Abstract

Firms that sell products over a limited selling season often have only imperfect information about (a) the exact timing of that season, (b) the demand volume to expect, and (c) the temporal distribution of demand over the selling season. Given these uncertainties, firms must determine not only how much inventory to stock but also when to make that inventory available to customers. We thus ask: What is a firm's optimal inventory quantity and timing for products sold during a stochastic selling season? Although the newsvendor literature has developed a thorough understanding of the firm's optimal inventory quantity, it has failed to inform decision‐makers about choosing the optimal inventory timing. We address this issue by developing a theoretical model of a firm that sells a product over a stochastic selling season, and we study how this firm should choose its inventory timing and inventory quantity so as to maximize expected profits. We also identify the effects of optimal inventory timing on the firm's ability to satisfy customer demand and show how early inventory timing can be detrimental to customer service. Our core results imply three immediate recommendations for managers. First, optimal inventory timing is an effective weapon for combating both high inventory holding costs and high levels of uncertainty in the firm's customer demand pattern. Second, to be effective, a firm's inventory timing must be carefully aligned with the firm's inventory quantity. Third, naïve decision rules (e.g., “earlier is better”) may reduce not only the firm's profits but also its capacity to serve customer demand.

INTRODUCTION

Inventory management of crop protection chemicals (e.g., fungicides, herbicides, and insecticides) shares many of the challenges associated with a classic newsvendor setting: (i) strong seasonal demand, (ii) considerable demand uncertainty, and (iii) long production lead times. Most crop protection chemicals are targeted at a particular phase of the crops' maturation process and can therefore be applied only a few weeks each year (see, e.g., Sainz Rozas et al., 2004; Vetsch & Randall, 2004). In addition, the type of chemicals that farmers must apply to their fields—as well as how much of them and when—depends heavily on that season's weather conditions (Caseley, 1983; Frey et al., 1973; Van Alphen & Stoorvogel, 2002). Hence farmers postpone the acquisition of their crop‐protecting chemicals until they can predict, with sufficient precision, such factors as sunshine and precipitation levels; thus the chemicals in question are not purchased until shortly before their application. Exacerbating the uncertainty is that fluctuating crop prices and changing environmental policies can have a sizable effect on farmers' incentives to invest (or not) in yield‐enhancing crop treatment (see, e.g., Böcker & Finger, 2017, and the references therein). Overall, then, agrochemical manufacturers face significant demand uncertainty and so are confronted with challenging inventory decisions. Complicating the problem further is that production processes for crop protection chemicals are, like those for pharmaceuticals, complex and time consuming: the total lead time of active ingredient synthesis, product formulation, and product distribution can run as long as 18 months (Comhaire & Papier, 2015; Shah, 2005). It follows that agrochemical manufacturers must make their inventory decisions well ahead of their products' selling seasons.

Given the foregoing description of the agrochemical market (and the properties of crop protection chemicals), one might be tempted to derive optimal inventory policies by applying the classic newsvendor model. Upon closer inspection of the setting, however, it is evident that two assumptions of that model severely limit its applicability in this context—similar limitations can be found for other products whose sales follow climatic seasons and that must be preproduced (e.g., lawn and gardening items, sun care products, and nonfood specials at discount retailers). First, the newsvendor model assumes that demand materializes at a single moment in time; thus it abstracts from the extended period of time characteristic of many selling seasons. In doing so, the model ignores that customer demand may change over time—for instance, there might be little demand at the start of the selling season but strong demand at the end (or vice versa). Accounting for the customer demand pattern becomes relevant when a firm is confronted with nonnegligible costs of holding inventory, as is the case for agrochemical manufacturers. In the agrochemical industry, contribution margins can differ widely across products; and while inventory holding costs may only have a minor impact on the profitability of high‐margin products, the impact is substantial for low‐margin products. For instance, holding a product with a gross margin of 20% for 3 months even at a moderate monthly holding cost rate of 1% erases a significant share of that product's financial potential. For other products, the situation is even worse: toxicity and special storage requirements can lead to much higher inventory holding cost rates.

