Abstract

As the gambling industry evolved into an online consumer commodity, gambling operators are adopting financial technologies as the preferred way to process deposits and win withdrawals. These technologies allow consumers to connect different payment methods, hence enabling cross-sectional fund access and creating financial footprints that have the potential to help prevent excessive gambling. This prompts an exploration of how payment solution providers can contribute to responsible spending, given their increasing participation in the gambling industry. Despite such possibilities, there is a paucity of research on how transactional data can be harnessed to infer (problematic) gambling behavior and pathways to bring digital payment solution (DPS) providers on board the Responsible Gambling agenda. Following a comprehensive literature review that developed gambling behavior indicators within payment transactions, we conducted a three-round Delphi study to evaluate this set of preliminary indicators. Sixteen experts with diverse backgrounds were asked to evaluate if a given indicator has the potential to evaluate gambling consumption. The study considered an 80% rate as consensus, and indicators under the level of consensus were returned for further reappraisal to the participants. Building on our findings, we present a conceptual framework that could provide a pathway to incorporate financial institutions into initiatives promoting responsible gambling practices. In addition, these insights may inform policy discussions regarding the active involvement of financial institutions serving gambling operators in advocating responsible gambling behavior.

INTRODUCTION

In the last two decades, there has been a paradigm shift in how we purchase consumer goods and, with it, the role of financial institutions. Digital payment solutions are increasingly becoming an essential part of our everyday lives, being used for online purchases, receiving money, investing, buying houses, or managing retirement funds. 1 Digital payments have also found their way to the gambling sector, where most online operators are now integrated with financial institutions to process payments associated with players’ deposits and win withdrawals. These institutions are considered a key infrastructure for online gambling, allowing players to connect their bank accounts, cards, and (depending on the jurisdiction) invoices/credit payments to one account, providing a convenient way to access different sources of funds, often with only negligible delay.

Given their central position in facilitating deposit and withdrawal transactions for gambling activities, financial institutions could potentially play a pivotal role in promoting moderate gambling consumption. However, their influence on consumer gambling behavior remains largely unexplored, with potentially adverse consequences. 2 First, financial institutions can facilitate “uninterrupted funds” for gambling consumption by connecting users’ accounts to different fund sources. Disregarding all other dimensions, this can appear as a user-centric design feature developed in a collaborative effort between players and payment providers. However, as Schüll 3 noted, such collaboration is asymmetrical in that while both payment providers and gambling operators profit, it can lead to a depletion of funds for the consumer and have negative consequences outside the immediate consumption context.

Another concern comes from the innate nature of digital payment itself. In general, financial institutions are not incentivized for their customer to do well but to shop well. The industry does better with volume and therefore continuously strives to find ways to influence consumer experience: better UX, convenience, and speed, and even creating new consumer experiences such as Buy Now, Pay Later models. In the context of gambling consumption, however, fast-paced spending and convenience do not equate to a better end-user experience, at least not long term. Research across the fields consistently shows that digital payment can alter consumer behavior by lessening the “pain of paying” that can result in suboptimal financial decisions.4,5 Gainsbury and Blaszczynski 6 noted that digital payment could “diminish the value or lower awareness” of money spent, contributing to gambling overconsumption.

Although the extant literature on the role of financial institutions in gambling behavior is scarce, gambling-related financial harms have been extensively studied. There exists a consensus that consumer financial harms are the first recognizable sign of gambling overconsumption. 7 Such early signs may include being unable to meet ends, increased financial fragility, and a loss of financial security and freedom that can be observed at the individual, family, and societal levels. 8 Marionneau et al. 9 pointed out that societal-level financial harms may encompass strain on the public health system and rising living expenses, while individuals and families could experience decreased income, debt accumulation, or even homelessness.

Current Responsible Gambling (RG) strategies focus on three areas: (1) operator-based gambling harm minimization tools; (2) government policies and interventions, including regulating the market; and (3) individuals’ responsibility to practice RG behavior. 10 In many jurisdictions, gambling operators are required to use RG tools such as behavior tracking, self-exclusion mechanisms, setting budget limits, enforced breaks, and pop-up messages. In addition to enforcing these requirements, government agencies regulate the gambling market and the availability of help for problem gamblers. Ultimately, most current intervention strategy settings put the onus on individual gamblers to seek help, adopt RG tools, and self-regulate to exhibit responsible behavior. 11 Despite the extensive effort to examine gambling-related financial harms, there is a scarcity of research that attempts to comprehensively capture and frame the potential role of financial institutions in the effort to promote RG.

The aim of the current study is, therefore, two-fold. First, the study aimed to develop a preliminary set of potential financial indicators derived from players’ financial and gambling transaction behavior. These indicators could be used by financial institutions to identify and assess gambling consumption. The indicators can be directly observed within financial institutions datasets, indirectly inferred from deposit and withdrawal behaviors, or obtained through collaboration with gambling operators. This initial set of proposed indicators is neither exhaustive nor definitive but could nonetheless provide a basis for future research. Second, it aimed to formulate a viable framework for payment solution providers to adopt the agenda of RG within their capacity as financial institutions.

