Abstract

Advances in mobile communication and information technology have resulted in wireless sensor network (WSN) systems in which mobile phones (smart phones) can be used to conduct a wide variety of commercial, social, entertainment, and file-sharing transactions. In particular, mobile commerce (m-commerce) allows users to conduct payment, business, and service transactions over portable mobile devices. This trend has been enhanced by the development of near-field communication (NFC) technology and the increased market for NFC-embedded (smart phones). NFC technology is a standards-based wireless communication technology that allows data to be exchanged between devices located a few centimeters apart, such as radio-frequency identification (RFID tags and readers). To refine the m-commerce process in the NFC-based mobile environment, we study NFC and location-based services propose a WSN-hosted m-payment system based on these technologies.

1. Introduction

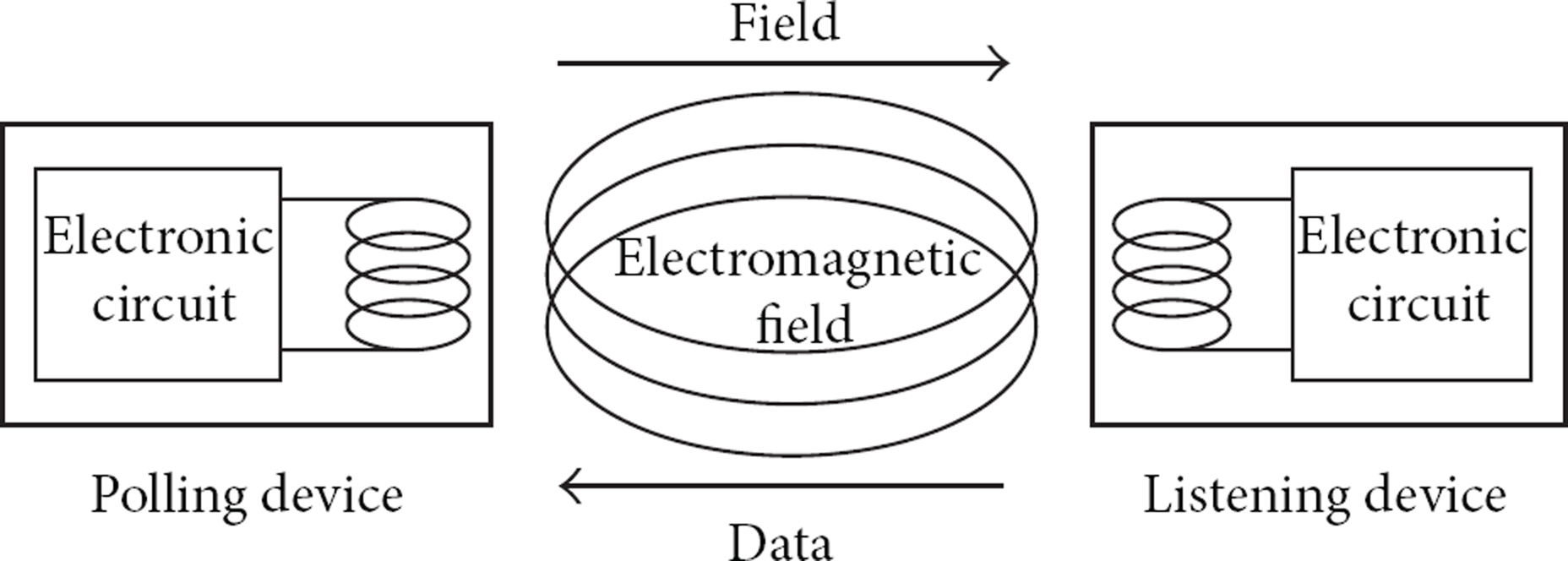

Advances in mobile communication and information technology have resulted in wireless sensor network (WSN) systems [1–5] in which mobile phones (smart phones) can be used for a wide variety of purposes, including making phone calls; sending text messages (e.g., through short message services or SMS), photos, or movies; visiting web sites; sending emails; watching TV; buying products (through mobile payments); mobile ticketing; and accessing company intranets. Mobile commerce (m-commerce) allows users to conduct business and service transactions through mobile payments in which two parties exchange financial value using portable mobile devices. This trend has been enhanced by the rise of near-field communication (NFC) technology and the market for NFC-embedded smart phones. ABI Research estimates that 200 million NFC-enabled handsets have been sold globally to date and that 1.55 billion will be shipped annually by the year 2017 [6]. Owing to the success of a series of pilots, the use of NFC for payment is becoming better known to the consumer, and a report by Juniper Research in May 2012 found that worldwide NFC mobile payments are expected to exceed US$180 billion globally in 2017 [7]. NFC technology is a standards-based wireless communication technology that allows data to be exchanged between devices such as radio-frequency identification (RFID) tags and readers that are located a few centimeters apart [8]. Polling device (initiator) and listening device (target) configuration are shown in Figure 1. The technology can be used in a wide variety of mobile applications such as making payment by waving close to or touching contactless point-of-sale (POS) reader or reading information on special offers, coupons, or discounts from smart posters or billboards embedded with RF tags. M-commerce trials and research based on NFC technology have been conducted worldwide [9–23].

