Abstract

With over half a trillion dollars in trade credit flowing between firms in the United States, it is critically important for managers to understand how the trade credit that their firm receives and provides affect its value. Trade credit is a strategic investment in supply chain relationships that allows the recipient to make payment later rather than at the time of the sale. A firm provides trade credit to its downstream business customers and also receives trade credit from its upstream suppliers. Although research has shown that

Keywords

Introduction

Trade credit is economically significant. By some estimates, provided trade credit and received trade credit respectively account for 20% of the assets and 44% of the liabilities of US public firms (Lieberman 2017). Indeed, US nonfinancial firms now have about $500 billion in each of provided trade credit and received trade credit (Federal Reserve Board 2021). Unsurprisingly then, trade credit has received renewed attention from empirical researchers in operations management (Cai et al. 2014, Wu et al. 2019; Wuttke et al. 2019), marketing (Frennea et al. 2019), and finance (Hill et al. 2012).

The amounts of trade credit a firm provides to its customers and receives from its suppliers are key B2B marketing and supply chain decisions. Firms report these amounts in their reports to investors presumably because they believe that their received trade credit and provided trade credit influence their shareholder value. In this article, we develop a conceptual framework for how a firm's received trade credit and provided trade credit affect a firm's value and empirically test their direct and indirect effects.

Recent research in marketing (Frennea et al. 2019) and finance (Hill et al. 2012) has shown that provided trade credit builds a firm's shareholder value. Such research draws from the interorganizational relationship theory that a firm's investments in its customer relationships improve customers' perceptions (e.g., commitment and trust) of the firm (Dwyer et al. 1987, Hibbard et al. 2001, Rousseau et al. 1998), which influence the firm's performance (Palmatier et al. 2007a, 2007b, 2009, Tuli et al. 2010, Wathne et al. 2018). However, extant research lacks theoretical arguments and empirical evidence on the effect of

A firm seeks trade credit from its suppliers for the same reason that customers seek trade credit from the firm—it allows the firm to delay payments that it owes its suppliers. Such delayed payments decrease the firm's costs and increase the firm's profit. Because profit increases firm value, received trade credit

However, received trade credit has a negative

While the primary contribution of this article is providing insight into the value of received trade credit, the secondary contribution is providing additional insight into the value of provided trade credit. We replicate extant research's finding that provided trade credit has a positive direct effect on the firm's value. We further document that provided trade credit

By showing how received trade credit and provided trade credit differentially affect firm value, our research extends the multidisciplinary theory on interorganizational relationships. We document that received trade credit builds firm value by increasing the firm's profit but destroys it by increasing the firm's dependence on its suppliers. In contrast, provided trade credit builds firm value by increasing customers' dependence on the firm but destroys it by decreasing the firm's profit. That is, both received trade credit and provided trade credit build firm value, albeit through different theoretical mechanisms. These findings also contribute to theoretical (Devalkar and Krishnan 2019, Gupta and Wang 2009, Jing et al. 2012, Kouvelis and Zhao 2012, Wu et al. 2019) and empirical (Cai et al. 2014, Wu et al. 2019) operations management research, which shows that trade credit can help manage the supply chain. The research also relates to the literature on how marketing builds firm value (e.g., Edeling et al. 2020, Srinivasan and Hanssens 2009) and the emerging evidence on how operations builds firm value (e.g., Hendricks and Singhal 2003, Jacobs and Singhal 2020, Modi and Mishra 2011).

We organize the rest of the article as follows. We begin by summarizing the relevant literature on interorganizational relationship theory, our theoretical lens. Then, we develop our conceptual arguments and hypotheses for how received trade credit and provided trade credit differentially affect firm value. Next, we discuss our method, define the measure for each of our variables, specify our models, explain the identification strategy, and describe our data. We then present and discuss the results of our analyses, quantify the effect sizes, and assess the robustness of our effects. Finally, we review the implications and limitations of our research and suggest directions for future research.

