Abstract

Socially responsible investing (SRI) is gaining traction in the financial sector, but it is unclear whether the dominant financial logic complements or competes with the social logic in the founding of SRI funds. Based on insights we gained from observation at an Asian SRI industry association, interviews with SRI professionals in the U.S. and Europe, and other fieldwork, we questioned explanations for SRI’s conflicted relationship with the financial logic. Our observations prompted us to build a panel database of SRI fund foundings from 1970 to 2014 in 19 countries so that we could examine how a dominant logic interacts with alternative logics to promote or stifle institutional change. We decomposed the financial logic into interdependent dimensions as the provider of means (resources, practices, and knowledge) for novel financial ventures to be founded and the enforcer of profit-maximizing ends that constrain such foundings. Our theory suggests a paradoxical role for the financial logic, which explains an intriguing empirical finding: the founding of SRI funds has a curvilinear, inverted-U-shaped relationship with the prevalence of the financial logic. We propose and find that the relationship between the dominant financial logic and the social logic of SRI shifts from complementary to competing as the financial logic becomes more prevalent in society and its profit-maximizing end becomes taken for granted. We examined how certain alternative logics—those of unions, religion, and green political parties—moderate these effects. Our results shed light on how and to what extent institutional change can occur in fields in which one institutional logic is dominant. They also reveal country-level institutional factors that drive SRI.

Keywords

Institutional logics define the organizing principles of an institutional order, such as its values, norms, assumptions, and practices (Thornton, Ocasio, and Lounsbury, 2012). In the financial sector, a dominant financial logic that focuses on individualism and profit maximization plays this guiding role (Friedman, 1970; Jensen, 2002). A number of authors have observed that the financial logic increasingly characterizes the functioning, priorities, and values of business organizations, financial and otherwise (Epstein, 2005; Krippner, 2005; Davis and Kim, 2015). In the context of this growing prevalence of the financial logic worldwide, often seen as an intrinsic part of the global diffusion of economic rationality (Meyer et al., 1997; Polillo and Guillén, 2005; Weber, Davis, and Lounsbury, 2009), the emergence of socially responsible investing (SRI) is somewhat puzzling. SRI, a hybrid practice that brings environmental and social goals into the world of investments, has emerged as a promising and potentially impactful alternative to mainstream financial investment practices (Sparkes, 2003; Pache and Santos, 2013; Battilana and Lee, 2014; GSI-Alliance, 2015), but it seems to contradict the central individualistic values and premises of the financial logic.

Several authors studying institutional logics have observed that logics are “mutually dependent, yet also contradictory” (Friedland and Alford, 1991: 250), but we need to know more about the conditions under which logics like those underlying SRI are complementary or competing, or may even shift from one to the other. Previous studies of SRI and other financial organizations with social ends have found a conflicting relationship between the financial logic and social goals. In the Swedish mutual fund industry, for instance, the more that investment professionals were steeped in the financial logic, the more firmly and persistently they resisted the emergence of SRI funds (Jonsson, 2009; Jonsson and Regnér, 2009), because SRI was perceived as inconsistent with the norm of maximizing financial returns. In U.S. community banks, Almandoz (2012) similarly showed that founders’ deeper embeddedness in a financial logic was detrimental to the founding team’s success in starting a community-oriented bank. But other studies have found that financial and economic institutional logics are potentially complementary with other logics (Lee and Lounsbury, 2015; Smets et al., 2015). Mainstream financial organizations steeped in an existing financial logic, such as mutual funds (Lounsbury and Crumley, 2007) or commercial banks (Marquis and Lounsbury, 2007), may be sources of well-trained personnel who leave those firms to found competing organizations based on other logics (Thornton, Ocasio, and Lounsbury, 2012). In this way, the financial logic can simultaneously provide means that can be used for a variety of social ends and constrain those ends by making enterprises steeped in social goals illegitimate. In terms of the rise of SRI funds, some aspects of the financial logic related to its profit-maximizing ends may be detrimental, while other aspects related to actors’ knowledge, expertise, and practices, which could be redeployed as means for a variety of social ends, may be beneficial.

Whether the financial logic is complementary or competing with other social goals likely depends on the overall prevalence of the financial logic in society. The more prevalent it is, the more that the financial end of profit maximization becomes taken for granted, especially in the financial domain, and the more likely it is that financial means will be employed toward only that end. Therefore, as the financial logic becomes more prevalent in society, the relationship between financial and social logics should shift from complementary, leading to more SRI founding, to competing, leading to less SRI founding. Both forces may be present simultaneously, but at a certain point of financial prevalence, the constraining influence of the financial logic may equal or even surpass its enabling role. A peak of SRI foundings could be reached followed by a decline in SRI foundings when the means and resources of the financial logic are redeployed almost exclusively to serve traditional financial end goals.

While the financial logic plays a dominant role in the field of financial organizations (Reay and Hinings, 2009), other institutional forces can shape the dynamics of the field and thus contribute to the emergence of SRI (e.g., Durand and Jourdan, 2012). Community, religion, and the state are three of the most commonly studied and relevant institutional logics in the SRI context, because they foster ends that complement the social ends of SRI and conflict with the profit-maximizing end of the financial logic. On one hand, these alternative ends could allow social logics to engage more successfully with the means (resources) available to actors steeped in the financial logic and better facilitate the establishment of new SRI funds. On the other hand, these alternative ends could suffer from a “deviance discount” imposed by the financial logic (Jonsson, 2009; Jonsson and Regnér, 2009) that may hinder their usefulness for SRI emergence. When the dominant financial logic and those alternative logics are all highly prevalent, the resulting friction may diminish the likelihood of financial and social logics successfully integrating for the emergence of new SRI funds.

Other scholars have shown that one logic may amplify or hinder the influence of another (Reay and Hinings, 2009; Lee and Lounsbury, 2015), but we hope to show that such influence varies depending on how prevalent a dominant logic is in society. We also examine whether decomposing institutional logics into means and ends helps to explain how the relationship between the dominant financial logic and the social logic shifts from complementary to competing, and thus we suggest a potentially important framework in the analysis of the adoption of hybrid practices and of institutional change. Finally, we aim to shed light on what drives the emergence of SRI across time and countries, as a special case of the expansion of a hybrid practice.

Competing and Complementary Logics

The Complexity of Socially Responsible Investing

There is considerable heterogeneity in terminologies, definitions, strategies, and practices (Sandberg et al., 2009), but in broad terms SRI is a hybrid form of investing that incorporates non-financial concerns—such as environmental, moral, and social—into investment decisions. This form of investing embodies institutional complexity: the presence of competing stakeholders (Fligstein and McAdam, 2012; Scott, 2014) and contradictory prescriptions from multiple logics (Kraatz and Block, 2008; Greenwood et al., 2011). The institutional origins of SRI reflect this complexity. The roots of modern SRI had strong religious underpinnings, particularly in Christianity, because Christian churches “played a pioneering role in the development of SRI globally” (Sparkes, 2006: 43). In the U.S., SRI began with John Wesley, one of the founders of the Methodist movement in the eighteenth century, who opposed investing in sinful activities, such as the slave trade, the arms trade, and alcohol. The first modern SRI mutual fund in the world, the PAX World Balance Fund, was established in 1971 by United Methodist ministers concerned about profiting from the Vietnam War. As the market offered “no alternatives at the time” (Sparkes, 1995: 115), those ministers mobilized and created, with the help of financial professionals, a niche sector for retail investors that attracted churches, charities, endowments, nongovernmental organizations (NGOs), and socially conscious individuals. Thus the religious logic is important in this domain.

As SRI moved beyond niche market segments, it expanded from merely abstaining from certain sectors to advocating for socially responsible practices, including fair employee compensation and benefits and, more broadly, human rights. For that reason, trade unions representing workers’ rights were at the frontline of the SRI movement (Jonsson and Regnér, 2009; Arjaliès, 2010; Giamporcaro and Gond, 2016). The first SRI legal case in the U.S., Cowan v. Scargill, was brought to court in 1984 by trustees of the mineworkers’ pension fund. SRI attracted more interest in the mid-1990s, when sweatshop scandals erupted at public corporations, leading unionized workers to move their pension fund assets away from those organizations (Rivoli, 2003). Worker and trade unions played a role in the diffusion of SRI practices because of their governance role in many pension funds, which are increasingly dominant in capital markets (Sparkes, 2003; Vitols, 2011).

States started to influence the development of SRI when SRI began to occupy a significant portion of total investment assets (Lewis and Juravle, 2009). A critical moment with global repercussions came in 1997 when the Labor government in the UK instituted SRI disclosure requirements for pension assets (Sparkes, 2003). France, Germany, Sweden, Belgium, Norway, Austria, and Italy quickly followed suit (Vitols, 2011). The adoption of SRI policies in 2004 by the Norwegian Sovereign Wealth Fund was also important, as it resulted in some high-profile decisions such as its 2008 divestment from Walmart (Vasudeva, 2013).

In spite of its social goals and ambition, SRI is a financial investment practice and thus deeply rooted in the financial logic; that logic is dominant and central in the construction of an SRI fund (Besharov and Smith, 2014). An uncompromising component of SRI is that financial return is important. In fact, “One of the key factors distinguishing SRI from charitable giving is concern for financial returns” (Sparkes, 2003: 22). Logue (2009: 1) stated that “done incorrectly . . . [SRI] sometimes emphasizes feeling good over making money. That’s unfortunate [because SRI] isn’t separate from good investing.” The importance of both social and financial goals highlights the complexity surrounding this hybrid investment practice. The main concern with SRI is that the social goals important to SRI founders are not perceived as legitimate in the context of the global financial logic in which SRI is embedded.

A Global Financial Logic

Due to the global diffusion of rationality in society’s governance (Meyer et al., 1997), the utilitarian, materialistic culture of the financial logic has powerfully affected nation-states (Polillo and Guillén, 2005; Weber, Davis, and Lounsbury, 2009) and has universally prescribed self-interested and profit-maximizing norms, values, and practices (Fourcade, 2006). But even though it has a global and deepening reach (Davis and Kim, 2015), the financial logic has seeped into each country’s institutional fabric to a different depth. The greater prevalence of the financial logic in a country increases the probability that financial values, norms, and ends will be taken for granted and externalized as objective facts (Berger and Luckmann, 1966), not only in the financial field but in society more broadly.

The financial logic is so prevalent in the U.S. that it is natural for people to refer to education as investing in human capital and to friendship as building social capital (Davis, 2009): various spheres of personal life have increasingly become understood in financial terms and therefore as potential objects for securitization (Zelizer, 2007). In that kind of society, it is not surprising that even the value of such social organizations as nonprofit hospitals (Brickley and Van Horn, 2002) would be measured in terms of financial goals. Dominant logics prevalent in society thus appear to exert a gravitational pull on other logics, altering their orientations. Alternative logics might resist this colonization (Marquis and Lounsbury, 2007) or find complementarities with the dominant ones at the level of practices (Smets, Morris, and Greenwood, 2012). Under what conditions dominant and alternative logics can be complementary remains an open question.

