Abstract

Firms who buy from suppliers often engage in supplier development to reduce the supplier's production cost. Being aware that their efforts may benefit a rival firm when there is a shared supplier, some buyers only invest in “specific supplier development,” that is, in those processes or technologies where spillover cannot occur. Other buyers willingly accept the spillover that arises from supplier development, and invest in “generic supplier development.” Our game‐theoretic model captures a buyer's choice to invest in these distinct supplier development types as a way to endogenize spillovers. In contrast to the literature, this paper considers the benefits of investing in a combination (i.e., portfolio) of cost‐reducing generic and specific supplier development. We demonstrate how supplier development affects a shared supplier's wholesale pricing decisions; whereas generic supplier development lowers wholesale prices equally across buyers, specific supplier development only lowers the wholesale price of the investing party. Our model shows that buyers should treat the spillovers from generic supplier development as an investment opportunity rather than a threat. In equilibrium, a buyer will always invest in a portfolio of both supplier development types, and having a better generic than specific investment capability may even make generic supplier development the most prevalent option for him, depending on the level of competition. Moreover, even if the buyers can commit to only investing in specific supplier investment, the resulting equilibrium gives lower buyer profits than a portfolio that includes generic investments. We also find that the presence of specific investments may raise generic supplier development, benefiting all supply chain actors. However, incorporating specific supplier development into a supplier development portfolio or a commitment to investment in only specific supplier development can lead to a prisoner's dilemma in terms of buyer profits. We show how investment capabilities and competitive intensity drive the buyers' investment decisions and supply chain actors' profits. The paper's main results also hold for asymmetric generic investment capabilities, though we highlight that the least capable buyer will free‐ride on his rival's investments, consequently making him earn higher profits.

INTRODUCTION

Many downstream firms engage in supplier development activities to help improve supply chain metrics such as supply base cost, quality, delivery performance, lead time, and productivity. For instance, in the automobile industry, Honda's supplier development program has raised suppliers' productivity and quality by about 50% and 30%, respectively, while much of the supplier's cost savings are shared with Honda (Liker & Choi, 2004). Similarly, firms like Toyota, Porsche, and Renault‐Nissan have dedicated supplier improvement teams with key capabilities that the suppliers often lack. Interfirm competition seems to be an important factor pushing firms to raise their supplier development investments. For instance, when automaker Hyundai‐Kia was lagging behind Toyota in terms of supplier management, they replicated its supplier development practices while aiming for similar benefits (Dyer et al., 2018).

Firms that compete often source their inputs from shared (or common) suppliers. This begs the question, what happens when the knowledge generated within a particular buyer–supplier relationship as a result of supplier development spills over to the rival buyer. Some buyers consider such spillovers a serious concern (Muthulingam & Agrawal, 2016). The tractor manufacturer John Deere, for example, made substantial investments in supplier development programs to establish a superior supplier base. However, the firm became suspicious of rivals' efforts to free‐ride on their investments, leading them to reconsider their supplier development training program (Mesquita et al., 2008). At the same time, some investments in castings or information systems are unique to the relationship with an individual supplier, yielding cost savings that only benefit John Deere (Stegner et al., 2002). Some buyers value confidentiality in supplier development to such an extent that they even help the supplier physically separate manufacturing operations for the buyer, preventing competitors from getting deep insight into these processes (Handfield et al., 2000).

Other buyers in the automobile industry take quite the opposite stance. Honda managers take the perspective of “a rising tide lifts all boats,” welcoming the knowledge transfer of supplier development to rivals such as Ford and GM (MacDuffie & Helper, 1999). Toyota is also well aware of the spillovers to rivals from supplier development and is willing to accept these (Dyer & Hatch, 2006). Moreover, Toyota embeds the supplier development activities that generate spillovers into a portfolio of supplier development types, as its supplier development program targets not only suppliers' generic production capabilities but also processes purely dedicated to Toyota such as tailored computer‐aided design (CAD) systems and shared inventory systems (Liker & Choi, 2004).

