Abstract

This paper studies two fundamental questions regarding probabilistic selling in vertically differentiated markets: When is it profitable and how does one design it optimally? For the first question, we identify an important but overlooked economic mechanism driving probabilistic selling in vertically differentiated markets: the convexity of consumer preferences. In stark contrast to the literature finding that probabilistic selling is never profitable except in the presence of certain capacity constraint or consumer bounded rationality, we find that with many alternative utility functions capable of representing convex preference, probabilistic selling is always profitable. For the second question, we study the optimal strategy of probabilistic selling, including the design and price of the probabilistic good and the prices of the component goods. We show that under some technical conditions, the optimal price of the high‐quality component good increases while the optimal price of the low‐quality component good decreases upon the introduction of probabilistic selling, thereby increasing the market coverage and the economic efficiency without launching an actual new product line. To further illustrate the design of probabilistic selling, we use an example based on the canonical utility function, which is widely used in the economics literature on vertical product differentiation. We derive a closed‐form solution to the problem of optimal probabilistic selling. We also take advantage of the analytical tractability of the canonical utility to further explore the design of multiple probabilistic goods.

Keywords

INTRODUCTION

A probabilistic good is a synthetic good consisting of a mix, often in the form of a lottery, between existing goods (hereafter, component goods). The selling of probabilistic goods, a practice known as probabilistic selling or opaque selling, is an innovative way of combining products or services that are mostly homogeneous but differ in one important attribute, either horizontally or vertically.

Earlier works (Fay & Xie, 2008, 2010; Jerath et al., 2010; Jiang, 2007) on probabilistic selling focus on horizontally differentiated component goods such as sweaters of different colors or flights at different times of the day between the same pair of origin and destination cities. These studies help explain the economic forces driving probabilistic selling in numerous horizontal markets. As noted in another pioneering work on probabilistic selling (Zhang et al., 2015), “there are equally numerous quality‐differentiated markets where consumers strictly prefer one product over the other” and “it is important to ask whether probabilistic selling will prove profitable in quality‐differentiated markets.” In fact, the practice of selling a synthetic product has been documented in the Internet broadband service industry, where high‐ and low‐speed services are mixed as a probabilistic good (Zhang et al., 2015; Zheng et al., 2019); in the car rental industry, where cars of different sizes are mixed (Zheng et al., 2019); in the airline industry, where seats of different classes 1 are mixed (Zhang et al., 2015); in the hotel industry, where hotels 2 of different star ratings are mixed; in the online retailing industry, where earphones of different qualities are mixed (Zheng et al., 2019). Given the practices of probabilistic selling in such markets, Zhang et al. (2015) argue probabilistic selling is a profitable way for the disposal of the excess capacity of the high‐quality goods. Alternatively, Huang and Yu (2014) and Zheng et al. (2019) suggest bounded rationality, whether because of anecdotal reasoning or overweighting of salient attributes by consumers' salient thinking, may also lead to the emergence of probabilistic selling in vertically differentiated markets. The current paper contributes to this new stream of work on probabilistic selling.

The first main contribution of this paper is the revelation of an important but overlooked economic factor underlying the profitability of probabilistic selling in vertically differentiated markets: convexity of consumer preferences. Unlike Huang and Yu (2014) and Zheng et al. (2019), consumers are fully rational in our model. Different from Zhang et al. (2015) who assume that there is excess capacity for the high‐quality component goods but insufficient capacity for the low‐quality component goods, we do not impose a constraint on the capacity of either component good. The extant literature would suggest that probabilistic selling cannot be profitable in our setting. However, we show that once we move beyond linear utility function and consider preference convexity, probabilistic selling can be profitable for many utility functions. We further identify a sufficient condition that guarantees the profitability of probabilistic selling, based on our proposed concept of λ‐concavity, which is a joint property of two distinct objects: consumer preference and consumer type distribution.

To understand the basic intuition underlying the importance of preference convexity, consider a risk‐neutral seller who evaluates the profitability of offering a probabilistic good by mixing two component goods of different qualities before any price or capacity optimization. Because of the opportunity cost, the seller is unwilling to sell the probabilistic good at a price below the average price of the component goods weighted by the mixing probability. So, other than possibly risk lovers, why would any rational consumer, instead of consuming one of the component goods, ever be interested in consuming the probabilistic good at a price above the weighted average price? The reason, we believe, is that the consumer dislikes extreme allocation of her budget between quality improvement of the focal good and the consumption of other goods. This important property of consumer preference, formalized in economics as the crucial concept of preference convexity, is not an uncommon technical property. Rather, it is a central premise capturing the fundamental principle of diminishing marginal rates of substitution.