How Means and Ends Affect the Complementarity of Logics

Decomposing the financial logic into means and ends can shed light on the conditions under which that logic complements or competes with alternative logics in society. Institutions not only prescribe “the end goals towards which actors should be directed, but also the means by which those ends are achieved” (Friedland and Alford, 1991: 251). Decomposing logics into means and ends, either explicitly or implicitly, is a fairly common practice in the institutional literature (Friedland and Alford, 1991; Pache and Santos, 2010; Durand and Jourdan, 2012; Wijen, 2014). Many frequently discussed components of institutional logics, such as motivations, values, interests, and goals, can be categorized as ends, whereas others, such as material practices, resources, experiences, and expertise, could be classified as means. This decomposition may help explore tensions and contradictions within a dominant institutional logic in a field when that logic provides means for practices inspired by alternative institutional logics that may contradict the ends considered legitimate in the dominant logic’s particular domain. 1 The relevance of the means or the ends may be different in different contexts, which could have implications for whether the dominant institutional logic complements or competes with alternative logics.

Exploring this form of intra-institutional complexity (Meyer and Hollerer, 2016), with the means and the ends of the same institutional logic pulling in different directions, may provide important insights about complexity, the diffusion of hybrid practices, and institutional change. Most research on complex institutional environments has focused on how different logics exercise competing demands, but some researchers have distinguished the impact of complexity based on different dimensions of logics. Pache and Santos (2010) proposed that conflicts about the ends of institutional logics bring about more explicit contestation or defiance and a lower likelihood of compromise than conflicts about means. Durand and his colleagues found especially severe conflict among organizations when competition involved end goals (Durand and Paolella, 2013; Paolella and Durand, 2016). By contrast, other research has found that carriers of different logics may have a collaborative relationship (Lee and Lounsbury, 2015), as one institutional logic may provide symbolic and material resources (Swidler, 1986; Thornton, Ocasio, and Lounsbury, 2012; Durand et al., 2013) to actors imbued with the other logic (Lounsbury, Ventresca, and Hirsch, 2003; McPherson and Sauder, 2013) who may pursue divergent goals and interests. But to our knowledge no scholarship so far has addressed how different dimensions (means and ends) of the same institutional logic exercise competing influences and how a dominant institutional logic may shift, depending on contingent factors, from being complementary to competing with alternative logics.

The means of a logic (resources, practices, knowledge) should initially be more versatile than its ends, as they can be deployed toward various ends. The ends of the logic give these means a direction (provide a purpose) and imbue them with values (legitimizing them). Over time, if a logic becomes more prevalent, audiences increasingly see the means of that logic solely as an expression of the logic’s ends. This univocal interpretation of a logic’s means is normatively enforced by stigmatizing any other use of those means as unprofessional, amateurish, or even sacrilegious. Yet these means can be redeployed toward different ends by actors in the field who are carriers of more than one logic (Almandoz, 2014; Scott, 2014), and that redeployment can, in turn, translate into a creative hybrid recombination of the original logics and be an engine for institutional change. This process is more likely to happen when the means of the logic are mature enough to be useful and transferable across ends and when the ends are not so pervasive in society that they limit actors’ ability to see the opportunities for reusing the same means to different ends.

In terms of SRI founding, while legitimacy constraints enforced by the ends of the financial logic may decrease SRI founding in countries where the financial logic is more predominant, transferrable resources generated by the financial logic, such as financial experience and skills, may provide the means to facilitate such founding. As one SRI professional we interviewed put it, “I have been in this industry for 20 years. What I do now is to apply finance skills in areas other than large banks. In social sectors, [these] skills are badly needed” (fieldnote, 5/30/14). Thus, paradoxically, the financial logic could simultaneously aid and constrain the founding of SRI funds. Which of the two effects has a greater impact on such foundings likely depends on the prevalence of the financial logic in society, with the constraining effect being stronger at higher levels of prevalence.

The Paradoxical Effect of the Financial Logic

Although the founding of SRI ventures is obviously affected by general market conditions and consumer demands, it fundamentally depends on two interdependent factors: strategic actors’ choice or motivation to form an SRI fund and the available resources or means for doing so, which in turn are shaped by the characteristics of the institutional environment. The financial logic likely affects both factors: finance as a source of legitimate ends constrains the founders’ motivations to start SRI funds, and finance as a provider of means supplies the societal resources to establish SRI funds. Given that both factors are necessary and complement each other in SRI foundings, the number of SRI funds founded in a given society each year should be a multiplicative function of these two interrelated forces arising from the financial logic.

Low prevalence of the financial logic

When the financial logic’s prevalence in a society is low, financial values and beliefs are accepted but not taken for granted. Thus the ends of the logic do not significantly constrain how the means it provides are used, and actors can more freely incorporate ends and goals supplied by other logics. In such societies, financial organizations embodying various end goals could be legitimate (Durand and Paolella, 2013; Paolella and Durand, 2016). In the early history of SRI, many of its pioneers were able to diverge from what would become taken-for-granted financial norms, because their normative status had not been established (Lounsbury, 2002), and various forms of financial organizations were considered legitimate. One such pioneer, Joan Bavaria, launched her own SRI initiatives in the 1970s, when the professional norms of finance were less strictly defined in the U.S. than they are now. As the country experienced a period of social unrest and reflection, Joan “was open to new and different considerations in the practice of investment management: practices that encompassed social and environmental, as well as financial, criteria” (Waddock, 2008: 71).

A weak financial logic could even need to defer to alternative social, community, and state logics to enhance its standing in society, giving rise in some cases to SRI entrepreneurship. Jourdan, Durand, and Thornton (2017) documented a case of such deference in the context of private equity funds (the financial logic) financing unprofitable art-house French films (an alternative logic), thus conveying appreciation and respect to those film producers, to increase the funders’ standing in the field.

But founding an SRI fund always requires some resources from a financial logic, typically available only in a society in which finance is at least modestly prevalent. Robert Zevin, another SRI pioneer in the U.S., was already a financial expert when he started his own SRI firm; as a Harvard economics Ph.D., he was among the first fund managers to use modern portfolio management theory and was deeply familiar with the resources provided by finance. When financial resources are unavailable, few SRI foundings are expected. One SRI expert attributed the marginal presence of SRI in emerging economies to the undeveloped nature of their financial markets and institutions. As she explained, one does not expect SRI to emerge “when the stock market and major pension funds are immature and the regulatory processes need time, and potentially a lot of time”; in those cases, “to develop SRI is simply too exotic” (e-mail communication, 10/27/12).

Moderate prevalence of the financial logic

Various material and cultural means provided by the financial logic are portable and can be incorporated in a variety of organizations with multiple end goals. At moderate levels of financial prevalence, actors may be able to deviate from financial end goals yet still gain access to these means. In this case, alternative institutional forces may play a more complementary role with the financial logic in fostering novel financial ventures, and traditional financial actors and deviant players with different interests and identities will more likely be able to manage the rivalry of competing institutional logics through collaborative relationships (Reay and Hinings, 2009).

High prevalence of the financial logic

In societies in which the financial logic is highly prevalent, even if the resources conferred by that logic are plentiful, those resources are less likely to be diverted toward financial organizations with goals other than profit maximization because their goals may be categorized as deviant and thus illegitimate (Durand and Paolella, 2013; Paolella and Durand, 2016). Financial values and beliefs are not only accepted but taken as the normative and exclusive way of organizing the economy (Friedman, 1970; Jensen, 2002), especially the financial sector. This is because neo-classical economic thinking has shaped the ends of the financial logic and has established profit maximization as a normative principle (Friedman, 1970; Ferraro, Pfeffer, and Sutton, 2005). When maximizing financial returns becomes the only legitimate end goal in the financial sector, nonfinancial goals are considered inappropriate. Thus when the prevalence of the financial logic is higher, the means and ends associated with the financial logic are likely to be more tightly coupled. Under these conditions, the financial logic may not completely drive out SRI, but it may reduce considerably the number of SRI foundings.

In interviews with SRI professionals, we found a great deal of resistance toward SRI coming from actors deeply embedded in the financial logic, as they could measure the effectiveness of SRI only in terms of financial performance. A research analyst based in Hong Kong—where the financial logic is highly predominant—explained how his colleagues perceive SRI: “In our company, if you go around and say SRI, they will go mad. ‘Could you quantify SRI impact [on returns] on a three-month basis?’” (fieldnote, 3/18/13). This is consistent with prior findings on SRI in Sweden; as Jonsson (2009: 177) stated, SRI was not considered “sound asset management” because “[investment] should be done to earn money.” In societies with predominant financial logics, leaders of the SRI communities admit a “continuous frustration” that SRI is often opposed on the basis that “it hurts returns” (fieldnote, 3/18/13), and SRI managers we interviewed often made a point of distancing themselves from purely social objectives, insisting that their goal was to achieve competitive financial returns. The managing director of an SRI investment firm in the UK said, “It is not altruistic; it is about good returns on a good investment which happens to have a beneficial byproduct” (Financial Times, 1/23/12). The regional head of a large U.S.-based asset manager stated at an SRI conference, “We must be able to stand in front of the clients and say our [SRI] approach helps returns” (fieldnote, 3/18/13).

In a society in which the prevalence of finance is increasingly growing, the number of SRI funds being established would likely increase with the prevalence of the financial logic until potentially a peak would be reached, and then foundings would decline at higher levels of financial prevalence. It is hard to tell ex ante whether the number of SRI funds being founded will reach a peak and then inflect downward in every country, as not all countries reach high levels of financial prevalence. But we can theoretically hypothesize an inverted-U-shaped curvilinear relationship 2 :

The Impact of Alternative Institutional Logics

Organizational fields are typically structured by a dominant institutional logic, but alternative logics may also play an important role (Reay and Hinings, 2009; Durand and Jourdan, 2012). The logics of community, religion, and the state represent ends that complement those of the social logic of SRI but compete with those of the financial logic. Similar to research showing that certain logics amplify or dampen influences arising from other institutional forces (Lee and Lounsbury, 2015), we propose that other institutional forces will also moderate the effect of the dominant financial logic on the founding of SRI funds.

In the SRI context, both prior literature and our fieldwork and interviews suggest that labor unions, Christianity, and green parties in government exemplify the kind of institutional forces that could have a moderating relationship with the founding of SRI funds. In the case of unions, the logic prioritizes workers’ welfare over the goal of profit maximization. In the case of Christianity, the end is salvation and social justice. And in the case of green parties, the goal is ecological and environmental sustainability rather than making as much money as possible. The strength of these alternative institutional forces was acknowledged by one informant who described the SRI field as a “complex [phenomenon], with religious, political, and social dimensions” (fieldnote, 1/10/13). When the financial logic is sufficiently present but not very prevalent, the dominant financial logic can defer to the ends of the alternative logics (Jourdan, Durand, and Thornton, 2017) and provide sufficient resources for establishing new SRI funds. Under these circumstances, the ends and values promoted by unions, churches, and green parties in government could promote SRI fund startups (Durand et al., 2013; McPherson and Sauder, 2013).