The potential existence of spillovers in the context of supplier development is clearly recognized by buyers. Yet, the examples mentioned above illustrate that buyers have divergent ways of dealing with these. We devise a game‐theoretic framework to explicitly capture these opposite choices. An important feature of the model is the consideration of investment spillover as an endogenous phenomenon, which is in line with practice because buyers have different investment options. To do so, the model accounts for the crucial difference between investment in knowledge exclusive to the relationship and those supplier development investments that spill over to a rival buyer. That is, we differentiate between supplier development investments into a shared supplier's specific production technology and generic production technology. An example of “specific supplier development” (also referred to as “specific investments”) is a buyer purchasing a computer numerical control (CNC)‐machine tailored to making parts for this buyer only, installing it at the supplier's site, and training the supplier to work with the machine. Examples of “generic supplier development” (or, “generic investments”) include a buyer's investment in a part of a supplier's production line that also serves other buyers, or an investment into a supplier's corporate lean manufacturing program. Another novel feature of our model, in line with the Toyota example given above, is that the buyers have the opportunity to invest in a portfolio of supplier development types. This allows us to study the interaction between generic and specific supplier development decisions, whether the buyers and the shared supplier benefit from investing in a portfolio of investment types or prefer focusing on a particular supplier development type instead.

In our framework, the buyers invest in generic and/or specific supplier development, before the shared supplier decides on her optimal wholesale prices. In setting prices, the supplier can discriminate between the buyers and can decide for each of the buyers how much of the cost reductions resulting from supplier development she returns to the buyers in lowering her wholesale prices. In studying the buyers' investment decisions, we consider two important model elements that drive the paper's results. First, we allow a buyer's capability to invest in generic supplier development to be different from specific investment capability, which means that investment in one supplier development type may be costlier than investment in the other. This is quite natural as, for example, a buyer may excel in manufacturing engineering, making it easy to clearly pinpoint improvements at the supplier's side from which the buyer can directly benefit. But, at the same time, the buyer may implement a costly supplier development training program from which the rival benefits as well. These capability differences affect a buyer's preference to invest in one type over the other. We also study what happens when the buyers differ in terms of their generic investment capability. Second, this paper investigates the role of competitive intensity in the product market, which is modeled as product substitutability. If the buyers are monopolists in their own respective markets, then supplier development spillovers are unlikely to be a cause of concern as they do not harm the firm's competitiveness. Higher levels of rivalry raise the relative importance of specific supplier development as the buyer uses specific investments to differentiate himself from his rival (via a lower wholesale price).

Consequently, our analyses center around three main questions: (1) What choices will the buyers make, if they can invest in a portfolio of generic and specific supplier development? (2) How do the buyers' equilibrium choices depend on competitive intensity and supplier development capability? (3) What are the profit implications for the buyers and shared supplier given the equilibrium investments, and what happens if the buyers can commit to excluding specific or generic supplier development? In answering these questions, we obtain a range of new insights, which help to explain why different approaches are observed in practice:

First, we find that the buyers will always gain from using both generic and specific supplier development in their portfolio. The opportunity to make generic investments benefits both buyers equally and provides the buyers an incentive to raise their specific investments. For low levels of competition, generic supplier development levels—that is, the cost reductions resulting from generic investments—may exceed those of specific supplier development, but as competitive intensity grows, specific supplier development becomes a more important tool for the buyers, and this holds even when the buyer has greater capability for generic investments. An important insight is that when the buyers are asymmetric in terms of generic investment capability, the most capable buyer will invest more in generic supplier development, but at the same time, his profits are lower than the profits of the least capable buyer, who invests less but free‐rides on his more capable rival.

Second, it is never beneficial for the buyers and shared supplier to exclude generic supplier development from the investment options. The results show that the presence of generic investments always pushes the buyers to raise their specific supplier development levels, and they do so in a way that never hurts them. The supplier benefits from the combination of supplier development investments by selling more products and improving her profit margins.

Third, we demonstrate that for high enough levels of competition and investment capabilities, both buyers and shared supplier would be better off not investing in specific supplier development, and should focus on only generic supplier development. In fact, investing in specific supplier development may trap the buyers into a prisoner's dilemma, both when the buyers invest in a portfolio of supplier development, or when the buyers only invest in specific supplier development. These insights are managerially relevant as they underline the positive role of spillovers from generic supplier development investment while showing that the presence of specific supplier development can actually hurt the supply chain.

