Abstract

This study examines the optimal reporting time a regulator should choose for firms to report their information when the firms' effort choices influence the outcome of projects. Our analysis shows that, the regulator's optimal choice of reporting time to maximize overall efficiency is contingent on a trade‐off between motivating a firm's effort to improve the outcome and saving the liquidation value for the creditor to reduce the firm's financing cost. We also find that to induce the firm's effort, the reporting time should be either early enough or late enough—depending on the effectiveness of the effort to turn bad projects into successes. Furthermore, we examine the regulator's optimal choice of reporting time for an economy with heterogenous firms/industries, and we show that the optimal reporting time changes nonmonotonically in the probability of good projects in the economy.

INTRODUCTION

Timing of corporate disclosures has drawn attention from both regulators and academics, and it has been routinely debated whether regulators should require firms to disclose their information sooner. On the one hand, requiring earlier reports may allow investors to take faster, more timely decisions. For instance, in 2004, the Securities and Exchange Commission (SEC) adopted Rule 33‐8400 for 8‐K disclosures, which expands the number of reportable events and accelerates disclosures by shortening the filing deadline from 15 calendar days to 4 business days after an event occurs. 1 The SEC claims that, “The (acceleration) amendments are intended to improve the amount, quality and timeliness of current information available to investors and the financial markets. This should improve the ability of investors to make informed investment and voting decisions” (SEC, 2004). On the other hand, earlier disclosures come with coarser information and lower report quality, because when an event has just occurred, it is difficult to precisely gauge its forward‐looking magnitude, impact, and consequences within a short window of time. This is particularly concerning as accounting standards now require more forward‐looking information and greater discretion in firms' financial reports. 2 The adverse effects of requiring earlier reports on financial statements' quality have also been documented by some empirical studies (Bryant‐Kutcher et al., 2013; Doyle & Magilke, 2013; Lambert et al., 2017; Watkins, 2018). Nevertheless, in the debate over disclosure timing, an often‐overlooked aspect is the effect of reporting time on managerial incentives. The requirement to produce a report that informs investors and affects their decisions also influences ex ante actions taken by firms' management. As the timing of a report affects its informativeness and hence, investors' ability to use the report to guide their decisions, reporting time may also affect the real actions of firms' managers.

In this study, we examine the consequences of report timing on firms' and investors' real decisions. We first analyze optimal report timing for a representative firm/industry, and subsequently examine the optimal timing for an economy composed of heterogenous firms/industries. In our main setting, we have a representative firm seeking funds from a representative creditor to implement a project. The project's success could be determined by its good nature/state, but the firm's diligent work (we refer to it as the firm's effort in our model) could turn a bad‐state project into a success. This is to highlight the fact that firms' effort is crucial and can be the key to success even if the project's nature/state is not favorable.

We assume the nature/state of the project is unknown at the beginning, but it may be revealed to the firm as the project progresses. If the state information is revealed to the firm by reporting time t, which is determined by a regulator, the information will be disclosed by the report. Upon observing bad‐state information from the report, the creditor may liquidate the project to recover some of her investment, and the liquidation value declines with time. In other words, the sooner the creditor liquidates the project, the more of her investment is recoverable, which captures the importance of report timeliness in helping investors recover liquidation value.

We find that the regulator's optimal choice of reporting time to maximize overall efficiency is contingent on a trade‐off between motivating the firm's effort to improve the outcome and saving the liquidation value for the creditor to reduce the firm's financing cost. Interestingly, we find that to induce effort, the regulator should set the reporting time either early enough or late enough—depending on the effectiveness of effort to turn bad projects into successes. Specifically, when the firm's effort is highly effective, the reporting time should be sufficiently late. A very late reporting time guarantees no liquidation by the creditor, as liquidation value at this stage is small, while there is still a possibility that the bad state of the project can be overturned by the firm's highly effective effort. In other words, setting the reporting time sufficiently late functions as an ex ante commitment to no liquidation, and thus the firm is motivated to exert effort.

