Abstract

Accounting rules have improved the transparency of corporate operations. Financial statements provide shareholders with reliable information on performance and risk. However, these standards do not provide a larger vision of the role of a company in society; nor do they include any information on sustainable and responsible corporate strategies. This article proposes a new type of financial statement, one that addresses the issue of the evaluation of externalities for a company. This new financial statement is intended to enlighten stakeholders with respect to the environmental, social, and economic impacts of a company.

Introduction

In accounting, four standard financial statements permit analysis of the economic health of a company as follows.

The balance sheet—an overview of a company's financial situation documenting how resources (liabilities) are used.

The profit-and-loss statement—an accounting of the evaluation of corporate performance.

The cash flow statement—a more detailed view of corporate financial health, including details of variations in cash flow.

The statement of changes in equity—a reflection of corporate wealth that includes details of the increase (or decrease) in the wealth of shareholders.

Financial statements are connected by accounting principles, which in turn give guidelines for auditing the information provided in the financial statements. Taken together, the financial statements provide a common set of rules that enable comparison of companies, which can be based on performance, risk, or management.

Some elements of corporate finance are beyond the control of most shareholders. These items include those relating to sustainability and long-term strategy—which is often limited to qualitative and descriptive information on financial statements —and the externalities generated by a company (i.e., its contribution/liability to society) (Searcy, 2016). Existing standards fail to account for externalities and long-term strategies. These shortcomings can be attributed to (Fagerström, Hartwig, & Cunningham, 2017):

analyses of long-term strategies are qualitative and thus difficult to compare and audit; accounting principles, which are mainly based upon accrual accounting and fair value (when a right of use exists) from a company perspective; and a company's financial performance, which is one of the main objectives of accounting.

Definitions

Externality: an impact, positive or negative, on any party not involved in a given transaction or economic act, for example the gap between social cost and private cost.

Environment: the ecosystem, resources, and community of beneficiaries of externalities (society).

Company (or consortium of businesses): an economic agent that employs capital for the conduct of an activity and attempts to generate profits for its shareholders.

Innovation (as employed in this context): new ideas or methodologies that are having an impact on the environment and therefore need a market for patented innovation (innovations that cannot be used outside the company, cannot generate externalities).

Norm: a rule standard, or law that maintains a balance between a positive and negative externality on the environment.

Pigovian tax: tax on market activity that generates negative externalities (the tax is intended to correct an undesirable or inefficient market outcome) (Pigou, 1932)

As a consequence, information on externalities must originate from additional corporate statements (Hartwig, Kågstrom, & Fagerström, 2014; Glensvig, Sørensen, Frier et al., 2014) because incorporation of the externalities concept into standard financial statements would impair their interpretation (due to nonmiscible concepts) (Hahn & Kühnen, 2013). This article proposes a formal structure to classify these externalities, and a way to determine their value based on accessible elements (Magee, Scerri, James et al., 2013; Moldan, Janouskova, & Hak, 2012).

Assumptions

Sources of Externalities (Economic)

Externalities arise when there is a difference between social cost (overall cost for society) and private cost (cost borne by a company). In addition, a mutualization system between a company and its third parties is a source of indirect externalities; for example, the state and insurance companies are intermediaries that manage a social cost (private costs may be different). All financial exchanges can be considered provided one of the two preceding elements can be identified (i.e., the difference between social cost and private cost, and/or the existence of a mutualization system) (Assumption 1).

The State as a Regulator of Externalities

The state is supposed to act in the public interest. In this case, assume that the state imposes taxes to counterbalance the value of externalities (all taxes are Pigovian) (Assumption 2) (Pigou, 1932), externalities match the value of taxes collected, and taxes allow compensating for the gap between social and private costs. The state defines standards that make it possible to keep the balance between the environment (social cost) and economic activity (private cost) and, therefore, tends toward the neutrality of externalities (Assumption 3). This assumption is valid given that:

States are bound to defend the public interest. People delegate authority to rulers to ensure that the externalities that may affect them are neutralized or compensated for (the state guarantees a balance between different economic agents), and

The transaction costs of taxes (collection, control, etc.) are negligible.

