Abstract

Blockchain is a prominently discussed technology in operations and supply chain management and firms increasingly engage in blockchain initiatives. Yet, an understanding of the technology's financial value remains elusive. Based on 175 firm announcements between 2015 and 2019, we conduct an international event study to estimate the impact of blockchain initiatives on the market value of the firm. We empirically demonstrate that blockchain announcements are associated with a significant average abnormal return of 0.30% on the announcement day, and that there are indications of positive long‐term effects on shareholder value. We further demonstrate how blockchain use case, project, and firm characteristics affect the stock market reaction. Specifically, we find that the stock market reaction to blockchain announcements is less positive when blockchain is used to trace physical objects or to share sensitive data, providing empirical evidence for the risk associated with current challenges in the design of blockchain use cases. Our results also suggest that the involvement of an external information technology service provider in a blockchain project attenuates the positive stock market reaction. Interestingly, more innovative firms do not experience a stronger stock market reaction to blockchain announcements. Leveraging the international scope of our sample, we further shed light on how the firm's competitive (i.e., industry factors) and macro environment (i.e., country factors) affect the stock market reaction. Our findings indicate that the industry's R&D intensity and the country's data restriction level play a crucial role in driving the value attributed to blockchain initiatives.

Introduction

Every region and industry has developed an intense interest in how blockchain can be used to improve market efficiencies and reduce costs and latency. But there's still a significant gap between the hype and market reality. Gartner Research, Jul 2019

Numerous startups have been founded and inter‐organizational projects initiated in order to explore blockchain's potential for operations management, seeking cost reductions and opportunities for radical business model innovation (Choudary et al. 2019). The early adopters Maersk and Walmart made headlines around the globe with pilot projects of global trade platforms (Choudary et al. 2019) and food traceability solutions (Furlonger and Uzureau 2019). More recently, the MediLedger blockchain consortium, including Pfizer, Sanofi and Novartis, announced the success of a large‐scale pilot project, proposing the use of blockchain for secure prescription drug track and trace services for the U.S. Food and Drug Administration (MediLedger 2020). The academic community reflects this immense industry interest in blockchain. The mostly conceptual and analytical literature discusses a wide range of potential blockchain applications for operations and supply chain management, including supply chain transparency (Chod et al. 2020, Gaur and Gaiha 2020, Hastig and Sodhi 2020), inventory management (Babich and Hilary 2020), counterfeit detection (Pun et al. 2021, Shen et al. 2021), or multiparty data sharing (Wang et al. 2021).

In contrast to the high expectations, the market reality suggests that blockchain applications in operations and supply chain management, which can generate actual business value, are still scarce (Furlonger and Uzureau 2019). In fact, only around 8% of 26,000 blockchain projects in 2017 were still active one year after their launch (Babich and Hilary 2020). An article in the Forbes Magazine even raised the question (Marr 2018): “Is This The End Of Blockchain?.” Despite increasingly critical press, initial pilot projects provide anecdotal evidence for the technology's potential to reduce cost (Radocchia 2019). In the aerospace industry, for instance, firms like Moog, Honeywell or Air New Zealand are leveraging blockchain to create secure digital marketplaces for 3D‐printed aircraft parts, reporting cost savings of up to 30% (Tampi 2020). Building on the anecdotal evidence, more research on the value of blockchain is crucial to further narrow the gap between expectations and reality.

The value of information technology (IT) has always been a topic of central importance at the interface of information systems and operations management. Examining IT business value, multiple studies find empirical evidence for a positive relationship between IT initiatives and financial firm performance (e.g., Bose and Leung 2019, Bradley et al. 2018). IT initiatives are generally associated with cost reductions and operational efficiency gains, generating revenue, and firm value (see Bose and Leung 2019, Melville et al. 2004). Examining the short‐ or long‐term consequences of IT initiatives on the stock market, prior studies find an increase in stock market returns after announcements of e‐commerce platforms (Dehning et al. 2004, Subramani and Walden 2001), ERP systems (Hendricks et al. 2007, Ranganathan and Brown 2006), or mobile apps (Boyd et al. 2019).

In the context of blockchain, Cheng et al. (2019) explore investor overreaction in times of a “blockchain mania,” characterized by overly positive technology expectations. The authors use the Bitcoin price as a proxy for the public attention towards the technology, and empirically demonstrate that investors overreact to speculative blockchain announcements. Examples for speculative announcements are not associated with a specific blockchain project and include appointments of board members with blockchain experience, or simply vague plans to adopt blockchain in the future. The stock market reaction is stronger when Bitcoin prices are higher. While this study investigates the implications of the hype around firm announcements using blockchain as an example, the authors are not specifically examining the value of substantiated blockchain initiatives. Substantiated blockchain initiatives are associated with specific projects that define a clear use case for blockchain, beyond solely exploratory purposes. Similar to Cheng et al. (2019), Cahill et al. (2020) use an international sample of mainly speculative blockchain announcements to empirically link the stock market reaction to the price performance of Bitcoin. To the best of our knowledge, no empirical studies examine the financial consequences of substantiated blockchain initiatives and explore the effects of use case, project, and firm characteristics.

In light of the high academic and practitioner interest in the technology, it is crucial to approach the question regarding the value created by blockchain. Scholars commonly employ the event study method as a first attempt to quantify the value of novel IT systems (Bose and Leung 2019, Dehning et al. 2004). An event study approach allows measuring the short‐term value that investors attribute to newly announced IT initiatives, based on expectations of future cash flows (Boyd et al. 2019). At the current stage of blockchain maturity, the method can provide a first indication for the (future) business value associated with blockchain initiatives in operations and supply chain management. Specifically, we conduct an international event study, analyzing a sample of 175 blockchain announcements from 100 unique firms across 11 industries and 15 different countries, to provide evidence of the shareholder value implications associated with blockchain initiatives. We complement our analysis with five robustness checks to ensure that endogeneity‐induced effects are not biasing our results, including a propensity score matching (PSM) approach and a Heckman two‐step model.

Our contribution related to the value of blockchain is threefold. First, we find a positive stock market reaction to announcements of blockchain initiatives in the context of operations and supply chain management. Specifically, we demonstrate that our sample firms experience a significant average abnormal return of 0.30% on the announcement day. In a post‐hoc test, we further find indications for a positive long‐term effect on shareholder value. Providing empirical evidence for an increase in stock market value, our study adds to the largely conceptual discussion on how blockchain can create value for firms (Babich and Hilary 2020, Hastig and Sodhi 2020). Second, as the information systems literature suggests that IT business value is sensitive to different factors in‐ and outside the focal firm (Melville et al. 2004), we explore when blockchain initiatives create the most value. We show that investors value blockchain use cases that are characterized by the tracing of physical objects and the sharing of sensitive data less positively, potentially anticipating additional challenges. We further find that firms involving an external IT service provider to implement blockchain experience significantly less positive stock market reactions. More innovative firms experience a weaker and more productive firms a stronger stock market reaction. Our findings complement the information systems and operations management literature on the value and conditions of IT initiatives (e.g., Bose and Leung 2019, Boyd et al. 2019, Hendricks et al. 2007). Third, in a post‐hoc test, we extend our scope of factors driving IT business value. We examine how firms' competitive and macro environment affect the stock market reaction to announcements of blockchain initiatives, suggesting that industry R&D intensity accentuates the positive stock market reaction, while certain country factors, such as the data regulation restrictiveness, attenuate the positive impact on shareholder value.