Conversely, when the firm's effort is not highly effective in turning bad‐state projects into successes, the reporting time should be sufficiently early. An early reporting time still provides enough incentive for the firm to exert effort because an early report is very likely to be uninformative about the project state, and thus the probability of liquidation is not large enough to discourage effort. However, when the firm's effort is not effective in turning a bad project into a success, an early reporting time allows the creditor to liquidate following a bad‐state report to recover more value, and helps reduce the financing cost for the firm.

We also examine the regulator's optimal choice of reporting time in an economy comprising heterogenous firms/industries. We find that the optimal reporting time in the economy changes nonmonotonically in the probability of good projects. When most projects in the economy are bad, inducing firms to exert effort (rather than saving the liquidation value) is the regulator's priority because effort can turn bad projects into successes. Therefore, the regulator sets the reporting time to be late, which functions as an ex ante commitment of no liquidation in order to motivate effort. As the probability of good projects increases, firms' incentive to exert effort becomes weaker because their effort is only useful for bad projects. Thus, to motivate effort, the regulator needs to move the reporting time even later to discourage liquidation. However, once the probability of good projects reaches a threshold and there are sufficient good projects in the economy, inducing effort becomes less desirable as most projects are good and the effort is likely to be futile. Therefore, the regulator's priority switches to saving liquidation values (which lowers firms' financing costs), and she sets the reporting time to be early to maximize liquidation values.

This study is related to studies on financial information disclosure timing. Among theoretical studies, Dierker and Subrahmanyam (2017) analyze the optimal timing of voluntary disclosure and show that delaying disclosure could be optimal, as it encourages acquisition of information by investors. Chen, Huang, Jiang, Zhang, and Zhang (2021) study the asymmetric timeliness in disclosures of good versus bad news. Guttman (2010) examines a timing game between two analysts with respect to their earnings forecasting strategies. Hofmann and Rothenberg (2019) focus on a principal's choice of whether to produce a signal about the outcome before or after an agent's effort choice. Numerous empirical studies have examined the timing of reports as well, and many have found that accelerated reporting requirements have unintended consequences, including a higher likelihood of restatements, lower earnings quality, and lower overall information content of the reports (Bryant‐Kutcher et al., 2013; Doyle & Magilke, 2013; Ernstberger et al., 2017; Kraft, Vashishtha, and Venkatachalam, 2018; Lambert et al., 2017; Watkins, 2018).

More broadly, our study relates to a large literature in production and operations management regarding timing decisions. Many studies in this body of literature focus on the timing of strategic decisions in competitions (Anderson & Yang, 2015; Arya & Mittendorf, 2018; Guan & Chen, 2016; Niu et al., 2019; Ulku et al., 2005). Some studies focus on the timing of vulnerability disclosures in software industries (Sen et al., 2020) and the introduction timing of product‐line extensions (Ke et al., 2013). Our study contributes to this literature by examining a regulator's optimal choice of financial report timing to motivate firms' effort and to improve efficiency.

The remainder of this paper proceeds as follows. In Section 2, we describe the model setup; and in Section 3, we analyze the equilibrium strategies given the reporting time. Section 4 examines the regulator's optimal choice of the reporting time in the main setting with a representative firm/industry, and Section 5 investigates the optimal choice in an economy with heterogenous firms/industries. We also include a couple of extensions in Section 6. Section 7 concludes the paper and provides empirical and regulatory implications.

THE MODEL

This study aims to examine a regulator's optimal choice of the reporting time to maximize overall efficiency. We start by analyzing a single‐firm/industry setting, and in a later section we consider the regulator's choice of reporting time for an economy comprising heterogenous firms/industries.

In the main setting with a single firm/industry, we assume a representative firm from a specific industry needs investment I to finance its project, and the firm seeks funding from a representative creditor (“she” ) in a competitive debt market.

