Abstract

In this study, we argue that parents’ class position may influence the type and timing of their offspring's investments in financial assets. These investments may facilitate net worth accumulation beyond direct transfers, contributing to the intergenerational reproduction of social positions. We test these expectations using retrospective life history and prospective panel data for 14 countries from the Survey of Health, Ageing and Retirement in Europe. We apply discrete-time event history analyses to examine the first financial investments’ timing over the life course and conduct a mediation analysis of net worth. We find that individuals from advantaged parental classes are more likely to invest in stocks and mutual funds. When considering horizontal differentiation, managerial classes with relatively more economic capital than cultural capital are more likely to invest in financial assets. However, we do not find robust evidence for distinct timings of financial investments by parental class. Advantaged parental class is positively associated with net worth in later life. However, this association cannot be explained by the specific investments of individuals from advantaged parental classes.

Introduction

How advantaged parents transfer their social positions to their children remains a central question in sociology. Research in social mobility and status attainment typically focuses on the intergenerational transmission of education and occupation. However, given the increasing level of wealth inequalities in recent decades (Piketty, 2014), the role of wealth in the intergenerational transmission of advantage has received increasing attention (Hällsten and Pfeffer, 2017). Wealth is an essential factor in the intergenerational transmission of advantages because of the overall rise in wealth compared to income (Piketty, 2014) and the specific mechanisms of wealth transmissions. While wealth transmission and accumulation are closely coupled to education and occupation, they also exceed the meritocratic logic of status attainment via education and occupational placement that typically is at the core focus of sociological mobility research. Wealth is partly directly transmitted across generations through gifts and transfers (Killewald et al., 2017). In addition, in this study, we argue that the wealth-related transmission of advantage may also work through parental influence on the financial investment in the offspring generation beyond direct transfers. This argument is in line with other recent sociological efforts to unveil the indirect reproduction of wealth across generations (e.g., Hansen and Toft, 2021).

If and when people invest in which type of financial assets considerably influences people's wealth accumulation over the life course (Bach et al., 2020; Chang, 2005; Keister, 2005, p. 239). In particular, investments in stocks are associated with higher returns in the long run, on average. For instance, between 1926 and 2017, stocks had an average annual return of 10.3% with losses in 25 out of 92 years in the United States, while at the same time bonds, as a more secure investment, had an average annual return of 5.4% with losses in 14 out of 92 years (The Vanguard Group, 2018; see also Jordà et al., 2019 for comparison to housing investments). Thus, individuals with early investments in more profitable but risky assets such as stocks may be more likely to reach or maintain advantaged social positions over time than otherwise similar individuals with later and less profitable investments.

We argue that parents’ class may influence their offsprings' financial investments beyond the direct transmission of wealth and beyond the offspring's social position (Hansen and Toft, 2021). We define class based on labor market positions. We build on Oesch's (2006) class concept in which positions in the labor market are vertically differentiated by employment relationships (dependent on marketable skills of workers) and horizontally divided by work logics (technical, organizational, and interpersonal) which relates to differences in daily work experience. We argue that individuals from vertically advanced social origins may be more inclined to use financial investments to maintain their social positions.

Moreover, individuals from managerial classes are argued to be more likely to invest in risky but profitable financial investments, whereas socio-cultural professionals may be more prone to secure investments such as pension funds and life insurance. By investing in risky assets in addition to other investments such as homeownership, managerial classes are also likely to diversify their wealth portfolio (Hansen and Toft 2021; Waitkus and Groh-Samberg, 2019). In interaction with environmental conditions such as financial market performance, these investment strategies will substantially shape wealth attainment for the offspring generation. They may result in higher net worth over the life course. Preliminary evidence supports the idea that social origin influences the composition of the wealth portfolio (Charles and Hurst, 2003; Chiteji and Stafford, 1999; Lersch and Luijkx, 2015), but knowledge about the influence of parental class remains sketchy. Recent research on the origin-class wealth gap focussed on the gap in net (and gross) worth and did not examine specific investment strategies (Hansen and Toft, 2021).

To address this gap in the literature, we ask three related questions: (1) Does parental class influence the occurrence of investments in risky financial assets such as stocks? (2) Does parental class influence the timing of these investments? (3) Do individuals from advantaged parental classes accumulate more net worth because of their investment strategies? To answer these questions, we use retrospective life history data combined with prospective panel data for 14 countries from the Survey of Health, Ageing and Retirement in Europe (SHARE). These data are unique in providing retrospective information about the timing of financial investments over the life course in combination with parental background characteristics and net worth in later life. We examine these data using discrete-time event history analysis of the timing of investments, OLS regression of net worth, and mediation analysis of net worth.

Previous research

A large body of literature finds substantial inequality in the ownership of financial assets (e.g., Bertaut and Starr-McCluer, 2002). Foremost, a large share of the population has no wealth (Killewald et al., 2017). Among those with wealth, the share held in financial assets varies widely. In 13 European countries that participate in the SHARELIFE survey only about 60% of men and 47% of women ever invested in any of the following assets: stocks (ever invested by 24%), mutual funds (22%), life insurance (31%), and private retirement plans (26%) (Cavapozzi et al., 2011). Investment rates are exceptionally high in Sweden and Denmark and the lowest in Greece. Stocks and other risky financial assets are more often held among the more affluent, while saving accounts and homeownership are more widespread in the population (Keister, 2005, p. 70ff; Spilerman, 2000). In addition, owning risky assets is strongly positively correlated with higher education (Keister, 2000). Stock ownership and other aspects of portfolio composition are also positively correlated across generations within families (Charles and Hurst, 2003; Chiteji and Stafford, 1999). While not the focus of our study, there is also mature literature on intergenerational links for homeownership (e.g., Lersch and Luijkx, 2015).

More specifically and close to our study, Cavapozzi et al. (2013) investigate the event of first-time investments in stocks and mutual funds over the life course controlling for previous investment in life insurance with the SHARELIFE data. Concerning social origin, the authors find that the hazard of investing in stocks or mutual funds increases for individuals where the primary breadwinner in the household at age 10 was a professional or white-collar worker compared to households with blue-collar workers. This relationship remains significant, controlling for individuals’ lifetime incomes, their mathematical skills at age 10, homeownership status of the family at age 10, and a wide range of other control variables. Having fewer books in the household at age 10 is associated with lower hazards of investing in stocks or mutual funds.