Effects of Interorganizational Relationship Investments on Firm Performance

Interorganizational relationship theory conceptualizes relationship investment as a firm's investment in its relationships with customers (Palmatier et al. 2006a, 2006b). Relationship investment increases the favorability of customers' perceptions of the provider firm and the relationship. These include customers' commitment to the relationship (Frennea et al. 2019, Palmatier et al. 2006a, 2006b), trust in the firm's reliability and integrity (Frennea et al. 2019, Palmatier et al. 2006a, 2006b), assessed strength and closeness (i.e., quality) of the relationship (Crosby et al. 1990), satisfaction with the relationship (Bowman and Narayandas 2004), gratitude toward the firm (Palmatier et al. 2009), perceived efficiency in the exchange (Palmatier et al. 2008), and favorable perceptions of the firm's timely responses to and effective resolution of customer issues (Bowman and Narayandas 2004). Favorable customer perceptions, in turn, strengthen customer behaviors such as the expectation of continuity (Palmatier et al. 2006a, 2006b), loyalty (Bowman and Narayandas 2004, De Wulf et al. 2001), and word of mouth (Palmatier et al. 2006a, 2006b). Customers' positive behaviors thus enhance the firm's performance (Palmatier et al. 2006a, 2006b).

Table 1 summarizes the research on the effects of interorganizational relationship investment on a firm's performance. Research has found unequivocally that relationship investment increases the firm's share of customers' wallet (Bowman and Narayandas 2004, De Wulf et al. 2001, Palmatier et al. 2008), increases sales (Bowman and Narayandas 2004, Palmatier et al. 2007a, 2007b, 2009, Tuli et al. 2010), and decreases costs (Kalwani and Narayandas 1995, Wathne et al. 2018). The evidence regarding the effects of relationship investment on the firm's profit, however, is mixed. Whereas Palmatier et al. (2006a, 2006b) find that relationship investment helps profit, Bowman and Narayandas (2004) find that it hurts profit. Recently, research has shown that relationship investment increases the firm's value (Frennea et al. 2019, Hill et al. 2012).

Research on the Effects of Interorganizational Relationship Investment on a Firm's Performance

We extend interorganizational relationship theory in two ways. First, whereas extant research has focused solely on the effect of the relationship investment provided to downstream customers, we expand the lens to also assess the effect of the relationship investment

Trade Credit

Trade credit is a type of relationship investment (Frennea et al. 2019, Hill et al. 2012). It allows the recipient customers to receive products (goods, services, and ideas) and pay for them later rather than at the time of the sale. For example, a firm may provide “net 30” payment terms, which indicates that the firm is providing the customer with trade credit that allows the customer to take up to 30 days to make payment.

Table 2 presents examples of trade credit terms that are stated in firms' payment policies. A firm generally has standard payment terms, which are influenced by its industry's norm (e.g., PYMNTS 2020, Vetter 2020), as well as custom payment terms for specific customers. Because discrimination through pricing is often not permissible (e.g., due to concerns of violating the Robinson–Patman Act), customizing trade credit terms allows the firm to discriminate between its customers (e.g., Giannetti et al. 2021).

Examples of Payment Terms: Standardized and Customized

To assess the extent to which trade credit varies across and within industries, in Figure A1 of the Online Appendix we present box plots of provided trade credit by industry. We note the substantial variation in the median provided trade credit (denoted by the bold vertical line inside the boxes) across industries, which suggests that trade credit norms vary across industries. We also note a large interquartile range of provided trade credit (denoted by the size of the box) in most industries, which suggests that there is substantial variation in provided trade credit across firms in most industries.

Effects of Received Trade Credit and Provided Trade Credit on Firm Value

A firm is generally both a receiver and provider of trade credit. A firm receives trade credit from its upstream suppliers, which allows it to pay the suppliers later. It also provides trade credit to its downstream customers, which allows the customers to pay the firm later.

Recent research has theorized that trade credit builds mutual commitment and trust between a receiver and a provider, forming closer and stronger relationships between them (Frennea et al. 2019). In terms of commitment, which has been defined as “an implicit or explicit pledge of relational continuity between exchange partners” (Dwyer et al. 1987, p. 19), the provider commits to allowing the receiver to take additional time to make payments and the receiver commits to making the payments under the agreed terms (Frennea et al. 2019, Petersen and Rajan 1997). Reciprocally, the receiver commits to disclosing its sensitive financial information to the provider, and the provider commits to safeguarding the information.