Unions

The presence of unions represents not only an institutional force but also a set of organized actors who own financial assets and determine how they are invested. Pension fund reforms in many countries have allowed unions to convert workers’ savings into financial assets managed by fund professionals, thus transforming workers into legal owners (Drucker, 1976; Hacker, 2004; Davis and Kim, 2015). As workers’ pensions were increasingly invested in corporations, unions gained influence over their policies and practices, which gave unions a reason to overcome their dislike for the financial sector and develop a relationship with it (Penalva-Icher, 2012). In December 2007, the largest international association of trade union organizations issued a statement on “Responsible approaches to the stewardship of workers’ capital” and urged “pension funds, their trustees, and fund managers to include in their investment decision-making process the impact, both positive and negative, of their investments on workers, communities and the environment” (TUAC, 2007).

Prior research and our qualitative evidence suggest that when the financial logic is not highly prevalent, the presence of unions may complement the financial logic to foster the founding of SRI funds. Jonsson and Regnér’s (2009) analysis indicated that union ownership of mutual fund firms encouraged the adoption of SRI practices. Arjaliès (2010), Giamporcaro and Gond (2016), and Gond and Boxenbaum (2013) revealed the important role that unions played in initiating and sustaining the SRI movement in France. Our qualitative evidence also reveals that labor union leaders were active in launching the Principles for Responsible Investment (PRI) in 2006, a United Nations–sponsored global association of responsible investors. Three labor union leaders sitting on PRI’s board were also trustees of large pension funds. 3 This evidence suggests that if the normative constraints of the financial logic are not too rigid, the more that unions are prevalent in society, the more likely union leaders are to influence corporate pension funds’ supervisory boards (Powdrill, 2006) and invest in companies that treat their employees well.

When the financial logic’s prevalence is high, however, financial values and norms are likely to be more dominant. When profit maximizing has been normalized as the uncontested end goal of the financial institutional order, polarization and conflict between competing ends are likely to occur when union actors become involved in the financial sector (e.g., Pache and Santos, 2010; Almandoz, 2012; Battilana and Lee, 2014). Such tensions are likely to diminish the likelihood of collaboration among opposing actors embedded in different logics (Glynn, 2000; Reay and Hinings, 2009).

Although the increasing prevalence of the financial logic is still likely to provide financial resources for the founding of SRI funds, its constraining effect may be stronger in the presence of prevalent unions, causing the SRI founding curve to drop at a higher rate after surpassing a certain threshold of financial prevalence. The strength of forces such as unions may affect the popularity and performance of SRI funds, but those forces may have little influence on SRI entrepreneurship if they clash with the boundaries of what is considered legitimate in the financial domain. Taken together, these arguments suggest that a stronger union presence is likely to moderate the relationship between the financial logic and the founding of SRI funds, making the curvilinear relationship steeper. Union presence will strengthen the complementarity between the financial and social logics up to a certain threshold of the financial logic, after which it will heighten the conflict between the financial and social logics. We thus propose:

Religion

As an institutional force, religion operates primarily through its cultural or moral influence on society, which is very different from unions’ mechanisms of influence on the establishment of SRI funds. We have already noted the influence of the Methodist Church on SRI founding. In 1983, the Religious Society of Friends and the Methodist Church sponsored the foundation of the UK ethical research service EIRIS, a key SRI service provider. The first generation of SRI investors included mostly religious individuals and organizations who wanted to align their moral beliefs with their investment practices. Religion, specifically Christianity, also played a crucial role when SRI spread globally. As one informant put it, “Religion played a much more important role in SRI than is recognized. Many Asians who started green-tech funds were Christians. I see nothing essentially different between religious investors in Asia and in Europe or America” (fieldnote, 1/10/13).

Assuming that religious values make a significant difference in people’s daily behavior, we propose that, in the absence of a strong prevalence of the financial logic, there is a positive relationship between a more widespread presence of religious values and the founding of SRI funds, as the means of the financial logic are deployed toward that end. When the prevalence of both logics is high, however, then religious and financial values are more likely to compete (society will be more polarized), which will make it more difficult to reconcile social and financial ends in the establishment of new SRI funds. In those societies, profit maximization is more likely to be institutionalized as the only goal in the financial sector. These arguments combined suggest that a stronger presence of Christianity is likely to moderate the relationship between the financial logic and the founding of SRI funds, making the expected curvilinear relationship steeper. We thus propose:

Green political parties

The strength of green political parties represents an institutional force that is both cultural (affecting ecological sustainability) and coercive (tapping the power of the state). Upholding a distinct institutional logic that emphasizes societal welfare and stability (Greenwood et al., 2010), the state may play a crucial role in creating a regulatory environment that increases or decreases the influence of the financial logic on SRI entrepreneurship. Several historical examples illustrate the importance of state influence (Yan and Ferraro, 2016), such as the inclusion of SRI disclosure requirements for pension assets in the UK (Sparkes, 2003) and Norway’s instruction to its sovereign wealth fund to adopt responsible investing principles (Vasudeva, 2013). Green parties have rarely been in power, but they have occasionally been able to shape mainstream policy discourse and practice by forging alliances with larger parties (Rüdig, 1991; Little, 2016). Studying a cross-national sample in Organization for Economic Co-operation and Development (OECD) countries, Knill, Debus, and Heichel (2010) found that when political parties stressing environmental issues were well represented in a country’s parliament, governments were more likely to adopt a higher number of environmental policies that could encourage wider green activism. Even if green parties do not explicitly endorse SRI, they can foster a more SRI-friendly regulatory environment, for example, by supporting subsidies to green sectors (Scholtens, 2005). The presence of strong green parties in a given country would be correlated with a higher likelihood of environmental motivations at the origin of SRI fund startups.

In the absence of normative resistance arising from the financial sector, the strength of green parties is likely to positively moderate the relationship between the dominant financial logic and the founding of SRI because those environmental motivations in society can engage the means and resources provided by the financial logic. Since its founding, SRI has been closely associated with care for the environment (Sparkes, 1995: 9; Domini, 2001: xvii), which is the central concern of green parties. But sustainability represents a competing end to profit maximization, so as the prevalence of the financial logic approaches a certain threshold, resistance to state green activism is likely to increase. For example, the National Association of Pension Funds in the UK publicly opposed the government’s decision to introduce SRI into pension systems by suggesting that SRI “would lead to higher administrative costs” (Sparkes, 2003: 11). Because of a polarization of ends at higher levels of prevalence of the financial logic, we would expect a lower likelihood of collaboration between green and financial actors and thus that the strength of green parties is likely to moderate negatively the relationship between the dominant financial logic and the founding of SRI funds.

Methods

With our broad goal to understand what drove the emergence of SRI internationally, we conducted several exploratory field projects at multiple sites from 2008 to 2014. The projects included following the activity of the Interfaith Center for Corporate Responsibility (ICCR) from 2008 until 2012, conducting an interview-based study of the evolution of the field from the perspective of data providers, and completing both a year-long participatory observation (Spradley, 1980) at an Asian SRI industry association (2012–2013) and a stint as a participant-observer in a China-based, mid-sized SRI mutual fund. In the process, we participated in over 20 SRI industry conferences and interviewed 81 professionals in the field. As we worked on these projects, we noticed that SRI professionals had a conflicted relationship with the financial logic: they carried it with pride but were also frustrated by how it was developing over time. As we tried to make sense of this from a theoretical point of view, we developed the idea of decomposing the financial logic into means and ends and then developed testable hypotheses.

Data Sources

We collected all our SRI information from Bloomberg. 5 Many prior studies on SRI funds have relied on the classification by the United States Social Investment Forum (e.g., Hong and Kostovetsky, 2012), which is produced in collaboration with Bloomberg. Bloomberg has also classified the attributes of funds by having analysts read through each firm’s prospectus. Because the prospectus is legally binding, this ensures that the status of being an SRI fund is reasonably reliable. The data are free from survivorship bias, so we can track which funds are still active and which ones are already closed. Bloomberg provides inception dates for most funds, which we used to determine the founding year of the funds. We excluded funds that did not have founding dates (1.81 percent of the entire SRI population). We collected country-level variables from the World Bank, the International Labor Organization, World Value Surveys, the International Monetary Fund, International Institute for Management Development World Competitiveness Report, and the OECD.

Sample

Our sample covers a broad range of fund types that cater to different investors. While retail funds account for 55 percent of the sample, it also includes funds oriented toward a variety of institutional investors, including superannuation funds, insurance firms, and pensions. We used a conservative measure of socially responsible funds, which is those that are explicitly categorized as “socially responsible.” Other fund types could implicitly follow similar principles, but including those categories may introduce too much noise in the dependent variable. Not only may there be many false positives in those categories, but in some cases those funds may be driven primarily by other institutional forces outside of the financial logic’s domain. 6

Following prior studies (Khorana, Servaes and Tufano, 2005), we identified each fund’s country by its legal domicile. We excluded from the analysis all funds domiciled in known offshore sites (Khorana, Servaes and Tufano, 2005), such as Luxembourg, Liechtenstein, Cayman Islands, Ireland, Isle of Man, British Virgin Islands, Jersey, Guernsey, Netherlands Antilles, and Bermuda, because it was difficult to ascertain the societal influences of these offshore sites on the SRI funds. 7 Due to missing values and non-variation in the dependent variable, Stata dropped 16 countries from the population of countries in which SRI is present. These countries averaged 4.5 founding events throughout our observation window, so excluding them was unlikely to affect our main findings. Our final sample consisted of 670 observations across 19 countries from 1970 to 2014.

