Abstract

Following the Internet, the Internet of Things (IoT) becomes a prime vehicle for supporting auction. The use of market mechanisms to solve computer science problems is gaining significant traction. More and more clues show that the bidders tend to be risk-averse ones. However, traditional nonparametric approach is only applicable for the case of risk neutrality in a centralized server. This study proposes a generalized nonparametric structural estimation procedure for the first-price auctions in the distributed sensor networks. To evaluate the performance of the aggregated parameter estimators, extensive Monte Carlo simulation experiments are conducted for ten different values of risk aversion parameters including the risk neutrality case in multiple classic scenes. Moreover, in order to improve the usability of the aggregated parameter estimators, some guidance is also given for real-world applications.

1. Introduction

Auctions are suggested as a basic pricing mechanism for setting prices for access to shared resources, including bandwidth sharing in wireless sensor networks (WSNs) [1]. Following the Internet, the Internet of Things (IoT) [2, 3] becomes a prime vehicle for supporting auction [4]. Moreover, the use of market mechanisms to solve computer science problems such as resource sharing [1, 5, 6], load awareness [7], task allocation [8], and network routing [9–11], is gaining significant traction.

In addition to the real-time concerns associated with auctions in distributed sensor networks (DSNs), privacy concerns are also very important [12–15]. Therefore, many protocols are proposed in the literature. For example, the protocol for a sealed-bid auction proposed by Franklin and Reiter [12] uses a set of distributed auctioneers and features an innovative primitive called verifiable signature-sharing. Recently, Lee et al. [14] put forward an efficient multiround anonymous auction protocol. When there are more than one party bidding the same highest price for auctioned objects, the protocol picks out the bidders offering the same highest price in the first round to the next round.

Risk aversion is used to explain the advertisers' behavior under uncertainty. The auction model and the optimal mechanism design for risk-averse bidders have been studied by [16–18]. Within the private value paradigm, risk-averse bidders tend to shade less their private values relative to the risk neutral case, which often results in some overbidding [19]. More and more clues show that the bidders indeed tend to be risk-averse ones [20–22].

In recent years, in order to gain some insight from auction data, structural approaches, pioneered by Paarsch [23], have attracted extensive attention. Some of them rely upon a parametric specification of the bidders' private values distribution, for example, the piecewise pseudomaximum likelihood estimation (PPMLE) approach [24, 25]. Laffont et al. [26] have proposed a simulated nonlinear least square estimation method, which allows general parametric specifications. However, all of the methods rely on some assumption on parametric structures.

Without any parametric assumptions, Guerre et al. [27] have presented a computationally convenient nonparametric estimation procedure. But it is only applicable for the case of risk neutrality. Therefore, it cannot explain the agents' behavior very well. To overcome this problem, this paper generalizes nonparametric estimation procedure, so that it can be applicable for risk aversion in the first-price auction. Our previous work restricts us to a special case only with two different numbers of bidders [28] or to a centralized server [29], but in this study we lose these restriction to distributed sensor networks.

The rest of the paper is organized as follows. After the risk-averse model for first-price auction with independent private value is briefly introduced in Section 2, a generalized distributed nonparametric estimation procedure is proposed for sensor networks in Section 3. In Section 4, extensive Monte Carlo simulation experiments are conducted, and Section 5 concludes this work.

2. Preliminary: Risk-Averse Model

A single and indivisible object

The Schematic diagram for auction model.

In this paper, the private value paradigm is considered, where every bidder has a private value

Intuitively, every bidder is potentially risk-averse with a von Neuman Morgensten utility function

Let

The first-order condition for maximizing expected utility can be written as

Additionally,

Let

3. Risk Aversion Parameter Estimation

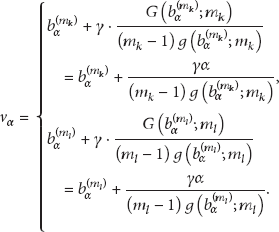

3.1. Meta-Parameter Estimators

As suggestions by Campo et al. [22], let

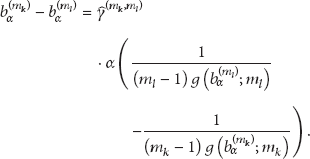

Through simple arithmetic operations on (6), one can obtain the following estimator

On closer examination on (7), it is very surprising that

Since these estimators cannot utilize the global information, but only local information, they are named meta-parameter estimators in the work. In the next subsection, some weighted combinations of all meta-parameter estimators, called aggregated parameter estimators, will be introduced. These aggregated parameter estimators will be more helpful for the real-world applications.