In terms of trust, the receiver gains trust in the provider by receiving time to inspect the quality of the provider's offerings before paying for them (Babich and Tang 2012, Mian and Smith 1992, Ng et al. 1999, Rui and Lai 2015, Smith 1987). Reciprocally, the provider gains trust in the receiver by regularly monitoring the receiver's creditworthiness, default risk, and timeliness of payments (Lee and Stowe 1993, Levy and Grant 1980, Long et al. 1993).

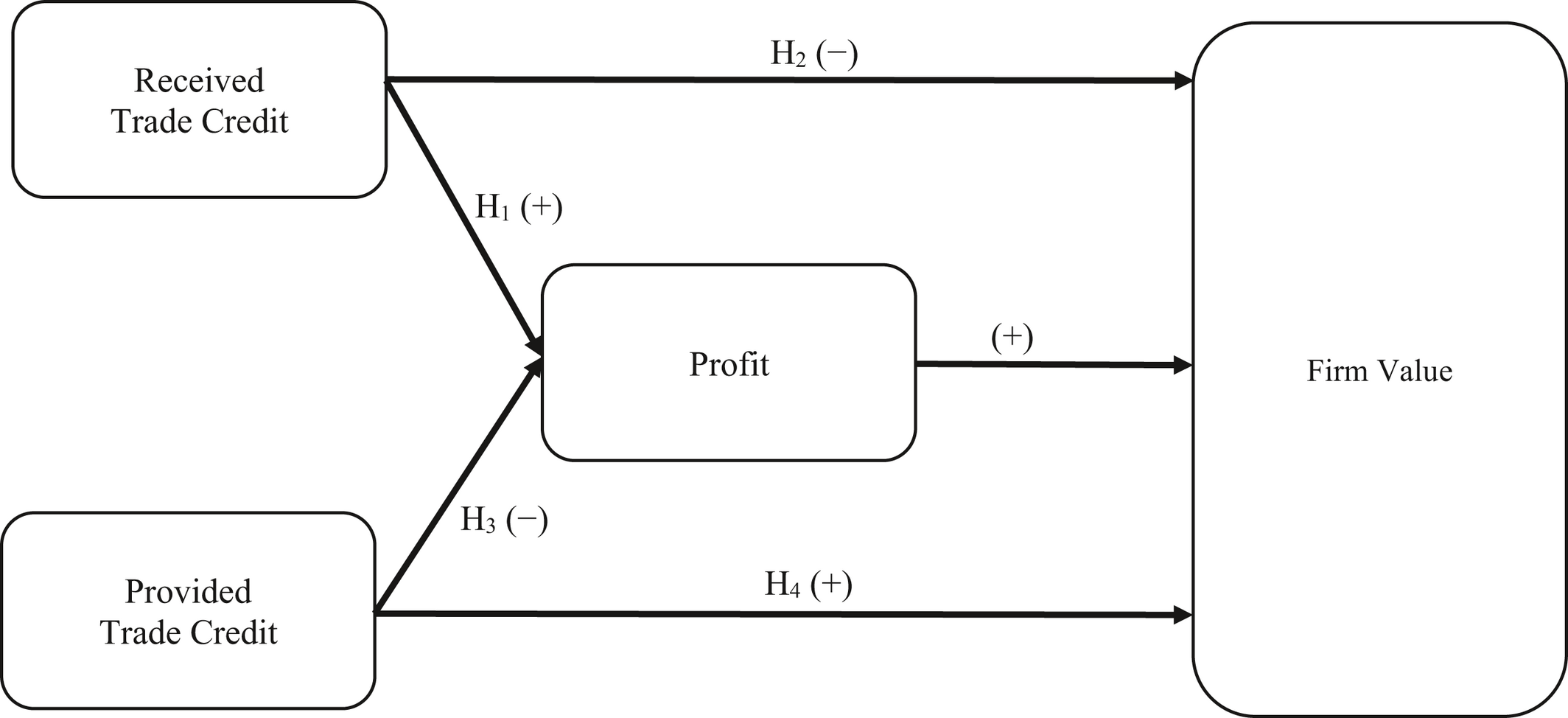

In the following subsections, we develop conceptual arguments for how the trade credit that a firm receives from its suppliers indirectly and directly affects the firm's value. Then, we develop arguments for how the trade credit that a firm provides to its customers indirectly affects the firm's value and review arguments from extant research on how it directly affects the firm's value. Figure 1 depicts our conceptual framework.