Polling device (initiator) and listening device (target) configuration.

In this paper, to improve the m-commerce process for NFC-based mobile environment we propose an m-payment system based on NFC as well as on location-based services (LBS) technology that can help detect the locations of people or items using portable equipment through a wireless communication network.

We investigate (1) NFC, (2) LBS, and (3) m-payment systems and propose (4) an m-payment system conducting m-commerce over a WSN that uses NFC and is based on the LBS technique. In light of the diffusion of NFC-embedded phones and the development of WSNs, the proposed pass through system represents a potentially useful method for implementing, m-payments using NFC technology for m-commerce.

2. Related Work

2.1. Near-Field Communication (NFC)

The concept of NFC [8, 24–27] adapts existing noncontact card payment methods that use a high frequency (HF) range of 13.56 MHz to enable authorization and payment to be made when a mobile phone is close to a payment system. Via POS terminals, micropayments, internet banking, and internet shopping mall payments can all be made via NFC instead of SMS in automats or conveniences stores. NFC is a low-power, low-cost communication solution that focuses on personalized communication and allows various types of sensitive data to be exchanged in perfect security.

2.1.1. Basics of Data Transmission with NFC

As in RFID Standard 14443 and FeliCa, NFC involves the use of inductive coupling in which, much like a power transformer, the magnetic near field of two conductor coils is used to couple a polling device (initiator) with a listening device (target) at an operating frequency of 13.56 MHz.

2.1.2. Wireless Communication Mode and Interface

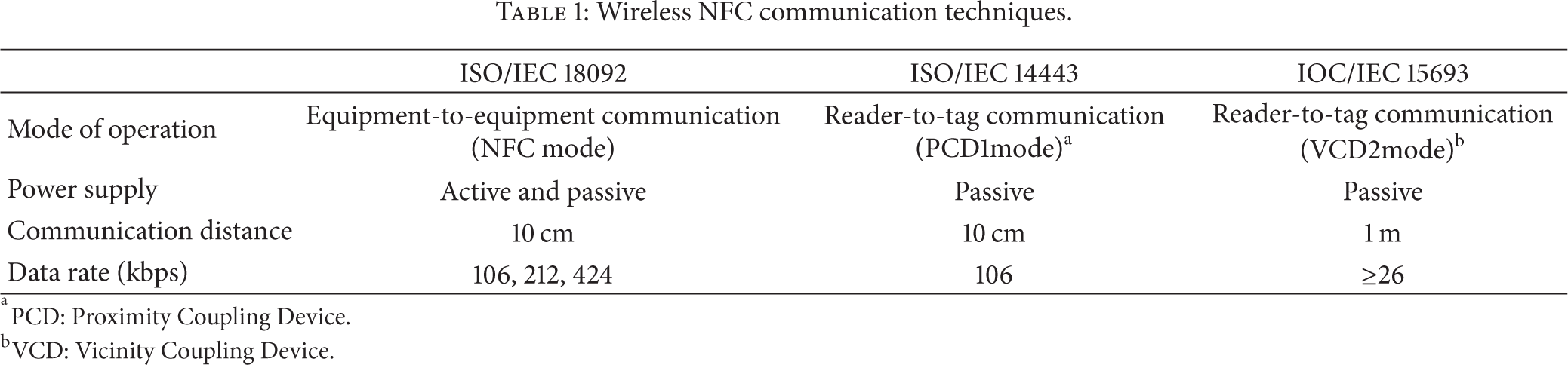

NFC is a short distance radio communication technology that enables communication between two devices in close proximity to each other (e.g., within 10 cm). This technology is being increasingly considered as a solution for contactless payment processing models. NFC has three radio communication modes, as shown in Table 1: reader/writer, peer-to-peer, and card emulation mode.

