Abstract

We consider a car rental network revenue management (RM) problem, accounting for the key operational characteristics of car rental services such as the varying length of rentals and mobility of inventories, which imply the intertemporal and spatial correlations of rental demands for inventories across different locations and days. The problem is formulated as an infinite‐horizon cyclic stochastic dynamic program to account for the time‐varying and cyclic nature of car rental businesses. To tackle the curse of dimensionality, we propose a Lagrangian relaxation (LR) approach with product‐ and time‐dependent Lagrangian multipliers to decomposing the dynamic network problem into multiple single‐station single‐day subproblems. We show that the Lagrangian dual problem is a convex program and then develop a subgradient‐based algorithm to solve the dual problem and derive an LR‐based bid price policy. To improve the scalability of the LR approach, we further propose three simpler LR‐based bid price policy variants with either location‐dependent or leadtime‐dependent Lagrangian multipliers, or both. Our numerical study indicates that the LR‐based bid price policies can outperform some commonly used heuristics. Using a set of real‐world booking data, we provide a case study in which we empirically demonstrate the operational characteristics of car rental services, calibrate the arrival process of booking requests using a Poisson regression model, and demonstrate that the LR‐based bid price policies indeed outperform other heuristics consistently in both in‐sample and out‐of‐sample horizons.

INTRODUCTION

Revenue management (RM), also called yield management, originated in the airline industry in the 1970s, and has been widely adopted across various industries, including airlines, cruise lines, hotels, car rental, and manufacturing (Talluri & van Ryzin, 2004). See Klein et al. (2020) for a review of the recent developments and applications of RM. For car rentals, one of the successes of RM is that it saved National Car Rental from bankruptcy, turning losses into profits in 1994 (Geraghty & Johnson, 1997). Nowadays, the majority of car rental operators are equipped with RM systems. Carroll and Grimes (1995) describe the RM system implemented in Hertz and report an average revenue increase of

Despite its prevalence in practice, car rental RM has received limited attention in the literature compared with the airline RM that has been studied extensively (Talluri & van Ryzin, 2004). While sharing some characteristics with airlines, such as limited capacity (i.e., resource scarcity) and limited inventory lifetime (i.e., perishability), car rental is also characterized by length of rental (LoR) and mobility of cars among stations, which implies that car rental systems combine the features of advance bookings of airline RM (see, e.g., Talluri & van Ryzin, 1998) and the capacity allocation of queuing networks (see, e.g., Balseiro et al., 2021; Gans & Savin, 2007; George & Xia, 2010; Savin et al., 2005). Note that hotel RM also features advance booking and multiday length of stay, and the usage of a hotel room is similar to the round‐trip; see, for example, Li and Pang (2017) for a discussion on the equivalence of the booking limit control for a hotel and a single car rental station with only round‐trips. Hence, the mobility of cars is a unique feature of the car rental network compared with other hospitality industries such as airlines and hotels. A typical car rental booking request must specify where and when to pick up and return the car, which implies that a car rental product is characterized by the combination of origin, destination, pick‐up time, and LoR. Hence car rental demands for inventories in different locations and days are spatially and intertemporally correlated. The car rental network RM system can be viewed as a stochastic network with advance booking control and therefore has much more complex dynamics than conventional airline RM systems, introducing significant modeling and computational challenges.

Bid price, also referred to as shadow price, is a key economic concept in RM to measure the opportunity cost of a resource. Bid price controls are a class of policies that use the optimal or approximate bid prices of the resources for a product to control its capacity. Bid price policies have been recognized as a powerful tool in RM; see Talluri and van Ryzin (2004) and the references therein. Under bid price control, a booking request for a product as a combination of multiple resources is accepted only if all the associated resources are available and the revenue from this request is greater than the sum of the bid prices associated with the resources of the product (Talluri & van Ryzin, 1998). Such an idea is appealing in practice since it is intuitive and easy to implement once the bid prices are available. However, computing the optimal bid prices can be challenging for network RM problems in light of the high dimensionality of the state space and the lack of analytical tractability, which leads to the research focus on developing efficient heuristics.

An efficient method commonly used in dynamic resource allocation problems is the Lagrangian relaxation (LR) approach. The core idea of the LR approach is to relax the constraints that link different resources through Lagrangian multipliers and then obtain the optimal Lagrangian multipliers as well as the optimal decisions by solving the dual problem. The LR approach was first proposed by Jiang (2006) to solve the probabilistic nonlinear program (PNLP) model for airline network RM. For a dynamic capacity allocation model in airline network RM, Topaloglu (2009) proposes an LR approach that decouples the acceptance decisions for each product over the resources that it uses through product‐ and time‐dependent Lagrange multipliers. Kunnumkal and Talluri (2016) further show that the optimal Lagrangian multipliers can be obtained through a linear programming formulation of the decomposed dynamic programs (DPs). For a spoke‐and‐hub mobility service (e.g., ride hailing) network, Balseiro et al. (2021) propose an LR approach with a single Lagrangian multiplier that relaxes the total capacity constraint to decompose the network problem into multiple single‐station problems with each station (spoke) using dynamic pricing to relocate cars between the spoke and the hub. These LR approaches, though similar in spirit in terms of assigning bid prices to resources to relax resource constraints and decompose a high‐dimensional problem into multiple single‐dimensional problems, do not readily apply to the car rental network RM problems, which need to simultaneously account for the spatial and intertemporal linkages of resources. Our paper aims to fill this gap by introducing an LR approach that captures the aforementioned key operational characteristics of car rental network RM.