Conceptual Framework

The Effect of Received Trade Credit on Profit (Indirect Effect)

We argue that the trade credit received from suppliers increases a firm's profit by lowering its financing and opportunity costs. If a firm did not receive trade credit, it would need to make payments immediately, which would reduce the amount of cash it has available to invest in profitable opportunities. The more trade credit a firm receives, the longer the firm can delay its payments to suppliers, and the more cash it has available to invest in profitable opportunities (Devalkar and Krishnan 2019, Levy and Grant 1980).

The cash flow benefits of received trade credit decrease a firm's financing and opportunity costs. The higher level of available cash decreases the firm's need to seek other, more costly financing for profitable opportunities such as borrowing cash from a bank (Monroe and Bitta 1978, Murfin and Njoroge 2015, Nadiri 1969). The higher cash level also decreases the firm's need to incur the opportunity costs of redirecting funding from other profitable opportunities. Thus, we hypothesize that the higher the firm's received trade credit, the greater its profit. Formally:

A firm's received trade credit increases its profit.

Because an increase in a firm's profit increases its value, received trade credit has a positive indirect effect on the firm's value. In the following subsection, we develop conceptual arguments for the direct effect of received trade credit on firm value. That is, we reason that after controlling for the effect on the firm's profit, received trade credit has an additional effect on the firm's value.

The Effect of Received Trade Credit on Firm Value (Direct Effect)

In addition to affecting a firm's profit, trade credit also directly affects a firm's value by building relationship equity between the provider and the receiver. We argue that although the commitment and trust built by trade credit are mutual, they affect the relationship equity for the provider and the receiver in opposite ways. Whereas the strengthened relationship enhances equity for the provider (Frennea et al. 2019), it reduces equity for the receiver. This occurs because received trade credit increases a firm's

First, as a firm's received trade credit increases, the number of alternative suppliers that are willing and able to offer the firm more favorable payment terms decreases. Thus, if the firm chooses to switch suppliers, it will either receive less favorable payment terms or constrain its choices to a smaller set of alternative suppliers, both of which increase the firm's switching costs. Therefore, an increase in received trade credit increases the firm's cost of switching suppliers, which increases the firm's dependence on its current suppliers (Jain 2001, Suh and Kim 2018). Conversely, a decrease in the firm's received trade credit increases the number of suppliers that are willing and able to extend credit on more favorable terms, which lowers the firm's switching costs and dependence on its current suppliers.

Second, as a firm's received trade credit increases, its suppliers forego profits so that the firm can retain more cash to invest in profitable opportunities. Because the suppliers' foregone profits signal their commitment to their relationships with the focal firm, an increase in received trade credit raises the firm's status as the beneficiary of such commitments. Relationship marketing theory suggests that an increase in benefits from suppliers' commitments increases a firm's obligation to reciprocate (Bagozzi 1995, Johnson and Sohi 2001). We reason that such an obligation to reciprocate increases the firm's dependence on its suppliers. Conversely, a decrease in the firm's received trade credit lowers the extent to which the firm benefits from its suppliers' commitments, which lowers the firm's obligation to reciprocate and lower its dependence on its suppliers.

Because an increase in dependence hampers a firm's future prospects (Hibbard et al. 2001, Scheer et al. 2015), we hypothesize that the dependence built through an increase in received trade credit decreases the firm's value. That is, the higher a firm's received trade credit, the lower its shareholder value.

A firm's received trade credit decreases its shareholder value.

The Effect of Provided Trade Credit on Firm Value

Extant research argues that the trade credit a firm provides to its customers increases the firm's value by building mutual commitment and trust between the firm and its customers (Frennea et al. 2019, Hill et al. 2012). We argue that, in addition to this positive direct effect on firm value, provided trade credit also indirectly harms firm value by decreasing the firm's profit. Next, we develop our conceptual arguments for the negative effect of provided trade credit on profit and then discuss how the arguments in extant research for the positive direct effects on firm value fit into our broader conceptual framework.