Wireless NFC communication techniques.

aPCD: Proximity Coupling Device.

bVCD: Vicinity Coupling Device.

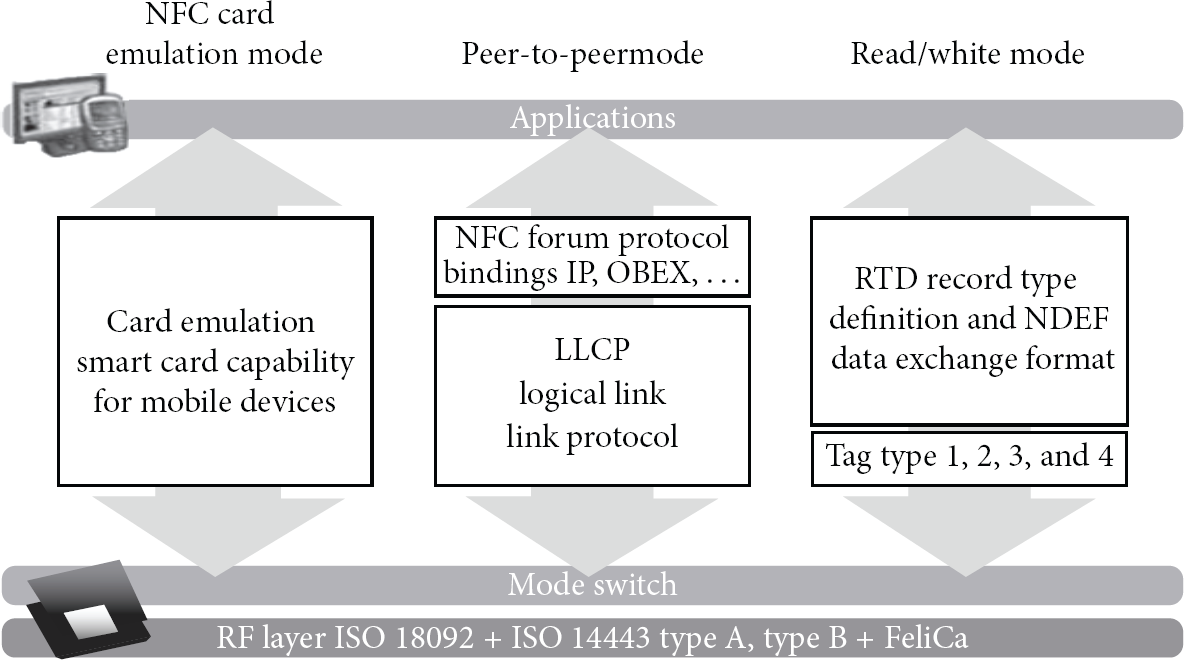

To enable mobile contactless payments, the NFC-enabled mobile device operates in card emulation mode and appears to an external reader to be a traditional contactless smart card. NFC provides a mode switch function as shown in Figure 2.

NFC technology (NFC forum).

NFC-enabled devices are governed by standards in ISO/IEC (ISO/IEC 18092), ETSI (ETSI TS 102 10 V1.1.1 (2003-03)), and ECMA International (ECMA-340) and by specifications published by the NFC Forum. ISO/IEC 18092 allows for backward compatibility with existing contactless devices by supporting ISO/IEC 14443 (the standard used by payment network-branded contactless payment cards and devices), as well as FeliCa contactless interface protocols.

In the context of mobile payment processing, an NFC enabled mobile device can interact with an NFC enabled POS device to perform payment functions through NFC connectivity by leveraging ISO/IEC 14443 standards for NFC card readers (PCD readers) and NFC devices, that is, for NFC client proximity integrated circuit card (PICC) communication. To complete a mobile commerce transaction, it is essential that the mobile devices and POS equipment are both NFC enabled.