Theory

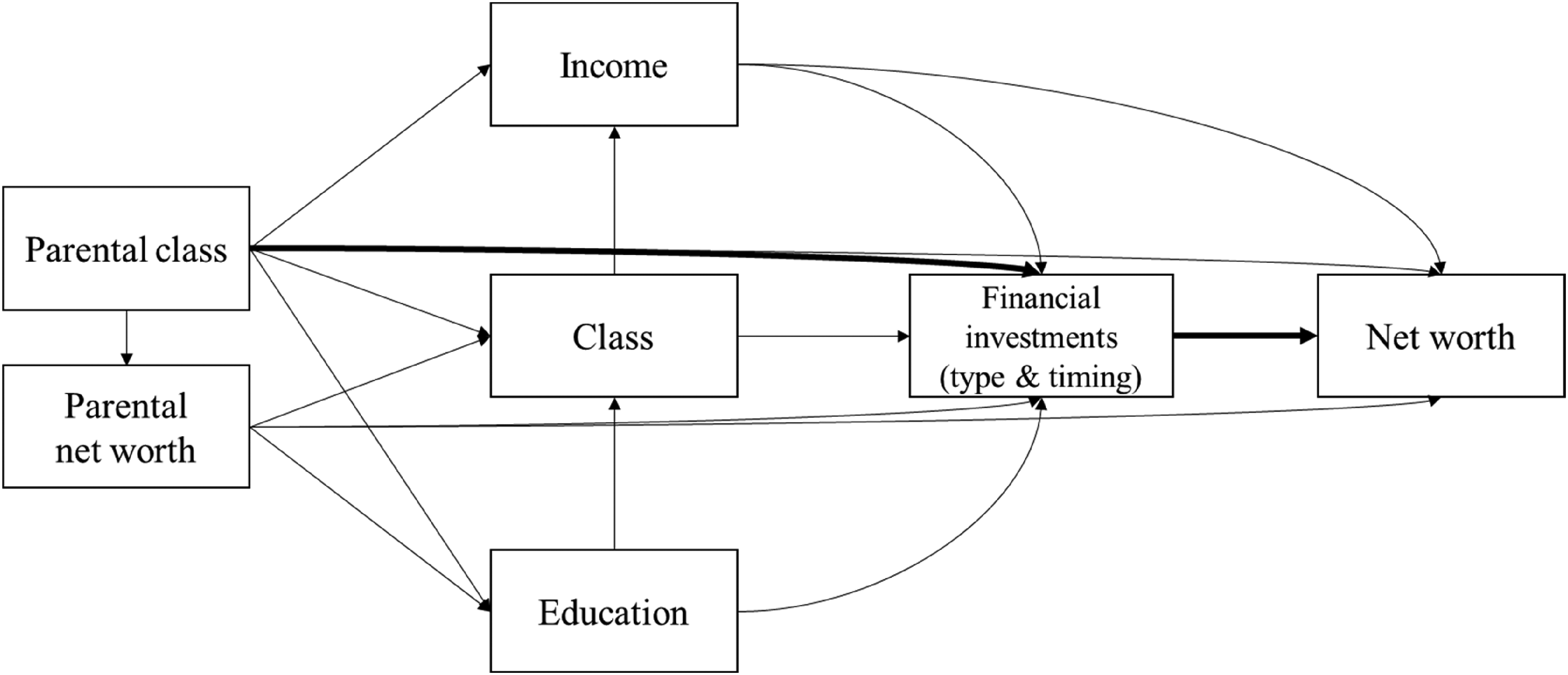

The social origin may be relevant for financial investments and net worth in the offspring generation in multiple ways, as depicted in Figure 1. In the current study, we focus on the effect of parental class on financial investments in assets such as stocks and mutual funds net of parental wealth and children's class position, education, and income. Yet, we acknowledge that social origin may also affect wealth attainment through the intergenerational transmission of class positions (and education and income) from parents (Charles and Hurst, 2003).

Hypothesized causal relationships between parental class, financial investments in offspring generation and net worth.

Class origin and financial investment decision making

Why may social origin matter for the type of financial investments and their timing? We assume that individuals consider subjectively expected costs and benefits in their financial decisions making conditioned by constraints and opportunities they face and the resources they can access. Thereby, they make subjectively reasonable (but not necessarily objectively rational) decisions. Compared to other investments, the rationality of decisions may be even more restricted for investments in stock markets, which can be characterized as “hypercomplex” (Schimank, 2010). This complexity constitutes a substantial entry barrier for investment.

Early investments in stocks and other high-risk, high-return investments can increase net worth in the long run. Moreover, wealth may serve as a private safety net against risky life course decisions (e.g., family formation), including status attainment decisions (e.g., educational decisions). Thus, financial investments can help maintain social status over the life course and reproduce social status across generations (Henretta and Campbell, 1978; Spilerman, 2000). Beyond these positive effects of wealth, we argue that the ownership of wealth may also create expectations of further wealth accumulation or at least wealth reproduction. Wealth is not only an instrument of social status attainment and reproduction but may become a component of social status in itself (e.g., Henretta and Campbell, 1978; Sherman, 2018). Consequently, wealth accumulation, or at least wealth reproduction, becomes an imperative of (higher) social status reproduction (Hansen and Toft, 2021).

In the following, we discuss four mechanisms that can differentiate individuals’ investment decisions by parental class: relative risk aversion, time discount preference, differences in ability expectations, and access to institutions and networks. In our elaboration, we will first focus on vertically differentiated class positions before turning to horizontal differentiation.

Relative risk aversion

It can be assumed that individuals strive to avoid downward social mobility (Breen and Goldthorpe, 1997). Financial investment decisions can be risky and may lead to economic losses and, thus, downward mobility. Higher profits may be reaped by those who invest early in risky assets such as stocks and who hold these assets in the long run than by those who invest in more secure assets such as life insurance. At the same time, the risk of losing these investments is also relatively high, particularly in the short run. For those originating from higher social positions, returns on profitable investment may be necessary to achieve and maintain social positions comparable to the parental generation over the life course. However, for individuals originating from lower social positions, the risks associated with particular financial investments may outweigh the benefits if they can maintain their social positions without returns on risky assets. In addition, higher-status parents can better provide a safety net that allows their offspring to invest early in risky assets (Charles and Hurst, 2003), e.g., by compensating for life course events that negatively affect income.

Time discounting preferences

Individuals have unequal time discounting preferences which may affect their consumption and financial investments (Knoll et al., 2012). In the economic literature, time discounting preferences relate to how individuals prefer immediate compared to future gratification (Frederick et al., 2002). Empirical studies find that lower time discount rates are positively associated with higher saving rates, i.e., delaying consumption in the life course (Ersner-Hershfield et al., 2009). Individuals with higher time discount rates, in contrast, may have little motivation to delay consumption by making financial investments.

Sociologists have argued that time preferences are socially structured through the class-specific experience of uncertain living conditions. As individuals in lower-class positions have a higher risk of experiencing disruptive life course events such as unemployment and divorce, they are rational to discount uncertain future rewards (Sørenson, 2000). Thus, offspring from higher-status parents may be less likely to discount future rewards than present rewards and, thereby, invest more and earlier in financial assets.

Differences in ability and expectations of profitable investments

The complexity of financial markets constitutes a substantial entry barrier for potential investors. Cognitive abilities, especially mathematic abilities, are likely to reduce this barrier (Cavapozzi et al., 2013). In addition, financial literacy as a more specific skill is positively associated with participation in stock markets (van Rooij et al., 2011). Financial literacy is also positively associated with more successful participation in the stock market, e.g., choosing mutual funds with lower costs (Hastings and Tejeda-Ashton, 2008). Empirical studies show that these differences in ability are related to parental background characteristics. For instance, financial literacy is positively correlated with the education of individuals’ mothers and the stock market participation of their parents (Lusardi et al., 2010). Furthermore, exposure to diverse financial options in the family of origin may increase the subjective range of investment options later in life (Charles and Hurst, 2003; Chiteji and Stafford, 1999). Furthermore, subjectively expected gains from financial investments are likely to vary. For instance, successful investments of parents and other social contacts may increase the subjective expectations of successful investments. Such experience is more likely for offspring from high-class parents, who are more likely to own financial assets (Keister, 2005, p. 70ff).

Access to institutions and networks

Children from advantaged class positions may have privileged access to financial institutions and network resources that facilitate beneficial investments. For instance, recent sociological research shows that families at the upper end of the wealth distribution strategically ensure the transmission of dynastic wealth through family offices and other forms of wealth management (Harrington, 2016; Kuusela, 2018). Even without consulting expensive family offices, adult children may be more inclined to use financial institutions such as hedge funds or financial planners. This may be because their parents use or even work in these institutions (see next section on horizontal differentiation).

The parents themselves and their more comprehensive network of social contacts may provide relevant resources such as knowledge. Children may draw from such resources when making investments. For instance, financial knowledge in social networks, which is likely stratified by class position, may help overcome an individual's lack of financial literacy as a barrier to investments (Chang, 2005). Wealth in the broader social network of parents may additionally facilitate investments similar to what has been argued about parental wealth above. For instance, wealth in the social network may be used as a safety net in times of financial needs, and it may also be drawn upon as seed money for a business.

Vertical and horizontal differentiation in class and financial investments

In addition to the vertical position in the class hierarchy, we consider the effect of horizontal differentiation across different work logics and the relative importance of economic versus cultural capital (Bourdieu, 1984). The concept of work logic primarily refers to work organization in different occupations (e.g., hierarchies, bureaucratization, supervision, career ladders, and interpersonal relations). Nevertheless, it broadly aligns with Bourdieu's concept of the horizontal axis of the social space according to the relative composition of economic and cultural capital (Waitkus and Groh-Samberg, 2019).

Socio-cultural occupations are characterized by a relative dominance of cultural capital in terms of formal education and the social and cultural skills, expertise, and knowledge required. Socio-cultural occupations produce public goods such as providing education, health, and social services. In contrast, managerial occupations follow a market- and profit-oriented work ethos, aiming at meeting the demands of the respective markets. While these occupations may also require higher formal education (typically business education), all other forms of capital are subordinated to economic capital and market success. In the Oesch class scheme, however, managerial occupations are grouped together with administrative occupations. Regarding the relative composition of cultural and economic capital, and the affinities to investments in financial assets, we consider both administrative and, finally, technical occupations to range in between the economic/managerial and the socio-cultural pole of horizontal class differentiation. Therefore, in our empirical analysis, we focus on comparing sociocultural professionals against other occupations.