Second, and even more problematic, the classic newsvendor model assumes that firms have perfect information about the timing of customer demand—in other words, it assumes that the demand timing is deterministic. As a result, the newsvendor model yields a simple inventory timing criterion: inventory should be made available just before demand occurs. However, this simplistic rule does not work for products with climatic seasons as, for instance, in the agrochemical market. Because farmers adjust their purchase of crop‐protecting chemicals in response to a number of erratic factors—including weather conditions as well as (volatile) crop prices—the timing of their demand is uncertain from the vendor's perspective; hence agrochemical manufacturers must make their inventory decisions in the context of great uncertainty regarding demand timing and quantity (Bouma, 2003; Teasdale & Shirley, 1998). In order to manage these uncertainties proactively, firms must carefully choose not only their inventory quantity but also their inventory timing. Deriving the optimal inventory quantity and timing and studying the interaction effects between these two decisions are the aims of our study.

As for inventory timing, agrochemical manufacturers could place a safe bet and decide to have next season's inventory ready immediately after the previous season ends. Yet such an inventory policy is economically infeasible: manufacturers would incur prohibitive inventory holding costs because items would be held in stock for many months without a single purchase. Also, because of highly complex production processes, classic quick‐response strategies in the spirit of Fisher et al. (2001) can hardly be applied in this context either. To save on holding costs, firms must therefore choose an inventory timing that is much closer to the expected start of the selling season; however, the later their inventory becomes available, the higher is the risk of early customer demand not being satisfied. So in their choice of inventory timing, firms must strike a balance between reducing their holding costs and increasing their risk of unserved demand. Naturally, this trade‐off also has immediate implications for a product's optimal inventory quantity.

The extant literature on inventory management for products with a limited selling season has more than adequately addressed the topic of how best to choose an optimal inventory quantity (see, e.g., Arrow et al., 1951; Cachon & Kök, 2007; Silver et al., 2017; Song et al., 2020). Yet it has failed to inform decision‐makers about how to choose the optimal inventory timing, especially in the case of a stochastic selling season, and neither has it discussed the interaction effects between a firm's inventory timing and quantity decisions. We seek to fill this research gap by developing a stylized model that captures the basic trade‐offs underlying the firm's inventory timing and inventory quantity decision. In short, our model enables a systematic study of the firm's optimal inventory policy.

Our contributions

The theoretical model we develop yields two novel insights concerning the management of inventories of products for which there is a limited (and stochastic) selling season.

First, we characterize an optimal inventory policy by deriving the firm's optimal inventory timing and also its optimal inventory quantity. We find that the latter reflects a timing‐adjusted critical fractile solution, whereas the former depends on (a) the expected customer demand pattern and (b) the hazard rate of the season's starting time. In addition, our results identify a nontrivial interaction between the firm's quantity and timing decisions. We also show how a firm can use its inventory timing to manage inventory holding costs; thus the firm, in essence, uses its timing decision to “steer” the effective profit margin of its products. It is this endogenization of profit margins that allows the firm to sell its products profitably even when faced with significant holding costs and highly uncertain demand. We also quantify the effect of an optimal inventory timing on a product's profitability by conducting a numerical analysis for a realistic range of parameters: we find that optimal inventory timing increases expected gross margins by

Second, we disentangle the performance implications of an optimally chosen inventory timing. More specifically, we identify the conditions under which, with a later inventory timing, the firm not only increases its profits but also improves customer service—even though the risk of missing early season demand increases. The reason for this rather surprising result is the existence of subtle interaction effects between the firm's inventory timing and quantity decisions. With a later inventory timing, the firm increases (decreases) its effective underage (overage) costs because it saves on inventory holding costs; this altered cost structure may lead the firm to stock more items and thereby allow it to satisfy more demand. Our analysis reveals that this interaction effect is most prominent when inventory holding costs and demand uncertainty are significant.

