Abstract

Firms sometimes acquire partial ownership of their upstream suppliers. Such ownership entails no direct control over the target firm's decision‐making; however, both firms might change their pricing strategies after forming a partial ownership relationship. This paper studies the economic impacts of partial vertical ownership (PVO) in a market with downstream competition, where a manufacturer supplies two competing retailers. We find that dividend payments between firms can alter firms’ incentives in their operational decisions and, hence, serve as an “invisible hand” to downstream competition and vertical interaction. We show that a higher PVO percentage can have both positive and negative effects because the acquiring retailer's gain from PVO depends on not only its own sales but also the competitor's sales. Thus, the PVO decision (i.e., the percentage of ownership to acquire) has an inverted U‐shaped effect on the resulting profit for both the acquiring retailer and the manufacturer, which implies an intermediate PVO percentage in equilibrium. Second, the relative strength of the positive and negative effects depends on the acquiring retailer's competitive position. We show that the manufacturer prefers establishing PVO with the retailer with a valuation disadvantage because the disadvantaged retailer can obtain more benefits from PVO and is willing to pay higher than the competitor. Last, we find that consumers benefit from PVO when the acquiring retailer is the retailer with a valuation advantage but may become worse off when the disadvantaged retailer acquires PVO. Our research provides managers with guidance on the optimal PVO percentage and policymakers with insights on regulating PVOs for consumer protection.

INTRODUCTION

It has become a common business phenomenon that downstream firms hold passive—namely, non‐controlling—partial ownership interests in upstream firms (Allen & Phillips 2000, Greenlee & Raskovich, 2006; Hunold & Stahl, 2016). For example, JD.com acquired an 8.8% stake in the furniture manufacturer Shangpin Home Collection (iNews, 2022), Walgreens acquired 26% of the drug wholesaler AmerisourceBergen (Siconolfi, 2018), and Walmart announced in 2022 that it had agreed to invest in Plenty, a vertical farming company who also supplies other grocery stores, for example, Whole Foods Market and Albertsons (Repko, 2022; Wells, 2022). By acquiring such a passive interest, the downstream firm simply acquires claims on the target firm's profit (dividends) without control rights, mainly with the purpose of lowering input costs and enhancing its competitiveness in the downstream market (Greenlee & Raskovich, 2006; Hunold & Stahl, 2016). By contrast, the full vertical integration or partial ownership with control rights would typically require significant financial investment and management adjustment; thus, passive partial vertical ownership (PVO) offers downstream firms a less expensive and less complicated alternative for lowering input costs, which can explain its increasing popularity in practice. 1

Passive shareholders often do not vote and exert no control over the upstream's decision‐making, for example, pricing (see Kay, 2015; Law Right, 2016; Levy et al., 2018). 2 Prior studies have focused on full integration or controlling ownership interests as a means to mitigate double marginalization by directly controlling upstream pricing decisions. However, it remains underexplored how non‐controlling PVO affects firms’ profits and consumer surplus in a competitive, horizontally differentiated market. Although PVO gives no direct control over the target firm's decision‐making, it can affect the strategic interactions in both vertical relationships and horizontal competition because the ownership interest will reap a dividend from the acquired upstream firm's profit. Such dividend payments between firms can serve as an “invisible hand” to alter their incentives in their operational decisions in the market. The economic impacts of PVO on firms’ pricing, profits, and consumer surplus remain underexplored in the literature.

PVOs are popular in some sectors but not in others, and some companies acquire a large share, while others only a small portion. So, there can be both practical and academic interest in understanding under what conditions firms will profitably form PVO and how PVO affects the market outcome. We develop an analytical model to examine the following research questions: (1) In the presence of downstream competition, how will non‐controlling PVO affect firms’ pricing strategy and profitability? (2) What percentage of PVO will be chosen in equilibrium? (3) Does the upstream firm prefer forming PVO with an advantaged or disadvantaged downstream firm? (4) What are the effects of PVO on consumers and the total profit of the supply chain?

In our analytical model, an upstream firm supplies a core product to two horizontally differentiated downstream firms, one of whom may consider acquiring a minority interest in the upstream supplier. For expositional simplicity, we hereafter refer to the upstream firm as the manufacturer and the downstream firms as retailers. One retailer's offering has a (weakly) higher value to the consumer than the other retailer's, for example, due to a more lenient return policy or better pre‐ or post‐sales customer services. Thus, we refer to the retailer with a higher‐value offering as the retailer with a valuation advantage and the other as the retailer with a valuation disadvantage. This framework allows us to study whether the economic consequences of PVO (such as the PVO percentage, the manufacturer's preference, and the consumer surplus) depend on the asymmetry between the retailers.

