Abstract

The study of time‐inconsistent decision‐making, in particular present bias, has greatly influenced the field of behavioral economics over the last two decades. Moreover, it has resulted in the design and implementation of widely used incentive schemes for various important applications. However, the effect of present bias on decision‐making for operational problems has been studied less. This work considers the effect of present bias in a simple scheduling system that requires decisions about project timing and sequencing. We design algorithms that enable optimization of revenue less cost under present bias for both naive and sophisticated (i.e., self‐aware) decision‐makers. We describe managerial insights about the relative performance of time‐consistent, naive, and sophisticated decision‐makers, and how to mitigate the effects of present bias. Both theoretical and computational results support these insights.

INTRODUCTION

The study of intertemporal preferences in decision‐making originates from the work of Phelps and Pollak (1968). Under intertemporal preferences, a decision‐maker views the same trade‐off differently at different times. Akerlof (1991) uses this concept to explain recurring procrastination as a result of greater salience for present costs or rewards than for future ones, that is, present bias. He discusses applications to purchasing, savings, gang behavior, and politics. Laibson (1994) presents a model that unifies conventional time‐consistent discounting and present bias. As discussed in Section 2, present bias has been the subject of several empirical studies within behavioral economics.

O'Donoghue and Rabin (1999a) distinguish naive decision‐makers who make decisions under the incorrect assumption that their future decisions will be time‐consistent from sophisticated decision‐makers who are aware of their future bias. In the context of a principal–agent model with asymmetric information, O'Donoghue and Rabin (1999b) design incentives for time‐inconsistent procrastinating agents. O'Donoghue and Rabin (2001) study a multiperiod model where a decision‐maker chooses a unit‐length task to process. The authors show that, due to present bias, an attractive new option can cause a decision‐maker to switch from doing something beneficial to doing nothing. They further show that a decision‐maker may procrastinate more to pursue important goals than unimportant ones. Thaler and Benartzi (2004) propose an employer‐supported savings plan, Save More Tomorrow

The study of time‐inconsistent preferences has received limited but increasing attention within the operations management literature. Su (2009) considers a problem where consumers delay purchases in situations where an immediate purchase is a rational choice. Such a delay is attributed to present bias in a situation when payment is immediate, and consumption is delayed. Plambeck and Wang (2013) compare charging options for a service with immediate costs and conclude that subscription charging is optimal. Gao et al. (2014) describe an optimal dynamic pricing policy for a manufacturer selling to customers with time‐inconsistent preferences. Li et al. (2017) consider an environment that evolves stochastically, for which an optimal stopping policy is needed. A naive decision‐maker follows a threshold stopping policy, and a sophisticated agent also does so if revenues are immediate. Kouvelis et al. (2018) address time inconsistency in a joint inventory and financial hedging problem in the mean‐variance framework, where in each period a firm perceives a greater variability of the terminal wealth than the anticipated variability in a future period. Liao and Chen (2021) design a long‐term conditional cash transfer program to encourage healthy habits assuming people's present‐biased preferences. Li and Jiang (2022) study the influence of present bias on the pricing strategies of two competing firms that sell quality‐differentiated products. Shi et al. (2022) demonstrate computationally that a considerable amount of project delay can be explained by present bias and design an incentive scheme that mitigates it. Zhang et al. (2022) investigate consumers' present bias in digital content consumption and their strategic self‐control manners. In contrast with the above works, we consider decisions under present bias over both sequencing and timing decisions.

Closest to our application is the work of Wu et al. (2014), who consider a two‐period model of a simple project without task precedence structure and with either a single worker or a team of workers. The effect of present bias is to reduce the work rate in the first period, which backloads work into the second period. A possible solution is to increase rewards for work that is completed in the first period. Our work differs from Wu et al. (2014) in two ways. First, we consider the effect of present bias on decisions that affect individual projects rather than an aggregate work rate. Second, we distinguish between decisions made by naive time‐inconsistent decision‐makers and those made by their sophisticated counterparts.

More generally, our study of present bias differs from all the above works in several ways. First, we consider both timing and sequencing decisions over multiple projects. Second, because we consider a sequence of many projects, we model the effect of present bias as it evolves sequentially based on previous decisions. Third, we examine trade‐offs that arise between revenues and costs when the timing of both is altered by present bias. Fourth, we allow the level of present bias in decision‐making to change over time.

There are many heuristic algorithms designed for the scheduling of projects, but these algorithms are primarily designed to alleviate the issue of computational intractability. By contrast, present bias exists for decisions over many problems, including those which are not computationally intractable. We observe that the number of projects to process is typically small for the behavioral decision‐making environments studied in the literature. Our objective in this work is not to investigate optimization and approximation in the scheduling of projects from an algorithmic perspective, since there are many published works on this topic. Rather, our focus is on a more general question: how present bias, as modeled by a present bias coefficient and a level of self‐awareness of the bias, affects decisions in scheduling of projects and how to mitigate biases in such decisions.