Background and Hypotheses Development

We conduct our hypotheses development in two steps. First, we present previous work on the financial consequences of IT initiatives and review the limited set of studies on blockchain, to argue for a systematic stock market reaction to blockchain announcements in the context of operations and supply chain management. Second, we discuss the effects of blockchain use case, project, and firm characteristics on the magnitude of the stock market reaction.

Stock Market Reaction to Blockchain Announcements

As prior studies show that announcements of IT initiatives can generate stock market value (e.g., Bose and Leung 2019, Boyd et al. 2019), we argue that investors will also react to the potential benefits associated with the announced blockchain initiatives. In operations and supply chain management, blockchain is mainly associated with (1) the reduction of inter‐organizational transaction costs and (2) the facilitation of new business models (Babich and Hilary 2020, Olsen and Tomlin 2020). Specifically, research suggests that blockchain could improve supply chain traceability (Hastig and Sodhi 2020, Pun et al. 2021, Sodhi and Tang 2019), enhance data and knowledge sharing between supply chain partners (Olsen and Tomlin 2020, Wang et al. 2021), secure and speed up inter‐organizational payments (Kumar et al. 2018), and automate order processing (Babich and Hilary 2020), all ultimately leading to more cost‐efficient processes. In practice, first successfully completed projects provide anecdotal evidence. For instance, the consumer goods company Unilever reports substantial cost savings using blockchain to safeguard digital advertisement spending (Guzenko 2019).

Blockchain can also facilitate business model innovation. One promising application domain is additive manufacturing, where blockchain could address notable intellectual property (IP) and data security concerns, facilitating the emergence of inter‐organizational additive manufacturing networks. These networks allow participants to trade IP‐protected additive manufacturing design files and sell unused manufacturing capacities, generating additional revenue streams for firms (Lacity 2018). In general, extending existing or adopting new business models provide new sources of revenue, increasing anticipated future cash flows. In sum, we propose that investors positively assess the cost reduction and business model potential of blockchain initiatives, reflected in an overall positive stock market reaction.

Blockchain announcements are associated with a positive stock market reaction.

Factors Influencing the Stock Market Reaction

Multiple studies examine different factors that influence the effect of IT on financial firm performance (Bose and Leung 2019, Ranganathan and Brown 2006). These factors can be both internal and external to the focal firm. According to the IT business value framework by Melville et al. (2004), internal factors correspond to characteristics of the focal firm, while external factors relate to business partners, the competitive environment (i.e., industry factors), and the macro environment (i.e., country factors).

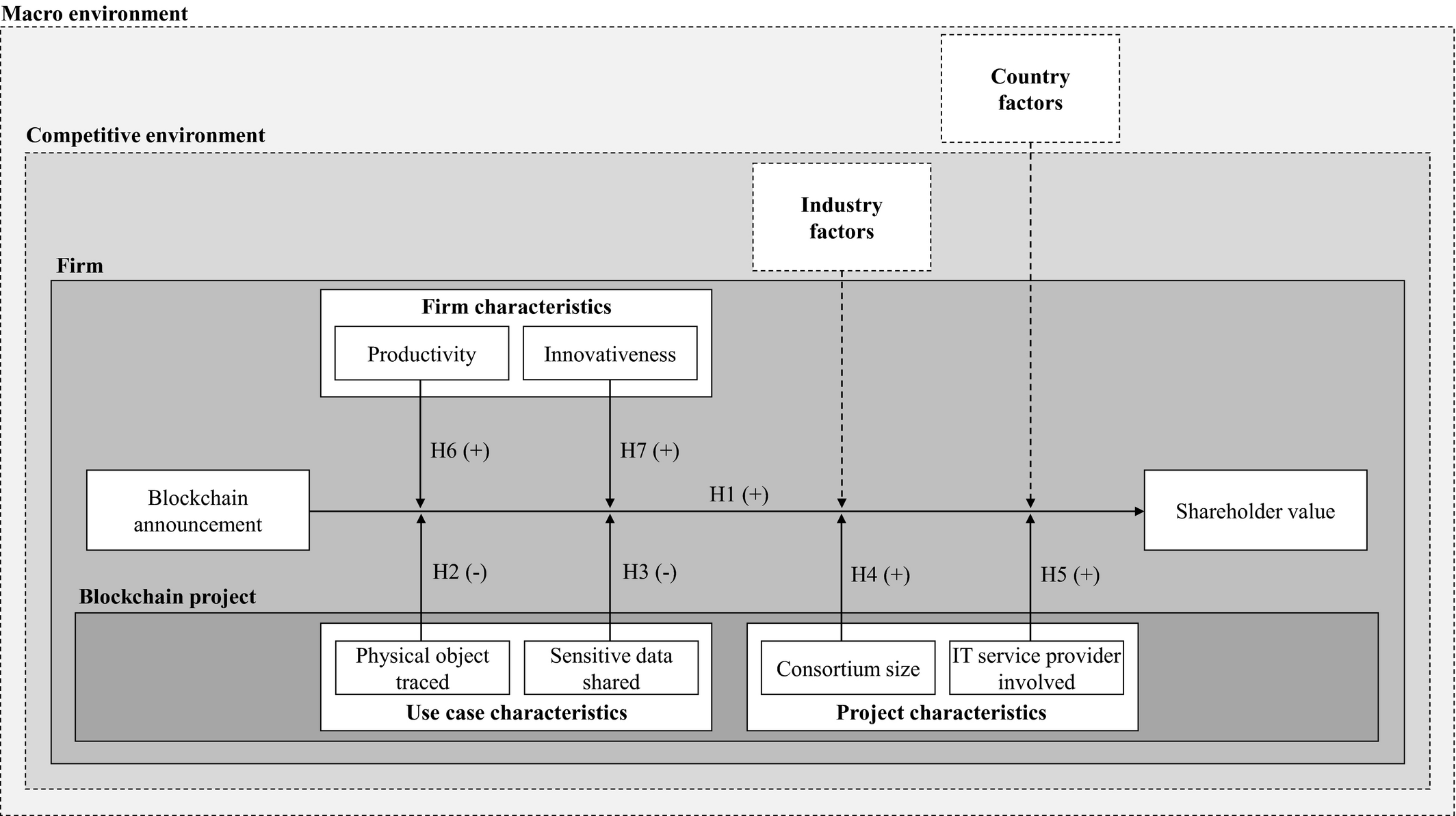

Since the business value of blockchain applications critically depends on an adequate use case design (Furlonger and Uzureau 2019, Pun et al. 2021, Tucker and Catalini 2018), we first focus on the designated blockchain use case. We specifically argue how certain blockchain use case characteristics affect the stock market reaction. Since blockchain is an inter‐organizational technology, the information systems literature suggests that the IT project setting is particularly important in determining IT business value. Hence, second, we discuss the effects of blockchain project characteristics. Third, we provide arguments on how firm characteristics influence the stock market reaction to blockchain announcements. In our post‐hoc analysis, we further explore the role of industry and country factors. The resulting conceptual framework is depicted in Figure 1.