Our main focus in this research will be financial institutions that are integrated with online gambling operators. A financial institution is an organization that provides various financial services such as deposit management, loans, investments, insurance, wealth management, and payment facilitation. Financial service providers vary in their specializations, ranging from large institutions like banks that offer a wide array of financial services to smaller entities such as digital payment solution (DPS) providers, which heavily use financial technologies (Fintech). In addition to accepting direct card and account-to-account bank payments, most online gambling operators now use DPS providers that can read and transfer payments from a customer to a merchant’s bank account. When integrated into gambling sites, DPS platforms facilitate deposits and withdrawals through methods such as direct bank transfers, card payments, and real-time invoices, thereby acting as intermediaries between customers and gambling operators. Even though DPSs are the main focus of the current research, the relevance of this study can extend to any financial institution catering to gambling customers.

Most DPS platforms with gambling customers retain account-based records of consumer transaction history of gambling. These transaction datasets could be used to probe both individuals’ holistic financial health and gambling spending behavior. For instance, Deng et al. 12 proposed a variation of deposit size over time within transactional data to evaluate one’s gambling trajectory, frequency, or intensity. Other transactional makers examined to interpret players’ behavior include crashing deposits, reversing withdrawals, requests to remove limits, successive sprees of increasing deposit amount, and steady increases in wagers. 13 In their extensive work, Ghaharian et al. 14 showed the potential use of transactional data to identify harmful gambling markers within payment behavior. In addition, the potential implementation of RG tools at the DSP providers level was the topic of discussion where players will have an umbrella of financial protection regardless of gambling operators’ RG tools. 15 In this setting, RG tools implemented by DPS providers, such as setting gambling spending budgets and using self-blocking features, have been examined as indicators for evaluating consumers’ gambling behavior.

Two recent studies using gambling transactional data have demonstrated that integrating various data points from different sources can offer a more comprehensive understanding of gambling customers. Using a data fusion method, Zendle and Newall 16 showed that novel insights about gambling behavior can be obtained by using multiple sources of data including bank transactional data, self-reported measures including gambling behavior (PGSI items), sociodemographic (age and gender), bank income reports, and mental health self-reports. Similarly, Marionneau et al. 17 used bank transaction data from applicants for debt consolidation services, analyzing transactions such as deposits, withdrawals from gambling winnings, gambling activity types, and both secured and unsecured personal loans to investigate gambling-related indebtedness. In addition to novel methodological approaches, these studies demonstrate that financial institutions can offer a comprehensive and detailed perspective on individuals’ gambling behaviors and their impact on everyday lives.

Operator-based gambling transactional data, including wager and win payouts that customers sometimes keep in their operators’ deposit accounts, have been widely used to assess gambling-related harms. Particular emphasis has been placed on wagering behavior—such as sudden drops or irregular decreases in wager size, arbitrary increases, wagering sprees, and other spending patterns—to evaluate gambling-related harms. 18 Even though such wagering data are not directly accessible to DPS platforms, their close collaboration with gambling operators can open up a data-sharing opportunity to effectively track gambling consumption. 19

There is a growing consensus that financial institutions have specific obligations and responsibilities toward their customers’ financial well-being (FWB). For example, they must protect customers from credit risk and ensure that customers fully understand their rights and obligations before entering any agreement. 20 In addition, financial institutions have a corporate social responsibility (CSR) to help improve their customers’ financial health and make positive contributions to society. Transparency in bank information, for example, is expected to enhance financial literacy, thereby improving consumer FWB. 21 Current well-being frameworks commonly used by financial institutions such as CSR, however, center on the broader ethical standards in business practices and do not provide a suitable platform to address the responsible gambling agenda. 22 As such, it remains elusive to what extent and in what capacity financial institutions can engage in addressing harmful gambling.

The present study extends the extant literature on financial indicators of gambling by performing a three-round qualitative Delphi study to evaluate key manifestations of gambling behavior that could, in theory, be derived from players’ transactional data. Given that the primary objective is to onboard financial institutions such as DPS platforms to the RG agenda, the manifestation of these indicators in a way accessible to DPS platforms (whether identified within their datasets, indirectly inferred from deposit and withdrawal behavior, or obtained through collaboration with other actors such as operators) will be discussed based on the findings. In addition, the research aims to provide a conceptual framing of categorizing financial indicators of gambling harms using the financial health knowledge base, hence providing a practical pathway to onboard the DPS platforms in the overall effort of promoting RG.

METHOD

Ethical consideration

The Swedish Ethical Review Authority (Etikprövningsmyndigheten) approved the study (2022 05843-01). All participants received full study information and provided digital consent to participate. Data were deidentified before analysis and stored in a secure location approved for handling personal data.

Design

The current study departs from a previous, two-step narrative literature review work that involved identifying key conceptual indicators of individuals’ FWB using a financial research knowledge base and then contextualizing it to the gambling field. 23 The review generated a list of key financial indicators, in the form of consumer deposit behavior, win withdrawal patterns, and wager transaction activities (see Supplementary Appendix SA2). Although certain indicators, such as specific wager amounts, may or may not be directly visible in the DPS dataset, they could be accessible through collaborative data sharing with operators. As noted later in the discussion section, in the absence of such collaboration, overarching patterns could potentially be inferred from deposit and withdrawal behaviors.