We summarize the contributions of our work. We introduce present bias into a simple scheduling system that requires project timing and sequencing decisions by a project company. We consider situations where cost is immediate and revenue occurs at project completion and the opposite case. For both timing and sequencing decisions, we design algorithms that enable optimization of revenue less cost under present bias for naive and sophisticated decision‐makers. Based on this analysis, we describe managerial insights about the relative performance of time‐consistent, naive, and sophisticated decision‐makers, and how to mitigate the effects of present bias. Both theoretical and computational results support these insights. Applications of these insights are broad from understanding the efficiency of individual projects to influencing the design of project portfolios by managers.

This paper is organized as follows. Section 2 provides our notation and develops and contrasts time‐consistent and time‐inconsistent models for minimizing project scheduling costs. Section 3 studies the effect of present bias on timing decisions in scheduling. Sequencing decisions are similarly studied in Section 4. We provide a summary, general insights, and suggestions for future work in Section 5.

NOTATION AND MODELS

Consider a project management company that schedules projects

A schedule σ is defined by the starting time

Since we consider decisions involving revenue and cost at different times, to capture the time value of money, we consider a discrete discount rate r. Evaluated at time 0, a revenue v earned at time t has a present value of

We now formally define present bias in our timing and sequencing decisions. To model the decision‐maker's present bias level, we introduce a present bias coefficient

The present bias coefficient β, without distinguishing its time of occurrence and hence with subscript t omitted, has been subject to extensive empirical research within the behavioral economics literature. Existing works provide several empirical estimates of β, for example, 0.40 (Paserman, 2008), 0.78 (Meier & Sprenger, 2015), 0.82 (Kaur et al., 2015), 0.61 (Ericson, 2017), and 0.83 (Augenblick & Rabin, 2019). Examining 220 estimates of the present‐bias parameter from 28 papers, Imai et al. (2021) find that those estimates vary considerably across studies, due primarily to the different characteristics of their applications.

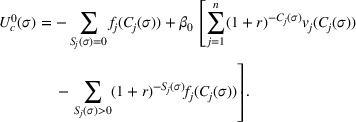

With present bias and immediate costs, for a given schedule σ, at time zero, the decision‐maker's intertemporal profit is

Alternatively, with present bias and immediate revenues, for a given schedule σ, the decision‐maker's intertemporal profit at time zero is

In both (1) and (2), parameter β0,

A time‐inconsistent decision‐maker with

For a naif, even knowing time‐consistent decisions does not necessarily lead to implementing such decisions. At period t, decisions are determined that should be implemented at periods

As mentioned above, the concepts of naivety and sophistication used in our work closely follow the literature of behavioral economics; however, they can also be interpreted in a more general context. The naive decision‐maker is naive only about the present bias that affects their decision‐making, and their cognitive ability is not affected. Therefore, it is reasonable for them to assume that they will make a fully rational decision in the future. Such behavior is commonly observed in situations of repeated procrastination, such as, “I will quit smoking tomorrow” or “I will start saving for retirement next year” (O'Donoghue & Rabin, 2015). Observe that, in such situations, the procrastinating behavior does not reduce the decision‐maker's understanding of what constitutes positive behavior.

On the other hand, the sophisticate's awareness of their present bias does not enable them to correct it. O'Donoghue and Rabin (2002) describe their solutions as playing a game against their future selves. Thus, their behavior partly reflects negative behavior by their future selves, which they cannot control, and partly reflects attempts to induce positive behavior from their future selves. An example would be delaying the opening of a food or drink item due to an awareness of one's tendency to finish it immediately once opened. Various practical situations related to addictions exemplify this. Observe that, in such situations, the decision‐maker's awareness of their addiction does not by itself eliminate the addiction.

TIMING DECISIONS

Time‐consistent decisions

We illustrate the timing decisions of a time‐consistent decision‐maker (TC). We assume the planning horizon is from 0 to T. Consistent with the classical scheduling literature, the time horizon [0, T] is discretized, where a decision can only be made at integer time points. For feasibility of scheduling all projects, we assume the total processing time of all projects,

For the case with immediate costs, the time‐consistent decision‐making problem can be solved by the following dynamic program.