Our analysis reveals several key findings. First, a larger percentage of non‐controlling PVO does not necessarily benefit the acquiring retailer. A larger PVO percentage lowers the acquiring retailer's effective wholesale price and allows it to shift more sales away from the competing retailer, but the competitor's reduced sales also decrease the acquiring retailer's dividend from its PVO of the manufacturer. Such intertwined effects have two managerial implications. On the one hand, the negative effect implies that the establishment of PVO may not always be profitable for a given PVO percentage. Specifically, the negative effect can dominate and render PVO infeasible when the horizontal differentiation between the retailers is sufficiently low. On the other hand, the two opposing effects create an inverted U‐shaped effect of the PVO percentage on the acquiring and target firms’ total gain from PVO. We show that regardless of who (either the acquiring retailer or the manufacturer) proposes the formation of PVO, the equilibrium PVO percentage is an intermediate value that maximizes the joint profit of the two parties. Our finding offers insights to practitioners by suggesting that aggressively acquiring a higher share of PVO may not be a preferred strategy in the presence of downstream competition.

Second, the relative strength of the aforementioned positive and negative effects of PVO percentage depends on the acquiring retailer's competitive (dis)advantage. Specifically, the acquiring retailer in a weaker competitive position can gain more benefits from PVO. In this case, due to the competing retailer's stronger competitive position, a larger PVO percentage does not cause a significant reduction in its sales relative to its original demand, allowing the acquiring retailer to still significantly benefit from the competitor's sales via dividends earned from the PVO. In other words, the above‐mentioned negative effect is relatively weaker when the retailer with a valuation disadvantage acquires PVO. Consequently, a larger percentage of PVO is preferred when the acquiring firm has a valuation disadvantage. Moreover, when the two retailers compete for PVO, the retailer with a valuation disadvantage is willing to pay more to acquire the same PVO percentage, and hence the manufacturer prefers forming PVO with the disadvantaged retailer.

Last, PVO has an impact on consumer surplus, but the impact depends on the acquiring retailer's competitive position. Specifically, the establishment of PVO will increase consumer surplus when the acquiring retailer has a valuation advantage but may reduce consumer surplus when the acquiring retailer has a valuation disadvantage. In the former case, consumer surplus increases because more consumers buy from the advantaged acquiring retailer and enjoy a price drop after the establishment of PVO. In the latter case, even though consumers who buy from the disadvantaged acquiring retailer enjoy a price drop, more consumers buy from the advantaged competitor and pay a higher post‐PVO price. When the retailers have relatively low horizontal differentiation, many consumers buy from the competing retailer such that the negative effect of PVO on consumer surplus outweighs its positive effect; thus, PVO can reduce the overall consumer surplus. We also show that this result holds regardless of the market coverage. Our findings offer useful insights to regulators by suggesting that the acquiring retailer's competitive position is an important factor to consider for consumer protection. Moreover, we find that regardless of the acquiring firm's competitive position and market coverage, PVO maximizes the joint profit of the target and acquiring firms as in the case of full integration. Hence, our study shows that passive PVO can alleviate double marginalization between the manufacturer and the acquiring retailer. However, PVO worsens the double marginalization effect for the competing retailer because PVO raises its costs; this negative effect can dominate and lead to lower total profits for the entire supply chain, compared with no PVO.