2.1.3. NFC-Enabled Device and UICC

Mobile phone payment information is stored in a secure element within the phone a smart card chip that protects stored data and enables secure transactions and contactless payments can be conducted through NFC devices without changing the existing acceptance infrastructure. The interfaces between an NFC-embedded mobile phone, NFC device, and mobile network are shown in Figure 3.

Interfaces of NFC-embedded mobile phone, NFC device, and mobile network.

The secure element is the component within the connected mobile device that provides the application, network, and user with the appropriate levels of security and identity management necessary to assure the safe delivery of a particular service; such an element can be embedded within the phone or within a secure memory card, either of which can be delivered simply and cost-effectively to the mobile environment. Indeed, the most common secure element within the mobile space and the most widely used security platform in the world is the subscriber identifier module (SIM) or, more accurately in current nomenclature, the universal integrated circuit card (UICC). The UICC, which sits at the heart of the handset and manages and authenticates secure access between a connected device and a host, can be used to take full advantage of the increasing number of IP and cloud-based services and applications in helping to deliver on the promise of mass-market NFC technology adoption.

The UICC is considered by mobile networks operators to be the preferred secure element for use within mobile devices. The architecture of a mobile device integrated-NFC is shown in Figure 4.

Architecture of mobile device-integrated NFC.

2.2. Location-Based System (LBS)

2.2.1. Location-Based System

Location-based system (LBS) is service that can be used to help detect the locations of people or items through portable-equipment based on a wireless communication network. LBS can provide various information services related to position or location; for instance, a customer in a strange region who wants to find the nearest store, bank, bookstore, or hospital can simply use an LBS, to display this information on the screen of mobile phone. Similarly, an individual seeking to buy a particular item can use the positioning system and information database to locate it. LBS can even cooperate with websites in providing enhanced information services.

2.2.2. NFC Embedded Phone in LBS Area

When a user with an NFC-embedded mobile phone enters a specific LBS area, their phone is detected by a 3G/4G mobile wireless network that transmits the user's location information to a server system, which replies in turn with that user's consumption history within a fixed distance. Based on the user's current location, the 3G/4G mobile wireless network can transmit SMS or map information to the user's NFC-embedded phone, and user data can be transmitted and extracted from a database DB server system.

An LBS area with a 3G/4G mobile wireless network is shown in Figure 5 and functions as follows.

NFC-embedded phone in specific LBS area.

Step 1. A user with an NFC-embedded mobile phone arrives in specific LBS area; their location information is sent to a base station.

Step 2. The base station relays the user's location information to a 3G/4G mobile wireless network.

Step 3. Using this location information, a back-end DB server system is used to extract more detailed user information.

Step 4. The more detailed user information is sent back to the base station.

Step 5. The 3G/4G mobile wireless network is connected to the NFC-embedded phone of the user through the base station.

3. M-Payment System

3.1. Typical M-Payment System

A typical m-payment system is shown schematically in Figure 6.

Typical m-payment system.

3.1.1. Customer

An m-payment customer must be a subscriber of a mobile network operator, which provides an NFC-enabled mobile phone with a compliant UICC a hardware-based secure identity. To facilitate NFC m-payment service, the customer enters a service agreement with a card issuing bank (CIB).

3.1.2. Merchant

The merchant or provider of the goods and services being purchased by the customer at the POS terminal has a contract with a merchant acquirer that allows the merchant to accept credit and debit payments that are then processed over an appropriate payment processing network. To enable m-payment, the merchant must be equipped with a contactless POS terminal based on the ISO 14443 standard.

3.1.3. Acquirer

The acquirer maintains the account that permits the merchant to accept credit and debit transactions. The acquirer also provides an interface to the processing network for authorization and clearing of the merchant's transactions.

3.1.4. Card Issuing Bank

The card issuing bank (CIB) provides overall payment services and is responsible for delivering associated customer care. The CIB is responsible for issuing payment applications and customer personalization data as well as for establishing the formal agreement with the customer for payment service that is undertaken prior to provisioning the UICC.

3.1.5. Payment Solutions Company

Payment solutions companies, for example, Visa, MasterCard, American Express, China UnionPay, and JCB, maintain payment networks, provide services such as approval and certification to associated banks, and define their own brand requirements for different payment form factors. They also define payment specifications and provide transaction processing services to support these.