Algorithm time consistent for timing (TCT)

Input

Given T, r,

Value function

Boundary condition

Optimal solution value

Recurrence relation

Also, for the case with immediate revenues, the time‐consistent decision‐making problem can be solved by a similar algorithm. The only change is that the second alternative in the recurrence relation becomes

Time‐inconsistent decisions

We consider time‐inconsistent decisions with immediate costs and revenues at project completion in Section 3.2.1 and with immediate revenues and costs at project completion in Section 3.2.2.

Immediate costs

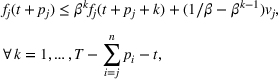

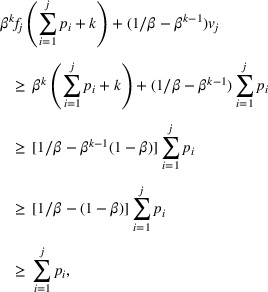

We consider a naif or sophisticate's timing decisions for multiple projects with immediate costs. Recall that a naif assumes in the future he will make time‐consistent decisions. The value of a naif's timing decision is defined by the function

Algorithm naive immediate costs for timing (NICT)

Value function

Boundary condition

Recurrence relation

Due to present bias in decision‐making, a naif may procrastinate project processing. Consider the following example. The time horizon is

For Example 1, the TC's profits characterized by function

TC's values in Example 1

The naif's profits defined by function

Naif's perceived values in Example 1

We next consider a sophisticate.

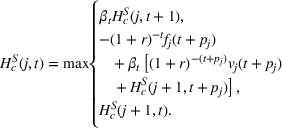

Algorithm sophisticated immediate costs for timing (SICT)

Value function

Boundary condition

Recurrence relation

For a TC, the perceived profit is equal to the realized profit if he follows Algorithm TCT's decisions. For a sophisticate, the scheduling decisions he plans are the same as he later implements. The true net profit from the schedule, as adjusted by present bias, equals the sophisticate's perceived profit when he makes his scheduling decisions. However, this is not the case for a naif because a naif's anticipated future decisions may not match the actual decisions he will make in the future.

The sophisticate's profits defined by function

Sophisticate's values in Example 1

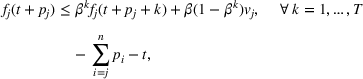

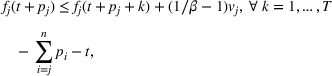

From Example 1, procrastination of project processing has different impacts on the naif's and sophisticate's intertemporal profits. This example illustrates how, with immediate costs, regular scheduling costs, and reasonably large project values, a naif procrastinates more than a sophisticate. We have the following related result. Consider projects with immediate costs, namely projects If project j is not rejected, and If project j is not rejected, and

Note that project j can only be feasibly processed with starting time Next, consider a sophisticate's decision. Suppose a sophisticate is idle from t to

For a TC, a regular scheduling cost is sufficient to prevent any procrastination of project processing. For a naif, to eliminate procrastination, a stronger condition on scheduling cost is needed, as specified by condition (9); that is, the present scheduling cost needs to be no more than the future scheduling cost adjusted by the present bias coefficient. For a sophisticate, project revenues play a role in scheduling decisions, as characterized by condition (10). Intuitively, when a project's revenue is sufficiently large relative to its cost, it is not procrastinated by a sophisticate.

Immediate revenues

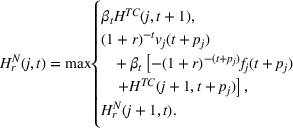

Algorithm naive immediate revenues for timing (NIRT)

Value function

Boundary condition

Recurrence relation

To show how present bias can affect a decision‐maker's choice, consider the following example where the scheduling cost is linearly decreasing in the project completion time. Such a cost structure applies when projects have specific due dates, and earliness costs occur when a project is completed before its due date (Garey et al., 1988). The scheduling cost is

For Example 2, the TC's profits defined by function

TC's values in Example 2

The naif's profits defined by function

Naif's perceived values in Example 2

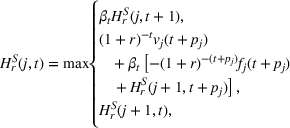

Similarly, a sophisticate's timing decision over multiple projects on a single facility can be characterized by the function

Algorithm sophisticated immediate revenues for timing (SIRT)

Value function

Boundary condition

Recurrence relation

For Example 2, a sophisticate's profit defined by

Sophisticate's values in Example 2

Example 2 demonstrates that with immediate revenues, project processing can be preproperated by a decision‐maker with present bias. We next characterize conditions under which procrastination of project processing is unnecessary with immediate revenues. In a situation with immediate revenues, consider projects If project j is not rejected, and If project j is not rejected, and

Project j can only feasibly start at times Now, consider a sophisticate's decision. Suppose a sophisticate starts a project j at time

Observe that condition (15) is weaker than regularity of scheduling cost. Therefore, with regular scheduling costs and without rejection, a naif's timing decision is the same as that of a TC, where no idle time occurs between processing any two projects. However, with general scheduling costs, a naif may process projects too early due to present bias. For a sophisticate, condition (16) is weaker than condition (10) in Proposition 1. Therefore, for a sophisticate, a smaller project revenue can lead to earlier processing of a project with immediate revenues compared to the situation with immediate costs.