Our main insights suggest a set of key managerial guidelines. First, the findings presented here underscore that managers should choose their inventory timing carefully. Being overly hasty and always offering inventories early on is not necessarily a wise strategy; in fact, such a naïve decision rule may well reduce profits as well as customer service. Second, managers should realize that their inventory timing flexibility is an effective tool with which to combat high inventory holding costs and high levels of uncertainty about customer demand patterns. It is ultimately a product's inventory timing that determines whether or not that product will be profitably sold. Last, managers should carefully align their inventory quantity and timing decisions and thus consider them jointly in their planning process.

Related literature

Inventory management for products that have uncertain customer demand patterns is a topic of long‐standing academic interest (Arrow et al., 1951; Petruzzi & Dada, 1999; Ravindran, 1972; Silver et al., 2017; Whitin, 1955). The central question addressed by this stream of literature is as follows: How much inventory should be stocked so that uncertain future customer demand is best satisfied? Given the importance of this question for virtually every product, scholars have devised a wide range of answers regarding many different product and market environments; for an excellent overview of the extant research, see Axsäter (2015). Most closely related to our work is the classic newsvendor literature on inventory management for products with a limited selling season. In essence, that model characterizes the optimal inventory quantity for a firm selling a single product with probabilistic demand over a single selling season (Porteus, 1990). This model has been extended to enhance its practical applicability by incorporating additional pricing decisions (Cachon & Kök, 2007; Petruzzi & Dada, 1999; Raz & Porteus, 2006; Salinger & Ampudia, 2011), different risk attitudes (Chen et al., 2009; Eeckhoudt et al., 1995), varying degrees of demand information (Ben‐Tal et al., 2013; Perakis & Roels, 2008), the benefits of quick‐response strategies (Cachon & Swinney, 2011; Iyer & Bergen, 1997; Milner & Kouvelis, 2005), and the impact of different inventory financing options (Gaur & Seshadri, 2005; Kouvelis & Zhao, 2012).

The extension with the greatest bearing on our study examines the value of postponing production in a newsvendor context (e.g., Anupindi & Jiang, 2008; Iyer et al., 2003; Ülkü et al., 2005; Van Mieghem & Dada, 1999). This stream of literature studies the optimal starting time for a firm's inventory production, with a later production leading to more accurate demand forecasts yet also to higher production costs. Research has extended initial findings to discuss the applicability of different mechanisms for updating demand forecasts (Boyaci & Özer, 2010; Oh & Özer, 2013; T. Wang et al., 2012), the role of production lead times (Y. Wang & Tomlin, 2009), and the impact of multiple sales opportunities (Song & Zipkin, 2012). We concur with these papers' argument that a firm's production (or inventory) timing is a critical decision for effective inventory management; however, we extend—and complement—previous research by analyzing a practically relevant yet overlooked trade‐off. In particular, the primary reason for a later inventory timing may not always be the acquisition of more precise demand information; rather, such timing serves as a tool for reducing high inventory holding costs while hedging against uncertainty in the demand pattern of customers. Of course, a firm's cost structure also interacts with the firm's ability to wait for advanced demand information: reduced inventory holding costs allow the firm to wait longer for more precise demand information, and once obtained, this advanced information can then be used to lower inventory holding costs even further.

Finally, our contribution can be viewed from the perspective of research on (random) product obsolescence and its effects on a firm's optimal inventory quantity. Initiated by the pioneering work of Hadley and Whitin (1961), Hadley (1962), and Hadley and Whitin (1962) and later extended by Pierskalla (1969), Nahmias (1977, 1982), and Song and Zipkin (1996), this literature addresses the optimal inventory quantity for a firm that must balance its inventory holding costs with the risks originating from a stochastic selling season. We follow this stream of work by investigating how inventory holding costs affect a firm's optimal inventory policy when the firm's selling season is stochastic. However, we depart from this literature by allowing the firm to choose its inventory timing endogenously. Because the papers cited here all assume that a firm's inventory timing is exogenous, they ignore the effects of holding costs or a stochastic selling season on a firm's inventory timing decision.

