Abstract

This article uses a study of the Swiss mechanical watch industry to build theory about how a legacy technology, instead of being supplanted by a new dominant design as current theory would predict, is able to reemerge and achieve new market growth. The introduction of the battery-powered quartz watch in the 1970s made mechanical watches largely obsolete, but by 2008 the Swiss mechanical watchmaking industry had rematerialized to become the world’s leading exporter (in monetary value) of watches. This study uncovers the process and mechanisms associated with technology reemergence: the resurgence of substantive and sustained demand for a legacy technology following the introduction of a new dominant design. It reveals that technology reemergence involves a cognitive process of redefining both the meanings and values associated with the legacy technology and the boundaries of the market for that technology. Watchmakers redefined and combined values of craftsmanship, luxury, and precision to create new meanings and values for mechanical watch technology; repositioned the mechanical watch as an identity and status marker; temporally distanced themselves from the period of the discontinuous quartz technology by recalling their founding and more successful past and connecting it to the future; and used conceptual bridges such as analogies and metaphors to help employees and consumers understand the new meanings. They redefined market boundaries by reclaiming the competitive set, rebuilding the community of mechanical watchmakers, and mobilizing groups of enthusiast consumers who valued the mechanical watch. For mechanical watchmakers, reemergence culminated in competitive and consumer differentiation that ushered in reinvestment in innovation and substantive and sustained demand growth for the legacy technology.

Keywords

Schumpeter (1934) argued that the forces of creative destruction overturn existing market structures and force the dismantling of old technologies, as well as their applications in products, processes, and practices. For decades, scholars have linked industry evolution to technology cycles in which a dominant technology is displaced by a new one that initiates a new regime (e.g., Tushman and Rosenkopf, 1992; Utterback and Suárez, 1993; Klepper, 1996). Prevailing theory emphasizes technological displacement, assuming that older technologies disappear when newer ones arrive: “The dying technology provides the compost, which allows its own seeds, its own variants, to grow and thrive” (Tushman and Anderson, 1997: 12).

Yet displacement is not inevitable. Market demand for some legacy technologies—products such as sailing ships, vinyl records, fountain pens, and streetcars—declined and then reemerged. This study examines the possibility that demand for some legacy technologies may not die away (Henderson, 1995; Adner and Snow, 2010) but persist in a generative form that permits sizeable market expansion. Existing scholarship, however, leaves little room for a legacy technology in a field or industry to reemerge. The aim of this paper is to induce the process of technology reemergence associated with such a possibility by considering how demand for a legacy technology—Swiss mechanical watches—rematerializes to achieve substantive and sustained market growth.

An in-depth study of this anomalous process can extend theory in important ways. First, as the pace of technology change and technology cycles continues to rise, organizations must manage the trajectories of their legacy technologies far more frequently. Building on prior research that has theorized that contracted demand niches can develop for legacy technologies after a field settles on a new dominant design (e.g., Porter, 1980; Adner and Snow, 2010; Furr and Snow, 2014), this paper examines how a legacy technology, and the organizations and community that support it, achieves substantive and sustained market growth following the introduction of a new dominant design. Second, this study can identify the processes and temporal sequence related to technology reemergence that have not been accounted for in theories related to technology cycles and industry evolution.

Technology Cycles and Legacy Technology Trajectories

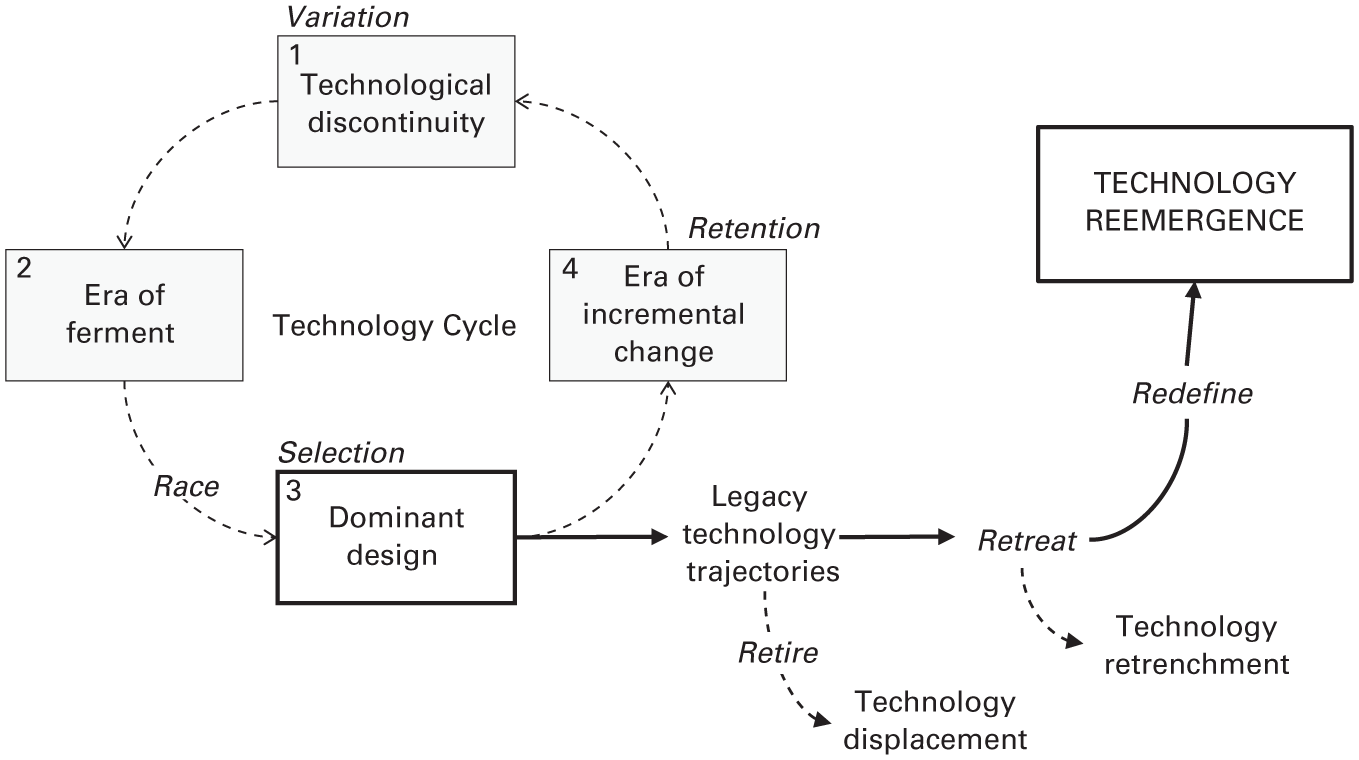

Technology cycles continuously reshape the trajectories of old and new technologies and the competitive landscape of incumbent firms (Schumpeter, 1934; Dosi, 1982; Tushman and Rosenkopf, 1992). Research on technology cycles has largely focused on the introduction of new technologies and how demand in a field initially fluctuates between variants during an era of ferment but then settles on a new dominant design (Suárez and Utterback, 1995; Murmann and Frenken, 2006). Marked by phases of variation, selection, and retention (Basalla, 1988), such cycles have been theorized as a “highly path-dependent process” (Kaplan and Tripsas, 2008: 790) in which legacy technologies are assumed to reach a natural limit and eventually fade away (Fleming, 2001).

For the legacy technology, technological discontinuities may initially generate capricious market demand as consumers’ preferences vacillate between the old and new technological variants (Abernathy and Utterback, 1978; Eggers, 2012). Prior to a new dominant design, incumbents often try to preserve market demand for the legacy technology by engaging in a technological race, extending the performance of the old technology to compete with new technological variants (e.g., Lerner, 1997). These races may also induce incumbents to incorporate features of a discontinuous variant into the legacy technology. For example, carburetor (Furr and Snow, 2014, 2015) and sailing ship (Rosenberg, 1976) producers experienced productivity gains by adopting intergenerational components from electronic fuel injectors and steam ships, respectively. Although these strategies may temporarily extend a technology’s life, such late-stage efficiency gains have been shown only to delay the eventual demise of the legacy technology (Tripsas, 1997). As a result, technology cycle research has focused primarily on the mechanisms that facilitate the rise of discontinuous technologies and the emergence of markets associated with them (e.g., Suárez, Grodal, and Gotsopoulos, 2015), deemphasizing the possible trajectories of the legacy technology after the introduction of a new dominant design.

Legacy Technology Trajectories

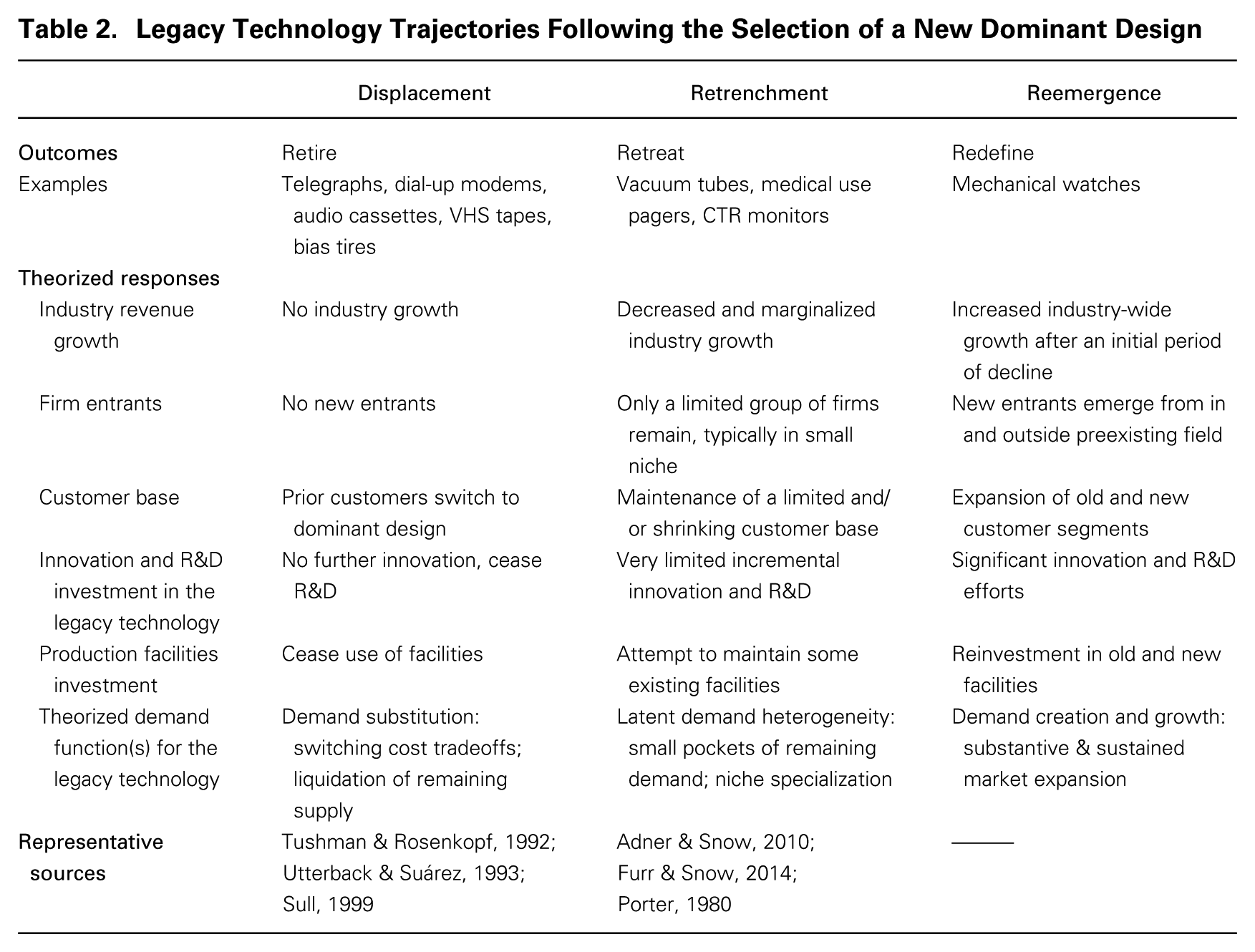

Scholars have generally devoted little attention to legacy technologies (Furr and Snow, 2014), possibly because of the dominance of the Schumpeterian paradigm and a pro-innovation bias in organizational theory (Rogers, 1995; Gopalakrishnan and Damanpour, 1997). A review of the extant literature indicates that legacy technologies are expected to follow one of two possible trajectories: technology displacement or technology retrenchment (Dosi, 1982; Anderson and Tushman, 1990; Adner and Snow, 2010).