3.1.6. Mobile Network Operator

The mobile network operator (MNO) is a key addition to this ecosystem that is essential for enabling m-payments. The role of the MNO is to

provide and maintain the network infrastructure that enables secure OTA delivery and maintenance of payment applications to a UICC smart card; provide the security domain for payment applications on the UICC, which is then controlled by the trusted service manager (TSM) or CIB; when required, provide the customer with NFC-enabled handsets and a required UICC smart card; provide mobile services customer care.

The MNO brings the assets of a mobile customer base along with a smart card and network infrastructure into the m-payment relationship.

3.1.7. Trusted Service Manager

The trusted service manager (TSM) is a new addition to the payment industry. This entity is primarily responsible for secure distribution, provisioning, and life-cycle management of m-payment applications and other NFC services to a mobile network operator’ subscriber base on behalf of service providers; as such, the TSM will have business relationships with both the mobile network operators and the service providers.

No significant change is anticipated to the payment transaction infrastructure and process described above. The role of the various players in this new ecosystem is briefly described below.

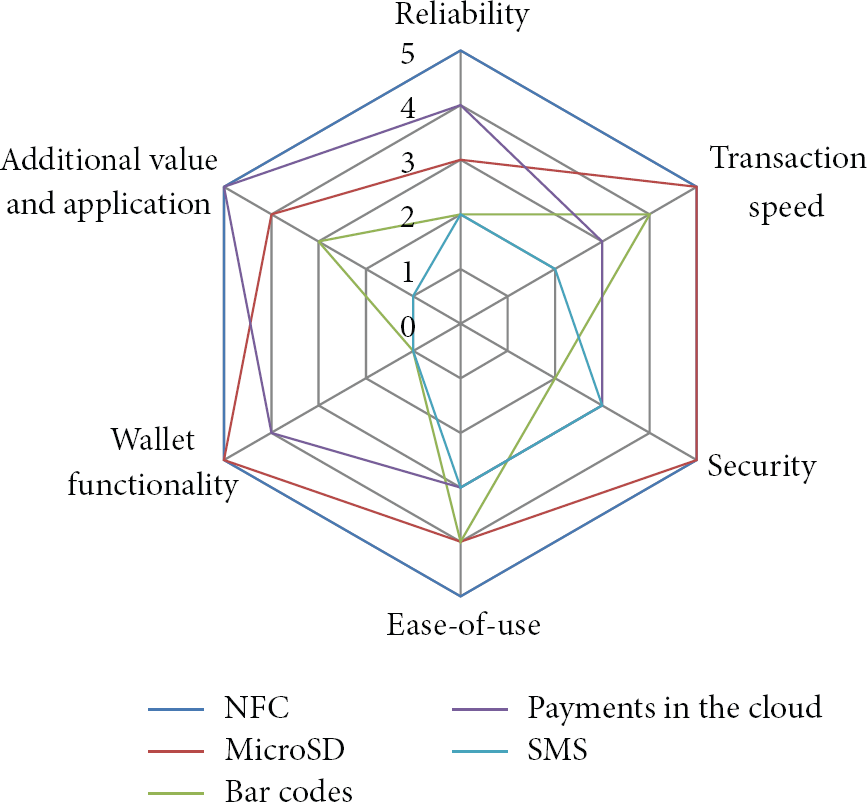

3.2. Comparative Evaluation of Approaches to M-Payment

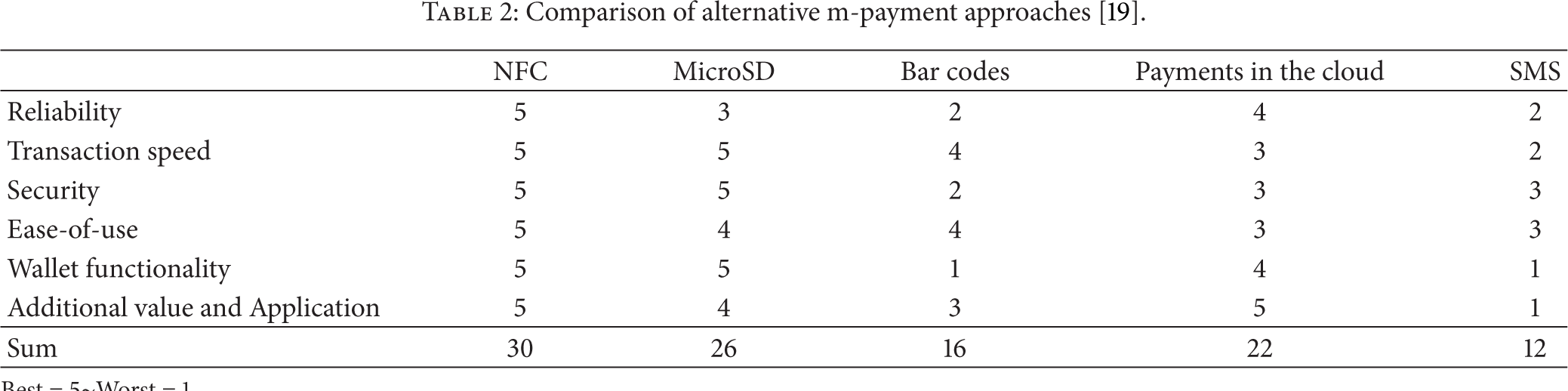

To evaluate various m-payment solutions, we compared NFC, MicroSD, Bar Codes, Payment in the Cloud, and SMS. Each solution was rated in terms of six evaluation criteria as 1~5, where 1 = worst and 5 = best. From these evaluation results, which are presented in Table 2 and Figure 7, it is seen that the NFC method is the best solution for m-payment.

Comparison of alternative m-payment approaches [19].

Best = 5~Worst = 1.

Comparison of alternative m-payment approaches.

3.3. Benefits of NFC M-Payments

The benefits of NFC mobile contactless payments include the following:

as handsets are more ubiquitous than credit cards, consumers are more likely to carry their phones than a traditional wallet or purse; the processing power of a handset supports a robust interface and the ability to integrate core payment functionality with other applications; the wallet interface can support value-added applications such as loyalty programs; payment credentials are stored in an integrated services environment (SE) and accessible through an application that can be protected by a passcode or other means; existing payment networks and the growing infrastructure for card-based contactless payments can be leveraged.

3.4. Basic NFC M-Payment Methods