The paper is organized as follows. We introduce our theoretical model in Section 2 before we derive the firm's optimal inventory policy in Section 3. We then study how varying customer demand patterns affect the firm's optimal inventory policy (Section 4), and we provide a numerical study that quantifies the benefits of an optimal inventory timing (Section 5). Section 6 summarizes our results and discusses some limitations of our analysis. All proofs are relegated to Appendix A.

MODEL SETUP

We base our model of a firm with a stochastic selling season on the fundamentals of the classic newsvendor model. Thus, we consider a firm that sells a single product over a limited selling season and that must decide on an inventory policy well before the season starts. So, when selecting its inventory policy, the firm has imperfect information about customer demand—in terms of the product's demand volume and the exact shape and timing of the customer demand pattern. Once production is completed and the firm's inventory becomes available, the firm can use that inventory to satisfy customer demand; yet the firm also incurs inventory holding costs until the inventory is either depleted or salvaged. The salvaging of all unsold items occurs at the end of the selling season when customer demand has ceased. The rest of this section details our model setup and assumptions.

Inventory policy and stochastic selling season

The classic newsvendor model—the starting point of our theoretical model—is useful for firms that are confronted with stochastic demand over a finite selling season and that must make a single inventory quantity decision before the start of their selling season. As discussed in Section 1, those assumptions approximate the reality in our motivating example, the agrochemical industry, reasonably well. In particular, in the agrochemical industry, demand is clearly uncertain and seasonal. Moreover, due to complex production processes and a global supply chain structure, production lead times are long, which severely limits an agrochemical manufacturer's ability to adjust inventory quantities close to the selling season. Furthermore, significant setup costs prevent agrochemical manufacturers from spreading production over time; thus while the details of the production process are of course more complex, the assumption of a single‐order opportunity captures the essence of a manufacturer's limited flexibility rather well.

Those commonalities notwithstanding, the classic newsvendor model also exhibits a major shortcoming: it ignores the possibility of a stochastic selling season, which is a key issue in the agrochemical industry. To account for the peculiarities of a stochastic selling season, we extend the classic newsvendor model along two dimensions. First, besides deciding on the inventory quantity

Second, we depart from previous work by considering stochasticity in the product's selling season (i.e., in the shape and timing of the customer demand pattern), and not just the product's demand volume

We assume that customer demand occurs only within the selling season and that unserved customers are lost. The mathematical implication is that, for any given