Based on these arguments, we expect that children from parents with managerial occupations (which we cannot disentangle from administrative occupations) benefit from their proximity to and professional knowledge of (complex financial) markets and, thus, invest more and earlier in risky assets. Given the relatively greater value that economic capital enjoys in their capital portfolios, they are also able to reap surplus-premiums from engaging in emerging new types of financial assets. In contrast, children from socio-cultural professionals will mainly rely on more secure and established long-term investments in wealth such as life insurance.

Summary and hypotheses

Based on these arguments, we formulate hypotheses about the association between parental class, occurrence and timing of risky financial investments over the life course, and net worth. We expect these hypotheses to hold net of individuals’ class position, education, and income, and net of parents’ net worth. We do not test specific mechanisms yet as our current aim is to understand the general relationship between, on the one hand, parental class and, on the other hand, investments and net worth.

Individuals from advantaged class origins invest more frequently in risky financial assets (stocks and mutual funds) than individuals with less advantaged class origins (Occurrence Hypothesis). Individuals from advantaged class origins invest earlier in risky financial assets than individuals with less advantaged class origins (Timing Hypothesis). Individuals originating from socio-cultural professionals with dominant cultural capital (a) invest less and (b) later in risky assets compared to vertically similar class positions with dominant economic capital (Cultural Capital Hypothesis). Individuals from advantaged class origins (a) have more net worth and (b) this can partly be explained by more and earlier investments in risky financial assets (Net Worth Hypothesis).

Note that we do not aim to investigate cross-national differences in financial investments. Due to few country cases and few observed investment events in each country, we cannot formally test hypotheses about country differences. Therefore, we test our hypotheses on a pooled sample of countries.

Data and methods

Data

We use data from the SHARE. SHARE is the only survey we are aware of which includes full retrospective biographies on financial investments. We combine retrospective information mainly collected in waves 3 and 7 (SHARELIFE) with prospective information (for net worth) from all survey waves (Börsch-Supan, 2019a, 2019b, 2019c, 2019d, 2019e, 2019f, 2020, 2021; Börsch-Supan et al., 2013). We also use the integrated SHARE Job Episodes Panel (Brugiavini et al., 2019). The original SHARE sample consists of individuals born in 1954 or earlier and their partners from several European countries first interviewed in 2004. Booster samples and additional countries cases (including Israel as a non-European country) have been added to the data over time. The complete European Union is covered from wave 7 onwards. After entering the sample, respondents have been re-interviewed each year if they did not leave the panel. Life histories have been recorded using computer-assisted personal interviews with visual event history calendars to increase recall accuracy (Schröder, 2011). 1 The initial response rate in the first wave of SHARE was about 62%. For example, the individual retention rate for the third wave was about 77% (Bergmann et al., 2019). We organize the data in a longitudinal individual-year format.

Sample

Our sample includes respondents from 14 countries, namely Austria, Germany, Sweden, the Netherlands, Spain, Italy, France, Denmark, Greece, Switzerland, Belgium, Israel, Luxemburg, and Portugal. Ireland, Cyprus, Finland, and Malta are not included because data from these countries, which entered SHARE later, do not yet include all the necessary information for our analysis. Observations from formerly socialist countries and East Germany for the analytical sample are excluded because financial investments were strongly regulated during the socialist regime (Cavapozzi et al., 2013). The primary interview respondents and their partners are identified in wave 3 and wave 7 and their retrospective information (age 20 to 69) is included in the analysis. Additional information from other waves is merged with the data. We exclude observations with missing values on analytical variables. Our sample consists of between 21,992 and 23,018 respondents (with an average of 20 to 43 individual-year observations per respondent) depending on the outcome variable. In addition, we observe the net worth of 20,839 respondents.

Measures

Outcome variables

For the analyses of financial investments, we examine four outcome variables that measure the timing of financial investments (Table O.1 in the online appendix shows summary statistics for all variables). The first outcome variable indicates the age at first investment in stocks by measuring whether an investment in stocks occurs for the first time (coded 1), or not (coded 0) within each year of the life history. Similarly, we consider investments in mutual funds, investment in life insurance, and investment in private retirement plans. 2 Table O.3 in the online appendix shows the frequency of different investments in each country and total. We consider investments in stocks and mutual funds as risky and investments in life insurance and retirement plans as secure investments. 3 We study the latter two types of investments and investment in homeownership for comparison, even though we have no hypothesis about these outcomes. Respondents who never make any investment during the observation period are right-censored. 4

We examine net worth as an additional outcome, where net worth is the sum of all current financial and non-financial assets minus mortgages and loans. We apply a year-specific rank transformation within countries because of the highly skewed wealth distribution. We measure net worth at the household level. We take the individual-specific mean of all available net worth information to reduce measurement error (Killewald et al., 2017). 5

Explanatory variables

Our primary explanatory variable is the class of parents to capture the social origin of respondents. Respondents report the current or last observed occupation of their parents when interviewed for the first time in SHARE. We measure parents’ class using a modified version of Oesch's (2006) class scheme with seven categories: higher-grade service class, lower-grade service class, socio-cultural professionals, socio-cultural semi-professionals, skilled workers, unskilled workers, not in the civil labor force. In contrast to the original Oesch class scheme, we separate the socio-cultural professionals and socio-cultural semi-professionals which are initially part of the higher (professionals) and lower (semi-professionals) grade service class. For the parental generation, we can only draw on occupations measured with ISCO, and we cannot use information about the self-employment status and the number of employees in constructing the class measure. We use the highest class observed of both parents (dominance rule). This variable is time-constant.

Mediating variables

When we examine the relationship between parents’ class and net worth, we consider the timing and occurrence of financial investments as mediators. We treat the earliest 33% of investments in each country for each investment type as early investments (see Table O.2 in the online appendix for cut-off ages). For example, for Austria investments in stocks are considered early when they occur up to age 43. Other investments are treated as late investments. We additionally include variables for whether individuals ever invested in specific assets.

Control variables

We include the following control variables, which are partly time-varying variables tracking changes over the life course and partly time-constant variables (see the Online Appendix Section 8.4 for more details). Class of respondents is measured with Oesch's class scheme similar to the parents’ class position but additionally differentiating more granular positions within the upper-grade service class. 6 We also include women, immigrants, lived with both parents at age 10, any siblings, in education, unemployed, retired, education, period, and country dummies in all models. To proxy parental net worth, we include an indicator of inheritance of at least 5000 EUR, whether parents were in homeownership during childhood, and rooms per head during childhood. We additionally report models in which we control for income (rank) from (self-)employment (time-varying). 7 Because the retrospective income report is prone to recall bias and is plagued by many missing responses, we do not include income in the main models.

Analytical strategy

First, the unconditional hazard rates and failure rates of first investments by social origin are presented. Second, we examine first investments in a multivariate framework using discrete-time event history analysis for single events (Allison, 1984). We use a discrete-time model because investment timing is only recorded in yearly time intervals. Therefore, we calculate hazard rates for each yearly time interval using a logistic regression framework. Respondents enter the risk set at age 20. Years since age 19 is used as the clock for the event history analysis. In general, the model can be written as:

To test the Net Worth Hypothesis, we first estimate OLS regression models for the outcome rank-transformed net worth. We then decompose the coefficient for the class of parents in the direct effect and the indirect effect working through financial investments using mediation analysis. We use the KHB routine in Stata for the decomposition (Kohler et al., 2011).

