Abstract

Startup accelerators, which aim to improve the set of choices representing a startup’s entry strategy, have become increasingly influential in both regional development and the strategies of individual startups. This article explores an accelerator’s impact on startup performance and whether that impact varies substantially by features of the startup’s founding environment. Leveraging data from a leading startup accelerator, I use a regression discontinuity framework to hold startup quality constant so that I can compare the performance of admitted startups to those that do not make the cut, and I examine whether any observed performance differentials are driven by accelerator admission and by characteristics of the startup’s earlier environment. I find evidence that startups from better pre-accelerator environments experience stronger gains from accelerator admission. I also find evidence of home bias, as local startups have a stronger treatment effect. These results provide evidence of ecosystem effects whereby the impact of one organizational sponsor in an ecosystem is strongly moderated by other features in the ecosystem. The findings help to explain the concentration of accelerator programs in already successful entrepreneurial ecosystems and reveal how such programs may interact with founding environments to complement resource abundance or magnify prior resource inequalities.

Techstars, the world’s second-oldest startup accelerator, was founded in 2006 with a focus on revitalizing Boulder, Colorado’s entrepreneurship ecosystem. One of its founders, David Cohen, reflected on this motivation when he said, “Although Techstars started because I wanted to find a better way to make angel investments, the equally important reason was that I wanted to improve the startup community in Boulder” (Feld, 2012: 110). After Techstars experienced early success in the Boulder area, another of its founders, Brad Feld, reported that “there is a startup revolution occurring. Every major metro area in the world will eventually be able to support an accelerator.” 1 A sample of U.S. accelerator founders showed that spurring regional development is a common goal: 47 percent reported regional or ecosystem development as a primary motivation for founding their program (Fehder and Hochberg, 2021).

Theories about organizational sponsorship that underlie our current understanding of how accelerators improve startup performance support the belief that accelerators can serve a key role in regional development. Such theories posit that organizations like accelerators provide resources and connections that mitigate deficiencies in a startup’s early environment, such as lack of financing or social capital, which have been shown to negatively impact startup performance (Flynn, 1993; Yli-Renko, Autio, and Sapienza, 2001; Shane and Stuart, 2002; Amezcua et al., 2013). 2 Recent work on accelerators has shown that the largest positive effects of organizational sponsorship require proper program design so that the increased information provided by the accelerator also creates internal changes to the startup’s learning and decision-making processes (Cohen, Bingham, and Hallen, 2019; Hallen, Cohen, and Bingham, 2020; Yu, 2020). While empirical work on organizational sponsorship has shown that sponsoring organizations can be more or less effective depending on how well the resources they provide fit with a startup’s external environment (Amezcua et al., 2013), this research has largely theorized the process as driven by the sponsoring organization and has paid little attention to how startup characteristics affect sponsorships.

Overall, research on accelerators and other related organizational sponsors suggests that these programs have their largest effects on startups in the regional environments most deficient in key resources. Research has shown that incubators play a particularly important role in bolstering firm capabilities and ecosystem quality where institutional deficits are the largest (Amezcua et al., 2013; Dutt et al., 2016; Armanios et al., 2017). 3 Related, preliminary evidence of accelerators’ impact on their regional environments has focused on underdeveloped regions, suggesting that accelerators create positive change in their entrepreneurial ecosystems (Fehder and Hochberg, 2021).

Yet, most U.S. accelerators are concentrated in highly successful regions rather than dispersed across the country. In 2015, nearly 27 percent of U.S. accelerators operated in the greater Silicon Valley area, and an additional 23 percent operated in the next five highest U.S. cities in terms of venture capital allocation intensity as measured by number of early-stage deals (Hathaway, 2016). Furthermore, half of the top-performing accelerators in recent years were in Silicon Valley (Hochberg, Cohen, and Fehder, 2017; Hallen, Cohen, and Park, 2023). If accelerators have a positive impact on startups in less-developed regions, why are accelerators so concentrated in already successful entrepreneurial ecosystems?

To begin to answer this question, I first observe that startups admitted to accelerators tend to be in innovative industries. Because these industries are suffused with technological and market uncertainties, the relationship between a startup and a potential competitor or partner can change quickly (Gans and Stern, 2003; Marx, Gans, and Hsu, 2014). Under these conditions, regional ecosystems can emerge in which startups, industry incumbents, and other stakeholders such as investors create open systems through which knowledge and resources are exchanged freely because the benefits of learning and the resolution of uncertainty outweigh the costs of sharing with potential competitors, especially for centrally networked actors (Powell, Koput, and Smith-Doerr, 1996; Owen-Smith and Powell, 2004; Whittington, Owen-Smith, and Powell, 2009; Shi and Shi, 2022). Incumbent firms and even investors that do not engage effectively in exploratory networking are at higher risk of failure (Dushnitsky and Lenox, 2005; Hochberg, Ljungqvist, and Lu, 2007). Within this environment, startups play a special role as they can explore opportunities with particularly high uncertainty, providing useful information even in cases of failure and valuable partnerships in cases of success (Hsu, 2006; Agrawal, Gans, and Stern, 2021).

To further explore why accelerators are disproportionately located in active entrepreneurial ecosystems, we need to focus on the impact of an accelerator’s ecosystem on the startups it supports. We know that accelerators affect startup performance by orchestrating free and open interactions between peer startups and mentors (Cohen et al., 2019; Krishnan et al., 2021); the accelerator’s environment mimics and potentially improves upon environmental factors that underlie successful entrepreneurial ecosystems. The direct brokerage of relationships inside an accelerator might then facilitate unstructured and informal practices in the broader ecosystem. Thus, the positive and open behavior inside the accelerator may spill over to other firms and stakeholders that do not initially have direct relationships with the accelerator program, by facilitating improved exchanges between accelerated firms and organizations that want to get in the game for fear of missing important opportunities (Giudici, Reinmoeller, and Ravasi, 2018). In highly developed ecosystems, these potential spillovers may provide a particularly important channel through which accelerators impact their startups—a channel that existing theories of organizational sponsorship have not explored.

In this article, I provide concrete evidence of these ecosystem spillovers by measuring how variation in startups’ founding environments affects the extent to which the startups benefit from participation in a top U.S. accelerator, MassChallenge. Understanding whether accelerators work in part by increasing a startup’s access to resources in its broader ecosystem has important implications for deeper understanding of how targeted policies and programs catalyze entrepreneurial ecosystem development (Vedula and Fitza, 2019; Vedula and Kim, 2019). Specifically, I seek to explore the potential cumulative dynamics that seem to push increasingly more entrepreneurship and innovation into a smaller number of regions (Florida and King, 2018; Chattergoon and Kerr, 2022). If startups from richer ecosystems benefit the most from acceleration, then these accelerators might intensify rather than mitigate inequality between regions.

Accelerating Ecosystems by Accelerating Firms

Accelerators admit innovation-driven startups that are at an early stage of development: the startups have not received substantial external investments or revenue from customers, and they must clarify their business plan before they can grow (Cohen et al., 2019; Botelho, Fehder, and Hochberg, 2021). 4 At this stage of development, a startup’s environment, especially the external resources to which it has potential access, impacts its chances of survival and growth (Dess and Beard, 1984; Shane and Venkataraman, 2000; Shane and Stuart, 2002), especially in industries with high technological uncertainty (Tushman and Anderson, 1986; Yli-Renko, Autio, and Sapienza, 2001). In such industries, a key resource that impacts a startup’s performance is access to technical and business information that improves the startup’s business plan or strategy (Davidsson and Honig, 2003; Chatterji et al., 2019).

By providing access to technical and business experts, an accelerator can improve a startup’s performance by improving its learning process. Early-stage startups face significant time and resource constraints that create substantial hurdles to pursuing new market or technical information, and these obstacles can create inertia that leads startups to prefer to execute their current strategy instead of refining it (Boeker, 1989; Karp and O’Mahony, 2019). By facilitating hundreds of feedback sessions with diverse stakeholders, including potential customers, partners, and investors, accelerators push startups to consider alternative approaches to creating and capturing value, mitigating their boundedly rational preference for their initial strategy (Cohen, Bingham, and Hallen, 2019; Cohen et al., 2019; Hallen, Cohen, and Bingham, 2020). Accelerators also improve the quality of these encounters by engendering trust and openness among each startup, its peers, and the mentors who contribute to the program (Cohen, Bingham, and Hallen, 2019; Krishnan et al., 2021).

By emphasizing the importance of early-stage firms’ access to information from technical and business experts, research on accelerators has improved our understanding of organizational sponsorship. An organizational sponsor seeks to improve a startup’s environment in ways that increase startup survival and performance through direct provision of resources (e.g., financing, space) or by bridging to key external resource holders (Flynn, 1993; Amezcua et al., 2013). Prior research has emphasized the organizational sponsor’s role in relieving environmental constraints, but careful studies on activity inside the accelerator have also emphasized that the full effect of an enriched environment comes from internal changes in the startup’s learning and cognition (Cohen, Bingham, and Hallen, 2019; Karp and O’Mahony, 2019). Presumably, the importance of downstream organizational change for the success of organizational sponsorship helps explain why small differences in design features seem to drive substantial differences in the effects of different accelerators, as shown in studies leveraging between-accelerator design variation (Cohen et al., 2019; Hallen, Cohen, and Bingham, 2020) and within-accelerator variation (Gonzalez-Uribe and Leatherbee, 2018).

Recent scholarship on accelerators has also improved the empirical methods used to measure the value of organizational sponsorship, as studies have measured the value of admission to an accelerator by comparing the average growth of its admitted startups to that of unadmitted startups or of startups admitted to accelerators with different design features. Scholars have measured a startup’s growth using the level of multiple key resources the startup acquired, especially external financing and employees, because startups grow differently and realize higher levels of various resources depending on their strategy (Botelho, Fehder, and Hochberg, 2021). Most important, because startups can vary substantially in their underlying quality and their attractiveness to providers of growth-related resources (Stuart, Hoang, and Hybels, 1999), most quantitative accelerator studies have tried to compare nearly admitted startups to recently admitted startups, to control for perceived quality at the time of application (Gonzalez-Uribe and Leatherbee, 2018; Hallen, Cohen, and Bingham, 2020). By comparing untreated firms to firms of perceived similar quality that were treated by different accelerator designs, researchers have found that small differences in accelerators’ organizational design can create dramatic differences in the accelerators’ average level of impact on admitted firms relative to similar firms that did not gain admission (Hallen, Cohen, and Bingham, 2020; Hallen, Cohen, and Park, 2023).

Unlike prior accelerator research, this study leverages variation in applicant startups rather than variation in program features, to explore how a startup’s founding environment moderates the impact of accelerator treatment. Given prior scholarship’s range of estimated treatment effects of accelerators, it is critical to first gain a baseline measure of the accelerator program’s impact on a startup’s growth in resources to ensure that the measure maps to the positive effects of high-quality accelerators observed in prior studies using similar methods. Thus, I offer this hypothesis:

Scholars have argued that organizational sponsors can foster systems of ecosystem learning not only by acting as direct brokers but also by propagating and maintaining beneficial practices within the ecosystem. Accelerators, incubators, and other organizational sponsors often try to develop rich networks of peer startups inside and outside their programs (Bøllingtoft and Ulhøi, 2005; Amezcua et al., 2013; Dutt et al., 2016; Wu, Wang, and Wu, 2021), as well as positive interactions with corporations, investors, government agencies, and universities (Hanssen-Bauer and Snow, 1996; Sapsed, Grantham, and DeFillippi, 2007; Arıkan and Schilling, 2011; Paquin and Howard-Grenville, 2013). Successful interorganizational routines inside an accelerator can diffuse as open ecosystem practices gain legitimacy (Aldrich and Fiol, 1994; Goswami, Mitchell, and Bhagavatula, 2018; Harper-Anderson, 2018). As more exchanges occur under better conditions, startups and other ecosystem actors learn to lean on their network to recognize and clarify opportunities (Davidsson and Honig, 2003; Giudici, Reinmoeller, and Ravasi, 2018). Current research theorizes that organizational sponsors achieve these improvements in ecosystem organization mainly by filling gaps in newly established ecosystems (Dutt et al., 2016; Giudici, Reinmoeller, and Ravasi, 2018) or by using privileged access to resources that enables them to establish a useful brokerage position (Dhanaraj and Parkhe, 2006; Arıkan and Schilling, 2011; Paquin and Howard-Grenville, 2013).