There are two basic NFC m-payment methods, which are shown in Figure 8.

Methods for transacting basic NFC m-payment.

3.4.1. Card Based Payment Processing

In this payment transaction processing method, an NFC enabled mobile device is used to make card based (credit or debit) payments with an associated NFC enabled POS device. In this processing, the actual card details along with the pin details are stored in the mobile device NFC controller such as an NFC enabled smartcard. After a commercial transaction has been completed at an NFC enabled POS, subsequent payments can be made from an NFC mobile device, by bringing it into contact with the same POS. Upon contact, bill details are passed to the mobile device and users are able see the bill and press a button to make payment, while card details and pin are passed to the NFC enabled POS, which further processes the card information to complete the payment transaction. A payment transaction between the NFC POS and the payment gateway service provider then continues as in a normal payment scenario. Upon completion of payment processing, the NFC POS sends a payment confirmation message to the NFC mobile device, and the overall mobile transaction is closed.

3.4.2. Mobile Wallet (M-Wallet) Processing

In this method, an NFC enabled mobile device is used to make payments with an NFC enabled POS, through the user's mobile m-wallet account, which is used in of credit cards. The NFC enabled POS will present a bill to the user, who upon accepting it sends their m-wallet account details back to the NFC POS, which further interacts with the m-wallet account service provider to close the payment transaction. Upon successful payment processing, the NFC-POS sends a confirmation message to the mobile device and then the overall transaction is closed.

4. Proposition and Simulation

4.1. Proposed M-Payment System Using NFC Based on Specific LBS

The proposed M-payment system using NFC based on specific LBS is shown in Figure 9. A detailed description of the proposed system is as follows.

Proposed M-payment system using NFC based on specific LBS.

Step 1. An NFC embedded mobile phone user arrives in a specific LBS area (e.g., a sightseeing area, tourist market, shopping center, etc.) and the user's location information is sent a base station.

Step 2. The base station relays this location information to a 3G/4G mobile wireless network.

Step 3. Using the basic location information, a back-end DB server system is used to obtain more detailed local information.

Step 4. This more detailed local information and data (for instance, discount coupons that can be used in the specific LBS area) is sent via the 3G/4G mobile wireless network back to the base station.