Our paper complements the literature that studies supply chain integration, whereby one member in the supply chain merges with another downstream or upstream member. Corbett and Karmarkar (2001) find that with symmetric competing two‐tier supply chains, the vertical integration of each supply chain can reduce the supply chain's total profit because of the foregone benefits of upstream competition. Lin et al. (2014) study the benefits of backward integration relative to forward integration in a market with two identical three‐tier supply chains and show that the presence of competition increases the attractiveness of backward integration relative to forward integration. Jin et al. (2019) find that in a duopoly supply chain setting, a manufacturer tends to invest more in supplier development to reduce the latter's cost after it integrates with the supplier and that the manufacturer with lower supplier‐development capabilities is less likely to integrate with its supplier. Federgruen and Hu (2020) study the effect of vertical mergers on product variety and show that the equilibrium product assortment shrinks after a vertical merger. Some research (e.g., Bernstein & Federgruen, 2003; Lee & Whang, 2002; Netessine & Zhang, 2005; Qi et al., 2015) has examined the effects of vertical integration on production quantity or replenishment decisions. Another stream of literature has studied the effect of vertical integration on channel choices (e.g., manufacturers’ incentive of selling products through a centralized or decentralized channel). For example, McGuire and Staelin (1983) study a setting with two manufacturers selling competing products, either through their own stores (i.e., a centralized channel) or through independent retailers. They show that it is profitable for upstream manufacturers to integrate with their downstream retailers only if product substitutability is low and that consumers are better off when manufacturers sell directly through their direct channels. Several later studies (e.g., Coughlan, 1985; Gupta & Loulou, 1998; Moorthy, 1988) extend McGuire and Staelin's (1983) study to various settings and confirm that with high product substitutability, decentralized channels are more profitable than integrated channels. Our research complements the above literature by examining the effects of passive PVO. In contrast with vertical integration, by acquiring passive PVO, the downstream firm claims only on the target's profits without controlling its decision‐making (Greenlee & Raskovich, 2006). More specifically, the retailer that acquires a minority PVO of the manufacturer cannot dictate the manufacturer's operating decisions (e.g., the wholesale pricing decision). In our model, the effects of PVO are solely driven indirectly by the profit dividend that the acquiring retailer obtains from the minority PVO interest. Our paper finds an inverted U‐shaped effect of the PVO percentage on the benefit to the target or the acquiring firm. Moreover, adding to the prior studies that focus on top‐down coordination via suppliers‐proposed supply contracts, for example, revenue‐sharing and quantity‐flexibility contracts (e.g., Cachon & Lariviere, 2005; Tsay, 1999), our study proposes a bottom‐up coordination mechanism where a downstream retailer proposes a partial ownership interest to align the incentives of a decentralized channel. We show that PVO can achieve the same total profit of the acquiring retailer and the manufacturer as that under full integration, but PVO requires a lower acquisition payment.

Our paper also contributes to the literature studying PVO. This stream of literature either does not model product differentiation (e.g., Levy et al., 2018; Serbera, 2019) or assumes reduced‐form demand functions (e.g., Brito et al., 2016; Fiocco, 2016; Greenlee & Raskovich, 2006; Hunold & Stahl, 2016). For example, Brito et al. (2016), Greenlee and Raskovich (2006), and Hunold and Stahl (2016) show that in a reduced‐form demand model with downstream competition, passive backward PVO does not affect or may harm the consumer. Chen et al. (2017) examine vertical cross‐ownership in a setting with an exogenous retail price and no downstream competition, and they do not study consumer surplus. In contrast, we show that PVO can lead to either

Finally, several recent studies have examined horizontal mergers (i.e., the mergers between competing firms). Cho (2014) studies the effect of a horizontal merger on a decentralized supply chain. Cho and Wang (2017) study horizontal mergers among newsvendors. Korpeoglu et al. (2020) study how the number of retailers affects buying power and how the integration of two wholesale markets affects the supply chain profits. Some research (e.g., Davidson & Mukherjee, 2007; Lommerud et al,., 2005, Perry & Porter 1985; Salant et al., 1983; Ziss, 1955) shows that horizontal partial ownerships or mergers can help reduce competition and may also contribute to efficiency gains in the presence of endogenous downstream competition or vertical interactions. In particular, Symeonidis (2010) finds that a merger between downstream firms may increase or reduce consumer surplus, depending on the nature of competition (in quantities or in prices) and whether upstream firms are independent. Our research complements these studies by examining

The rest of the paper is organized as follows. Section 2 describes the model setup. In Section 3, we study the economic impacts of PVO based on whether the acquiring retailer has a valuation advantage or disadvantage. In Section 4, we extend our model to various settings, for example, the incorporation of market‐expansion effects (i.e., a non‐fully covered market), the manufacturer charging different wholesale prices, and the acquiring retailer's partial influence on the manufacturer's wholesale price decision. We offer managerial implications and conclude the paper in Section 5. Analyses and proofs for equilibrium results have all been relegated to the Online Appendix.