More specifically, we consider the bid price control problem for a car rental network. Booking requests arrive sequentially during each day, which is formulated as a discrete‐time point process as an approximation of the Poisson arrival process. Each booking requests a car and specifies the locations (i.e., the origin and destination stations) and dates to pick up and return the car. It can be either round‐trip or one‐way. The bookings are restricted to a maximum booking window (the latest pick‐up day from the current day) and a maximum LoR. The rental price for each product is given, with the average daily rental rate varying across products. Upon arrival of each booking request, the operator decides whether to accept the booking.

We formulate the car rental RM problem into an infinite‐horizon cyclic stochastic DP that accounts for the cyclic and stochastic nature of the arrival process of booking requests and the characteristics of car rental products. The goal is to optimize the capacity allocation policy to maximize the expected total discounted revenue. The underlying Markov decision process is described with a set of state variables that represent the number of idle cars for each station and each of the future days that are within the regular booking and rental time window. The regular booking and rental window rolls forward when a new day starts. In car rental, a booking may affect the resources across two stations and over multiple rental days, and its dynamics can be seen as a combination of an advance booking process and a closed queueing network. A booking of a multiday one‐way rental occupies a unit of car of the original station from the pick‐up day onwards and then transfers the car to the destination station, which requires tracking the changes of all states over the rolling time window of all bookings and rentals. The state space of the model grows exponentially as the dimensionality increases.

To tackle the curse of dimensionality, we propose an LR approach to decompose the resources over days and across stations by decoupling the decisions for each booking (product) via Lagrangian multipliers. Inspired by Topaloglu (2009) and Kunnumkal and Talluri (2016), we introduce the product‐ and time‐dependent Lagrangian multipliers to decompose the DP into multiple single‐station and single‐day problems. Intuitively, such a decomposition can be viewed as if there existed a virtual station such that all bookings were independent transactions between the virtual station and individual stations. We show that each decomposed problem with respect to a rental day for a station can be formulated as a finite‐horizon single‐resource DP. For days beyond the current booking and rental time window, it suffices to use a single state variable to describe the dynamics of the system with a rolling time window, and the problem can be formulated as an infinite horizon one‐dimensional DP. Given a set of Lagrangian multipliers, the expected total discounted revenue of the whole system is the sum of the expected total discounted revenue from all stations plus the expected total discounted net profit of the virtual station. We show that weak duality holds.

We characterize the structural properties for the optimal value functions of the decomposed problems. In particular, we show that the decomposed value functions are monotone and convex in the Lagrangian multipliers and the expected total discounted revenue is also convex in the Lagrangian multipliers, ensuring that the Lagrangian dual problem is a convex program. The dual problem provides a mechanism to relink the decomposed problems through these optimal Lagrangian multipliers and provide the tightest bound under LR. We show that there exists an optimal set of Lagrangian multipliers, among which those related to the same product sum to the corresponding rental price. We also show that the dual problem can be solved with a subgradient‐based algorithm. The bid prices based on the optimal Lagrangian multipliers serve as an approximation of the optimal bid prices, which allows us to define a bid price control policy.

The product‐ and time‐dependent approach, though analytically appealing, requires computing a large number of Lagrangian multipliers that grow exponentially with the problem size, leading to limited scalability for large networks. To increase the scalability, we propose a second LR approach that only requires the Lagrangian multiplies to be station‐ and leadtime dependent, which allows us to significantly reduce the number of Lagrangian multipliers. We further restrict the Lagrangian multipliers to be either leadtime dependent or station dependent, leading to two other simplified LR approaches. The subgradient method also applies to these three variants.

We then perform a numerical study to examine the performances of the proposed LR‐based bid price policies against other commonly used heuristics in network RM, including the deterministic linear program (DLP), the PNLP, and the randomized linear program (RLP). The numerical results indicate that the proposed bid price policies outperform the alternative policies in most instances. The second approach, though slightly worse in terms of revenue, is much faster, as expected, making it a strong alternative to the first approach. The third approach yields comparable performance to the second one for small instances, but is outperformed by the latter for larger instances. The last approach has the weakest performance.

To facilitate the understanding of operational characteristics of car rental systems, we provide an empirical case study on a regional car rental network of a major operator. We summarize the characteristics of the bookings among major stations in the network. More specifically, we report the summary statistics for the round‐trip and one‐way bookings between stations, the cumulative bookings for different booking windows, the distribution among LoRs, and the bookings pattern over time. We implement the proposed LR‐based bid price policies and other alternative heuristics using the empirical data. The results confirm the robustness of the superior performance of the proposed LR approaches.

The contributions of our paper to the literature are threefold. First, to the best of our knowledge, this is the first paper that addresses the bid price control problem for a dynamic car rental network RM using the LR approaches. Second, we further advance the developments of LR‐based bid price policies for car rental network RM problems. Although our product‐ and time‐dependent LR approach follows the spirit of Topaloglu (2009) and Kunnumkal and Talluri (2016) for airline RM problems, the analysis and algorithm development are much more sophisticated in a car rental network, which is essentially a stochastic queueing network with advance booking control. To improve the scalability of the LR heuristic, we propose three simpler variants that require much smaller numbers of Lagrangian multipliers. Our numerical study shows that the proposed bid price policies significantly outperform other commonly used heuristics in most of the tested instances. Third, we use real‐world data to provide a case study to validate the model and the performance of the proposed bid price policies, providing more practical insights into car rental RM.