In this study, we conducted a Delphi study that includes three survey rounds using an online tool to examine and evaluate financial indicators that were identified in the literature review. Each participant was asked to submit a rating for a list of financial indicators to detect consumers’ gambling behavior. The Delphi method is a systematic, iterative process designed for researchers to obtain a collective view from the panel of experts. 24 The typical multistage process involves researchers collecting input from experts on a set of questions, synthesizing their feedback, and guiding them to consensus. 25 The method was chosen for the following reasons: (1) it enables the integration of expert stakeholders from various geographical regions and diverse backgrounds; (2) it facilitates iterative feedback, enhancing and incorporating new concepts into the study; and (3) in addition to its anonymity, stakeholders can participate at their convenience (limiting sampling bias).

Participant recruitment

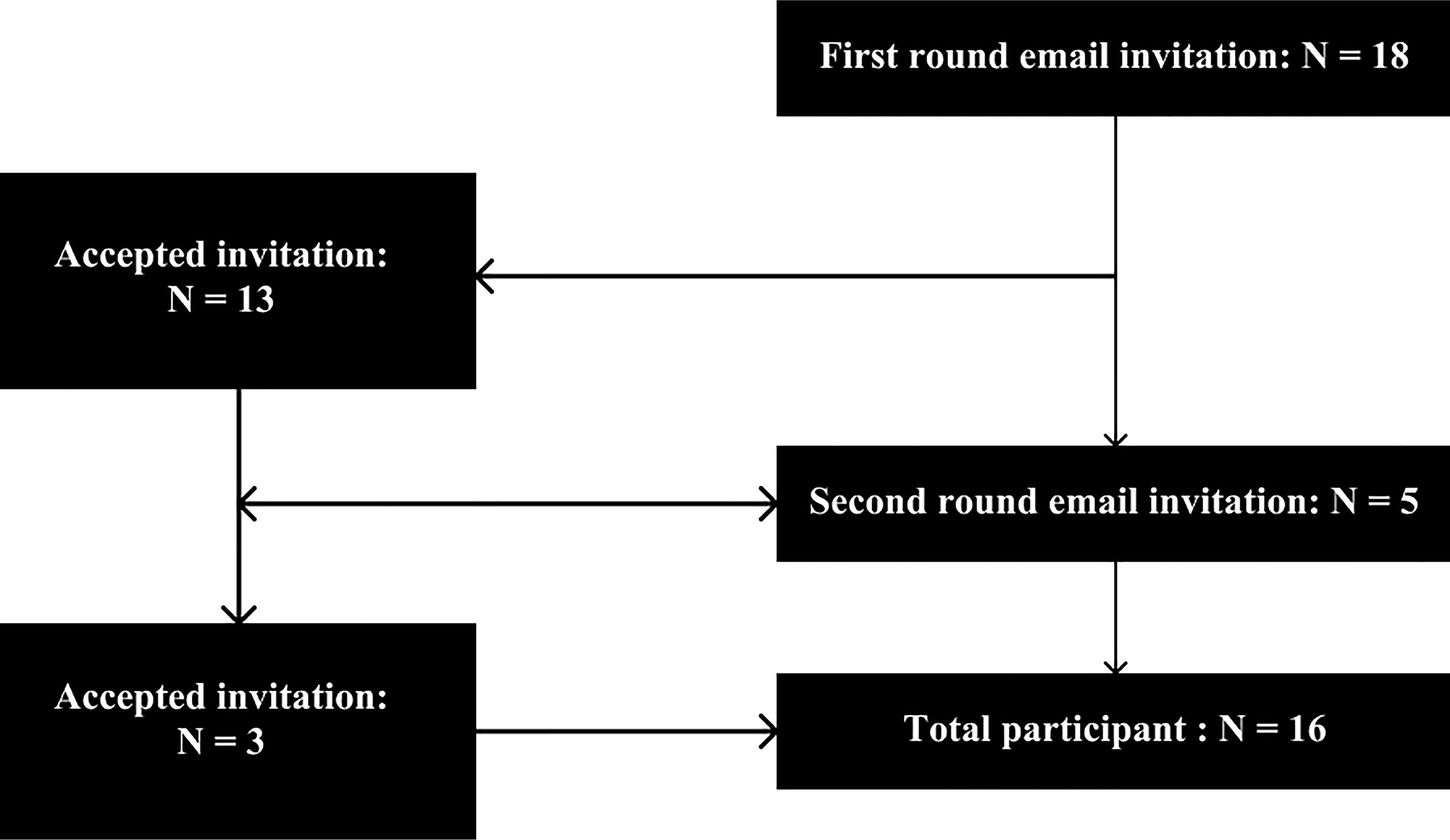

Participant panelists came from a broad set of stakeholders, including representatives from Fintech, gambling operators, academic researchers, and professional organizations working with counseling around gambling addiction. In total, we reached out to 23 potential participants via email, and 16 participants in total accepted our invitation (n = 16, 69.6% of invitees). In addition to our network of contacts (n = 13, 81% of participants), we identified and recruited candidates with a specific research focus on gambling and financial institutions from a literature review we conducted in a separate study (n = 3, 18% of participants). Participants from academia had diverse backgrounds: 5 in psychology, 3 in public health policy, and 1 in epidemiology. Among them, five hold full professorships specializing in the field of gambling research at their respective academic institutions. All opinions received equal weight. While Figure 1 shows the recruitment flow, Table 1 summarizes the characteristics of the participants.