Technology displacement (retire)

The literature on technology displacement (e.g., Cooper and Schendel, 1976; Tushman and Anderson, 1986) has assumed that once demand for an older technology is supplanted by a new dominant design, the field will reorient itself and incumbent firms will retire the legacy technology. The displaced technology is presumed to have little or no utility, leaving incumbents with few options but to wind down production, reallocate or disband investments in manufacturing facilities, and cease R&D devoted to that technology (Klepper, 1996). Technology displacement is most often associated with the fate of VHS tapes, audio cassettes, bias tires, and dial-up modems; in each case, the selection of a new dominant design (DVDs, compact discs, radial tires, and the Ethernet) shifted significant market demand away from the old technology (Cusumano, Mylonadis, and Rosenbloom, 1992; Sull, 1999). Technology displacement may occur rapidly or over a protracted period of time (Henderson, 1995), contingent on several factors. Existing consumers may face high switching costs (Hall and Khan, 2003) associated with maintaining preexisting social ties or institutional norms associated with the legacy technology (Fuentelsaz, Garrido, and Maicas, 2015). Or the residual benefits of the old technology may initially outweigh consumers’ perceived benefit of adopting the new dominant design and thus delay the firm’s need to retire the legacy technology (e.g., Ansari and Garud, 2009). Eventually, however, the prominent mechanism of technology displacement is demand substitution; the displaced legacy technology is theorized to be “swept away” as consumer demand shifts toward the new dominant technology (Utterback, 1996: xix).

Technology retrenchment (retreat)

Adner and Snow (2010) identified an alternative technology trajectory, technology retrenchment: the legacy technology moves into a contracted niche in its home market or relocates in a new market application. They advanced the notion of a technology “retreat” whereby a legacy technology exploits heterogeneity in its demand environment that permits a limited alternative use (p. 1655). Adner and Snow (2010: 1657) specified limits to market growth associated with technology retrenchment, however, arguing, “The goal and expectation of technology retreats is not for growth and expansion, but rather for survival and contraction.” Thus a core assumption of technology retrenchment is that the market for the old technology will decline, and only a small subset of firms will be able to survive by exploiting the remaining pockets of latent demand.

There has been limited empirical work on technology retrenchment, but illustrative examples include the prolonged use of paging devices in the medical community after others adopted mobile technology and the use of CTR monitors by a subset of video game enthusiasts after the introduction of flat screen technology (Adner and Snow, 2010). Alternatively, some technologies may find other uses that can sustain a contracted niche (Porter, 1980). For instance, after silicon transistors replaced vacuum tubes in radios (Cartwright, 2012), a small cohort of firms continued to produce vacuum tubes for use in guitar amplifiers for musicians who preferred their tonal quality over solid state alternatives. Notably, Adner and Snow (2010) highlighted mechanical watchmaking as an example of such latent demand heterogeneity, theorizing that because quartz watches were far superior to mechanical ones in their ability to keep time, a limited niche for mechanical watches emerged that decoupled elements associated with technological determinism (e.g., precision timekeeping) from other aspects (e.g., nostalgia). In their treatment, retrenchment explained a diminished market for the legacy technology. Although the Swiss watch industry experienced an initial phase of retrenchment and contracted demand for the mechanical watch as predicted by Adner and Snow (2010), it also experienced a subsequent unexpected process of significant demand growth not explained by prior theory on legacy technology trajectories. It may be better explained by another trajectory that extends from the notion of retrenchment to account for another unique possibility: technology reemergence.

Technology reemergence (redefine)

Technology reemergence is a path whereby market demand for a legacy technology first retrenches and contracts into a limited niche but later achieves substantive and sustained demand growth. Demand for Swiss mechanical watches dissipated and contracted into a market niche following the mass production of quartz watches, but beginning in the late 1980s, Swiss mechanical watchmakers unexpectedly experienced significant revenue expansion that exceeded even that of quartz manufacturing. After a period of mechanical R&D stagnation while they focused on quartz technology, new entrants and incumbents began to invest heavily in mechanical watchmaking. These efforts led to innovations that extended well beyond the field’s prior technical achievements and illustrate the possibility that an entire community—not just a remaining few firms—may choose to reinvest in technical innovation and manufacturing assets associated with a legacy technology.

Method

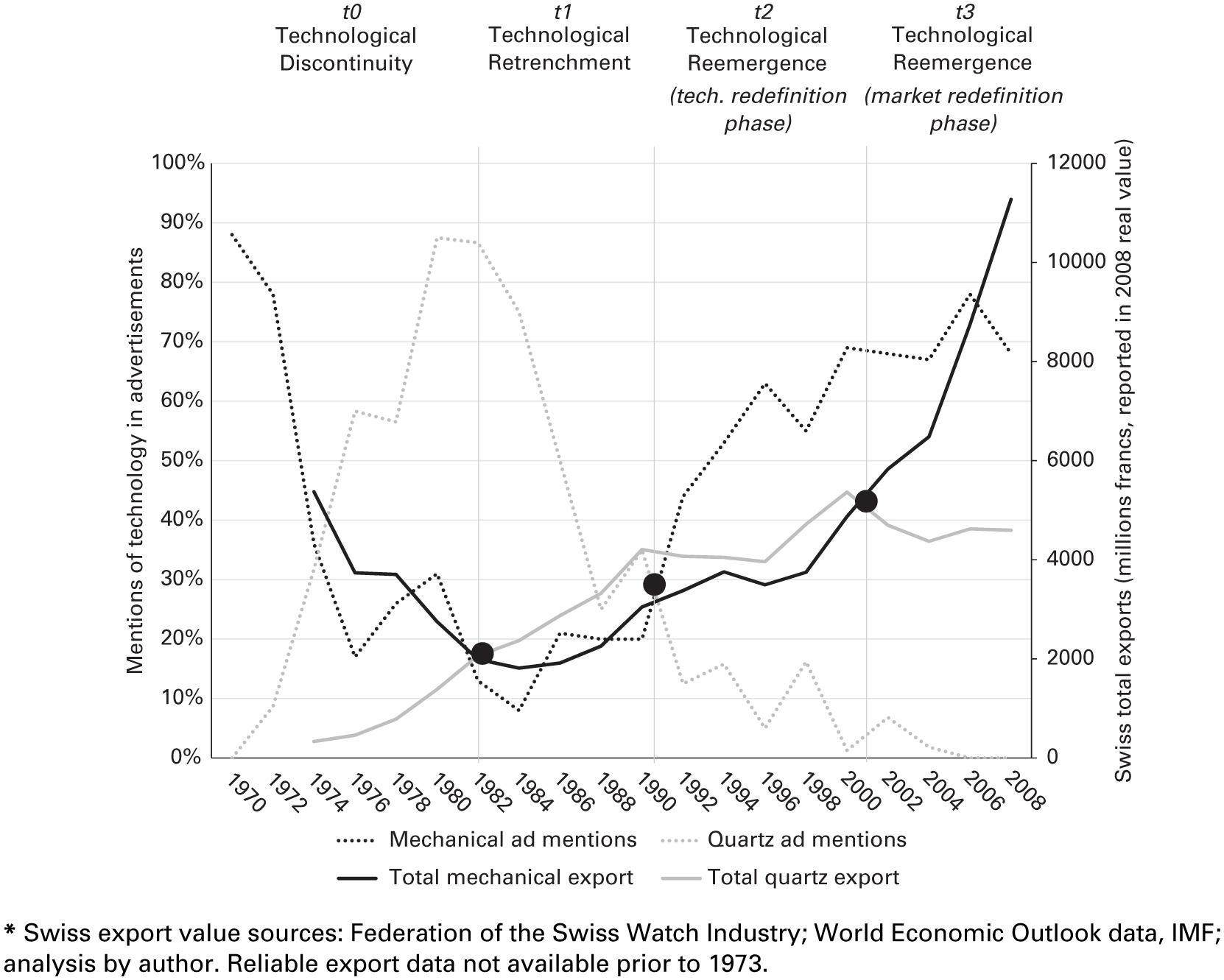

The research setting is the Swiss watch industry from 1970 to 2008. For over 200 years, beginning in the mid-eighteenth century, the Swiss dominated the mechanical watch industry (Donze, 2011); Swiss mechanical watches were universally considered a symbol of technological supremacy and innovation (Sobel, 1996). Their reign ended abruptly in the 1970s with the onset of the quartz revolution (or quartz crisis) and with the expectation that the battery-powered quartz movement would displace the mechanical watch. The Swiss dropped from holding over 50 percent of the world’s export market (in monetary value) to less than 30 percent a decade later. 1 By 1983, over half of watchmakers had gone bankrupt and two-thirds of all Swiss watch-industry jobs had disappeared (Perret, 2008). Industry experts predicted that mechanical watches and the communities of watchmakers who built them would disappear (Landes, 1983; Donze, 2011). Quite unexpectedly, however, demand for Swiss mechanical watches began to resurge. From 2000 to 2008, increased consumer demand for mechanical watches led to unprecedented market growth, a proliferation of mechanical watch innovations, and the emergence of schools, trade shows, competitions, and government policies that propagated the field of mechanical watch production. By 2008, the Swiss, led by mechanical watch production, resurfaced as the leading exporter of watches and reclaimed 55 percent of the global watch industry’s export value.