The extant literature all focus on the linear utility function, which cannot represent a (strictly) convex preference. We believe this largely contributes to the negative findings 3 in the literature. For example, Zhang et al. (2015) find probabilistic selling is never optimal without excess capacity of the high‐quality component goods, whereas Huang and Yu (2014) and Zheng et al. (2019) find probabilistic selling is never optimal unless they introduce some form of bounded rationality. The linear utility function, popular in the literature, and was originally suggested as a linear approximation to more realistic utility functions for analytical tractability. However, once we stop using linear approximation, these negative findings start to disappear. For example, if consumers have Cobb–Douglas utility functions and their types are uniformly distributed, probabilistic selling is always profitable. Hence, this paper complements the extant literature theoretically by revealing the crucial role of preference convexity in probabilistic selling in vertically differentiated markets.

Two practical implications of this theoretical finding are immediate. First, because preference convexity is well accepted in economics and is commonly assumed for consumer theory in standard microeconomics textbooks (Jehle & Reny, 2011; Kreps, 1990, 2013; Mas‐colell et al., 1995; Pindyck & Rubinfeld, 2018; Varian, 1992), our finding suggests probabilistic selling can be more widely utilized by firms that offer quality‐differentiated products. Hence, probabilistic selling can potentially be profitable in contexts currently overlooked in academia and by practitioners. Second, we believe that the proposed economic mechanism complements the current explanations of probabilistic selling in vertically differentiated markets, especially the one based on the excess (insufficient) capacity of the high‐quality (low‐quality) component goods. 4 Indeed, the existence of such an asymmetric mismatch between the supply of and the demand for quality‐differentiated component goods is unclear. Excess capacity, especially of high‐quality component goods, is costly, and a profit‐maximizing firm should have a strong incentive to match its capacity with the demand, especially in the long run. Moreover, Zheng et al. (2019) show that once we model consumer types as continuous instead of dichotomous as in Zhang et al. (2015), probabilistic selling is never optimal even with excess (insufficient) capacity of the high‐quality (low‐quality) component goods.

To aid the application of probabilistic selling in vertically differentiated markets, we develop a theory of optimal probabilistic selling, which is the second main contribution of the paper. First, we study the implications of probabilistic selling on the optimal prices of the component goods without using any specific functional form of the utility. We prove under some regularity conditions that the optimal price of the high‐quality component good increases while the optimal price of the low‐quality component good decreases, as the result of optimal probabilistic selling. Therefore, the practice of probabilistic selling can increase the market coverage and the economic efficiency without launching an actual new product line. This insight is useful both to practitioners and future researchers whose choice of utility function will inevitably vary depending on market characteristics. Second, we illustrate the optimal design of probabilistic selling using the canonical utility function that is often adopted in the economics literature to study vertical market differentiation. The explicit and simple form of the utility function allows us to derive a closed‐form solution to the problem of optimal probabilistic selling. Third, we explore the optimal design of probabilistic selling when the seller can offer multiple levels of probabilistic goods, which the extant literature has called for but not yet studied.

The rest of the paper is organized as follows. In Section 2, we briefly review previous studies on probabilistic selling in order to position the current paper in the literature. In Section 3, we set up the model with a generic two‐attribute utility function to reveal the importance of preference convexity and the sufficiency of λ‐concavity for probabilistic selling to be profitable without introducing bounded rationality. In Section 4, we develop a theory of optimal probabilistic selling and illustrate the optimal design in detail with a fully solved example. Finally, we conclude the paper in Section 5 with a discussion of its contributions, managerial implications, and limitations.

LITERATURE REVIEW

This literature can be broadly categorized based on two important modeling choices: whether the component goods are horizontally differentiated or vertically differentiated, and whether the model assumes rational consumers or consumers with bounded rationality. Accordingly, we list in Table 1 some representative works in each category and review those most closely related to the current paper. For a more comprehensive review of the literature on probabilistic selling, we refer interested readers to Jerath et al. (2009) or Zhang et al. (2015).