Dependent Variable

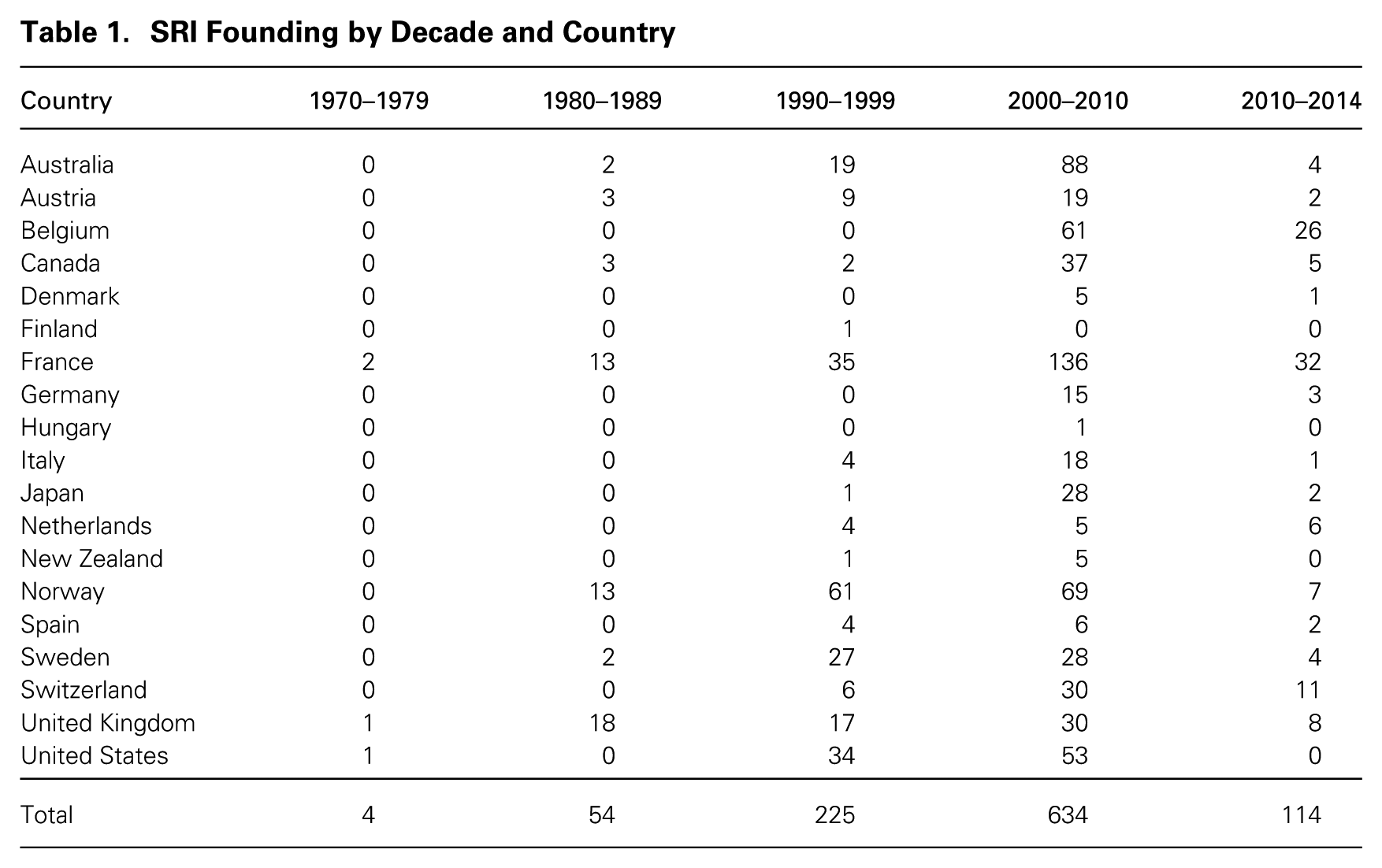

Following most organizational analysis on new venture creations (Carroll and Hannan, 2000), we modeled founding of SRI funds as an event count: the number of newly started SRI funds per country year. This measure reflects entrepreneurial activity arising from the financial sector in a given country. It is better than the cumulative number of SRI funds, which reflects the confounding effects of fund failures and societal conditions in previous years, and also better than assets under management, which reflects founding success (Marquis and Lounsbury, 2007) and consumer demand for SRI instead of entrepreneurial activity—the subject of this study. See table 1 for a summary of SRI founding by country and time.

SRI Founding by Decade and Country

Independent Variable

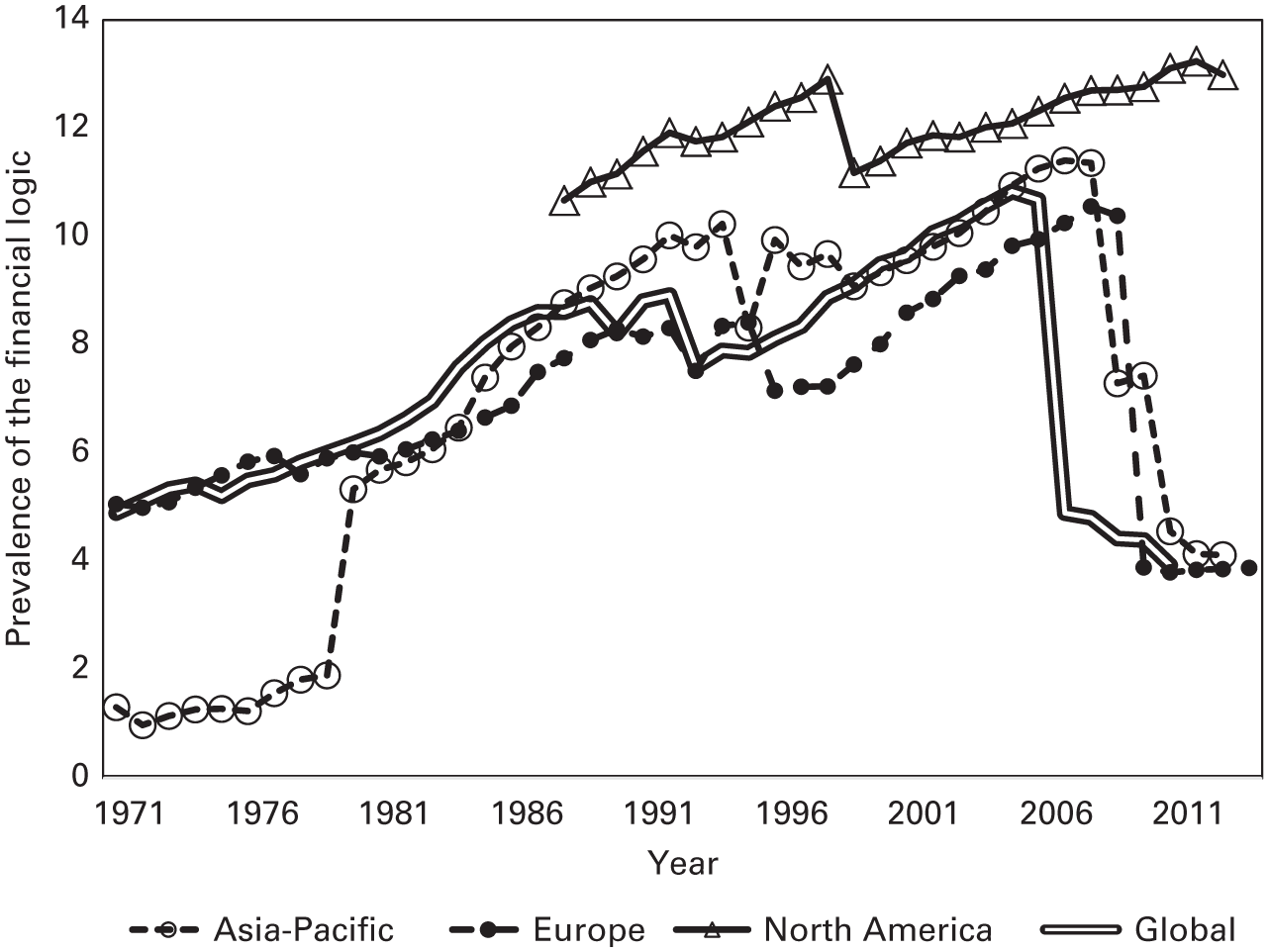

We measured the prevalence of the financial logic in society by using the proportion of the workforce employed in the financial sector based on International Labor Organization data; see figure 1 for financial prevalence by continent and year. We followed the definition of the financial sector from prior studies, which have used the employment proportion in finance, insurance, and real estate—the FIRE sector (see Krippner, 2005, for a justification for including the real estate sector and Tomaskovic-Devey and Lin, 2011; Lin and Tomaskovic-Devey, 2013, for empirical applications).

The prevalence of the financial logic by continent and year and the global trend over time.

Our use of this indicator was appropriate for two reasons. First, the proportion of the workforce employed in the financial sector captures the means or resources that the financial logic can provide to potential initiatives such as founding SRI funds, which require financial skills and familiarity with financial organizations. To assess the backgrounds of people entering the SRI industry, we also checked 4,385 career moves involving 2,523 people that appeared on responsible-investor.com, the primary news outlet dedicated to the SRI community, and found that professionals joining SRI funds came almost exclusively from commercial banking, investment banking, and asset management companies.

Second, that same proportion is also a good indicator of the degree to which the ideological component of the financial logic—emphasis on self-interest and profit-maximizing end goals—is likely to be legitimate or normative in society, especially in the context of establishing new financial organizations. Abundant research has shown that education in finance and economics imprints in people a cognitive mindset that is conducive to self-interested and profit-maximizing behavior (Frank, Gilovich, and Regan, 1993), and therefore finance professionals are likely carriers of the financial institutional logic, especially its normative ends (Scott, 2014). Prior studies have used professional experience in finance as a measurement of individuals’ and teams’ embeddedness in the financial logic, and their results have suggested that embeddedness in the financial logic is stronger in its ideological effects at higher levels of aggregation, such as in larger groups (Almandoz, 2014), and hence even stronger at country levels. 8

To tease out the effect of the financial logic as means and ends, we conducted a separate analysis using two independent variables to directly measure means and ends. We used financial institution depth from the International Monetary Fund (Svirydzenka, 2016), which reflects the financial sector’s capacity to support multiple initiatives, including SRI founding. This measure, which is independent from ideological considerations about financial or social logics, aggregates private-sector credit to GDP, pension fund assets, mutual fund assets, and insurance premiums in the national economy. We also constructed a measure termed materialism to serve as a proxy for the ends that are legitimate in the financial logic. This measure, which is independent from other means-related considerations related to the financial logic, was based on aggregated data from the World Values Survey and was constructed from a survey question about whether society should place more or less “emphasis on money and material possessions.” We used linear interpolation to fill in the missing variables. The World Values Survey is conducted every five years and has broad international coverage.

Moderators

Unions

We measured union density as the percentage of employees who are unionized in a country. We obtained this measure from the OECD, which calculated the value using survey and administrative data adjusted for non-active and self-employed members. As most countries in the sample are developed ones, the union density averaged more than 38 percent. Yet the variation of union density is high, with a standard deviation higher than 20 percent, reflecting the varying strengths of unions across countries.

Religion

We used the logged number of Christians in the population as a measure of the religious logic for three primary reasons. First, Christian churches “played a pioneering role in the development of SRI globally,” even in countries in which it was a minority religion (Sparkes, 2006: 43). A long sociological tradition has established the relevance of Christianity, especially in its Protestant denomination (Weber, 1976), in the global financial domain (Meyer et al., 1997; La Porta et al., 1998; Weber et al., 2009). Second, all countries in our sample except Japan have a Christian majority. On average, 81.9 percent of the population identified themselves as Christians. And third, there is no evidence that other religions have played an important role in the domain of SRI, according to existing reviews of SRI history (Sparkes, 2003, 2006). Data for this variable came from the Association of Religion Data Archives (Maoz and Henderson, 2013). 9

State

We used the share of seats in parliament held by green parties as a measure of the extent to which the state is geared toward environmental causes. A country might have one or more green parties, so we aggregated all the green seats. We used the share of seats in a given parliament instead of the vote share to indicate the power of the green parties. This measure was taken from the Comparative Political Dataset (Armingeon et al., 2016).

Control Variables

Based on prior cross-national studies of the fund management industry and financial markets in general (Khorana, Servaes, and Tufano, 2005; Weber, Davis, and Lounsbury, 2009), we included the following control variables that may influence SRI founding: GDP per capita (one-year lag and logged), population (one-year lag and logged), trade openness (one-year lag), trade cohesion (one-year lag), years of formal education in the country (one-year lag), foreign direct investment over GDP (one-year lag), and the prior year’s founding number of SRI funds.