3

The creditor requests a debt repayment D in exchange of her investment I to break even ex ante, as the debt market is competitive. The project's outcome depends on the state of the project as well as the firm's effort in the project. The state of the project, denoted by ω, can be either good or bad,

If the project's state is good, it will be a success and generate a positive cash flow, R, with certainty. If the project's state is bad, without any effort from the firm, the project will be a failure and generate zero cash flow. However, the project can be turned into a success with probability q if the firm exerts effort on the project. This captures the fact that, in reality, managerial effort on service/product improvement, market promotion, customer satisfaction, and so forth could be crucial to success even though the project started with an unfavorable nature. The probability q can be regarded as a measure of the effort's effectiveness. We use

The firm's effort decision is unobservable to outsiders. In the case of a successful outcome, the firm pays the creditor repayment D and keeps the remaining

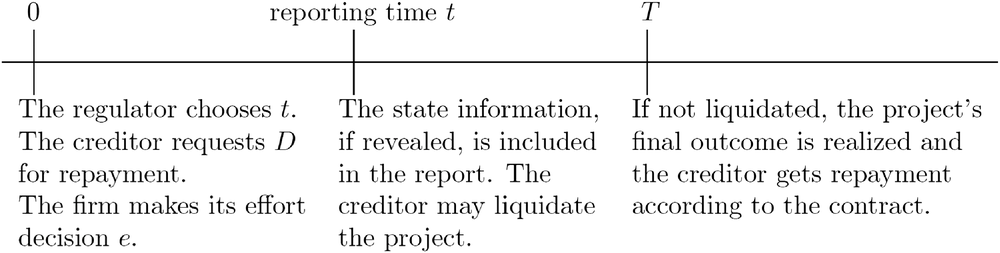

At the start of the project, its state is unknown. The regulator chooses a reporting time

If the report shows that the project state is bad, the creditor has the right to immediately liquidate the project to recover part of her investment before its final realization. We denote the creditor's liquidation decision by

Time line

The regulator's goal is to choose the reporting time to maximize overall efficiency. We define overall efficiency as the sum of the firm's and the creditor's ex ante expected payoffs. The firm's ex ante expected payoff is

To solve for the optimal reporting time, we first analyze the firm's and the creditor's equilibrium strategies with a given reporting time. Upon obtaining the equilibrium strategies for each given t, we are able to examine the regulator's optimal choice of reporting time to maximize the overall efficiency.

THE EQUILIBRIUM ANALYSIS

To analyze the equilibrium strategies given a reporting time, first note that the firm, when making its effort decision, must conjecture the creditor's liquidation decision upon an informative report. As the firm's effort decision is made before the report is released, if the creditor liquidates the project upon a bad‐state report, the firm's costly effort will be in vain. The more likely the creditor liquidates upon a bad‐state report, the less motivated the firm is to exert effort. Second, the creditor, when observing a bad‐state report, may not liquidate the project if she believes the firm has exerted effort and a large enough possibility exists that the bad‐state project is overturned. The reporting time, t, plays a role in both the firm's and the creditor's decisions. The earlier the reporting time, the less likely the report is informative and thus, the less likely the creditor liquidates the project. However, the later the reporting time, the lower the liquidation value and thus, the more reluctant the creditor is to liquidate, if she believes that the firm has exerted effort. Anticipating a lower likelihood of liquidation, the firm is more motivated to exert effort ex ante.

The liquidation decision

By backward induction, we first analyze the creditor's liquidation decision upon the report at time t. As stated earlier, the creditor may liquidate the project only upon a bad‐state report; if the report is uninformative about the state or reveals a good state, the creditor does nothing. The creditor liquidates the project upon a bad‐state report if and only if

If the creditor believes that the firm has not exerted effort Given a reporting time t, if the creditor believes the firm has not exerted effort ( if the creditor believes the firm has exerted effort (

All proofs are in the Appendix.