3.2. Aggregated Parameter Estimators

It is very important to choose a proper estimator for risk aversion parameter in the real-world applications. But which one is better? Intuitively, it seems that some (weighted) combinations of all meta-parameter estimators in Section 3.1 may be appealing.

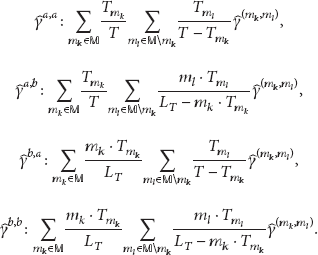

In this study, two-level combinations are considered. Specially, for any

Inner weights for aggregated parameter estimators.

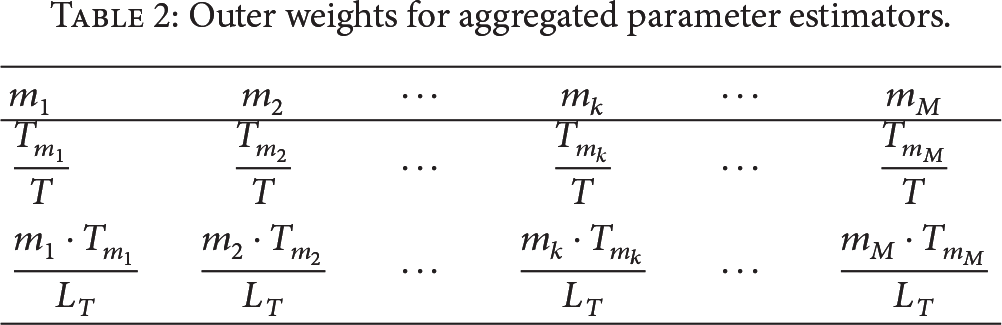

Outer weights for aggregated parameter estimators.

Now there are only four aggregated estimators for risk aversion parameters for users to choose from. However, in fact, there is no apparent reason to prefer one estimator to another, and many factors may influence one's choice: such as, auctions' number and the number of bidders.

In this situation, Monte Carlo simulations and methods [30, 31] can be utilized to examine the performance of each estimator. Please see Section 4 for more details. But before this, the next subsection will describe in detail the parameter estimation procedure in the distributed sensor networks.