GDP per capita is a measure of general wealth, which is expected to show the personal income available for consumer fund products. Population captures the size of the market. We controlled for the sum of years of primary and secondary education at the national level, as prior studies have suggested that education influences the extent of business involvement in social causes (Ioannou and Serafeim, 2012). We also controlled for the founding of SRI funds in the prior year to account for other potential legitimation and competition effects (Freeman, Carroll, and Hannan, 1983; Carroll and Hannan, 1989). It is also likely to absorb much of the unobserved heterogeneity that can confound our results because this lagged dependent variable can be interpreted as a summary measure reflecting the effects of all past factors that may influence the founding of SRI funds. We also assessed whether our finding was sensitive to alternative specifications of density dependence; we ran separate regressions to include linear and squared terms of SRI density—the existing number of SRI funds—in the models and obtained substantially similar results.

Additionally, we controlled for the size of foreign direct investment (FDI) over GDP to account for the influence of multinational corporations, and trade openness and trade cohesion to account for the fact that SRI may spread as a consequence of a focal country being influenced by trade-partner countries that already have SRI establishments. Trade openness, a measure of integration in the global financial systems (Weber, Davis, and Lounsbury, 2009), is expected to positively influence the rise of SRI funds, as economically open countries are more likely to invest in novel economic activities (Weber, Davis, and Lounsbury, 2009; Scholtens and Sievänen, 2012). As for trade cohesion, we adapted the measure from prior studies (Guler, Guillén, and Macpherson, 2002; Polillo and Guillén, 2005) as follows:

where SRI is the existing number of SRI funds for country j at time t–1, Tradeijt–1 is the total trade between country i and country j during year t–1, and Tradeit–1 is country i’s total trade during the same period.

We also considered control variables on civil society actors, as well as alternative diffusion mechanisms, such as economic globalization and financial openness, because prior studies have identified them as relevant in predicting the founding of new organizations and corporate social responsibility (Ioannou and Serafeim, 2012; Lim and Tsutsui, 2012). We examined the extent to which civil society is powerful in the country (Marquis, Toffel, and Zhou, 2016) and the extent to which the country has links to international NGOs (Lim and Tsutsui, 2012; Smith and Wiest, 2012). We also examined the economic globalization index and the KA financial openness index (Marquis, Toffel, and Zhou, 2016). The main results remained consistent after controlling for these alternative influences. We decided not to include them in the main models because doing so would remove a large part of the overall sample.

Statistical Model

Following prior studies on founding rates (Carroll and Swaminathan, 2000; Stuart and Sorenson, 2003; Hiatt, Sine, and Tolbert, 2009), we applied the conditional fixed-effects negative binomial estimators at the country level (Hausman, Hall, and Griliches, 1984) to most models, because this was more appropriate with overdispersed count data and was helpful to account for static national characteristics, such as legal traditions, culture, and world-system position (Guillén and Capron, 2016). As a robustness check, we used a Poisson model with fixed effects, which did not change the main results. We also tested with random effects, and the results remained consistent. Year dummies were included in all models to account for yearly macro conditions that could confound the findings. As the conditional fixed effects estimated the distribution of founding conditional on the total number of events observed, Stata automatically dropped countries that had only one observation and that had no variation within.

Results

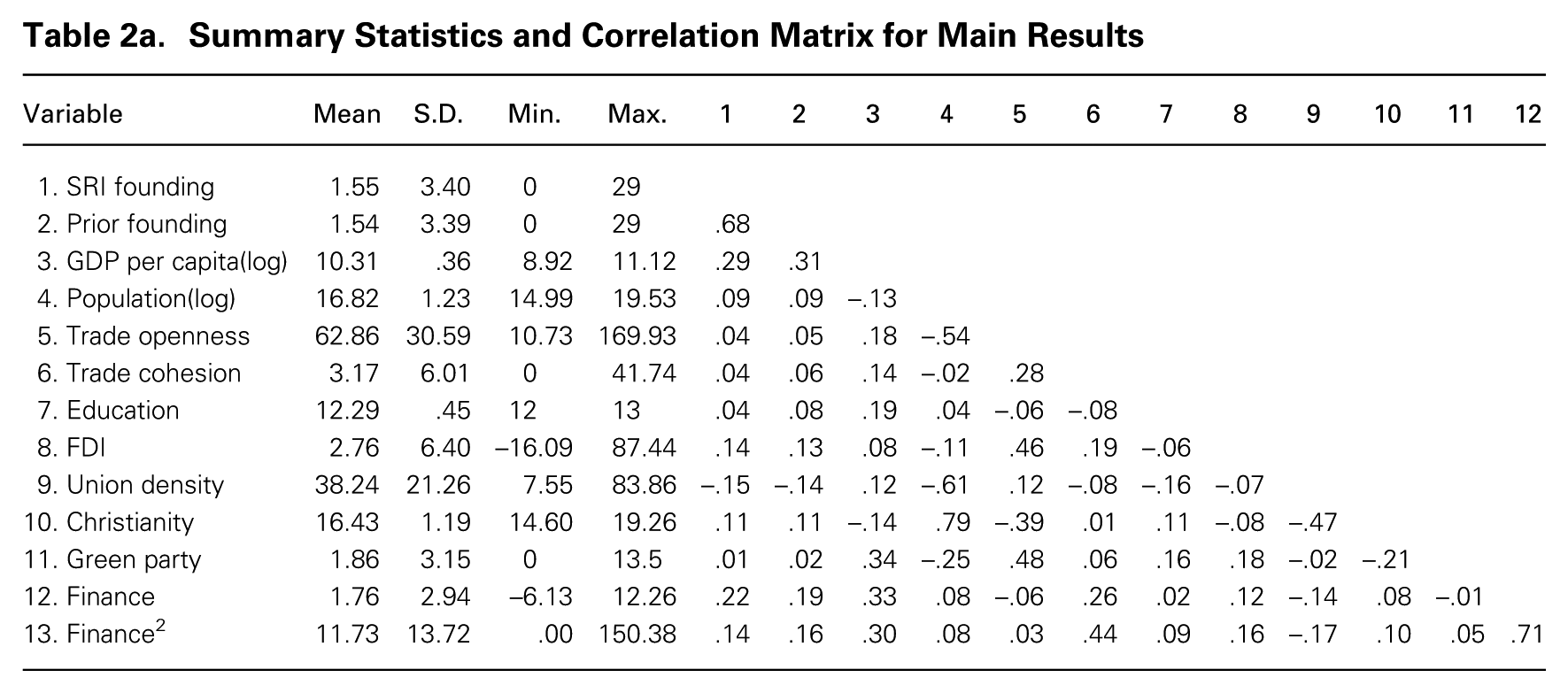

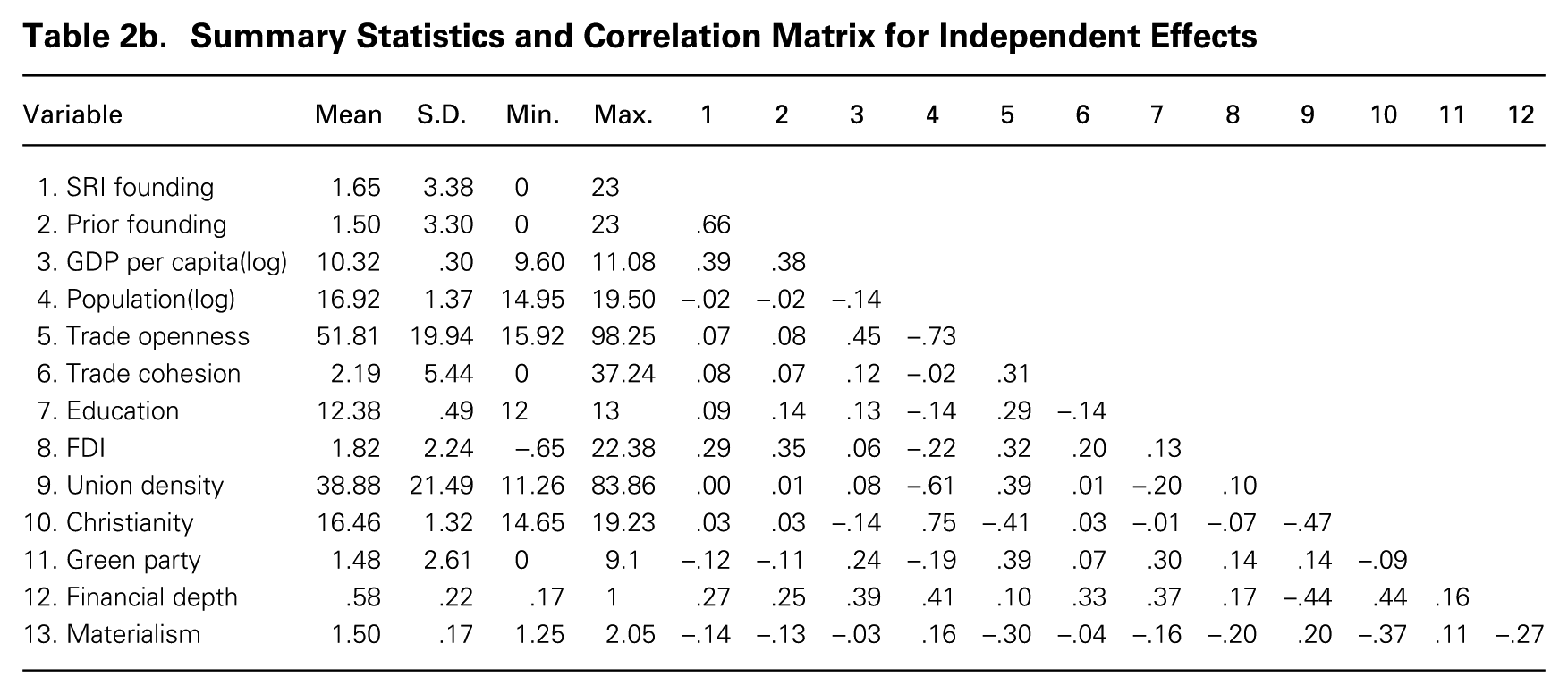

Tables 2a and 2b show the summary statistics and correlation matrix for the two tests of the relationship between the financial logic and the rise of SRI, one based on the measure of the financial logic using the proportion of employment in FIRE and the other based on proxies of the two paradoxical effects of the financial logic as a provider of means and as an enforcer of ends. We calculated variance inflation factor scores for all independent and control variables with Stata’s Collin command, and all values were below the threshold of 10, suggesting that multicollinearity should not be a big concern.

Summary Statistics and Correlation Matrix for Main Results

Summary Statistics and Correlation Matrix for Independent Effects

The prevalence of the financial logic varied across countries and time, as shown in figure 1. In some countries, financial employment prevalence was as low as .23 percent, but in other countries it ran as high as 18.62 percent. It is important to note that a 1-percent change in the prevalence of finance in a society is potentially very significant. Even excluding China and India, since 1990 the countries in our sample have averaged a workforce totaling more than 70 million. Hence, a one-unit change in financial logic prevalence might indicate an average increase in the finance workforce of up to a million workers.