Conceptual Framework (dashed lines indicate scope of post‐hoc analysis)

The Effects of Blockchain Use Case Characteristics

Since the fit between a technology and the corresponding business process is essential (Drake et al. 2016, Melville et al. 2004), we examine how the blockchain use case, understood as the business process to be improved by blockchain, affects the stock market reaction. Research has identified several blockchain use cases in operations and supply chain management (e.g., Babich and Hilary 2020, Kumar et al. 2018, Wang et al. 2021). However, multiple use cases are subject to various uncertainties and are not yet fully understood. We argue that the risks and uncertainties associated with specific use case characteristics can affect how a blockchain announcement is valued on the stock market. Specifically, we explore the effects of two associated use case design characteristics, tracing physical objects and sharing sensitive data.

On the one hand, blockchain initiatives in operations and supply chain management can be fully digital solutions (i.e., digital‐native), such as sharing data across the supply chain, managing IP, or distributing tokens for digital services (Babich and Hilary 2020, Olsen and Tomlin 2020). On the other hand, blockchain applications are also frequently designed to trace physical objects, providing a non‐repudiable digital record of data that has to be linked to a physical object. Common examples include blockchain‐based supply chain traceability for food or drugs, authentication of luxury products, or tracing of industrial parts (Hastig and Sodhi 2020, Pun et al. 2021, Sodhi and Tang 2019).

Few studies explore the potential cost savings associated with using blockchain for product traceability. Pun et al. (2021), for example, analytically demonstrate that for a manufacturer selling products in the presence of counterfeits, the adoption of blockchain is beneficial compared to alternative strategies, such as differential pricing. Chod et al. (2020) find that using blockchain for supply chain transparency can also reduce inventory signaling cost. In practice, Walmart has started tracing the flow of Chinese pork on a blockchain throughout the supply chain, assuring provenance from raw material suppliers to end customers. Similarly, startups like Luxchain and Arianee are working with established brands to build blockchain‐based solutions for luxury product authentication (Rossow 2018). Investors might positively value the potential cost savings and revenue gains associated with tracing physical objects.

However, all of these non‐digital‐native applications have to deal with one particular challenge – linking the physical object unequivocally to its data entry on the blockchain (Tucker and Catalini 2018). While data is considered relatively secure and tamper‐proof once stored on the blockchain, verifying the input data remains challenging, exposing the interface between the physical and digital world as the major weak link (Babich and Hilary 2020, Tucker and Catalini 2018). Clearly, digital‐native use cases may also be subject to potential fraud and manipulation, however, it is inherently more difficult, since the digital ecosystem is “closed.”

Consider the example of the UK startup Everledger offering blockchain‐based diamond tracing services. In this case, the initial authentication of the physical diamonds is done manually by an individual, creating a systemic vulnerability (Wollenhaupt 2019). So, if the input data is unreliable, the system is potentially compromised, and blockchain's security potentials undermined. The resulting problem is referred to as garbage in, garbage out (Babich and Hilary 2020). Even though automated solutions utilizing IoT sensors, NFC or RFID chip tagging are being developed and researched (e.g., Shu and Barton 2012), manipulation and fraud through human intervention can still occur (Babich and Hilary 2020, Olsen and Tomlin 2020).

In addition, tracing physical objects may only generate value if it covers the entire life cycle (Wang et al. 2021). Some suppliers might lack the necessary infrastructure and resources to actively participate in blockchain‐based physical object tracing. In contrast to digital‐native applications, physical object tracing requires substantially more technical infrastructure to securely manage the link between the digital and physical world (Lacity 2018). Such infrastructure is costly and strongly depends on the properties of the traced object (e.g., its material, surface, size), making the development of cost‐efficient, standardized and scalable bridging solutions unlikely in the near future.

Until there is a reliable and cost‐efficient way to bridge the physical and digital world, we assume that the perceived business value attributed to a blockchain‐based tracing solution decreases with reliance on external data inputs. Even though using blockchain to trace physical objects has the potential to reduce cost, we assume investors are aware of the ongoing issues related to bridging the physical and digital spheres, and will therefore perceive the potential business value to be lower than for digital‐native use cases.

The positive stock market reaction to blockchain announcements is weaker when the blockchain is used to trace physical objects.

Blockchain, as a database, can also be used to facilitate data sharing. In general, research recognizes that inter‐organizational information sharing drives financial firm performance, as it enhances supply chain visibility and responsiveness, and improves sales forecasting and operational planning. However, a prominent issue with data sharing use cases relates to the ongoing discussion on data security and privacy (Babich and Hilary 2020, Massimino et al. 2018).

Data security is about protecting data from malicious threats, most often by external parties. Blockchain is commonly associated with multiple security and encryption features (Babich and Hilary 2020). Given the distributed nature of blockchain, there is no inherent single point of failure, and external cyber‐attacks could be potentially detected by different members of the blockchain network. Investors might positively value the inherent security features of blockchain. In contrast, data privacy is about using sensitive data responsibly, including internal access and visibility. While multiple studies propose information sharing behavior that results in all parties benefiting (Ghoshal et al. 2020, Scheele et al. 2018), in practice, firms are often reluctant to share information with business partners due to a mutual lack of trust (Guo et al. 2014, Shang et al. 2016). Blockchain is generally portrayed as a system that enables data sharing without the need for mutual trust. In practice, firms face multiple new challenges. For example, the digital ledger is considered “permanent,” which is oftentimes seen as a benefit. However, this can also turn into a disadvantage. As data cannot be erased in retrospect, complying with data privacy regulations can become a challenge (Babich and Hilary 2020). Furthermore, unauthorized access by other members of the blockchain and diffusion of proprietary information, even if unintended, become far more likely (Feng and Shanthikumar 2018). Overall, external and internal vulnerabilities create the risk of sensitive data loss or exposure.

Recent headlines of hacked blockchains and stolen Bitcoins worth millions of U.S. dollars question the security associated with blockchain (Hirtenstein 2021, Orcutt 2019). Based on 72 blockchain breaches reported between 2011 and 2018, Madnick (2019) illustrates the vulnerability of blockchain to external threats, some of which exploit blockchain peculiarities regarding distributed control, anonymity, and immutability. The contradicting evidence on blockchain security may create uncertainty among investors regarding the valuation of blockchain initiatives, especially at an early stage of technological advancement. Prior studies on general data breaches further show that data breaches resulting in the loss of sensitive data have substantial financial consequences (Gwebu et al. 2018, Modi et al. 2015).