The remainder of this paper is organized as follows. Section 2 reviews the related literature. Section 3 formulates the problem as a stochastic DP. Section 4 introduces the LR approach with product‐ and time‐dependent Lagrangian multipliers, which decomposes the network problem into a number of single‐station single‐day subproblems. Section 5 discusses the Lagrangian dual problem and proposes a subgradient algorithm, followed by the introduction of three simpler variants. Section 6 provides a numerical study to compare their performance against three network‐based bid price policies. Section 7 implements the model and the bid price policies in a case study with the empirical data. Section 8 concludes the paper. We extend the model to dynamic pricing and staff‐operated shuttling problems, which, along with the technical proofs and full details of the case study, are included in the Supporting Information. Throughout this paper, let

RELATED LITERATURE

Our paper is related to two bodies of literature: optimal control of rental or mobility service systems and capacity allocation in network RM.

In the first body of literature, the rental or mobility service systems are modeled as queueing systems. For example, Savin et al. (2005) study capacity management in rental businesses with two customer bases. They formulate a continuous time DP and show that the optimal control policy can be characterized with thresholds. Gans and Savin (2007) further extend this analysis for rental systems to integrate pricing and capacity rationing decisions. George and Xia (2010) formulate a car rental system as a stationary stochastic closed queueing network and provide a performance analysis for fleet sizing and service availability. Balseiro et al. (2021) study dynamic pricing of resource relocation in a hub‐and‐spoke network with an application to ride hailing. Assuming zero‐transit time for each trip, they formulate the problem as an infinite‐horizon DP and develop an LR method to solve it. Of note, none of these models consider advance bookings.

Our study is also related to the field of airline network RM and, more specifically, to the capacity allocation problem. See Talluri and van Ryzin (2004) for an excellent review of early contributions. As a result of its limited tractability, most of the studies focus on developing efficient algorithms. Specifically, this literature includes three streams of development.

The first stream of network RM research focuses on static heuristics. A simple heuristic involves formulating the problem as a DLP and using the dual prices of the capacity constraints as the bid prices (Talluri & van Ryzin, 2004). Dynamic bid prices can be generated through reoptimization. Other similar variants include the PNLP (Li & Pang, 2017; Talluri & van Ryzin, 1998, 2004), the RLP (Talluri & van Ryzin, 2004), and the stochastic program (SP) (Haensel et al., 2012).

The second stream of network RM research adopts approximate dynamic programming methods to approximate the optimal value functions of DPs with some parameterized functions. A representative work is Adelman (2007), who approximates the value functions using an affine combination of basis functions and solves the dual of the resulting linear program with column generation to obtain time‐dependent bid prices. He shows that the proposed bid price control policy significantly outperforms DLP. More recently, Kunnumkal and Talluri (2016) propose a piecewise linear approximation to the value function, and develop an efficient separation algorithm to generate constraints “on the fly” to solve the resulting linear program.

The third stream of network RM research decomposes a network problem into multiple single‐resource problems that are more tractable, and then uses the single‐leg models to generate bid prices for each individual resource. A powerful decomposition approach is based on LR. Jiang (2006) applies the LR approach to a PNLP formulation of the airline network RM problem. Topaloglu (2009) appears to be the first to apply the LR approach to the dynamic airline network RM problem, assigning Lagrangian multipliers for the constraints that associate decisions of all legs of the same itinerary to break the interdependency between resources. He shows that the approximate value function is the sum of the value functions obtained from the decomposed problems for the corresponding resources and provides an upper bound for the optimal value function. The bid prices derived from the approximate value function are time‐ and capacity dependent. The numerical study shows that the proposed bid price policy outperforms not only the DLP‐based bid price policy but also that based on the affine linear approximation of Adelman (2007). In a similar fashion, alternative Lagrangian decomposition approaches have been developed (see, e.g., Kunnumkal & Topaloglu, 2010a, 2010b and the references therein). It is interesting to note that there exists a close connection between the approximate linear programming and LR approaches. Tong and Topaloglu (2014) show that the LR approach of Kunnumkal and Topaloglu (2010b) results in the same bid prices as those from the affine approximation of Adelman (2007). Kunnumkal and Talluri (2016) also find that the piecewise linear approximation and the LR in Topaloglu (2009) lead to the same linear program. Both studies observe that the LR approach is more computationally efficient than approximate linear programs.

Compared with airline network RM, car rental RM has a significantly larger state space as a result of the features of LoRs and mobility of inventories among stations that require one to account for both the spatial‐ and intertemporal linkages of resources. Schmidt (2009) proposes DLP and PNLP formulations to generate bid price heuristics for car rental network booking control problems. Haensel et al. (2012) propose a two‐stage SP formulation to generate heuristic booking limit policies. Both papers restrict the models to a single booking and rental time window, and thus ignore the effects of current decisions on the future beyond the current booking and rental time window. More recently, Guerriero and Olivito (2014) incorporate one‐way rentals into booking controls and propose a DLP method for both booking limit and bid price control policies. They also present a DP formulation of the problem over a finite time window, but no attempt is made to solve it. To the best of our knowledge, the only studies on dynamic capacity control policies in a car rental setting are Steinhardt and Gönsch (2012) and Li and Pang (2017). However, both of these are restricted to the single‐station problem. Specifically, Steinhardt and Gönsch (2012) simultaneously consider bid price control and product upgrade decisions, and then formulate the problem as a finite horizon DP and solve it via the standard decomposition approaches (see, e.g., Talluri & van Ryzin, 2004). Li and Pang (2017) appear to be the first to directly address the dynamic booking limit control for car rental RM problem. They first formulate the problem as an infinite‐horizon stochastic DP with a rolling‐over booking and rental time window, and then propose a decomposition approach to decomposing the problem into multiple single‐day problems by treating a product of multiday LoR as a set of independent products of only single‐day LoR. Our paper extends this literature to car rental network RM problems.