The Effect of Provided Trade Credit on Profit (Indirect Effect)

If a firm did not provide trade credit, it would receive payments immediately, which would increase the amount of cash it has available to invest in profitable opportunities. When a firm provides trade credit to its business customers, it increases the customers' available cash by reducing its own cash. That is, the more trade credit a firm provides, the longer it takes the firm to receive payments from its customers, and the less cash it has available to invest in its profitable opportunities (Levy and Grant 1980). Although the provided trade credit lowers the customers' financing and opportunity costs, it increases the firm's financing and opportunity costs, which decreases the firm's profit.

The increased opportunity costs arise because the firm may need to cut back on investments in its profitable opportunities to fund the trade credit it provides to its customers. For example, research shows that smaller firms cut back on their capital expenditures and operating expenses when they increase their provided trade credit (Murfin and Njoroge 2015). For firms that have alternative sources of financing, they can reduce the opportunity costs of providing trade credit by seeking cash from outside sources (e.g., banks) to invest in profitable opportunities. This, however, increases their financing costs. Therefore, because provided trade credit increases financing and opportunity costs, we hypothesize that the higher a firm's provided trade credit, the lower its profit.

A firm's provided trade credit decreases its profit.

Because a decrease in a firm's profit decreases its value, provided trade credit has a negative indirect effect on the firm's value. In contrast, as discussed in the following subsection, provided trade credit has a positive direct effect on firm value.

The Effect of Provided Trade Credit on Firm Value (Direct Effect)

We previously reasoned that received trade credit increases the firm's dependence on its suppliers. Mirroring this logic would suggest that provided trade credit increases the customers' dependence on the firm. Whereas the customers' dependence is value‐diminishing for them, it is value‐enhancing for the firm. Indeed, interorganizational relationship theory argues that closer and stronger customer ties that arise from providing trade credit increase customers' switching costs, which enhances the value of the customer relationships for the firm (Frennea et al. 2019). The value of these customer relationships, in turn, increases the firm's discounted sum of expected future cash flows and, consequently, the firm's value (Srivastava et al. 1998).

In addition, like other relationship investments, trade credit is characterized by frequent interactions and high‐quality information sharing between the firm and its customers (Palmatier et al. 2006a, 2006b). Frequent interactions and superior communication enable the firm to lower its costs and reduce sales uncertainty (Dyer and Singh 1998, Mohr et al. 1996, Wuyts and Geyskens 2005), which also increase the firm's value. Therefore, we expect to replicate findings from extant research showing that the higher a firm's provided trade credit, the greater its shareholder value (Frennea et al. 2019, Hill et al. 2012).

A firm's provided trade credit increases its shareholder value.

Method

To test our hypotheses, we use a stock return response model, which is the predominant method used in recent research on marketing's effect on firm value (for a recent review, see Edeling et al. 2020). The main idea behind this method is that if a marketing investment affects firm value, an unanticipated change in the investment affects the firm's stock return. A key benefit of using stock return (i.e., the percentage change in firm value) is that it allows researchers to account for differences in firm size without the bias that is introduced by scaling used by measures such as market‐to‐book or Tobin's

In this section, we begin by defining the measures we use for each of our variables. Next, we specify our models and the approach used to estimate the unanticipated changes in variables. We follow up by discussing our identification strategy, reviewing our estimation approach, and describing the data set assembled to estimate the models.

Variables

Following extant literature, we estimate this model for each firm using its daily stock return during the 252 trading days in year

Predictor Variables

Models

We use a stock return model, which includes the unanticipated changes in received trade credit (

First, we add year indicator variables

The firm‐specific random error term controls for firm characteristics that do not change over time (e.g., firm strategy). However, unobserved time‐varying firm characteristics may also affect the stock return and correlate with the unanticipated changes in received or provided trade credit. For example, collections inefficiencies (e.g., sending late or error‐filled invoices to customers) may cause a delay in customer payments that increases the firm's provided trade credit (Barron 2010, 2011, Horngren et al. 1999, Shappell 2012). To the extent that collections inefficiencies change over time and influence stock return, their omission from our specification could lead to issues of endogeneity. Therefore, we specify a model with instrumental variables to account for this possibility.