While the inherent security features of blockchain indicate the potential to facilitate data sharing, we believe that there is still uncertainty regarding the reliability of these features. We propose that a blockchain used to share sensitive information exhibits higher operational risk, potentially taken into consideration by investors.

The positive stock market reaction to blockchain announcements is weaker when the blockchain is used to share sensitive data.

The Effects of Blockchain Project Characteristics

IT increasingly spans organizational boundaries, driving project‐based IT development. Clearly, organizational project partners are crucial factors that influence IT business value for the focal firm (Han et al. 2012, Ranganathan and Brown 2006). Drawing from the conceptual work of Melville et al. (2004) and empirical studies examining announcements of IT initiatives, we explore the effects of blockchain project characteristics. Specifically, we argue that both the consortium size and the involvement of an external IT service provider affect the stock market reaction.

Blockchain initiatives are commonly organized and developed in inter‐organizational consortia (Babich and Hilary 2020). The consortium size is the number of unique project members that are part of the blockchain development and implementation process, but not necessarily members of the operative blockchain network. Consultancies and universities, for example, can be an important part of a consortium, but not of the eventual blockchain network. In general, literature suggests that announcements of firm collaboration for IT innovation are positively assessed by investors. For instance, Han et al. (2012) show that firms participating in IT development alliances experience significantly higher stock market returns after the announcement. We expect a similar reaction for three reasons.

First, larger consortia generally show a higher degree of organizational diversity, including suppliers, competitors, academic institutions, or public authorities. Combining and leveraging complementary partner resources is a key driver for innovation project success (Ravichandran and Giura 2019). Successful projects can realize cost savings and potential revenue gains earlier. Second, a larger consortium size can be an indicator for the maturity and practical relevance of a blockchain project and affect its perceived value. Arguably, the more project members are involved, the stronger the signal that more parties are willing to invest and dedicate time and resources to the blockchain initiative. In that sense, larger consortia might convey a message to investors that the project has high potential value for the involved firms, driving its chances for success. Third, the value of blockchain initiatives for all members inherently depends on data exchange to create operational efficiencies (Choudary et al. 2019, Niculescu et al. 2018). It seems reasonable that larger consortia are indicative of higher data volumes and coverage at the onset of the blockchain initiative, enhancing the overall quality and completeness of the blockchain input data, which is key to benefiting from information sharing (Chen and Deng 2015, Ebrahim‐Khanjari et al. 2012).

In contrast, larger consortia also exhibit disadvantages. The general willingness to share data could be impeded by a larger number of partners, due to privacy concerns (Pun et al. 2021). A diverse set of consortium members are further more likely to have conflicting interests within the project, driving coordination costs (Vakili and Kaplan 2020). Investors might consider the risks and costs involved with larger and more diverse consortia, cautioning their valuation of blockchain initiatives. Despite these potential issues, in sum, we argue that larger consortia evoke a more positive stock market reaction.

The positive stock market reaction to blockchain announcements is stronger when the consortium is larger.

The information systems literature suggests that especially IT resources and capabilities of project partners influence IT business value (see Melville et al. 2004). Consequently, firms regularly engage in IT outsourcing in order to reduce cost, focus on their core competencies, and regain operational flexibility (Anand and Goyal 2019). Sufficient IT capabilities are crucial when implementing a complex inter‐organizational technology like blockchain. Involving external partners grants access to the latest emerging technologies, such as blockchain, and to the resources and capabilities needed for its adoption. IT service providers with a proven track record in blockchain, such as IBM or Accenture, can contribute a wealth of experience to a new blockchain initiative (Tiwana and Kim 2016). In addition, unlike the majority of transactional databases, blockchain builds upon a decentralized architecture. The decentralized architecture ensures that all blockchain participants hold an independent instance of the database, driving the complexity of the overall IT infrastructure. Including an external IT service provider can help to reduce and manage the technological complexity. Investors may positively value the improved chances of success for the blockchain initiative, as well as the associated financial benefits.

However, in reality, many blockchain initiatives are dominated by one organization, oftentimes the IT firm initiating the project. As a result, the mostly centralized system can lead to undesirable dependencies and asymmetries for the other blockchain network members, while also undermining the core idea of a decentralized blockchain architecture (Furlonger and Uzureau 2019). In addition, blockchain still requires trust in its algorithms and protocols, especially if they have been implemented by a third party, such as an external IT service provider. This problem is referred to as the black‐box effect (Babich and Hilary 2020). To mitigate concerns about data and system security, firms may engage in safeguarding processes, resulting in monitoring costs on top of the regular service charges. Investors might anticipate the costs and risks associated with the involvement of external IT service providers.

However, in the case of blockchain, we argue that the potential benefits associated with the involvement of an external IT service provider will outweigh these risks and uncertainties.

The positive stock market reaction to blockchain announcements is stronger when the project involves an external IT service provider.

The Effects of Firm Characteristics

In line with prior studies on IT initiatives, we discuss how firm characteristics might influence the stock market reaction to blockchain announcements. In this section, we provide arguments on how firm productivity and innovativeness could affect stock market returns.

Firms with higher productivity are generally characterized by the ability to efficiently convert inputs, for example materials or other assets, into outputs, such as products and ultimately revenue (Atkinson et al. 2001, Lanier Jr et al. 2010). Specifically, productivity is associated with superior resource utilization (Chen et al. 2015). We expect such firms to better design, launch, and execute blockchain projects. First, we argue that there are reciprocal effects between IT initiatives and firm productivity, in form of a (positive) feedback loop. Research suggests that IT investments lead to higher firm productivity (Wu et al. 2020). As a technology designed to facilitate secure inter‐organizational information exchange, we expect blockchain to similarly enhance firm operations, and consequently productivity (Babich and Hilary 2020, Hastig and Sodhi 2020). Second, firm productivity is also associated with higher financial agility (Serpa and Krishnan 2018), allowing firms to flexibly allocate sufficient resources to a project, which potentially increases its success rate. Further, it seems reasonable to assume that highly productive firms have more streamlined processes and IT infrastructures. These characteristics indicate substantially lower internal blockchain implementation barriers, in particular the alignment with internal data and IT structures is expected to be less complex and costly (Babich and Hilary 2020). While investors might perceive the potential efficiency gains of blockchain as more marginal for already productive firms, we still propose an overall stronger positive stock market reaction for more productive firms.

The positive stock market reaction to blockchain announcements is stronger when the announcing firm is more productive.