THE MODEL

Problem description

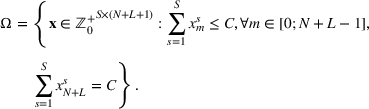

Consider a car rental network with S rental stations distributed across different geographic locations, indexed by

The car rental network is operated under a typical point‐to‐point model such that customers can book in advance or on the spot, and pick up rental cars from and return them to any of the stations. A typical booking request specifies the pick‐up station (origin o), return station (destination d), leadtime of pick‐up day (n), and LoR (ℓ). A car rental booking quadruple

For convenience, let

For simplicity, we restrict our analysis to the setting with only one fare class for each product. Our model can be readily generalized to the setting with multiple fare classes for each product, as in the classic capacity allocation models in airline RM (see, e.g., Feng & Xiao, 2000, and Talluri & van Ryzin, 2004, and references therein). In addition, we only consider one type of car (car group), as an upgrade/substitution is beyond the scope of this work. Let

In car rental operations, it is possible to perform staff‐operated shuttling to rebalance the car distribution within the network, which may incur significant additional operating costs. Our model does not account for the shuttling decision. Instead, we take full advantage of one‐way rentals, which allow us to use bid price control to maximize revenue while redistributing the fleet. Nevertheless, in the Supporting Information, we provide an extended model to address staff‐operated shuttling.

Stochastic dynamic programming formulation

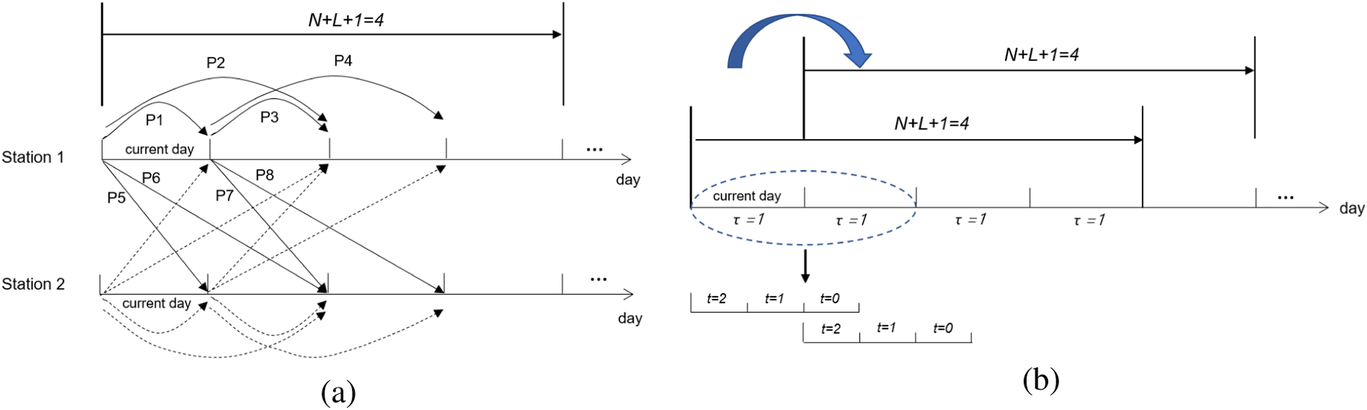

The problem alluded to in the previous section can be formulated as a stochastic DP. We consider an infinite time horizon with a rolling time window of

To account for the temporal variations and seasonality of car rental demand, we consider a demand cycle of

Customer requests arrive according to inhomogeneous Poisson processes. Consider a discrete approximation to the Poisson arrivals by assuming that the time interval of each epoch is small enough such that there is at most one customer arrival in each epoch. The probability of a customer arrival in epoch t of season τ, or

The system state can be represented by an

A round‐trip booking of

For notational convenience, we define an

Let

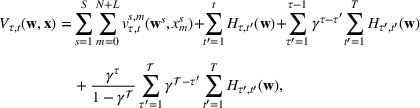

Following Li and Pang (2017), we assume that the objective of the revenue manager is to maximize the expected total discounted revenue over an infinite horizon with a daily discount factor

The infinite‐horizon cyclic dynamic programming formulation (6) accounts for not only variations of booking demand over time within a day and across days but also the rolling time window nature of the car rental operations. It captures the salient features of car rental network RM: advance bookings, LoRs, and mobility of cars among stations. It is related to some existing models in the literature as follows.