I chose 1970 as the starting point of this study because it marked the first full year after the initial quartz timepiece was introduced to the market, and it represented the height of Swiss mechanical watchmaking’s dominance of world markets. It allowed me to track more than a decade of performance data, events, and critical decisions that occurred immediately after the introduction of quartz technology as the field’s new dominant design. The study’s endpoint is 2008, the onset of a global financial downturn that watch industry experts argued led to changes in industry performance that extended beyond the scope of this research.

Data Sources

This study draws on data from multiple sources. I provide an overview of my sources here and list them in table A1 in the Online Appendix (http://journals.sagepub.com/doi/suppl/10.1177/0001839218778505).

Interviews and observation

I conducted 136 interviews with senior executives, watchmakers, distributors, retailers, industry analysts, collectors, government officials, company historians, auction house representatives, and museum curators associated with the watch industry. The average interview lasted 91 minutes. Twenty-nine percent (N = 39) of the individuals interviewed started their careers in the watch industry prior to 1990, 24 percent (N = 34) started between 1990 and 2000, and the remaining 47 percent (N = 63) joined the industry in 2000 or later. The sample included interviews with executives from watch companies that cumulatively accounted for roughly 85 percent of all watch sales in Switzerland between 1970 and 2008. I also led four focus groups with 42 watchmakers and collectors in Switzerland and the U.S. I attended Baselworld, the industry’s largest annual field-configuring event (Lampel and Meyer, 2008), to observe the interactions of over 100,000 participants, 1,800 exhibitors from 45 countries, and 3,300 journalists. Further observations included private tours of nine watch factories. Finally, to converse fluently with executives and watchmakers, I observed a watchmaking course taught by prominent horologists at the National Association of Watch and Clock Collectors’ School of Horology. 2

Advertisements

To better understand emerging trends in the field data, I developed a custom database of company advertisements from the three most prominent watch industry trade journals between 1970 and 2008. I searched horological archives located in Switzerland, the U.S., and France, compiled a set of all prior magazine issues, and scanned every ad in the first three issues of each even year between 1970 and 2008. This process led to an initial sample of 845 ads. I narrowed the sample to the 700 ads related to Swiss watch companies, which constituted my final sample. The main data source for the ads was the Journal Suisse D’Horlogerie (JSH), published in Switzerland. From its inception in 1876, JSH was the foremost authority on industry trends, events, and innovations in the watchmaking industry. Field interviews confirmed that the journal’s readership consisted of members of all facets of the watchmaking industry, including watchmakers, dealers, parts suppliers, consumers, and watch enthusiasts. I also used the journal to study industry announcements, trends, and innovations. The journal suspended publication in 2000. Because no single journal ran during the entire length of the study, I relied on two additional leading watch journals, Chronos and International Watch (iW), for the remaining years of analysis. Chronos was first published in 1993 and iW in 1989. I chose these journals after asking numerous industry experts, historians, and company CEOs about which journals played a similar role in the watch industry as JSH. To ensure the composition of ads in my sample remained consistent across all three journals, I began my analysis of Chronos and iW in 1996 so I could verify that no significant differences existed among the three journals during the four years their publication overlapped.

Archival documents and interviews

I collected data from several additional archival sources. These included the annual reports issued by the Federation of the Swiss Watch Industry, which provided information on sales and broad demographic trends for the entire watch industry. I also collected all historical employment data while visiting the Convention Patronale de l’Industrie Horlogère Suisse, the umbrella organization for employees of the Swiss watch industry. I reviewed press releases and Swiss parliamentary testimony from the Swiss Federal Institute of Intellectual Property, the federal agency in Switzerland responsible for the “Swissness Project,” an initiative that protected products from counterfeiting. Finally, I coded an additional 27 interviews with Swiss watch CEOs published throughout the 1990s and 2000s in TimeZone, a leading industry news source. I relied on these historical interviews to confirm that what I had learned in my field interviews was not subject to recollection bias.

Data Analysis

Data analysis evolved in three stages. First, I reconstructed the historical evolution of Swiss watchmaking to delineate substantive market demand shifts for mechanical watches between 1970 and 2008. From this analysis, I charted the chronology of Swiss mechanical watchmaking through several distinct periods: a technological discontinuity marked by a technology race with quartz technology; a period of retrenchment and contracted market growth; and a period of significant market growth and reemergence.

In the second stage of data analysis, I developed a process model associated with technology reemergence. This stage involved concurrent data gathering and analysis of interview data, archival documents, and ad data. I used NVivo 10 to initially code the interview transcripts and archival data for descriptive elements related to key events, individuals, organizations, and community activities associated with mechanical watchmaking. During this initial coding process, I induced and began to discern that the reemergence process was influenced by several mechanisms that appeared to sit at the intersection of cognition and technology change (cf. Kaplan and Tripsas, 2008). Accordingly, I began to develop codes associated with the cognitive meanings and values (e.g., Schultz and Hernes, 2013) that organizational and community-level actors had attached over time to mechanical watches and the mechanical watch market. Online Appendix B, including table B1, provides a more detailed description of how these themes evolved and resulted in a preliminary codebook that informed my analysis of the ad data.

To analyze the ads, I initially collaborated with a management professor and a trained research assistant to conduct pilot coding sessions (e.g., Hsu and Grodal, 2015). We coded 100 ads not included in the final sample to assess the validity of the codes and the reliability of my codebook. We independently assigned codes to approximately 30 ads at a time and then met to compare scores, resolve discrepancies, and reach consensus; we repeated this process twice until we achieved roughly 95-percent consistency, with the remaining 5 percent attributed to human error such as mistyping intended codes in the spreadsheet. I then coded the sample and had the research associate code 10 percent to verify continued consistency.

Next, I attempted to identify distinct time periods (Langley, 1999) between 1970 and 2008 that could be mapped to the shifts in the trajectory of the legacy mechanical watch technology. Using annual export data for both quartz and mechanical watches, I initially identified inflection-point years in which the total Swiss export values for quartz or mechanical watches crossed and eclipsed each other (e.g., 1982, 2002). As I became more interested in delineating cognitive shifts in the Swiss watch community’s primary espoused focus on quartz or mechanical watches, I coded each ad’s explicit mention of the watch as “mechanical” or “quartz” (or “no mention”). I used the ads coded as mechanical to conduct analyses related to the process and mechanisms of technology reemergence. I then identified even-year inflection points at which the majority of ads representing either technology shifted to the other (e.g., 1992). By overlaying the export data on the ad technology mentions, the distinct inflection cross-over points delineated four specific time periods in the trajectory of the mechanical watch: t0: discontinuity (1970–1980); t1: retrenchment (1982–1990); and two distinct phases of reemergence, t2: (1992–2000) and t3: (2002–2008); see figure 1. 3 Extensive field interviews provided additional qualitative support for these conceptual period distinctions. Finally, I conducted analyses of variance (ANOVAs) for every code in the ads, comparing differences across each period and for all possible permutations (e.g., t0 compared with t1; t0 compared with t2). 4 For models that reported significant results, I conducted Tukey’s honest significant difference (HSD) post hoc analyses to find posteriori differences among the sample means. As it was possible to assign more than one code to an ad, I conducted a similar analysis for all co-occurring codes that appeared in the ads during reemergence (t2 or t3) and compared these co-occurring codes with earlier periods (t0 or t1).

Trajectory of the Swiss mechanical watch.*

The results helped me triangulate the ad data with the other data sources and to identify the mechanisms associated with an emerging process model. For example, company historians, whose role I discovered in interviews was to capture their company’s traditions in watchmaking, noted the importance of bridging the past with the future. I then began to look for this theme in the ads. Doing so led me to induce the mechanism of temporal distancing, which I then coded for in the ads in a subsequent round of coding. A similar iterative process informed how I induced the other mechanisms.

In the third stage of data analysis, I returned to the field. In focus group sessions and additional interviews, I asked individuals to comment on my nascent theoretical models and provide additional context. I also conducted checks with these informants to validate whether my representation of the phenomenon aligned with their experience. I continued to combine descriptive codes to form thematic and eventually theoretical codes (Glaser and Strauss, 1999). The entire process was iterative—alternating among data sources, analysis, and extant theory, and returning to the field to collect more data to validate my findings—to induce a process model associated with technology reemergence.

The Process of Technology Reemergence

Phases of the Technology Life Cycle in the Swiss Watch Industry

Switzerland’s dominance in watch production arose in the eighteenth century, and by 1940 its exports represented 80 percent of the global industry’s total value and dominated industry sales until the introduction of quartz technology in the 1970s. I catalogued three distinct phases that followed, culminating in the reemergence of mechanical watch technology and renewal of the Swiss watch industry.

Technological discontinuity (1970–1980)

Ironically, a group of Swiss watch companies working together introduced the first prototype for a quartz battery–powered watch. Quartz technology included a circuit that allowed a precisely cut quartz crystal to turn vibrations into electric pulses that measured time. At first, quartz watches were extremely expensive to produce but were 20 times more accurate than their hand-wound mechanical counterparts. Most Swiss watchmakers doubted that quartz technology would replace their centuries-old mechanical traditions and chose to race against quartz variants by investing resources in improving the mechanical watch’s accuracy. Because of their early investments in electronics, however, Japanese firms such as Seiko and Casio entered and dominated the quartz market by reducing the price by a factor of 100. To compete with the Japanese, by 1974 Swiss mentions of quartz watches in ads surpassed their mentions of mechanical watches for the first time. But Japanese dominance had already taken hold. An executive I interviewed recalled of that time, “Everyone [in Switzerland] believed the future was in quartz.” Most of the remaining Swiss watchmaking firms began to retool their manufacturing lines to accommodate quartz watch production (Donze, 2011). Experts predicted quartz technology would completely displace mechanical watches within a decade (Landes, 1983).

Technological retrenchment (1982–1990)

By 1982, Swiss quartz watch sales surpassed Swiss mechanical watch sales for the first time. That year, executives at the Swiss Corporation for Microelectronics and Watchmaking Industries Ltd. (SMH) introduced the Swatch watch that combined quartz technology with artistic design (Taylor, 1993; Moon, 2004). Within five years 50 million Swatches were sold, showing that the Swiss watchmaking community could compete in the quartz market. The Swiss firms’ shift toward quartz technology, however, also ushered in a period of technology retrenchment for the mechanical watch. Latent demand benefited a subset of remaining mechanical watch firms that recognized a consumer niche that still valued these watches (Adner and Snow, 2010). An executive I interviewed said he successfully targeted a remaining customer niche by running ads that celebrated Swiss watchmaking traditions. Swiss executives were also surprised that watch collectors began to pay record prices for vintage mechanical watches at auction (Reardon, 2008), especially because most companies were liquidating their assets associated with “outdated” mechanical production.

Technological reemergence (1992–2008)

By 1990, the broader Swiss watchmaking community had taken note that a market for mechanical watches was viable, and many more firms turned their attention back to mechanical production (Donze, 2011). This community-wide shift toward mechanical watchmaking is evident in 1992, marking the first even year since the 1970s in which Swiss ads for mechanical watches appeared more frequently than quartz watch ads. Unlike in the preceding period of retrenchment, in which only a small subset of firms maintained a limited niche for mechanical sales, Swiss mechanical sales began to experience prolific growth, eventually surpassing quartz sales in 2002. By 2008, mechanical sales were no longer confined to a limited niche; hundreds of Swiss watch companies were selling mechanical watches, and numerous mechanical watchmaking schools reopened to accommodate renewed demand. In its 2008 annual report, the Swiss Watch Federation noted, “The watch industry is today, as it was yesterday, one of the brightest stars in the Swiss economic firmament.”