Literature position of the current paper

Literature position of the current paper

Naturally, most of the academic literature on probabilistic selling concerns two fundamental questions regarding the phenomenon: Under what conditions can probabilistic selling be profitable, and how does one optimally design probabilistic goods? Jiang (2007) and Fay and Xie (2008) are among the earliest works on probabilistic selling, and they focus on the case in which the two component goods are horizontally differentiated. For example, Jiang (2007) considers a Hotelling model with two component goods (e.g., morning flights and afternoon flights for the same origin–destination pair) placed at the two ends of the Hotelling line. The paper shows that probabilistic selling, with equal probability of selecting the two component goods, can sometimes improve profit by essentially price discriminating against consumers with less flexibility in terms of the choice between the two component goods. Fay and Xie (2008) also adopt the Hotelling framework. They find that probabilistic selling strictly improves profit if the marginal cost of the (symmetric) component goods is sufficiently low. They also find the optimal mixing probability of the component goods to be exactly 0.5, thereby providing a justification for the equal‐probability assumption in Jiang (2007). In addition, Fay and Xie (2008) also reveal that demand uncertainty and mismatch between capacity and demand can also motivate the use of probabilistic selling. Our paper differs from these papers mainly in our focus on vertically differentiated component goods rather than horizontally differentiated component goods.

More recently, researchers started to investigate the emergence of probabilistic selling in vertically differentiated markets. Huang and Yu (2014) first show probabilistic selling is never optimal when homogeneous consumers have rational expectations. However, if consumers have bounded rationality as is captured by anecdotal reasoning, probabilistic selling can be optimal. Similarly, Zheng et al. (2019) study probabilistic selling by taking into account consumers' salient thinking behavior. They show probabilistic selling is never profitable with rational consumers but does improve the seller's profit with salient thinkers. Different from these behavioral economics models, Zhang et al. (2015) study probabilistic selling in vertically differentiated markets with rational consumers, which is also assumed in the current paper. They find probabilistic selling can be profitable only if the capacity of the high‐quality (low‐quality) component good exceeds (falls below) the market demand. In contrast to findings from these studies, our paper suggests probabilistic selling can be profitable in more general situations with neither bounded rationality nor asymmetric capacity constraint. Such a different finding is rooted in the fact that in the extant literature (Huang & Yu, 2014; Zhang et al., 2015; Zheng et al., 2019), consumer preference is modeled by a utility function that does not satisfy the property of strict convexity, which is an important factor for probabilistic selling to be profitable in vertically differentiated markets.

In a sense, our paper bridges the gap between the literature on probabilistic selling in horizontally differentiated markets and the literature on probabilistic selling in vertically differentiated markets. The extant literature poses a puzzle regarding the applicability of probabilistic selling in these two market settings. For horizontally differentiated markets, probabilistic selling seems to be well justified in a wide variety of markets, but for vertically differentiated markets, probabilistic selling seems to only work in special circumstances (e.g., bounded rationality, salient thinking, excess [insufficient] capacity of high‐quality [low‐quality] component goods). An important insight from our paper is that such an asymmetry between horizontally differentiated markets and vertically differentiated markets is largely artificial, driven by the restrictive model of consumer preference selected in the extant literature to study vertically differentiated markets.

PROFITABILITY OF PROBABILISTIC SELLING

We consider a focal good that is an indivisible good with its quality denoted by q. Each consumer has a unit demand for the focal good. Before introducing a probabilistic good, the focal good has two quality levels,

We model consumer preference using a generic two‐attribute utility function,

Consumers are heterogeneous in their budget level w, which has a distribution that is absolutely continuous with its support normalized to [0,1]. Let

In the absence of a probabilistic good, the consumer maximizes her utility by comparing the above three utility levels.

We assume the utility function is strictly increasing in each attribute, and impose the following regularity conditions on its structure:

The first regularity condition, known as the single‐crossing condition or the Spence Mirrlees property (Milgrom & Shannon, 1994), is often assumed in the literature.