Managerial insights for timing decisions

We investigate how present bias affects a naif and a sophisticate's timing decision with scheduling cost defined as If with immediate costs, either a naif or a sophisticate may procrastinate project processing; with immediate revenues, a naif processes his projects without inserted idle time; but a sophisticate may procrastinate. However, if

Part (i) follows from Example 1. For part (ii), with immediate revenues, a naif will not procrastinate, as shown by Remark 2. For a sophisticate, consider an example with present bias coefficient Now, consider the case where If some projects among

Theorem 1 shows that immediate revenues can help prevent procrastination for the timing problem. We observe that the cost function

The number of projects is fixed at

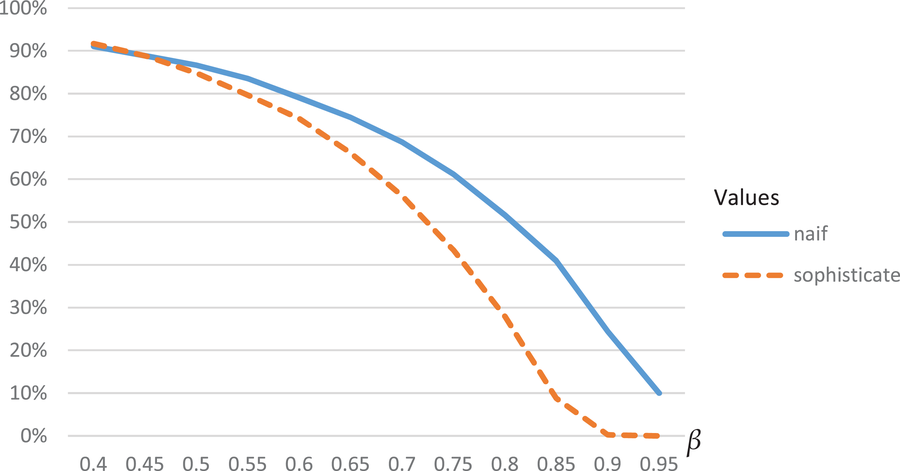

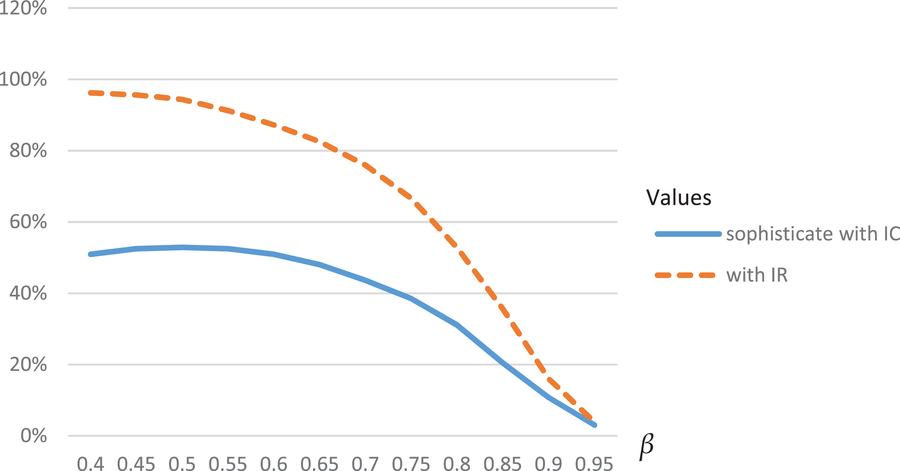

We observe that the profit loss from present bias can result from both procrastination and overrejection. To separate these two effects, we consider procrastination and rejection separately, by first assuming that all projects are contractually required. In the following, each figure is based on results from all the instances. That is, for the value of one parameter under study (e.g., β in Figure 1), we use the average from instances with all the values of other parameters (e.g., α and t for Figure 1). First, we require all the projects to be processed and obtain results in Figures 1–3. Figure 1 shows that, as expected, a higher degree of present bias represented by smaller values of β causes a more significant loss of profit. Also, a naif incurs greater profit loss than a sophisticate; interestingly, this difference increases with β when β is relatively small but decreases with β when β is relatively large.