MODEL SETUP

We study a two‐tier supply chain where an upstream manufacturer (labeled by

We adopt the Hotelling model (Hotelling, 1929) to capture the horizontal competition. A unit mass of consumers is uniformly distributed on the line segment [0, 1]. That is, one can think of the consumers as residing uniformly in a linear city represented by the line segment between 0 and 1. Retailer 1 is located at 0, and Retailer 2 is located at 1. Let

For simplicity, the manufacturer's production costs and retailers’ retail costs are normalized to zero. Each consumer demands at most one unit of the product, and the consumer's utility of no purchase is normalized to zero.

ANALYSIS

Benchmark: No PVO

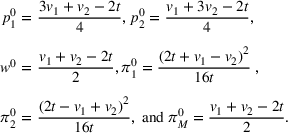

In this section, we consider a benchmark without PVO. In this case, the sequence of events is as follows. The manufacturer first decides its wholesale price,

Given the prices, there exists a marginal consumer, located at

Main model

We now turn to the main model by analyzing two scenarios: the acquiring retailer has a valuation advantage (in Section 3.2.1), and the acquiring retailer has a valuation disadvantage (in Section 3.2.2). As noted earlier, the retailer's PVO entails no direct control over the manufacturer's pricing decision. Thus, in both scenarios, the manufacturer determines its wholesale price by maximizing its own operating profit.

PVO by the retailer with a valuation advantage

In this setting, the acquiring firm is the retailer with a valuation advantage (i.e., Retailer 1). The game proceeds as follows. First, Retailer 1 proposes a payment

We show that in the parameter space of our interest (i.e.,

We analyze the game using backward induction. Briefly, we first derive retailers’ retail prices in Stage 3, given the manufacturer's wholesale price

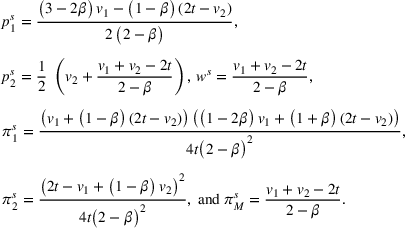

The analysis of the third stage of the game is similar to that in the benchmark case. In the following, we present and discuss the retailers’ and the manufacturer's pricing decisions,

The purpose of discussing the pricing subgame equilibrium results is to understand how PVO of a given percentage (β) affects the firms’ pricing decisions and profitability. Specifically, by comparing the cases in which PVO is formed versus not, we determine how the formation of PVO affects the wholesale and retail prices; Lemma 1 summarizes our findings. Note that the payment If PVO of a given percentage β is formed, the manufacturer's wholesale price (

In the presence of PVO (of a given percentage β), given the same wholesale price as in the case of no PVO, Retailer 1's share of the manufacturer's profit results in a lower effective wholesale price

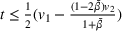

Next, we study a scheme of PVO can be formed if

Lemma 2 suggests that PVO can be formed when the horizontal differentiation between the two retailers is sufficiently large such that there exists a viable payment scheme acceptable to both the acquiring retailer and the manufacturer. Even though the manufacturer and Retailer 1 form PVO to squeeze Retailer 2's sales, they nonetheless obtain a profit from Retailer 2's sales. When

Lemma 2 suggests that for a given PVO percentage, establishing PVO can benefit both the manufacturer and Retailer 1 only under some conditions. Proposition 1 summarizes the equilibrium PVO percentage

When the acquiring retailer has a valuation advantage over its competitor, the equilibrium PVO percentage is at an intermediate level The equilibrium

Proposition 1(a) suggests in equilibrium, PVO is formed at an intermediate level of ownership percentage

First, this intermediate level of equilibrium ownership percentage is due to the non‐monotonic impact of PVO percentage, which stems from two opposing effects of β on the manufacturer and Retailer 1's total profit. The positive effect of PVO is due to the above‐mentioned “collusion” effect. The discussion of Lemma 2 also implies that if the establishment of PVO shifts too much demand from Retailer 2, it may also cause a backfire and hurt both the manufacturer and Retailer 1's gain because Retailer 2's sales contribute to both firms’ profits. This negative effect dominates when the PVO percentage is sufficiently large.

10

This property of equilibrium

Second, this equilibrium ownership percentage maximizes the joint profit of the two parties, regardless of who proposes PVO. The rationale is that the one‐time payment

As a technical note, let us consider that payment

In the parameter region we focus on (such that the two retailers profitably co‐exist), the equilibrium PVO share naturally satisfies

From the equilibrium PVO percentage The equilibrium PVO percentage

Proposition 2 summarizes the effect of intrinsic values and horizontal differentiation on the equilibrium PVO percentage. As explained above, the presence of PVO helps the acquiring firm shift demand from Retailer 2. When

Second, the equilibrium PVO percentage

After understanding the economic effect of PVO on firms, we discuss how the formation of PVO affects the consumer. When the acquiring retailer has a valuation advantage over its competitor, consumer surplus increases compared with the case without PVO.