5

Depending on its interpretation as

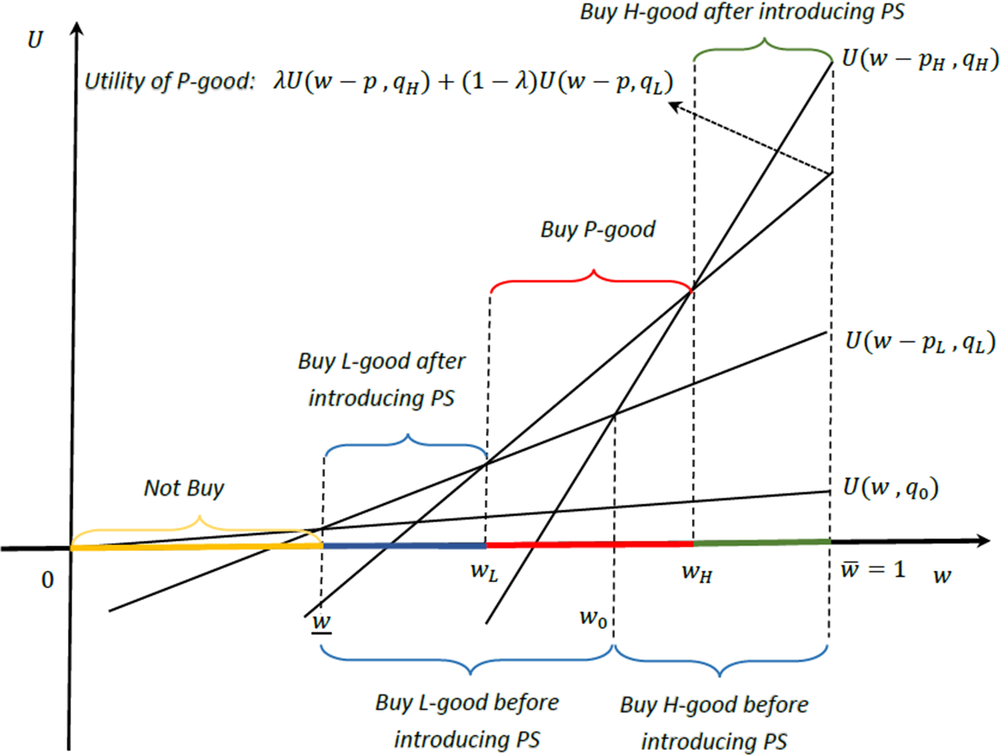

An illustration of market segmentation based on consumer heterogeneity in their budget level w

Let w0 be the budget level at which a consumer is indifferent

6

between the high‐ and low‐quality component goods, that is,

We represent a probabilistic good by the pair

With the introduction of a probabilistic good, consumers essentially have an intermediate quality level to choose and some may find it the best choice if the price of the probabilistic good is not too high. This is the case in the illustration of Figure 1 where the curve The demand for probabilistic good

The above result suggests that whether the demand for the probabilistic good is positive crucially depends on how those consumers with budget level w0 (henceforth the pivotal consumers) rank the probabilistic good.

The importance of preference convexity

In this subsection, we demonstrate the importance of preference convexity for probabilistic selling to be profitable and offer our explanation of the development of the current literature. Besides this theoretical insight, an important practical implication is that the potential application of probabilistic selling is beyond what the current literature has identified. First, recall the mathematical definition of preference convexity. A preference relation ⪰ on

Zhang et al. (2015) explains the profitability of probabilistic selling in vertically differentiated markets without introducing bounded rationality. The key factor there is the excess capacity of the high‐quality component good and the insufficient capacity of the low‐quality component goods. Such a result is obtained by assuming two types of consumers. However, Zheng et al. (2019) pointed out that with a continuous distribution of consumer types, probabilistic selling is never profitable for any level of capacity constraint. This negative result indirectly demonstrates the importance of modeling consumer preference as strictly convex because the result is obtained by assuming a linear preference, and classical economic theory typically only considers rational preference that is either strictly convex or weakly convex (i.e., linear). This indirect approach is analytically tractable thanks to the simplicity of linear utility function.

One drawback of this indirect approach is that the intuition for the role of preference convexity in probabilistic selling is obscured, which might have explained why the literature immediately examined the possible role of bounded rationality in probabilistic selling. Our goal in this subsection is to directly demonstrate the importance of preference convexity, using a generic utility function to model consumer preference. Unlike the indirect approach, explicitly solving for and comparing the solutions of two optimization problem involving a utility function that is not linear, hence abstract, is difficult, if possible at all. To circumvent this difficulty, we instead consider a benchmark setting where the seller offers the probabilistic good without expanding capacity and adjusting the prices of component goods. Such a setting reflects a short‐term scenario where the capacity is relatively fixed and the price of the component goods are relatively stable. For practitioners, this is likely the first scenario to consider while evaluating the profitability of probabilistic selling. Although highly stylized, this scenario can clearly reveal the importance of preference convexity, as is illustrated in the next proposition. Without capacity expansion and price adjustment for component goods, probabilistic selling is profitable only if consumer preference is strictly convex.

Intuitively, offering probabilistic goods gives consumers the option of an intermediate quality level at an intermediate price. Such an option can only be attractive to consumers if they are averse to “extreme” allocation of their budget between the focal good and the composite good, which is the essence of strict convexity of preference.