Results

Unconditional association between parental class and investments

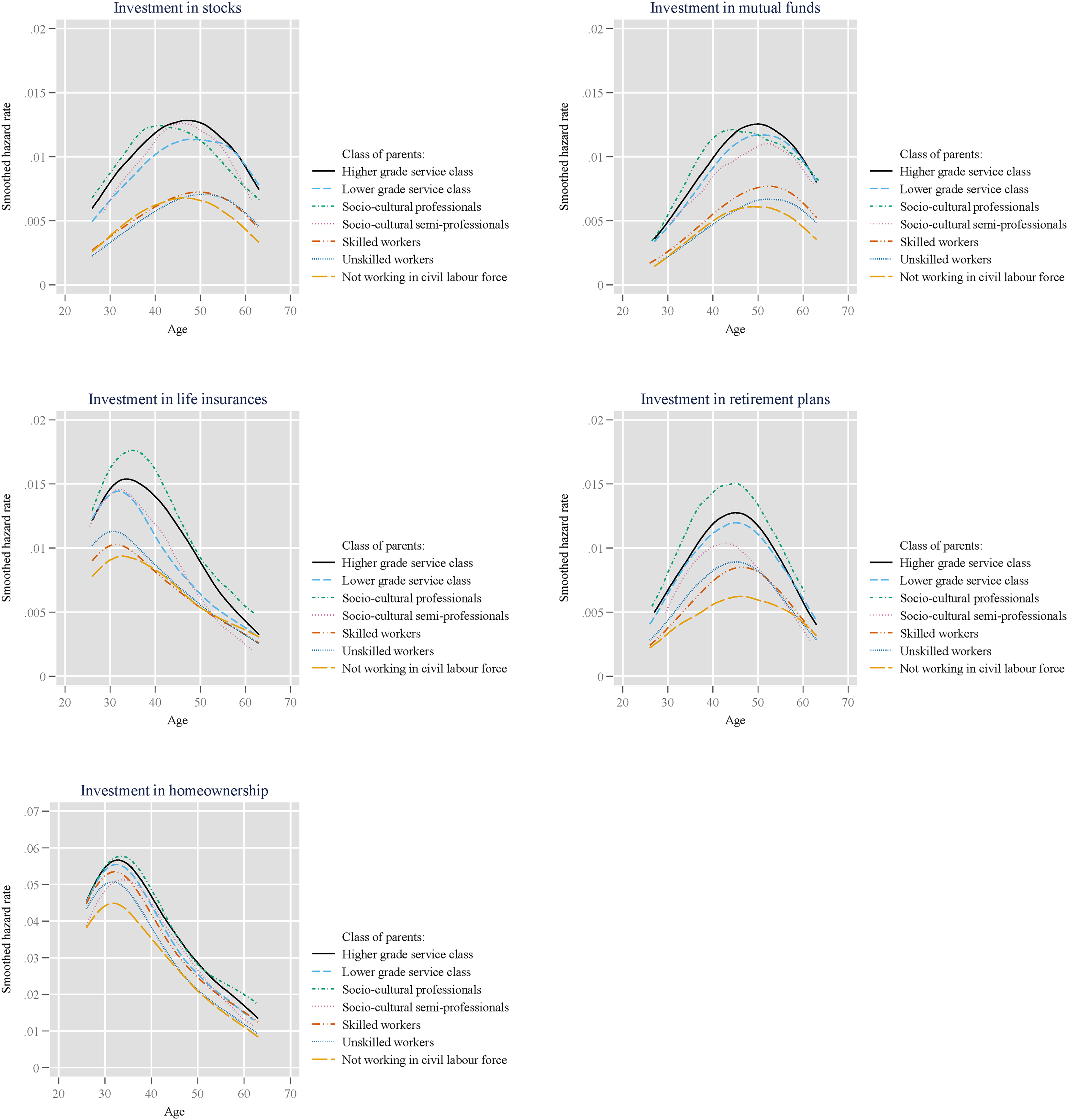

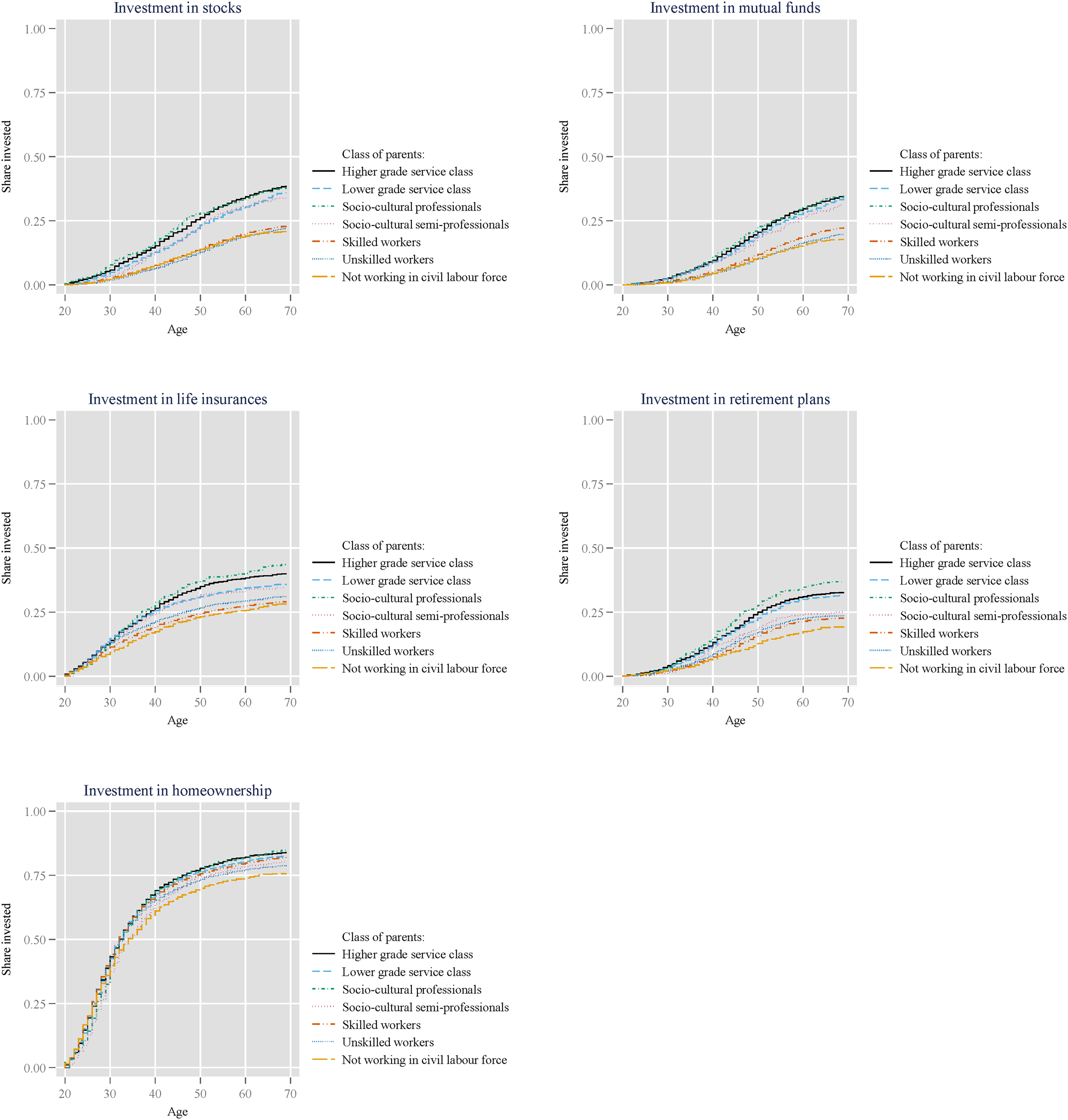

In Figure 2, we plot the smoothed hazard rates for the four types of investments into financial assets and investments in homeownership by parental class and age. The chances of entering homeownership (note that we use a different y-scale) are considerably higher across most ages than the chances of investing in stocks, mutual funds, life insurance, or retirement plans (see also Figure 3 for cumulative rates of investment). Across all investment types, we find consistent patterns of slightly earlier and more widespread investments of the offspring of higher classes. Against our expectations, the offspring of the socio-cultural professionals stands out with high and early investment rates in these descriptive analyses. The differences in investments across parental class positions are particularly pronounced for stocks and mutual funds. For example, at age 30, 6% of children of the higher-grade service class have already invested in stocks, whereas less than 2% of those originating from the unskilled workers class did so. These differences increase to 26% and 13% at age 50. However, the general age patterns of investments seem to be similar across parental classes, and we generally find no evidence for distinct timing of financial investments by parental class. Across all parental classes, the smoothed hazard rates for investments follow hump-shaped trajectories with peak hazard rates for investments in stocks, mutual funds, and private retirement plans around age 50 except for socio-cultural professionals for whom the peak is reached earlier, around age 40. Investments in life insurance and homeownership occur earlier and are most likely when respondents are in their 30s. Especially investments in life insurance and retirement plans become less likely beyond age 50.

Smoothed hazard rates of investments by class of parents. Data: SHARE & SHARELIFE, unweighted, own computation. Note: For all figures, we use Stata packages by Jann (2014) and Bischof (2017).

Cumulative rates of investments by class of parents. Data: SHARE & SHARELIFE, unweighted, own computation.