To date, research on organizational sponsorship has not distinguished these mechanisms and has largely focused on the direct effects of sponsorship: the connection between the sponsor’s goals and activities and the average performance of sponsored entrepreneurial firms (Amezcua et al., 2013; Dutt et al., 2016; Hallen, Cohen, and Bingham, 2020). It has also emphasized deficits in startups’ early environments, such that theories of organizational sponsorship may obscure the importance of the broader ecosystem, which may play a key role in the success of organizational sponsorship in some contexts. This focus on direct effects may seem like an obvious choice for studying how accelerators mitigate information deficits associated with weak founding environments (Hallen, 2008; Eggers and Song, 2015; Hallen and Pahnke, 2016). But does this approach explain what happens in environments in which resources available to firms are more plentiful?

This is an important question, as most U.S. accelerators exist in highly resource-rich environments, which, because of their culture of openness (Lawson and Lorenz, 1999) and deep, active interlinkages between organizations and individuals (Keeble and Wilkinson, 1999; Bell, 2005; Arıkan and Schilling, 2011), are more capable than other environments of fostering high-performing startups. High-quality ecosystems provide timely access to key resources as well as diverse perspectives on technological and market information, all of which allow firms to successfully pursue new opportunities (Powell, Koput, and Smith-Doerr, 1996; Beckman and Haunschild, 2002; Tallman et al., 2004; Spigel, 2017). Critically, startups that have a greater number of and more-central ties to these ecosystems seem to grow faster and acquire more resources than do startups that are part of the ecosystem but not as central (Powell, Koput, and Smith-Doerr, 1996; Owen-Smith and Powell, 2004). Thus, even though startups in resource-rich environments already have opportunities to access resources, information, and ties, organizational sponsors such as accelerators may help startups in these environments by enabling them to gain additional access.

Focusing on a startup’s founding environment may help clarify whether accelerators also provide value by virtue of their position within a developed ecosystem. Because they have greater access to new technical and market information (Tallman et al., 2004), startups in highly developed ecosystems can pursue more-novel opportunities. Exploring such opportunities can lead to technical and market insights that may be useful for multiple participants in the ecosystem (Gans, Stern, and Wu, 2019), yielding potential for valuable exchanges between the startup and other ecosystem participants. Entrepreneurs themselves may, therefore, be able to draw in resources from their environment during their period of acceleration by using the early discovery and growth process to share information and resources in ways that draw in more ecosystem participants (Fritsch, 2001; Feldman and Francis, 2004; Feldman, Francis, and Bercovitz, 2005; Feldman and Zoller, 2012). A startup’s learning and networking activity inside the accelerator may spill over to other key resource holders in its founding environment, drawing them into the accelerator ecosystem (Dushnitsky and Lenox, 2005; Ferrary and Granovetter, 2009).

Thus, we see different perspectives in the literature on the connection between organizational sponsors and broader ecosystems: one perspective emphasizes sponsors’ direct effect, and another perspective suggests that startups benefit from the ecosystem in which they are embedded. In other words, the latter perspective implies that startups may be able to fill information and resource gaps themselves after a period of early discovery and growth. These perspectives provide different ideas about which firms may benefit most from admission to an accelerator program. If an accelerator program’s main role is to provide direct organizational sponsorship (i.e., resource buffering and direct bridging ties), there should be no difference between an accelerator’s impact on firms founded in the accelerator’s ecosystem and its impact on those founded elsewhere. Thus, if an accelerator’s effect occurs entirely through the direct structured process inside the program, the only difference in terms of resource acquisition should be between admitted and unadmitted firms. If, however, a key piece of an accelerator’s effect emerges from the accelerator facilitating systems of interorganizational learning and exchange, startups that come from the region in which the accelerator operates should benefit more from acceleration because they carry with them both overlapping and nonoverlapping connections relative to the accelerator. Nonoverlapping connections bring new perspectives and information into the accelerator (Beckman and Haunschild, 2002), while overlapping ties bring increased trust and familiarity (Gulati, 1995). Therefore, if ecosystem spillovers provide an additional channel through which an accelerator impacts its startups, I would expect differences in levels of resource acquisition between admitted firms originally from the accelerator’s ecosystem and admitted firms from outside the ecosystem.

If startups admitted to an accelerator draw in new resources or improve existing interconnections in their founding ecosystem, their ability to do so depends in part on the quality of that environment. A key dimension in defining this quality is geographic proximity to organizational actors with key resources that the startup needs for growth, actors such as venture capitalists (Sorenson and Stuart, 2001) and corporations that can serve as early partners and customers (Agrawal and Cockburn, 2003). Geographic proximity increases the likelihood of many of the social exchanges that enable new ties with these organizational actors (Hallen, Davis, and Murray, 2020). Not surprisingly, startups that are founded closer to venture capitalists or corporations are more likely to eventually form relationships with them (Sorenson and Stuart, 2001; Agrawal and Cockburn, 2003; Chen et al., 2010).

Venture capitalists in particular play a critical role in not only startup performance but also the strengthening of entrepreneurial ecosystems within and across geographic boundaries. 5 In addition to providing early-stage capital to new firms, venture capitalists provide technical information, advice, and connections that improve startup outcomes (Pahnke, Katila, and Eisenhardt, 2015; Bernstein, Giroud, and Townsend, 2016). Venture capitalists also help shape entrepreneurial activity in a region by improving information flow between new and established firms (Hsu, 2006; Romanelli and Feldman, 2006). While the activity of venture capitalists tends to be highly geographically localized (Sorenson and Stuart, 2001; Chen et al., 2010), they can be responsive to new opportunities in other regions (Hausman, Fehder, and Hochberg, 2020). Venture capitalists often use syndication activity to broaden their scope outside narrow geographic boundaries (Sorenson and Stuart, 2001).

Startups with potential to connect to venture capitalists through geographic proximity at founding may be able to use the good news of accelerator admission to generate interest from nearby venture capitalists (Hallen, 2008) and draw them into the ecosystem being orchestrated by the accelerator. Thus, a startup’s proximity to venture capitalists in its founding environment may provide a potent input to the acceleration process.

Accelerator programs foster organizational processes and interaction norms among program participants that increase the flow of information and insights. The design of accelerator programs can vary substantially in terms of the structure of mentorship, the composition of program cohorts, and the degree to which participants interact, especially through shared work space; differences in design choices can substantially alter the program’s impact on startups (Cohen et al., 2019; Hallen, Cohen, and Park, 2023). The most successful accelerator programs exhibit interlocking design choices that increase openness, transparency, and reciprocal sharing of information and resource leads (Hallen, Cohen, and Bingham, 2020; Krishnan et al., 2021).

Moreover, overlapping entrepreneurial support programs in the accelerator ecosystem can yield strong complementarities. A growing literature has documented how the presence of interdependent support organizations and sponsors promotes entrepreneurial entry and survival (Autio et al., 2018; Vedula and Fitza, 2019; Vedula and Kim, 2019), and accelerator practitioners also note the importance of overlapping programs. Techstars founder Brad Feld found that regularly scheduled networking meetings in Boulder were a key input to the formation of Techstars, allowing its founders to draw both prospective startups and mentors into the program (Feld, 2012). A founder of MassChallenge similarly noted the importance of a regular entrepreneurship meetup in the Boston area: “In many ways the Venture Café program provided an early boost to our program by providing a group of investors and executives that already saw the benefit of meeting new startups, giving them advice, and seeing how they develop on a regular basis.”

In startups’ founding environments, formal networking meetings offer important training that better prepares startups for participation in an accelerator. Startups benefit substantially from regular contact with other entrepreneurs and stakeholders who can provide information, feedback, and resource leads (Baum, Calabrese, and Silverman, 2000; Davidsson and Honig, 2003). Planned networking meetings may also be viewed as a marker of the level of social capital in an entrepreneurial ecosystem. While definitions of social capital vary substantially (Putnam, Leonardi, and Nanetti, 1994; Fukuyama, 1995; Glaeser, Laibson, and Sacerdote, 2002), one prominent research stream connects associational activity in a region to prevailing norms of openness and trust (Putnam, 1993, 1995). Within this tradition, frequent meetings of broad groups of community members in religious and civic settings are both a cause and a consequence of higher social capital (Ruef and Kwon, 2016).

Higher levels of social capital and the associated improvements in generalized trust and openness have been connected to increased information flow (Adler and Kwon, 2002), which is important for many types of economic activity. While many studies have conceptualized social capital as an individual-level construct that can be appropriated by strategic individuals (Hoang and Antoncic, 2003), a growing body of evidence suggests that community-level social capital is as important or more important for explaining rates of entry and aggregate entrepreneurial performance (Laursen, Masciarelli, and Prencipe, 2012; Kwon, Heflin, and Ruef, 2013). Related, higher levels of associational activity in a region, both a cause and consequence of social capital, lead to higher levels of entrepreneurship in the region (Schulz and Baumgartner, 2013). More generally, rates of entrepreneurship may be sensitive to the ease with which individuals mix socially (Samila and Sorenson, 2017) and geographically (Dutta, Armanios, and Desai, 2021).

Thus, proximity to formal networking events in a startup’s founding ecosystem can have several related effects that might influence the impact of acceleration. Given entrepreneurs’ sensitivity to the proximity of key resources (Guzman and Stern, 2015; Egan, 2021), founders of startups that are nearer to formal entrepreneurship networking events are more likely to attend and benefit from them. In addition, the presence of these events nearby signals higher levels of community-level social capital. Startup founders who have their earliest experiences in higher-trust environments are more likely to commit to the norms of openness inside accelerators. They are also more likely to carry the accelerator’s exchange norms into a receptive community. For these reasons, I argue the following:

Research characterizing which features of a startup’s ecosystem improve performance (Autio et al., 2018; Vedula and Fitza, 2019; Vedula and Kim, 2019) has emerged but reflects substantial variation in the geographic scale used to proxy for the ecosystem. Recent research has suggested that macro-level entrepreneurial ecosystems can be broken down further into sub-clusters in which entrepreneurs tend to spend most of their time (Kerr and Kominers, 2014). Scholars have observed similar sub-cluster effects among venture capitalists (Florida and King, 2018). Small differences in distance and access can have large impacts on the types of information exchange necessary for innovation and entrepreneurship (Arzaghi and Henderson, 2008; Catalini, 2018). Thus, startups founded in the same ecosystem may differ in their ability to take advantage of an accelerator program if their access and proximity to organizational sponsors such as venture capitalists differs. A participant in MassChallenge’s accelerator program who hailed from Kendall Square, a center of entrepreneurship in the Boston region, shared, “I already knew many of the people I wanted to talk to, and participating in the program seemed like an easy way to line up a series of conversations without having to call in a lot of favors.” While this founder already clearly understood the people and institutions they wished to access while in the accelerator program, not all startups founded in the same ecosystem would necessarily have the same access and proximity to investors. Thus, I argue the following:

Methods

Empirical Context

This study exploits rich administrative data from MassChallenge, a top accelerator and the world’s largest startup accelerator program by cohort size (Hochberg, Cohen, and Fehder, 2017). MassChallenge admits 128 startup firms each year in late June. MassChallenge’s program broadly fits with the structure of standard accelerator programs that focus on provision of advice and information from a broad set of experts, commonly referred to as mentors, in the accelerator community (Cohen and Hochberg, 2014; Cohen et al., 2019).

The quality of an accelerator program is driven substantially by the quality of the mentor community available to help its portfolio firms (Cohen et al., 2019), and MassChallenge’s mentor community includes some of the most important investors and entrepreneurs in the Boston metropolitan area. MassChallenge was founded by a graduate of MIT Sloan and a graduate of HBS with substantial input, guidance, and support from faculty members and alumni from both institutions. MassChallenge’s mentor community sits at the center of Boston’s innovation-driven entrepreneurship community.