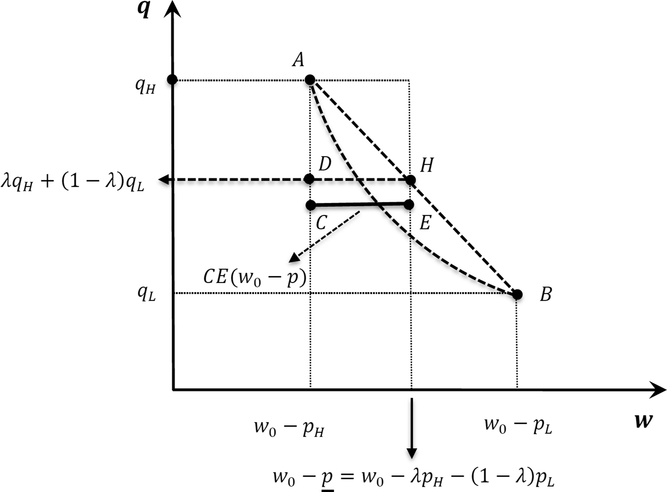

To better illustrate the crucial role of preference convexity in the emergence of probabilistic goods, we explain the underlying logic graphically in Figure 2 where the vertical axis represents the quality of the focal good and the horizontal axis represents the remaining budget spent on the composite good. Because consumer utility function is strictly increasing in both attributes, moving northeast to an indifference curve will increase utility. The consumption portfolios from purchasing the high‐ and low‐quality goods correspond to point A and B, respectively. It is easy to see that point H in the figure, representing the portfolio

A graphical proof of Proposition 2 based on indifference curve analysis of the pivotal consumers

Considered “a formal expression of basic inclination of economic agent for diversification” (Mas‐colell et al., 1995), preference convexity is a central concept in economics, implying that the marginal rate of substitution (MRS) diminishes along the indifference curve because we can expect that a consumer will prefer to give up fewer and fewer units of a second good to get additional units of the first one. A rational preference is (strictly) convex if and only if it can be represented by a (strictly) quasiconcave 10 utility function, which is related to but more general than (strictly) concave utility functions. Strict convexity of consumer preference simply means the preference is convex and not degenerate (i.e., linear). With convex preference, an agent prefers holding a mix of two extreme portfolios to holding either of them. Therefore, our analysis suggests that the profitability of probabilistic selling is related to rational consumers' desire for diversification: They do not want to hold an extreme portfolio of either definitely/always consuming low‐quality goods or definitely/always paying a high price.

The notion of preference convexity is well accepted in economics, and microeconomics textbooks (Jehle & Reny, 2011; Kreps, 1990, 2013; Mas‐colell et al., 1995; Pindyck & Rubinfeld, 2018; Varian, 1992) commonly assume it for the development of consumer theory. For example, (Varian, 1992, p. 157) argues that “if demand functions are well defined and everywhere continuous and are derived from preference maximization, then the underlying preference must be strictly convex.” In other words, in microeconomics theory, a well‐behaved demand function requires that consumers have a strict convex preference over a bundle of goods. Hence, preference convexity is also important in the theory of general equilibrium. As (Varian, 1992, p. 393) argues, “Usually, the assumption of strict convexity has been used to assure that the demand function is well‐defined – that there is only a single bundle demanded at each price – and that the demand function is continuous – that small changes in prices give rise to small changes in demand. The convexity assumption appears to be necessary for the existence of an equilibrium allocation since it is easy to construct examples where nonconvexities cause discontinuities of demand and thus nonexistence of equilibrium prices.”

The extant literature of probabilistic selling on vertically differentiated markets began by modeling consumer preference using the utility function

The sufficiency of λ‐concavity

Now that we understand the importance of preference convexity to the profitability of probabilistic selling, it is natural to identify some sufficient condition for the profitability of probabilistic selling, which will complement the insight of the previous subsection. From now on, we allow the seller to freely adjust its capacity and price of each component goods so as to maximize its profit in a long‐term equilibrium. To characterize the sufficient condition, we first define the concept of λ‐concavity which describes a pair Fix

For ease of exposition, we also say a preference (distribution) is λ‐concave with a distribution (preference) if the pair is λ‐concave. In our context, the triple

Let Probabilistic selling is profitable if the consumer preference and their budget distribution are λ‐concave for some

To understand the intuition without getting into the technical details, we summarize the proof of Proposition 3 here. First, we can show that at the optimal prices (without probabilistic selling) Consider the linear utility function

This example partially explains the negative finding in the extant literature that probabilistic selling is generally not profitable if consumers have rational preferences. Our next example offers a stark contrast to this literature finding by showing the general profitability of probabilistic selling for the well‐known family of Cobb–Douglas utility