Percentage of profit loss by procrastination as a function of β

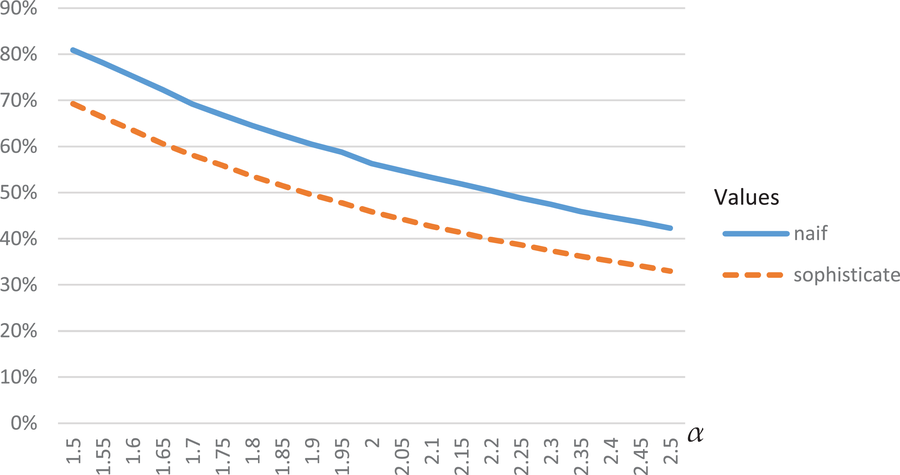

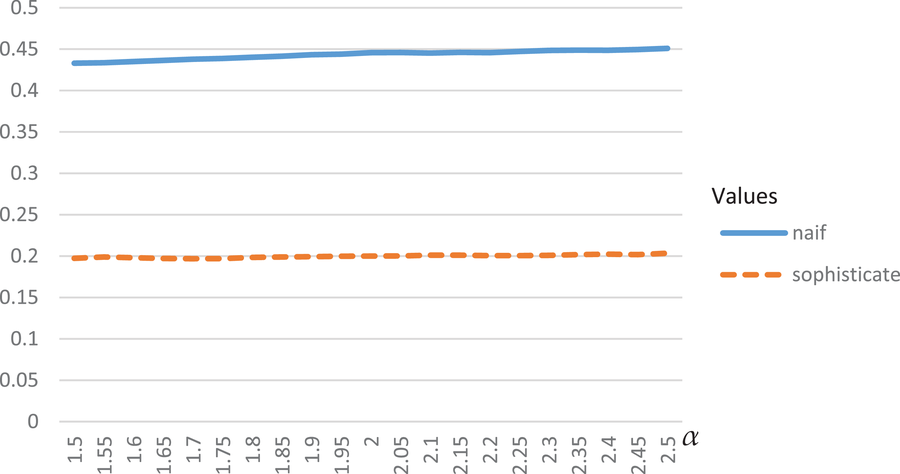

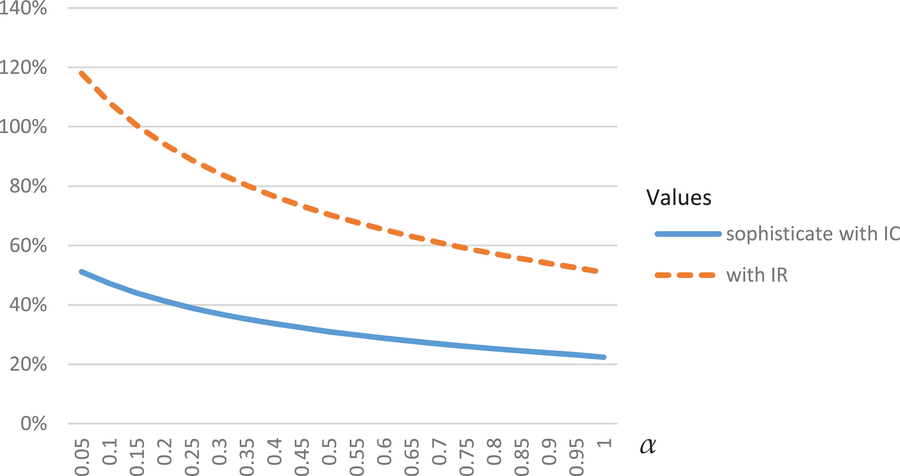

Percentage of profit loss by procrastination as a function of α

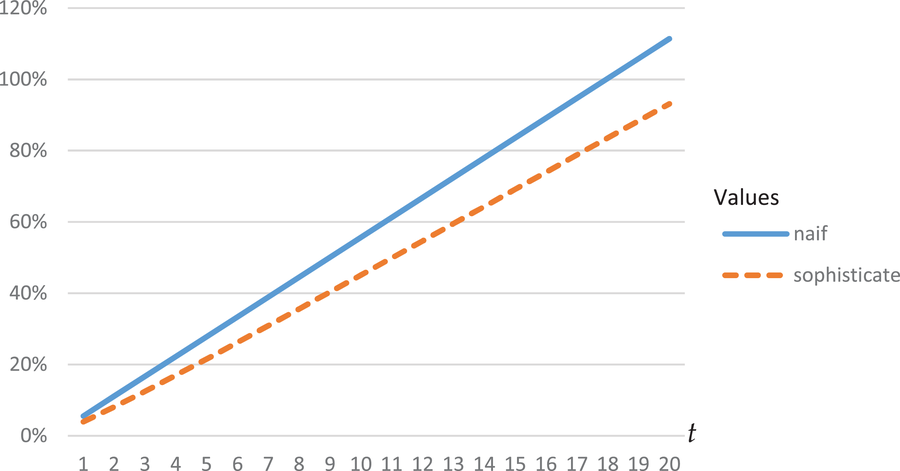

Percentage of profit loss by procrastination as a function of t

Figure 2 demonstrates that the profit loss decreases with the ratio of project values to project processing times. Note that, in our instances, larger processing times lead to greater scheduling costs. The pattern in Figure 2 occurs because the timing decision does not impact project values, and the relative profit loss decreases as the projects become more valuable. Figure 3 shows that with a longer time horizon the loss of profit from present bias is more significant. This echoes the following well‐known phenomenon in project management: a looser deadline causes more project delays (Gutierrez & Kouvelis, 1991).

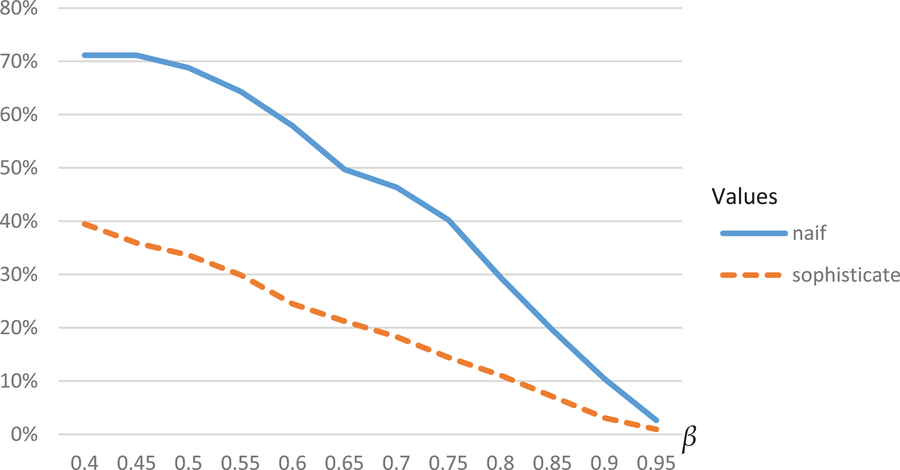

Next, we assume that, in the absence of contractual obligations, the project company can choose which projects to process. To focus on the rejection issue, we assume that project processing starts from time 0, and there is no inserted idle time between any two projects. Thus, present bias causes no procrastination here. For our instances, on average, a TC rejects 3.60 out of the 10 available projects. A naif and sophisticate reject 7.58 and 6.17 projects and incur profit losses of 44.3% and 20.0%, respectively. Intuitively, a naif overestimates his rationality in the future and consequently overrates his future profit. As a result, he is more willing to forego a current project to reduce the cost of future projects; however, those