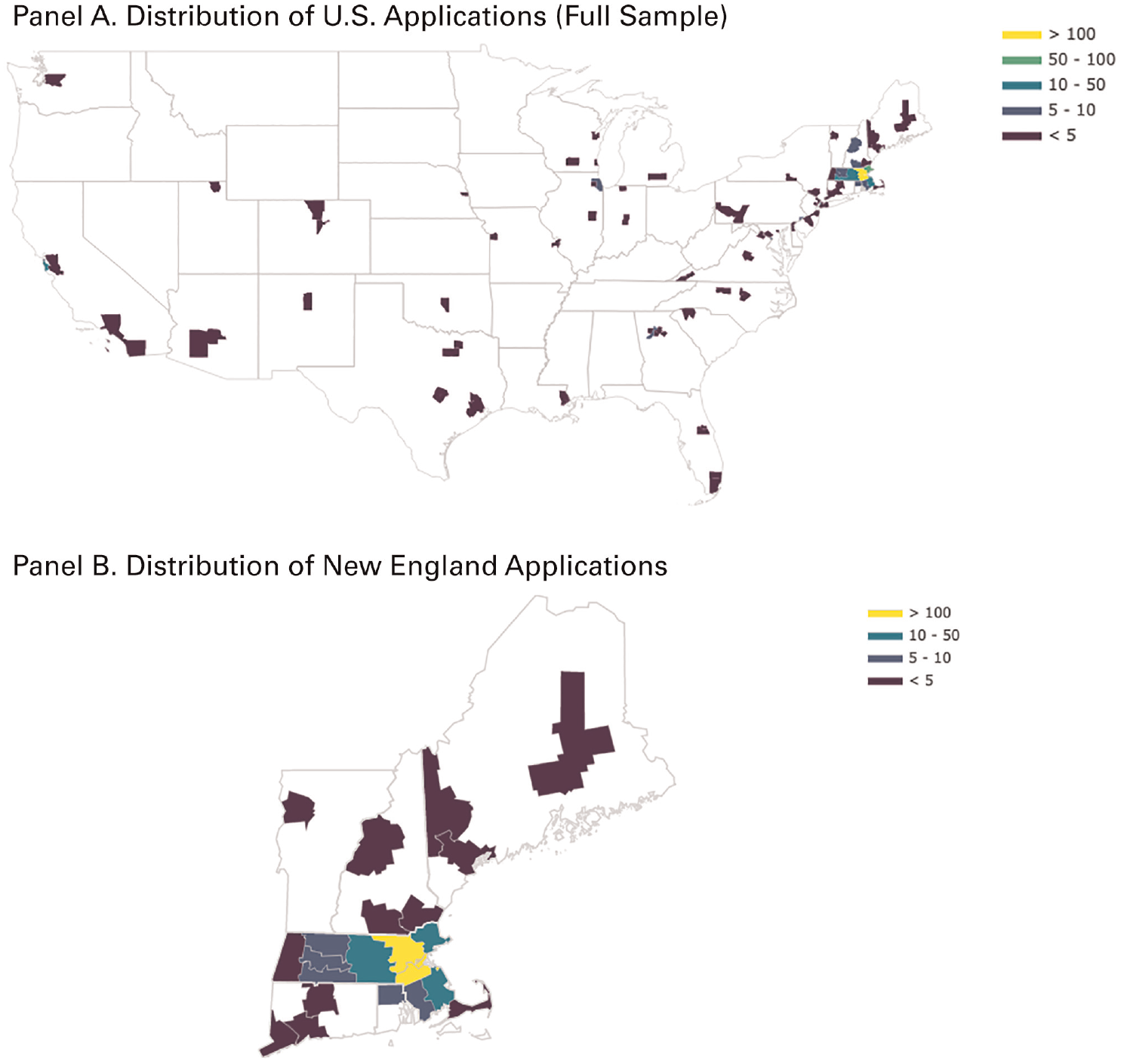

MassChallenge also draws broadly from regions across the United States, although its applicant pool is centered in the greater Boston metro area. Figure 1 shows the distribution of applicants by county both across the United States (panel A) and in the New England region (panel B). The majority of applicants in the sample (58 percent) were founded in the Boston combined metropolitan statistical area, but there are significant clusters of applicants from Philadelphia, New York, Atlanta, and Silicon Valley. In the analysis below, I use this variation in founding locations (local and distant) and in the quality of the startups’ local environments to disentangle the impact of location on acceleration.

Mapping the Distribution of MassChallenge Applications by U.S. County

MassChallenge is relatively unusual in that it keeps careful quantitative measures of its admission process. Each year, each startup applicant is evaluated by three to five experts drawn randomly from a pool of venture capitalists, successful entrepreneurs, corporate innovation officers, and lawyers specializing in serving new innovation-driven firms. Critically, evaluations are designed to be independent and fair. Each judge is randomly assigned to the evaluation panel, conditional on their not having had previous contact with the startup. Each judge provides an independent score of the startup based on a written application and in-person (or video) pitch that describes the startup’s business plan and the quality of its founding team. While MassChallenge collects information on the startup’s founding location at the time of application, it is not part of the formal evaluation process. The individual scores from each judge are averaged across all judges, and each startup’s average score plays a nearly deterministic role in admission to MassChallenge for a fixed number of slots. 6

I explore the importance of the judging process in my section below on empirical approach, where I argue that it provides an ex ante measure of the perceived quality of each firm. Note that my analysis does not require the judges to be right in their assessments; rather, it requires their scoring to reflect the startup’s underlying quality but also to reflect some errors, so that startups of similar quality can end up above and below the score cutoff required to garner one of the 128 spots.

Sample

My sample was composed of 1,150 startups that were semi-finalists or finalists in the MassChallenge accelerator from 2010–2013. This represents all cohorts from the beginning of the program for which at least two years of performance data could be collected at the time of data collection. I excluded social enterprise not-for-profit startups, which would not pursue outside financing from venture capitalists.

I observed key characteristics of each startup from their application to MassChallenge. First, I observed their geography. For startups that did not provide their location at the zip code level, I conducted web searches to supplement the information. Second, I obtained the identities of founding team members from MassChallenge and downloaded links to personal websites and social media accounts, which allowed me to code the founding team for a range of covariates, including gender, age, and educational background. Lastly, I observed the aggregate Judge score for each startup, which generates the admission decision for MassChallenge. Table 1 summarizes the data sources for each variable described below.

Data and Sources*

MC–MC application; LI–LinkedIn; VX–VentureXpert; CB–Crunchbase; MT–Meetup.com; ACS–American Community Survey of the Census; NSF–National Science Foundation.

Dependent Variables: Resource Acquisition

Like most accelerators, MassChallenge requires applicants to be at an early stage of development: they cannot have received funding beyond friends and family or have entered their intended market in a substantial way. The purpose of the MassChallenge program, and accelerators more broadly, is to improve the constellation of choices (from customer choice to business model) that represent a startup’s entry strategy (Hallen, Cohen, and Bingham, 2020).

The effects of acceleration are thus best observed in a limited time window after firms’ graduation. Because all firms that applied to the accelerator were in the same early stage of development at the time of their application, I could compare how admitted and unadmitted firms fared in their ability to move from an early stage of development focused on ideation to an execution phase during which firms must acquire resources to enter their market and grow. While the extent of their resource needs varies by their strategy, nearly all growth-oriented startups need both external financing and employees. Prior research has noted that the two are interrelated but not perfectly correlated, as some firms may use revenue from early customers to fund the hiring of employees, while others use higher levels of early-stage financing from VCs to do so (Piezunka and Dahlander, 2015; Hallen, Cohen, and Bingham, 2020; Botelho, Fehder, and Hochberg, 2021).

To assess the impact of accelerator admission on firms’ ability to acquire the resources necessary for growth, I used four measures of resource acquisition in the two years after the graduation of the accelerator cohort to which the startup applied. The first two dependent variables measure the level of external financing the firm obtained within the first two years after the graduation of the cohort to which the startup applied; the second two measure the number of employees in the firm. Two of the four dependent variables are dichotomized, with thresholds determined based on a series of interviews with venture capitalists and angel investors affiliated with MassChallenge. I set the thresholds to represent the best separating values between startups that identified a valuable opportunity and were actively building an organization to pursue it and those that did not. These dichotomized variables ensure that no extra weight was given to startups that pursued higher levels of capital or employment for business-specific reasons. In addition, they provide an easy, probabilistic interpretation of marginal effects (Angrist, 2001).

To construct my external financing variables, I first downloaded early-stage financing data from VentureXpert and Crunchbase and filtered to include only funding that occurred in the first two years after the graduation of the cohort to which the startup applied. Using a proprietary dataset of funding rounds obtained from an investor, I determined that VentureXpert was more accurate for later rounds of financing from institutional investors but could miss early investments from angel investors. If data from both sources existed for a startup, I used the Crunchbase data for financing rounds that occurred prior to the first round listed in VentureXpert. If data from only one source existed, I used only that one. Startups without any financing data were listed as having zero external financing. Having constructed these aggregated external financing data, I recorded the total amount of financing each startup raised in the two years after having applied to MassChallenge. I set Substantial funding to one when a startup received more than $500,000 in early-stage funding and to zero otherwise. This threshold was chosen because investors report that contracts above this threshold generally are more complicated and have clear milestones (i.e., significant uncertainty has been resolved in the opportunity). I set Logged funding as log(1+x) where x represents the total amount of financing raised.

To construct employment measures, I collected information from LinkedIn on all startup employees, careful to count only non-founder and non-intern workers listing employment in the startup within the first two years after the graduation of the cohort to which the startup applied. From these data, I constructed two variables. I set Substantial employment to one when a startup had 15 or more employees and to zero otherwise. This threshold was chosen because the investors I interviewed suggested that this number was a good indicator of when a firm was transitioning from exploring potential business models to executing a specific one that had shown promise. Next, I constructed Logged employment as the log of total employment, using the formula log(1+x).

Independent Variables: Accelerator Admission, Proximity to Venture Capitalists, and Regional Social Capital

A formal admission process drives access to the accelerated environment provided by MassChallenge. I captured two key elements of this process: (1) whether a startup in my sample received a formal offer of admission to the accelerator, coded as the dichotomous variable Accelerated, and (2) how close the startup was to the admission threshold. To characterize distance from the admission threshold, I normalized the average judge score for each organization by the score of the 128th-ranked startup in that year’s applicant class. Because admission offers are based almost entirely on the relative rank generated by average judge scores, I could create cohorts of nearly admitted and nearly rejected organizations.

For my next two independent variables, building on the work of Sorenson and Audia (2000), I calculated an index that measures the geographic proximity of each startup’s home environment to key ecosystem resources at the time of application. These measures count the occurrence of a key resource, like venture capitalists or networking meetings in a startup’s environment, but they weight more-distant resources less than those closer to the startup’s location. While I provide more detail on each index below, I first describe the overall index calculation procedure.

Using the address of each startup from its MassChallenge application, I first used Google’s geocode platform to geocode each startup’s headquarters as a latitude and longitude based on the center of its zip code. Next, I calculated the distance between each startup and each occurrence of a specific resource type (e.g., venture capitalists or networking meetings). Then, I collected counts of each resource type within one-mile bands from the startup (e.g., one mile away, two miles away). With these data, I computed the index using the formula

where for startup i,

For my measure of networking opportunities, Meetings, I collected all data on entrepreneurial meetup groups in the United States from the website Meetup.com, a platform for informal interest-based communities to form and organize meetings. I captured the number of entrepreneurship group meetings that were held in each U.S. zip code and then computed my proximity index, Meetings, as the distance-weighted count of proximate opportunities, using the Sorenson and Audia (2000) formula.

I created a similar proximity index for Regional investors by downloading information from VentureXpert on all investment activity in the three years before each application year to MassChallenge. I created counts of distinct investors with headquarters in each zip code and computed my proximity index as the distance-weighted count of proximate opportunities, using the Sorenson and Audia (2000) formula.

Control Variables

My empirical approach used each startup’s average judge score to proxy broadly for the factors that might impact a venture’s attractiveness to the resource holders from whom it likely sought ties. I approached this proxy for perceived quality with caution by providing additional controls for characteristics that may have affected each venture’s ability to form ties.

I began with a series of dichotomous control variables to control for founder demographic characteristics that prior research has found to be related to a startup’s performance. I coded Female founder as one if at least one founder listed in the application was female and zero otherwise. Following the convention in other entrepreneurship research (Piezunka and Dahlander, 2015; Hallen, Cohen, and Bingham, 2020), I coded Elite education as one if at least one member of the founding team attended a school rated in the top 15 according to the U.S. News and World Report survey, and zero otherwise. I coded MBA as one if at least one founding team member had an MBA degree and zero otherwise.