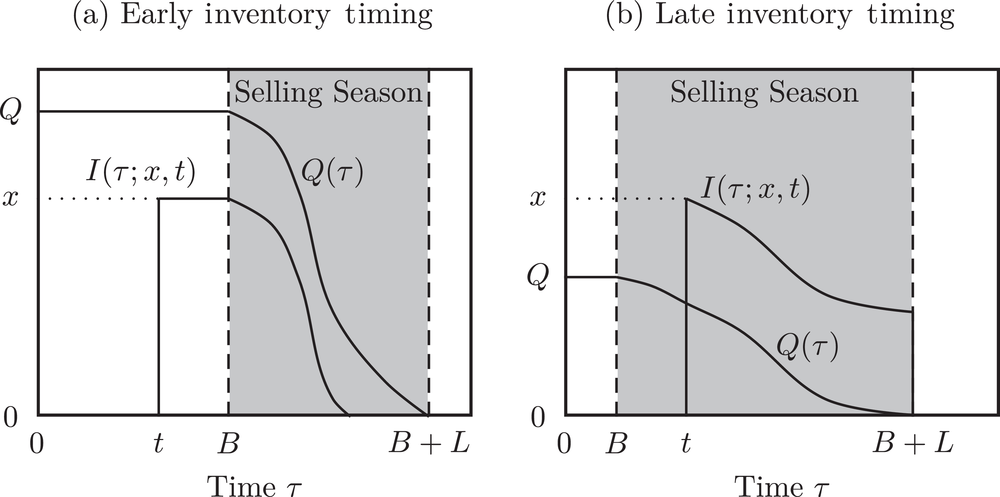

Figure 1 illustrates the relationships among a product's demand volume, the properties of its selling season, and the firm's inventory policy: in the left panel, the firm's inventory timing occurs prior to the beginning of the selling season (i.e.,

Inventory policy and customer demand pattern

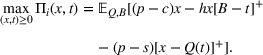

The firm's optimization problem

The firm's goal is to maximize its profits. As in the classic newsvendor model, the firm incurs a per‐unit production cost

Taken together, these considerations require the firm to choose an inventory policy

SERVING A STOCHASTIC SEASON

We now study the properties of a firm's optimal inventory policy. We begin by formally deriving the firm's optimal inventory quantity and timing (Section 3.1). Then we investigate how those optimal decisions interact and evaluate how the chosen inventory policy affects the firm's ability to satisfy customer demand (Section 3.2).

The optimal inventory policy

To better disentangle the different forces at play, we derive the firm's optimal inventory policy in two steps. First, we characterize the firm's optimal inventory quantity For given for any for any

Moreover,

The proposition shows, in line with prior work on the newsvendor problem (see, e.g., Cachon & Kök, 2007; Petruzzi & Dada, 2010), that the optimal inventory quantity

As in the classic newsvendor model, the firm's optimal inventory quantity increases with the product's sales price

Proposition 1 reveals that the firm's inventory timing affects the optimal inventory quantity in two distinct ways: namely by (a) determining the addressable portion of demand

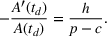

Equipped with these insights, we now turn to the firm's optimal inventory timing decision. To this end, we analyze how the firm selects its optimal inventory timing The optimal inventory timing

Two opposing effects determine the firm's optimal inventory timing. With a later inventory timing, the firm is able to reduce the time that items, which are sold later in the season, must be stored; the firm can hence reduce inventory holding costs. At the same time, however, the firm becomes more susceptible to losing demand early in the season; as a result, some items may need to be stored for a longer period of time until they are sold—if they are sold at all. Proposition 2 shows that the optimal inventory timing equates to the marginal impact of

Proposition 2 also establishes that, as a consequence, choosing the earliest possible inventory timing (i.e.,

Inventory timing and customer service

Because the firm's future demand volume

As a starting point, we shed more light on the interaction between the firm's inventory timing Let

Lemma 1 provides a necessary and sufficient condition for

Parts (i) and (ii) of Lemma 1 provide further insights into the leading role that inventory holding costs play in the interaction between a firm's inventory quantity and timing decision. If there are no holding costs (

As an aside, Lemma 1 also establishes an interesting interplay between demand uncertainty and the firm's optimal inventory quantity. Suppose that

So far, we have established that the optimal inventory quantity may (or may not) increase with the firm's inventory timing. This finding allows us to examine the impact of the firm's inventory timing on its performance in terms of satisfying customer demand. In particular, will an earlier inventory timing always lead to a greater amount of satisfied demand, or equivalently, to a lesser amount of lost sales?

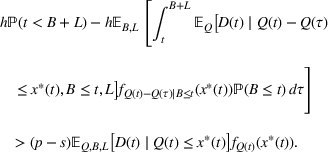

Note that lost sales in our setting occur for two different reasons: (i) demand occurs before the firm's inventory timing or (ii) the inventory quantity has been depleted. So for a given inventory policy

The main outcome of Proposition 3 is that, in optimum, the firm's expected lost sales may decrease with its inventory timing—but only if inventory holding costs are sufficiently high. So if

From a managerial perspective, Proposition 3 falsifies the seemingly convincing argument that earlier inventory availability necessarily leads to a higher level of satisfied demand. In fact, a premature inventory timing may reduce a firm's capacity to satisfy demand because high inventory holding costs may force the firm to reduce its inventory quantity which, in turn, harms its service performance.