future projects will not be processed as he expects, and additional profit loss will occur. On the other hand, a sophisticate has a better understanding of his present bias in the future and incurs a less severe overrejection. The profit loss due to overrejection is shown in Figures 4 and 5. Figure 4 shows that profit loss due to overrejection decreases where there is a low level of present bias, that is, a high β value. At most levels of present bias, a naif's profit loss percentage approximately doubles that of a sophisticate. Figure 5 shows that the relative profit loss percentage caused by overrejection is insensitive to the relative value of projects compared to their costs.

Percentage of profit loss by rejection as a function of β

Percentage of profit loss by rejection as a function of α

We now discuss our managerial insights from the above analysis in Sections 3.1–3.3. We are interested in how far a naif or a sophisticate's decision deviates from that of a TC and what mechanisms we can use to mitigate the resulting loss of profit.

First, we find that, in general, immediate costs incentivize a naif or sophisticate to delay his project processing or even reject projects. This is because an immediate cost is overevaluated relative to future values of projects by a present‐biased decision‐maker. In contrast, immediate revenues encourage a naif or sophisticate to advance his project processing more than optimally due to the discounted future cost perceived by a biased decision‐maker. Therefore, under present bias, to avoid delay or rejection of an urgent project, a project owner may offer a contract with immediate revenues; and to postpone a project strategically, a project owner may offer one with immediate costs.