12

functions, which is frequently used by standard microeconomics textbooks

13

to illustrate the classical demand theory. The family of Cobb–Douglas utility functions and the uniform distribution are 1/2‐concave for any

The drastic difference between Examples 1 and 2 illustrates the importance of modeling preference beyond linearity when we study probabilistic selling in vertically differentiated markets. We conclude this section with a positive finding that further demonstrates this point. Given any

The proof is straightforward once we rewrite (5) as

DESIGN AND MARKET IMPLICATION OF PROBABILISTIC SELLING

In this section, we address our second research question: the optimal design and the market implication of probabilistic selling. Our objective in this section is twofold. First, because the choice of consumer utility function depends on market contexts, and for many realistic utility functions, no closed‐form solution for the optimal probabilistic good

General model

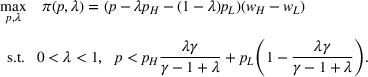

The problem of optimal probabilistic selling can be framed as a two‐stage decision problem where the seller chooses the prices of the component goods during the first stage, and design the probabilistic good

Because we characterize the optimal probabilistic selling without assuming specific utility function, in order to have some tractability, we follow the literature (Gabszewicz & Thisse, 1979; Shaked & Sutton, 1982, 1983) by assuming uniform distribution of w. The optimal design of the probabilistic good, given the prices of the two component goods, is the following optimization problem where the objective function is the profit gain from the introduction of the probabilistic good:

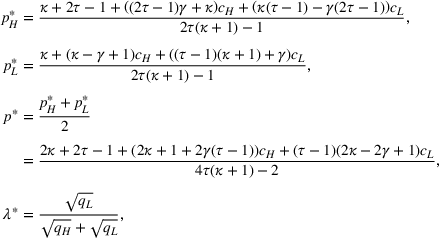

Recall w0 is an implicit function of For any price pair of the component goods

The above result suggests the optimal profit gain as a function of component‐good prices is always increasing in one while decreasing in the other and at the same rate, regardless of the prices of the component goods. Note Proposition 4 is a local property and does not imply the monotonicity of

Denote by π0 the profit without probabilistic selling, that is,

Recall

Of particular interest is the comparison between

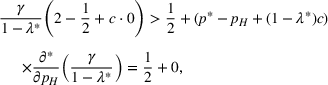

To compare If

Condition (12) is a sufficient condition for the profit function

Condition (13) is the necessary and sufficient condition for the optimal profit gain from probabilistic selling to increase (decrease) in

Given that the objective function is strictly concave, and thanks to some of its structural properties, the optimal prices of the component goods with probabilistic selling can be obtained by increasing the price of the high‐quality component good and decreasing the price of the low‐quality component good. The linearity assumption of

Example: Canonical utility function

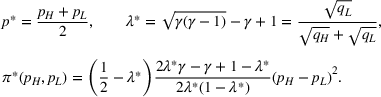

In this section, we illustrate the design of probabilistic selling using a particular utility function as an example. This utility function,

The canonical utility function is both rich enough to represent strictly convex preference, and simple enough to allow for analytical tractability. The closed‐form solution with this utility function not only allows us to illustrate the optimal design of probabilistic selling, but also enables us to explore the design of an arbitrary number of probabilistic goods, which is the first direction of future research emphasized by Zhang et al. (2015) in their conclusion.

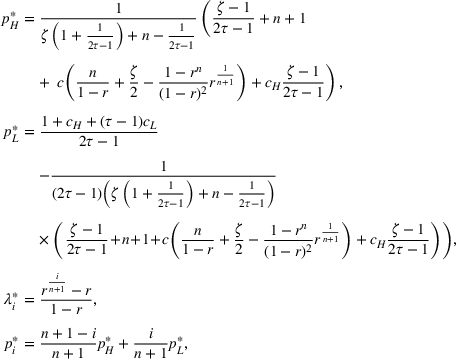

For the canonical utility function, we can solve for the following values based on their definitions in Section 3, where

We first design the optimal probabilistic good given the prices of the two component goods. We then use backward induction to explicitly solve for the optimal prices of the two component goods. With the canonical utility function, we have Given the prices of the two component goods

Different from the literature finding for horizontally differentiated markets (Fay & Xie, 2008; Huang & Yu, 2014) that equal‐probability mixing is optimal, Lemma 1 gives an example where the optimal mixing probability is strictly below 0.5. Interestingly, the optimal price of the probabilistic good is the arithmetic mean of the prices of the two component goods, whereas the optimal quality of the probabilistic good is the geometric mean of the qualities of the component goods (i.e.,