3.3. Distributed Parameter Estimation Procedure

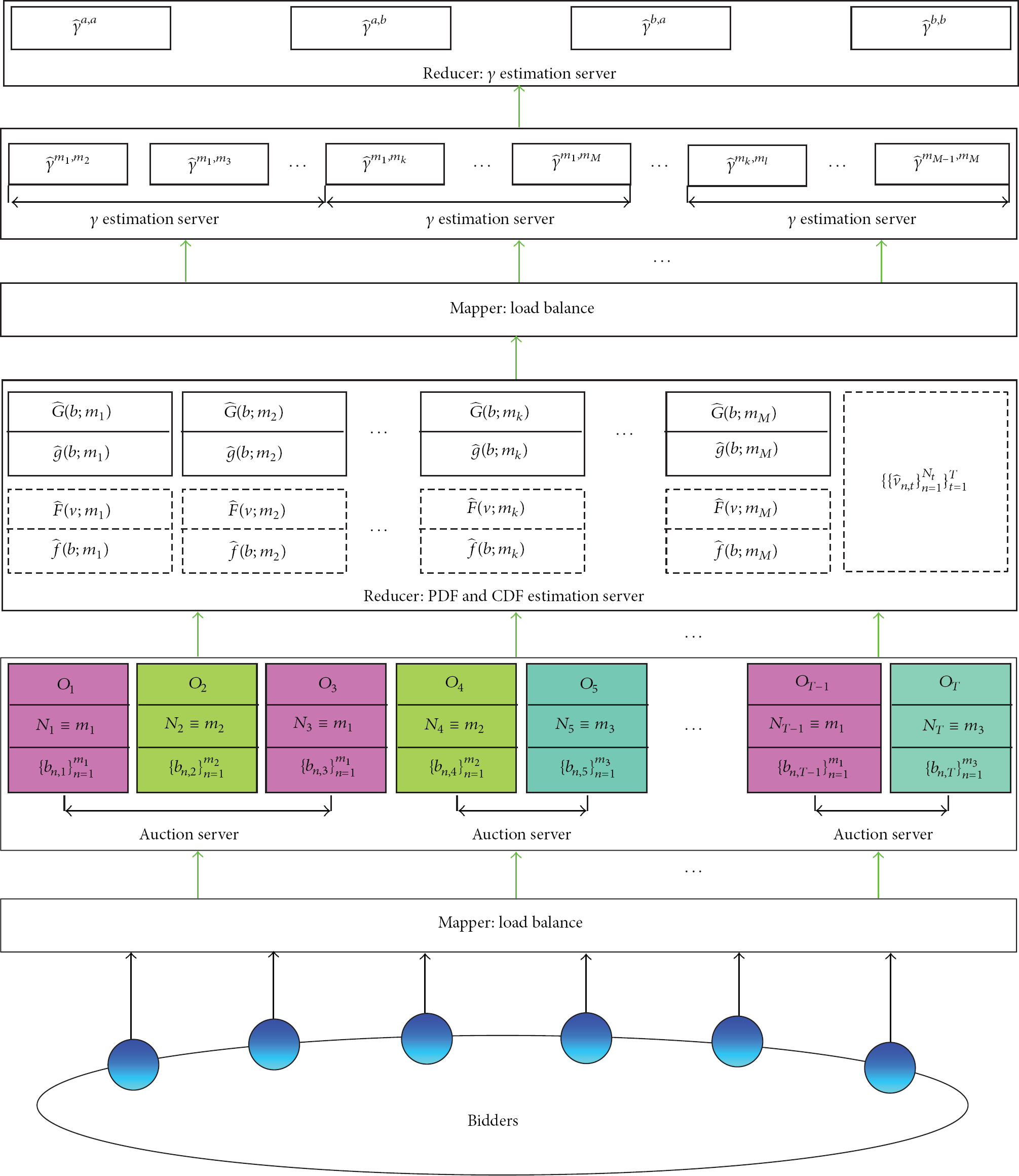

Our distributed parameter estimation procedure is inspired by MapReduce [32, 33], a programming model for processing large data sets with a distributed algorithm on a cluster. The schematic diagram for our procedure is shown in Figure 2. In fact, two-hierarchical Mapper-Reducer structure is adopted in our estimation procedure. More specifically, the whole estimation procedure is summarized as follows.

The schematic diagram for distributed risk aversion parameter estimation.

Step 1.

Each bidder with a sensor prepares his/her bid price for each of interested auctioned objects. And then he/she submits his secrete bid price and ID to Mapper server through distributed sensor networks, whose ID was assigned by an auctioneer.

Step 2.

The Mapper server will decide to transfer the corresponding bid prices and IDs to different auction server. Usually, auctioned objects will be divided into several groups and deployed in different auction servers.

Step 3.

At the end of auctions, each of auctioned objects will receive different number of bidders. In Figure 2, auction servers with the same color mean the same number of bidders. Now, auction servers will transfer all bids to PDF & CDF estimation server.

Step 4.

The PDF & CDF estimation server will estimate the

Step 4 .1. To estimate

Step 4.2. To estimate

Step 4.3. To estimate

It is worth noting that Steps 4.2 and 4.3 are optional. If one does not want to estimate them, he/she can just skip these two steps. That is why they are shown by dotted boxes in Figure 2.

Step 5.

The estimated values for

Step 6.

Another Reducer will calculate the four aggregated parameter estimators according by (8).