Next, I captured two measures of each startup firm that have been correlated to startup performance in previous research. I coded Firm age as the year of each startup’s application to MassChallenge minus the year of the startup’s founding. I coded Team size as the number of founders and full-time, non-founder employees at the startup’s time of application.

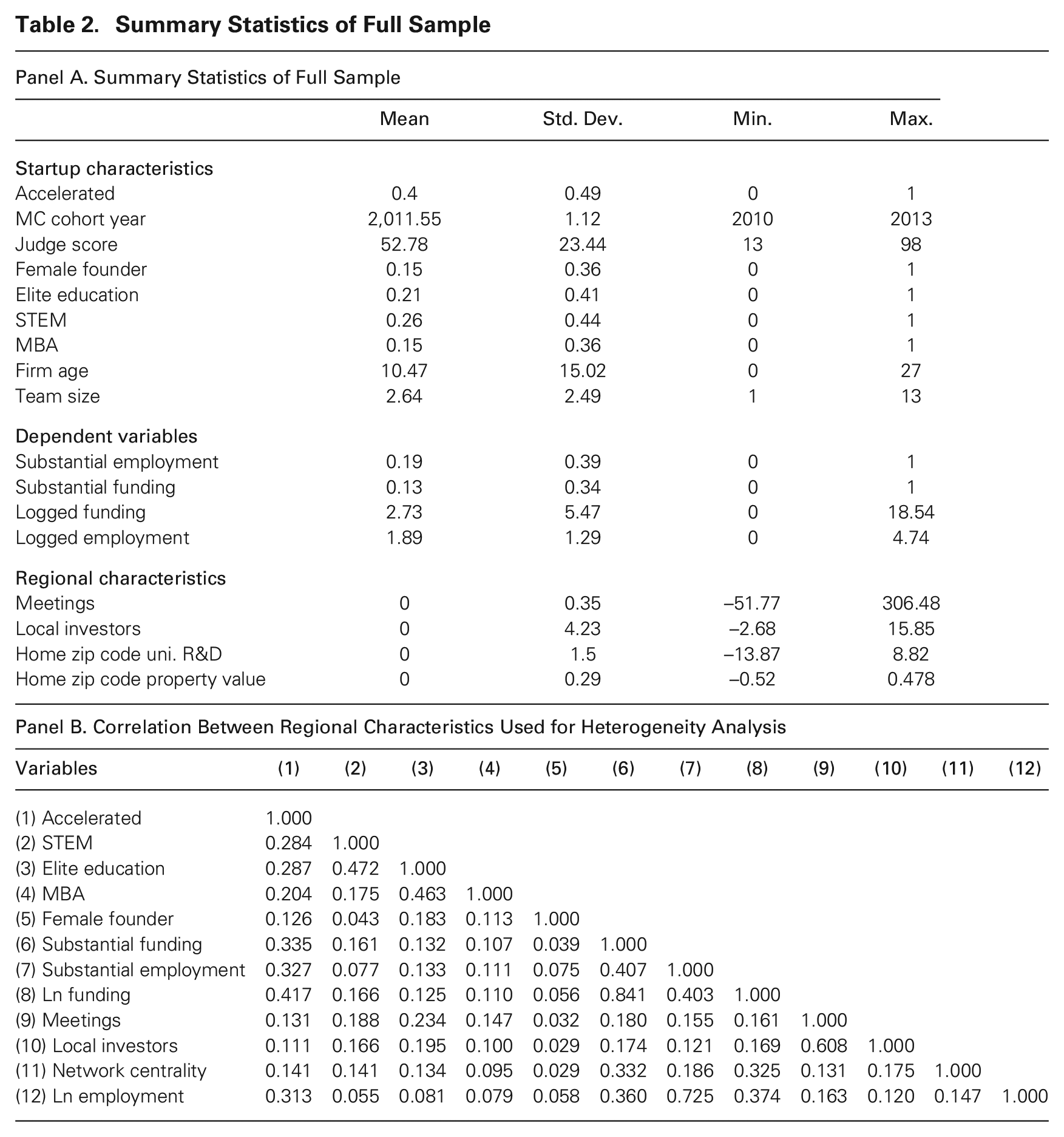

Table 2 provides summary statistics for each variable used in my analyses. The startups considered in this study are those that reached semifinalist status, meaning all startups in the sample that were judged to be attractive ventures in an initial screening round. It is not surprising, therefore, that the unconditional mean for a startup to obtain Substantial funding was 0.13, or 13 percent of the sample. This is far above the funding rate for new startups, even in funding-rich areas like Boston or Silicon Valley (Guzman and Stern, 2020). Similarly, the unconditional chance of a startup reaching Substantial employment was 0.19 in the sample, or 19 percent of the total study population. While all startups face significant challenges, these startups are high quality regardless of the admission decision to MassChallenge.

Summary Statistics of Full Sample

Each semifinalist received an average score from a panel of judges. The highest theoretical score was 100, while the lowest theoretical score was 0. In my sample, I observed an average of 52.78, with a minimum score of 13 and a high score of 98—substantial variation in the perceived quality of the startups. This variation served an important role in creating cohorts of admitted and unadmitted organizations that were substantially similar, as I describe below.

Empirical Analysis

I had three main objectives for this study. The first was to create two sets of organizations that would allow me to characterize the attractiveness of the accelerated environment. One set was given access to a new environment (i.e., admitted to the accelerator), and the other set remained in their founding environments but were plausibly similar to the admitted startups in their perceived quality. The difference in resources acquired between the two sets of organizations provides a direct measure of the quality of the accelerated environment. The second objective was to observe whether local environmental variables at founding influenced the accelerator’s subsequent impact on admitted organizations, relative to the organizations that did not gain admission. The third objective was to account for whether the impact of the founding environment varied for startups founded in the same ecosystem as MassChallenge, relative to startups admitted to MassChallenge that were founded elsewhere.

The heart of my empirical strategy was to exploit the judge’s numerical scores of perceived venture quality, which generated admission decisions, in order to compare startups that nearly received access to those that nearly did not receive access to the accelerated environment. To do so, I used a regression discontinuity framework.

For each startup that applied to MassChallenge, I observed a set of characteristics at the time of application, whether it was admitted, and how the startup performed over time in terms of reaching key performance objectives. Thus, the following equation describes the basic linear relationship between admission to the program, the characteristics of the startups at the time of application, and subsequent realized resource acquisition:

Here, γ measures the relationship between admission to the accelerator program, Accelerated, and the startup’s performance conditional on the level of other covariates; β measures the relationship between the startup’s baseline observable characteristics and performance; and

Thus, a simple ordinary least-squared estimate of equation (2) will likely yield a biased estimate of the quality of the accelerated environment in MassChallenge if the firms admitted to the accelerator vary substantially in an unmeasured variable, like startup quality, that is omitted from the regression but substantially correlates with the dependent variables measuring firms’ performance. If one could obtain estimates of startup quality that were free of measurement error, then equation (1) could still recover the causal impact of admission to a startup accelerator. Unfortunately, such measurements are unlikely, for even experienced investors are not necessarily able to distinguish good and truly excellent ideas (Kerr, Nanda, and Rhodes-Kropf, 2014). Fortunately, I observed a useful proxy for startup quality in my setting: the judge score in the MassChallenge admissions process—the quantitative score used for admitting firms to the program.

While the judge score is not a perfect measurement of startup quality, it relates to downstream performance of startups in two ways. First, it is correlated with the likelihood that startups can secure ties to resource holders and thereby grow substantially but is not perfectly correlated with the other observed characteristics of the startup and startup founders. Thus, the judge score picks up aspects of a startup’s quality that cannot be observed through available demographics. Next, the judge score drives admission decisions for MassChallenge. Indeed, because MassChallenge has a limited and fixed number of slots each year, the admission procedure creates the possibility that startups with very similar judge scores receive different admission decisions.

If there is a discontinuous jump in the probability of receiving admission to MassChallenge that is driven by institutional capacity constraints defined before judges review applications, this jump can serve as a useful wedge to separate ex ante quality, observable characteristics, treatment, and performance. When such a jump exists, the startups that very nearly received admission form a control group for the startups that barely gained admission because very small differences in the judge scores generate very large differences in treatment probability (Lee and Lemieux, 2010). Central to this use of discontinuous jump in probability of treatment is the assumption that startups just above and just below the capacity threshold are comparable. Statistically, a set of assumptions drives the comparability of treatment units above and below the threshold: (1) the score used to generate admission decisions has a random component, (2) neither judges nor applicants can manipulate the score to move a firm over the cutoff, and (3) there are no discontinuities in other observed covariates at the treatment threshold. The first assumption is satisfied trivially by the underlying uncertainty in judging early-stage entrepreneurial projects. The second and third assumptions require careful knowledge of the scoring process and ex post evaluation of potential sorting of candidates at the margin (see Online Appendix A for this analysis).

The fuzzy regression discontinuity framework in the MassChallenge context

My main empirical approach employed a fuzzy regression discontinuity framework (Lee and Lemieux, 2010). Regression discontinuity uses information about an individual startup’s proximity to a threshold for treatment, to estimate the impact of treatment on startups near the cutoff. In its most basic form, when treatment is a deterministic function of receiving a score above the cutoff, a regression discontinuity design estimates the following model:

Here,

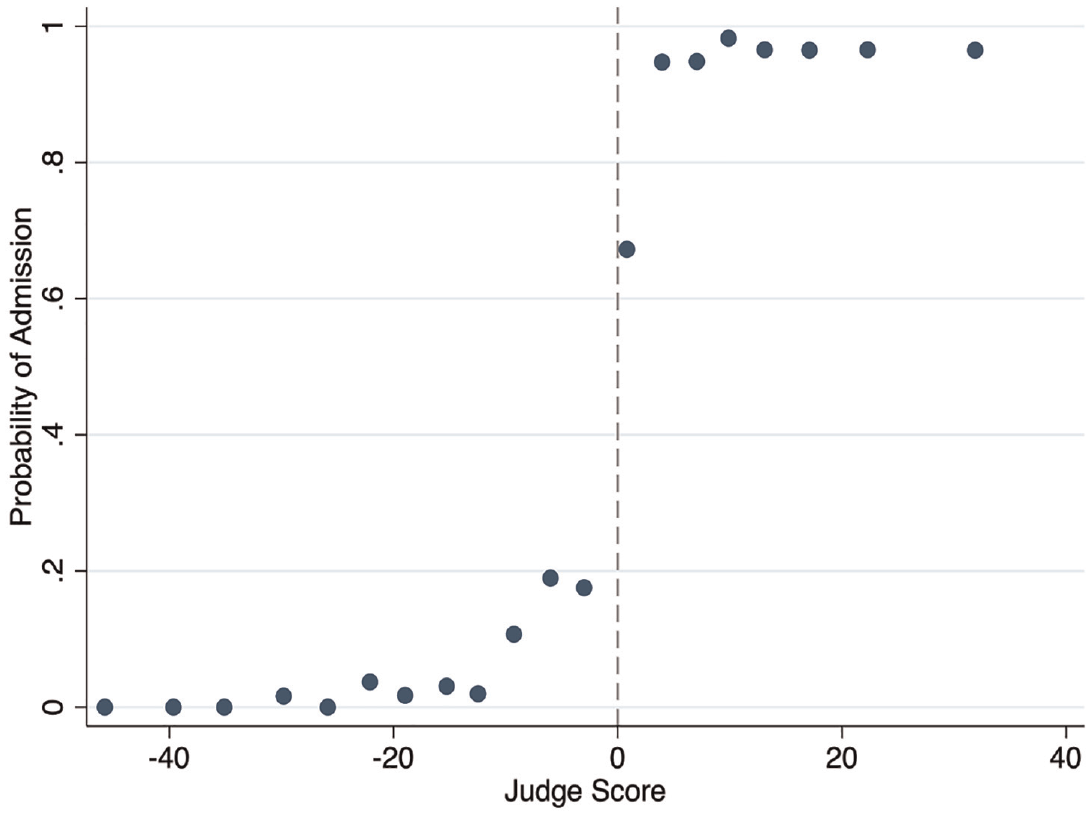

In my data, treatment is not a deterministic function of the score function. In Figure 2, I plot the probability of treatment as a function of the judge score, using a binned scatter plot with 20 equally spaced buckets. While there is a clear discontinuous jump in the probability of treatment at the capacity threshold, some startups below the threshold are admitted, and some startups above the threshold are not admitted, requiring the implementation of a fuzzy regression discontinuity approach. To implement it, I estimated a two-stage regression in which receiving a score above the capacity threshold for admission was a predictor for admission to MassChallenge. My fuzzy regression discontinuity regressions estimated the following:

Relationship Between Judge Score and the Probability of Admission to MassChallenge*

I used the judge score and the fixed capacity of the program to compare startups with scores near the score cutoff for admission. The non-linearity displayed in Figure 2 and measured in equation 4 identifies the local average treatment effect (LATE) of admission to MassChallenge as long as there is continuity in the potential treatment effect above and below the treatment threshold (McCrary, 2008). In simpler terms, startups need to be similar to one another just above and just below the probability discontinuity for treatment.