For

For

These special cases demonstrate the generality of our model. They also imply that it is the LoR and the mobility of rental cars in the network that drive the rolling time window of the system. The need to account for advance booking and fleet rebalancing at the same time makes car rental RM much more challenging. It is also clear that, because of the queueing feature (i.e., the LoR), it is natural and convenient to consider an infinite horizon for the car rental system (see, e.g., Balseiro et al., 2021; Gans & Savin, 2007; Li & Pang, 2017; Savin et al., 2005). One can readily reformulate the problem as a finite‐horizon DP. To this end, it suffices to replace

Given any

We next provide an illustrative running example that will be used throughout this paper. Consider a car rental network with two stations (

Products for the running example

Products for the running example

The running example

LR DECOMPOSITION

There are two types of interdependencies in the system that drive the high dimensionality: a spatial interdependency (the linkage between stations due to one‐way rentals) and a temporal interdependency (the linkage between rental days due to multiday LoRs). The decomposition approach proposed by Li and Pang (2017) for a single‐station car rental RM model only accounts for the intertemporal dependency while the typical LR approach in airline RM (e.g., Topaloglu, 2009) can account for the spatial interdependency. The core idea of LR approaches is to decouple the admission decision for each product via a set of Lagrangian multipliers corresponding to the resources used by the product. Topaloglu (2009) proposes an LR approach with product‐ and time‐dependent Lagrangian multipliers. We adopt such an approach to decompose the car rental network RM problem into single‐station single‐day (i.e., single‐resource) subproblems.

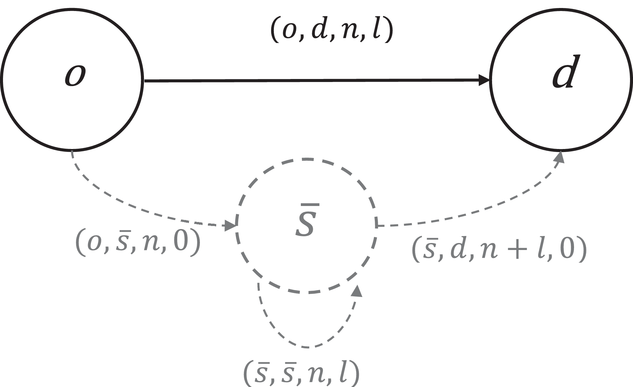

To illustrate the idea of the LR approach, we introduce a virtual station

Decomposition with a virtual station

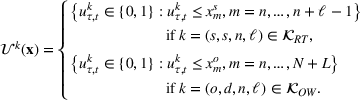

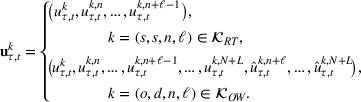

We then introduce a set of ancillary decision variables. For any one‐way booking

Denote by

Using the above ancillary decision variables, DP (6) can be rewritten as

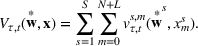

The Lagrangian multipliers for constraints (10b) to (10d) are denoted by

Define the set of Lagrangian multipliers as

In particular, for each round‐trip booking

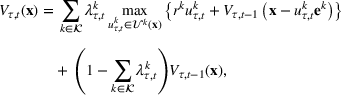

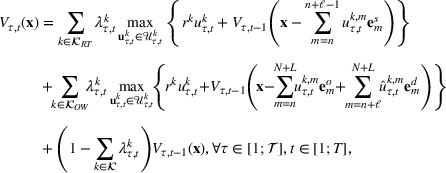

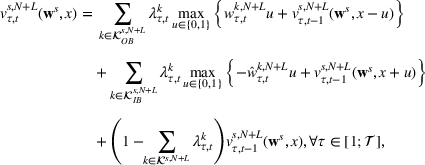

The key idea of LR is to relax the constraints (10b) to (10d), which results in the Lagrangian problem with the value function

The following proposition shows that the value function For any

We next show that

It is more straightforward to identify these bookings for one‐way rentals. For outbound rentals, such bookings include all of those with a pick‐up day on or prior to the service day, while for inbound rentals, such bookings include all of those with a return date prior to the service day.

Denote by

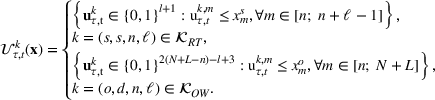

The state variable x takes values from the set

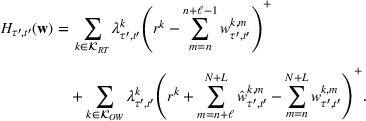

The problem (15) can be seen as a single‐leg capacity allocation model in the airline RM literature (see, e.g., Talluri & van Ryzin, 2004). Clearly, given the state

From day

Note that the recursion (16a) is similar to (15a), except that x denotes the common inventory level of station s from day

Our approach decomposes the network problem for each station into

The single‐dimensional problems have the following structural properties. For any

Lemma 1 reveals the two fundamental structural properties in RM: the concavity in inventory levels (which reflects the resource scarcity) and the supermodularity in remaining time and inventory levels (which reflects the time perishability) (Pang et al., 2015). Note that for the finite‐horizon case (i.e.,

The following lemma shows that the value functions of the single‐dimensional problems are convex and monotone in the Lagrangian multipliers with limited sensitivities. For any Sensitivity

The next proposition shows that the value function For all τ and t, the value function

Decomposition

We next provide the intuition for the decomposition representation for the optimal LR revenue function (17) using the idea of virtual stations. Through LR, we decompose the dynamic network into a set of separated single‐station single‐day units. The bookings that associate resources across stations and across different days are decomposed as individual transactions with the virtual station. The Lagrangian multiplier for each resource serves as the compensation for occupying a unit of capacity of this resource or the charge for receiving an additional unit of capacity (for the inbound cars), while the actual rental prices

LAGRANGIAN DUAL PROBLEM

The weak duality property implies that there may exist a positive gap between the relaxed value function

Product‐ and time‐dependent Lagrangian multipliers (LR1)

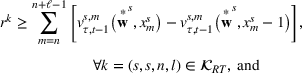

The optimal Lagrangian multipliers can be chosen by solving the convex Lagrangian dual problem: For all

The convexity of There exist optimal Lagrangian multipliers to the dual problem (19) satisfying the following relationships for all τ and t:

Optimal Lagrangian Multipliers

Proposition 4 shows that the optimal Lagrangian multipliers for resources of product k can be obtained by decoupling its price

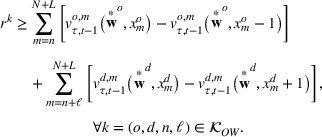

Under the optimal Lagrangian multipliers, the decomposition representation (17) reduces to

The convex Lagrangian dual (19) can be solved through standard subgradient optimization; see Jiang (2006) and Topaloglu (2009) for its applications to airline RM problems. To develop a subgradient‐based algorithm, we need to derive a subgradient of the value functions.