Multivariate results

Parental class and investments

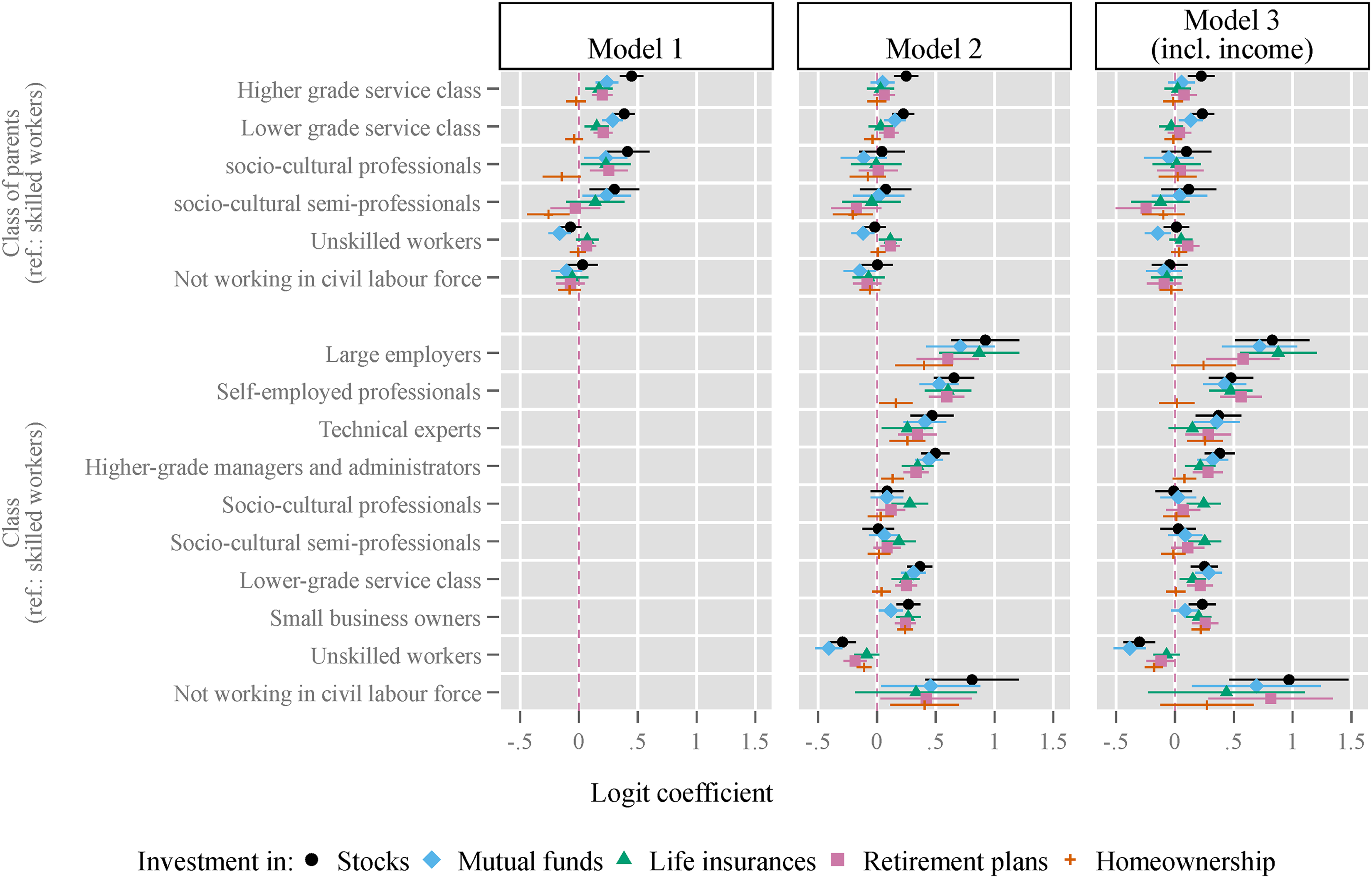

Figure 4 shows results from multivariate event history analyses. We are interested in the coefficients for parents’ class. In the Occurrence Hypothesis, we expected that individuals with parents from more advantaged classes invest more in risky financial assets such as stocks and mutual funds compared to individuals with less advantaged parents. In addition, in the Cultural Capital Hypothesis, we expect that individuals who originate from class positions with dominant cultural capital to invest less and later in risky assets compared to vertically similar class positions with dominant economic capital.

Multivariate discrete-time event history models separately estimated for each type of investment. Data: SHARE & SHARELIFE, unweighted, own computation. Note: Random-effects logistic regression, all models include control variables for woman, immigrant, lived with both parents at age 10, any siblings, inheritance, parents were in home ownership during childhood, rooms per head during childhood, period, and country. Models 2 and 3 additionally include in education, unemployed, retired, and education. Model 3 additionally includes income (log). Model 3 based on smaller sample size. Full estimation results in Table O.4 in the online appendix.

In the first step, we consider constant shifts in the hazard rates and we report models without (Model 1) and with (Model 2) adjusting for respondents’ own class position and their income (Model 3). The results indicate that when not adjusting for respondents’ own class position, parents’ class is associated with the investments of their offspring. Respondents with parents who are in the higher-grade or lower-grade service class or are socio-cultural professionals are more likely to invest in stocks, mutual funds, life insurance, and retirement plans than those whose parents are skilled workers. Respondents with parents who are socio-cultural semi-professionals are more likely to invest in stocks and mutual funds than those whose parents are skilled workers. For instance, individuals with parents who are in the higher-grade service class are by a factor of 1.57 ( = e0.45) more likely to invest in stocks than individuals with parents who are skilled workers. Comparing respondents with parents from the higher-grade service class, lower-grade service class, or whose parents are socio-cultural (semi-) professionals, the chances to invest in stocks and mutual funds are similar.

Once we adjust for respondents’ class position (Model 2), the estimated effects of parental class on investments in stocks and mutual funds are substantially reduced in size, and most of them are no longer statistically significant. Only regarding investments in stocks (and mutual funds for the lower-grade service class), we still find respondents with parents in the higher- or lower-grade service class to be more likely to invest than children of skilled workers. This is not the case for respondents whose parents are socio-cultural (semi-) professionals. Respondents with parents who are unskilled workers or not employed in the civil labor force are less likely to invest in mutual funds than respondents whose parents are skilled workers once respondents’ class position is added to the model. Additionally controlling for income (Model 3) only marginally changes the coefficients for parental class, and only slightly reduces the effect sizes of own class position, suggesting that income differences are largely explained by occupational class. Overall, these results are in line with the Occurrence Hypothesis about more frequent investments in risky assets such as stocks among individuals from advantaged parental classes. We also find partial evidence for the Cultural Capital Hypothesis because the offspring of socio-cultural (semi-) professionals is less likely to invest in risky assets compared to other parts of the service class.

We find that the hazard rates for investments are clearly stratified by respondents’ own class positions (Model 2). Compared to skilled workers, we find large employers, self-employed professionals, technical experts, and lower-grade managers and administrators more likely to invest in stocks, mutual funds, life insurance, retirement plans, and homeownership. Socio-cultural (semi-) professionals, however, are only more likely to invest in life insurance compared to skilled workers. The lower-grade service class and small business owners are more likely to invest in all types of assets compared to skilled workers with the exception of homeownership for the lower-grade service class. Unskilled workers are mostly less likely to invest while those not working in the civil labor force are mostly more likely to invest than skilled workers. These differences change little when controlling for individual income. Other control variables behave mostly as expected (see Table O.4 in the online appendix for full model results).