Participant recruitment process.

Description of Participants

Study procedure

As noted earlier, the findings from the previously conducted comprehensive literature review were used to develop and categorize a list of key indicators of consumer behavior in players’ financial data (see Supplementary Appendix SA1 and Supplementary Appendix SA2). To design a survey-friendly structure, a simplified three-theme structure was constructed from Supplementary Appendix SA2 to organize the indicators: background information (user profile and sociodemographic factors), payment behavior (financial behavior and psychological factors), and financial literacy (financial knowledge and literacy).

In total, k = 40 consumer financial behavior indicators were identified as candidates to infer gambling behavior, and one indicator was later removed due to its content overlap with other indicators. Supplementary Appendix SA3 presents the final list of indicators and their conceptual organization. The 39 indicators were then distributed online via the REDCap survey tool, which allows sending emails with individual links to the survey. Participants were given 15 days to respond in each round, and all outgoing surveys were set with two reminders. In each round, participants were asked to rate to what extent they agreed that a given indicator—individually or in combination with other indicators—could be used to infer gambling behavior on a 5-point Likert scale (strongly agree to strongly disagree). The consensus was defined as 80% of the participants’ scoring of the respective indicator with either a “strongly agree” or “agree” scale. In addition, the survey tool provided an opportunity for participants to give comments or recommend more indicators, and this was also encouraged in the individual email communications with the participants.

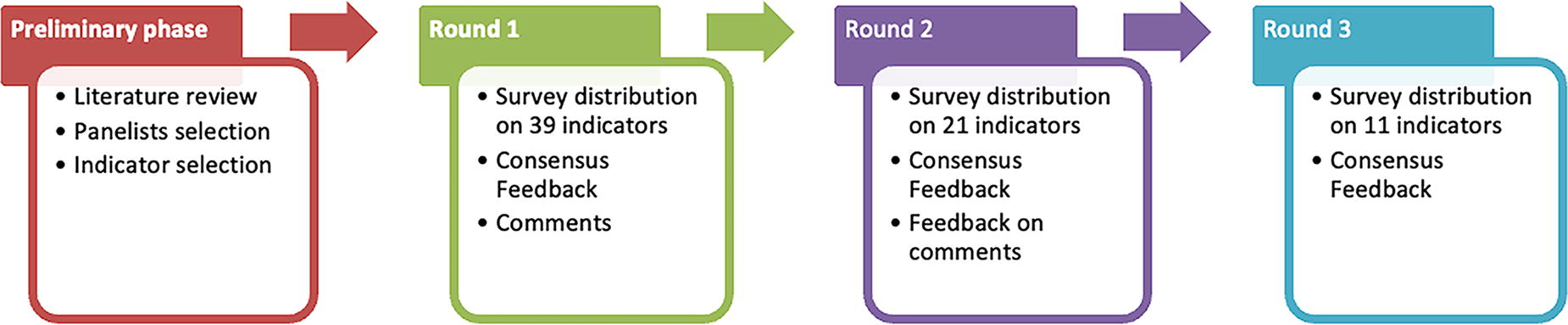

Each participant’s response was pseudonymized using a numeric code before data analysis (e.g., Delphi participant 1). After each round, data were downloaded from REDCap into SPSS 27.0 to analyze the rating scores, and feedback on the consensus level on each indicator was then given individually via email as a PDF attachment (see Table 2). Adding the consensus level allowed participants to revisit their responses in light of other panelists’ opinions. In each consecutive round, indicators that were under the 80% level of consensus were returned for participants’ reappraisal until round three, where replication stability of response was achieved. Each qualitative feedback received from participants was individually addressed. In cases where general feedback to all participants was required, we added additional descriptive comments to the subsequent round survey’s introduction. Figure 2 summarizes the study design.

The study design.

Example of Consensus Level Feedback To a Participants

RESULT

Round one

All participants completed the first round, rating all 39 indicators. Consensus was reached on 19 indicators, of which seven indicators received a 100% consensus. Five indicators received an under 50% consensus rate, with the area of residence being the least rated indicator at 31%. We also received qualitative feedback from seven participants that mainly concerned the different assumptions they had while rating the indicators. Three participants noted that they could only consider some of the indicators if they appeared in interaction with other indicators. We did not receive suggestions for new indicators per se, nor could we deduce any by thematically analyzing the feedback due to the nature of the comments.