4. Experimental Design and Discussions

In order to evaluate the performance of all estimators, extensive Monte Carlo experiments are conducted in this section.

4.1. Experimental Design

In all the simulation experiments, the private costs are drawn from a uniform distribution on

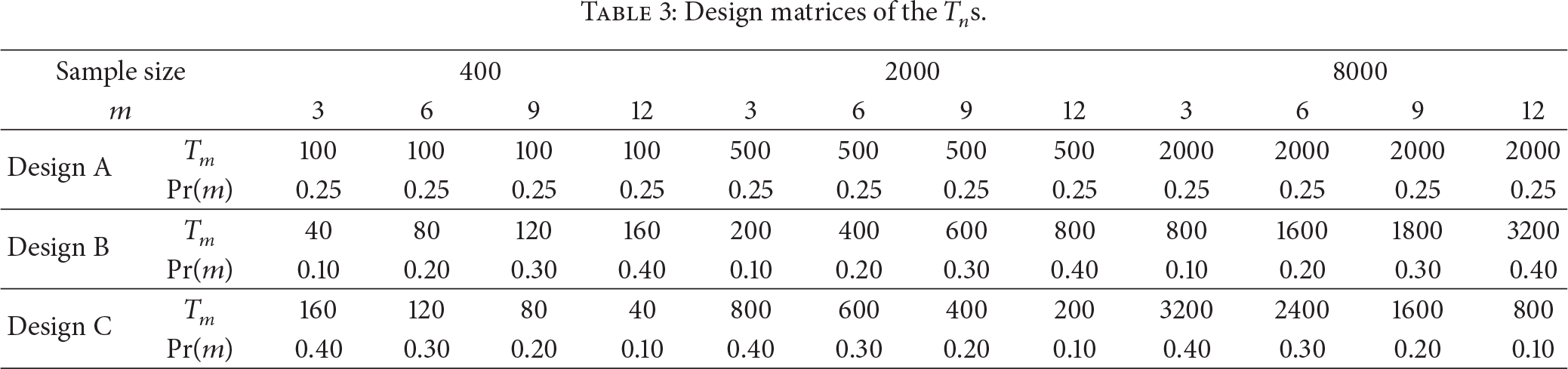

In order to simulate the real auction data as closely as possible, the experiment considers three kinds of sample sizes T: 400, 2000, and 8000, which corresponds to small, median, and large sample, respectively. In each of these samples, the number of bidder

Design matrices of the

Specifically, we first generate randomly private valuations for different designs from the uniform distribution. We then compute numerically bids using (4) with different values for γ. Note that the random numbers for the experiments are generated using the multiplicative congruential method with modulus