Main Results

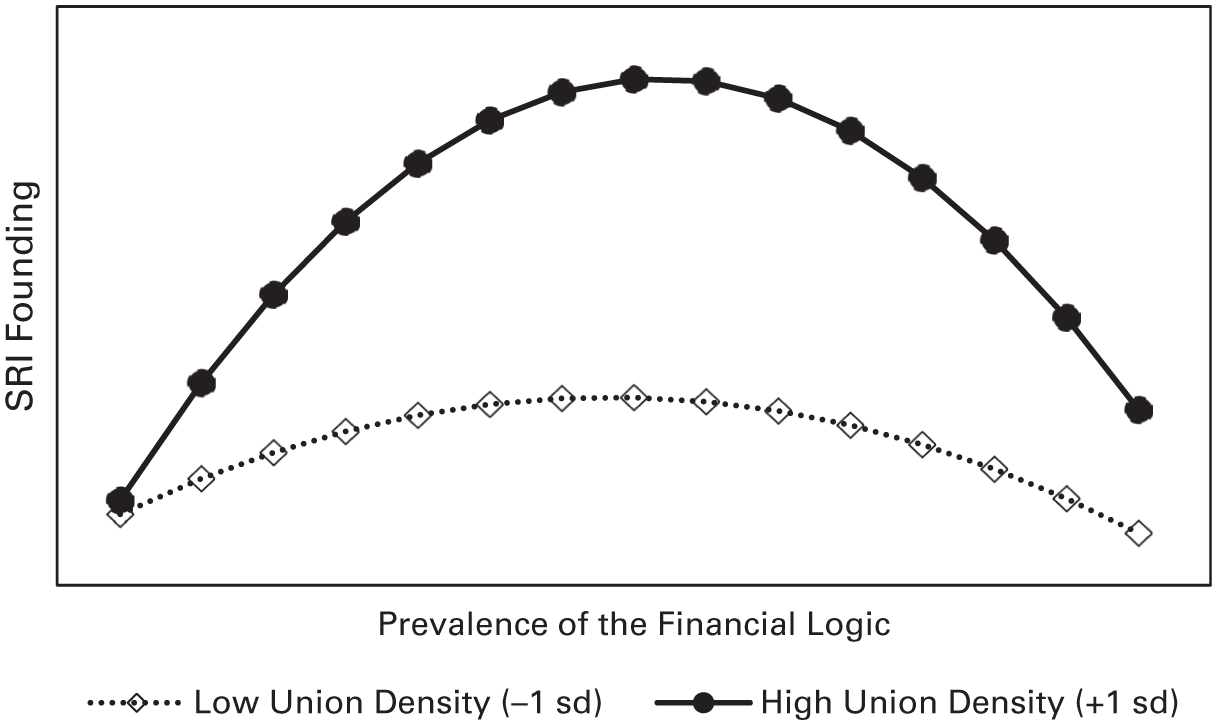

Table 3 illustrates the results from the analysis of the paradoxical effects of the financial logic, as measured by the proportion of national employment in the FIRE industries. In model 1, only control variables were included. Prior founding of SRI funds strongly predicts current SRI founding, possibly indicating legitimation effects from the existence of other SRI funds. GDP per capita was positive and significant in all models, indicating that a wealthier population was more likely to have a higher founding number of SRI funds. Trade openness and trade cohesion show positive and significant effects from models 1 to 4, consistent with prior studies on SRI founding (Scholtens and Sievänen, 2012) and the diffusion of novel practices (Guler, Guillén, and Macpherson, 2002; Polillo and Guillén, 2005). Years of education have significant and negative effects on SRI founding, which might be interpreted as SRI entrepreneurs being more motivated to provide SRI funds as a finance-based solution to social problems arising from societies lacking strong educational systems (Ioannou and Serafeim, 2012). Foreign direct investment (FDI) over GDP is positive and significant in most models, indicating multinational corporations’ strong influence in the rise of SRI internationally.

Paradoxical Effects of the Financial Logic on SRI Founding*

p < .10; • p < .05; •• p < .01; ••• p < .001.

N = 670 in 19 countries; country fixed effects and year dummies are included in all models; t statistics are in parentheses.

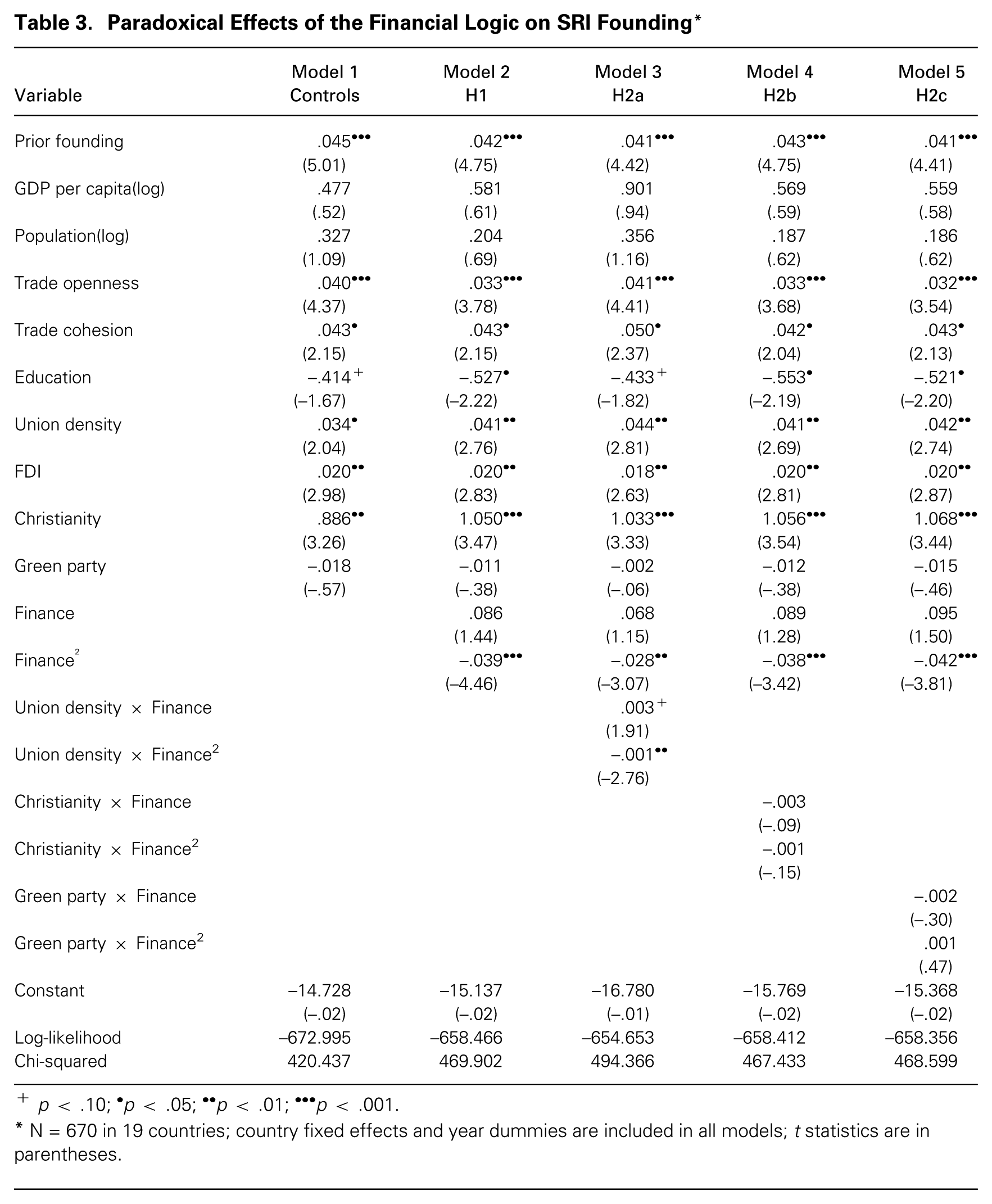

In model 2, we find support for H1, which proposed the curvilinear, inverted-U-shaped effect of the financial logic on SRI founding; figure 2 is a graphic representation of the effect. A visual inspection of figure 2 suggests that the curve is not fully symmetric, as there are some countries with a high prevalence of the financial logic with some incidence of SRI founding. The turning point, or the SRI founding peak, occurs when the prevalence of the financial logic reaches 1.11. Because the variable has been centered, the real non-centered level of the SRI founding peak is when employment in FIRE industries is at 9.23 percent of total employment. After that point, our theory proposes that the positive impact of finance as a provider of means is overtaken by finance as a source of legitimate ends. Though not every country may have reached a peak in SRI foundings, the results suggest a general pattern that as the financial logic becomes more prevalent, the constraining influence of the financial logic is stronger than its enabling role.

Predicted curvilinear effects of the financial logic on SRI founding.

To further check the existence of an inverted-U-shaped relationship (Haans, Pieters, and He, 2015), we used the Lind and Mehlum (2010) method to check the inverted U by using their utest code in Stata. The overall inverted-U test has a t-value of 3.65, and the p value is .00014, which is highly significant. As another robustness check, we tested whether the relationship might be S-shaped by including a cubic term of the financial prevalence, but we did not find any significant result for that coefficient, while the rest of the coefficients remained substantially similar. To dispel the concern that the results were driven by outliers, we winsorized all control and independent variables at the .5-percent level (top and bottom) and obtained similar results. We also ran separate regressions excluding different combinations of countries with the highest cumulative SRI founding numbers (France, Norway, Belgium, and the UK) and obtained similar results. Another potential concern arises from the possibility that the result is a mere statistical artifact (Becker, 2005; Carlson and Wu, 2011; Spector and Brannick, 2011) driven by the choice of control variables. We ran a robustness check in which all controls were removed except for the fixed effect on year and country and obtained substantially the same results. We ran additional robustness checks, such as taking additional lags in the independent variable (two-year, three-year, four-year, and five-year), and found similar patterns. The squared term of financial prevalence was consistently significant in these alternative specifications.

Although we found strong support for H1, there were outliers that behaved differently from the inverted-U-shaped relationship, and they are worth examining more closely. Belgium in the 2010s had a relatively high number of SRI foundings (more than 10) but also had a low level of financial logic prevalence. The high level of union density might help explain this anomaly. Norway in the 2000s experienced a high number of SRI foundings despite a high level of financial logic prevalence, but state forces in favor of SRI and the later adoption of SRI in its sovereign wealth fund might explain this phenomenon. Australia in the 1970s did not experience high SRI founding events, although the prevalence of the financial logic was moderate, which may be because it was undergoing an economic recession.