IMPACT OF CUSTOMER DEMAND PATTERN

The conditions that characterize the optimal inventory quantity and timing for a firm that faces a stochastic selling season are rather complex; this complexity is due to the interplay of several opposing forces (cf. Section 3.1). In this section, we aim to isolate some of those relevant effects to garner further insights by studying two special cases that are both instructive and practically relevant. In the first case, a firm is confronted with instantaneous demand; this setting allows us to isolate how uncertainty in demand timing (as captured by

Instantaneous demand

It is common in the newsvendor literature to abstract from the dynamics within the selling season and instead to assume that all demand occurs at a single and ex ante known moment in time (see, e.g., Choi, 2012; Petruzzi & Dada, 1999, 2010; Qin et al., 2011). Given that assumption, the firm's inventory timing is trivial: inventory should be made available just before demand occurs. In this section, we follow the assumption of instantaneous demand—that is, in our demand model, we set the season length to zero:

Despite its simplicity, the assumption of instantaneous demand is a reasonable approximation of the market structure in many real‐world scenarios. Thus instantaneous demand is a realistic assumption if (a) a firm's selling season is indeed short (e.g., only a few days) and/or (b) its in‐season holding costs are negligible (though preseason holding costs may still be important). Under those conditions, the firm's optimization problem (1) reduces to Assume that

As in our base model, the firm's optimal inventory quantity is determined by a critical fractile condition on

There is an appreciable reduction in complexity when comparing the firm's inventory timing under instantaneous demand (as given by (8)) with our base case of a finite season length (as given by (3)). Here, the firm's optimal inventory timing is determined by a simple hazard rate condition that balances the firm's earliness/holding costs with its tardiness costs (i.e., expected lost revenues). In particular, the firm should choose its inventory timing such that, at

According to Proposition 4, a firm's optimal inventory timing

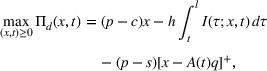

Deterministic selling season

In this section, we study more closely how the properties of Assume that

This proposition reveals that, for a deterministic selling season and moderate holding costs, the firm simply chooses its inventory quantity so as to satisfy all demand that occurs after the inventory timing (i.e.,

An intriguing observation is that a firm's optimal inventory timing depends on the slope and curvature of

QUANTIFYING THE IMPACT OF INVENTORY TIMING

Having characterized the main trade‐offs that the firm must balance with its inventory policy when serving a stochastic selling season, we now turn to the magnitude of the effects resulting from an optimally chosen inventory policy. Through an extensive numerical simulation, we investigate (a) whether (or not) inventory timing has a first‐order effect on firm profits and (b) how the firm's inventory policy and profits are affected by parameter changes.

Simulation setup and choice of parameters

To shed light on the influence of our various model parameters, we constructed our simulation study in a full factorial design over a wide range of parameter values, as listed in the leftmost column of Table 1. In total, we analyze 2187 different scenarios. The chosen parameter values reflect typical agrochemical products and their selling seasons, as discussed below.