The process associated with the reemergence of the mechanical watch took place across several periods. After the introduction of quartz technology (t0: 1970–1980), there was a period of latent demand that exposed a contracted demand niche for mechanical watches (t1: 1982–1990). The subsequent process of technology reemergence evolved in two distinct phases. During an initial phase of reemergence (t2: 1992–2000), Swiss mechanical watchmaking firms first focused on redefining the legacy technology. During a second phase (t3: 2002–2008), when demand for mechanical watches superseded that for quartz, watchmakers shifted the reemergence process toward redefining the market for mechanical watches. Several intermediate outcomes followed. New firms began to enter the mechanical watchmaking field, creating additional competition and the need for mechanical watchmakers to further differentiate from each other. Having established new meanings and boundaries to distinguish mechanical watchmaking from the quartz dominant design, competitive and consumer differentiation contributed to an increase in innovation in the mechanical watchmaking community. Together, these processes facilitated significant sustained demand growth and a reemergence of the legacy mechanical watch.

First Phase of Reemergence: Redefining the Legacy Technology

From 1992 to 2000 (t2), Swiss firms focused on redefining several aspects of mechanical watch technology. This initial cognitive shift led to the emergence and interplay of three mechanisms—recombining values, promoting watches as identity markers, and watchmakers distancing themselves from the quartz market discontinuity and drawing on their founding and traditions—and to the adoption of communication practices such as the use of metaphors and analogies that created conceptual bridges for consumers. I explain these mechanisms and practices here, and table C1 in the Online Appendix offers additional supporting data.

Recombining values

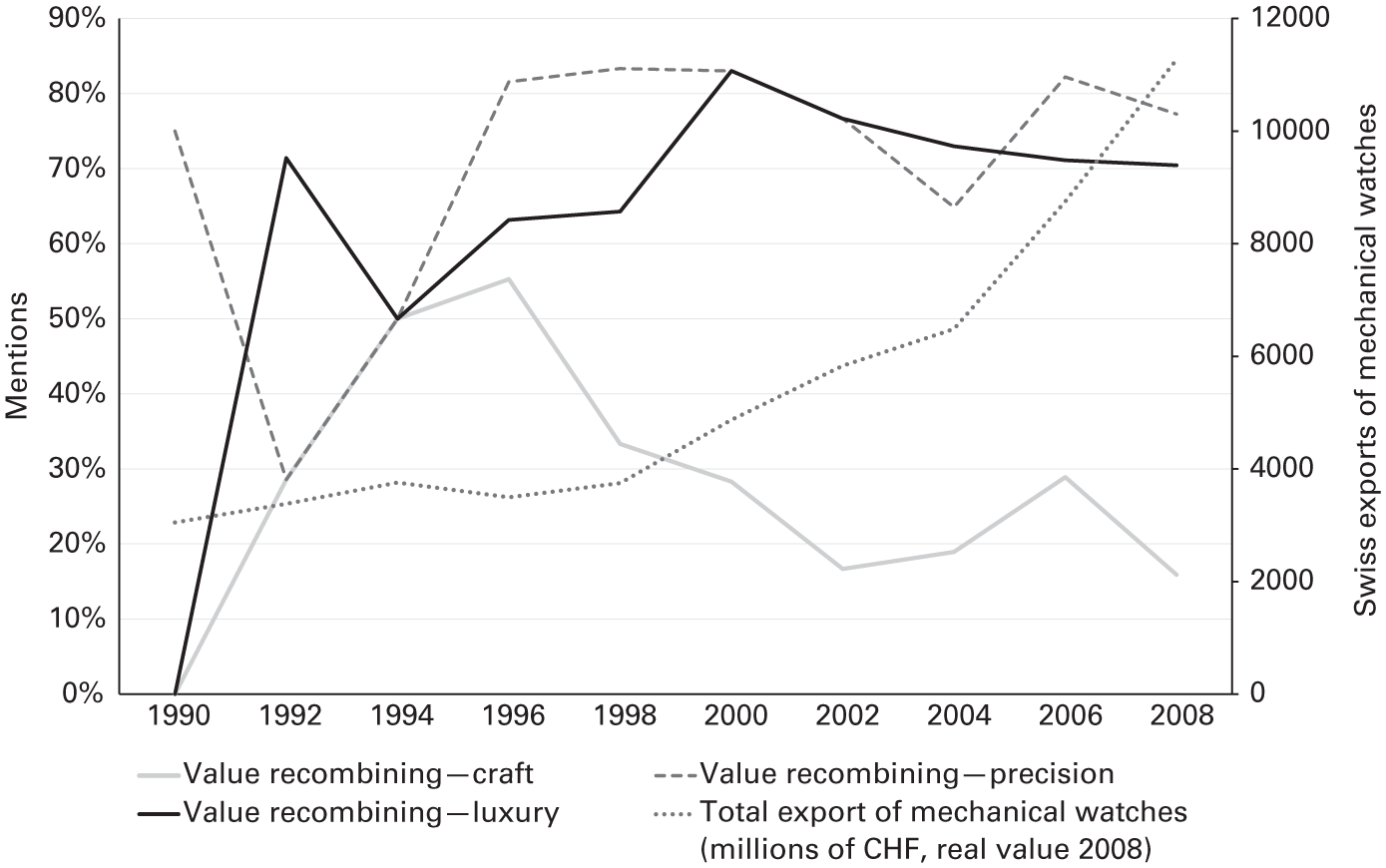

My informants attributed the early reemergence of the Swiss mechanical watch to a series of actions organizations took to cognitively redefine and combine the values of craft, luxury, and precision attached to the legacy mechanical technology. This process of recombining values—interpreting multiple “qualities that we have not seen together before in quite this combination” (Weick, 1990: 170)—permitted mechanical watchmakers to reactivate several latent value claims and conjoin them with novel values and new meaning. Figure 2 graphs mentions of recombining values over time.

Average mentions of value recombination—precision, luxury, and craft—in ads during technological reemergence (1990–2008).

First, during the early 1990s, watchmakers began to adopt and assert novel value claims related to craftsmanship, explicitly touting the handmade process that went into producing mechanical watches. One CEO stated, “When we tell customers about our company, we start with innovation, independence, continuity, and craftsmanship. Craftsmanship is now assumed to be a must.” Another senior executive explained how an emphasis on craftsmanship evoked new value for mechanical technology:

Despite the fact you need machines for most modern technology, it is all men and women behind the machines. They’re the machine. They’re giving their best, for their little piece to be as perfect as possible. At the end, all the pieces come together so the watchmaker can assemble them. You see people dedicated to their work, dedicated—some even scoff at the machinery.

Craftsmanship distinguished mechanical watchmaking from the mass manufacturing processes associated with quartz technology production. Mechanical watchmakers capitalized on this novel distinction; claims of craftsmanship aimed to shift the notion of the mechanical watch away from being merely a commodity good and toward “art.”

Second, firms preserved preexisting value claims related to precision—one executive noted, “During the comeback, we continued to emphasize precision, accuracy, and function”—but most mechanical watchmakers stopped using precision claims to compete directly with quartz timepieces. According to one industry spokesperson, “Precision is not sufficient. You have to give the customer more.” Thus watchmakers began to incorporate notions of luxury and status during this initial reemergence phase (t2) to reshape the values attached to the mechanical watch. An executive noted, “We now think of the [mechanical] watch as a status symbol. These are the intrinsic emotional values we have been trying to transmit related to the luxury lifestyle.”

Through the mechanism of recombining values, firms redefined value to include aspects of both luxury and craftsmanship. Precision appeared to take on a new meaning, serving as a proxy for the level of mastery required to produce a mechanical watch and, as with pieces of fine art and luxury handmade goods, began to justify higher prices. Combining these novel and latent value claims began to distinguish the mechanical watch from its quartz rival. A watch historian discussed how the recombination of values helped to redefine mechanical watchmaking (Trueb, 2005: 11):

[Mechanical watches] became something rare and very special: high-tech machinery, almost artistic skills and tremendous experience were required to make, assemble and service them. Damn the wonderfully accurate but mass-produced timepieces: intricate micromechanics are something exclusive and deeply emotional, and only limited quantities of such timepieces can be produced.

Patterns in the ad data validate how these reported shifts in value claims evolved over time. A majority of mechanical watch ads focused primarily on precision timekeeping during the retrenchment period (t1 = 85 percent), but during reemergence (t2), the combination of precision and craft with luxury became prevalent. Rolex released an ad in the 2000s stating, “Carved from the world’s most precious metal. ‘Made’ hardly seems appropriate. The Oyster Perpetual Day-Date in platinum. Nearly a year in the making, its 220 individual components demand such a process.” The ad touts the precision handmade manufacturing process and also highlights the use of platinum, often found in luxury jewelry. Mechanical watchmaking began to be seen as a form of high-end functional art, as illustrated in the following ad:

The beating heart of Piaget is its luxury watchmaking workshops. Crafted to very high technical specifications, a movement manufactured by Piaget is a thing of beauty, fascination and pride. World-famous as the specialist of extra-thin movements, Piaget harnesses its exclusive expertise to do justice to its signature creativity.