The effort decision and the debt repayment decision

Back to time 0, the firm's decision on whether to exert effort is based on the creditor's requested repayment D and its conjecture about the creditor's future liquidation strategy. The creditor, when determining the requested repayment D, conjectures the firm's effort decision. If the firm's conjecture is that the creditor believes effort has been exerted ( If the firm's conjecture is that the creditor believes effort has been exerted ( We call this equilibrium the “Effort, Liquidation upon bad report” equilibrium, or “(E, L)” equilibrium. Otherwise, we will be in an equilibrium in which the firm does not exert effort, and the creditor in equilibrium correctly conjectures no effort and liquidates upon a bad‐state report. Anticipating no effort by the firm, the creditor's expected payoff is We refer to this equilibrium as the “No effort, Liquidation upon bad report” equilibrium, or “(NE, L)” equilibrium.

The equilibrium strategies

With the analysis of the firm and the creditor's strategies, we present the equilibrium strategies given a reporting time in the following proposition. We denote the “Effort, No liquidation (E, NL) ” equilibrium by “e,nl ” in subscripts, denote the “Effort, Liquidation upon bad report (E, L)” equilibrium by “e,l,” and denote the “No effort, Liquidation upon bad report (NE, L)” equilibrium by “ne,l. ”

“ “ “

The (E, NL) equilibrium and the (E, L) equilibrium do not share any common parameter space because one requires

Distribution of sustainable equilibria.

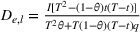

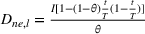

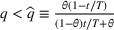

It is also helpful to analyze how the creditor's equilibrium debt repayment decision, D, changes with model parameters. At the beginning of the project, the creditor determines the debt repayment to break even, based on her conjecture of the firm's effort decision and her future liquidation decision. These decisions, in turn, depend on the reporting time as well as parameters c, θ, and q. We summarize the properties of the equilibrium debt repayment in the following corollary. In equilibrium, if if if

Intuitively, the debt repayment always decreases in the prior probability of good state, θ; as the chance of good state and, therefore, the chance of a successful outcome become larger, the creditor asks for a lower repayment to break even. We also find that when the effort cost c is low, the debt repayment decreases in q, whereas when the effort cost is high, the debt repayment is independent of q. When the effort cost is low, in equilibrium the firm is motivated to exert effort, and the higher the effort effectiveness q, the more likely a successful project outcome. Therefore, the creditor's requested debt repayment decreases with the effectiveness of effort. However, when the effort cost is high, in equilibrium no effort is exerted, and thus, the creditor's requested repayment is independent of effort effectiveness.

The way in which the debt repayment changes with reporting time t is interesting. First, when the effort cost c is low, and the reporting time is too late (

However, in other cases, the creditor always liquidates upon a bad‐state report, and we find the debt repayment changes nonmonotonically in t. There are two scenarios that show a nonmonotonic pattern.

One scenario is when the effort cost c is high (the first bullet in Corollary 1). In this scenario, the creditor does not anticipate the firm's effort, and she faces a simple trade‐off regarding the reporting time. That is, an earlier reporting time implies a larger amount of recovered investment from liquidation upon a bad‐state report, but the chance of receiving the state information by the reporting time (and thus the chance of liquidating upon a bad‐state report) is also smaller; whereas a later reporting time results in a smaller liquidation value but the chance of receiving the state information is greater. In this case, the debt repayment changes nonmonotonically in the reporting time with a U‐shaped pattern (first decreases and then increases in t). If the reporting time is close to the beginning (t is close to 0), it is almost impossible to receive the state information by t and thus no way to liquidate; therefore, the creditor sets a large debt repayment. As the reporting time is delayed, the likelihood the creditor is able to liquidate and recover some of her investment increases, and therefore, the debt repayment decreases. However, when the reporting time is delayed further, although the likelihood of receiving the liquidation value increases, the liquidation value diminishes; therefore, the creditor's requested debt repayment starts to increase as the reporting time gets later.

Another scenario is when the effort cost is low but the effort is not effective (the second bullet in Corollary 1). In this scenario, the creditor faces a more subtle trade‐off. She still liquidates upon a bad‐state report, but she conjectures that the firm has exerted effort, and thus, she also considers the opportunity cost of liquidating a bad‐state project that could be a success. Due to this additional cost of liquidation, although her debt repayment still follows a nonmonotonic, U‐shaped pattern in the reporting time, it starts to increase sooner in t (that is, the lowest debt repayment happens sooner) than in the high effort cost scenario.