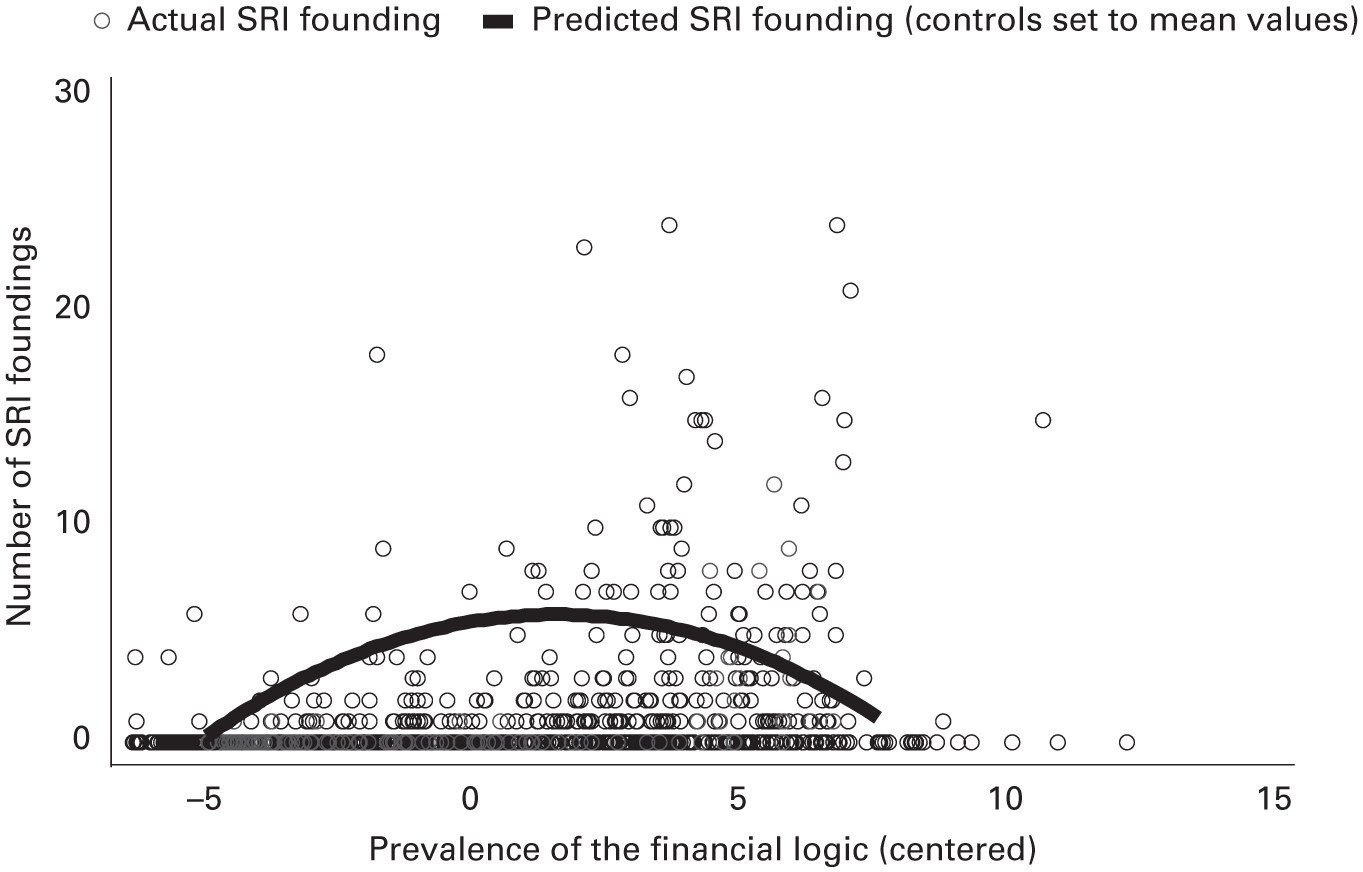

As for moderation effects, H2a receives some support from model 3; see figure 3 for a graphic illustration. The interaction term of union density with the quadratic term of the prevalence of the financial logic is negative and significant. Because the curve is an inverted-U shape, the negative coefficient confirms that union density steepens the curve. 10 As our empirical model is a conditional negative binomial model and testing for moderations in these models is not straightforward (Haans, Pieters and He, 2015), we conducted a further analysis to confirm this finding. As different shapes of curves correspond to the different values of the moderating variable (i.e., union density), we picked union density at two values—one standard deviation above and below the mean—to obtain the respective curves of SRI founding, reflecting the relationship between the prevalence of the financial logic and the rise of SRI. From those two curves, we calculated their peak points, chose one standard deviation away from these peak points, and calculated differences in the slopes between the curves with the lincom command in Stata. The test indicates that at both points (mean − 1 s.d. and mean + 1 s.d.), the differences in slopes are significantly different (coefficient = –.11, p-value = .063). Thus there is some evidence to suggest that at higher levels of union density, the curvilinear relationship between financial prevalence and the founding of SRI steepens.

Effects of union density on SRI founding.

In model 4, H2b was not supported. This suggests perhaps that religious ends do not have an effect in the context of material means or ends supplied by the financial logic, which may operate in a completely independent sphere. We started with the assumption that the ends of the religious logic may be complementary with those of the social logic and competing with those of the financial logic. The interpretation of this nonsignificant effect may be that the religious logic is compartmentalized and applies to social domains that are independent of the social and financial logics relevant to SRI. As models 1–5 suggest, the prevalence of Christianity does have a positive independent effect on the rise of SRI, but it does not moderate the relationship of the prevalence of the financial logic with the rise of SRI. In model 5, H2c was not supported, as the coefficient of the squared interaction term is statistically insignificant. Results from models 1 to 5 also show that green parties do not directly influence the rise of SRI funds. The analysis below based on the separate measures of means and ends of the financial logic helps explain the reasons we do not find a moderating effect in these two hypotheses.

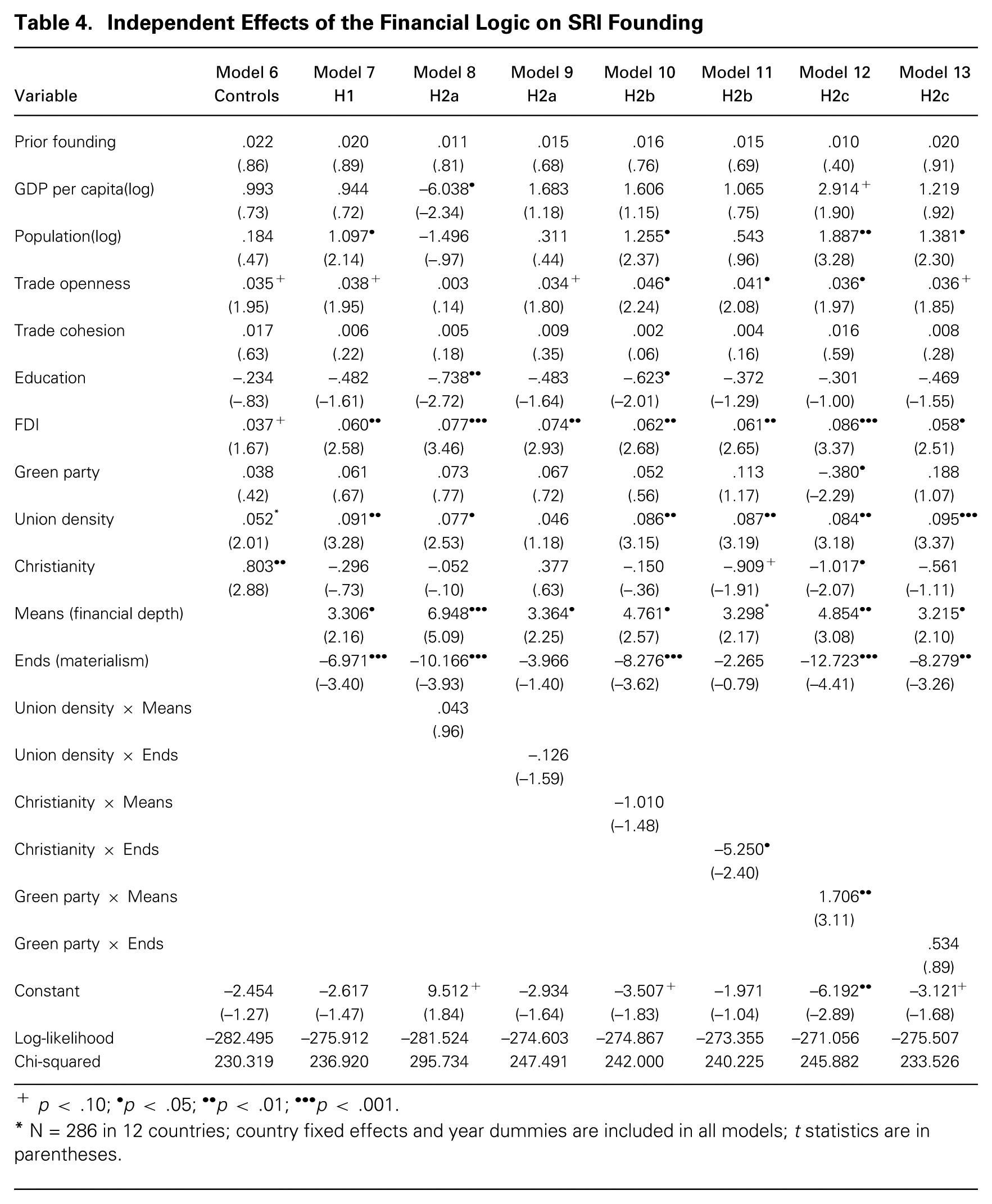

Results of the Means/Ends Analysis

Table 4 illustrates the results of the analysis in which we directly measured means as “financial institution depth” and ends as “materialism.” We present results with all predictor variables mean centered to obtain more consistent estimates, although using original values produces substantially similar results. In model 6, only control variables were included. Model 7, which includes both financial institution depth and materialism, shows that both effects are significant. The results—that financial institution depth has a positive relationship with the rise of SRI, while materialism has a negative relationship—support indirectly both the enabling and constraining effects of the financial logic in the rise of SRI, which are the joint mechanisms behind H1.

Independent Effects of the Financial Logic on SRI Founding

p < .10; • p < .05; •• p < .01; ••• p < .001.

N = 286 in 12 countries; country fixed effects and year dummies are included in all models; t statistics are in parentheses.

Results from models 8 and 9 do not provide support for H2a, although the signs of the moderation terms with the prevalence of unions are consistent with our theory. In fully saturated models, which we report in Online Appendix B (http://journals.sagepub.com/doi/suppl/10.1177/0001839218773324), we include all interactions and find evidence that unions compete with the financial logic. The lack of support here could be explained by the proxies’ inability to fully capture the means (financial depth) and ends (materialism) dimensions of the financial logic the way we understand them in this paper. Although those variables include important dimensions of the means and ends, they leave out other relevant aspects in the context of unions. Financial depth, which refers to a nation’s capacity to support multiple initiatives, is broader than the capacity to support social initiatives, especially SRI, which would be most relevant in this context. It also misses the specific human capital component captured by the FIRE industries. Similarly, materialism as a measure of the ends of the financial logic is a society-level variable going beyond the financial sector, which is the domain in which the interaction between the prevalence of unions and the ends of the financial logic would be most relevant.

Results from model 10 also suggest that the prevalence of Christianity did not moderate the relationship between means provided by the financial logic and the rise of SRI, which may help explain why the moderation effect in the prior analysis (table 4) did not appear. The explanation above about the religious logic being compartmentalized from domains relevant to the financial logic may be relevant here. As a compartmentalized logic, it may not interact favorably with the means provided by the financial logic. Additionally, a population-level measure of Christianity as the number of believers in a country does not capture religious actors’ capacity to mobilize in the same way as with unions or green political parties, which would be relevant to the interaction of the religious logic with the means of the financial logic.