Timing of financial investments

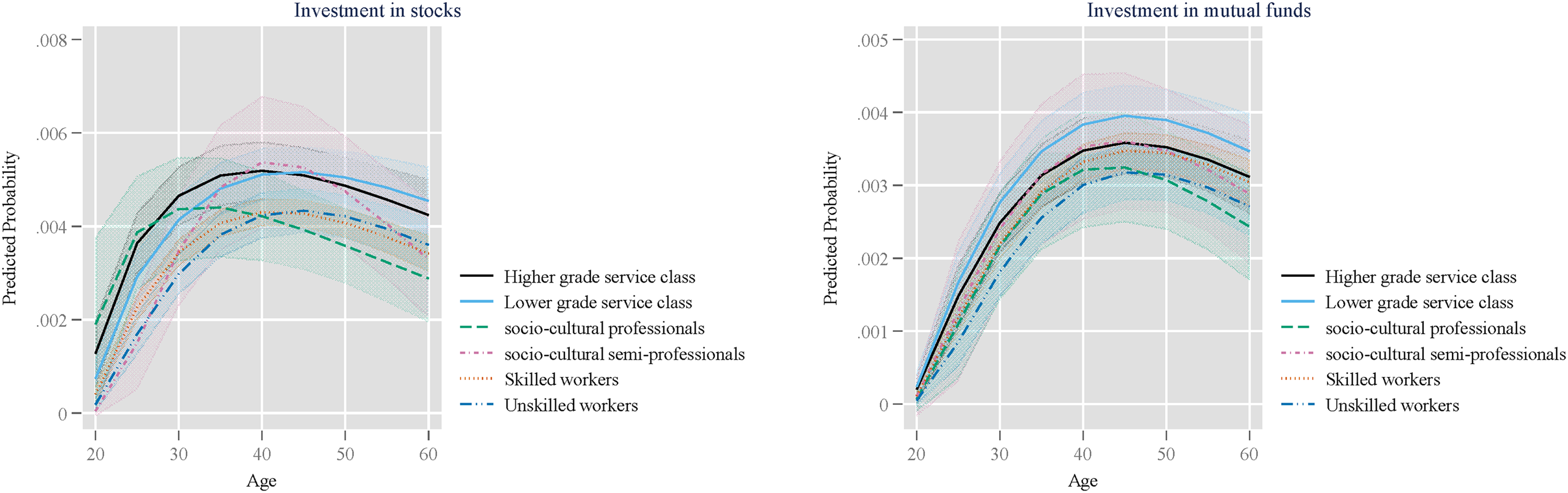

Figure 5 shows results from multivariate event history analysis of first investments in stocks and mutual funds, allowing for timing effects of social origin by including interactions between years since age 19 and parents’ class. We find the timing of financial investments in stocks and mutual funds to be similar by parental class in line with the descriptive results presented earlier (see Table O.5 in the online appendix for estimation results). While Figure 4 shows minor differences in the shape of the predicted probability over age, these differences are far from statistically significant. Thus, while advantaged parental class is associated with an overall higher occurrence of investments in stocks and mutual funds, individuals from advantaged parental class do not systematically invest earlier in their life course than individuals from the less advantaged parental class.

Predicted probability of first-time investment in stocks and mutual funds. Data: SHARE & SHARELIFE, unweighted, own computation. Note: Random-effects logistic regression, cluster-robust standard errors, all models include control variables for woman, immigrant, lived with both parents at age 10, any siblings, inheritance, parents were in home ownership during childhood, rooms per head during childhood, in education, unemployed, retired, education, period, and country. Full estimation results in Table O.5 in the online appendix. Trajectories are statistically not different from each other at the 95% confidence level.

Net worth

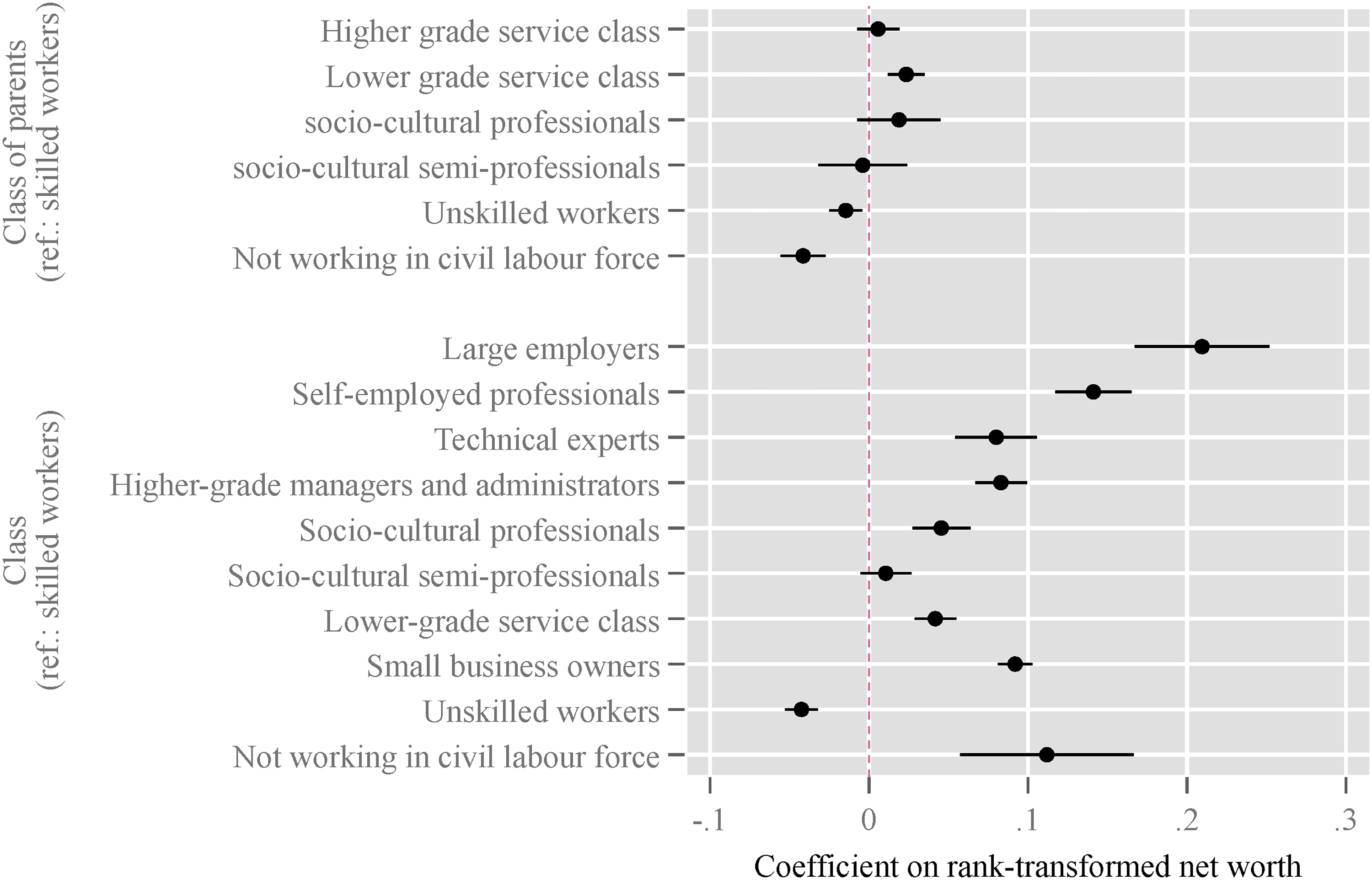

We now turn to the last hypothesis concerning net worth. We expected individuals from advantaged parental classes to have more net worth, and we expected this to be partly explained by more and earlier investments in risky assets. Figure 6 shows only partly evidence favoring the first part of the hypothesis. Individuals with parents who are from the lower-grade service class (but not from the higher-grade service class) have significantly more net worth compared to skilled workers controlled for proxies of parents’ net worth (i.e., inheritances above EUR 5000, whether parents were in home ownership during childhood, and rooms per head during childhood) and individuals own class positions. On average, individuals with parents from the lower-grade service class are about 2 percentiles higher in the wealth distribution than individuals with parents who are skilled workers. This effect may be considered small; however, given the comprehensive control strategy employed, we believe this effect to be substantial. Those with parents who are unskilled workers (about 1 percentiles lower) and not working in the civil labor force (about 4 percentiles lower) have significantly less net worth compared to skilled workers. For individuals’ own class positions, a much more stratified picture emerges with large employers and self-employed professionals having the largest net worth. We also find evidence for horizontal differentiation with socio-cultural professionals having similar net worth compared to lower-grade service class and socio-cultural semi-professionals having less net worth than other members of the lower-grade service class.

Results from OLS regression of net worth for parental class and individuals’ class. Data: SHARE & SHARELIFE, unweighted, own computation. Note: OLS regression, all models include control variables for woman, immigrant, lived with both parents at age 10, any siblings, inheritance, parents were in home ownership during childhood, rooms per head during childhood, in education, unemployed, retired, education, period, and country. Full estimation results in Table O.6 in the online appendix.