This article proceeds as follows. The next section reviews the literature (Section 2). After that, the model is described (Section 3). The results are analyzed in Section 4, and we conclude in Section 5.

LITERATURE

Supplier development refers to a buyer's effort to identify, measure, and improve supplier performance (Krause et al., 1998). Empirical studies have shown how site visits and training programs of supplier personnel positively influence performance dimensions such as on‐time delivery and product design (e.g., Modi & Mabert, 2007). Supplier development has been studied frequently with analytical models. Many of these papers revolve around the decisions of a single buyer (e.g., Iyer et al., 2005; Lee & Li, 2018; Li, 2013). Our paper belongs to the strand of literature involving multiple buyers and one or more suppliers. An example is the study by Jin et al. (2019), who consider a setting with two buyers and two suppliers. The buyers compete in the market selling products that consist of two components, which may be sourced from either of the two suppliers. Their paper incorporates a variety of system structures, centering around the question whether the buyers should integrate with a supplier, and how this decision drives cost‐reducing supplier development. Our model is different in that we consider supplier development spillovers, and the composition of the supplier development portfolio if buyers can invest in a combination of both relation‐specific projects (i.e., specific investments) and generic supplier development projects (i.e., generic investments) that yield a spillover to a rival.

Studies involving spillovers have focused on horizontal competition and cooperation (d'Aspremont & Jacquemin, 1988), horizontal cooperation in supply chains (Gupta, 2008), and vertical cooperation (Ge et al., 2015). While these papers have advanced our understanding of how cooperation mode and locus of innovation affect innovative effort and firm profits when spillovers are exogenous, they provide little insight into supply chain actors' preferences in terms of spillovers, particularly when these spillovers are the focus of a firm's decisions, as in our paper.

Spillovers in supply chains are particularly relevant in networks with multiple buyers and a shared (or common) supplier. Similar to the papers cited above, the supplier development literature in shared supplier contexts has acknowledged the importance of spillovers, but generally assumes that spillover is not the choice of the buyer, or entirely exogenous. A common feature quite central to literature on exogenous innovation spillovers in general and supplier development spillovers in particular, is that some fraction of the investment results, such as unit reduction cost, yield, or product quality, benefits a rival or supply chain partner. Several papers within this stream focus on the context of buyer investments to develop shared suppliers, addressing issues such as investment timing. In the model of Agrawal et al. (2016), the supplier plays an active role in the quality improvement process, while the buyers initially have incomplete information on the quality improvement potential of the supplier. They study the question how the timing of the first investment into a shared supplier is affected by the interplay of spillovers, competition, and supplier capabilities, and they identify the conditions under which the investment is delayed or hastened. Kim et al. (2017) use a repeated model with deteriorating quality of a shared supplier's products. They show why this setting invokes inefficient supplier development delays. Rather than studying the timing of investments and their associated spillovers, our paper focuses on the level of spillover investments, and how they arise in the context of multiple investment types.

Other papers have looked more closely at the size of investments and profitability impacts. For example, Wang et al. (2014) study the effect of supplier development on a shared supplier's delivery reliability. They find that supplier development typically decreases with spillovers, but also that spillovers improve firm profits. In a paper somewhat closer to ours, Friedl and Wagner (2016) find that spillovers of cost‐reducing supplier development hurt investments, although this is shown only for the case where investment costs are independent from the size of the spillover. Papers such as these typically find that firms prefer to suppress spillover investments to raise profits. Our paper, in contrast, paints a more positive picture of spillover investments and shows that by allowing specific and generic investments to be part of an investment portfolio, an investing party would never want to eliminate spillovers from his investments, possibly even to the extent that generic investments are preferred over specific investments.