In addition to visually inspecting the data in Figure 2, I performed the recommended McCrary test and found that I could not reject the null hypothesis of local continuity. Thus, I interpreted

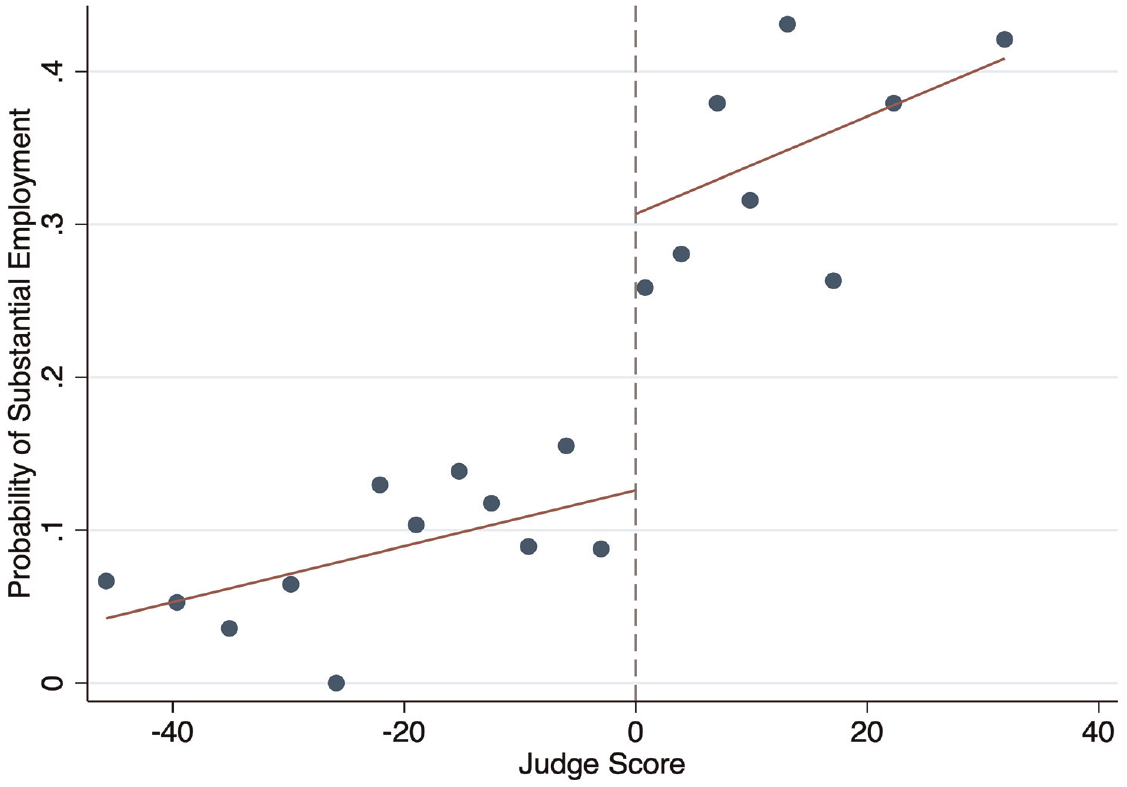

Relationship Between Judge Score and the Probability of Substantial Employment*

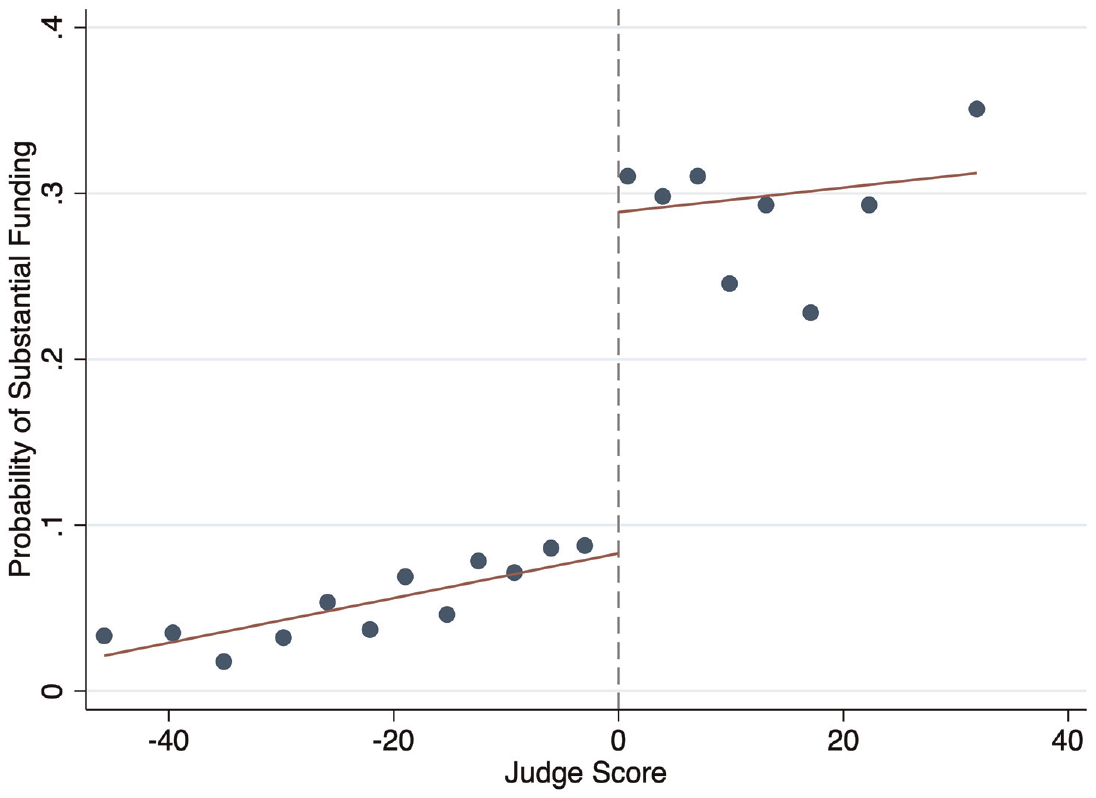

Relationship Between Judge Score and the Probability of Substantial Funding*

While

Again,

Results

Does an Accelerated Environment Improve Startup Performance?

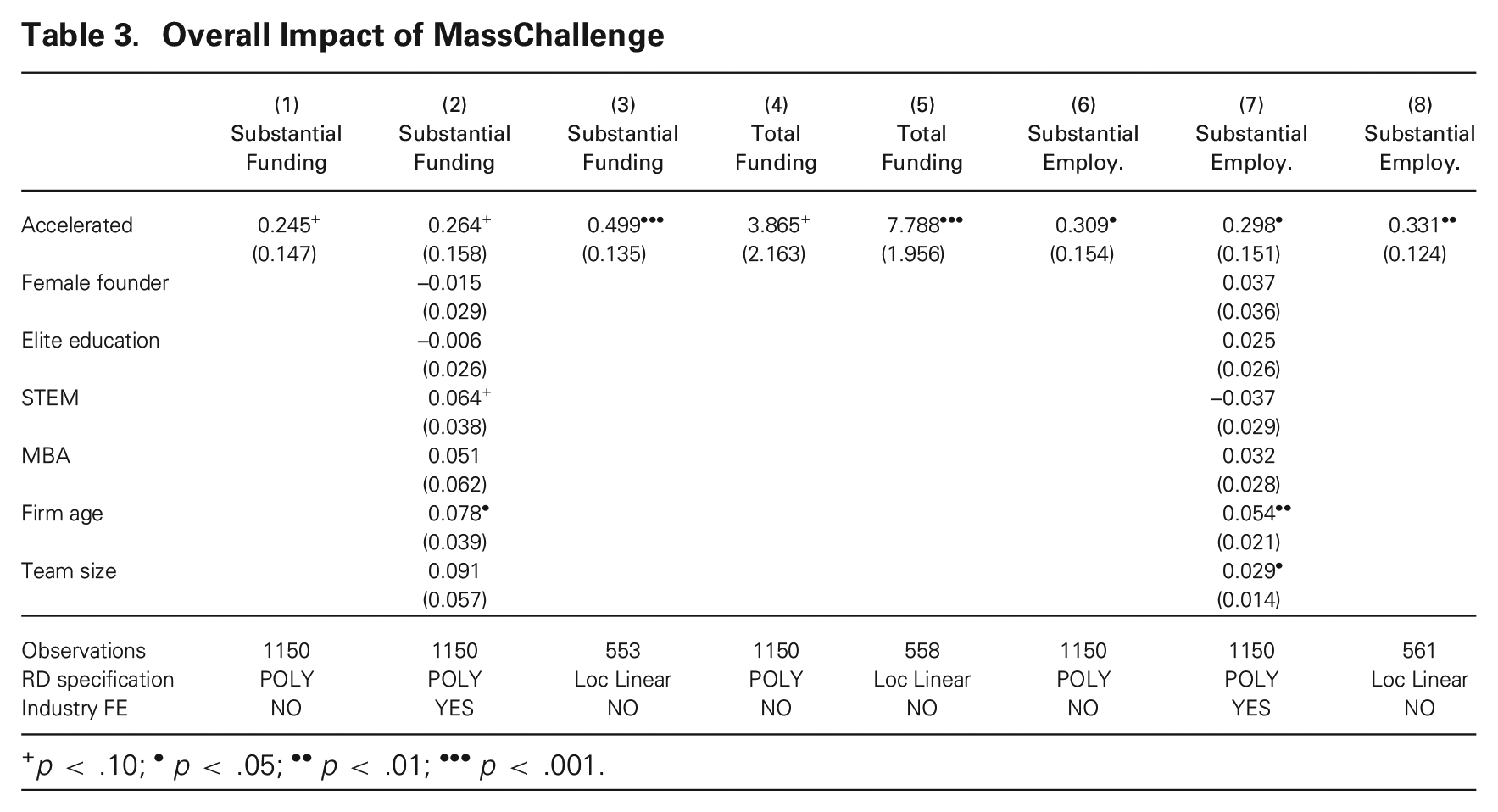

I first examined whether admission to an accelerated environment improves startup performance by improving access to information and experts. My baseline Hypothesis 1 posits that MassChallenge has an overall treatment effect similar to other successful accelerators that have been explored in other research studies. To test H1, I compared accelerated ventures to substantially similar non-accelerated firms, using a regression discontinuity design. The results of the analysis are in Table 3. In Model 3-1, I predicted the likelihood of receiving substantial funding and found that admission is associated with a statistically significant 24.5 percentage point increase in the likelihood of reaching the funding threshold. Model 3-2 confirms that this result is robust to the inclusion of controls.

Overall Impact of MassChallenge

p < .10; •p < .05; ••p < .01; •••p < .001.

Next, I turned to employment as another measure of an organization’s progression and found that gaining access to the accelerated environment increased the chances of reaching substantial employment by a statistically significant 30.9 percentage points (Model 3-6). Models 3-7 and 3-8 explore the robustness of this result to different modeling choices. Thus, I found evidence to support H1.