Firm capabilities and knowledge also shape the creation of IT business value. For example, Ba et al. (2013) argue that innovative firms posses specific resources and processes, increasing the probability of a more successful execution of an innovation project. Prior research provides evidence for the potential spillover effects of innovation capabilities (Hu et al. 2020, Wu et al. 2020). For example, Lee and Chen (2009) find that firm resources (such as innovativeness) affect the stock market reaction to new product introduction announcements. Similarly, Jacobs and Singhal (2014) argue that such firms are more dependent on a continuous stream of innovations, corresponding to higher motivation to innovate. They also demonstrate that the announcing firm's innovation intensity positively moderates the effect of product development announcements on the stock market. We assume that investors acknowledge the associated innovation capabilities, potentially realizing synergies and cost savings.

In contrast, investors could perceive the benefits innovative firms might gain through blockchain adoption as incremental, compared to less innovative firms, which represent more potential to innovate by leveraging new technologies like blockchain. Similarly, according to cue utilization theory (Bose and Leung 2019, Cox 1967), investors might perceive the announcement of a novel IT initiative by less innovative firms as a signaling cue, conveying a message that the firm is shifting towards a more innovation‐oriented trajectory. However, taken together, we argue that general firm innovation capabilities likely outweigh the signaling arguments for less innovative firms.

The positive stock market reaction to blockchain announcements is stronger when the announcing firm is more innovative.

Methodology

To test Hypothesis 1, we conduct an international event study, examining the stock market reaction to blockchain announcements. We then test the influence of several factors on the stock market reaction, corresponding to Hypotheses 2–7.

Data Collection

To assess the stock market reaction, we collected two main types of data, blockchain announcements and international stock market returns.

Blockchain Announcements

Following an approach similar to Borah and Tellis (2014), we identified announcements based on a predefined set of sample firms. Specifically, we built our sample on firms included in the Morgan Stanley Capital International (MSCI) World Index. Selecting the MSCI World Index holds three advantages. First, the MSCI World is the leading world market index capturing approximately 85% of the free float‐adjusted market capitalization in each included country (MSCI 2020). Second, since its constituents are mainly large and mid cap firms, all stocks are heavily traded. This is particularly relevant because low trading volumes weaken the assumption of an efficient market, which is foundational to our methodology (Subramani and Walden 2001). Third, the index includes firms from 23 developed markets. The international orientation of our study enables us to examine country‐related factors. Therefore, the MSCI World Index is commonly applied in financial studies (Asness et al. 2013, Atanasov et al. 2020). This led to a sample firm pool of the 1654 MSCI World constituents. To collect an initial set of blockchain announcements, we leveraged the LexisNexis database to search the leading news agencies PR Newswire, Business Wire, GlobeNewswire, and Newstex. We searched for announcements between January 2015 and December 2019. We combined each firm name with variations of blockchain, distributed ledger, DLT and variations of supply chain, logistics, production, operations, manufacturing, warehousing, inventory, purchasing, procurement, and transport. Our initial keyword search led to a total of 14,707 potential announcements. Similar to the procedure used by Hendricks et al. (2015), we ensured that the announced initiatives fit our study context, as set by our keywords. We only included announcements of adopting firms that use blockchain to improve the business processes related to the production of goods or delivery of services (Babich and Hilary 2020). Additionally, we screened all articles using the following exclusion criteria: The article did not announce a blockchain initiative. We excluded industry and analyst reports, trading forecasts, or market outlooks. The article was a duplicate. We eliminated duplicate articles from other sources that referred to the same blockchain initiative. The blockchain initiative does not involve an MSCI World Index‐listed firm. To not distort our sampling strategy, we did not consider firms that are involved in blockchain initiatives, but not a constituent of our MSCI World Index sampling frame. The implementation of blockchain was not the primary objective of the initiative. For example, we excluded announcements of general digitalization initiatives.

The screening phase left us with 207 announcements. To ensure that the stock market reaction can be attributed to the related announcement of a blockchain initiative, we further excluded 32 blockchain announcements with confounding events around the announcement date, such as earnings announcements, changes on the management board, or mergers and acquisitions (McWilliams and Siegel 1997, Schmidt et al. 2020). Since correct announcement dates are crucial to ensure the validity of an event study, we also double‐checked all event dates using publicly available information (Brown and Warner 1985, Kalaignanam et al. 2013). Our final sample consists of 175 announcements from 100 unique firms. Announced blockchain initiatives include blockchain applications for product traceability, object authentication, raw material trading, efficient contract and data management, and related areas. Appendix Table C1 provides exemplary announcement excerpts. Table 1 presents a sample summary, including the distribution across announcement years (Panel A), industries (Panel B), and countries (Panel C).

Sample Summary Statistics

Notes

Morgan Stanley Capital International (MSCI) % refers to the MSCI World Index distribution of firms across GICS industries and countries.

International Stock Market Returns

To compute daily stock market returns, we retrieved daily closing prices for all sample firms from Thomson Reuters. To facilitate the international setting of our study, we further collected daily closing prices of the main national market indices. We consider the leading stock market index of the firm's country (Hendricks et al. 2020). For example, we use the S&P 500 index for U.S. firms, the Nikkei 225 index for Japanese firms, and the DAX index for German firms. Appendix Table C2 shows all sample countries and the corresponding market index used in this study. Regional Fama‐French factors were retrieved from the Dartmouth College database (Bose and Leung 2019, Fama and French 1993).

Variables and Measures

To examine how the use case, project, and firm characteristics influence the stock market reaction to blockchain announcements, we consider a range of variables. Table 2 provides an overview.

Measurement Details for Hypothesized and Control Variables

Hypothesized Variables

To test Hypotheses 2–5, we coded the blockchain announcements along several dimensions. To assess whether tracing physical objects affects the stock market reaction, we carefully screened each announcement, coding as 1 when the blockchain infrastructure is used to store information about a physical object (e.g., food, drugs, or spare parts). Similarly, we classified the corresponding variable as 1 when the blockchain is used to share sensitive data. For example, firm‐specific financial information, customer data (e.g., identification number, payment information, name, or health data), pricing information, or contract data were considered sensitive. Non‐sensitive information, for instance, includes product condition data, such as origin, temperature, weight, or humidity. On the project level, we used the number of project partners, available from public sources, as the measure for the blockchain consortium size. Project partners include other adopting firms, IT service providers, academic organizations, financial institutions, or public authorities. The involvement of an external IT service provider was also coded as a binary indicator variable. External IT service providers were either established players (e.g., IBM or Accenture) or blockchain startups. In addition to the authors, two independent coders, not involved in the research project, assessed the characteristics of the blockchain announcements following our coding scheme, yielding sufficient inter‐rater reliability for all variables (Landis and Koch 1977). Cases of non‐congruent coding outcomes were discussed and resolved within the team of authors.

To test Hypotheses 6 and 7, we collected additional firm data from Thomson Reuters. We use asset turnover to measure firm productivity (Atkinson et al. 2001, Lanier Jr et al. 2010). The number of patents is a common indicator of firm innovativeness (Borah and Tellis 2014, Zhang et al. 2014). As the number of patent applications is generally correlated with firm size, we use the ratio of the number of patents and firm assets, to capture firm innovation intensity.