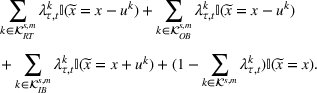

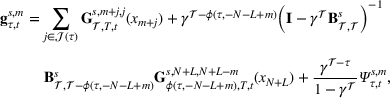

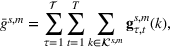

For notational convenience, we introduce the matrix form for the Bellman equations (15a) and (16a). For each station s, denote by

Let

Let

The subgradient‐based Algorithm 1 is described in EC.3 of the Supporting Information. The initial values of the Lagrangian multipliers are chosen based on Proposition 4. More specifically, for a round‐trip booking

The optimal dual function

Station‐ and leadtime‐dependent Lagrangian multipliers (LR2)

Although the optimal solution to the dual problem (19) has an appealing analytical structure, as demonstrated by Proposition 4, it remains challenging to compute. An effective way to reduce the number of Lagrangian multipliers is to associate Lagrangian multipliers directly with each rental day in each station. Since the fleet size in the car rental network is fixed, we let the Lagrangian multipliers depend only on the leadtime for each station. More specifically, let

It follows immediately from (3) that

Leadtime‐dependent Lagrangian multipliers (LR3)

We can further reduce the number of Lagrangian multipliers by removing the station dependence in LR2. Let

Station‐dependent Lagrangian multipliers (LR4)

An alternative way to further reduce the number of Lagrangian multipliers is to remove the leadtime dependence in LR2. Let

Revenue performance comparison for the running example

We next apply the above LR approaches to Running Example 1 and compare them to the optimal policy derived from the original DP (6). To this end, we first obtain the best bid prices of the dual problem under each LR‐based bid price policy as well as the optimal DP policy, and then apply them to a simulated sample of 500 randomly generated demand replications over a 90‐day time horizon. Assuming at the beginning that each station has one car available and there are no outstanding bookings, we calculate the total discounted revenue achieved under each policy. A discount factor of 0.9 has been used to calculate the present value of the revenue on the future days. Table 2 outlines the optimal Lagrangian multipliers under each approach. For brevity, we only present selected results for LR1; the full results are included in Table EC.1 of the Supporting Information. It is obvious that the optimal Lagrangian multipliers under LR1 satisfy Proposition 4. For LR2 and LR3, the Lagrangian multipliers decline over time, reflecting the perishability of capacity. For LR4, the Lagrangian multiplier value is higher for station 1, reflecting the higher demand in this station. The performance results are reported in Table 3, where we can observe that LR1 and LR2 have revenue performance that is slightly lower than the optimum but much better than that of LR3 and LR4, while the computation effort, represented by the number of iterations, under LR1 is almost twice that under LR2 and significantly greater than that of LR3 and LR4.

Optimal Lagrangian multipliers for the running example

Running example results

NUMERICAL STUDY

We next provide a numerical study to systematically assess the performances of the proposed LR approaches and compare them to three commonly used heuristics in the network RM literature—DLP, PNLP, and RLP. Detailed descriptions of these heuristics are provided in Section EC.4 in the Supporting Information.

Problem instances

We first introduce the demand‐to‐supply ratio to represent the relative fleet size of the network:

The demand‐to‐supply ratio is related to the fleet utilization rate or average fleet utilization, which is commonly used in the car rental industry as a key operational performance indicator. The fleet utilization rate is based on the number of rental days that vehicles are rented compared with the total amount of time that vehicles are available for rent, which typically varies between 50% and 90%. For example, Avis reported that its average fleet utilization was about 70% in 2021 (Avis Budget Group, 2022), while Hertz reported that its fleet utilization rate increased from 53% in 2020 to 77% in 2021 (Hertz, 2022). Bui and Irwin (2021) report that, in 2021, rental demand and prices were soaring while the market was short of inventory. These facts indicate that though actual demand could be much higher, the realized utilization rate could be significantly lower due to the mismatch between demand and supply, which may cause significant lost sales. The demand‐to‐supply ratio can be viewed as the theoretical upper bound of the actual utilization rate, if all demand could be fully met. Hence, to test the performance of the bid price heuristics in different market environments, we vary the demand‐to‐supply ratio between 80% and 500%.

In addition to the demand‐to‐supply ratio, to thoroughly examine the performance of the proposed LR policies against other heuristics, we generate a number of testing instances in different settings, as summarized in Table 4. The demand is generated according to the actual patterns observed in practice. Specifically, the booking requests for round‐trips are higher than those for one‐way trips and increase with a shorter booking leadtime and shorter LoR. For instances with three seasons, the demand in the middle and low seasons are 80% and 60% of that in the high season, respectively. The rental rates per day decline with the LoR, and they are higher for one‐way trips than round‐trips. For each instance, we consider either 12 or 24 booking epochs within a day while allowing ρ value to vary between 0.8 and 5.