THE OPTIMAL CHOICE OF THE REPORTING TIME

We now analyze the regulator's optimal choice of the reporting time in this single‐firm/industry setting. We characterize the optimal reporting time in the cases of “high effort cost” and “low effort cost,” respectively.

High effort cost

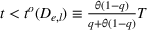

When the effort cost is sufficiently high, it is not desirable to induce effort in equilibrium because the effort does not improve overall efficiency due to its high cost. As there is no effort exerted in equilibrium, a bad‐state project generates zero cash flow with certainty. Therefore, the creditor should always liquidate the project upon a bad‐state report. In other words, the optimal equilibrium to induce is the “No effort, Liquidation upon bad report (NE, L)” equilibrium. In this case, the timing of the report has two effects. On the one hand, as the probability that the state of the project is revealed gradually increases as the project progresses toward the final point T, it may be beneficial to have a late reporting time and thus, a larger likelihood of an informative report. On the other hand, the sooner the creditor liquidates the project, the more she can recover from her investment. If the reporting time is very late, the creditor suffers from a lower liquidation value even if she liquidates the project immediately upon a bad‐state report. The regulator's optimal choice of the reporting time, denoted by When c is sufficiently high (

Low effort cost

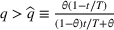

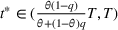

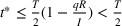

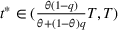

The case of low effort cost is more interesting. When the firm's effort cost is sufficiently low, as the effort may overturn a bad‐state project to be a success, it is efficient to induce the firm to exert effort in equilibrium. However, it may or may not be efficient to induce the creditor's liquidation upon a bad‐state report. We find that the reporting time to maximize efficiency depends on the effort effectiveness, q. Specifically, we have the following results: When c is sufficiently low ( if q is high ( if q is low (

Proposition 3 shows an interesting result that, to induce effort from a low‐cost firm, the optimal reporting time is either early enough or late enough, depending on the effort effectiveness. When the firm's effort is highly effective in overturning bad‐state projects (

In contrast, when the firm's effort is not as effective (

To further understand the results in Proposition 3 , we analyze the cost and benefit of inducing liquidation upon a bad report, given that the firm exerts effort in equilibrium. On the one hand, inducing the creditor to liquidate upon a bad‐state report provides the creditor with more protection, because she is able to obtain the liquidation value instead of losing all her investment if the outcome turns out to be a failure. Therefore, the creditor asks for a lower requested repayment, D; that is, the firm's expected financing cost is lowered, which implies higher overall efficiency (i.e., higher expected payoff of the firm). We call this benefit of allowing liquidation the lower repayment benefit. On the other hand, inducing liquidation also has a downside of inefficient liquidation, as the creditor may liquidate a project that, if not liquidated, would be successful and generate a higher payoff in the end. This downside of inducing liquidation represents an opportunity cost.

We can express the lower repayment benefit of inducing liquidation by

The opportunity cost of inducing liquidation can be expressed as

Given that the lower repayment benefit of inducing liquidation is concave in t while the opportunity cost linearly increases in t, and the lower repayment benefit equals the opportunity cost at

The benefit and cost of inducing liquidation, given a sufficiently low effort cost c and

The benefit and cost of inducing liquidation, given a sufficiently low effort cost c and

When

When

THE OPTIMAL CHOICE OF THE REPORTING TIME FOR AN ECONOMY

Thus far, we have examined the regulator's optimal choice of the reporting time in a single‐firm/industry setting. In reality, a regulator needs to set a reporting time for a whole economy composed of heterogenous firms/industries. We, therefore, pose a more interesting and relevant question that will provide regulatory implications: In an economy with firms from heterogenous industries, what should be a regulator's choice of reporting time to maximize overall efficiency?