A substantial literature has emerged providing alternative statistical frameworks for estimating treatment effects in fuzzy regression discontinuity designs (Imbens and Kalyanaraman, 2012). While the use of a standard linear framework with polynomials remains the most common form of regression discontinuity, methodological concerns have emerged about how to use observations that are farther away from the discontinuity. New procedures have emerged that can help assess the sensitivity of regression discontinuity results to choices of how observations farther from the discontinuity are weighted. In Models 3-3, 3-5, and 3-8, I explored the robustness of my main specifications to one key alternative approach. In each of these regressions, I followed a procedure described in Imbens and Kalyanaraman (2012), or IK: I used the data to choose a distance from the 128th-ranked discontinuity (the IK bandwidth) beyond which I excluded data from the regression, and even after excluding data I used a triangular kernel to strongly down-weight observations farther from the discontinuity. Using this alternative approach in Model 3-3, I found an even stronger impact of the MassChallenge program, with a 49 percentage point increase in the likelihood of achieving substantial funding, compared to a 24.5 percentage point increase in Model 3-1. Using this approach, I found substantially similar estimates for substantial employment in Model 3-8, which shows a 33 percentage point increase in the likelihood of reaching the employment threshold, compared to a 31 percentage point increase in Model 3-6, for which I used the polynomial estimate. Given that the polynomial models are more frequently employed in empirical research and more easily interpreted, I continued the rest of my analysis with only the polynomial models, for simplicity of exposition.

I also tested whether my results are robust to my choice of cutoff for my dichotomous dependent variables. Models 3-4 and 3-5 show that my results do not depend on an arbitrary choice of threshold, as I found similar results for logged funding as with the dichotomous dependent variable. Throughout the rest of this discussion of results, I continue to present both the dichotomous and logged versions of the results.

Do Local Startups Experience More Acceleration?

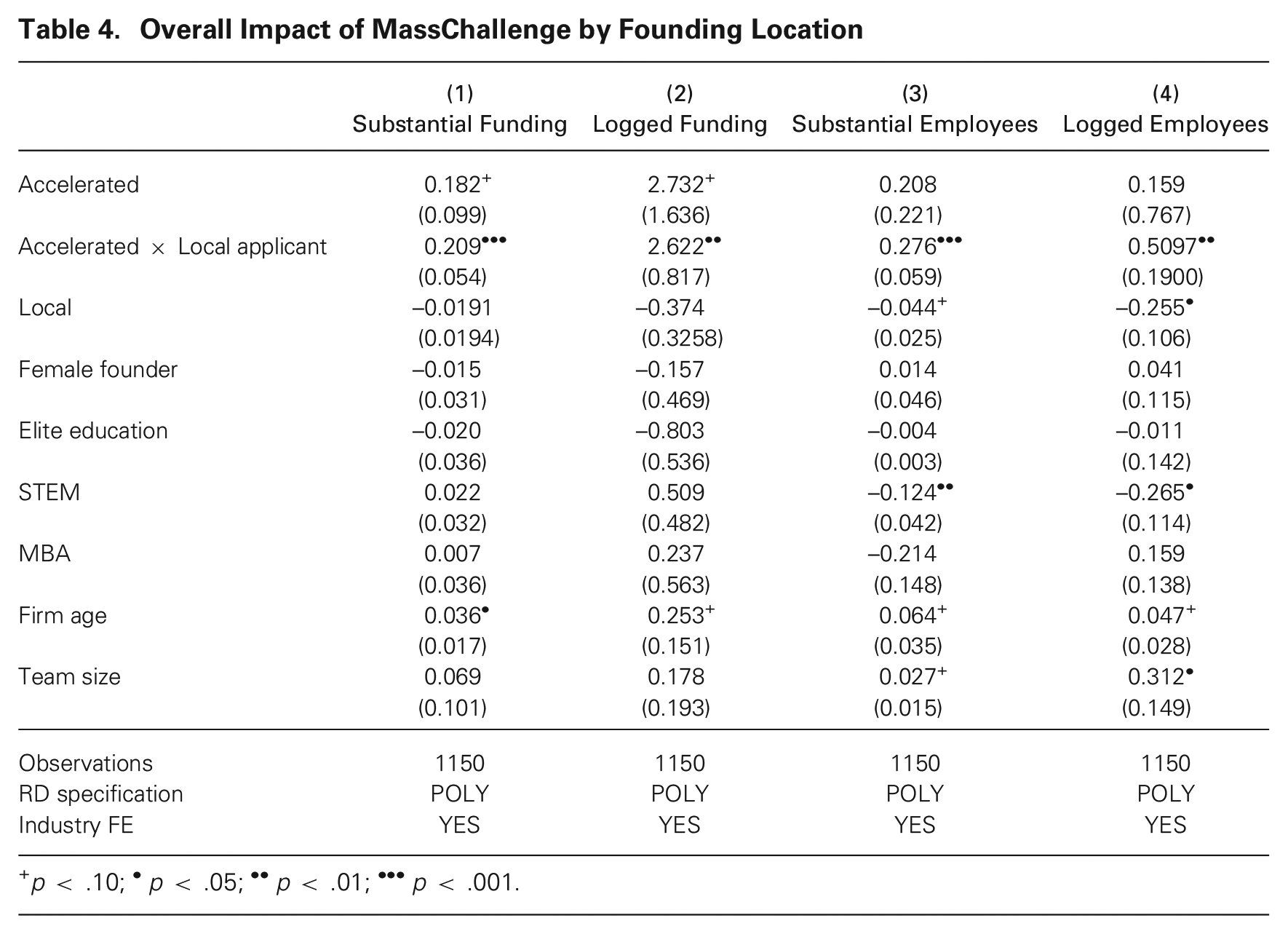

In Hypothesis 2, I argue that startups founded in the Boston entrepreneurial ecosystem will benefit more from admission to MassChallenge relative to admitted startups that were founded in other regions. Table 4 presents the results of the analysis exploring this hypothesis. Model 4-1 shows that firms experienced a statistically significant increase of 18.2 percentage points in their likelihood of gaining substantial funding upon admission to MassChallenge, but local firms experienced a statistically significant additional 20.9 percentage point increase. Model 4-2 repeats the same analysis using logged funding to ensure that this result is not driven by my choice of threshold. Similarly, Model 4-3 shows that firms founded in the same ecosystem as MassChallenge’s seem more likely to reach significant levels of employees, a result that is echoed in Model 4-4 with logged employment data. Taken together, these results support H2.

Overall Impact of MassChallenge by Founding Location

p < .10; •p < .05; ••p < .01; •••p < .001.

Does Founding Environment Moderate Acceleration?

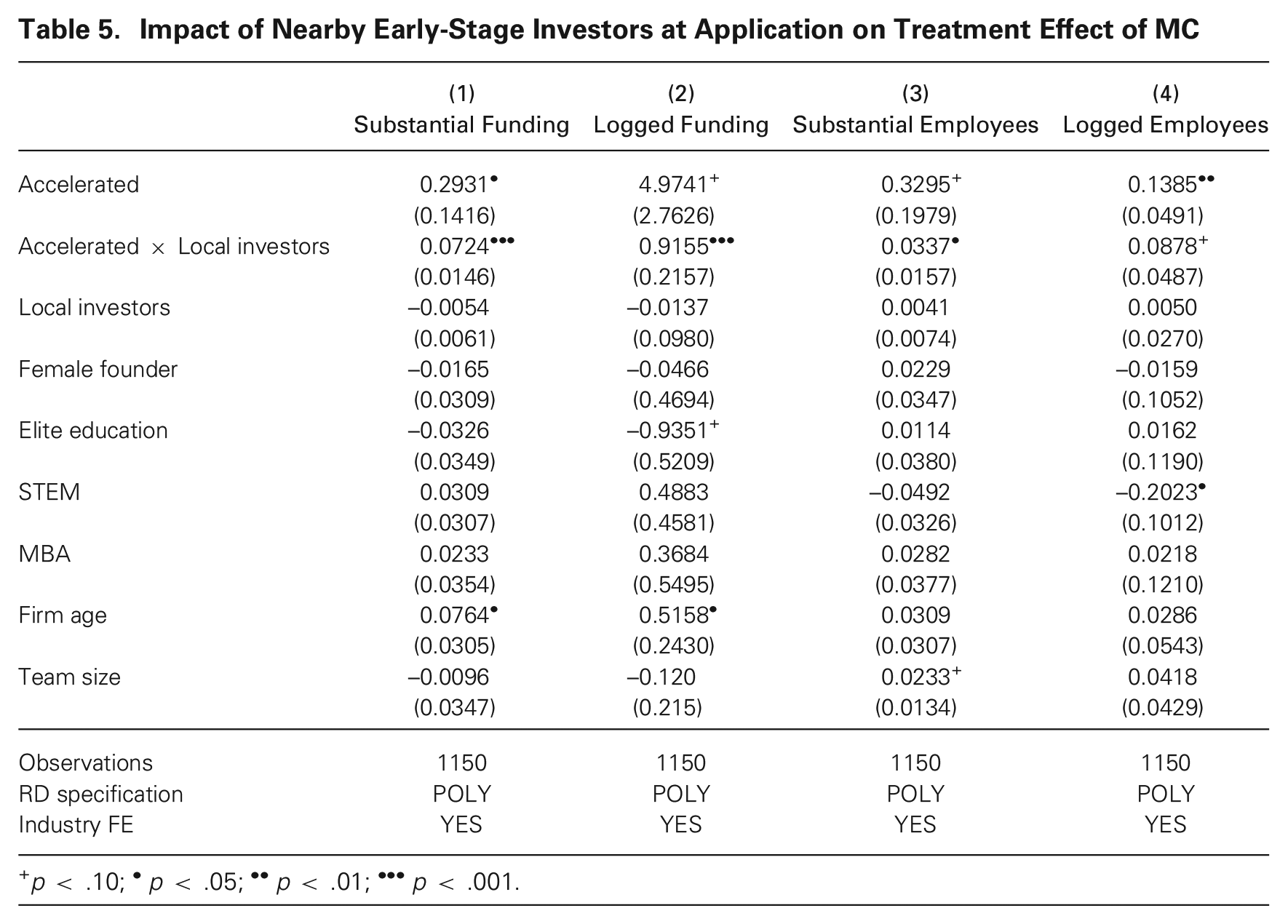

To test Hypothesis 3, I explored whether startups founded in an environment with higher proximity to early-stage investors received greater benefit from the MassChallenge program than startups without this proximity received. For this analysis, the key parameter of interest is the coefficient for the interaction term between Accelerated and Local investors, the index of the number of geographically proximate investors in the startup’s founding environment. An increase of one in the local investors index can come from one additional investor within a mile of the startup’s founding headquarters, from two additional investors more than a mile but less than two miles away, and so on.

In Model 5-1 in Table 5, I found that for a unit increase in the local investor index, there is a positive and statistically significant increase of 7 percentage points in the likelihood of achieving substantial funding. Model 5-2 provides similar results, using logged funding as an alternative measure of external financing. For measures of employment intensity, Model 5-3 shows a statistically significant increase in the likelihood of reaching a significant number of employees, while Model 5-4 confirms the robustness of this result. Taken together, these results support H3.

Impact of Nearby Early-Stage Investors at Application on Treatment Effect of MC

p < .10; •p < .05; ••p < .01; •••p < .001.