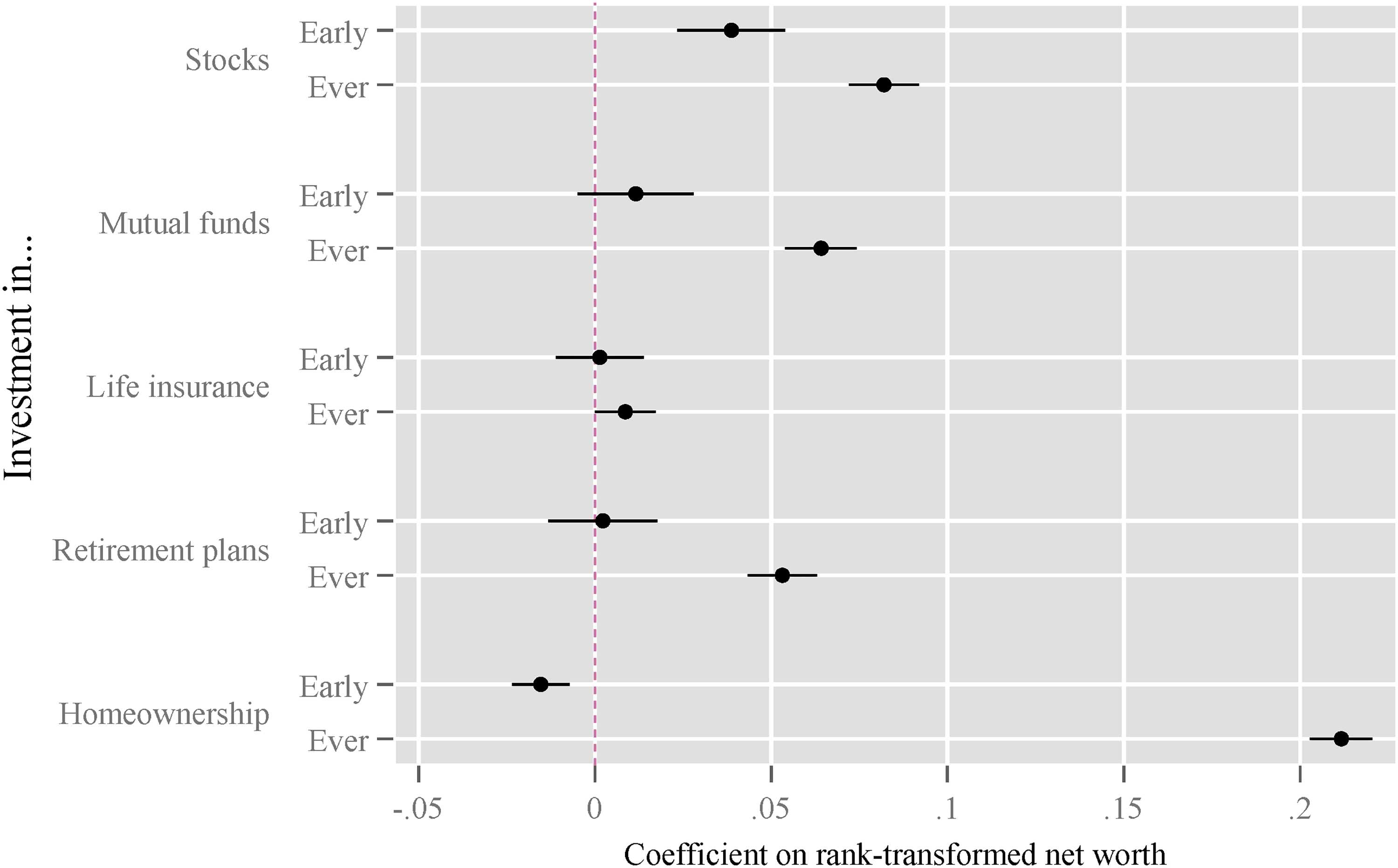

Figure 7 shows that early investments in stocks are positively associated with net worth. Early investment increases the position in the wealth distribution by about 4 percentiles beyond the positive estimated effect of ever investing in stocks over their life courses which are associated with about 8 percentiles higher net worth. For mutual funds, we do not find a significant association between early investments and later-life net worth, and this is also the case for investments in life insurance and retirement plans. Interestingly, early investment in homeownership is associated with a net worth penalty in our data. We find positive associations between ever investing in any of the assets and net worth. In particular, having ever invested in homeownership is associated with about 22 percentiles higher net worth compared to having never invested. This is in line with the wealth-enhancing consequences of entering homeownership found elsewhere (Killewald and Bryan, 2016), e.g., through “forced” savings by repaying mortgages. Homeownership also constitutes the largest share in most people's wealth portfolios and, thus, can have a substantial influence on their overall wealth positions.

Results from OLS regression of net worth for different types of investment. Data: SHARE & SHARELIFE, unweighted, own computation. Note: OLS regression, all models include control variables for class of parents, class, woman, immigrant, lived with both parents at age 10, any siblings, inheritance, parents were in home ownership during childhood, rooms per head during childhood, in education, unemployed, retired, education, period, and country. Full estimation results in Table O.6 in the online appendix.

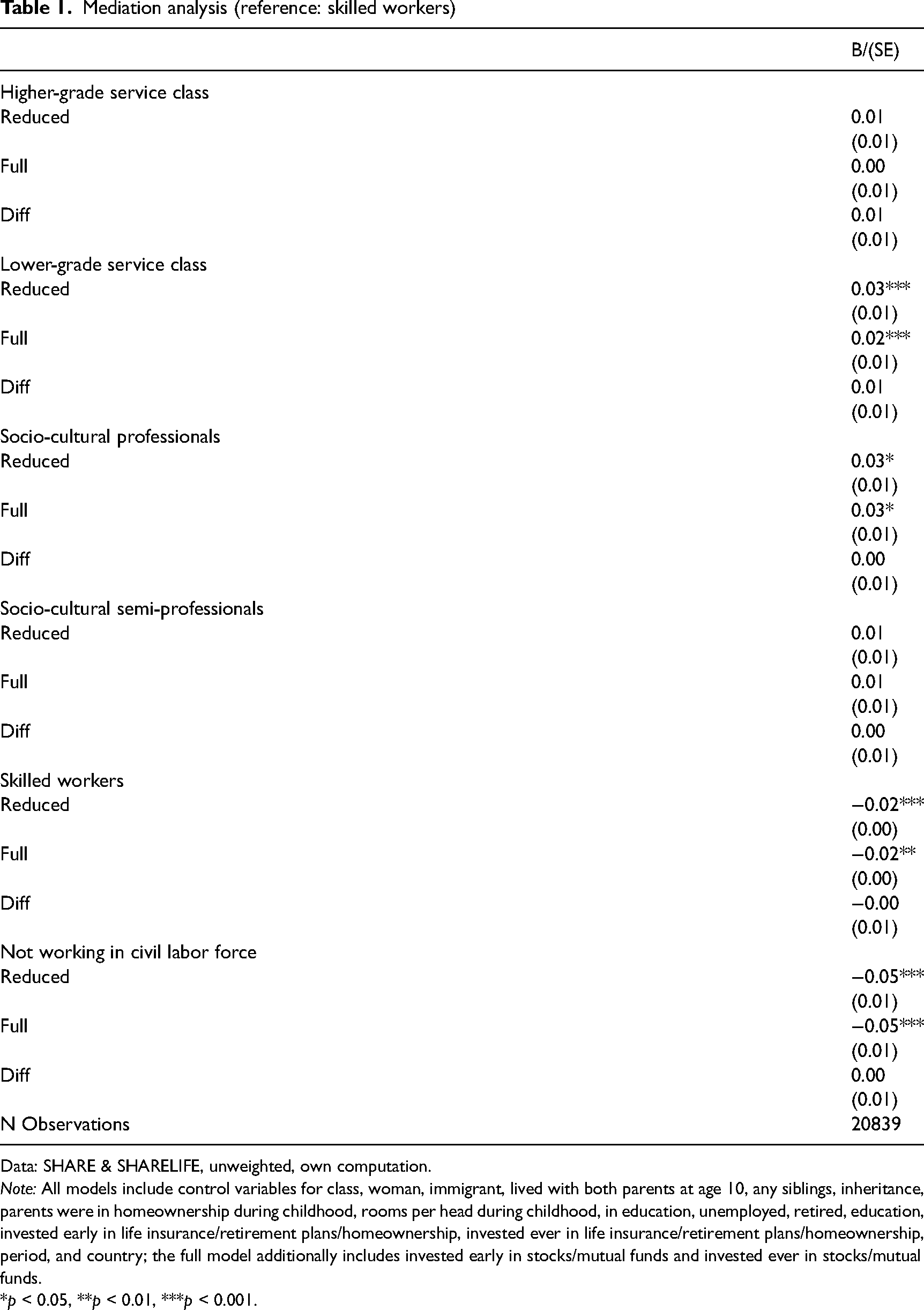

Finally, we conduct a mediation analysis (Table 1) to test the second part of the Net Worth Hypothesis. Does parents’ class position influences net worth through changing individuals’ investment behavior? To answer this question, results in Table 1 compare a model of net worth without including the timing and occurrence of financial investments in stocks and mutual funds (Reduced) with a model in which these variables are included (Full). We find no evidence that the net worth of individuals whose parents are from more advantaged classes have higher net worth because they invest earlier or more often in risky assets such as stocks and mutual funds. None of the estimated differences in coefficients for parental class between the reduced and full model reaches statistical significance. The sizes of the differences are close to 0 for all class categories.