Testing instances

We apply Algorithm 1 to compute the optimal dual solutions for the four LR heuristics. For comparison purpose, we adopt the common termination criteria in all the instances, as detailed in Section EC.3 of the Supporting Information. The optimal dual values and run time are reported in Section 6.2. Due to the high dimensionality, it is unrealistic to compute the optimal policy. Hence, we compare the performance of the heuristic bid price policies via simulation. For each instance, we apply these policies to 500 randomly generated demand replications over a 90‐day time horizon. The network‐based heuristics are reoptimized every 9 days over the horizon, while the dual problems for the LR approaches are only solved once at the beginning of the simulation. The discount factor is 0.9. Assuming at the beginning the fleet is evenly distributed within the network and there are no outstanding bookings, we calculate the expected revenue achieved under each policy. The results are reported in Section 6.3. All the experiments are executed with high performance computing clusters consisting of multiple nodes, each with Intel Xeon X5650 CPUs and 24GB RAM.

Optimal dual values and run time of the LR approaches

Since the optimal dual values of the LR approaches provide upper bounds on the expected total revenue, in Table 5 we report the optimal dual values of each LR approach for all instances with

The upper bounds (optimal dual values) and pair‐wise comparisons of the LR approaches,

Table 5 shows that, first, LR1 does not always produce the tightest upper bounds, given the negative percentage of numbers comparing the upper bound of LR2 against that of LR1 in the same instance. In those instances, Algorithm 1 for LR1 stops after the first 100 iterations; it does not find any improvement of the dual values before reaching the termination criteria. In the other instances, more iterations are completed and LR1 always leads to the tightest upper bounds. Second, among the simpler variants, LR2 always produces tighter upper bounds than LR3 except in two instances, where Algorithm 1 for the former stops much earlier than that for the latter. Third, in all but five instances, LR3 produces tighter upper bounds than LR4, and the gap between them could be up to 51.9%. In addition, similar results for the optimal dual values are also observed for

Table 6 summarizes the total CPU time and the time per iteration that Algorithm 1 takes for instances with

The total CPU time and the time per iteration of the LR approaches,

Where the total CPU time is more than 3600s, the extra time is used to complete the last iteration before the algorithm is terminated.

Revenue performance of alternative bid price policies

Table 7 reports the revenue performance under the bid price policies for all instances with

The revenue of alternative bid price policies and percentage extra revenue under LR1,

The results for

Importantly, the results in both tables indicate that the superiority of LR1 over the network heuristics increases first in ρ, and then tends to decrease after a certain point. When ρ is small, there are many cars in the network and much demand can be accepted regardless of the booking control policy. With the fleet decreasing, the outcomes of good and bad decisions become more distinct and thus the difference between them increases. When the fleet size is too small, few bookings can be accepted, resulting in less revenue difference between the policies.

In summary, LR1 yields the strongest revenue performance but suffers longer computational time. LR2 has the right balance between the revenue performance and the scalability, especially for large problems. LR3 is a strong contender for smaller problems while LR4 is not a reliable policy.

CASE STUDY

To examine the potential performance of the proposed LR approaches over the alternative network heuristics in real‐world applications, we next provide a case study based on a sample of booking data in a car rental network of a major service operator in the United Kingdom. For simplicity, we restrict our focus to the regional network around London. The data used in this case include the booking requests received by the car rental operator within the 5‐month period from May to September in 2011. We use the empirical data in the first 3 months to calibrate the arrival processes as a Poisson regression model and implement the proposed policies with the estimated arrival probabilities. The problem parameters are