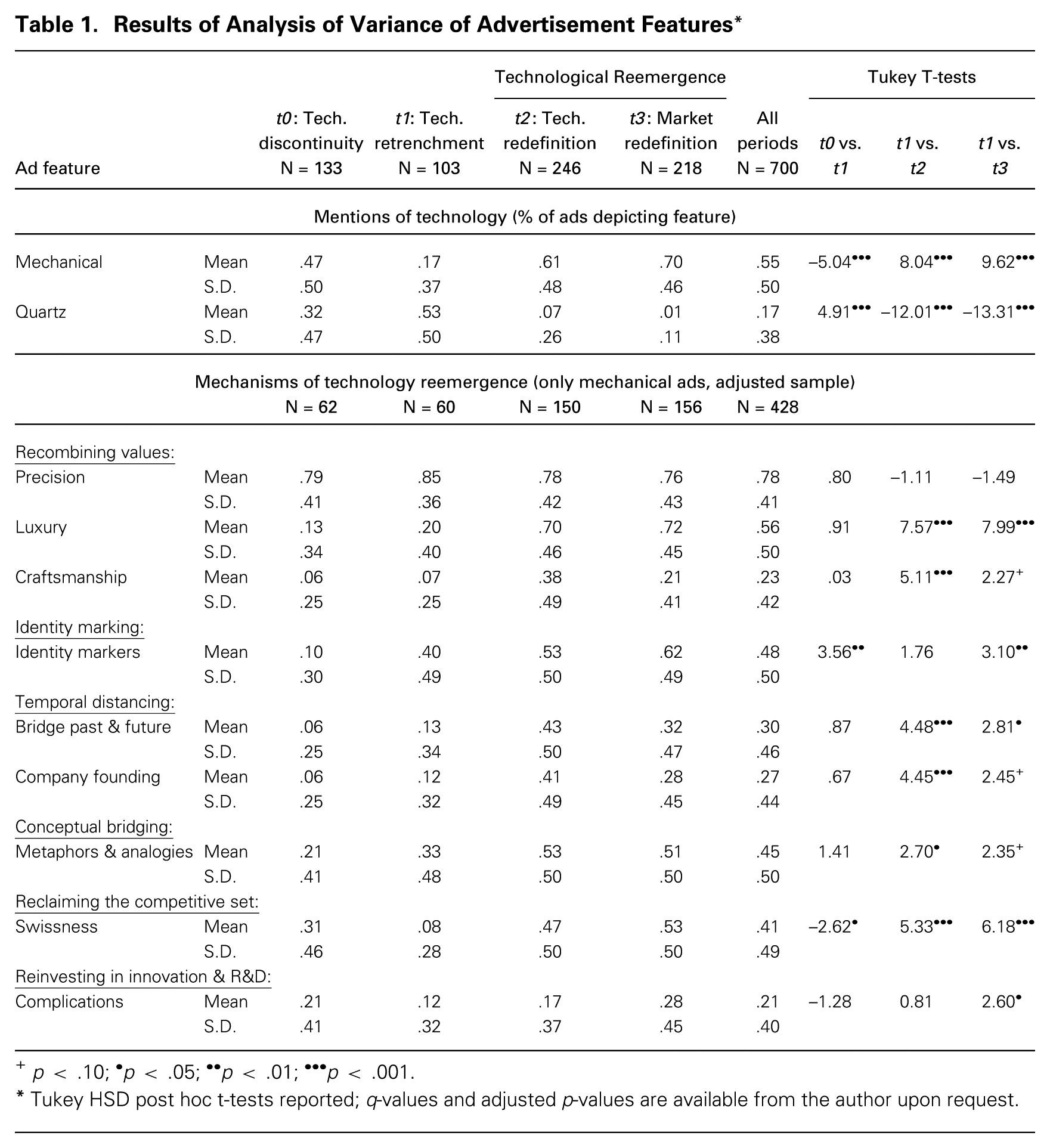

Results of analysis of variance tests, presented in table 1, showed significant differences in the value claims that Swiss firms assigned to the mechanical watch during reemergence (t2) compared with earlier periods. Compared with retrenchment (t1), significant increases occurred in mentions of craftsmanship [q(4, 410) = 7.22, p < .001] and luxury [q(4, 410) = 10.71, p < .001]. 5 Whereas 7 percent of ads were coded as craftsmanship and 20 percent as luxury during retrenchment (t1), 38 percent were coded as craftsmanship and 70 percent as luxury during reemergence (t2). Interviews indicated no significant shifts in precision at any point during the study’s timeframe, suggesting that watchmakers never relinquished their focus on producing precision timepieces but rather combined the notion of precision with other values. Several executives mentioned that precision and craftsmanship eventually became synonymous, which likely explains why references to craft eventually tapered off; co-occurrences of precision and craft rose from an average of 3 percent during retrenchment (t1) to 32 percent during reemergence (t2) and then leveled off to 20 percent (t3). Finally, tests confirmed increases in all combinations of co-occurrences among the three value claims during reemergence (t2) compared with retrenchment (t1); see table C2 in the Online Appendix. Additional tests between the two periods showed a significant increase in the co-occurrence of all three value claims appearing in ads simultaneously [q(4, 410) = 5.98, p < .001].

Results of Analysis of Variance of Advertisement Features*

p < .10; •p < .05; ••p < .01; •••p < .001.

Tukey HSD post hoc t-tests reported; q-values and adjusted p-values are available from the author upon request.

Swiss watchmakers’ ability to reactivate the latent values of precision and luxury reinforced the salience of latent demand heterogeneity as a demand function for a legacy technology. During reemergence, however, recombining values led to a distinct set of outcomes whereby latent and novel values formed new meanings and values attached to the mechanical watch. The ability to not only reactivate prior values but also generate new meanings and values associated with a legacy technology appears to be a distinguishable characteristic of technology reemergence.

Identity marking

Shifts in meaning attached to the legacy technology also stemmed from firms’ attempts to redefine the mechanical watch as a self-expressive “identity marker” (e.g., Pratt and Rafaeli, 1997; Mittal, 2006) for the consumer. Marketing research has associated identity marking with a product’s ability to “provide a vehicle by which a person can proclaim a particular self-image” (Aaker and Joachimsthaler, 2000: 49). Identity marking emerged as an important mechanism to help consumers personally identify with the mechanical watch. In the wake of quartz technology, many Swiss watchmakers noted that they reframed the mechanical watch as an expressive tool to showcase aspects of the consumer’s interests or personality. One executive stated, “When you buy a Swiss [mechanical] watch it’s no longer for just having the time on your wrist. It’s first of all to have an accessory that corresponds with your personality and the things you like.” A CEO described how he communicated this shift to consumers and his employees: “Your watch lives with you. You don’t look to it for accuracy. You look for the soul, the beauty, the art. You look to the watch as a communicating instrument of your personality. Your watch is part of you. The watch belongs to you. The watch is you.”

Using the ad data, I coded for explicit mentions and visual representations of the watch as a self-expressive identity marker (see Online Appendix table B1 for examples). One such ad stated, “Discreet individualism is the mark of people who wear Girard-Perregaux watches—and of those who make them.” Analysis of variance tests confirmed that identity marking more than quadrupled during reemergence (t2 = 53 percent) compared with displacement (t0 = 10 percent) [q(4, 410) = 9.19, p < .001]. During reemergence (t2), identity marking also co-occurred more frequently with luxury value claims than it did during retrenchment (t1) [q(4, 410) = 7.27, p < .001]. An industry veteran I interviewed noted that most firms began to combine these two elements: “Your mechanical Rolex or your Patek is a portable status symbol. It shows your status, your bank account, your power.” During reemergence (t2), identity marker and luxury co-occurrences increased fivefold (t2 = 43 percent) compared with retrenchment (t1 = 8 percent). Such co-occurring patterns illustrated how identity marking and recombining values worked in tandem to shift the meanings attached to the legacy mechanical watch. Identity marking initially became salient during retrenchment (t1 = 40 percent, compared with t0 = 11 percent) [q(4, 410) = 5.03, p < .002], but it took a different form, showing the watch as an extension of individuals as they engaged in recreational activities (e.g., sports, music, painting); these claims paralleled how Swiss quartz watches (e.g., the Swatch) were being positioned during retrenchment as accessories to compliment daily life. Notably, co-occurrences of identity marking and luxury were sparse during retrenchment (t1 = 8 percent).

Temporal distancing

During reemergence (t2), mechanical watch firms began to distance themselves from the period of technological discontinuity (t0). This mechanism, which I label temporal distancing, enabled watchmakers to “selectively forget” (e.g., Anteby and Molnár, 2012) elements of the legacy technology’s recent turbulent past and reclaim earlier, more successful periods. As one company historian explained, “We take care to distance ourselves from the [quartz] crisis. We prefer to go back to the founding of our business when we mention mechanical watches.” Another noted, “In producing mechanical watches, companies cast themselves in the role of guarantors of a centuries-old regional tradition” (Pasquier, 2008: 314). When asked to share the history of their company, no senior executive explicitly mentioned the quartz crisis unless provoked. My field notes indicated that responses typically focused on the company’s early or most recent mechanical watchmaking achievements, how they had reinvested in R&D, or how they continued to advance a centuries-old tradition of watchmaking.

Analysis of interview transcripts revealed that temporal distancing emerged in two forms. First, mechanical watch firms began to use language that bridged the distant past with the future, i.e., explicitly overlooking recent history associated with the period of discontinuity (t0) and retrenchment (t1). When asked about the role of temporal distancing, an executive explained:

During the crisis, the consumer didn’t give a [expletive] about the history of the company. The consumer began taking watches totally for granted. . . . It didn’t matter how long the company had been around. A watch became a disposable item . . . replaceable when it went bad. All these issues became irrelevant. In an attempt to market their brands, watch companies decided to emphasize only some parts of their history. Many companies have rewritten their histories.