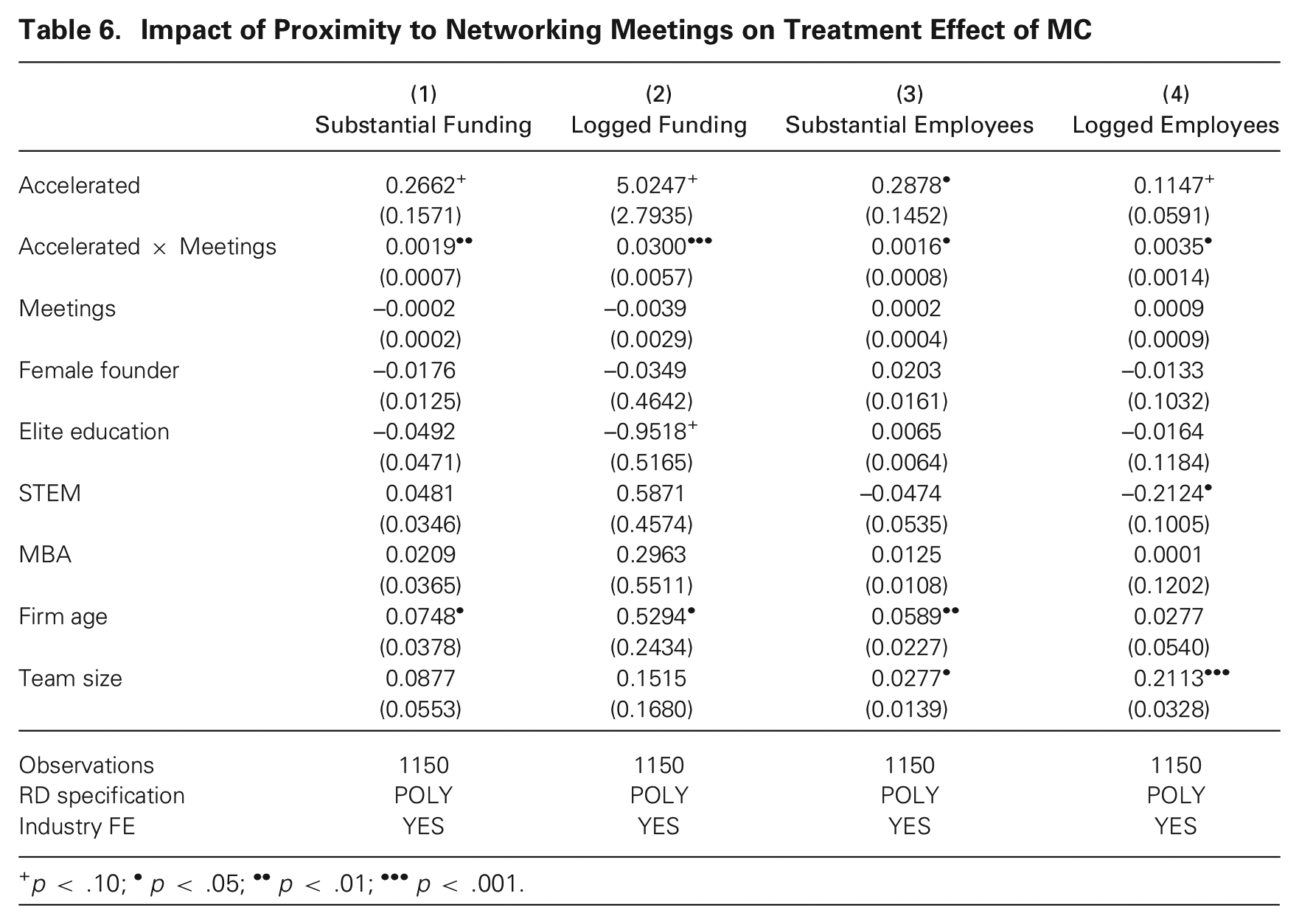

I next tested Hypothesis 4, the moderating impact of proximity to networking events on the treatment effect of MassChallenge. The key parameter of interest in this analysis was the interaction term between Accelerated and Meetings, the index of the number of entrepreneurial networking meetings geographically proximate to the startup’s founding environment. An increase of one in the index can correspond to one additional networking event within a mile of the startup’s founding headquarters, two events within two miles but greater than one mile, and so on. In Models 6-1 and 6-3 in Table 6, I found an overall positive moderating influence of proximity to networking events on the impact of MassChallenge admission on both the likelihood of receiving substantial funding and achieving substantial employment. Models 6-2 and 6-4 show that these results are robust to alternative measures of external financing and employment. In Online Appendix B, I confirm the robustness of these findings to the inclusion of additional covariates describing the startup’s founding environment. In addition, Appendix B provides evidence that the quality of a startup’s founding environment also predicts the quantity of customer and investor referrals that admitted firms are able to obtain from mentors during the accelerator program.

Impact of Proximity to Networking Meetings on Treatment Effect of MC

p < .10; •p < .05; ••p < .01; •••p < .001.

Exploring the Joint Impact of Founding Environment and Proximity to MassChallenge

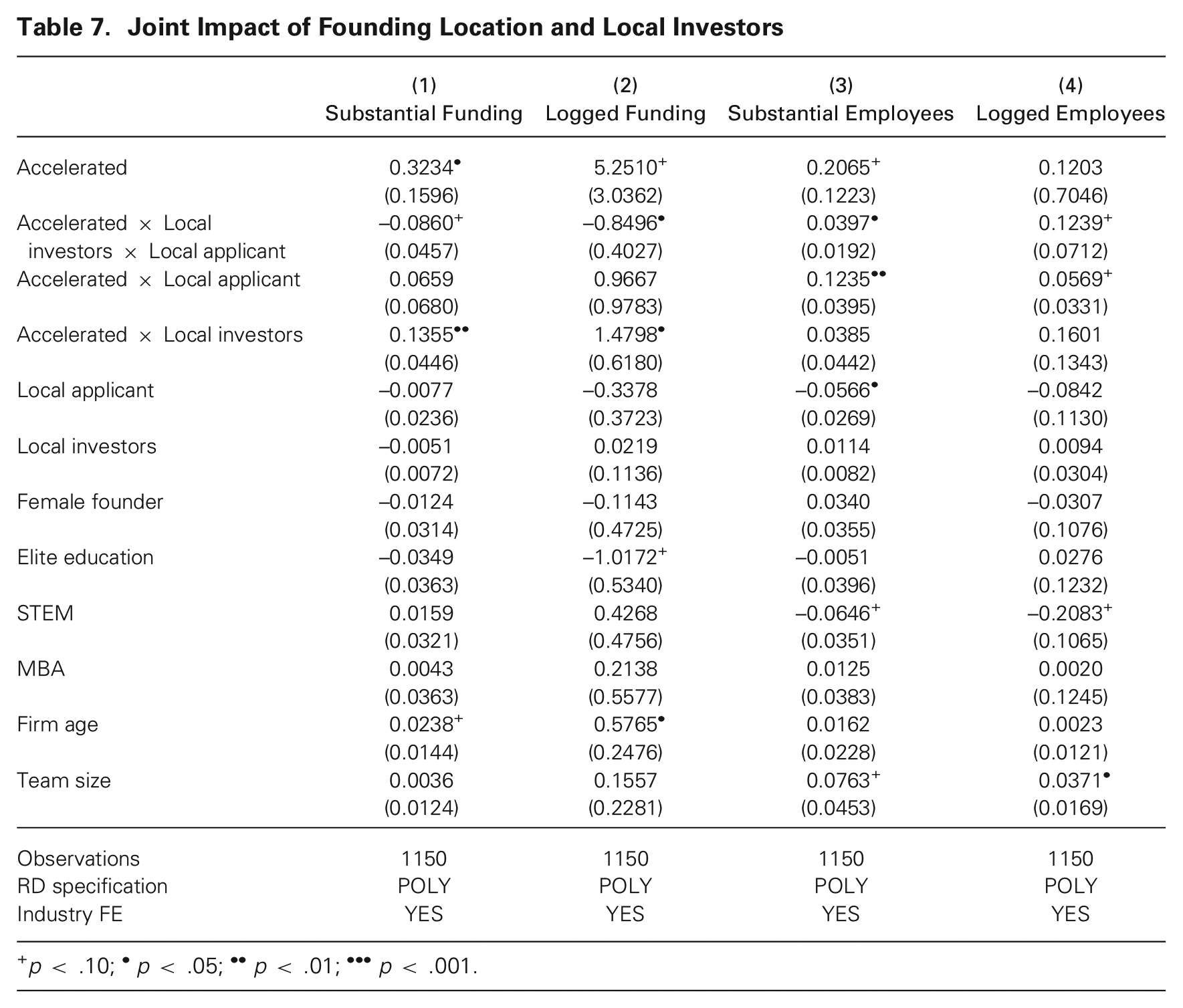

In the prior analysis, I considered separately the impact of two key aspects of a startup’s founding environment on the average benefits derived from admission to an accelerator: geographic proximity to the accelerator and the quality of the startup founding environment in terms of geographic proximity to other key resources. Having established that both the startup’s founding environment and its location in the same ecosystem as MassChallenge’s separately moderate the treatment effect of admission to the program, here I present evidence for Hypothesis 5, which posits that there will be a positive interaction effect of both the founding environment and being founded locally.

Table 7 presents results on the joint impact of founding location and the number of local investors in the startup’s early environment. Interestingly, I observed a negative interaction effect in Models 7-1 and 7-2, meaning that the moderating influence of proximate early-stage investors on raising external financing is smaller for startups founded in the same region as that of MassChallenge than for those founded in more-distant regions. These results suggest that while proximity to investors matters, the role of investor proximity might shift when startups travel from outside their home regions to attend MassChallenge. Founders who are interacting with Boston venture capitalists for the first time may experience heightened readiness for those interactions, compared with local founders who are more likely to have interacted with local venture capitalists prior to participating in the accelerator. Startups local to Boston may not need the accelerator to catalyze those connections as much as startups from other areas do.

Joint Impact of Founding Location and Local Investors

p < .10; •p < .05; ••p < .01; •••p < .001.

In contrast, the moderating influence of investor proximity in a startup’s founding environment is reversed in the probability of employment levels. Model 7-3 shows a positive and statistically significant triple interaction term, meaning local startups with close proximity to investors are more likely to have larger workforces. This result is robust to different measures of employment, as shown in model 7-4.

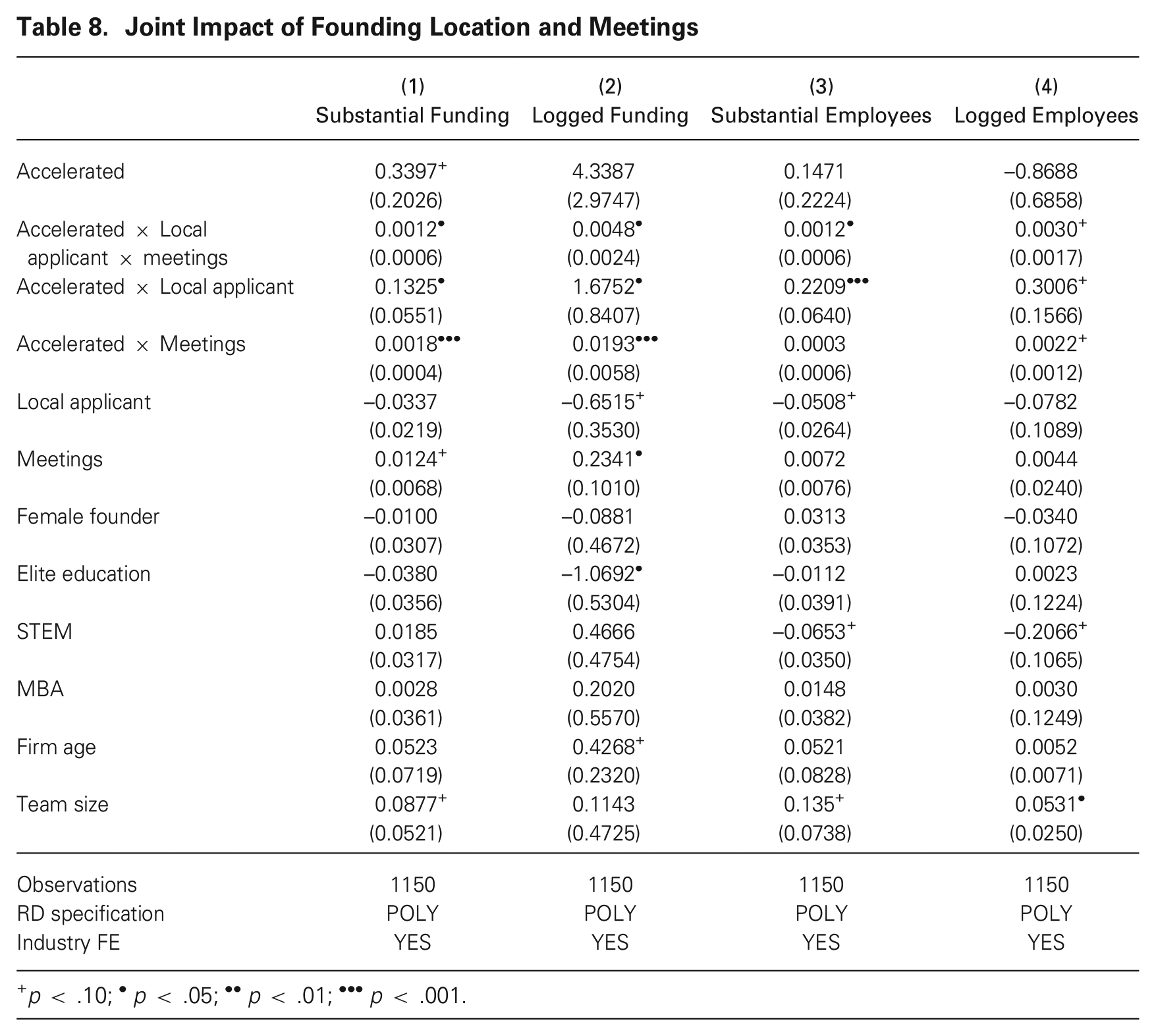

Table 8 shows that analysis repeated, but in this case it examines the joint interaction of a startup’s proximity to formal networking meetings and having been founded in the same ecosystem as that of MassChallenge. Here, I find positive interactions between being a local applicant and being in close proximity to formal network meetings in terms of gaining significant amounts of external financing and having higher levels of employment.