Spillover endogeneity has been recognized as an important topic in general (e.g., Amir et al., 2003) though investigations in supply chains are unusual. Hu et al. (2020) model a game consisting of an innovative firm that outsources to a contract manufacturer that is possibly a product market rival. They find that the innovative firm may outsource to a product market rival in equilibrium, as outsourcing leads to an innovation spillover but simultaneously allows that firm to charge a price premium. In their study, the occurrence of voluntary spillovers is associated with the outsourcing decision, while in our study, spillovers arise as an investment decision by the buyer. In contrast to our work, none of the papers discussed so far consider investment portfolios, even though it is clear from the examples in the introduction that firms embed different investment types into such portfolios, involving investments with varying degrees of spillovers. Our paper finds the conditions under which firms prefer investment in multiple supplier development types.

Literature studying endogenous spillovers in supplier development investment models is more scarce. The paper most similar to ours is Qi et al. (2015), who model supplier development as capacity investment, and analyze the decisions of two buyers investing in a shared supplier. Their model differentiates between exclusive investment (where excess capacity cannot be used for supplying a rival) and the spillover effect caused by investment in capacity where the buyer is given first priority but where excess capacity can benefit a rival (first‐priority investment). They find that a buyer may allow capacity spillover to a rival if that discourages a rival to invest himself. Qi et al. (2019) extend this work by considering stochastic demand, while the buyers' demands are exogenous but correlated. They obtain the interesting result that firms are more likely to consider the exclusive investment approach when demand correlation decreases. In both papers, the investment regime is a special example of spillover endogeneity.

Our model is different from Qi et al. (2015, 2019) by assuming that supplier development reduces the supplier's production cost. Our framework also differs in terms of the nature of spillovers. In their models, only one firm (with the smallest capacity) can potentially benefit from a (capacity) spillover, while in our model, the buyers can benefit from each other's investments. More importantly, in the context of their models, a buyer engages in either exclusive or first‐priority investment, while simultaneously using both options has little meaning. In contrast, our paper considers cost reduction at the supplier's site as the main target, while these cost reductions can result from different investment types that may or may not benefit the other buyer. In practice, buyers can choose to combine different supplier development investments. Hence, our paper's main concern is studying the benefits of a buyer's investment portfolio, allowing us to consider whether buyers have an incentive to invest in both specific and generic supplier development, and if and how different investment types complement each other. In contrast to their papers, our model also examines how the composition of an investment portfolio is affected by competition and the buyers' distinct capabilities in terms of investing in specific and generic supplier development, which our model allows to differ within a company, but also across companies. This helps to gain managerial insight into how companies' supplier development portfolios should be aligned both with external conditions and the competencies of a firm's supplier development team.

THE MODEL

Our game‐theoretic model comprises a setting with one shared supplier and two buyers. A buyer (he) needs exactly one component for each product he produces. The supplier (she) manufactures a component for buyer

Market demand

Buyer competition is based on prices, which is natural in a context where the buyer exerts effort into reducing the supplier's production cost. In line with past studies such as Anderson and Bao (2010), Cachon and Kök (2010), and Li and Liu (2021), we model buyer

We assume

Supplier development investments

When a buyer engages in supplier development, he reduces the supplier's unit production cost while carrying the investment cost. The cost reduction can be seen as the direct result of targeted process improvements. Similar to Hu et al. (2017), the supplier's pricing decisions are separated contractually from any supplier development investments. This reflects current practice in, for instance, the automobile industry (Sako, 2004). To incorporate endogenous supplier development spillovers, the buyers may invest into the supplier's generic and specific production technology. We denote

In the model, the results of generic investments yield a spillover to a rival buyer, while those of specific investments do not. Formally, the cost of supplying buyer

As typically organizational budgets are constrained, it is common to model investment costs of cost reduction projects, including supplier development, as convex functions that represent decreasing returns to scale (d'Aspremont & Jacquemin, 1988; Veldman et al., 2014). We will assume quadratic costs, and consider total investment costs for buyer