When the acquiring firm is the retailer with a valuation advantage, that is, Retailer 1, its existing buyers enjoy a price drop (

We also find that the total profit of all three parties decreases, compared with the case of no PVO. This is because Retailer 1 and the manufacturer maximize their own respective payoffs and essentially “collude” through the “invisible hand” of the PVO relationship to squeeze Retailer 2's profit, and the loss of Retailer 2's profit overweighs the gain of the formers. Although double marginalization between the manufacturer and the acquiring retailer is alleviated, it worsens for the competing retailer who receives a higher wholesale price than without PVO.

PVO by the retailer with a valuation disadvantage

In this section, we consider the situation where the acquiring firm is the retailer with a valuation disadvantage, that is, Retailer 2. The sequence of events remains the same except that in Stage 3, the two retailers simultaneously choose their prices,

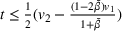

In the following discussion, we focus on those results that are distinct from the scenario of the advantaged retailer acquiring PVO. Regarding the feasibility of PVO for a given ownership percentage β, we find that the lower bound When the acquiring retailer has a valuation disadvantage over its competitor, The feasible payment range The equilibrium PVO percentage,

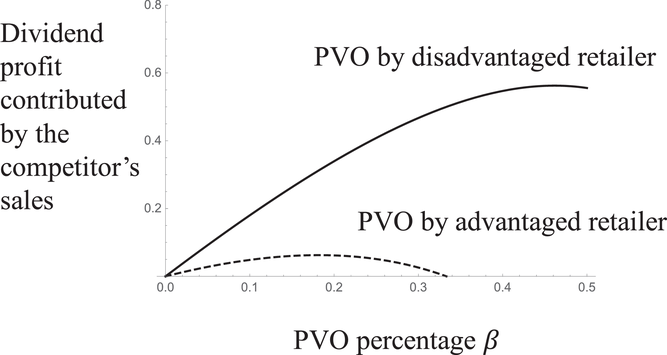

We know that either acquiring firm (Retailer 1 or 2) gains profits from both its own sales and those of the competing retailer. If the acquiring retailer has a valuation advantage, the main contribution to the acquiring firm's profit still comes from its own sales; by contrast, if the acquiring retailer has a valuation disadvantage, the acquiring retailer can obtain greater benefits from the advantaged competitor's sales due to the latter's stronger competitive position. In other words, the above‐mentioned negative effect of a larger PVO percentage is weakened in the case of the disadvantaged retailer acquiring PVO.

Figure 1 numerically (

Profit contribution from the competing retailer between the two scenarios. PVO, partial vertical ownership

Given that Retailer 2 gains more from a given percentage PVO and the manufacturer's profit remains the same regardless of which retailer acquires PVO (because the wholesale prices in the two cases are the same), the total net gain from PVO of the two firms is higher when the retailer with a valuation disadvantage acquires PVO than when the retailer with a valuation advantage acquires PVO. Consequently, this results in a higher equilibrium PVO percentage

We find that if the two retailers compete for PVO, the retailer with a valuation disadvantage is willing to pay more to form PVO with the manufacturer than the retailer with a valuation advantage. More specifically, the disadvantaged retailer's maximum willingness‐to‐pay, which is given by its total profit (including its dividend from PVO) when it acquires PVO minus its profit when the advantaged retailer acquires PVO, is higher than that of the advantaged retailer, for any given PVO percentage. Consequently, the manufacturer prefers forming PVO with the retailer with a valuation disadvantage. Proposition 5 documents this result. The manufacturer prefers forming PVO with the retailer with a valuation disadvantage.

According to this result, in our motivating example, the common supplier, Shangpin Home Collection, would prefer forming PVO with JD.com because JD.com is generally considered less competitive than Alibaba in the Chinese retail industry. This is consistent with what happened in reality (iNews, 2022) though we acknowledge that there may be other plausible explanations.