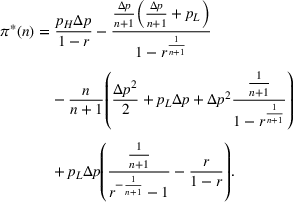

Given the closed‐form expression of The optimal design of probabilistic selling is given by

By viewing the probabilistic good as another “component” good, we can potentially design two additional probabilistic goods, with one mixing the high‐quality component good and the probabilistic good, and the other mixing the low‐quality component good and the probabilistic good. In fact, such a construction process can be repeated, which leads to the general questions of whether and how to design multiple probabilistic goods based on the two (original) component goods. To shed light on this interesting question, we take advantage of the analytical tractability of the canonical utility function to solve for the optimal menu of probabilistic goods.

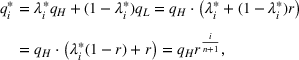

Suppose the seller creates n probabilistic goods from the two component goods, H and L, with different mixing probabilities and hence different prices. Indexing these probabilistic goods by

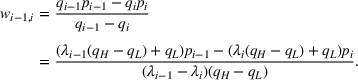

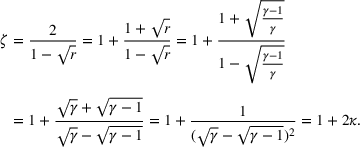

Denote the intersection of

With the result of Lemma 1, we can derive a series of explicit relations of the optimal mixing probabilities as well as the optimal prices among all probabilistic goods. The key insight is that for any probabilistic good to be optimal, it must be the optimal single probabilistic good when it is considered as a probabilistic good constructed using its two neighboring goods in the sequence of synthetic or component goods. For any Given

The result above suggests the optimal sequence of probabilistic goods is characterized by an arithmetic sequence of prices and a geometric sequence of qualities. That the price sequence forms an arithmetic sequence is clear from (22), which is rooted in Lemma 1, where we showed the price of the optimal single probabilistic good is the arithmetic mean of the prices of the component goods. To see why the qualities of probabilistic goods form a geometric sequence, note

Finally, we consider the optimal pricing of component goods when multiple probabilistic goods are offered. The following proposition summarizes the result and includes Proposition 6 as a special case. The optimal design of probabilistic selling with n probabilistic goods is given by

It is clear from the solution that

CONCLUSION

This paper studies two fundamental questions regarding probabilistic selling in vertically differentiated markets: When is it profitable and how does one design it optimally? For the first question, we identified convexity of consumer preference as an important factor and λ‐concavity as a sufficient condition for probabilistic selling to be profitable. This insight helps us explain why the extant literature finds probabilistic selling is never profitable unless one introduces certain capacity constraint or bounded rationality. For the second question, we developed a theory of optimal probabilistic selling.

Our contributions to the literature are fourfold. First, we identified an important but overlooked driver of the benefit of probabilistic selling, which is rooted in consumer preference. Hence, probabilistic selling can be a profitable strategy in economic situations even in the absence of the factors suggested by the extant literature (Huang & Yu, 2014; Zhang et al., 2015; Zheng et al., 2019). Second, we characterized some important structural properties of the optimal probabilistic selling strategy that should apply to many settings. In particular, we find probabilistic selling can increase market coverage and economic efficiency. Third, we initiated the study of designing multiple probabilistic goods, which, given the exclusive focus on the design of single probabilistic good in the extant literature and the call for attention to this question by Zhang et al. (2015), is both theoretically interesting and practically relevant. Although we characterized the optimal design of multiple probabilistic goods based on a specific utility function that is often used in the economics literature on product vertical differentiation, our approach to reduce the dimensionality of the optimization problem for the design of multiple probabilistic goods should be applicable when other types of utility functions are considered. Fourth, the drastically different finding obtained from strictly convex consumer preference suggests linear approximation is not always without consequence. Analytical research can sometimes benefit from a robustness check with some alternative utility functions.