Second, when project revenues are sufficient to cover their costs, with either immediate revenues or costs, a naif may procrastinate project processing or reject projects more than a sophisticate. On the other hand, a sophisticate may preproperate project processing more than a naif. We observe that a naif only discounts his future values once when he makes a decision. However, a sophisticate applies compound discounting for revenues that occur later when he makes a decision. Thus, when completed projects can provide positive net profit, a naif is more likely to overestimate the future values of later projects and hence is more willing to delay a currently available project or even reject it.

SEQUENCING DECISIONS

Immediate costs

A TC's sequencing decision constitutes a classical scheduling problem. We consider the sequencing problem faced by a naif with immediate costs and revenues at project completion. Recall that a naif assumes he will be time consistent in all later decisions.

Consider the following algorithm for a naif. Let

Algorithm naive immediate costs for sequencing (NICS)

Given Set For each project Let Set If a TC's sequencing problem can be solved optimally in

At any time given t, for any given set J of unprocessed projects, Algorithm NICS chooses the project to process next that maximizes a naif's perceived profit at time t. If the maximized profit at time t for projects in J is negative, then the naif cannot perceive any positive value at time t for any subset of projects in J and rejects all the projects in J. Therefore, Algorithm NICS is optimal from the viewpoint of a naif. Regarding the time complexity, Step 1 is applied n times, and each application calls an optimal algorithm with time complexity bounded by

We observe that an The scheduling cost function is the weighted completion time, that is,

To minimize the total weighted completion time, for a TC, the shortest weighted processing time first sequence, where projects are sequenced by the nondecreasing ratio of processing time to weight

In the problem considered below, the scheduling cost is the weighted number of late projects. For a TC, there exists a pseudopolynomial time algorithm (Lawler & Moore, 1969), but the problem is binary NP‐hard (Karp, 1972). Consider a scheduling cost function is

Consider a schedule in which the on‐time projects are sequenced by nondecreasing due dates, followed by the late projects with nondecreasing weights. This sequence is optimal for a TC (Lawler & Moore, 1969). Assume projects are sequentially indexed as To show the optimality of sequence First, when Second, when

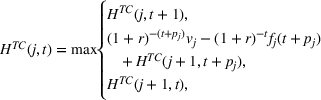

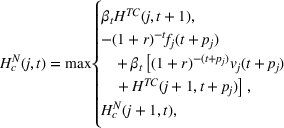

For a general scheduling cost function, the following algorithm optimizes the sequencing decisions of a sophisticate.

Algorithm sophisticated immediate costs for sequencing (SICS)

Input

Given

Value function

Boundary condition

Optimal solution value

Recurrence relation

In the recurrence relation, in the first alternative, a project

The optimality of Algorithm SICS follows from its implicit enumeration in the recurrence relation. In the value function, there are up to 2

n

different sets J and up to P different values of t. The recurrence relation selects j from J, which requires up to n comparisons. Therefore, the overall time complexity of the algorithm is

Immediate revenues

We consider the sequencing problem, for a naif, with immediate revenues and costs at project completion. Let

Algorithm naive immediate revenues for sequencing (NIRS)

Set For each project Let Set

If a TC's sequencing problem can be solved optimally in

The proof of Proposition 5 is similar to that of Proposition 3 and is therefore omitted.

With immediate revenues and project completion time cost, the shortest processing time first (SPT) rule which is optimal for a TC is not necessarily optimal for a naif. This is because, with immediate revenues, project revenue strongly influences the total net profit of a schedule. Consider the following example. The scheduling cost function is the project completion time, that is,

For Example 4, the SPT sequence 1 → 2 provides a net perceived profit of

Similar to the case with immediate costs, we present the following algorithm that optimizes the sequencing decision of a sophisticate with immediate revenues.