Following extant research on marketing's effect on firm value (e.g., McAlister et al. 2016, Sridhar et al. 2016), we use peer behavior as instrument. Specifically, we use as instruments (i) the unanticipated change in the median value of received trade credit and (ii) the unanticipated change in the median value of provided trade credit for other firms that operate in the focal firm's industry. For the instruments to be valid, they must be relevant (i.e., correlate with

We use the same identification strategy and estimation approach for the profit model as we do for the stock return model. That is, we add year indicator variables to the model, account for unobserved firm effects, use the same instruments for received and provided trade credit, and use a 2SLSFE approach. The coefficient estimates for the instruments are significant in the associated first‐stage regressions, providing support for their relevance (

Data

To test our hypotheses, we create a data set that combines financial statement data from three sources: (i) Standard & Poor's Capital IQ Compustat database, (ii) stock return data from the Center for Research in Security Prices at the University of Chicago's Booth School of Business, and (iii) Fama–French financial model returns from Kenneth R. French's Data Library. Following extant research on firm value (Frennea et al. 2019, Modi and Mishra 2011, Rego et al. 2009), we exclude financial firms, utilities, foreign governments, international affairs, and nonoperating establishments.

Our data set spans from 1986 to 2017. Consistent with extant research on the stock market (e.g., Fama and French 1993), we assume that the relationship between stock return and market‐wide risk factors is not stationary across such a long span. Therefore, we estimate abnormal stock return as a function of risk factors that vary over time in Equation (1). Research shows that the value of trade credit was lower in the 1970s and has been relatively stable since then (Hill et al. 2012). Because our data set starts after the 1970s, we follow extant research and assume that the effect of trade credit on firm value is relatively stable across this period (Frennea et al. 2019, Hill et al. 2012).

Following extant research on the value of trade credit (e.g., Hill et al. 2012), we also Winsorize all continuous variables to reduce the influence of outliers. We set values higher (lower) than the 99th (1st) percentile of each variable to the 99th (1st) percentile value. 5 The final data set has 25,274 firm‐year observations for 2804 firms. Table 4 lists the industries represented in the sample.

Industries Represented in the Sample

Note

Industry classification is based on Standard Industrial Classification divisions.

To diagnose multicollinearity, we compute variance inflation factors, condition indices, and correlations. The variance inflation factors are below the “rule of thumb” of 10 (Marquardt 1970), and the condition indices are below the “rule of thumb” of 30 (Belsley et al. 1980), suggesting that multicollinearity is likely not a problem. Table 5 presents the descriptive statistics and pairwise correlation coefficients for the variables.

Descriptive Statistics and Correlation Coefficients

Note

Correlations smaller than |0.01| are not significant (

Results

We proposed two paths through which received and provided trade credit affect firm value. There is (i) a “direct effect” and (ii) an “indirect effect” through profit. We first present the direct effects and then the indirect effects.

Direct Effects

Column (I) of Table 6 presents the estimation results for the stock return model, which tests our hypotheses on the direct effects of received and provided trade credit on firm value. The coefficient estimate for received trade credit is negative and significant (

Direct and Indirect Effects of Received and Provided Trade Credit on Firm Value

Note

Cluster‐robust standard errors are included in parentheses.

The coefficient estimate for provided trade credit is positive and significant (

Indirect Effects

Column (II) of Table 6 shows the coefficient estimates for the profit model, which tests our hypotheses on the indirect effects of received and provided trade credit on firm value. The coefficient estimate for received trade credit is positive and significant (

The coefficient estimate for provided trade credit is negative and significant (

Effect Sizes

To quantify the indirect and direct effects of received and provided trade credit on firm value, we compute the change in predicted firm value associated with a 1 SD increase in the unanticipated change in received and provided trade credit. To calculate the direct effects, we use the coefficient estimates from column (I) of Table 6. The results, presented in Table 7, indicate that a 1 SD unanticipated increase in received trade credit directly decreases the stock return by 2.49%, consistent with H2. In contrast, a 1 SD unanticipated increase in provided trade credit directly increases the stock return by 3.24%, which is consistent with H4.