Accounting Principles

General Information

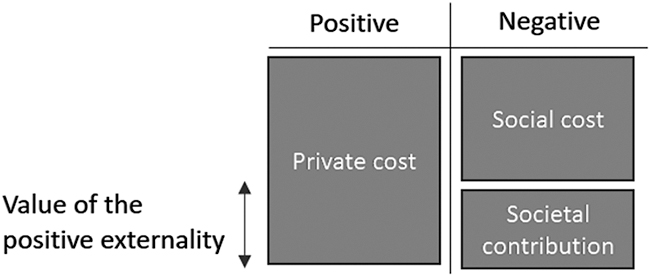

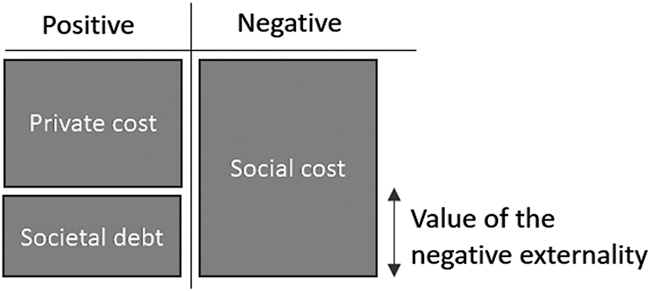

Externalities can be assessed via their social costs, which can be compared when they are considered negative externalities, and private costs are considered positive externalities (Coase, 1960). Accordingly, the externality is negative when the social cost is higher than the private cost (Figure 1) and positive when the social cost is lower than the private cost (Figure 2). The private cost is assessed by associating the costs and investments of a company with the sources of externalities (costs found in corporate accounting systems).

Negative externality

Positive externality

Social costs are assessed via 1.) damage costs, which imply the cost of impacts related to an activity managed by the company; 2.) control costs, defined as the assessment of all costs or investments necessary to control the externality; 3.) replacement costs (only for externalities related to resources), which are the costs of other resources that function in the same way without generating an externality; and 4.) taxes, which are costs assessed to cover externalities (Assumption 2). These methods of assessing social costs must come from other systems, namely, those not related to the accounting system.

Sources of Externalities

The sources of externalities influence the assessment method for social costs. In the balance of externalities, sources of externalities are connected to: nuisance (negative externality), depletion of the environment (capture of natural resources), taxes (Assumption 2), and other sources of positive externalities that benefit society as a whole.