We now examine an economy with a continuum of firms with heterogenous characteristics, including the effort cost and the effort effectiveness. For convenience, we assume each firm is a representative firm of an industry. Each firm's effort cost is

We have shown in the single‐firm/industry setting that when the effort cost is high ( In an economy with varying effort costs and effort effectiveness: if if

We find that the regulator's optimal choice of the reporting time for the economy

How

However, when θ becomes sufficiently high, as most projects in the economy are good, inducing effort is no longer important. Instead, the regulator cares more about saving the liquidation value for creditors. Hence, the regulator sets the reporting time to be earlier and closer to the middle point in order to retrieve more liquidation value. Once θ increases to 1—that is, once all projects in the economy are good—firms' effort is completely useless and retrieving liquidation value is the regulator's only goal. In this extreme case, the regulator sets the reporting time to the middle point to achieve the maximum expected liquidation value. 9

EXTENSIONS

Imperfect state information

In our main setting, we assume that the state information is received with some probability that increases with time, but if the information is received, it is perfect and accurately reflects the state. Here, we examine an alternative setting in which the firm can obtain a signal regarding the state at any given reporting time, but the signal can be incorrect and its accuracy is increasing with time. We believe this analysis is important, as it provides further insights into the debate regarding the timeliness and accuracy trade‐off of earlier reporting.

At the start of the project, the state of the project is unknown. Once the project is undertaken and is in progress, the firm can obtain and report a signal regarding the project's state,

We first analyze the creditor's liquidation decision upon the report at time t. The creditor liquidates the project upon a report of b if and only if

Back at time 0, the firm's decision about whether to exert effort is based on the creditor's requested debt repayment D and its conjecture about the creditor's future liquidation strategy. The creditor, when determining the repayment D, conjectures the firm's effort decision. As the firm's effort strategy is similar to that in our main setting, we relegate the related analysis to the Appendix in the Supporting Information.

Equilibrium strategies and the optimal reporting time

We find that, besides the three equilibria we have in the main setting, we now have an additional equilibrium, a “No effort, No liquidation (NE, NL)” equilibrium. This equilibrium arises because, unlike in the main setting, the state signal is not perfect, which raises the possibility that the project is good even though the signal is b. When the prior probability of a good state is sufficiently high, the creditor ignores the signal and never liquidates the project, even when no effort is exerted in equilibrium. With an imperfect signal, there is one new equilibrium. “

We now characterize the regulator's optimal choice of the reporting time in this setting with the possibility of an inaccurate signal. With an imperfect signal: when when when if q is high, the optimal reporting time satisfies if q is low, the optimal reporting time satisfies

First, note that when the prior belief of a good state is strong (

Private information before the effort decision

In the main setting, the firm has no information about the project state before its effort decision, and there is no information asymmetry between the firm and the creditor regarding the state. However, in reality, as a firm has closer proximity to the project, it may get more information about the project prior to determining its effort. In this section, we examine an extension of the main setting, in which the firm receives a noisy private signal

The equilibrium analysis

Given a requested debt repayment, D, upon receiving its private signal σ, if the firm anticipates no liquidation, we show that it exerts effort when With the firm's private signal, there are two new equilibria in which the firm only exerts effort upon private signal, “ “

Private information and efficiency

One may believe that additional private information for the firm would help improve overall efficiency, as the firm would now have more information about the project state and could make more efficient effort choices. However, our analysis shows that this is not always true. When the firm's effort cost is intermediate and δ is low, endowing firms with additional private information reduces overall efficiency; otherwise, the firm's private information improves overall efficiency.