Size of the Direct and Indirect Effects of a 1 SD Unanticipated Increase in Received and Provided Trade Credit

To calculate the indirect effects, we use the coefficient estimates from columns (I) and (II) of Table 6. We first calculate the effects of received and provided trade credit on predicted profit and then calculate how this impact on profit indirectly affects stock return. The results (Table 7) indicate that a 1 SD unanticipated increase in received trade credit leads to an unanticipated increase in profit by 0.10, which increases the stock return by 3.53%, consistent with H1. In contrast, a 1 SD unanticipated increase in provided trade credit causes an unanticipated decline in profit by 0.02, which decreases the stock return by 0.66%, consistent with H3.

Finally, we calculate the total effects of received and provided trade credit on firm value by summing their direct and indirect effects. The results indicate that a 1 SD unanticipated increase in received trade credit has a total effect of increasing stock return by 1.04%, equivalent to an average value of $118.28 million for the firms in our sample. The results also indicate that a 1 SD unanticipated increase in provided trade credit has a total effect of increasing stock return by 2.58%, equivalent to an average value of $295.77 million for the firms in our sample.

We note that the total effects are positive for both received trade credit and provided trade credit, suggesting that trade credit creates value for both the providing party and the receiving party and thus coordinates a supply chain (Long et al. 1993, Ng et al. 1999, Petersen and Rajan 1997). However, the means of appropriating value differ between the receiver and the provider. Specifically, while the receiver extracts the value through profit, the provider appropriates it by increased dependence of its customers, which increases its expected future cash flows. In addition, both parties incur costs—the receiver by becoming dependent on the suppliers and the provider by reducing its profit.

Additional Analyses

We conduct additional analyses to rule out alternative explanations. We also perform robustness tests to confirm the causal effects of received trade credit and provided trade credit on firm value. Table 8 summarizes the additional analyses we conducted and lists the alternative explanations we considered, the rationales for them, and our findings. Table A2 in the Online Appendix presents the measures for the additional variables included in these analyses.

Summary of Additional Analyses

Additional Analyses

Note

Cluster‐robust standard errors are included in parentheses. RTC = received trade credit, PTC = provided trade credit.

As an additional analysis, we adopt the identifying assumption used in the extant literature and re‐estimate our models without instrumental variables. The estimates (columns VII and VIII of Table 9) continue to support our hypotheses. The smaller magnitudes for the coefficient estimates suggest that received trade credit correlates with unobserved value‐enhancing factors (e.g., customers with positive reputations more likely receive favorable payment terms) and that provided trade credit correlates with unobserved value‐reducing factors (e.g., inefficient collections processes).

Additional Analyses

Note

Cluster‐robust standard errors are included in parentheses. RTC = received trade credit, PTC = provided trade credit.

In sum, we find that the empirical evidence is robust to alternative explanations, measures, and specifications.

Discussion

With trade credit in the United States now over $500 billion (Board of Governors of the Federal Reserve System 2020), research on how trade credit—both provided and received—creates firm value is important for businesses and the economy as a whole. While the amount of time a supplier provides to its business customers to make payments has long been recognized as a key marketing (e.g., Bartels 1964, Cross 1949) and supply chain (e.g., Wuttke et al. 2019) decision, our article is the first to theorize and document how received trade credit affects a firm's value. Our research provides several implications for the theory and practice of buyer–supplier relationships and those of trade credit.

Theoretical Implications

Our research has theoretical implications for two streams of research. First, it adds to the theory on interorganizational relationships (Chakravarty et al. 2014, Dahlquist and Griffith 2014, Kumar et al. 2011, Palmatier et al. 2007a, 2007b, Villena and Craighead 2017). Extant research on interorganizational relationships has theorized that the relationship investment that a firm receives is valuable to it (Bowman and Narayandas 2004, Palmatier et al. 2007a, 2007b). Our research builds on this theory by providing a more nuanced understanding of the value of received relationship investment. In the context of trade credit, we show that received relationship investment is a double‐edged sword. On the one hand, it improves the receiver's profit, which creates value for the receiver. On the other hand, it increases the receiver's dependence on the provider, which diminishes this value.