Table 3 presents a sample of these comments, selected for their unique perspectives and shared challenges in validating the indicators. The second round of the survey introduction section addressed round one comments with a remark on the assumption made in developing the Delphi study. In addition to addressing these concerns with the individual participants who raised the concerns, all other participants also received more information about the study assumptions, together with the result of round one via email. The result of all indicators evaluated in this round is presented in Table 4.

Sample Qualitative Feedback from Round One

Round One Consensus Level on the Indicators

Round two

In round two, the 20 questions that were under the 80% level of consensus were returned for participants’ reappraisal, and all 16 participants completed the survey. Consensus was now reached on nine indicators, of which one indicator (“the person asks for a bonus for gambling”) received a 100% consensus. Two indicators (“making a consecutive wager of equal amount to the same gambling operator during observation” and “Gender”) rated less compared with round one, with a drop in consensus from 8 and 10 to 7 and 9 consecutively. The largest change of mind among the participants was observed in the indicator of a ‘steady increase in wager accompanied by small win payouts’ with a rise from 43% to 81.3%. Except for one indicator, “the person asks a bonus for gambling,” the consensus level of round two had a score of either 81.3% (six indicators) or 87.7% (two indicators). While Table 5 presents the result of all indicators from round two; Table 6 shows an excerpt from the round two consensus report sent to a participant to illustrate how panelists changed the rating of indicators throughout the survey rounds.

Round Two Consensus Level on the Indicators.

Sample of Multiple Round Consensus Feedback Format

Round three

In the last round, the remaining 11 indicators were returned to participants, and three indicators were promoted to a consensus-level rating. The indicator “making a consecutive wager of equal amount to the same gambling operator during observation” received the lowest rating with 31.3%, while the three agreed-upon indicators’ scores were 87.7, 87.7, and 81.3. Table 7 presents the result of all indicators evaluated in round three. Examining the final scoring, we found three indicators that were often underrated throughout the survey rounds [“area of residence,” “similar wager ceiling in a given period (e.g., monthly),” and “making a consecutive wager of equal amount to the same gambling operator during observation”]. This is consistence with the SD values in which all indicators with a greater variance (SD > 1) in the first round were all rejected by the participants by the last round. In contrast, the top-rated indicator with 15 “strongly agree” votes in round one (“the person requests help for gambling problem”) had one of the lowest SD values (0.4).

Round Three Consensus Level on the Indicators

DISCUSSION

As DPSs are becoming more prevalent in online gambling, they can present both risks and opportunities. In the context of gambling activities, the convenience and speed that come with payment solutions may not always equate to a better end-user experience since these features may facilitate more time spent on gambling activities by enabling the connection of multiple funding sources into one account, rapid deposits, or a redeposit of wins. However, the birds’-eye view of consumer behaviors on different gambling sites could offer a unique opportunity for financial institutions in general, and DPS providers in particular to implement RG tools that avoid the pitfall of having RG tools tied to individual gambling providers.

Given this context, the present study began by identifying and validating potential indicators within financial and gambling transaction data. At the end of the final round, consensus was achieved for 31 (79%) of the original items that could serve as potential indicators to identify harmful gambling (see Supplementary Appendix SA4 for full percentage point report). Figure 3 presents how the consensus of indicators in the study unfolded through the three rounds of surveys. Across participants, the payment behavior category received a higher rating on average than the other two conceptual themes, in which out of 29 indicators, all but three indicators (10%) failed to reach a consensus. This level of agreement is consistent with the literature findings that deposit and win withdrawal behaviors are widely used to identify harmful gambling. 26 Similar to the general financial research literature, these findings point out the influence of behavior-oriented intervention approaches we also find in the gambling field.

The degree of consensus among panelists on indicators during each rating round.

One key objective of this study was to develop a preliminary list of indicators that financial institutions such as DPS platforms can use to assess their customers’ gambling activities. The set of financial and gambling transaction indicators validated by the participants can be manifested across multiple actors, including in the DPS and operator datasets. Supplementary Appendix SA5 organizes the 31 validated sets of indicators according to their primary points of manifestation. The first 17 indicators, categorized into payment history and financial literacy, can be directly obtained from DPS platforms and potentially from most financial institutions serving gambling customers. The remaining 14 indicators, classified as transactional gambling behavior indicators, are primarily found in the operator dataset, with wagering behavior serving as the primary marker. Transactional wagering data can offer insights into players’ psychological behaviors that ultimately influence financial decisions, such as impulsiveness, locus of control, and losing runs. Therefore, combining these data points with operators’ sharing these indicators with DPS platforms can offer crucial insights when evaluating overall consumer financial well-being. Such collaboration is in line with the recent calls for all gambling stakeholders, including financial institutions, to take responsibility for promoting healthy gambling. 27

In the absence of such data-sharing opportunities, DPS platforms can still use their deposit and withdrawal dataset to infer players’ behavioral tendencies and psychological traits. Supplementary Appendix SA5 provides potentially inferring data points that are readily available in the DPS platform dataset. Gambling players tend to use a specific DPS platform for their gambling activities across multiple operators. 28 In some settings—where for example players’ general financial impulsivity is evaluated—deposit-oriented inferred data can provide a more comprehensive overview of the player across multiple operators, which is not possible to get from a single operator wagering data. It is important to clarify that we are not claiming wagering transactional data is equivalent to deposit data from DPS providers, though in some cases, they can be similar. However, the initial list of financial indicators manifested in the financial institutions dataset in Supplementary Appendix SA5 could enable financial institutions to make distinctive and autonomous contributions to the RG agenda. Moreover, this set of indicators can lay the groundwork for refining and optimizing sustainable financial indicators for DPS platforms with gambling customers.