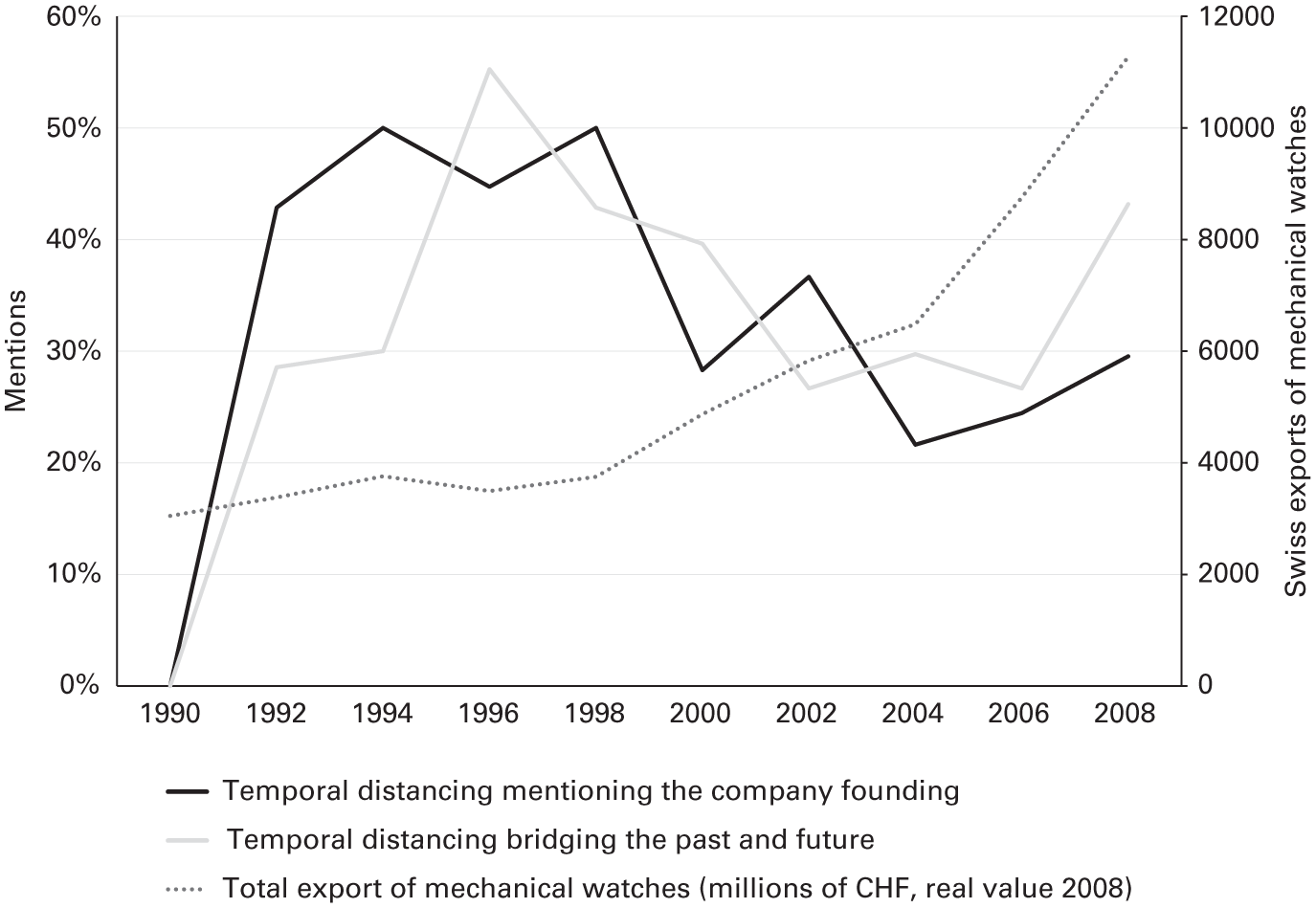

To understand how firms attempted to reframe their histories, I coded ads for statements that bridged references from the distant past with the future. One such ad showed a classic mechanical watch and stated, “The past inspiring the future.” During the quartz crisis (t0, t1), ads coded as bridging the distant past and future fluctuated (e.g., 11 percent in 1972, 8 percent in 1982, and 29 percent in 1988). Executives noted that in the 1980s customer preferences began to shift to all things “electronic” or “futuristic.” Firms recommitted to using references that bridged the distant past and future more often during reemergence (t2) than during retrenchment (t1) [q(4, 410) = 6.34, p < .001], as figure 3 shows. Temporal distancing codes that bridged the distant past and future reached 55 percent in 1996.

Average mentions of temporal distancing in ads during technological reemergence (1990–2008).

Second, I found that temporal distancing also consisted of firms reclaiming historical roots related to their initial founding date. Executives noted that they began to tout their founding date to communicate the origins of the firm’s mechanical watchmaking lineage. To codify this distant past, many firms began to hire Ph.D.s in history to write books on the company’s origin story. A new formal role, “brand historian,” was institutionalized in the industry in the 1990s. Such actions aimed to reinforce and authenticate the practices and traditions tied to early mechanical watchmaking. A brand historian I interviewed stated, “Companies go great distances to tell about their historical background and historical achievements. This is a kind of capital behind the product. It’s no longer just a very accurate product. When you buy a mechanical watch you buy something much more [too]; you buy history, you buy knowledge.”

Analysis of variance tests confirmed significant increases in the use of company founding dates in ads during reemergence (t2) as compared with retrenchment (t1) [q(4, 410) = 6.29, p < .001]. Ads appeared that made claims such as, “More than 250 years of uninterrupted history dedicated to perfection” and “Breguet. Since 1775. Known to history as the watchmaker’s watchmaker.” By comparison, from 1974 to 1980, not a single ad in the sample mentioned company founding, suggesting that companies had little interest in making claims to historical heritage as quartz technology was on the rise. Founding claims averaged only 10 percent before 1992, but during the first reemergence period (t2), such mentions averaged 41 percent and remained relevant during the second reemergence period (t3 = 28 percent). Founding date also appeared to reaffirm the firm’s historical role in shaping the “craft” of Swiss watchmaking. During the reemergence period (t2), 23 percent of ads included both founding date and craftsmanship, compared with only one such ad during retrenchment (t1) and discontinuity (t0) combined. In an archival interview, one CEO noted how his firm combined the notions of founding date and craftsmanship to redefine mechanical watchmaking:

Ulysse Nardin is one of very few watch companies which has been continuously in production. [It] was first owned and managed by five generations of Nardins before I took over in 1983. One should of course differentiate between a manufacture (or in English, a manufacturing company) and a marketing company. The longevity and history only have a meaning if it refers to a watch company which conducts its own research and development and manufactures watches. (Paige, 1999)

Through the mechanisms of recombining values, identity claiming, and temporal distancing, watchmakers redefined and shifted the meanings associated with mechanical watchmaking during the reemergence period. Swiss watchmaking became a form of “mechanical art,” infused with craftsmanship, luxury, and history. My analysis of the ad data further confirmed a notable co-evolution of these three mechanisms during the reemergence period (t2). The co-occurrence of every combination of these codes (precision, craftsmanship, luxury, identity marking, bridging the distant past and future, and company founding) increased during the first phase of reemergence (t2) relative to the period of retrenchment (t1).

Conceptual bridging

As watchmakers attempted to shift the values and meanings attached to mechanical watch technology, they adopted communication practices to help consumers and employees reconceptualize and interpret these meanings and values. Processes of “conceptual evolution” have been found to help consumers make sense of new discontinuous technologies, such as early automobiles (Clark, 1985) and electric lighting (Hargadon and Douglas, 2001). Watchmakers engaged in a similar process of conceptual bridging: the use of linguistic mechanisms to help actors develop “common ground in a step-by-step manner” (Cornelissen and Werner, 2014: 217) with a new technology. Firms used metaphors and analogies (Cameron, 1986; Bingham and Kahl, 2013) to communicate the new definitions and values attached to the legacy watch technology. As one executive said, “We don’t sell watches. We sell dreams.” Executives noted that they relied on such language to disassociate the mechanical watch from negative perceptions regarding accuracy and inferior technology formed during the quartz crisis. My interviewees frequently used metaphors and analogies to compare the mechanical watch with forms of art, culture, highly technical mechanical objects (e.g., cars, airplanes), and the human body. Several people likened the oscillating balance wheel of the mechanical watch to a “beating heart,” describing the watch’s gears as part of a “living organism” that needed to be “fed” with daily winding. A CEO stated, “A mechanical watch has a soul, it has a heart, it has life, it has something breathing inside of it.” Such descriptions evoked new meanings that consumers could assign to the legacy technology itself.

My analysis of the ad data showed a steady increase in the use of such conceptual bridging during the reemergence phase (t2) compared with retrenchment (t1) [q(4, 410) = 3.82, p < .036]. Tables B1 and C1 in the Online Appendix feature supplementary data demonstrating this trend. Such references grew from 14 percent of ads in 1992 to 58 percent in 2000, as shown in figure 4. Further analyses of the ad data revealed that conceptual bridging and aspects of recombining values began to appear more frequently together, as well as co-occurring with both aspects of temporal distancing: bridging the distant past and the future and highlighting a firm’s founding date. Analysis of variance tests showed a significant increase in the co-occurrence of the conceptual bridging code alongside codes for luxury [q(4, 410) = 7.65, p < .001], craftsmanship [q(4, 410) = 5.76, p < .001], and temporal distancing (i.e., bridging the distant past and the future) [q(4, 410) = 5.08, p < .002] between the periods of retrenchment (t1) and reemergence (t2). In addition, co-occurrences of conceptual bridging and identity marking appeared in 35 percent of all ads during the reemergence period (t2); one such ad stated, “Just like Achilles. But without the heel. We all have our weaknesses. Except for this watch, of course.” Thus conceptual bridging appeared to help watchmakers bring together a set of reconceptualized values and meanings attached to a revised definition of the legacy technology.

Average use of conceptual bridging—metaphors and similes— in ads during technological reemergence (1990–2008).

Related community and consumer factors

My analysis of interview and archival data also pointed to several community- and consumer-related factors that influenced the organizational mechanisms induced above. First, mechanical watchmakers benefited from and capitalized on market shifts that coincided with the mechanical watch’s initial reemergence. Between 1992 and 1998, discretionary household incomes rose for the top four countries that Swiss companies consistently exported watches to: by 26 percent in the U.S. between 1992 and 1998, and by 7 percent on average in Japan, Italy, and Germany between 1994 and 1998. Watchmakers also benefited from increased global demand for luxury goods. During the 1990s, luxury consumption increased four times faster than other forms of household spending (Frank, 1999). Comparing the 1990s to early-twentieth-century conspicuous consumption, Frank (1999: 15) noted, “We are in the midst of another luxury fever. . . . The quest to move up is currently in swing.” My analysis showed that growth consumption patterns for luxury goods were strongly correlated with the growth of mechanical Swiss watch exports from 1994 to 2008 (r = .95, p < .001).

Mechanical watchmaking was also influenced by, and likely contributed to, cultural shifts (cf. Giorgi, Lockwood, and Glynn, 2015) related to craftsmanship. The late twentieth century marked a change in how consumers defined product quality, initiating a rise in demand for handmade goods (Luckman, 2015) such that “More and more factories around the world are basing their work on this new paradigm that enhances craftsmanship. As the entrepreneur Bonotto (2011) says: ‘Time is the new luxury’; more attention to detail is given to adding quality and value to the product” (Cimatti and Campana, 2015: 13–14). New markets for high-end artisanal products began to emerge (e.g., Khaire and Wadhwani, 2010) in response to globalization and industrialization (Jones, 1989). Swiss watchmakers adopted and influenced many of the cultural trends related to slow manufacturing and craft (e.g., van Bommel and Spicer, 2011) in an attempt to reinforce their renewed definition of mechanical watchmaking.

Second Phase of Reemergence: Redefining the Market

Starting in 2002, Swiss mechanical watch exports eclipsed quartz exports, prompting a notable shift in focus in the watchmaking community that led to a reconstruction of market boundaries and significant reinvestments in mechanical watch technology. In the second phase of the reemergence process from 2002 to 2008 (t3), firms began to focus their efforts on reconstructing the community and consumer boundaries associated with the market for mechanical watchmaking. This redefinition process occurred via concurrent processes associated with two mechanisms: reclaiming the competitive set and mobilizing enthusiast consumers.

Reclaiming the competitive set

As market demand for mechanical watches surged, the Swiss watchmaking community began to reinterpret and reclaim the cognitive boundaries of its competitive set, i.e., “the causal beliefs that permit managers to define competitive boundaries and make sense of interactions within these boundaries” (Porac, Thomas, and Baden Fuller, 1989: 412). During the quartz crisis (t0), Swiss mechanical watchmakers defined Japanese quartz watchmakers as direct competitors and struggled to make sense of their new competitive landscape. A CEO noted, “I desperately tried to diversify [into quartz]. But it was difficult because there were now other channels that sold these products.” Reemergence (t3) marked a shift in focus that led the Swiss to reclaim membership boundaries to exclude firms that produced only quartz watches. During the 2000s, mechanical watchmakers reinforced these boundaries at the industry’s annual conference in Basel, Switzerland. Swiss industry insiders on the conference organizing committee awarded the most-coveted booth locations to firms that demonstrated a commitment to mechanical watchmaking; floor maps made these distinctions clear. An executive at a quartz manufacturer complained that his company had been denied a booth in the “main hall” and had been assigned a space in a temporary tent outside:

We are now seen as outside the family of watchmakers. All the [mechanical] companies are associated with the same watch manufacturer associations. They visit each other’s booths, but they don’t visit ours. There is an exchange of knowledge and information. We only receive guests from [other quartz watch companies], and same goes for them.