Decision sequence and information structure

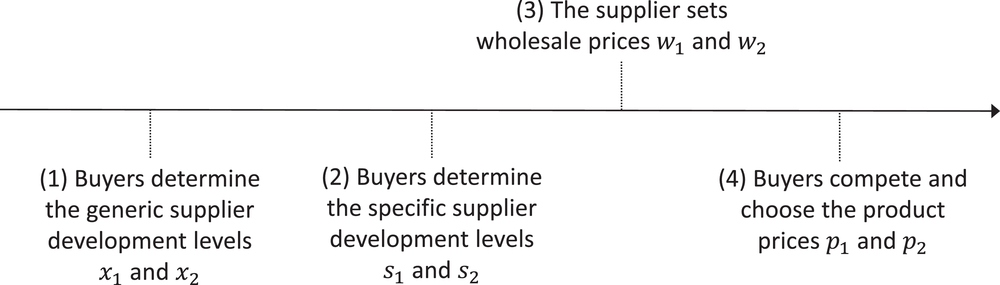

In setting up our model, we need to make choices about the sequence of events, and the information that is available. A timeline of the game is given in Figure 1. In the first two stages, generic and specific supplier development decisions are made. It is most natural to assume that for each buyer the specific supplier development level that is achieved is private information and not available to the other buyer. A buyer's generic supplier development level on the other hand is most likely to be known to the other buyer, and this is consistent with the spillover benefit available to the other buyer. In practice, opportunities for investment will occur at different times, so that a model of simultaneous investment in both generic and specific supplier development is less appropriate. Because of the absence of information available to the buyers on the amounts of earlier specific investment, a model in which specific investment occurs before generic investment reduces to the case of simultaneous investment. A further observation here is that generic investments often take place over a relatively long term. For these reasons, we have concentrated on the case where generic investment occurs first while noting that the paper's main results are robust to alternative model formulations where generic and specific investments are made simultaneously. 1

Timeline of the game

In the third stage, the supplier takes stock of the cost reductions stemming from supplier development before she decides on

In the last stage, the buyers observe

In this multistage game between the buyers, we look for a Nash equilibrium in pure strategies. Subgame‐perfect equilibrium outcomes are found using backward induction. Initially we assume that the buying firms are identical and we find that equilibria are symmetric, but our analysis is general and we later consider the asymmetric case. We use superscript

ANALYSIS

We note that each of the cases we consider has an associated feasible parameter region

Buyer and supplier pricing decisions

In the last stage, the supplier development investment costs are sunk, such that the buyer's problem is given by

This shows that product market prices are strategic complements as

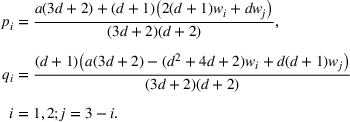

This demonstrates that the buyer that pays the lowest wholesale price also maintains the lowest product price, so that supplier development has strategic value if the resulting cost reductions induce the supplier to drop her wholesale prices. The equilibrium prices and quantities as functions of the supplier's wholesale prices are

In the preceding stage, the supplier determines her wholesale prices by solving

The expression in (5) shows that the wholesale price charged to buyer

Substituting these wholesale prices into the supplier's profit function, we have positive supplier profit margins for supplying buyer

The structure of the portfolio investment

In the second stage, after values for

We can show that the denominator in (6) is positive. Thus, we see that

Using the superscript

Notice that always

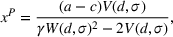

In the first stage, generic supplier development levels are chosen. From the reaction functions (which we do not show here for reasons of space), we can show that

The generic equilibrium supplier development levels are

We can check that both

A comparison between If the buyers can invest in both generic and specific supplier development, then there exists a threshold

Figure 2 illustrates Proposition 1, for different values of

The (dashed) switching curve

When

Now, we consider the way that the equilibrium outcomes change with the intensity of the buyers' rivalry. Product market competition has the following effects on the equilibrium outcomes for fixed values of γ and σ: Both the generic supplier development level The specific supplier development level The supplier's profit

That generic supplier development decreases in

It is more surprising that the signs of

Illustration of Proposition 2 to show how

The change in the supplier development levels leads to a change in supplier profits, which begin by increasing with

An extended analysis with

We can also analyze the relationships between the supplier development levels and profits for the two buyers in this asymmetric case, and we obtain the following proposition: When buyer the generic supplier development level of buyer the profits of buyer