The wider FWB literature routinely identifies sociodemographic factors such as age and gender as the main indicators of consumer financial health. 29 In the gambling literature, we also observed sociodemographic factors, including the area of residence, as potential indicators to evaluate risk in gambling. 30 However, “background information” indicators in our findings consistently trailed behind in building consensus. We hypothesize, congruent with our participants’ feedback, that a lack of context in the case of socially oriented indicators can present a challenge in building consensus across stakeholders since these indicators appear relevant when they are presented either in context or in interaction with the other indicator(s).

Another potential challenge in achieving consensus could stem from the intrinsic nature of Delphi study methods, which allow for the recruitment of participants with highly diverse backgrounds. This was well noted by one of the panelists, who wrote a personal email comment as follows:

“It seems there is some extreme responding (i.e., picking the highest categories), and it skews positively. For example, I was struck by the higher answers in “being rude to a customer service agent.” There could be a wide range of reasons for this – some people are just rude or having a bad day or experiencing something unrelated to their gambling – so this basically tells us nothing in a vacuum, but the bulk of the responses were on the higher end of the scale”.

Delphi participant 11 (printed with permission).

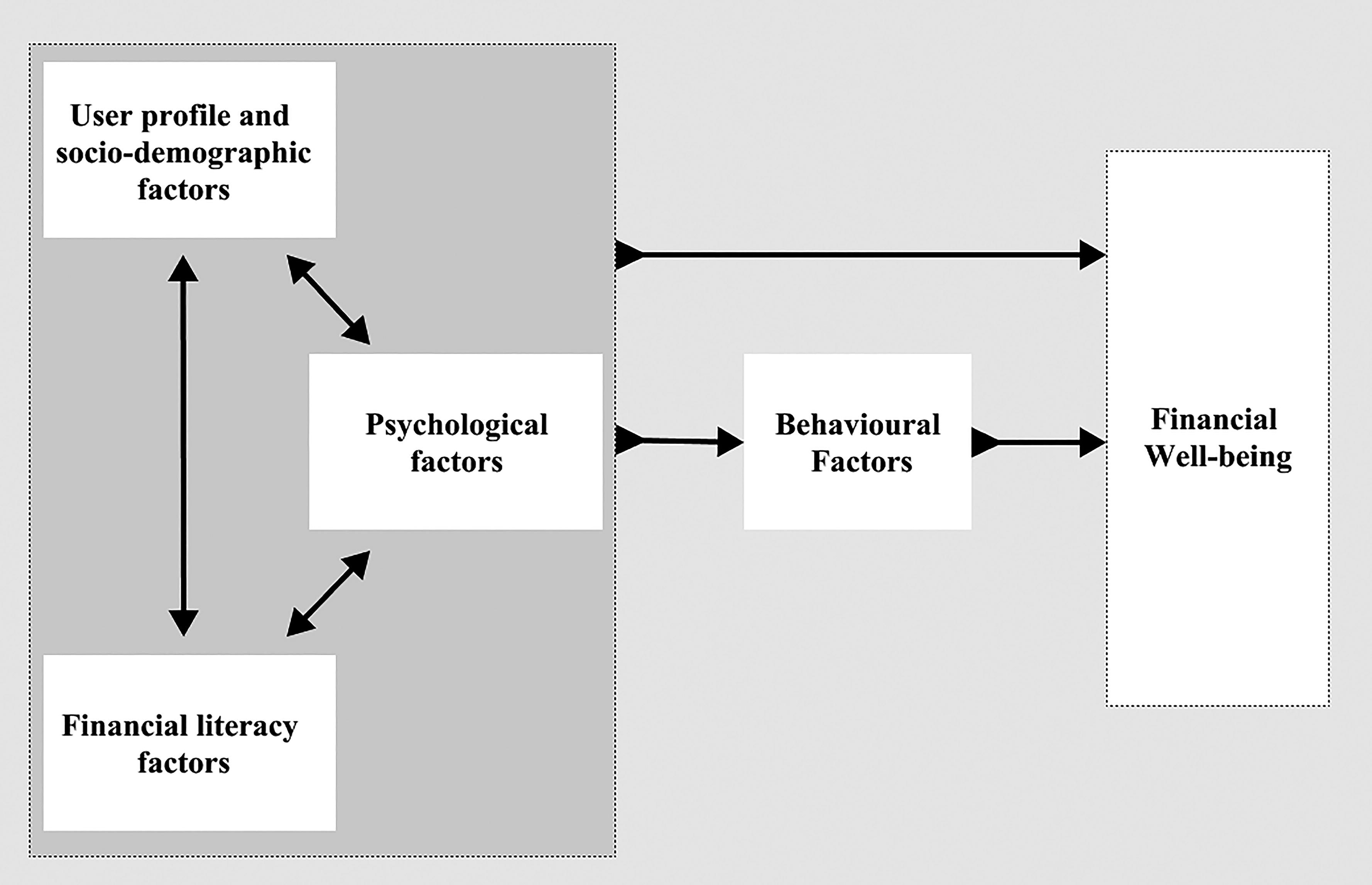

In addressing some of these shortcomings and further optimizing our findings in the financial institution context, we returned to the general FWB conceptual framework used as a base to create and categorize the list of indicators examined in the current Delphi study (see Supplementary Appendix SA1). In doing so, we applied the original conceptual framework as a lens to (1) visualize contextual settings and possible interactions between the categories and (2) thematized layers of players’ interrelated factors within the general FWB determinates. Figure 4 illustrates such a preliminary conceptual framing.

Conceptual framework of financial determinates in the context of gambling.

In the “first set” of the framework, we find three closely interconnected FWB determinates: user profile and sociodemographic, psychological, and financial literacy factors. Individually or together, these determinates established the conditions that can affect an individual’s financial behavior. 31 Research on harmful gambling also shows that “general sociodemographic factors and personal psychology” such as age, gender, personality, and temperament can influence an individual’s gambling behavior. 32 Consequently, the three determinates set the stage for what consumers (will) do (i.e., their behavior).

Most of the financial gambling makers in the current study can be traced back to the behavior-determinate construct. 33 Occasionally depicted as a determinant of financial capability, behavior exhibits the most robust correlation with an individual’s financial well-being. 34 Examining players’ behavior has also profoundly influenced the research agenda in gambling in both detecting harmful gambling patterns as well as implementing effective interventions. 35 As such, financial behavior is included as the primary pillar within the proposed conceptual framework.