Nuisance

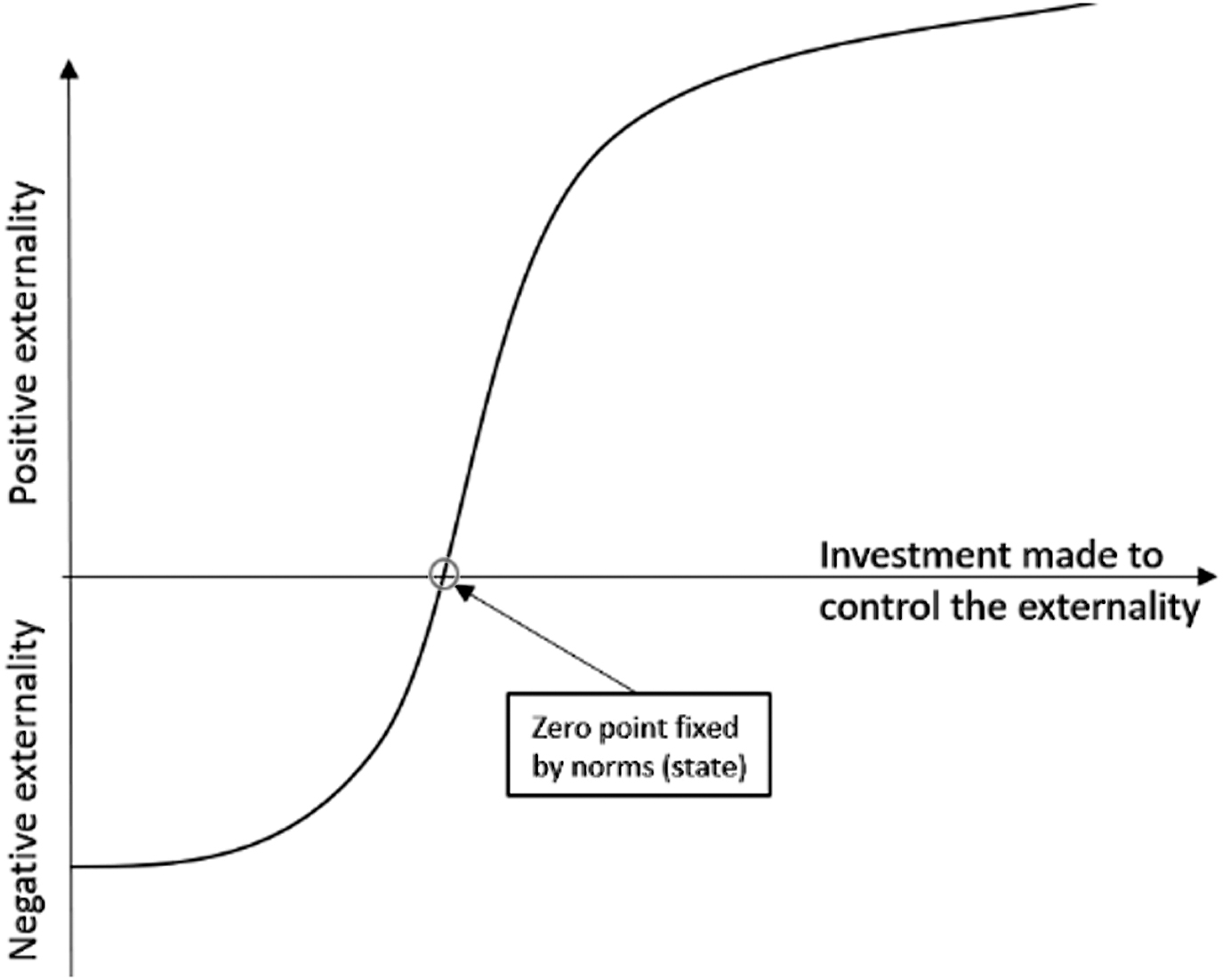

>When there is a source of nuisance, the state legislates to control the nuisance linked to this externality (Assumption 3). Assuming the company complies with the legislation, the private cost is the sum of investments and costs borne by the company to control the externality, and the social cost is the control value of the externality (equal in this case to the private cost).

The externality is assessed using its control cost (Figure 3). The control cost is assessed according to a standard set by the state. The state defines the threshold beyond which a nuisance becomes a source of externality.

Cost of control of an externality

In this scenario, two cases are possible:

The company exceeds the threshold set by the state.

The company falls behind the threshold set by the state.