In an attempt to capitalize on increasing demand for mechanical watches, some quartz manufacturers reintroduced mechanical watches into their product portfolios in the 2000s. One executive explained how difficult it was to reclaim membership in the mechanical watchmaking community, noting, “Once the image is set about a brand as ‘digital plastic,’ it’s quite difficult to reset the mind and convince others in the industry that we offer more.”

Further, reclaiming the competitive set established new boundaries inside the mechanical watchmaking community. Many executives I interviewed discussed a hierarchy that emerged, often noting (unsolicited) where they were located on an informal “industry pyramid” that sorted each brand by its ability to produce quality mechanical watches, and thus by price. Such distinctions created subcommunities within the mechanical watchmaking community. Companies that produced more mechanical components in-house were higher on the pyramid and more prestigious than those that sourced their components from others in Switzerland. An industry historian explained this distinction:

After the quartz industry crisis, few watchmakers had maintained the [machinery] needed to produce all the steps of making a [mechanical] watch. Many watchmakers had to rely on others [to make watch components]. Starting in the early 2000s, brands that produced their own components began to call themselves a “manufacture” in an attempt to distinguish themselves from others in the industry.

Reclaiming the competitive set extended beyond established firms; of the new-entrant Swiss watchmaking firms whose CEOs I interviewed, all claimed their company’s primary founding objective had been to compete primarily in the mechanical watch market.

A second dimension of reclaiming the competitive set consisted of reestablishing Swiss geographic boundaries, i.e., the community of organizations “influenced by embeddedness in similar geographic environments” (Marquis and Battilana, 2009: 285). One executive stated, “The integrity, the diligence, the value system. That is what makes ‘Swiss’ Swiss. Swiss markers indicate the whole Swiss way of doing things. It plays a large role in the business and the industry.” Several community-level intermediary actors helped reconceptualize and reinforce these membership boundaries. To defend against counterfeiting, the Swiss government implemented “Swissness” legislation that protected local products and communicated Swiss values of quality, exclusiveness, and reliability. A government official noted that his office had commissioned studies from local experts on the impact of foreign counterfeiting. Swiss watch academies started to limit the number of non-Swiss applicants enrolled in their programs and, as a result, who could apply for jobs. A non-Swiss watchmaker said, “By the 2000s, [Swiss] schools were training mostly their own people again. It was much more difficult for a foreigner to get accepted and then get a job in Switzerland.”

Reclaiming the competitive set also applied to the messages that mechanical watchmakers sent to consumers. I analyzed each ad for claims of “Swissness”—references to the watch being Swiss—either in the text or by prominently displaying “Swiss Made” in the ad photo or graphic. One such ad showed a mechanical watch sitting where cheese is placed on a mousetrap, with the tagline “100% Swiss. The world’s finest collection of Swiss watches.” Significant increases in references to Swissness occurred between the retrenchment and both reemergence periods [q(4, 410) = 7.54, p < .001], as figure 5 shows. During retrenchment (t1), when the future of the Swiss mechanical watch industry was still uncertain, Swiss watchmakers appeared to have distanced themselves from making such claims (t1 = 8 percent). During the first phase of reemergence, claims of Swissness began to increase (t2 = 46 percent). In interviews, several executives mentioned that during this phase mechanical watchmakers attempted to capitalize on the popularity of the Swiss-made Swatch quartz watch. An industry reporter recalled, “Swatch was a phenomenon that put the Swiss watch back on the map. I saw its impact in Switzerland. It was absolutely amazing.” After the Swatch craze began to subside, however, the use of Swissness took on new meaning; a common theme in interviews pointed to watchmakers’ invoking claims of Swissness (t3 = 53 percent) to establish new and distinct community boundaries that separated the field of Swiss mechanical watchmaking from quartz technology. This cognitive shift appears to have contributed to an additional significant increase in claims of Swissness between the two phases of reemergence [q(4, 410) = 1.56, p < .001].

Reclaiming the competitive set: Mentions of “Swissness” in ads (1990–2008).

Mobilizing enthusiast consumers

A concurrent set of processes led Swiss mechanical watchmakers to redefine the cognitive boundaries associated with their consumer base during this phase (t3). Some activities focused on existing customers, others were targeted at attracting new customers, and still others appealed to both old and new customers. First, firms began to reconceptualize and mobilize consumers as “enthusiasts.” Enthusiasts were distinct from typical consumers in that they would seek out higher levels of information, serve as opinion leaders, and actively engage in activities to “maintain, conserve, or enhance a product” (Bloch, 1986: 54). Firms first began to refocus their attention on enthusiasts who had continued to ascribe value to the mechanical watch during the quartz crisis. A former CEO discussed how he and other CEOs began to connect with these mechanical watch aficionados and collectors by traveling globally to seek their input. Many hosted events aimed at cultivating collector communities and re-engaging mechanical watch enthusiasts. Another executive noted that her company established a new norm of asking enthusiasts to participate in focus groups during the design of their new mechanical models, stating, “These individuals often know more about the brand and the technology than we do.” Enthusiasts took on new importance in the industry, not only because they bought watches, but because firms believed they could become third-party arbiters of value and authenticity for new consumers, much like art appraisers and wine connoisseurs (e.g., DiMaggio, 1987; Peterson, 2005).

Next, firms began to attract and cultivate new cohorts of enthusiasts. To do so, many broke from a long-held industry tradition of remaining highly secretive about their manufacturing processes. According to one executive, her firm began to invite potential enthusiasts on factory tours to witness their handcrafted production methods, noting, “If you see inside quality traditional watchmaking production, you have to appreciate it. Because it’s human, it’s real.” Once an unthinkable practice, factory tours became a way to educate and entice a wider range of consumers to become enthusiasts for brands and the community. On factory tours, I noted that guides encouraged participants to speak with watchmakers as they worked and to ask questions about the watchmaking process. Firms also hosted regional parties at exclusive clubs or hotels and flew their master watchmakers to these events to demonstrate how watches were crafted. Other brands hosted in-house watchmaking classes that gave new enthusiasts the opportunity to work alongside watchmakers. Such activities helped develop communities of enthusiasts, with the goal of cultivating a new generation of opinion leaders and informal “brand ambassadors.” Because consumer enthusiasts were “more often attracted, rather than repelled by product complexity” (e.g., Bloch, 1986: 54), many brands believed these individuals could serve as intermediaries to influence an even broader base of emerging watch consumers.

Communities of enthusiasts also helped Swiss watch firms identify emerging tastes and preferences of new consumers in previously untapped demographics. Mechanical watchmakers attempted to attract enthusiast consumers in new geographic regions. As household disposable incomes increased in countries outside the industry’s traditional U.S. and European markets, so too did the global appetite for luxury mechanical watches. The growth of worldwide watch sales offered increased stability to the mechanical watch industry in the early 2000s, especially as disposable incomes in the U.S. and Europe began to stagnate. A watch enthusiast in the Middle East, who was approached by several Swiss brands in the mid-2000s to become a retailer in the region, told me, “With this new wealth coming out, and more and more people having an interest in [mechanical] watchmaking, the mentality of people has changed. Nobody would have thought in the eighties that people would consider having three, four watches.” Mechanical watchmakers also targeted Asian markets. In 2008, the Federation of Swiss Watchmakers reported, “The Asian continent absorbed more than 46 percent of Swiss watch exports. Europe consumed almost a third, with the Old World recording a more modest increase (+4.4 percent). America lost some market share, accounting for 19 percent of Swiss export sales.” Several executives noted that their ability to cultivate enthusiasts in Asia, the Middle East, and Russia proved a critical driver of market growth during the 2000s.

Finally, firms relied on enthusiasts to help them better understand the tastes of younger consumers who had initially abandoned mechanical watches for future-oriented quartz watches. One CEO said that younger enthusiasts began to experience a shift in taste: “We now believe the younger population likes mechanical watches more and more because we’re working towards educating them. They are a highly technical customer, but they understand and appreciate the mechanical aspects.” Another CEO recalled that cultivating a younger consumer base had been critical to the resurgence of demand for mechanical watches, noting, “Young people wanted to wear mechanical watches again.” Consequently, mobilizing enthusiasts helped mechanical watchmakers expand their consumer base to a much wider and more diverse group of potential patrons.

Intermediate Outcomes of the Reemergence Process

Competitive differentiation

Several intermediate outcomes emerged from the phases of reemergence. First, the reconceptualization of community boundaries and membership had implications for competition. Executives reported that rising demand for mechanical watches, along with an influx of new entrants, generated a rise in competition among firms in the industry. Competitive differentiation took multiple forms. Some executives said that they purchased the naming rights to previously defunct brands that had gone bankrupt before or during the quartz crisis so they could sell mechanical watches under the legacy monikers again (e.g., Blancpain, Montres Leroy), and some luxury brands (e.g., Hermes, Montblanc) established watchmaking partnerships with Swiss manufacturers to produce “Swiss Made” mechanical watches. Many new brands entered the mechanical watchmaking community as well (e.g., Alpina, Frederique Constant). When asked how his firm differed from more-established brands, one new mechanical watchmaker explained, “We’re doing the mechanical watchmaking of the twenty-first century. . . . Everybody else is claiming to be from the nineteenth century.” Another CEO explained that it had become crucial to distinguish his watches from other mechanical watches: “We radically modernized the tradition of watches, placing [mechanical technology] in a very bold design, which was new because of the association with traditional mechanical movements.” The ad data offered evidence of mechanical watchmakers’ increased focus on competitive differentiation during reemergence. Reemergence (t3) saw a fourfold increase over retrenchment (t1) in the percentage of mechanical firms that chose to advertise, a measure of competitive differentiation often cited in marketing research (see Boulding, Lee, and Staelin, 1994) and especially luxury marketing (Fionda and Moore, 2009). Competitive differentiation appeared to serve as an intermediate outcome of the field having set new competitive boundaries and was an indication that competition in the newly established field had begun to ensue from within (e.g., Navis and Glynn, 2010).

Consumer differentiation

The expansion of consumer boundaries also led firms to begin differentiating customer preferences with far more granularity and within more-specific price segments. In the 1990s, industry consolidation led to the formation of the watchmaking “group” model, a firm comprising multiple brands under one owner. These brands often competed for the same customers (Donze, 2011; Breiding, 2013). Beginning in the 2000s, brands in the group model began to take great care to differentiate their consumers and vertically segment the market. According to a CEO in one group, the new strategy allowed each brand to target customers at a specific price point; for example, lower-priced brands might have sat at the bottom of an industry price pyramid but could still play an important role in attracting new customers. The CEO explained, “If you don’t have a base, you cannot have a top. A pyramid has a base. The larger its base, the higher you can build the top.” Another former CEO stated that his successor raised prices and quadrupled the company’s marketing budget to target consumers in a new price segment that didn’t compete with other brands in his group. The goal, he said, “was getting the company out of the mass market margins and into luxury market margins.” Alternatively, some brands that had traditionally focused on higher price segments were acquired and repositioned in the middle tier “in the hopes of luring the middle class” (Glasmeier, 2000: 249). One CEO explained how his brand exploited this strategy in the 2000s: “Clear product policy, clear marketing policy, clear distribution policy, and a very clear decision to stay in our price league. Every day I tell my people, stay in your [expletive] league.” Within each segment, brands began to employ unique strategies to attract a more specific type of core consumer. As demand for mechanical watches continued to increase during this period of market reemergence (t3), differentiating customers led firms to further refine the market for mechanicals to attract a more diverse base of consumers well beyond those who maintained the limited niche market for the legacy watch technology during the period of retrenchment (t1).