To understand the intuition behind this result, note that when the effort cost is low, the firm exerts effort regardless of its private signal. Hence, overall efficiency is the same as in the main setting in which the firm has no private information. Similarly, when the effort cost is high, the firm does not exert effort regardless of its private signal, and thus, overall efficiency is the same as in the main setting. Only when the effort cost is in an intermediate range does the firm's private information play a role, as the firm tailors its effort decision based on its private signal (i.e., the firm only exerts effort upon signal

The optimal reporting time with private information

Now, we study how the firm's private information affects the regulator's optimal reporting time choice. First, we observe that if the firm's private signal is too noisy (δ is sufficiently low), according to Corollary 2, private information hurts; therefore, it is efficient to induce the firm to ignore its private signal in equilibrium, and thus, the analysis of the optimal reporting time remains the same as in the main setting. Furthermore, even if the firm's private signal is sufficiently precise, if the effort cost is very high (low), the firm never (always) exerts effort anyway; therefore, the private signal still plays no role in the firm's effort decision, and again, the analysis remains the same as in the main setting. However, when the private signal is informative enough and the effort cost is not extreme, the optimal equilibrium to induce is either (Eb, L) or (Eb, NL); that is, it is efficient to induce effort only upon signal In the setting with private information: when δ is low or the effort cost is very high/low, the optimal reporting time results are the same as in the main setting; otherwise, when δ is high and the effort cost is not extreme, if if

As the above proposition shows, with the private information, the optimal reporting time results are very similar to that in the main setting, except that now the precision of the private information, δ, also plays a role. Particularly, when the private information is sufficiently precise and the effort cost is not extreme, the optimal reporting time is set to induce (Eb, _) instead of (E, _). Nevertheless, the intuition remains the same.

CONCLUSIONS AND IMPLICATIONS

This study uses a parsimonious model to study the timing of reporting and highlights the role of firms' effort decisions. We find that the regulator's choice of reporting time to maximize overall efficiency is determined by a trade‐off between motivating the firm's effort to improve the outcome and saving the liquidation value for the creditor to reduce the firm's financing cost. If effort is too costly, the optimal reporting time is at the mid‐point to induce no effort and to maximize the expected liquidation value. However, if the effort cost is not that high, it is efficient to motivate the firm to exert effort. Interestingly, to induce the firm to exert effort, we find the reporting time should be either early enough or late enough, depending on the effectiveness of effort in turning bad projects into successes. When the firm's effort is effective in overturning bad‐state projects into profitable ones, it is efficient to set the reporting time to be late, as the late reporting time guarantees no future liquidation and thus motivates the firm's ex ante effort. When the effort is not effective, it is optimal to set the reporting time to be sufficiently early. In this case, as the reporting time is early, the chance of an informative report is relatively low, and thus, the probability of liquidation is small enough to motivate the firm's effort. Nevertheless, as effort is not highly effective to overturn a bad project, it is efficient to allow the creditor to liquidate upon an early, bad‐state report to recover more liquidation value (which helps reduce the financing cost for the firm).

We also find that in an economy with heterogenous industries, the regulator's optimal choice of reporting time changes nonmonotonically in the probability of good projects. When most projects in the economy are bad, inducing low‐cost firms to exert effort is the regulator's priority because the effort can turn bad projects into successes. As the probability of good projects increases from a very low start point, the regulator sets the reporting time later to reduce the liquidation value and discourage the creditor from liquidating the project, which motivates firms' effort. However, once the probability of good projects is sufficiently high, inducing effort becomes less desirable. Therefore, the regulator weighs more on saving liquidation values and sets the reporting time earlier and closer to the mid‐point.

Our study may provide some empirical implications for future research. For example, we show that the optimal reporting time should be late if the firm's effort plays an important role in determining the outcome, whereas if the effort is not important or effective, it is better to have an early reporting time. This result implies that accelerating mandated financial reporting may have a negative impact on industries in which human capital investments and innovations are crucial for success (e.g., technology industries, pharmaceutical industries), whereas the acceleration may benefit some traditional, standardized industries in which human capital inputs are not so crucial (e.g., food industries, retailing industries). Our prediction can be potentially tested empirically by examining capital market responses in different industries to changes in mandated reporting timing. There are some extant empirical studies that analyze capital market responses to accelerated reporting requirements. For instance, Doyle and Magilke (2013) show that large filers experience greater capital market reactions to accelerated reporting requirements than small filers, and Kajuter et al. (2018) document a decrease in firm value for small firms required to switch from semi‐annual to quarterly reporting. Future empirical research may follow these studies' methods and test our prediction by comparing capital market reactions to the acceleration across different industries, and examine whether technology and pharmaceutical companies suffer from negative capital market reactions when the SEC accelerated the deadline for filing annual 10‐K reports and the 8‐K reports.