Control Variables

Consistent with prior event studies, we control for key firm financials which have been shown to influence stock market returns. We consider firm size, as larger companies are generally under more public scrutiny (Hendricks et al. 2020). Further, large firms are less likely to receive strong stock market reactions to individual events. In our case, one technology initiative might not affect the reaction of investors at large (Jacobs and Singhal 2014). We further control for firm growth, which captures pre‐announcement performance (Chatterjee et al. 2002). We also consider the market‐to‐book ratio and financial leverage as controls. The market‐to‐book ratio is a measure for stock overvaluation driving stock returns (Fama and French 1998, Gwebu et al. 2018). Financial leverage reflects the firm's capital structure and is indicative of risk (high leverage) and financial slack (low leverage) (Fama and French 1993, Hendricks et al. 2015). Since we also expect the market to respond more positively to blockchain announcements when public attention is fueled by high Bitcoin prices, we further include the Bitcoin price as a control variable (Cahill et al. 2020, Cheng et al. 2019). We also control for industry, regional, and time effects (Bose and Leung 2019, Modi et al. 2015). As the MSCI World Index is structured according to the Global Industry Classification Standard (GICS), we also use the GICS industry taxonomy, similar to prior studies (e.g., Bellamy et al. 2020). Table 2 presents measurement and operationalization details. Table 3 provides descriptive statistics for our explanatory variables.

Descriptive Statistics for Explanatory Variables

Notes

Variables are not logarithmized; N = 175.

Data Analysis

Our data analysis comprises two distinct steps. First, to test Hypothesis 1, we analyze the significance of the stock market reaction to blockchain announcements. Second, we estimate random effects regression models to examine the influencing factors according to Hypotheses 2–7.

Analysis of the Stock Market Reaction

In Hypothesis 1, we propose a positive stock market reaction to blockchain announcements. To test Hypothesis 1, we conduct an international event study (Bose and Leung 2019, Hendricks et al. 2020). The method presents a rigorous approach to analyze the isolated effect of discrete firm events (i.e., announcements) on stock market value (Brown and Warner 1985, MacKinlay 1997). It builds on the central assumption of an efficient market, in which stock prices (instantaneously) reflect all publicly available information (Sharpe 1964). Our data collection approach including heavily traded MSCI World stocks supports this assumption. We further assume that investors are capable of rationally assessing the announced initiatives. In this regard, the event study methodology has been validated as an adequate tool to examine the value of novel IT systems (e.g., Bose and Leung 2019, Boyd et al. 2019). We refer to Kothari and Warner (2006) and MacKinlay (1997) for more details on the event study method.

To facilitate the analysis of stock market data, we translated calendar days into trading days, where Day 0 denotes the day of the announcement, Day −1 the prior trading day, Day 1 the trading day following the event, and so forth. We first shifted announcements on non‐trading days (e.g., weekend days or public holidays) to the following trading day. Our results hold when we exclude the blockchain announcements on non‐trading days. Second, we also adjusted the announcement date to the next trading day when the time of the announcement was after the closing time of the respective stock exchange (e.g., 4:00 P.M. ET for the New York Stock Exchange) (Hendricks et al. 2015).

We compute the abnormal returns, given as the difference between actually observed firm returns and expected returns (MacKinlay 1997). To estimate expected returns, we use the Fama‐French four‐factor model (Carhart 1997, Fama and French 1993):

Similar to prior event studies, we present a five‐day event window, including two days before the event day, the event day, and the two subsequent trading days (Jacobs 2014, Kalaignanam et al. 2013). Averaging the abnormal returns over the sample of N announcements for day t results in the mean abnormal abnormal return

Analysis of Factors Influencing the Stock Market Reaction

To test Hypotheses 2–7, we estimate a set of random effects regression models (e.g., Schmidt et al. 2020). We thereby account for the unbalanced panel structure of our sample, as several firms (34 out of 100) announce multiple blockchain initiatives, denoted by j for every firm i. The Durbin–Wu–Hausman test suggests the use of a random, instead of a fixed, effects estimator (Wooldridge 2010). A random effects regression model also allows us to account for the potentially unobserved, firm‐individual heterogeneity.

Results

Stock Market Reaction to Blockchain Announcements

To examine Hypothesis 1, we test whether the abnormal stock returns in our event window are statistically different from zero. We use t‐tests, Wilcoxon signed rank tests, binomial sign tests, and additionally report Brown‐Warner, Corrado and generalized sign test results, as described in Appendix A.1. All event study tests are one‐tailed. Table 4 presents our event study results.

Event Study Results

Notes

Columns 1 and 2 of Table 4 indicate that there is no significant stock market reaction on the two trading days before the blockchain announcement. In Column 3, we see a significant positive mean abnormal stock return of 0.30% (t = 3.98, p < 0.001;

Factors Influencing the Stock Market Reaction

Table 5 presents the correlation matrix of our dependent and explanatory variables. We also assess the Variance Inflation Factors (VIFs). Correlation coefficients between covariates are smaller than 0.31 and VIFs are well below 2 for all variables, indicating that multicollinearity is not biasing our regression results (Kutner et al. 2005, Modi et al. 2015). To examine support for Hypotheses 2–7, we estimate random effects regression models using the abnormal stock market return on Day 0 as the dependent variable. Table 6 shows the resulting estimates. Column 1 presents a control model and Column 2 the main effects model including our hypothesized variables.

Correlation Matrix

Notes

Random Effects Regression Results

Notes

Providing support for Hypothesis 2, Column 2 indicates that blockchain applications intending to trace physical objects exhibit significantly lower abnormal stock returns (

Robustness Checks

To assess the sensitivity of our results to particular design choices, we conduct a series of robustness checks regarding sample selection, multiple firm announcements, technical blockchain specifications, influential data points, and alternative expected return models.

First, a firm's decision to launch or participate in a blockchain initiative is a strategic choice, and thus endogenous. Hence, our sample is determined by a non‐random self‐selection process of firms that decided to engage in blockchain, which might bias our results. To account for potential endogeneity issues, we use both a PSM approach (e.g., Boyd et al. 2019, Modi et al. 2015) and a Heckman two‐step model (e.g., Bose and Leung 2019, Hendricks et al. 2015). While PSM allows us to control for self‐selection based on observable firm characteristics, we implement the Heckman model to account for self‐selection based on unobservables that might influence both the decision to use blockchain and the stock market reaction (Boyd et al. 2019). Based on key financial controls, we build a PSM control group of firms, and use the risk‐adjusted returns of these control firms as benchmark returns for the event study. For the Heckman two‐step model (Heckman 1979), we first model the decision to announce a blockchain initiative, and then correct the second‐stage regression for a potential sample selection bias. Both the PSM procedure and the Heckman two‐step model confirm our main results, implying that our findings are likely not biased by self‐selection. Appendix A.2.1 provides more details on the procedure and the results.