Different from the case of the advantaged retailer acquiring PVO, the formation of PVO by the disadvantaged retailer may hurt consumers. Proposition 6 below summarizes the effect of PVO on consumer surplus. When the acquiring retailer has a valuation disadvantage over its competitor, consumer surplus may decrease compared with no PVO. Specifically, consumer surplus decreases when

Proposition 6 suggests that in contrast to the case of the advantaged retailer acquiring PVO, PVO by the retailer with a valuation disadvantage can harm consumers when the retailers have low horizontal differentiation, that is,

This result is also in sharp contrast with prior studies (e.g., Brito et al., 2016), showing that PVO either benefits or has no effect on consumer surplus. Additionally, we find that similar to the case of the advantaged retailer acquiring PVO, PVO reduces the total profit of the entire supply chain because the competing retailer is much worse off.

Comparison with full integration

In this section, we consider the case where retailer

With full integration, retailer

We first discuss the scenario in which the retailer with a valuation advantage fully integrates with the manufacturer and then compare it with the corresponding PVO case. Results are similar when the retailer with a valuation disadvantage fully integrates with the manufacturer. When the PVO percentage is lower or higher than the equilibrium level (i.e., for

Lemma 3 suggests that when the PVO percentage is not at the equilibrium level

Interestingly, when

Next, we discuss the equilibrium payment. When the advantaged retailer acquires PVO, the payment schemes that can incentivize full integration are given by At the equilibrium PVO percentage,

Proposition 7 suggests that the acquiring retailer and the manufacturer can use PVO to achieve the same total gain as that under full integration, even though, as we analytically show, PVO may require less capital for the acquiring firm. More specifically, both the lowest and highest possible payments that can incentivize the formation of PVO are lower than those that incentivize full integration. In other words, the acquiring retailer can obtain the full strategic benefit of backward integration without having to fully acquire the manufacturer; rather, an optimally selected non‐controlling minority interest would suffice to create the same market outcome as that under full integration between the acquiring retailer and the manufacturer. Intuitively, even though it is partial integration, both the acquiring retailer and the manufacturer have an incentive to optimally choose a PVO percentage that maximizes the joint profit and then choose a payment such that the other party would accept the offer. This is akin to the conventional double‐marginalization problem in a simple channel with one manufacturer and one retailer, where the manufacturer or the retailer will choose the wholesale price that maximizes their total channel profit and then uses a fixed fee to decide how to split the profit to make it acceptable for both firms. 13 Our finding provides a theoretical explanation for the increasing popularity of PVO in practice.

EXTENSIONS

Non‐fully covered market

Our main model has focused on the parameter region

Similarly, we focus on the parameter region where the level of horizontal differentiation

We confirm that our key results from the main model remain qualitatively the same. For example, it still holds that the equilibrium PVO percentage is at an intermediate level that maximizes the joint profit, and consumer surplus may decrease when the retailer with a valuation disadvantage acquires PVO. As a technical note, in this alternative model where the market expansion is possible, the indifferent customer's surplus can be positive or zero in equilibrium.

Manufacturer's price discrimination

A seller charging comparable competing buyers different prices for the same “commodity” is typically not allowed by antitrust laws, according to Federal Trade Commission. 15 However, one might wonder what will happen if such price discrimination is adopted, that is, the manufacturer could strategically charge different prices to the two competing retailers. 16 We show that in such cases, our key insights are robust. For example, the PVO percentage still has an inverted U‐shaped effect on the acquiring and target firms’ total gain from the PVO. Even though the manufacturer can charge different wholesale prices, our analysis shows that PVO still has a demand‐shifting effect—shifting some customers from the competitor to the acquiring retailer in equilibrium. Consequently, a larger PVO percentage can backfire as is the case in the main model. That is, we confirm that the equilibrium PVO percentage is still achieved at an intermediate level, regardless of the acquiring retailer's competitive position. 17

Partial influence on manufacturer's decision‐making

In reality, a firm with a significant minority interest can exert some influence on the target firm's decision‐making (e.g., through shareholders’ voting or the threat of exit). In this extension, we examine whether our main findings still hold if the acquiring retailer can have a partial influence on the manufacturer's decision‐making. We model this partial influence by incorporating a fraction γ of the acquiring retailer's profit into the manufacturer's objective function when it chooses its wholesale price, that is,

CONCLUSION

This paper investigates the economic and strategic implications of passive PVO of an upstream manufacturer by a downstream retailer in a market where a common manufacturer sells its product to two horizontally differentiated retailers. Unlike prior studies, we examine the role of downstream competition and the acquiring firm's competitive (dis)advantage in a horizontally differentiated market. The acquiring retailer can be either an advantaged or a disadvantaged one. We find that dividend payments between firms in vertical relationships can alter their incentives in their operational decisions and hence serve as an “invisible hand” to horizontal competition and vertical interaction.