In our experiments, let

4.2. Results and Discussions

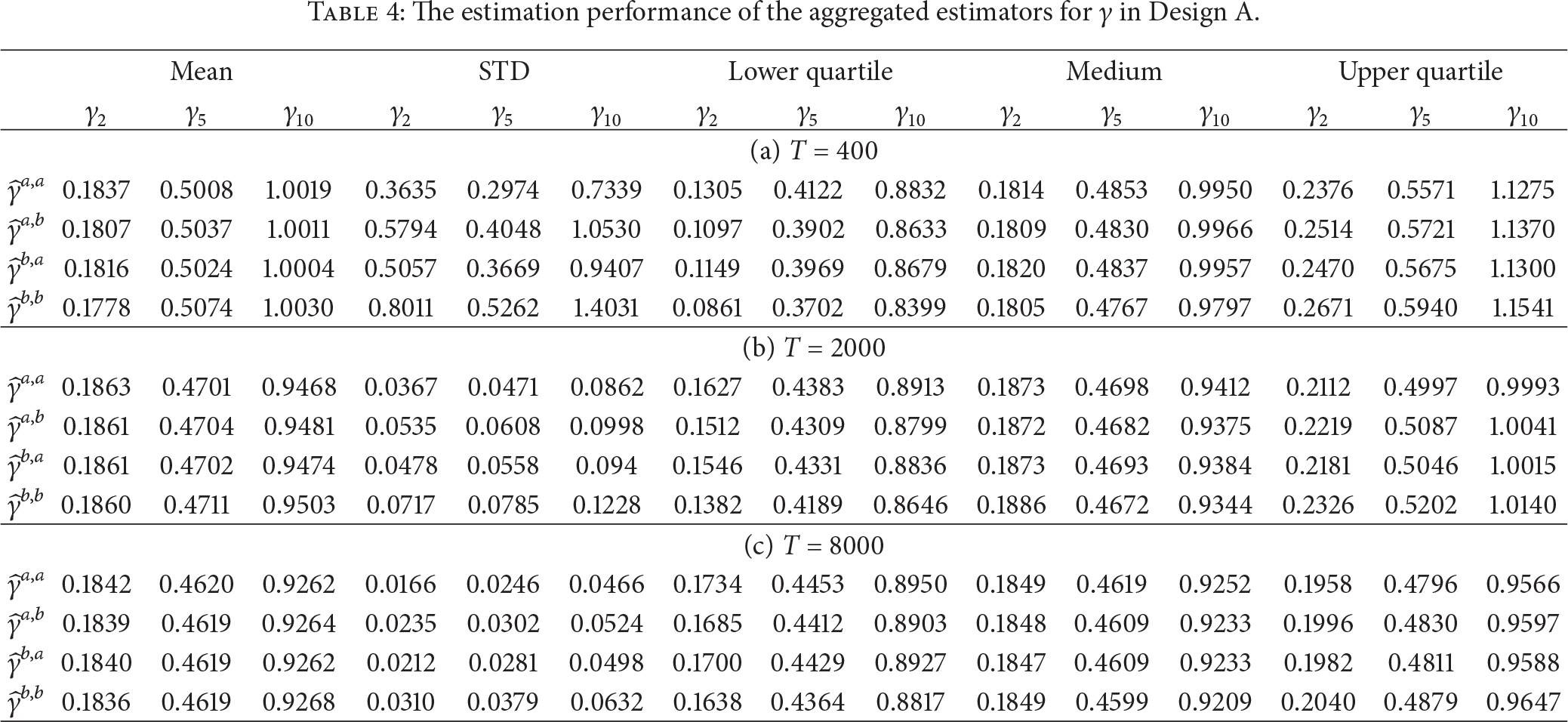

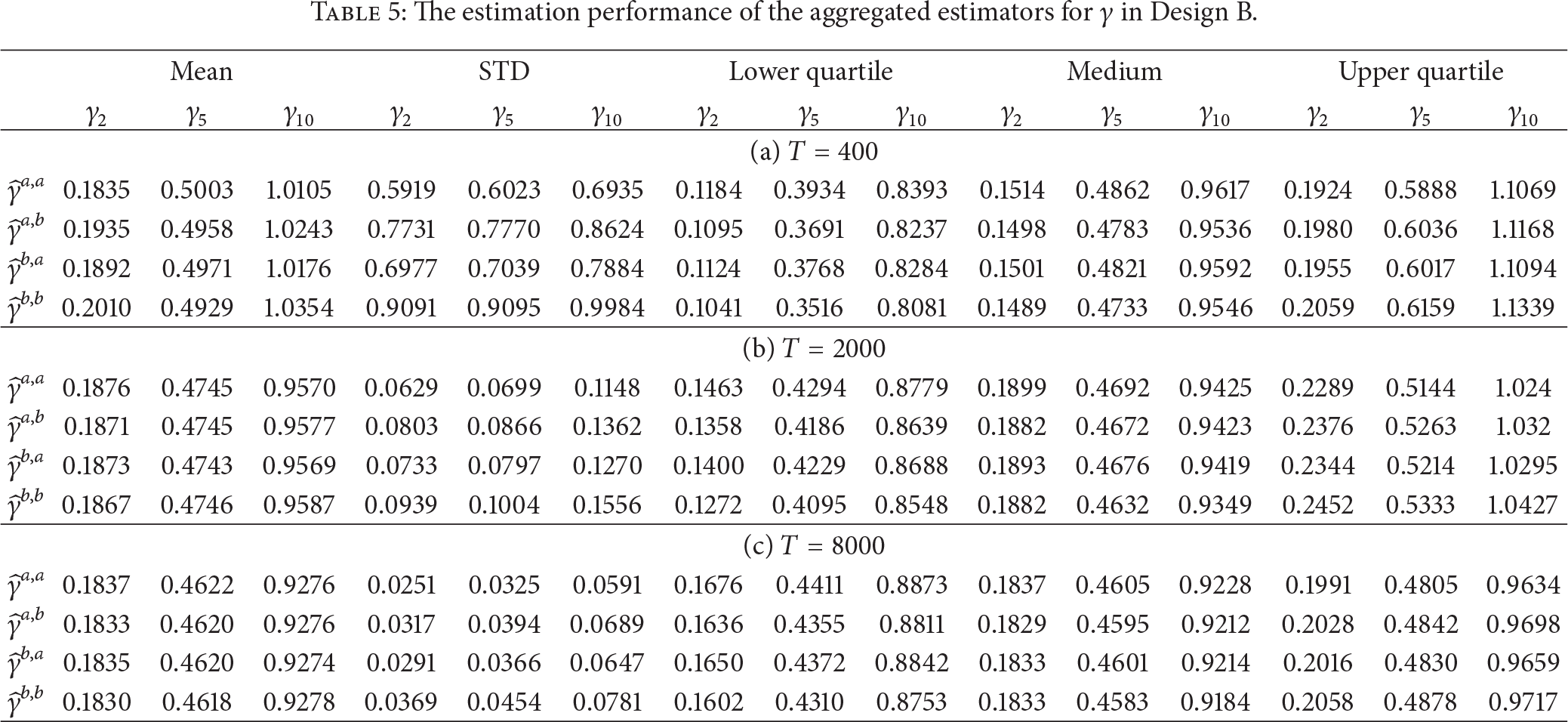

From (7), it is not difficult to see that the percentile α may influence the estimation performance for the risk aversion parameter γ. In order to minimize the influence α on the estimators, the percentile α is optimized to select