Results of numerical experiments

As for product characteristics, we account for the reality that agrochemical products differ widely in (a) their profit margins and (b) their inventory holding costs (e.g., because some products rely on more expensive raw materials than others or require special storage conditions). We represent products with different profit margins by fixing the sales price

With respect to the characteristics of the selling season, we differentiate between a “near‐instantaneous” season (

We implemented our numerical simulation in MATLAB. To identify the optimal inventory policy

The benchmark policies

To assess the value of an optimal inventory timing, we compare the optimal inventory policy

Our second benchmark mirrors current practice in the agrochemical industry much more closely. In our experience, managers find the quantity trade‐off easier to make than the timing‐related trade‐offs. As a result, while their inventory quantity effectively balances underage and overage costs, managers are biased in their timing decision toward early product availability—in an attempt to minimize lost sales. In addition, we observed that the interdependencies between quantity and timing choices tend to be overlooked. We mimic this behavior in our second benchmark policy, referred to as the “

Simulation results

The results of our numerical experiments are summarized in Table 1. Columns 2–5 show the simulated profits; for a given inventory policy

Table 1 also shows which parameters chiefly drive the profit increase. Clearly, when profit margins are sufficiently high or holding costs are low, then the firm's primary concern is to maximize demand coverage. Thus, the benefits of deviating from

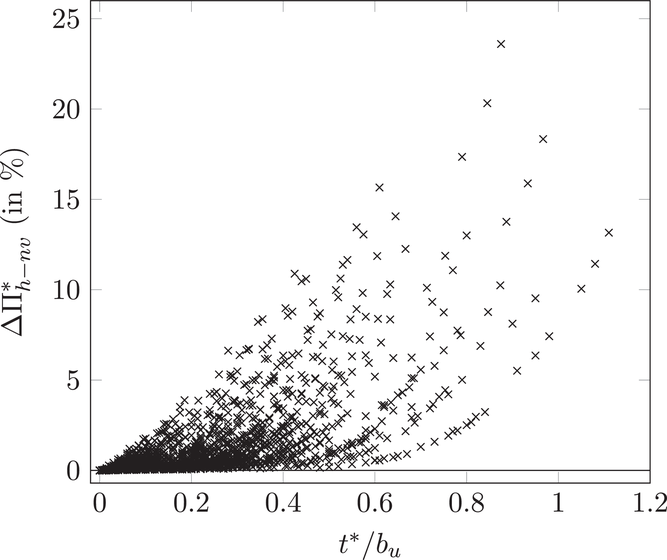

A second important observation is that inventory timing has a stronger effect on firm profits than an isolated adjustment of the firm's inventory quantity. In particular, whereas an optimally chosen inventory timing leads to as much as 10% higher profits in our numerical study (using the 95% quantile), adjusting the inventory quantity to holding costs—while fixing

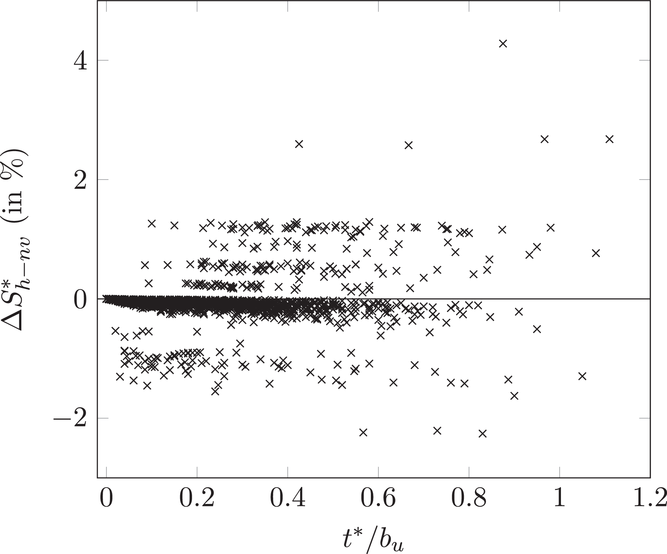

Figures 2 and 3 provide further insights into the optimal inventory policy and connect that policy to the more advanced