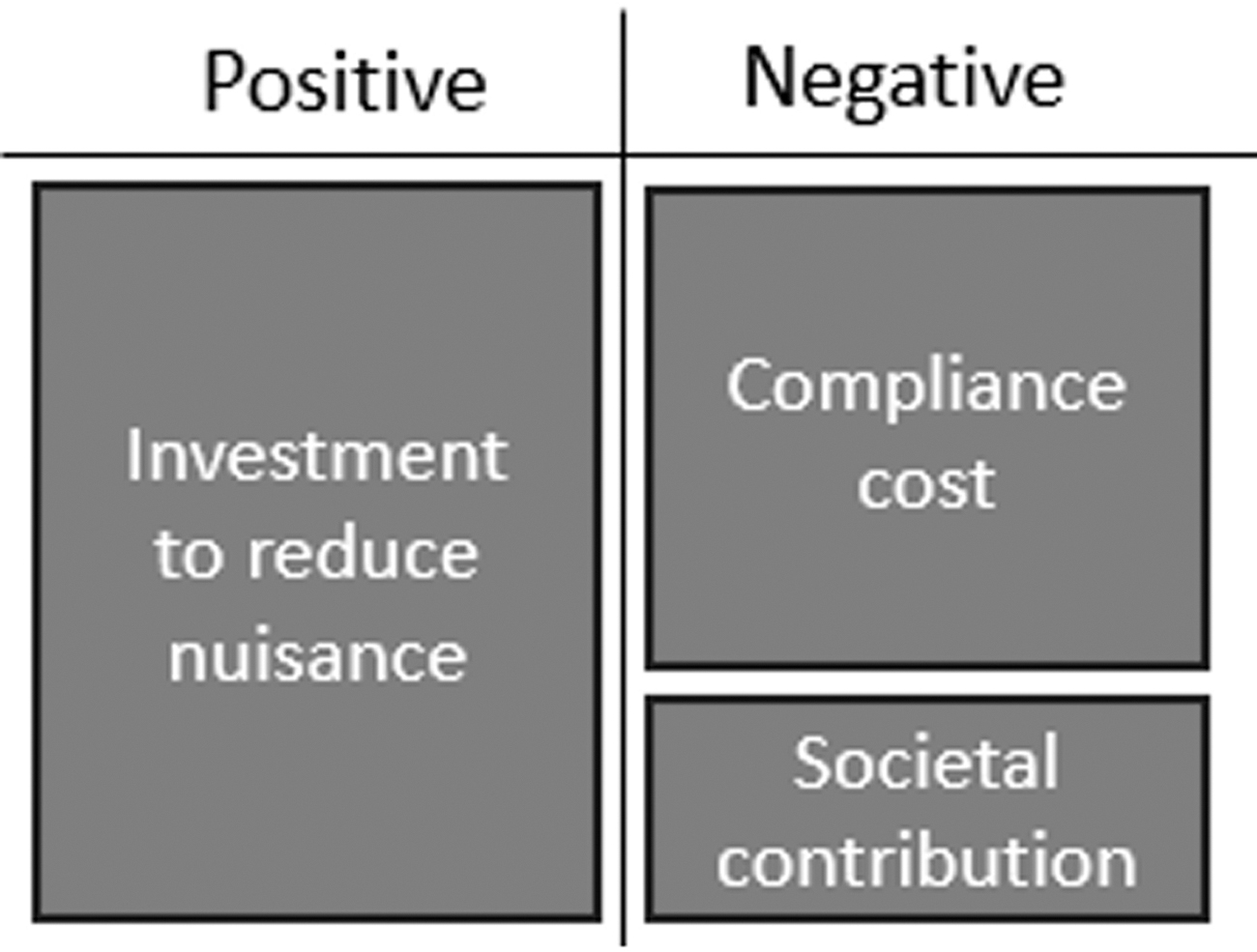

If the company exceeds the threshold, then the investment value (private costs) exceeds the social cost. The externality is positive. This externality value matches the surplus investment made to reduce the nuisance beyond what is necessary (Figure 4).

Externality when nuisance is controlled

If the company is below the threshold set by the state, the legislation provides for fines and compensation. Compensation may be covered by insurance or by the company. Thus, the negative externality is assessed through social costs—damages covered by all parties (insurance, state, company), and private costs—fines, insurance premiums, and other costs directly borne by the company.

Depletion of environmental resources

Social costs are assessed using natural resources. For renewable resources, they are assessed at the cost of regenerating the resource (agriculture, fish farming, etc.) For nonrenewable resources, if there is a reprocessing industry, they are assessed at the cost of reprocessing the resource (restitution to the initial state, recycling). If there is no reprocessing industry (irreversible transformations), they are assessed at the cost of substituting the resource for another renewable resource of the same utility (for example, in the case of fossil energy, the equivalent cost is to replace fossil energy with renewable energy).

Private cost is related to the acquisition of resources. Consequently, for renewable resources, the longer the regeneration cycles, the greater the risk of a high social cost (depending on the time value of the investments immobilized to regenerate the resource). For recyclable resources, the more consumable products are transformed, the more complex the reprocessing and the higher the social cost (the complexity of reversibility impacts the social cost). For nonrecyclable resources, the greater the price difference between two resources of the same utility (one renewable and the other nonrenewable), the higher the value of the externality per unit consumed.