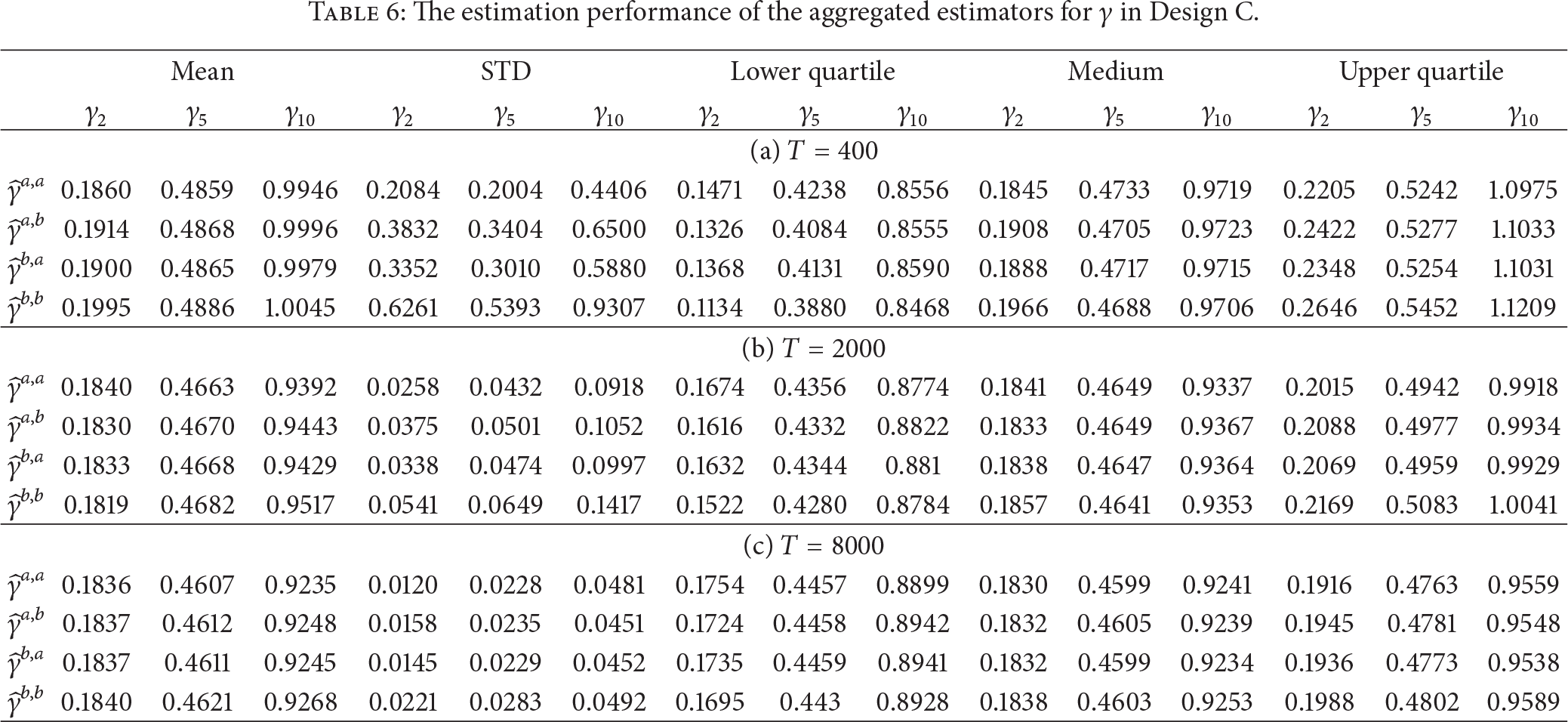

Tables 4, 5, and 6 report the estimation performance of the aggregated estimators for risk aversion parameter

The estimation performance of the aggregated estimators for γ in Design A.

The estimation performance of the aggregated estimators for γ in Design B.

The estimation performance of the aggregated estimators for γ in Design C.

In order to improve usability of these aggregated estimators, Table 8 gives some useful suggestions based on

To evaluate further the goodness of fit of the distributed risk aversion parameter estimation procedure, we also calculate the 2-norm between the estimated private valuations (5) and actual ones, defined formally as

The 2-norm between the estimated and actual private values.

The guidance on choice of the aggregated estimators.

5. Conclusions

Auctions are suggested as a basic pricing mechanism for setting prices for access to shared resources, including bandwidth sharing in wireless sensor networks (WSNs). Following the Internet, the Internet of Things (IoT) becomes a prime vehicle for supporting auction.

More and More clues show that the bidders tend to be risk-averse ones. However, traditional nonparametric approach is only applicable for the case of risk neutrality in a centralized server. In this paper, A generalized nonparametric structural estimation procedure is proposed for the first-price auctions in distributed sensor networks. In order to evaluate the performance, extensive Monte Carlo simulation experiments are conducted for ten different values of γ including the risk-neutral case in multiple classic scenes. Though there are no unique estimators for risk aversion parameter, four aggregated parameter estimators are obtained and some guidance is also given for real-world applications.

Similarly, our previous work on PPMLE [25] is also extended to distributed sensor networks. Additionally, if our distributed parameter estimation procedure is equipped with localization technologies [35–38], it can be utilized in more mobile situations.

Footnotes

Conflict of Interests

The authors declare that there is no conflict of interests regarding the publication of this paper.

Acknowledgments

This work was funded partially by Fundamental Research Funds for the Central Universities: Research on Entrepreneurial Mechanism, Clusters and Organizing Mechanism of Peasants in Forest Zone under Grant no JGTD2013-04, Beijing Forestry University Young Scientist Fund: Research on Econometric Methods of Auction with their Applications in the Circulation of Collective Forest Right under Grant no BLX2011028 and Key Technologies R&D Program of Chinese 12th Five-Year Plan (2011–2015): Key Technologies Researcher on Large Scale Semantic Computation for Foreign Scientific & Technical Knowledge Organization System, and Key Technologies Research on Data Mining from the Multiple Electric Vehicle Information Sources under Grant no 2011BAH10B04 and 2013BAG06B01, respectively. Our gratitude also goes to the anonymous reviewers for their valuable comments.