Inventory timing and firm profits

Inventory timing and expected sales

Naturally, the interaction between

IMPLICATIONS AND LIMITATIONS

The goals of this paper are to establish the importance of a firm's inventory timing decision and to show that inventory timing has a first‐order effect on both firm profits and customer service. We take the perspective of a firm that sells a single product over a stochastic selling season, which means that the firm has imperfect information about when exactly the selling season would be, how much demand there would be, and how demand would be distributed over the season. We motivated our analysis based on observations in the agrochemical industry; yet, similar multifaceted uncertainties are also present for other products with climatic selling seasons such as lawn and gardening items, sun care products, and nonfood specials at discount retailers. We establish the firm's optimal inventory policy, unravel the interaction effects between the firm's inventory quantity and inventory timing, demonstrate that an optimally chosen inventory timing enables the firm to increase profits and simultaneously reduce lost sales, and disentangle how the various properties of a selling season affect a firm's inventory policy. At the heart of this analysis is our insight that the firm, through its inventory timing, can endogenize (a) the profit margin of its products by determining its exposure to inventory holding costs and (b) its future demand and lost sales. We show that this flexibility may lead to a nonmonotonic interrelation between the optimal inventory quantity and timing.

A naïve approach to inventory timing might suggest to simply make products available right before the start of their selling season; yet our findings show that this thinking is flawed for two reasons. First, in many practical applications, it is not clear exactly when customer demand begins to occur (e.g., when demand depends on weather conditions). Managers thus have to determine at what moment in time their demand potential is sufficiently strong to justify inventory availability. The intuition behind this result is similar to the classic newsvendor logic that managers, when confronted with uncertain demand volumes, should not blindly maximize demand coverage. Second, even if the start of the selling season can be predicted fairly precisely, making inventory available immediately can be very costly; particularly so if inventory must be stored for a long period of time before being sold. Hence, managers—through their inventory timing—should always trade off (the risk of) losing some demand early in the season against higher profit margins for items that are sold later in the season. Our numerical analysis for a realistic range of parameters from the agrochemical industry shows that optimal inventory timing increases expected gross margins by

Like other theoretical models, ours is an abstraction of reality. In the formulation process, we chose to focus on a single‐product setting and to disregard capacity considerations. We believe that, in doing so, our framework takes a crucial first step toward the end of understanding optimal inventory timing decisions; in the real world, however, managers must coordinate the inventory timing of many different products—and especially when these products share a common (capacitated) production process. In the multiproduct case, managers must sequence the production of the different products and must therefore decide which products to produce earlier or later. That decision will directly influence each product's inventory holding costs and hence the product's effective profit margin. We view the interaction effects between different products and their inventory timing as a promising direction for future research.

Another practically relevant question concerns the specifics of the production process. On an aggregate level, we have considered production as an integrated process. Yet real‐world production processes are typically “layered”: the product passes through multiple production steps (e.g., synthesis of active ingredients, product formulation, packaging). Such a multistage production process poses additional constraints on a firm's inventory decisions. It would be instructive to explore how different production processes affect a firm's inventory timing. Last, for some practical applications, it might also be worthwhile to explicitly consider the influence of inventory availability on customer demand (see, e.g., Baron et al., 2011; Urban, 2005) and to endogenize a firm's pricing decision (see, e.g., Raz & Porteus, 2006; Petruzzi & Dada, 1999). Naturally, we would expect firms to choose an earlier inventory timing if inventory availability has a positive effect on customer demand; yet, the effect of an optimal pricing decision on a firm's inventory timing is not immediately obvious.

In sum, we believe that our work sheds light on the core trade‐offs underlying a fundamental managerial decision: a seasonal product's inventory timing. Our analysis of a firm's optimal inventory policy yields managerial recommendations as a function of the product's cost structures and the (stochastic) pattern of customer demand. Thus we have made some headway toward a better understanding of optimal inventory timing decisions for seasonal products.

Footnotes

PROOFS

ACKNOWLEDGMENTS

The authors thank the department editor, Panos Kouvelis, for his support throughout the review process. The authors are most grateful for the continuing support from the senior editor, and the thoughtful and constructive comments from two anonymous reviewers. Their suggestions considerably improved the manuscript.