Mediation analysis (reference: skilled workers)

Data: SHARE & SHARELIFE, unweighted, own computation.

Note: All models include control variables for class, woman, immigrant, lived with both parents at age 10, any siblings, inheritance, parents were in homeownership during childhood, rooms per head during childhood, in education, unemployed, retired, education, invested early in life insurance/retirement plans/homeownership, invested ever in life insurance/retirement plans/homeownership, period, and country; the full model additionally includes invested early in stocks/mutual funds and invested ever in stocks/mutual funds. *p < 0.05, **p < 0.01, ***p < 0.001.

Conclusion

In the current study, we documented variation in the financial investment behavior and net worth across the life courses by individuals’ class origin using retrospective life history data and prospective panel data from 13 European countries and Israel. We showed that individuals with parents from advantaged classes are more likely to invest in risky and profitable financial assets such as stocks above and beyond parental net worth and individuals’ class, income, and education. When considering horizontal differentiation, classes with more economic capital than cultural capital are more likely to invest in financial assets. We did not find an association between parental class and secure financial investments such as life insurance. The timing of risky financial investments did not systematically vary by parental class. Finally, we showed that advantaged parental class is positively associated with net worth in later life. However, this association cannot be explained by the specific investments of individuals from advantaged parental classes.

Previous scholarship on the intergenerational transmission of (dis-)advantage mainly focused on the transmission of class and income mediated through education—both outcomes of the labor market. In the current study, we emphasized another aspect of advantage, namely wealth. By considering financial investments related to the attainment of wealth, we examined transmission processes and reproduction strategies that are intertwined with but distinct from labor market outcomes. By studying these under-researched processes, which we believe are primarily complementary but could be compensatory to the transmission of class and income, we contribute essential additional insights into the mechanisms of the intergenerational transfer of advantage. We acknowledge that financial investments are limited in their importance for reproduction compared to education and occupational attainment. Nevertheless, financial investment decisions can be understood as critical additional components in the reproduction strategies for high-status parents. Our findings suggest that, in particular, originating from the higher-grade and lower-grade service class, except for socio-cultural (semi-)professionals, is associated with more investments in risky financial assets.

Innovatively, we examined not only vertical differentiation in class positions but also horizontal differentiation. Our findings suggest that offspring of parents with occupations with relatively more economic capital than cultural capital benefit from their proximity to and professional knowledge of financial markets in investing more in risky financial assets such as stocks. In contrast, offspring from parents with socio-cultural occupations seem to invest less often in risky financial assets. While not the focus of the current study, we also find marked differences in investments by children's own class position, where classes with dominant economic capital are more likely to invest in financial assets than classes with dominant cultural capital.

Our study also contributes to understanding the emergence of wealth inequality in current societies. Wealth inequality is immense in many rich democracies, with about twice as much wealth inequality as income inequality in most OECD countries (Balestra and Tonkin, 2018). Our results show the persistent association of parental class with adult children's wealth net of a wide range of controls at the parents’ and children's level in a broad selection of European countries in line with recent findings of class-origin wealth gaps in Norway (Hansen and Toft, 2021). Thereby, we unveil another aspect of the intergenerational transmission of advantage which leads to rigidities in the social structure and creates class-based inequalities in wealth.

While we found individuals with parents from advantaged parental classes to be wealthier, our hypothesis that distinct investment strategies may explain the wealth advantage was rejected. However, because of our imprecise measures of financial investment behavior, we should be careful to rule out investment behavior as a mediator. For example, those from advantaged social origins may be more likely to select profitable stocks or may be more likely to buy and hold instead of frequent trading. Such aspects of investments are not captured in our data. Unobserved characteristics of parents may also be associated with parents’ class and individuals’ net worth. However, it is not easy to think of such characteristics that do not work through parental net worth (if our proxies for parental net worth are adequate) and individuals’ social positions.

Our findings are subject to several limitations. First, we used retrospective data in which respondents reported on events over several decades. Recall error may create measurement error. We have analyzed “don't know” responses, indicating that response behavior is not systematically associated with social origin. Nevertheless, there may be differences in the accuracy by which respondents from different social origins recall their first investments, which we have not captured in the additional analysis. Second, our analysis examined the event of the first investment, but we did not consider how much money individuals invested and how successful their investments were. As discussed above, these are essential aspects of individuals’ investment histories, which we could not investigate in the present study. Third, we examined data from only 14 countries with few investment events per country. These data do not allow the formal study of the institutional environment.

Our study indicates several avenues for future research. First, tests of the underlying theoretical mechanisms that we outlined can be instructive to understand better how class-specific financial investments occur. The first step in this direction would be to examine how financial risk preferences, time discounting preferences, and financial literacy vary by the class position of individuals and their parents. Second, more research is needed to understand how contextual conditions such as the degree of financialization shape class-specific investments. Here large-scale cross-national and historical variation may be exploited, but currently, this endeavor will be hampered by a lack of data. Third, the nascent literature on ethnographies of how individuals use financial investments to transmit social status across generations (e.g., Glucksberg, 2018; Harrington, 2016) needs further advancement. The integration of their results with quantitative approaches can provide significant additional insights into families’ reproduction strategies regarding wealth.

Supplemental Material

sj-docx-1-asj-10.1177_00016993221129792 - Supplemental material for The long reach of class origin on financial investments and net worth

Supplemental material, sj-docx-1-asj-10.1177_00016993221129792 for The long reach of class origin on financial investments and net worth by Philipp M Lersch and Olaf Groh-Samberg in Acta Sociologica

Footnotes

Acknowledgments

This paper uses data from SHARE Waves 1, 2, 3, 4, 5, 6, 7 and 8 (DOIs: 10.6103/SHARE.w1.710, 10.6103/SHARE.w2.710, 10.6103/SHARE.w3.710, 10.6103/SHARE.w4.710, 10.6103/SHARE.w5.710, 10.6103/SHARE.w6.710, 10.6103/SHARE.w7.711, 10.6103/SHARE.w8.100, 10.6103/SHARE.w8ca.100), see Börsch-Supan et al. (2013) for methodological details. (1) The SHARE data collection has been funded by the European Commission, DG RTD through FP5 (QLK6-CT-2001-00360), FP6 (SHARE-I3: RII-CT-2006-062193, COMPARE: CIT5-CT-2005-028857, SHARELIFE: CIT4-CT-2006-028812), FP7 (SHARE-PREP: GA N°211909, SHARE-LEAP: GA N°227822, SHARE M4: GA N°261982, DASISH: GA N°283646) and Horizon 2020 (SHARE-DEV3: GA N°676536, SHARE-COHESION: GA N°870628, SERISS: GA N°654221, SSHOC: GA N°823782) and by DG Employment, Social Affairs & Inclusion through VS 2015/0195, VS 2016/0135, VS 2018/0285, VS 2019/0332, and VS 2020/0313. Additional funding from the German Ministry of Education and Research, the Max Planck Society for the Advancement of Science, the U.S. National Institute on Aging (U01_AG09740-13S2, P01_AG005842, P01_AG08291, P30_AG12815, R21_AG025169, Y1-AG-4553-01, IAG_BSR06-11, OGHA_04-064, HHSN271201300071C, RAG052527A) and from various national funding sources is gratefully acknowledged (see www.share-project.org). This paper uses data from the generated Job Episodes Panel (DOI: 10.6103/SHARE.jep.710), see Brugiavini et al. (2019) and ![]() for methodological details.

for methodological details.

Funding

Support Network for Interdisciplinary Social Policy Research (FIS) of the German Federal Ministry of Labor and Social Affairs, Deutsche Forschungsgemeinschaft (grant number 3612/5-1).

Supplemental material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.