The effect of asymmetric γs on generic supplier development levels is straightforward: The buyer with the highest generic investment capability chooses the highest level of generic supplier development. The second part of the result, that the more capable buyer is always worse off than his rival, is interesting. This result is driven by the fact that

The impact of generic investment

We have seen how the portfolio investment situation, in which both types of investment are possible, will lead to both types of investment being made in equilibrium. However, this does not answer the question as to whether restricting investment to only one type might be beneficial if both buyers were to commit to this in advance. In practice, many buyers treat specific supplier development as the instrument of choice in trying to gain a cost advantage over rival buyers while other buyers resort to generic supplier development, which is why we investigate whether buyers who only invest in specific supplier investment have any incentive to introduce generic investment. Proposition 4 shows that it is never beneficial for the buyers to restrict investment to specific supplier development, nor is it beneficial for the supplier for this restriction to be in place (we use the superscript Introducing generic supplier development in addition to specific supplier development has the following effects: The specific supplier development level always increases, that is, The buyer's profit always increases, that is, The supplier's profit always increases, that is,

Comparing

We can revisit the results given in Proposition 4 to see whether these change when the buyers are asymmetric in their generic investment capabilities. It turns out that all the results of this proposition continue to hold in this asymmetric case.

The impact of specific investment

The previous subsection showed that it is always beneficial for the supply chain actors to invest in generic supplier development as well as specific supplier development, while the resulting portfolio displays positive generic investments and increased levels of specific investments. In this section, we carry out a similar analysis, but now considering a situation in which the buyers choose to restrict themselves to generic investments only. We have seen how some companies such as Honda take a particularly favorable stance toward generic investments. We will show that if the product market competition is high enough, it will be beneficial for both the buyers to commit to only making generic investments. Recall we use the superscript Let If There is a switching curve

The effect of specific supplier development on generic supplier development can be demonstrated by comparing

The (dashed) switching curve

Proposition 5.i also considers the buyers' profit. Interestingly, for those parameters where

It is easier for the supplier to enforce a restriction on the types of investment that she will allow from buyers. This makes the second part of Proposition 5 of interest, since it shows that for

The (dashed) switching curve

Finally, similar to the previous analysis, we can consider

The buyers' prisoner's dilemma

We complete our analysis by considering the possibility that buyer profits are highest if both buyers can commit to not investing at all. Investment commitment games such as these can yield this type of prisoner's dilemma for the investing party. The following proposition identifies the parameters for which this may occur, using π0 to denote a buyer's equilibrium profits if the buyers do not invest. Comparisons of buyer profits with no investment at all, π0, to buyer profits under the investment regimes of generic investment only, Investment in generic supplier development only is always better for the buyer's profit than no investment at all, that is, If There is a switching curve

From Proposition 6.i, we see that if the buyers can commit to making generic investments only, then this is always preferable to not investing at all. The supplier development spillovers yield symmetric wholesale price reductions from which both buyers always benefit.

The situation is different for the buyers if only supplier‐specific investment options are available (Proposition 6.ii). Given σ, for small enough levels of competition, the buyers refrain from overinvesting in specific supplier development, making them always better off if positive investments are made. Notice that the choice of

Finally, according to Proposition 6.iii, a prisoner's dilemma can also occur when the buyers invest in a portfolio of supplier development types. The switching curve

CONCLUSION

In many manufacturing industries, a buyer will invest in supplier development to reduce the supplier's production cost. At the same time, the cost reduction resulting from such investments often spill over to competitors that source from the same (shared) supplier. Buyers should make careful decisions about the nature of their supplier development activities and proactively manage these spillovers. Though there is a wealth of evidence that in practice buyers' stance toward supplier development spillovers differs significantly, the literature has largely treated such spillover as an exogenous phenomenon. We argue differently and let the spillovers generated from supplier development investments be a choice of the buyer. We do so by explicitly differentiating between specific and generic supplier development. A buyer's investment in specific supplier development yields benefits unique to the relationship, while an investment in generic supplier development benefits a buyer's rival equally. We constructed a simple model and investigate a buyer's equilibrium portfolio decisions under different levels of competition and investment capabilities. Moreover, we assess the effectiveness of incorporating generic and specific investments into the buyers' investment portfolio.