Second, our findings add to the theory on the shareholder value of trade credit (Frennea et al. 2019, Hill et al. 2012). Extant research has theorized that the trade credit a firm provides has a positive direct effect on its shareholder value. Our findings extend this research by theorizing that provided trade credit also has an indirect effect on a firm's shareholder value. Importantly, we show that the direct and indirect effects of provided trade credit have opposing influences on a firm's shareholder value. Whereas the direct effect is positive, the indirect effect is negative.

Managerial Implications

Our findings have implications for both managers that negotiate the amount of trade credit their firm receives from its suppliers as well as managers that negotiate the amount of trade credit their firm provides to its customers. For managers responsible for negotiating trade credit received from suppliers, our results indicate that considering the effects of received trade credit on both their firm's profit and its dependence on suppliers will improve their assessments of the value of received trade credit. We find that a 1 SD increase in received trade credit increases firm value by 3.53% (by increasing profit) whereas it decreases firm value by 2.49% (by increasing dependence). The total effect of increasing firm value by 1.04% (3.53%–2.49%) represents an average of $118.28 million for the firms in our data set. Importantly, if managers myopically consider only the effects of received trade credit on their firm's profit, they will overestimate the value that it creates for their firm.

For managers responsible for negotiating trade credit provided to customers, recent research has shown that provided trade credit has a positive direct effect on firm value (Frennea et al. 2019). Our results indicate, however, that managers run the risk of overestimating the value of provided trade credit if they consider solely its positive direct effect on firm value and ignore its negative indirect effect (though profit) on firm value. We find that a 1 SD increase in provided trade credit has a positive direct effect of increasing firm value by 3.24% whereas it has a negative indirect effect of decreasing firm value by −0.66% (through decreasing profit). The total effect of increasing firm value by 2.58% (3.24%–0.66%) represents an average of $295.77 million for the firms in our data set.

Limitations and Future Research

Ours is the first study on how received trade credit affects firm value. Next, we identify five limitations of our research, each of which merits further research. First, we test our conceptual framework using firms that are publicly traded in the United States. Future research could study the link between received trade credit and firm value for private firms or firms outside the United States. In particular, results may differ in countries with mandates that restrict the amount of trade credit a firm can provide to its customers (Barrot 2016, Breza and Liberman 2017).

Second, we examine the effects of received vs. provided trade credit on shareholder value. Future research could study how trade credit affects other firm performance measures, such as stock return risk. Recent research has also shown that 16% of the debt owed by bankrupt firms is from received trade credit (Jindal 2020), arguing that managers can adjust provided trade credit to help ease customers' financial distress (Jindal and McAlister 2015). Trade credit may thus be relevant to debt holders. Future research could investigate how received vs. provided trade credit affects a firm's credit ratings (Bendig et al. 2017) and bankruptcy risk (Jindal and McAlister 2015).

Third, we consider a firm's relational investment in the form of trade credit. Future research could consider how other types of relationship investments affect a firm's value. For example, future research could compare how social (e.g., meals and entertainment) vs. structural (e.g., inventory control and dedicated personnel) vs. financial relationship investments affect firm value (Palmatier et al. 2006a, 2006b).

Fourth, if more detailed data become available on trade credit terms, future research could examine whether the specific terms have differential effects on firm value (Ng et al. 1999). For example, research might consider whether two‐part (e.g., 5/7 net 30) vs. net (e.g., net 30) payment terms differentially affect firm value for the provider or receiver. Fifth, our research focuses on an important outcome (firm value) of trade credit. Future research could consider whether dependence or other characteristics of interfirm relationships extend the evidence on accounting and financial determinants of trade credit (Iglesias et al. 2007; Long et al. 1993; Petersen and Rajan 1994).

Footnotes

Acknowledgments

The authors thank Elham Ghazimatin, Girish Mallapragada, Neil A. Morgan, Kenneth H. Wathne, and participants at the 2020 AMA Winter Academic Conference for feedback on earlier versions of the manuscript.

Some early articles have used Tobin's ![]() ).

).

We consider alternative models in our robustness analyses.

This measure is sometimes multiplied by 365 and referred to as DPO (days payables outstanding).

Like DPO, this measure is sometimes multiplied by 365 and referred to as DSO (days sales outstanding).

We also estimated our models using data that were not Winsorized and found that the coefficient estimates associated with trade credit were consistent in terms of the direction of their effects.