Our study provides the following three major insights to managers and regulators. First, we show that a greater PVO percentage can play both positive and negative roles. This is because the acquiring firm's gain from PVO depends on both its own sales and the competing retailer's sales. When the PVO percentage is sufficiently large, it can hurt the acquiring retailer because the competing retailer's sales will drop too much, reducing the dividend from PVO. The resulting inverted U‐shaped effect of PVO percentage implies an intermediate level of PVO percentage in equilibrium. We also show that this intermediate level of PVO percentage is a value that maximizes the joint profit of the target and acquiring firms. This finding offers some managerial insights by suggesting that aggressively acquiring PVO may not be a preferred strategy in the presence of downstream competition.

Second, the relative strength of the positive and negative roles of PVO percentage depends on the acquiring firm's competitive (dis)advantage. We find that the negative effect is relatively weak when the retailer with a valuation disadvantage acquires PVO because it benefits more from PVO's role in enhancing its competitive position and hence prefers a larger percentage of PVO. Our result suggests that when the two retailers compete for PVO, the manufacturer prefers forming PVO with the retailer with a valuation disadvantage. This result offers managerial insights by suggesting that the acquiring retailer's competitive position is an important factor in determining the optimal PVO percentage.

Third, we show that consumers always benefit from the establishment of PVO when the acquiring retailer has a valuation advantage, but consumers may suffer if the retailer with a valuation disadvantage acquires PVO and the horizontal differentiation in the market is low. This finding offers useful insights to regulators on regulating PVOs for consumer protection.

Last, our analysis reveals that passive, non‐controlling PVO alleviates double marginalization between the manufacturer and the acquiring retailer, and the acquiring retailer can obtain the full economic benefit of backward integration without having to fully acquire the manufacturer. However, PVO worsens double marginalization for the competing retailer; this negative effect can dominate and lead to lower total profits for the entire supply chain, compared with no PVO.

To the best of our knowledge, this research is the first to analytically examine the formation of PVO in the presence of both downstream competition and endogenous vertical interactions. Our findings highlight the importance of taking into account downstream competition and the acquiring retailer's competitive position in understanding the economic consequences of PVO in a horizontally differentiated market.

We acknowledge that our model has some limitations, which suggest some potential directions for future research. First, we study a downstream firm's PVO of an upstream firm. In practice, forward PVOs can also occur when an upstream firm acquires some shares of a downstream firm. Moreover, instead of a common upstream firm serving two competing downstream firms, multiple upstream firms may supply the downstream firms, for example, each downstream firm may have its own supplier or have multiple suppliers and share some of these suppliers. It would be interesting to examine the incentive for PVO formation in various supply chain configurations. In the presence of separate (or partially overlapped) competing supply chains, the incentive may be stronger because the negative effects brought by the PVO's demand‐shifting effect are likely weaker. It would also be interesting to study how horizontal differentiation and the acquiring firm's competitive position play a role in determining the equilibrium PVO percentage and consumer surplus in alternative supply chain configurations. We acknowledge that space limitations and technical complexity limit our ability to study all these different structures, and we leave them to future research.

Second, prior studies suggest that vertical integration can have additional benefits, for example, acquiring some private information about the target firm (Lin et al., 2014) and supplier development (Jin et al., 2019). In the case of PVO, firms with a limited budget may consider backward PVO to be an effective way of gaining some proprietary information about suppliers, such as cost structure or even some valuable information about competing firms served by the same supplier. Also, Hunold and Stahl (2016) argue that a motive for backward integration without control may be to mitigate agency problems when firm‐specific investment or financing decisions are taken under incomplete information. Moreover, the acquiring retailer can have a partial influence on specific clients that the supplier could serve. Future research can study these and other strategic roles of passive vertical ownership, for example, facilitating or enabling better product development.

Last, our model has focused on the case of symmetric information where the manufacturer's cost is common knowledge and normalized to zero. If the manufacturer's cost is explicitly modeled and is its private information, then a first‐mover retailer will have a screening problem, whereas the first‐mover manufacturer will have a signaling problem. Such alternative screening or signaling games are beyond the scope of our paper and deserve their own separate studies for the exploration of additional insights in the context of non‐controlling PVO.