Second, we assess the influence of some of our sample firms announcing more than one blockchain initiative, as investors might value subsequent announcements differently. We repeat our event study analysis and the second‐stage regression considering only the first blockchain announcement from each firm. Our main results remain structurally consistent. Appendix A.2.2 presents detailed results.

Third, investors might also take varying technical blockchain specifications into account. While all blockchain initiatives in our sample use blockchain as the base technology, the exact technical specification can vary in type (e.g., permissioned, public etc.) and underlying platform (e.g., Hyperledger, Ethereum, etc.). Additional analyses suggest that our results are not influenced by the blockchain specification (see Appendix A.2.3 for more details).

Fourth, as regression estimates are known to be sensitive to outliers, we identify and exclude the most influential data points (see Mitra and Singhal 2008). The detailed results in Appendix A.2.4 suggest that our results are robust to potential outliers.

Finally, our initial choice of the Fama‐French four‐factor model to estimate expected returns might affect the event study results. To assess the sensitivity of this design choice, we also test an international version of the Fama‐French three‐factor model and the traditional market model. Our results are robust to alternative expected return models, as presented in Appendix A.2.5.

Post‐hoc Analyses

Long‐term Stock Market Effects

The main objective of this study is to explore the financial value blockchain can create for firms in an operations and supply chain management context. To provide an additional perspective on blockchain's potential value, we also explore the long‐term effects associated with blockchain initiatives. This allows us to assess the sustained value blockchain may create for firms.

While short‐term event studies are dominant in the operations management and information systems literature, few long‐term event studies exist. Exemplary studies examine the shareholder value impact of identity theft countermeasure announcements (Bose and Leung 2019), product recalls (Liu et al. 2017), or supply chain disruptions (e.g., Hendricks and Singhal 2005). To conduct a long‐term event study, we follow prior studies and compute buy‐and‐hold abnormal returns (BHARs) based on one‐to‐one firm matches (Hendricks and Singhal 2005).

Our results indicate that there is a positive long‐term stock market effect of blockchain initiatives, as our sample firms significantly outperform their benchmark firm matches within a period of two years after the announcement. The difference in stock market performance between our sample and matched firms is significant and grows over time after the announcement. As depicted in Table 7, the mean (median) BHARs for the two‐year post‐event period grow up to 14.28% (16.86%) and are highly significant (t = 2.91, p < 0.01;

Long‐Term Event Study Results. Buy‐and‐Hold Abnormal Returns (BHARs)

Notes

The Competitive and Macro Environment

The information systems literature posits that the organizational value associated with IT initiatives partially depends on the firm's business environment (Melville et al. 2004). Research on the boundary conditions imposed by the focal firm's competitive environment (i.e., industry factors) and macro environment (i.e., country factors) is scarce. Thus, we explore how industry and country factors affect the value created by blockchain.

For our main analysis, we used dummy variables to account for industry and regional effects. In our post‐hoc analysis, we operationalize the firm's business environment more accurately. Appendix A.3.2 provides a detailed overview on the industry and country factors considered. To test the potential effects of environmental factors, we estimate random effects regression models, including all hypothesized and control variables, as well as the additional industry and country measures. In general, the structural results for our hypothesized effects are comparable to our main model (Table 6), suggesting further robustness of our main results. The industry and country factors indeed seem to play a pivotal role in the stock market valuation of blockchain announcements. On the industry level, we find that abnormal stock returns are significantly higher for announcing firms operating in industries with higher R&D intensity, emphasizing the importance of R&D proximity. On the country level, we find that stronger data‐related restrictions are negatively associated with the stock market reaction to blockchain announcements. This highlights that the regulatory dimension is crucial for the value of blockchain initiatives. Please refer to Appendix A.3.2 for full details.

Stock Market Reaction in Emerging Markets

Our main sample is based on constituents of the MSCI World Index. While the index covers firms from 23 developed countries, emerging markets are not included. Although it seems reasonable to assume that the constituent countries account for the large majority of blockchain initiatives, there are notable exceptions. For instance, several Chinese firms play an active role in the advancement of blockchain as technology providers and adopting firms (Kharpal 2019).

To complement our main analysis, we also explore the stock market reaction to blockchain initiatives in emerging markets. Extending the geographical scope of our original analysis, we sample firms from the MSCI Emerging Markets Index, which includes approximately 1400 mid and large cap firms from 27 emerging markets countries, such as China, Korea, and Taiwan. Applying the criteria consistent with our initial data collection approach (see section 3.1.1), we find 58 announcements from 37 different firms across 9 industries and 12 countries. The event study results indicate that there is no significant stock market reaction on the announcement day and the prior trading days, but, in contrast, a significantly positive stock market reaction on Day 1. Collectively, these results suggest that investors also positively value the announcements of blockchain initiatives in emerging markets, with a one‐day delay compared to our main findings. We refer to Appendix A.3.3 for more details on the methodology and the tabulated event study results.

Discussion, Implications, and Future Research

In this study, we examine the stock market reaction to 175 blockchain announcements across 11 industries and 15 different countries. We empirically demonstrate that investors positively react to announcements of blockchain initiatives in operations and supply chain management. We find a significant mean abnormal return of 0.30% on the announcement day, corresponding to an increase of more than $159 million in shareholder value for the median firm observation in our sample. In a post‐hoc test, we also find indications of positive long‐term stock market effects. We further identify a set of use case, project, and firm factors that influence the positive stock market reaction. Specifically, we find that firms using blockchain to trace physical objects or to share sensitive data experience a less positive stock market reaction. Likewise, the involvement of an external IT service provider and firm innovativeness are associated with a less positive stock market reaction. We find the stock market reaction to be significantly stronger for firms with higher productivity. Based on data exchange and diversity arguments, we further hypothesized that larger blockchain consortia are associated with higher stock market returns, which could not be supported by our analysis. One possible explanation might be that larger consortia involving more project partners are characterized by higher complexity, creating coordination costs and fostering related issues, such as delays and cost overruns (Ranganathan and Brown 2006). These uncertainties might cancel out the expected benefits of a larger consortium size.

Implications for Research

Our findings empirically substantiate the largely conceptual debate on the use of blockchain (e.g., Babich and Hilary 2020, Olsen and Tomlin 2020), and contribute to the growing discussion on emerging disruptive technologies in operations and supply chain management (e.g., Guha and Kumar 2018, Holmström et al. 2019). Although blockchain is still in an early stage, the value attribution from investors might be a first and reasonable indication to assess the value that blockchain may create (Bose and Leung 2019, Dehning et al. 2004).