We examine five different demand‐to‐supply ratios such that

Total revenue

Revenue per car per day and the fleet utilization

Figure 3 shows the cumulative revenue (for

Cumulative revenue for

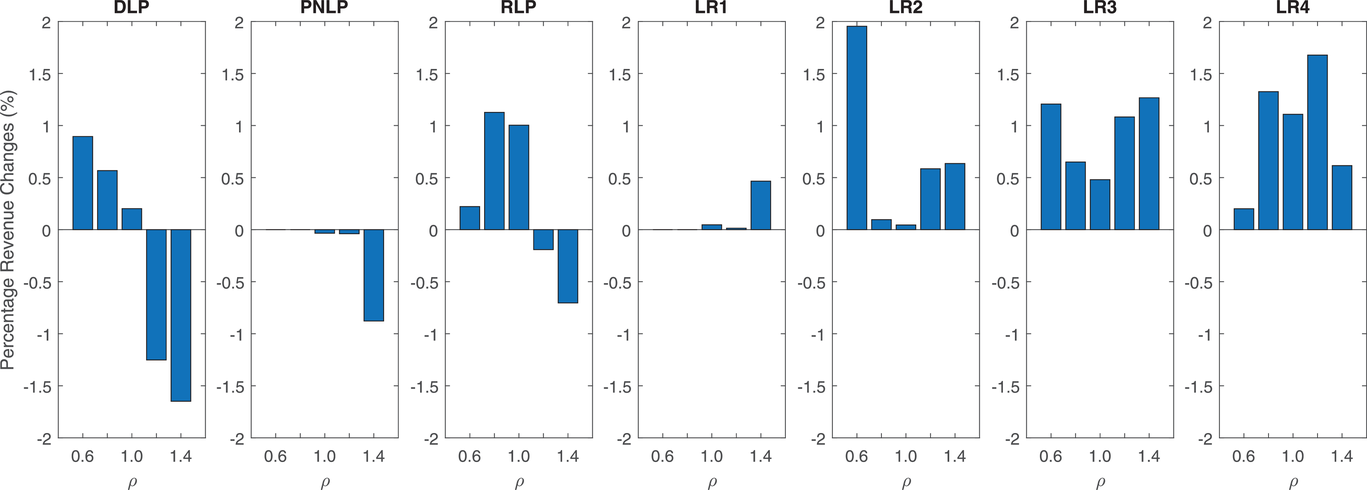

To assess the impact of more frequent reoptimization of the network bid price policies, we repeat the analysis by resolving DLP/PNLP/RLP twice as frequently (every 5 days). Similarly, we re‐solve the Lagrangian dual problems for the four LR approaches five times. In other words, they are solved at time T on day 0, 35, 70, 105, and 140 for the state then occupied. Figure 4 presents the percentage revenue changes (the actual revenue results are shown in Table EC.9 in the Supporting Information), showing that more frequent optimization of the network models does not necessarily lead to better performance. Indeed, in some cases based on the network heuristics, revenue actually reduces. The benefit of more frequent reoptimization is marginal for LR1, but is more noticeable for LR2, LR3, and LR4, which suggests that more frequent reoptimization can reduce, but not obliterate, the performance gap between these network heuristics and LR1.

Percentage revenue changes with more frequent reoptimization

To examine the robustness of the 1‐h time limit termination criterion, we have repeated the case study with 10‐h time limit. Our results indicate that there is almost no improvement when ρ is small, and when ρ is relatively large the extra revenue due to the longer computing time is always less than 0.44%. These observations suggest that it suffices to control the computation time within 1 h per instance.

CONCLUSIONS

Because of its complexity, RM in car rental is intrinsically challenging. A typical car rental network simultaneously possesses the characteristics of passenger airlines, such as demand sparsity, limited capacity (resource scarcity), and finite advance booking horizons (perishability), and the characteristics of hotel services, such as variations of LoR. The mobility of inventories due to one‐way rentals in the network differentiates car rental from hotel services. A basic booking request needs to specify when and where to pick‐up and return the car, which implies that the product in car rental should be characterized by the combination of origin, destination, pick‐up time, and LoR. Such a product can be seen as a bundle of resources; that is, the available cars each day in a particular station. These operational characteristics are further verified in the case study with a sample of real booking data from a regional car rental network in the United Kingdom.

In this paper, we formulate the RM problem of a car rental network as a cyclic stochastic DP with a rolling booking and rental time horizon, capturing the key characteristics of car rental operations. The underlying Markov decision process has a state space with the dimensionality equal to the number of stations in the network multiplied by the length of the regular booking and rental time window. To tackle the curse of dimensionality, we introduce an LR approach (LR1), which has been successfully applied to airline RM problems (see, e.g., Jiang, 2006; Topaloglu, 2009), to decomposing the car rental network problem into multiple single‐resource problems across stations and over time from the current day into the future. The key idea is to break the intertemporal correlation and the spatial correlation of the demands for capacities in different locations and days by decoupling the booking decision for a product over the resources that it uses via a set of product‐ and time‐dependent Lagrangian multipliers. The Lagrangian multipliers can be viewed as compensations for the round/outbound trips and charges for inbound trips related to each resource. We can then decompose the problem into multiple single‐resource subproblems. We characterize the structural properties of the decomposed problems and show that the value function under LR provides an upper bound for the optimal value function. We show that the dual problem is a convex program and propose a subgradient‐based optimization algorithm to solve it. The optimal dual function provides an approximate value function, which allows us to develop a bid price policy. Such an approach, though analytically appealing, requires computing a very large number of Lagrangian multipliers when the problem size becomes large, which restricts its scalability.

To enhance the scalability of the LR‐based bid price policies, we introduce three simpler LR approaches (LR2, LR3, and LR4) with the significantly reduced numbers of required Lagrangian multipliers. In the numerical study, we compare the performance of the proposed bid price policies and several commonly used heuristics such as DLP, PNLP, and RLP across various parameter settings. Our results show that LR1 outperforms those heuristics in most instances considered. LR2, though slightly worse than LR1, is much faster and therefore is more scalable, making it a great complement to LR1. LR3 is a strong contender for small instances but LR4 performs weakly in general. In the case study, we use the empirical data to calibrate the arrival processes as a Poisson regression model and implement the proposed policies with the estimated arrival probabilities. Both LR1 and LR2 deliver strong and robust performance in these real‐world settings.

We find that the LR approach is an insightful method that allows us to leverage the structural properties of the single resource RM models to construct the control policy for the network. Our development further advances the LR method in the context of car rental network RM. Such an approach can be potentially extended to other mobility services such as car sharing and ride hailing.

Nevertheless, our model has some limitations that raise suggestions for future research. First, our model does not address the uncertainty of LoRs. Like hotel RM, customers may sometimes extend or shorten the LoRs. Addressing random LoRs requires tracing each on‐rent car's rental time and forecasting its return time, which leads to a more sophisticated system. Second, our model only considers a single car group, while in reality consumers may choose different car models, which suggests that modeling consumer choice behavior toward the availability control could be an interesting generalization. Last but not the least, the emergence of on‐demand car sharing business models such as zipcar and car2go that allow customers to rent cars by the hour or the minute provides another interesting research topic for car rental network RM.

Footnotes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.