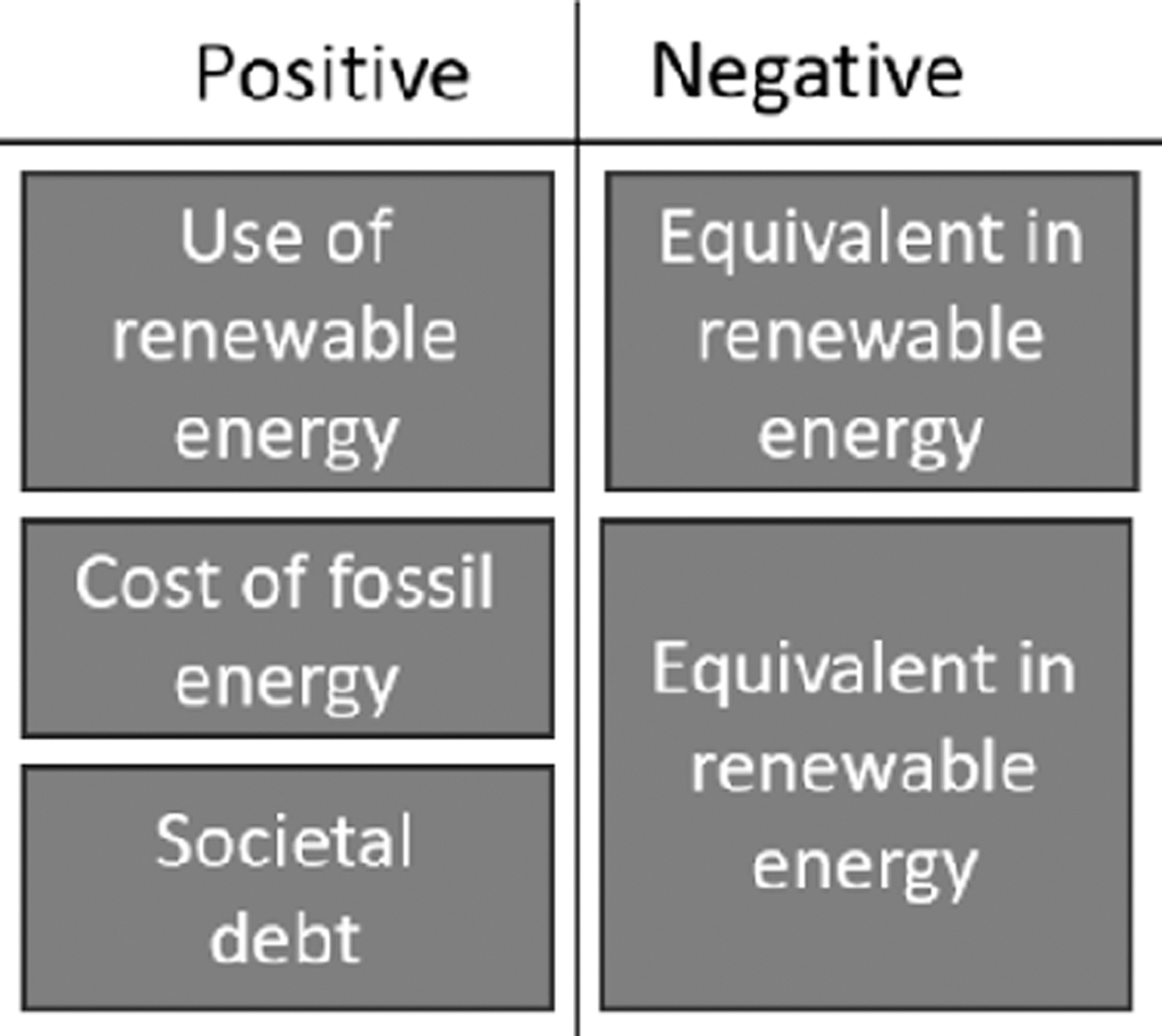

To reduce the value of its externalities, a company that consumes energy can take two actions. It can consume more renewable energies, which do not generate externalities (excluding investments). This would allow a steady consumption level, but it increases the unit cost of energy acquisition (assuming the unit cost of renewable energy is higher than the unit cost of nonrenewable energy) (Figure 5). It can also reduce its energy consumption. Note that this example does not include investments required to consume renewable energy, which are themselves a source of externalities. The supply chain has an impact on the balance of externalities and must therefore be considered.