Joint Impact of Founding Location and Meetings

p < .10; •p < .05; ••p < .01; •••p < .001.

From the results in Tables 7 and 8, I found strong but not perfect support for H5. Notably, being local and having close proximity to startup investors has a surprising negative interaction term. This result suggests that proximity to investors in the same ecosystem as that of MassChallenge at founding is partially a substitute for the treatment of MassChallenge.

Discussion

Theories of organizational sponsorship have substantially advanced our understanding of how entrepreneurial support organizations, like accelerators, can substantially improve startups’ performance by directly improving their environment. These theories have not, however, considered the potential impact of a startup’s initial founding environment on the success of the sponsorship relationship. In part, this lack of attention derives from the fact that organizational sponsorship has largely been studied in resource-poor contexts, in which a startup’s access to resources in its founding environment is likely to be negligible relative to sponsors’ contributions (Amezcua et al., 2013; Dutt et al., 2016; Ratinho et al., 2020). In this article, I have developed a complementary theory suggesting that a substantial portion of organizational sponsorship’s effect, especially in active entrepreneurial ecosystems, can come from improving access to broader ecosystem resources. Because the acceleration process focuses on the direct brokerage of knowledge and information from stakeholders in the accelerator’s broader ecosystem, I anchored this theory in the observation that the total impact of acceleration should be stronger for startups with founding environments that increase the likelihood that knowledge exchange inside the accelerator will spill over to create increased engagement with the broader ecosystem.

I found evidence broadly supporting the theory that the acceleration process can spill over into a startup’s broader environment if the conditions are right. Specifically, I found support for the home bias of accelerators, as startups that were already embedded in Boston’s startup ecosystem derived greater benefit from the MassChallenge program than did other participants. Similarly, I found that proximity to key resources at founding provides important inputs to the effect of acceleration. In addition, home bias and resource proximity have a largely complementary effect: acceleration has the greatest impact when a startup is founded in the same ecosystem as the program’s and is geographically proximate to key resources. These results broadly support the notion that the impact of acceleration occurs not only through the resources provided but also through accelerating access to ecosystem resources.

My finding of a negative two-way interaction between local startups and proximity to investors in their founding ecosystem provides a counterargument that may be important for understanding accelerators’ role in their broader ecosystem. Prior research has shown that close social proximity to venture capitalists dramatically increases a firm’s likelihood of gaining external financing (Shane and Stuart, 2002). My result suggests that accelerators might in part substitute for the role venture capitalists play in their ecosystem. Ferrary and Granovetter (2009) documented that access to a venture capitalist serves as an express entry to becoming embedded in a broader entrepreneurial ecosystem, but venture capitalists do not provide this service for free. Investors with higher status and, thus, potential to foster better future relationships for a startup can leverage their capabilities for pecuniary gain by taking a larger percentage of a startup for any level of investment (Hsu, 2004). My results suggest that if a startup was more likely to have a prior relationship with an investor in the Boston ecosystem, access to more investors through the MassChallenge program did not increase the productivity of this relationship.

Overall, these results have immediate policy implications for individuals and governments interested in using accelerators as a tool for regional development. If startups admitted to an accelerator benefit the most when they are already proximate to resources, then the accelerator program complements prior ecosystem munificence and magnifies prior inequalities in founding environments. While my results are at the individual startup level, they provide a clear mechanism for observed inequality at the macro level. If accelerating startups works best for firms already embedded in high-quality ecosystems, it is not surprising that there is more accelerator entry and success in regions like Silicon Valley. All else being equal, accelerators provide further thrust to ongoing positive dynamics in a region and are less likely to engender strong effects in regions where pre-existing ecosystem dynamics do not exist.

This does not mean that accelerators are not a valuable policy tool in certain cases. MassChallenge, after all, was founded in Boston with a clear regional development objective, and it has successfully met that objective. While its effects are strongest for local Boston startups, it also has a positive impact on transplant firms that hail originally from rich ecosystems. This result accords with other research showing that innovators can leverage multiple ecosystems and that doing so can actually help enrich less-developed areas (Simons and Roberts, 2008; Wang, 2015). This finding suggests that accelerators launched in less-developed ecosystems might want to draw applicants not only with good ideas but also from active entrepreneurial ecosystems like Silicon Valley because doing so might facilitate future interconnections between ecosystems. Interestingly, the Chilean government pursued this strategy when it launched Startup Chile in 2010 (Gonzalez-Uribe and Leatherbee, 2018).

More broadly, the arrival of accelerators in regions lacking high levels of entrepreneurship does prompt an increase in ecosystem activity, but the regions that seem to benefit the most have resources that had not previously been successfully incorporated into the entrepreneurial ecosystem. Fehder and Hochberg (2021) noted that in Cincinnati, an accelerator was able to catalyze an ecosystem focused on entrepreneurship in consumer-packaged goods and branding because of its proximity to and relationships with Procter & Gamble. These relationships allowed startups to develop new and valuable ideas. Thus, while my results suggest that ecosystem acceleration is one major mechanism for an accelerator’s success, this does not preclude the possibility that other channels might foster regional growth.

Future Research Opportunities

While this study, by bringing an ecosystem perspective, advances our knowledge of how accelerators improve startup performance, it has limits that may spur future research. MassChallenge is one of many possible accelerator designs, and prior research has shown that differences in accelerator design are associated with differences in accelerator performance (Cohen et al., 2019). From the beginning, MassChallenge was committed to regional development as its primary goal. The ecosystem acceleration effects of a program could vary according to accelerator design and the commitments of its founders and early stakeholders. Connecting the primary motivations of accelerator founders (e.g., profit versus regional development) to the recruitment of mentors would be a profitable area of future research.

In addition, this study’s setting in a highly evolved startup ecosystem means that I do not know whether a minimum level of ecosystem development is required before these ecosystem acceleration effects take hold. With a plethora of investors and innovative corporations, Boston is the second highest U.S. region in venture capital allocation per capita and the third or fourth highest in absolute terms. It is not clear what level of entrepreneurial and innovative activity is required before an accelerator has enough applicants and mentors to maintain engagement on all sides in a way that creates potential for spillovers.

Compared with other accelerators, MassChallenge might also have an unusual connection to its local entrepreneurial ecosystem. MassChallenge was founded by two people with close connections to important ecosystem institutions in Boston, MIT and Harvard, which gave the program immediate legitimacy in the eyes of other ecosystem actors. Whether similar effects would emerge for an accelerator founded by a relative outsider is unclear. Existing research has shown a connection between founders’ background and the design and performance of accelerators (Cohen et al., 2019), but the mechanisms generating these findings are not well understood.

This study also focuses on MassChallenge’s effects on startups at one point in time. Future research could enrich our understanding of accelerators overall and their connection to ecosystems in particular by exploring change over time. Taking a historical approach, future studies could explore in more detail the founding histories of accelerators to understand how they themselves became embedded in their ecosystems. Similar studies have explored how a program’s founders tailor their offering to fit their local environment (Kim, 2021). It would also be revealing to understand how stakeholders are engaged and how potential conflicts between them are resolved. In addition, future studies should explore, from an ecosystem perspective, the antecedents of accelerator death because accelerators, like other organizations, can and do close.

To date, most accelerator research has focused on programs at the higher end of the performance distribution. These studies have assumed that within these programs, the cooperation of investors and corporate executives who might be competitors in other contexts is stable. Research on other innovative communities, like open-source software, reveals a rich set of tactics to maintain cooperation among diverse and potentially divisive populations (O’Mahony and Bechky, 2008). Learning how cooperation is maintained inside an accelerator program would advance our understanding of how organizations can be used to effectively coordinate innovative communities (O’Mahony and Lakhani, 2011).

Related, this study has helped improve our understanding of organizational sponsorship, but the possibilities for future studies suggested here would help to move research on entrepreneurial support organizations closer to core themes in organizational theory. The payoffs to this move might be substantial both theoretically and in terms of our ability to give practical advice on the design of entrepreneurial support organizations. Accelerators are just one of a growing number of novel organizational forms that have emerged over the past 10 to 15 years. The need for durable theory that explains the role not only of accelerators but also of hackathons, pitch competitions, coworking, and their joint effects is only growing as the importance of entrepreneurship in the economy increases.

It would also be valuable to explore whether the ecosystem spillovers from organizational sponsorship that I observed in accelerators might be one example of a more general organizational phenomenon. I would expect to observe these ecosystem spillovers in organizational contexts with certain characteristics: pursuit of an innovative outcome, dependence on external resource holders, and a limited-duration process that enriches an individual’s or organization’s environment through information exchange. One suitable context outside of entrepreneurship could be prominent regional academic conferences, at which researchers could explore the impact of participation on developing academic careers. Similarly, art festivals at which theater troupes or visual artists exhibit their work might be a context in which an ecosystem’s focused engagement for a limited duration yields different returns depending on the initial environment of the troupes or artists.

Supplemental Material

sj-pdf-1-asq-10.1177_00018392231204839 – Supplemental material for Coming from a Good Pond: The Influence of a New Venture’s Founding Ecosystem on Accelerator Performance

Supplemental material, sj-pdf-1-asq-10.1177_00018392231204839 for Coming from a Good Pond: The Influence of a New Venture’s Founding Ecosystem on Accelerator Performance by Daniel C. Fehder in Administrative Science Quarterly

Footnotes

Acknowledgements

I thank Fiona Murray, Scott Stern, Yael Hochberg, and Ezra Zuckerman for their guidance. I also thank John Harthorne and Cory Bolotsky at MassChallenge for the opportunity to work with them and access their data. Financial support from the Ewing Marion Kaufmann Foundation is gratefully acknowledged. The faults are mine alone. Questions and comments are welcome:

2

Theoretical constructs related to organizational sponsorship, such as entrepreneurial support, have emerged in the policy literature and have substantial parallels to organizational sponsorship in their definition (e.g., Hanlon and Saunders, 2007; Ratinho et al., 2020; Bergman and McMullen, 2022). Given their strong conceptual similarities, I refer to research in both traditions as examples of organizational sponsorship, for ease of theoretical development.

3

The literature on accelerators, while growing, is still relatively small. I use theoretical and empirical insights, when applicable, from studies of other entrepreneurial support organizations such as incubators.

4

While not all startups admitted to an accelerator are traditional technology or software firms, these types of firms do predominate in accelerators. Non-technology firms admitted to accelerators tend to use higher levels of technology to enter a market than their current competitors use (Fehder and Hochberg, 2021).

5

Another source of early-stage capital to growth-oriented startups is angel investors, who engage in the same activities as venture capitalists do but invest their own money. Because the effects of angel investors are similar to those of venture capitalists and venture capitalists represent a disproportionately large share of the investments in early-stage firms, I simplify my theoretical exposition by referring only to venture capitalists. For more information on angel investors and their relationship to venture capitalists, see Botelho, Fehder, and Hochberg (2021).

6

In the first years of MassChallenge, the total number of slots was 125. In 2012, they expanded the program to 128 slots, a number of symbolic importance referring to the legendary Route 128 that encloses the Boston/Cambridge entrepreneurial ecosystem.

Author’s Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.