public policy–related exemptions, the German legislator clearly envisaged the possibility for addressees of s. 19a to advance objective justifications in defense of the presumed abusive forms of conduct. 149 By contrast, the presumptions under the SMS regime have a considerably less important weight because the SMS framework appears to accept a broader range of admissible rebuttal evidence. Unlike the DMA, the SMS framework recognizes the possibility for firms to plead an efficiency defense or objective justification to save conduct that otherwise violates their code of conduct. 150

In relying primarily on rule-like presumptions of considerable weight to lay down legal commands for digital platforms, the new platform regulations mark an inflection point in the trend from deductive to inductive decision making that shaped the more effects-based or economic approach and its operationalization through greater differentiation of legal commands. The immediate consequence of this reversal toward a more deductive mode of decision making and less differentiated rules is that competition authorities can more easily rely on prior probability estimates of anticompetitive harm to make a determination about the (un)lawful nature of the conduct at hand. The corollary of the revaluation of priors and decreased differentiation is the declining weight and amount of case-specific evidence that competition authorities are required to assess before impugned conduct can be legitimately qualified as anticompetitive.

C. Implications of the Increased Weight of Rule-Like Presumptions

This pivot toward a more deductive mode of decision making and the concomitant choice of priors, in the form of less differentiated rule-like presumptions, rather than differentiated, open-textured standards, to lay down legal commands and prescriptions for powerful platforms, has a number of significant implications.

The most important implication is that rule-like presumptions, unlike standards, have a modal character. They lay down moral desiderata that are considered true not only in the specific, actual world (that is, the world where a competition authority or court finds based on case-specific evidence that a firm has unduly interfered with another firm/competition) but across all relevant possible and legally permissible worlds. 151 Legal rules and rule-like presumptions thus formulate normative propositions or legal commands whose realization and enforcement is less contingent on changing, case-specific circumstances than legal standards that inform the inductive mode of decision making of modern antitrust law. Owing to their modal character, the rule-like presumptions enshrined in the new platform regulations follow a clearly preventative character. They seek to prevent designated platforms from engaging in certain forms of conduct that have a high probability of leading to anticompetitive outcomes or may result in anticompetitive harm of significant magnitude because they further entrench the market power of platforms and/or unduly raise the costs of horizontal platform and downstream business user competitors. Instead of sanctioning firms retroactively for any harm they caused, rule-like presumptions seek proactively to avert anticompetitive harm from materializing, by making specific conduct unavailable or prohibitively costly for designated platforms. 152

The corollary of the modal character of legal rules or rule-like presumptions is that they encode the proposition that the benefits (costs) of preventively outlawing specific conduct across different possible worlds outweigh (fall short of) the benefits (costs) of a more minute, casuistic analysis that seeks to minimize type 1 errors resulting from over-inclusive and less differentiated rules, but at the same time is inherently prone to type 2 errors. 153 Rule-like presumptions thus encapsulate the premise that specific conduct of designated platforms tends to be in such an overwhelming number of cases anticompetitive or to produce anticompetitive harm of such an important order of magnitude that the costs of a more elaborate analysis of their actual effects are not outweighed by the presumptive gains flowing from the reduction in type 1 error costs. 154 In other words, for specific conduct by powerful platforms the new platform regulations endorse a certain tolerance level of type 1 errors resulting from the inherently over-inclusive nature of legal rules.

What explains this shift from under-inclusive standards to over-inclusive rules or rule-like presumptions? A first reason for the adoption of broadly construed, self-executing rules is the recalibration of the error-cost framework. The important role of presumptions in platform regulations indeed signals that over- rather than under-enforcement is increasingly considered the optimal intervention standard in digital markets. It is a manifestation of the fundamental revision of the two axioms regarding the incidence of anticompetitive effects and costs/benefits of antitrust intervention underpinning the orthodox error-cost framework.

By codifying a number of theories of harm that formed part of recent antitrust cases and investigations against powerful online platforms, the rule-like presumptions encode the inference that certain forms of conduct by powerful platforms have a high probability of leading to anticompetitive outcomes. The increased weight of priors (

By revising the assumptions of the prior distribution of anti- and procompetitive effects for (specific) conduct of designated platforms and assuming that

The new rule-like presumptions also embody the belief that specific conduct by designated platforms will result in harm of greater magnitude than the conduct of other smaller platforms or comparable non-digital firms. The greater weight of presumptions under the new platform regulations thus also marks the departure from the second axiom underpinning the orthodox error-cost framework that the costs of antitrust intervention tend to outweigh its benefits, that is

A second reason for the greater role of self-executing rule-like presumptions is that the new platform regulations seek to enhance legal certainty not only for regulated gatekeeper platforms but also for competing platforms, businesses, and end users. 157 Less differentiated legal commands, in the form of legal rules and rule-like presumptions, indeed, outperform standards in ensuring legal certainty and predictability for all relevant stakeholders. 158 This comparative advantage of legal rules over standards in guaranteeing legal certainty and predictability is of particular relevance in digital markets. Given that gatekeeper platforms perform a high volume of transactions, the new platform regulations are likely to govern transactions and conduct that occur with high frequency. The informational and compliance costs of rule-like presumptions for enforcers and individual firms are inferior to those of standards when the frequency of the governed conduct is high. 159 In securing greater legal certainty, rule-like legal presumptions may not only contribute to enhanced deterrence and greater compliance 160 but also secure the incentives of regulated platforms and other market participants alike to invest in innovation.