Footnotes

ACKNOWLEDGMENTS

All authors have contributed equally to the paper and are listed alphabetically. The authors would like to thank three anonymous reviewers, the senior editor, and the department editor for their helpful comments.

1

Another potential reason of its popularity is that regulators also often impose restrictions on controlling interests in vertical relationships to encourage competition. For example, the US Federal Trade Commission required the 1995 Time Warner–Turner–TCI deal to be restructured so that the vertical ownership interest held by TCI in its upstream trading partner, Time Warner, would remain passive (Greenlee & Raskovich, ![]() ).

).

2

3

As a technical note, under the parameter region of our interest (such that the two retailers profitably co‐exist), we analytically show in Part A of the Online Appendix that the PVO formation does not cause competition to drop out, that is, it has no impact on the market structure. This is because the acquiring retailer gains benefits (dividend profit) from the competing retailer. This finding is also consistent with the literature that argues that the main purpose of acquiring a non‐controlling PVO is not to foreclose competitors (Hunold & Stahl, ![]() ).

).

4

As a technical note, in the equilibrium where the two retailers profitably co‐exist, it always holds that the indifferent customer receives a zero net surplus, regardless of whether PVO exists. One can prove this by contradiction. Suppose that in equilibrium, the indifferent customer receives a positive surplus and the market is competitive (fully covered with both firms making positive profits). In this case, the manufacturer will be able to raise its wholesale price by a positive infinitesimal amount, which induces infinitesimally higher retail prices

5

Our PVO scenario applies to private firms and some publicly traded firms. In practice, when a firm wants to acquire a significant ownership share of another publicly traded company, the transaction may also be negotiated directly with that company rather than executed directly in the stock market. This is because the number of shares involved in the transaction may be too large relative to the trading volume (or available float); the acquiring firm's purchase of a significant block of shares may create big upward swings in the stock price. So, sometimes the acquiring firm and the target firm privately negotiate a price for the proposed PVO, and the target firm will sell its “treasury shares” or issue new shares for the PVO transaction.

6

Note that a firm's executives in charge of managerial decisions are evaluated based on the focal firm's operating performance. But it does not make any difference to maximize the manufacturer's operating profit or its net profit

7

It is worth noting that PVO is typically a long‐term consideration, whereas pricing can be changed much more easily. That is why the PVO decision is made in the very

8

We show that the full equilibrium of the pricing subgame (including both wholesale and retail pricing) is unique. Also, refer to Figure A.4 and our explanation in Part A of the Online Appendix.

9

We analytically show that this critical value ![]() ).

).

10

More technically, the joint profit

11

Note that in this case, the acquiring retailer is the disadvantaged one and its operating profit margin can be negative. In the main model, we do not limit the acquiring retailer's retail price to be (weakly) higher than the wholesale price. We analyze an extension in the Online Appendix by adding a constraint that the retailer's price is at least as high as the wholesale price. Our key qualitative insights still hold. With this constraint, however, both the acquiring retailer's and the manufacturer's profits decrease. We also find that this constraint does not affect the results if the acquiring retailer has a valuation advantage.

12

In the parameter space we focus on (such that the two retailers profitably co‐exist), the equilibrium PVO share in the case of the disadvantaged retailer acquiring PVO naturally satisfies

13

It is worth pointing out that this does not mean that firms should never bother with full integration because it can have some advantages over partial ownership (though not modeled in this paper). For example, under full integration, firms can reduce agency issues, achieve better information transparency, strengthen supply assurance, leverage synergies (e.g., reduced transaction costs, consolidated human resources), and so forth (Buzzell, 1983; Gaille, 2017; Sraders, ![]() ). We thank an anonymous reviewer for suggesting this comparison, which has allowed us to produce these interesting insights.

). We thank an anonymous reviewer for suggesting this comparison, which has allowed us to produce these interesting insights.

14

Refer to Part C of the Online Appendix for the expressions of

15

See

16

There are two legal defenses to this type of price discriminations: (1) the price difference is justified by different costs in manufacture, sale, or delivery (e.g., volume discounts) and (2) the price concession was given in good faith to meet a competitor's price.

17

We thank an anonymous reviewer for suggesting this extension.

18

Note that it is possible that parameter γ increases with the PVO share percentage. Due to the technical complexity, we leave this as our future research.