Additionally, we show that the optimal reporting time in an economy changes nonmonotonically in the probability of good‐state projects. If most projects in the economy are bad, the regulator should set the reporting time late. However, once the probability of good projects is high enough, the optimal reporting time becomes early. This result indicates that an early reporting time may be optimal for booming industries/economies with many good opportunities but may hurt struggling industries/economies. Empirically, this prediction may be tested by looking at whether the SEC's acceleration of filing financial reports affects struggling industries versus booming industries differently.

Our study also has some regulatory implications. We show that earlier reporting may or may not be desirable in maximizing overall efficiency. If firms' effort is helpful but not highly effective in improving profitability, then it is efficient to require earlier reporting, which echoes the SEC's recent push to an accelerated reporting deadline to improve welfare. This probably applies to most traditional industries with stable business models. However, if firms' effort is highly effective and plays a critical role in the success of the business, it is better to require a relatively late reporting time. For example, for some emerging industries/businesses that rely heavily on human capital to be competitive and successful, it may not be a good idea to enforce earlier reporting. As the effectiveness of effort determines whether the optimal reporting time should be sooner or later, we demonstrate that it might not be efficient to subject all industries to the same reporting requirements.

Footnotes

ACKNOWLEDGMENTS

We would like to thank the department editor, senior editor, and the reviewers at Production and Operations Management for their excellent suggestions. We would also like to thank Ted Goodman for his valuable feedback.

1

In addition to the acceleration of 8‐K disclosures, the SEC also accelerated the deadline for filing annual 10‐K reports from 90 to 75 days, claiming that “it will accelerate the delivery of information to investors and the capital markets, enabling them to make informed investment and valuation decisions more quickly” (SEC, ![]() ). For large filers, the SEC further accelerated the deadline for filing 10‐K report from 75 to 60 days, as well as the filing of 10‐Qs from 45 to 40 days.

). For large filers, the SEC further accelerated the deadline for filing 10‐K report from 75 to 60 days, as well as the filing of 10‐Qs from 45 to 40 days.

2

Some examples of forward‐looking information that regulators ask firms to disclose include assessments of asset impairment and loan loss reserves, estimations of allowance for uncollectibles, evaluations of contingencies such as potential litigation losses, and discretion on revenue recognition according to ASC 606.

3

Although we assume financing through debt markets in the main setting, our results and analysis still hold if we consider a setting with equity market financing. A detailed analysis is available upon request.

4

We also examined an alternative setting with continuous support for the firm's effort,

5

In Subsection 6.1, we consider an alternative setting in which the information in the report may be incorrect, and its accuracy increases in time. Moreover, in Subsection 6.2, we also consider a setting in which the firm may receive private information about the project state before its effort decision.

6

We only focus on the information in the report regarding the project state, while in reality financial reports contain many other items that firms are required to report.

7

Alternatively, it can also be the case that the creditor invests continually in the project over the time period. If the bad state is revealed, the creditor can stop further investment and thus save the remaining capital.

It is easy to verify that the creditor does not want to liquidate upon a report with no information on the project state because the creditor's prior belief is not updated.

8

Note that the regulator's choice of

9

In our model, the firms' effort costs follow a uniform distribution. It is also interesting to consider a scenario in which in an economy the firms' effort costs follow a skewed distribution that features a very high fraction of high‐cost firms. In such a scenario, as it is not optimal for the regulator to induce effort from high‐cost firms, the regulator mainly cares about protecting creditors' liquidation value to lower firms' financing costs; therefore, the optimal reporting time would be close to the middle point,

PROOFS

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.