Third, as they obviate the need for market definition, the assessment of anticompetitive effects, and counter-factual analysis, rule-like presumptions reduce the amount of information competition authorities have to process and thereby facilitate swifter antitrust intervention. Rule-like presumptions thus allow affected consumers, competitors, or competition authorities to challenge anticompetitive conduct more readily and easily than open-textured standards. 161 The adoption of self-executing rules is hence cognizant of the importance of the time-dimension of error costs in digital markets, which are prone to tipping. It also embodies the realization that modern antitrust law, owing to its reliance on standards and a casuistic effects-based analysis, has proven too slow in preventing anticompetitive conduct that tipped markets on a lasting basis in favor of a dominant platform. 162

The important role of legal presumptions in the new regulations of digital platforms also shows that a more economic approach must not necessarily call for more differentiated legal commands and inductive analysis. Once one departs from the axioms of the orthodox error-cost framework that the probability of anticompetitive harm is low and the costs of type 1 errors tend to exceed the benefits of antitrust intervention, a more deductive analysis and less differentiated legal commands may be consonant with an economically informed approach. The reliance of the new platform regulations on rule-like presumptions thus operationalizes the belief that in digital markets the costs of type 2 errors and complex competition law analysis (i.e., regulation costs) outweigh the accuracy benefits of greater differentiation in terms of lower type 1 errors. 163

This trade-off between error costs and accuracy benefits of antitrust intervention does not necessarily have to take the form of a strictly dichotomous choice between rules and standards. The DMA and the SMS regime also illustrate that a balance can be struck through the fine-tuning of the specific design and implementation of rule-like presumptions. For instance, arts. 5 and 6 DMA both set out rule-like presumptions of illegality for certain conduct of designated platforms. Art. 6, however, creates room for greater flexibility in the implementation of these rules, by according an important role to the Commission in further specifying and designing solutions and remedies at the individual platform-level. Arts. 5 and 6 thus establish a framework for differentiated rules: while art. 5 presumptions uniformly apply to all gatekeepers across the board, art. 6 allows for more tailor-made interventions and remedies. 164 The proposed SMS regime goes one step further in creating wiggle room for further fine-tuning and differentiation of rule-like presumptions. While the codes of conduct envisaged by the SMS regime lay down, in a similar way to art. 5 DMA, specific rules that apply to all SMS platforms across the board, they provide at the same time the DMU with plenty of leeway to establish tailor-made rules for individual platforms. 165 By adopting a differentiated approach toward the design and fine-tuning of legal presumptions, the DMA and the SMS framework seek to minimize the type 1 errors associated with the inherent over-inclusiveness of legal rules by increasing the degree of differentiation of legal commands and blending rules with the flexibility of legal standards.

One might speculate about the extent to which the growing weight of presumptions in the new platform regulations and the heightened evidentiary burden for their rebuttal will also have spill-over effects on the competition law analysis of conduct or sectors not covered by the new platform regulations. This question is of particular relevance because the rule-like presumptions of the new platform regulations appear, at least in their current state, to primarily target non-price conduct, such as self-preferencing, refusals to ensure interoperability, or tying. This focus on non-price conduct is somewhat puzzling in so far as price conduct, such as loyalty rebates or exclusivity payments by dominant platforms, often have similar foreclosure effects and allow platforms to leverage and entrench their market power. 166 No explanation is so far provided as to why most forms of exclusionary price conduct fall outside the scope of the new platform regulations. This is problematic not least because the disparate treatment of non-price and price conduct by dominant gatekeeper platforms is liable to lead to incoherent outcomes. By way of example, under the new platform regulations tying by a dominant gatekeeper platform will be presumed unlawful regardless of the efficiency of competitors. By contrast, loyalty rebates or exclusivity payments will continue to be subject to a case-by-case analysis and, under certain circumstances, the application of an as-efficient competitor test under Section 2 Sherman Act, 167 art. 102 TFEU 168 and/or equivalent provisions of national law (i.e. s. 19 GWB or the Chapter II prohibition of the Competition Act 1998), although they may have the very same exclusionary effects. This incoherence in treatment of exclusionary price and non-price conduct needs addressing. This does not mean that the presumptions of anticompetitiveness should be necessarily expanded to price conduct. There are indeed important reasons—for instance, the goal of preserving dominant platforms’ incentives to compete aggressively on prices—that may support a dissimilar treatment of gatekeeper platforms’ price and non-price conduct. However, the reasons underpinning this inconsistent treatment should be clearly articulated.

VI. From Pure to Bounded Probabilism

A fifth element in which the new digital platform regulations depart from modern antitrust law relates to the standard of proof or threshold of intervention. Under the auspices of the more economic approach, conventional antitrust has increasingly moved toward what one can call “pure probabilism.” Modern antitrust indeed largely endorsed a probabilistic standard of proof that requires competition law plaintiffs to prove actual or likely anticompetitive effects for competition law intervention to be justified. The new platform regulations importantly digress from this purely probabilistic understanding of the standard of proof.

A. A Decision-Theoretic Operationalization of the Standard of Proof