Externality of energy supply

Tax

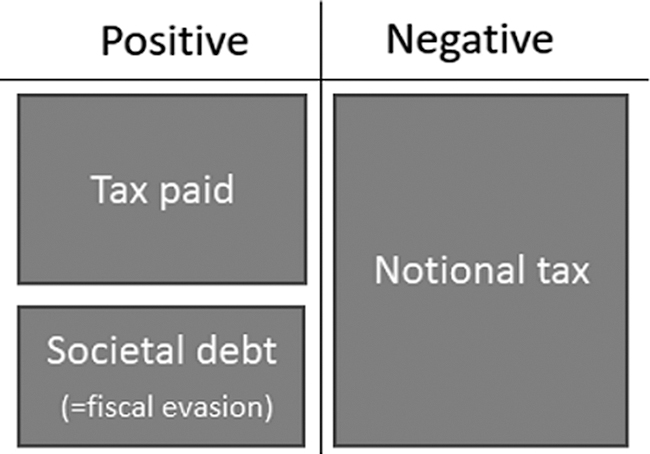

If the state manages a balance of externalities in which taxes due match the value of externalities (Assumption 2), then public spending that benefits the environment offsets a social cost such as education, security, and the environment. If a company pays its taxes, then the externality is zero insofar as the state's claims (social cost) match the company's payments (private cost). However, if the company evades its tax obligations, it can benefit from a market without paying taxes (free rider and negative externality), and the social cost becomes higher than the private cost (Figure 6). In this case, assume that the tax takes two values: 1.) private cost—a tax paid by companies (which is known), and 2.) social cost—a tax that the state is entitled to claim (a notional tax that needs to be clarified).

Tax evasion

The corporate income tax is a good example of this process. Companies pay corporate income tax per country. Nevertheless, the modernization of the economy (among other things) allows the repatriation of certain profits to countries with lower tax rates (tax evasion). In that case, where production is done without paying the official tax owed, a rule could be defined to reallocate the income before tax (depending on a repartition key, which could be the revenue by country, operating cost by country, etc.) and recalculate a tax due by country. The sum of all tax due is then the social cost, which could be compared to the tax paid.

Finally, this category can also include public subsidies or grants, which are sums given by the state, some with no private cost and some with a social cost. When the state subsidizes an activity, it expects the company or the economy to produce a positive externality in return, which offsets the social cost of the subsidy.

Further Sources of Positive Externalities

These include companies that may make investments to develop the company by investing in employee training, research projects, etc., or to strengthen the brand, or for tax reasons. In these cases, provided these investments benefit the environment, private costs are investment values, and social costs are possible subsidies, which would otherwise be zero. Without subsidies, the externality is positive.

Time Horizon

The balance of externalities must be calculated over a long horizon and with cumulative values, with a view to interpreting the long-term strategy of the company, as its identification, assessment, and correction might take time. With a long horizon (one of the consequences of uncertainty on the assessment of externalities), the impacts can be refined and adapted. Thus, it is necessary to provide for a system of reassessment of past social costs. A mechanism similar to fair value under IFRS (revaluation based on new elements) can be used to revaluate social costs.

Presentation Typology

The advantages of comparing positive and negative externalities include: identification of the sources of externalities (and their values) and matching by theme (or globally) the efforts made by a company versus the costs imposed on the environment by the actions of that company. Table 1 models this idea by theme. The difference in positive and negative externalities represents either a debt with the environment (if negative externalities exceed positive externalities) or a contribution (if the positive externalities exceed the negative externalities).

Example of Balance of Externalities

As shown in Table 1, externalities are classifiable in three categories:

Environmental—correspond to a depletion/enrichment of the environment (a biological, energy, mineral or land resource)

Social—correspond to a depletion/enrichment of human connections, including health, education, safety, justice, and culture

Economic—correspond to the economic flow, which contributes to externalities

Discussion

Extending the financial environment in which a company operates permits the determination of a company's externalities (positive and negative). However, there are two major drawbacks that should be noted. The process of compiling and monitoring all the costs (social and private) is complex. It presumes that the state is in the ideal position to act as the guarantor of the balance of externalities. On the other hand, this method has the advantage of providing a basis for comparing companies.