The paper also has important managerial implications for practitioners. First, because preference convexity is a widely accepted notion in economics about consumer preference, we believe the potential of probabilistic selling is beyond what has been discussed in the current literature. In the absence of the administrative cost of selling synthetic goods, probabilistic selling can be a generic pricing strategy profitable for a variety of products. Through online selling or technological innovation, the administrative cost of probabilistic selling can be made negligible in the future. Indeed, some innovative company may design and offer a common platform for all sellers who are interested in probabilistic selling, thereby driving down the administrative cost. Second, because the profit gain from probabilistic selling should increase as the quality (or price) difference between two component goods increases, probabilistic selling is particularly appealing in market settings where the quality (or price) difference between different goods is substantial. For example, in the airline industry, the quality and price difference between “first class” and “economy class” is large, hence, popular marketing strategies such as “elite membership” or upgradable tickets, which can be interpreted as forms of probabilistic selling, are likely profitable for airlines. Similarly, in the hotel industry, the quality and price difference between hotels of different star ratings or rooms of different sizes and amenities can be significant; hence, marketing strategies such as Delphina's Formula Roulette Prestige program or H10's Tenerife Roulette program are attractive to consumers who dislike extreme budge allocation between quality and money. On the other hand, for markets where product quality differences are small and administrative costs are large, probabilistic selling may not be profitable in practice. Third, a key result from our theory of optimal probabilistic selling is that under some technical conditions, the market coverage increases as a result of probabilistic selling. In other words, fewer consumers will be priced out of the market. Therefore, the practice of probabilistic selling not only improves profit, but also increases economic efficiency. This takeaway is an important one for policy makers as well as for sellers who have a strategic interest in market penetration. Finally, our theory of optimal probabilistic selling also provides direct guidance to practitioners when they implement the strategy.

The current paper has several limitations that are worth future exploration. First, although the concept of λ‐concavity is useful, many open questions remain. For example, for any strictly quasiconcave utility function satisfying the regularity conditions and any distribution, does there exist a

Footnotes

ACKNOWLEDGMENTS

The authors would like to thank the department editor Haresh Gurnani, the anonymous senior editor, and the two anonymous reviewers for their constructive comments and helpful suggestions that have significantly improved the paper. Ying He would also like to thank the Independent Research Fund Denmark that provided a grant (grant number: 7089‐00013B) to financially support visiting Huaxia Rui from July 2018 to October 2018 in Rochester, USA, to work on the project.

1

For example, airlines often sell “upgradable” tickets, which allows the ticket holder, with some positive probability, to upgrade seat class. Such an “upgradability” can be implemented in different ways. For example, consumers may pay a fare higher than the cost of a “non‐upgradable” ticket for this privilege. For most airlines, basic economy tickets, which are sold at the lowest price, are nonupgradable tickets. Customers may also join an elite membership program for such a privilege, and membership can be obtained upon achieving enough reward points or through direct purchase. In general, an upgrade is not guaranteed and the probability of upgrade may also differ among different consumers. For instance, American Airlines (AA) offers AAdvantage elite program, which consists of four different membership statuses. A higher status level increases the chance of being upgraded.

2

Such a program is often referred to as a roulette. A participant of the program pays a discounted price for a stay either in a (relatively) high‐end or a (relatively) low‐end hotel that is not revealed to the participant before the booking. See, for example, Delphina's Prestige Roulette Formula (

3

4

The size of the variable transaction cost specifically linked to probabilistic good also plays an important role in the explanation based on excess capacity. For example, Zhang et al. (![]() ) find that only with a sufficiently large transaction cost can the offering of both component goods along with the probabilistic good become optimal. However, in reality, we do observe the offering of probabilistic goods and both component goods even when such a variable transaction cost is negligible, at least compared with the prices of component goods.

) find that only with a sufficiently large transaction cost can the offering of both component goods along with the probabilistic good become optimal. However, in reality, we do observe the offering of probabilistic goods and both component goods even when such a variable transaction cost is negligible, at least compared with the prices of component goods.

5

For example, Shaked and Sutton (1987) assume the condition to study vertical product differentiation and industrial structure. Similarly, Zhang et al. (![]() ) assume it, albeit in a discrete setting. More specifically, in their context of two types of consumers, this regularity condition becomes

) assume it, albeit in a discrete setting. More specifically, in their context of two types of consumers, this regularity condition becomes

6

The existence of w0 is guaranteed as long as the budget interval is sufficiently large, which we assume throughout the paper. Otherwise, consumers either all prefer the high‐quality good or all prefer the low‐quality good, thereby excluding the very existence of a vertically differentiated market in the first place. Similar conditions have been imposed in the literature of vertical differentiation (Mussa & Rosen, 1978; Tirole, ![]() ) to ensure positive demand for products of different qualities.

) to ensure positive demand for products of different qualities.

7

To see this, note

8

Similar to the logic for the existence of w0, the existence of

9

10

A strictly quasiconcave utility is often defined as a function

11

Indeed, we can simply redefine it by its reciprocal and note an affine transformation of a utility function does not change the underlying preference.

12

A Cobb–Douglas utility function has the form of