The interaction effect between Christianity and materialism on the rise of SRI was negative and significant in model 11, however, thus supporting one of the mechanisms behind H2b: that the ends of the religious logic would conflict with the materialism of the financial logic and thus create an environment in which the integration of social and financial logics would be more difficult in SRI founding.

Results from models 12 and 13 suggest that the strength of green parties positively moderates the relationship between the means provided by the financial logic and the emergence of SRI. Contrary to the measure of the religious population, the strength of green parties captures an organizational element that can positively engage with the means of the financial logic in a way that may result in more SRI founding. But that same variable does not negatively moderate the relationship of the ends of the financial logic (proxied by the materialism variable) and the emergence of SRI. This could mean that the end goals of environmental sustainability are not necessarily in conflict with the ends of the financial logic.

We started with three alternative logics that were a priori competing with the ends of the financial logic and complementary with those of the social logic. The extent to which the end goals of those alternative logics are “distant” from that of the financial logic might explain these inconclusive results. We could consider the compatibility across the ends of different logics in terms of relative distance between them. In our context, a comparison between the ends of the logics we consider would suggest that the distance between the financial and green logics is shorter than the one between financial and religious logics. Fostering ecological sustainability and more environmentally friendly practices (the ends of the green logic) may be more compatible with the ends of the financial logic, as the relationship between sound environmental practices and long-term profitability has been well established (Eccles, Ioannou, and Serafeim, 2014). In contrast, the ends of religious logics might be more difficult to harmonize with the financial logic.

Discussion

Our study explored how decomposing the dominant financial logic into its roles as both the provider of financial means and as a constraint on legitimate ends accounts for its paradoxical influence in promoting change and maintaining stability in the financial sector. This decomposition can further our understanding of how different logics interact in competitive and complementary ways and how the prevalence of the dominant logic in society affects such interactions. Additional institutional logics in the broader society may interact synergistically with a dominant institutional logic to promote institutional change by supplying fresh motivations (or end goals) that could benefit from institutionally bound means and expertise. When the dominant institutional logic has clearly specified legitimate institutional ends appropriate for a specific sector, however, the clash of those additional logics with the competing ends of the dominant institutional logic may highlight the contrast and harden the static or inertial nature of the dominant logic, thus stifling institutional change.

Contributions to Institutional Theory

We contribute to research on institutional complexity and the emergence of hybrid organizations, institutional logics, and institutional change. Our theory contributes to research on institutional complexity (Kraatz and Block, 2008; Greenwood et al., 2011) by providing a new explanation of the circumstances under which a constellation of institutional logics may be conflicting (e.g., Thornton and Ocasio, 1999) or complementary (e.g., Smets et al., 2015). Recent studies such as that by Lee and Lounsbury (2015) have offered insights on how a dominant logic amplifies or dampens the influence of other institutional logics, yet few have examined the factors determining the shifting complementarity of the dominant logic with other logics in society. Hence there is inadequate research to show in a holistic way that institutional logics are “mutually dependent, yet also contradictory” (Friedland and Alford, 1991: 250).

To clarify the complex relationships among multiple institutional logics, our study suggests that when the end goals of a dominant logic are taken for granted and the coupling between means and ends is tight, alternative logics are more likely to compete with the dominant logic, and hence alternative forms of organizations that may drive institutional change may be subject to stronger isomorphic pressures (DiMaggio and Powell, 1983). When the dominant logic plays the role of provider of means, however, opportunities for institutional work may emerge (Lawrence and Suddaby, 2006; Hardy and Maguire, 2008), and multiple logics are likely to be complementary. All this obviously has consequences for the emergence of hybrid organizations, which incorporate alternative logics that may be either complementary or competing with the dominant logic depending on factors such as the prevalence of that dominant logic in society. Based on our analyses, the emergence of hybrid organizations may be more likely at moderate levels of prevalence than at low or high levels.

Our study also contributes to the institutional logics literature by proposing a more nuanced decomposition of the dominant logic into means and ends and by suggesting that the complementarity between the dominant logic and alternative ones depends on the prevalence of the former. Given that logics are global constructs—ideal types in which multiple elements are confounded—it is not easy to decompose them into meaningful and discrete dimensions. But this particular decomposition of means and ends seems to be especially relevant at the theoretical level, and our analyses show that it has measurable empirical effects. Our decomposition differs from those in prior studies in that we not only demarcate different dimensions of the same logic (cf. Meyer and Hollerer, 2016) but also explain how those dimensions are interdependent and interact. Much prior research has differentiated logics in a variety of ways, such as by geographic separation (Lounsbury, 2007), historical periods (Thornton and Ocasio, 1999), or societal orders (Zhao and Wry, 2016), but institutional logics are usually treated as monolithic entities that generally do not have internal differentiations. By theorizing the interdependent means–ends effects of the dominant logic, our study suggests that novel forms of organizations may arise from internal ruptures in that logic, as alternative competing logics redeploy the means provided by the dominant logic.

Our decomposition of the financial logic is potentially applicable to a variety of other logics and settings. In the context of finance, our findings are relevant to situations in which finance encounters goals that diverge from profit maximization. For example, China launched stock exchanges in 1990 with the goals of building the state and achieving state policy objectives (Hertz, 1996, 1998), rather than the goal of developing shareholder capitalism. Our findings are also relevant to other dominant logics in some settings, such as the state (Friedland and Alford, 1991; Thornton, Ocasio, and Lounsbury, 2012). The state may have its own constraining ideology that stifles institutional change but also provides resources that can enable ventures driven by ends that compete with that ideology. Peter Kinder, one of the founders of KLD, a pioneering SRI firm, saw his work through the lens of his legal training and his public service experience: “I suddenly realized what I was seeing, and what I was seeing was politics by other means. It was just another way of using the tools that I had learned in law school and state government, just in a different form. But the tools are identical” (personal interview, 8/17/08). Another field in which this dynamic is important is education, as charter schools driven by community or religious logics can receive government funding to operate independently from, and even compete with, the public school system (e.g., King, Clemens, and Fry, 2010). Future research should explore more empirical settings to understand the implications of decomposing a dominant logic into means and ends.

Finally, our study contributes to research on institutional change, which in this case may be prompted by the emergence of new hybrid organizations (Micelotta, Lounsbury, and Greenwood, 2017). We suggest that even within firmly established institutional orders there are seeds of change that can be activated under certain conditions, departing from prior literature that posits fragmentation and complexity of the field as primary contributors for change and agency (Oliver, 1991; Battilana, Leca, and Boxenbaum, 2009). Our results show that not all societies reach the critical point at which the dominant logic suppresses institutional change, and even when that happens, institutional change is not completely driven out, as the expertise and other resources provided by a dominant institutional logic may still be seeding institutional change. Thus institutional change may happen as the dominant logic broadens the scope of its legitimate institutional ends or as it combines with other institutional logics that supply alternative ends. The presence of competing logics is more likely to lead to institutional change when the dominant institutional logic can supply sufficient expertise and other portable means necessary to build new organizations. Our results also suggest that not all competing logics will likely benefit from the expertise provided by a dominant logic—we did not find that religion interacted with the means provided by the financial logic in the way we anticipated. Future research could explore the boundary conditions that determine whether a dominant logic as a provider of means can support the ends of competing logics.

Contribution to Socially Responsible Investing

Our paper also contributes to a better understanding of the country-level institutional factors that foster SRI founding. Given the relatively short history of SRI and the scarcity of data, it is not surprising that previous studies have focused on the evolution of the sector in one country (e.g., Arjaliès, 2010; Giamporcaro and Gond, 2016) or compared only a few cases (e.g., Scholtens and Sievänen, 2012; Gond and Boxenbaum, 2013; Yan and Ferraro, 2016). We learned much from these studies on the evolution of SRI in specific countries, but it was difficult to integrate these idiosyncratic narratives in a more systematic theory of how SRI is developing globally. Building on the institutional logic literature, our theory provides a coherent framework to explain the global spread of SRI, and our empirical findings show the important role played by the financial logic and its interaction with the presence of labor unions, religion, and green parties.

Our paper also extends current literature on SRI by reconciling prior insights with new findings. Prior literature has suggested the spread of finance is a sweeping force in the global economy (Epstein, 2005; Davis and Kim, 2015) and proposed constraining effects on the rise of hybrid organizations in the financial sector (Jonsson, 2009; Jonsson and Regnér, 2009), such as SRI funds. Our findings are consistent with prior literature when the ends of the financial logic take primacy but diverge from it when the means of the financial logic are playing a stronger role to serve alternative ends. This more nuanced view suggests that as countries become more integrated into the global society (Meyer et al., 1997), the increasingly prevalent financial logic plays a more complex role than is commonly understood.

Further research should explore how, in other settings, the emergence of novel hybrid organizations benefits from the means provided by established or dominant logics, even though their ends might be competing. It might be particularly useful to examine micro-level processes by which entrepreneurs succeed or fail to make use of means from dominant logics for alternative ends. It is also important for future research to shed light on the effects of distances among the end goals of multiple institutional logics.

Limitations

In cross-national studies (Lim and Tsutsui, 2012), it is difficult to compile consistent and reliable data. Although our data are comparable with prior studies on similar topics (Khorana, Servaes, and Tufano, 2005; Weber, Davis, and Lounsbury, 2009; Lim and Tsutsui, 2012; Guillén and Capron, 2016), we encourage future researchers to develop and make available more fine-grained data at the cross-national level. The choice to separate the relevant institutional spaces by national boundaries is also open to criticism, especially in the field of finance, which has experienced rapid globalization—although our observation window includes periods when the field was less globalized. Perhaps other research could compare other meaningful geographical differentiations, even though it is difficult to conceive of alternative data configurations.

Our study uses employment distribution in the FIRE industry sectors as a proxy for the prevalence of the financial logic in a country. Though research in economics (Clark, 1940; Bell, 1973), sociology (Castells, 1996), and micro-level organizational theory (Almandoz, 2012, 2014) has used individual employment trajectories in similar ways, and there is research suggesting that economics and finance training does affect individuals’ behavior, we are aware of the limitations of that measure. To remedy this deficiency, we conducted an additional analysis with two separate measures for means and ends, and we found largely consistent results. In addition, we used the number of all funds per country-year as an alternative proxy for both the means and ends of the financial logic in a robustness check and obtained consistent results.

Conclusion

We developed our institutional logics theory—especially the distinction between means and ends in the financial logic—to understand the emergence of SRI, but this approach could prove useful in understanding the broader process of institutional change that the financial sector is undergoing after the 2008 financial crisis. In addition to SRI funds, a number of organizational innovations have emerged, such as micro finance and other forms of community lending. Only time will tell whether the process of redeploying the means of the financial logics to different ends will ultimately create a financial sector more aligned with societal needs, but we believe that institutional theory could contribute to this shift by offering managers and policy makers an alternative framework to assess the progress the sector is making in this journey.

Supplemental Material