The proposed conceptual framework emphasizes individual-level characteristics, yet external factors beyond the control of individual players can also impact financial behavior. The general FWB conceptual framework noted in Supplementary Appendix SA1 noted that two additional components—interventions and external factors—have the potential to influence both an individual’s overall FWB and the other four determinants. External factors encompass nationwide economic effects, government regulations, technological advancements, and the overall environment in which gambling occurs. For instance, Lakew et al. 36 reported that technological features in DPSs can nudge, trigger, or facilitate certain behaviors, resulting in gambling dark flow, unsafe gambling activities, illusions of control, attention biases, and a reduced perception of the value of money spent. These structural factors, originating from the external environment, should be considered, especially when formulating policies for DPS providers in the context of gambling. Finally, gambling interventions, such as RG tools designed to influence players’ behavior and improve financial literacy, have the potential to impact an individual’s spending in gambling.

LIMITATIONS AND FUTURE RESEARCH

The current study is narrowly focused on identifying and validating individual-level markers of gambling behavior using transactional data. As a result, both the indicators and the proposed conceptual framework are centered on individual characteristics. As noted earlier, however, harmful financial behavior in gambling can also be influenced by external factors, including incentives provided by financial institutions, such as credit for gambling, bonuses, and fast deposit and withdrawal UX features. Consequently, future research should examine how external factors, including the business models of financial institutions, contribute to harmful gambling spending. Such research can assist in exploring policies and regulations designed to mitigate the harms associated with gambling products.

In addition, the recent integration of various data sources to create a comprehensive understanding of players’ spending behavior can pave the way for third-party participants in gambling activities to contribute to healthy consumption habits. More research is needed that incorporates additional data sources, such as registry data, income data, self-report results such as FWB and PGSI tests, and other credit check-related information, to thoroughly evaluate gambling spending behavior. This comprehensive approach can support the implementation of stricter policies, such as affordability checks.

In this study, we focused on DPS providers due to their significant role and growing adoption in the online gambling industry. However, the financial indicators we identified can also be observed in the datasets of most financial actors that serve gambling customers. Therefore, the findings from this study could apply to integrating any financial institution into the RG agenda if they cater to gambling activities. Given that some online operators still allow customers to link their bank cards or accounts directly to their gambling accounts, further research is needed to explore how large financial institutions, such as banks, can contribute to the financial well-being of gambling customers.

Finally, we want to stress that the conceptual framework presented here, as well as the categorization of indicators, should be seen as a starting point for further research. There is room for improvement in labeling the concepts, testing theme relationships, and identifying additional indicators, preferably using a quantitative dataset. Nevertheless, grounded in the financial research literature, the present study can serve as a preliminary foundation for formulating the role of financial institutions within the framework of RG initiatives.

CONCLUSION

With the growing digitalization of the financial sector, payment solution providers are no longer passive enablers but can play active roles in influencing consumer behavior in the setting they are employed. Naturally, being technological, they can exploit their information advantage, user behavior bias, and geographical location to increase purchase volume flows. However, with the vast behavior information they maintain, financial institutions can be used as a catalyst for positive change. Taking this into account, the gambling field has begun to examine how to formulate the role of financial institutions in the context of RG.37,38 The current study contributes to such efforts in the following ways.