Algorithm sophisticated immediate revenues for sequencing

Value function

Boundary condition

Recurrence relation

Managerial insights for sequencing decisions

As in Section 3.3, we first investigate with scheduling cost defined as project completion time, that is, If with immediate costs, a naif processes his projects by nondecreasing order of project processing time, as does a TC, with immediate costs, a sophisticate processes his projects by nondecreasing order of with immediate revenues, both a naif and a sophisticate process their projects by nondecreasing order of

For part (i), we first note that the SPT rule is optimal for a TC, that is, projects are sequenced by nondecreasing processing times. To see that the SPT rule is also optimal for a naif with immediate costs, consider an interchange argument with two projects i and j, where For part (ii), consider a sophisticate's sequencing decision for the same problem. Now consider a pairwise interchange argument involving projects i and j. Consider the following alternative decisions for a sophisticate. The following expressions are written for profit rather than cost, where

Comparing these expressions for profit, we have the difference in profit With For part (iii), to find an optimal sequence for a naif, consider a pairwise interchange argument involving projects i and j, with the following expressions written for profit:

Comparing these expressions for profit, we have Finally, consider a sophisticate's sequencing decision for the same problem. Let

Comparing these expressions for profit, we have

We note that in part (ii) of Theorem 2, for a sophisticate with

In part (iii) of Theorem 2, for the sequencing problem with immediate revenues and cost function

Overall, Theorem 2 shows that the design of projects with immediate costs by project owners can help prevent biased decisions for the sequencing problem.

Next, we use a numerical experiment to study how present bias can lead to inefficient sequencing decisions. The experimental design is similar to that in Section 3.3. To focus on sequencing in a given time window in length equal to the total processing time of the given projects, we do not allow rejection. Note that for the sequencing problem with

Figure 6 shows that the profit loss due to present bias is decreasing with β, there is a greater loss with immediate revenues, and there is a decreasing gap between the two mechanisms as β increases. Figure 7 depicts the same effects of α as in Figure 2.

Percentage of profit loss in sequencing as a function of β

Percentage of profit loss in sequencing as a function of α

We next discuss the managerial insights obtained from our study of sequencing decisions. Recall that the preference is always for an economically efficient time‐consistent decision. First, from a computational perspective, a TC's sequencing decision is the easiest, while a sophisticate's decision is the hardest. This observation has a favorable implication; since a sequencing decision is harder to make using a naive or sophisticated strategy, a naif or sophisticate may use a time‐consistent decision for ease of decision‐making.

Second, for immediate costs, with certain scheduling cost functions, for example, project completion time cost, that is,

Third, an optimal sequence under the naive or sophisticated strategy is closer to an optimal sequence as found by a time‐consistent strategy under immediate costs than under immediate revenues when sequencing decisions influence project costs more than project revenues. Intuitively, it is better to have either cost or revenue, whichever is more affected by sequencing decisions, at the beginning of a project to promote more efficient sequencing by project companies.

Fourth, we observe a tendency to process projects with more significant revenue and negligible cost earlier under biased decisions than under time‐consistent decisions. This is because present bias often prioritizes projects with a greater value‐to‐cost ratio. To mitigate the inefficiency that results from this tendency, project owners may assign costs and revenues more equally among projects or assign costs and revenues proportionately for projects during project contracting.

CONCLUDING REMARKS

This work is among the first to study the effect of the well‐documented phenomenon of present bias within a scheduling context. Within a simple scheduling system, we use examples to illustrate time‐inconsistent decision‐making and describe algorithms to optimize revenue less cost for both naive and sophisticated time‐inconsistent decision‐makers. This enables us to develop insights into the relative performance of time‐consistent, naive, and sophisticated decision‐makers, and how to mitigate the effects of present bias. These insights are validated both by theoretical results and computational studies.

This work studies how present bias, as modeled by a present bias coefficient and a level of self‐awareness of this bias, affects decisions in the scheduling of projects, as well as how to mitigate biases in such decisions. First, we study timing decisions for a fixed sequence of potential projects. Here, we find that it is helpful for a project owner, in anticipation of present bias by a project company, to offer a contract with immediate revenues, since doing so may avoid delay or rejection of an urgent project. Further, to encourage postponement of a project strategically, a project owner may offer one with immediate costs. For sequencing decisions between projects, it is beneficial for a project owner to have either cost or revenue, whichever is mainly affected by sequencing decisions, scheduled immediately at the beginning of a project, in order to promote more efficient sequencing by a project company.

For future research, an extension of our work is to consider scheduling decisions under present bias in different bias and awareness formats other than rate and naif/sophisticate awareness. We also recommend further comparisons of time‐consistent and time‐inconsistent decision‐making for operational decisions. The extensive classical scheduling literature (Demeulemeester & Herroelen, 2002; Pinedo, 2016) describes numerous directions by which to explore this comparison. In addition, models of simple inventory trade‐offs that require decision‐making over time under present bias, along with measures to mitigate its effects in that context, define interesting problems for study.

Footnotes

ACKNOWLEDGMENTS

The authors thank the senior editor and two anonymous reviewers for their constructive comments, which have substantially improved the quality of this work. The work of the first author was supported in part by Grant No. 71732003 (January 2018–December 2022) from the National Natural Sciences Foundation of China and in part by the Berry Professorship at the Fisher College of Business, The Ohio State University.