Finding empirical evidence for multiple factors influencing the positive stock market reaction to blockchain announcements extends the existing literature. Specifically, demonstrating that the stock market reaction to blockchain announcements is less positive in instances where blockchain is used to trace physical objects, empirically emphasizes a prominently discussed challenge of several blockchain use cases, the garbage in, garbage out problem (Olsen and Tomlin 2020, Tucker and Catalini 2018). As the sharing of sensitive data is valued less positively, our findings challenge assumptions made on blockchain's inherent security level (Babich and Hilary 2020, Massimino et al. 2018, Tucker and Catalini 2018), and add to recent critical assessments of the technology's security.

We also complement the understanding of the general relationship between IT initiatives and financial firm performance (Bose and Leung 2019, Hendricks et al. 2007, Melville et al. 2004). In comparison to recent event studies examining IT initiatives, announcements of blockchain initiatives yield a similar mean abnormal return of 0.30%. For example, assessing announcements of identity theft countermeasures in e‐commerce, Bose and Leung (2019) find a positive stock market reaction of 0.28% on the announcement day. Another recent study by Boyd et al. (2019) shows that announcements of branded mobile App launches are associated with a positive mean abnormal return of 0.21%. For announcements of general IT development alliances, Han et al. (2012) find a mean abnormal return of 0.23% for the announcement day and the preceding day.

Prior conceptual work has also argued that both country and industry factors play a crucial role for IT business value (Delen et al. 2007, Melville et al. 2004). However, we are among the few event studies leveraging an international sample, which allows us to provide empirical evidence on how the firm's competitive and macro environment affect the stock market reaction to blockchain announcements. As we find the industry R&D intensity to accentuate the positive stock market reaction, we emphasize the role of R&D propensity for technological innovation creation. On a country level, existing research has already acknowledged the role of regulatory bodies for IT business value (Babich and Hilary 2020, Lacity 2018). This finding seems especially critical for the specific literature on blockchain, an inter‐organizational technology that spans firm boundaries across industries and countries.

Implications for Practice

Our empirical results allow us to derive a set of managerial implications. First and most important, the positive effect of blockchain initiatives on a firm's short‐ and long‐term stock market value emphasizes the general potential of blockchain for use cases in operations and supply chain management. We encourage managers to explore blockchain and to initiate first pilots to elicit the benefits of the technology for firm operations.

Second, our findings suggest that the identification of appropriate use cases for blockchain remains a key issue. While blockchain may not be the “silver bullet” for all business challenges in operations and supply chain management, the technology can unfold its potential for certain application characteristics. Our findings help managers understand the conditions under which the benefits of the adoption may be maximized. For instance, we recommend practitioners to first focus on less complex business processes for blockchain adoption, involving digital‐native assets. It seems beneficial to build first blockchain solutions around information that is already digitized, for example data from ERP systems. Blockchain use cases, such as supply chain traceability, where secure bridging of the physical and digital world is essential, are more complex and require additional technology (e.g., smart sensor systems) to ensure accurate and synchronous information. After the successful exploration of less complex use cases, we encourage both researchers and managers to focus on the development of secure and cost‐efficient solutions for applications involving physical object tracing, which currently experience a weaker positive stock market reaction.

Third, in contrast to our hypothesis, our empirical results suggest that blockchain initiatives including an external IT service provider are valued less positively by investors. One possible explanation might lie in the dependencies and information asymmetries created by the commonly central organization of many blockchain initiatives, despite the intended decentralized architecture. Given the novelty of the technology, special trust in the implementing party is needed. To handle the potential consequences of this black‐box effect, firms probably need to implement safeguarding mechanisms, creating additional costs (Babich and Hilary 2020). Investors might anticipate the costs and risks associated with the involvement of external IT service providers in the specific case of blockchain to outweigh the associated benefits. Hence, we advise managers to be particularly cautious in instances where the blockchain solution is marketed and governed by a central entity.

The decision on including an external IT service provider is likely dependent on related firm characteristics, such as firm innovativeness. Based on additional empirical analyses, depicted in Appendix A.3, we recommend highly innovative firms with sufficient IT capabilities to develop blockchain solutions in‐house, avoiding the risks and dependencies associated with external service providers. Similarly, firms that are less innovative may also question the initial blockchain project governance structure. However, as firm innovativeness is likely associated with IT capabilities, less innovative firms might not be able to develop blockchain solutions on their own. Firms lacking the necessary capabilities could benefit from engaging an external IT service provider. However, we alternatively recommend joining non‐centrally governed consortia of peers. This would enable blockchain participation without the need for an entire self‐development, and allow firms to build up additional IT capabilities over time.

Fourth, our post‐hoc analysis of the industry and country factors affecting the valuation of blockchain initiatives may support decision‐makers in better understanding the specific competitive and macro conditions under which blockchain unfolds its potential. The positive effect of the industry's R&D intensity underscores the importance of innovation proximity, emphasizing our suggestion to join forces with peers in blockchain consortia, ideally in innovative industry environments. Analogously, our findings suggest that managers should consider the infrastructural IT conditions. As we show that the data restrictiveness level weakens the positive stock market reaction, we recommend managers to engage with regulatory bodies early on in the development phase, to optimize the value firms can generate with blockchain, ensuring that the blockchain solution is fully compliant with the existing regulatory environment.

Limitations and Future Research

As with any empirical study, this research is not without limitations. We discuss these limitations and point out four promising pathways for future research. First, this study is exclusively focusing on the firm's shareholder value as a key dimension of financial firm performance. While we strongly believe that the stock market valuation of firms' announcements of blockchain initiatives is a first and reasonable step towards measuring the rather elusive value of blockchain at the current stage, we cannot make any predictions regarding operating performance. After the completion of more operational blockchain projects and a more mature understanding of the technology, future studies should investigate operating performance implications to extend the discussion on the value of blockchain. In this context, qualitative work such as case studies, exploring the performance implications and moderation factors of specific blockchain initiatives, might also add new insights.

Second, while we intentionally focus on blockchain initiatives in an operations and supply chain management context, it is clear that blockchain may also be promising for other business fields and application domains. For example, blockchain is increasingly gaining traction in the financial services industry, where cryptocurrencies are expected to boost efficiency and reduce bureaucracy. Initial coin offerings (ICOs) are becoming promising investment vehicles, particularly for new venture funding (Wang et al. 2021). Future research could extend our functional scope, for instance by providing insights into blockchain applications at the interface of finance and operations management (Chod and Lyandres 2021).

Third, in a post‐hoc test, we provide early indications of a positive long‐term effect of blockchain initiatives. Since there is valid criticism regarding the reliability of long‐term event studies, it is important to interpret the long‐term results with caution. We encourage future studies to explore alternative approaches, such as using benchmarked portfolios (Bose and Leung 2019). Scholars could also examine long‐term effects on alternative measures of firm performance to gain more nuanced insights. Finally, we show that the positive stock market reaction to blockchain announcements is also existing in emerging markets. We observe a delayed stock market reaction pattern, which should be evaluated in future studies. As blockchain is often discussed as a leapfrogging opportunity for developing countries (Gupta and Knight 2017), we also encourage future interdisciplinary research to examine the success factors of blockchain for developing and emerging markets.