Several conclusions can be drawn from our analysis. We first observe that buyers make strictly positive generic investments, although specific investment is the buyers' main focus as competitive intensity increases if the buyers' investment capabilities are not too far apart. Buyer asymmetry in terms of differing generic investment capability does not fundamentally alter this result, though this does yield a remarkable outcome for the buyers, with the least capable buyer earning more than his more capable competitor. Thus, the spillovers resulting from generic supplier development persist even if the least capable buyer free‐rides on his capable rival. We also conclude that while the buyers should always invest in generic supplier development, this may not hold for specific investments. Specific investments turn out to make competition particularly fierce. This may not be a concern for the buyers when specific investments are embedded in a portfolio of investments, as the buyers are able to establish a proper balance between them. Yet, a focus on specific investments alone may trap the buyers into a prisoner's dilemma, with committing to no investment at all or generic investment only clearly being the preferred option. Finally, we conclude that the buyers' preferences may be different from those of the supplier. That is, for those parameters where the buyers prefer excluding specific investment from their portfolio (if they can commit to doing so), the supplier's preference may be to keep them. While the buyers' concern may be not to overinvest in specific supplier development to keep competition in check, the supplier actually benefits from intense rivalry. Managerially, these and other insights suggest that the buyers' investment capabilities and level of competition present in the product market are important driving forces of supplier development levels, and the resulting buyer and supplier profits. For many companies, it is crucial to recognize that the spillovers resulting from supplier development are beneficial for them, and that the use of a supplier development portfolio can enhance their profits, compared to restricting their attention to one supplier development type only.

Several future research opportunities exist. The model could incorporate a supplier's efforts as a determinant of the success of supplier development endeavors. Those efforts may not be observable by the buyers (as in Iyer et al., 2005). It is expected that this will lead to increased generic supplier development investments while specific supplier development investments are likely to drop. Also, our model relies on cost reduction as the main result of buyers' investments. It is important for supplier development research to also focus on sustainability outcomes , while in such a context, it is likely that the mechanisms and preferences for generic and specific supplier development change. Our model can be adapted to cater for this, for instance, by incorporating the demand effects of a product's sustainability features, cost effects at the product level, alternative investment cost functions (e.g., fixed instead of quadratic cost), and contractual mechanisms that ensure that the supplier manufactures a sustainable product.

Footnotes

ACKNOWLEDGMENT

We thank the Department Editor Jürgen Mihm, the anonymous senior editor, and two anonymous reviewers for their helpful feedback.

1

We have analyzed the outcomes of a three‐stage model in which buyers make both generic and specific investments at the same time. The main results of the paper continue to hold under this alternative model specification, with one notable exception. According to Proposition 5.i, there is a switching curve (illustrated in Figure 4) showing that for certain parameters, a buyer's generic supplier development level may be higher in the absence of specific investments than it is in the portfolio case (specifically, given a buyer's specific investment capability (σ), we see that ![]() ). In the three‐stage setup, in contrast, we always have that

). In the three‐stage setup, in contrast, we always have that

2

Nevertheless, there is a stream of literature that considers unobservable wholesale prices or, more generally, unobservable contract terms. In this case, we may still assume that the players determine the actions that match the usual equilibrium. However, the supply chain actors may also gain an advantage by behaving differently. This leads to different possible equilibrium concepts, centered around the different types of beliefs a downstream supply chain actor may hold with respect to the rival's contract terms (e.g., McAfee & Schwartz, 1994). Applications in the operations management context mostly rely on passive beliefs, suggesting that when a buyer receives an unexpected offer off the equilibrium path, it does not revise his beliefs about the offer made to the rival (e.g., see Arya & Mittendorf, 2013; Li & Liu, ![]() ). Throughout this paper, we assume the buyer has full information on his rival's contract terms, though we have results to show that the paper's main findings do not change qualitatively under passive beliefs.

). Throughout this paper, we assume the buyer has full information on his rival's contract terms, though we have results to show that the paper's main findings do not change qualitatively under passive beliefs.

CONDITIONS PER CASE

PROOFS

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.