Step 5. The base station then relays this enhanced information back to the NFC embedded mobile phone for downloading.

Step 6. If user goes to a shop within the LBS area the NFC embedded phone can read the NFC tags of products that attracts the user's attention transmit simple product information such as price and brand that has been embedded the NFC tag.

Step 7. After the user has selected a payment method, the NFC embedded mobile phone sends the product information, discount coupon, and payment method to the NFC reader of the POS system.

Step 8. The POS system sends the request and selected payment method to the financial network system for processing.

Step 9. The financial network system sends an authentication through the 3G/4G mobile wireless network. After confirmation of the authentication, the selected payment method is processed.

Step 10. The financial network system sends user payment method information to the POS system.

Step 11. The NFC embedded mobile phone payment is closed and the user obtains the desired product. The overall transaction is closed.

Step 12. The POS system sends the payment information phone back to the financial network back-end DB system and creates a purchase record.

4.2. Simulation and Analysis

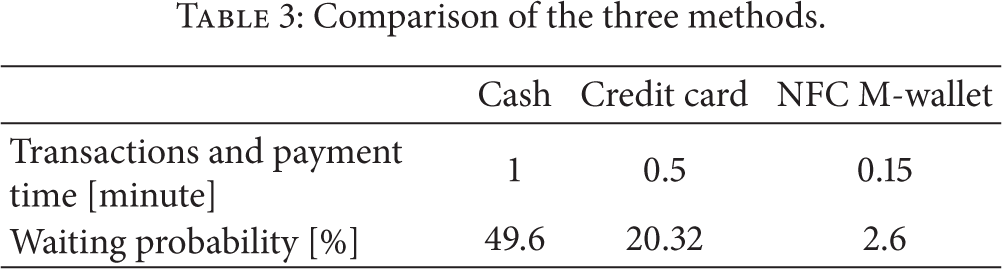

In Figure 9, if, up to 100 people (payer) came in shop during 1 hour (60 minute) and payer have make a transaction and payment with the three methods (cash, credit card, and NFC M-Wallet) to payee. Two more payers in counter are waited in line during 1 minute. Using three methods, usually transactions and payment time per 1 payer is shown Table 3. This is a Poisson distribution, (1), (2), and waited probability of payer in line is (3):

Comparison of the three methods.

The waited probability of payer in line is the same as Figure 10 and Table 3. As a result, to use proposed model, we confirmed that the more people come to the shop, the faster NFC M-wallet method is a transactions and payment method.

Waited probability of payer in line (x-axis: payer, y-axis: waited probability).

5. Conclusion

In WSN systems, with advancement of mobile communication and information technology, especially, mobile commerce (m-commerce) allowed users to conduct business and service transactions over portable mobile phone. This trend was amplified by the NFC technology and demand and supply of the mobile phone (Smart phone); it was NFC embedded phone. NFC technology is a standards-based wireless communication technology that allows data to be exchanged between devices (RFID Tag, Reader) located a few centimeters apart.

In this paper, an m-commerce process for an NFC-based mobile environment in specific LBS area was proposed. In doing so, several aspects of m-commerce were examined as follows:

NFC, LBS, and m-payment systems were investigated; the benefits of NFC m-payments were demonstrated through a comparison of various m-payment solutions; an m-payment system using NFC and based on LBS for m-commerce over a WSN was proposed; as a simulation result, to use proposed model, we confirmed that the more people come to the shop, the faster NFC M-wallet method is a transactions and payment method.

In developing the proposed pass through system, we demonstrated a method that can leverage the diffusion of NFC-embedded mobile phones and the development of WSN to deliver enhanced mobile solutions for loyalty and enable m-payments using NFC technology. In future studies, we will be investigating a hybrid NFC-cloud m-payment system, for use in a cloud environment.

Footnotes

Conflict of Interests

The authors declare that there is no conflict of interests regarding the publication of this paper.

Acknowledgments

This research was supported by Basic Science Research Program through the National Research Foundation of Korea (NRF) funded by the Ministry of Education (NRF-2009-0093828). And this research was supported partially by the MSIP (Ministry of Science, ICT, and Future Planning), Korea, under the C-ITRC (Convergence Information Technology Research Centre) Support Program (NIPA-2013-H0401-13-2006) supervised by the NIPA (National IT Industry Promotion Agency).