The State as Regulator of Externalities

The assumption that the state is the ideal regulator of externalities is debatable since it is based on the idea that states' only role is to manage a balance of externalities among the population, the economy, and the environment. In general, however, states do not systematically defend the common interest. Such an assumption is protectionist because it suggests that the state is the best arbiter of what is good for the environment. That said, the state is the only actor available to manage the common interest and therefore act to include externalities in its regulations. Thus, the state defines a pointer to identify the zero point, that is, the cancellation value of the externalities function, or the moment at which the function becomes a negative or positive externality.

Furthermore, assuming that it is the state's role to position the pointer simplifies the problem and helps avoid an absolute assessment of externalities. An absolute assessment would be more complex because of the multiple consequences of a nuisance or a withdrawal of resources (butterfly effect and never-ending problem), while the state limits itself to measurable and visible effects. Thus, the state allows for making some approximation but one with borders that can limit the problem.

Symmetry with Accounting Principles

Extending the financial environment in which a company operates allows for clarifying certain choices made around accounting principles and considers the transposition of certain accounting rules to the balance of externalities (Table 2).

Equivalence between Accounting and Balance of Externalities

Supply Chain

Global environmental effects are a source of externalities linked to consumption. For example, climate change involves the fossil fuels used to supply energy. These items have diverse costs from one state to another. Monitoring such costs is high since the process involves multiple sources and analysis of each. In this case, the state is a limiting factor because global effects need to be taken into consideration. To acquire and assess global and public data (states could be the source of this data), there needs to be a uniform method for evaluating externalities (social cost).

Manufactured products

Manufactured products involve an indirect extraction of natural resources. An automobile manufacturer, for example, uses raw materials for the production of the body, engine, etc. Therefore, the externality for an automobile manufacturer is a mix of different externalities (linked to recycling, extraction, logistics, etc.).

An accurate evaluation of the social costs of a manufactured product would involve one of two methods.

The tracing of processed raw materials and, for each component, a list of the composition and the quantity of energy involved in its production, followed by the valuation of externalities as a function of the list. This could be similar to labels on manufactured foods that list ingredients and nutrients.

The application of blockchain technologies to trace the origin and composition of traded products. (This is complex to deploy.)

Both methods involve data from suppliers, which can be complex to regulate and verify. In the absence of supplier data, secondary data (compiled and reported in a public database) could be used. This has the advantage of being accessible to all companies to produce their balance sheet. The disadvantage is that it would eliminate the ability to evaluate which suppliers play by the rules or even go beyond them because it would yield an average figure common to all suppliers. This would cancel the effect of the ability to have an ethical selection (a selection with low externalities) of suppliers).

Information Systems

Two types of information are necessary for processing and calculating a balance of externalities: private costs and social costs. Private costs are found in corporate accounting systems, but they are missing an attribute that can identify the source of an externality (see Supplementary SI-01). Social costs are the combination of private data and public data. Private data is company-specific, for example, in damage associated with an industrial disaster. It could be reported in terms of volume consumed (resources and nuisance), or may, in part, come from Global Reporting Initiative (GRI) reporting (or other databases).

Public data allows volume to be converted into social costs when the nuisance or resource is global or not company-specific. It is the most challenging data to gather and should be gathered by source (damages, resources), both realized and future, and linked to other measurements (temperature, bioresources, etc.).

Conclusion

Presentation of the impact of a company on its environment requires departure from existing financial statements so that these instruments can incorporate disparate concepts: negative and positive externalities (a relative vision) as a means of gauging the efforts toward social integration committed by a company; and externalities over a long-time horizon, given the inertia of the environment.

The evaluation of these externalities is based on two major changes to financial accounting:

Extension of the Pigovian tax to balance the gap between social cost and private cost to cover externalities, and

All interactions coming from a mutualized system should be included in the balance of externalities.

Some analogies exist with accounting structures, and some accounting rules could still be applicable in this context. The balance of externalities demonstrates the potential global impact of omitting externalities from financial accounting. Adding these externalities could encourage companies to reduce their environmental impacts by identifying companies that are free riders.

Footnotes

Funding Information

There are no funders to report for this submission

Author Disclosure Statement

No competing financial interests exist.