Reinvesting in innovation related to the legacy technology

The above processes culminated in firms reinvesting in innovation and manufacturing for mechanical technology across the field. The goals of these innovation efforts were to further distinguish each brand from others and to target the tastes of specific consumer segments. Early in the reemergence process (t2), only a few firms invested in mechanical innovation. While many Swiss firms remained focused on quartz innovation, one seller quipped that a small cohort began to shift its attention toward mechanical innovation: “We had high tech. Now we have ‘high mech’” (Passell, 1995: D9). During the second phase of reemergence (t3), the majority of Swiss brands followed suit and began to reinvest heavily in mechanical watch “complications”—innovations or functions on the watch other than the display of time (e.g., stopwatches, moon phase indicators, tourbillons). The CEO of a mechanical watch company established in the 2000s noted that his watchmaking methods were so novel that he applied for patents on the machinery needed to manufacture his designs. Innovation in material engineering also began to rise during the second phase of reemergence. Watchmakers utilized silicon, used in semiconductor chip manufacturing, to produce mechanical hairsprings that no longer required oil and offered improved accuracy. Others experimented in metallurgy. I embedded myself in one watch factory for a week to learn how the company had collaborated with a local university to develop a new alloy that fused 18-carat gold with ceramics. The process resulted in the world’s first non-corrosive and scratch-proof gold. Several executives acknowledged that their investments in mechanical watch innovation had fueled consumer demand in the 2000s. At an industry press conference, a CEO commented on how the industry had shifted: “In 1992 nobody wanted these [mechanical watches], nobody wanted to invest. Now, everybody talks about the success of the Swiss watch industry.”

Analysis of the ads illustrated a significant increase in mentions of innovation and new “complications.” During the second phase of reemergence (t3), an average of 28 percent of ads [q(4, 410) = 3.68, p < .001] mentioned watch complications; see figure 6. Between the period of displacement (t0) and retrenchment (t1), such mentions ranged from 21 to 11 percent, and there was no significant difference between retrenchment (t1) and the initial phase of reemergence (t2). These patterns reinforce interviewees’ statements that mechanical innovation and R&D resurged more broadly in the second phase of reemergence (t3) when firms began to redefine their market, but only after they had redefined the meanings and values of mechanical technology in the first reemergence phase (t2).

Average mentions of reinvestment in innovation and R&D—watch complications— in ads (1990–2008).

Technology reemergence

Nearly 40 years after the introduction of quartz watch technology had rendered Swiss mechanical watchmaking almost obsolete, 2008 marked 19 consecutive quarters of market growth for Swiss watch exports, 70 percent of which came from mechanical watches. The Swiss watchmaking community reported 67-percent growth over the previous five years and claimed record sales of 15.8 billion Swiss francs; its closest competitor, Hong Kong, reported 7.1 billion (Federation of the Swiss Watch Industry, 2009). The number of Swiss watchmaking employees had risen 40 percent since 1992, and as noted by one trade school instructor, watchmaking schools were again “blooming.” The Swiss had ceded their dominance in unit production to Chinese quartz competitors, but according to multiple industry analysts I interviewed, by redefining the technology and its market, Swiss mechanical watch producers were once again the “referent point” and “envy” of the industry in terms of demand growth, export value, innovation, design, and prestige.

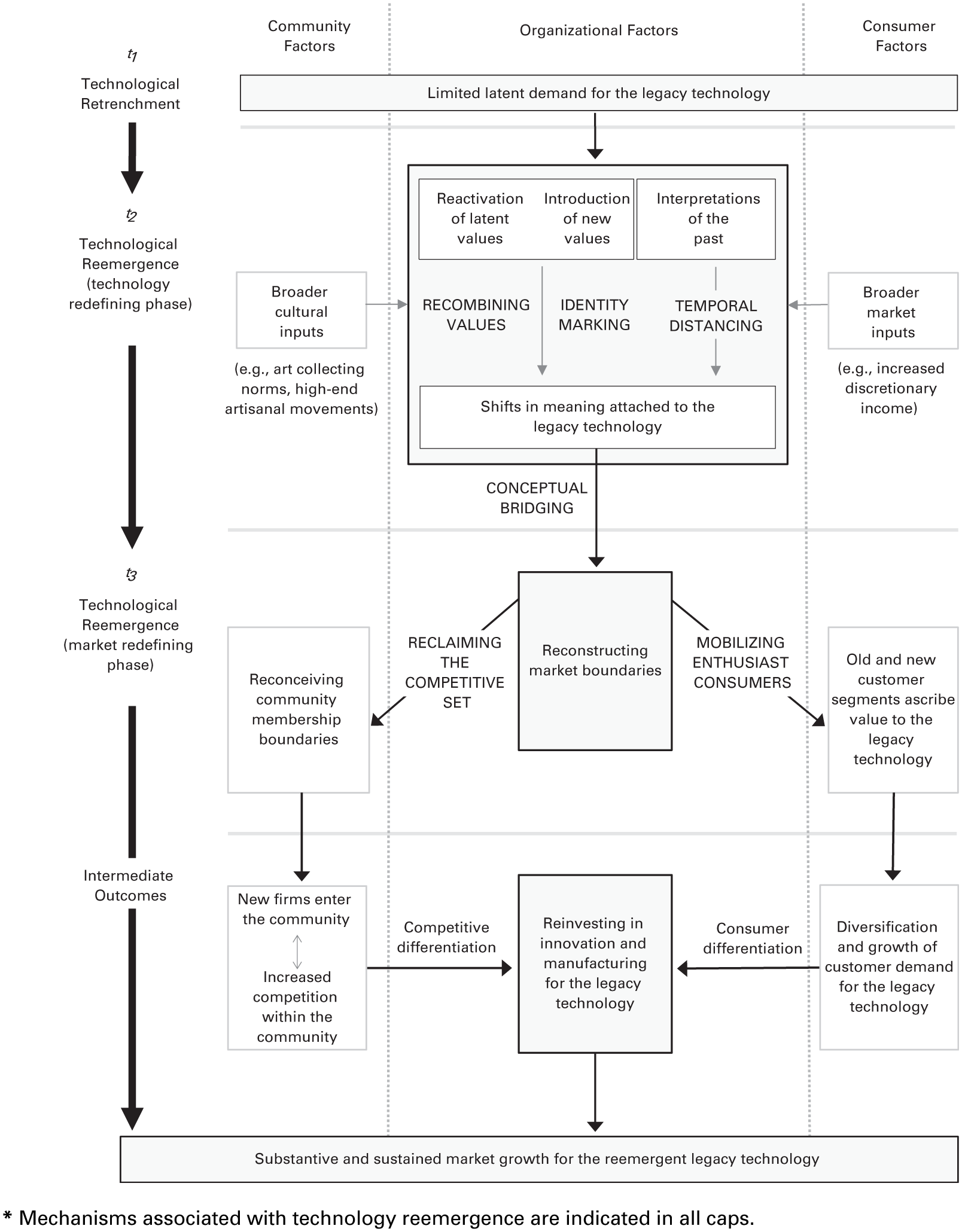

Figure 7 illustrates the process that led to the reemergence of market demand for mechanical watch technology. The figure also illustrates the co-evolution of the reemergence processes and mechanisms as they relate to various levels of analysis. It is divided into three sections that distinguish how the organizational-related mechanisms reported in the findings were influenced and affected by community- and consumer-related factors. Organizational factors are associated with the actions of individual watchmaking firms. Community factors identify “the set of organizations that have a stake in the development of the product class” and that “participate in technological information exchange, decision-making or standards-setting” (Rosenkopf and Tushman, 1998: 315, 316). Akin to Scott’s (1994: 207–208) conceptualization of an organizational field, these community-level factors focus on how mechanical watchmakers maintained a common meaning system for those who were seen as interacting “more frequently and fatefully with one another than with actors outside of the field.” Consumer factors are defined as the supply-side elements that influenced the consumer’s “willingness to pay for a product . . . [and] preference structure” (Adner and Levinthal, 2001: 612). The reemergence process summarized in the figure culminated in several intermediate outcomes associated with competitive and consumer differentiation, along with a reinvestment in mechanical innovations that coincided with a period of substantive and sustained demand growth for mechanical watch technology.

Process and mechanisms of technology reemergence.*

Discussion

This study contributes to literature at the intersection of technology cycles and cognition by explicating the process and mechanisms associated with technology reemergence: the resurgence of substantive and sustained market demand for a legacy technology following the introduction of a new dominant design. It extends prior work in the tradition of technology cycles and industry evolution (Abernathy and Utterback, 1978; Suárez, 2004) by explaining how a legacy technology and the firms and community that support it are able to generate multiple consecutive years of substantive demand growth and innovation after the introduction of a new discontinuous technology. In addition, this work advances a cognitive view of technological change in explaining technology reemergence and investigates how firms redefine meanings and markets (Eggers and Kaplan, 2013) associated with incumbents facing threats from discontinuous technologies. Taking a process approach to theory building (Langley, 1999), this research reveals several novel aspects of technological evolution and market cognition.

Expanding the Technology Cycle: Processes and Outcomes of Technology Reemergence

This paper extends theories related to technology life cycles and technology trajectories in multiple ways. First, it demonstrates that technology cycles may be more expansive than previously modeled, extending beyond birth (technology emergence) (e.g., Santos and Eisenhardt, 2009) and death or decline (technology displacement or retrenchment) (e.g., Sull, 1999; Adner and Snow, 2010) to include possible rebirth and reemergence. While technological shifts create waves of creative destruction, for some technologies these may not be permanent. Prior work on technology cycles (e.g., Tushman and Anderson, 1986; Suárez and Utterback, 1995) has focused on the discontinuous technology’s ascendance to a dominant design (see Henderson, 1995; Furr and Snow, 2015, for notable exceptions). Alternatively, this study’s focus on the trajectory of the legacy technology extends the notion of the technology cycle beyond the traditional path of variation, selection, and retention. The mechanical watch’s trajectory toward reemergence afforded the opportunity to reconsider several base assumptions about creative destruction (Schumpeter, 1934) and the path-dependent processes (Anderson and Tushman, 1990) that have consumed much of technology cycle research. Under certain conditions, demand for a legacy technology may rematerialize to generate significant market growth in ways that extend the traditional technology life cycle. Figure 8 illustrates how this research adds to our understanding of technology life cycles, and table 2 outlines legacy technology trajectories following the selection of a new dominant design.

Technology cycles and legacy technology trajectories.

Legacy Technology Trajectories Following the Selection of a New Dominant Design