First, it validates the use of indicators that could theoretically be used to flag gambling overconsumption using financial behavior datasets. By using these indicators, financial institutions can potentially identify harmful consumer behavior and use appropriate RG tools. Second, the study conceptualizes gambling behaviors in a “language” that could be understood by the financial sector. Previous research suggested that a lack of research that conceptualizes the role of financial institutions in gambling could partly be the reason for their lack of participation in the RG effort. 39 The current study deliberately applies financial concepts (e.g., FWB), indicators, and key transactional manifestations to conceptualize the role of financial institutions in a manner that could easily be understood across the industry.

Third, the current study aims to open up more research opportunities in terms of both intervention and prevention. The current RG effort is mainly focused on gambling operators’ or players’ behaviors and responsibilities. 40 Furthermore, implementing responsible gambling measures at the financial institution level can alleviate the onus on consumers to establish safety protocols across various gambling platforms. This can be achieved by offering a centralized safety net across all sites where they play (assuming the same payment solution is used), managed through a single account at the payment solution level. Finally, the study can guide financial regulators and policymakers on reasonable responsibilities and obligations that could be implemented by financial institutions serving gambling customers.

Footnotes

1

Todd H. Baker & Corey Stone, Making Outcome Matter: An Immodest Proposal for a New Consumer Financial Regulatory Paradigm, 4

2

T. B. Swanton & S. M. Gainsbury, Gambling-Related Consumer Credit Use and Debt Problems: A Brief Review, 31 Current Opinion in Behavioral Science 21 (2020).

3

Addiction by Design, in

4

Priya Raghubir & Joydeep Srivastava, Monopoly Money: The Effect of Payment Coupling and Form on Spending Behavior., 14 Journal of Experimental Psychology

5

Thomas B. Swanton et al., Cashless Gambling: Qualitative Analysis of Consumer Perspectives Regarding the Harm Minimization Potential of Digital Payment Systems for Electronic Gaming Machines.,

6

Gainsbury & Blaszczynski, digital gambling payment methods: digital gambling payment methods: harm minimization policy considerations, 24 Gaming Law Review-Economics Regulation Compliance and Policy 466 (2020).

7

N. Muggleton et al., The Association between Gambling and Financial, Social and Health Outcomes in Big Financial Data, 5

8

M. Hilbrecht et al., The Conceptual Framework of Harmful Gambling: A Revised Framework for Understanding Gambling Harm, 9

9

Virve Marionneau, Michael Egerer & Susanna Raisamo, Frameworks of Gambling Harms: A Comparative Review and Synthesis, 31

10

N. Hing, A. M. T. Russell & A. Hronis, A Definition and Set of Principles for Responsible Consumption of Gambling, 18 International Gambling S

11

N. Hing et al., Demographic, Behavioural and Normative Risk Factors for Gambling Problems Amongst Sports Bettors, 32

12

X. L. Deng, T. Lesch & L. Clark, Applying Data Science to Behavioral Analysis of Online Gambling, 6

13

Nicola Adami et al., Markers of Unsustainable Gambling for Early Detection of At-Risk Online Gamblers, 13 International Gambling Studies 188 (2013); Julia Braverman & Howard J. Shaffer, How Do Gamblers Start Gambling: Identifying Behavioural Markers for High-Risk Internet Gambling, 22

14

Kasra Ghaharian et al., Players Gonna Pay: Characterizing Gamblers and Gambling-Related Harm with Payments Transaction Data, 143 Computers in Human Behaviour 107717 (2023).

15

N. Lakew, “Show Me the Money”: Preliminary Lessons from an Implementation of Intervention Tools at the Payment Gateway Level, 38

16

David Zendle & Philip Newall, The Relationship between Gambling Behaviour and Gambling-Related Harm: A Data Fusion Approach Using Open Banking Data,

17

Virve K Marionneau, Aino E Lahtinen & Janne T Nikkinen, Gambling among Indebted Individuals: An Analysis of Bank Transaction Data., 34

18

Julia Braverman & Howard J. Shaffer, How Do Gamblers Start Gambling: Identifying Behavioural Markers for High-Risk Internet Gambling, 22

19

Lakew, supra note 18.

20

Robert C. Merton & Richard T. Thakor, Customers and Investors: A Framework for Understanding the Evolution of Financial Institutions, 39

21

M. Losada-Otalora et al., Enhancing Customer Knowledge: The Role of Banks in Financial Well-Being, 30

22

R. Miller & G. Michelson, Fixing the Game? Legitimacy, Morality Policy and Research in Gambling, 116

23

Lakew N, Jonsson J, Lindner P. Towards an Active Role of Financial Institutions in Preventing Problem Gambling: A Proposed Conceptual Framework and Taxonomy of Financial Wellbeing Indicators. J Gambl Stud. (2024); doi: 10.1007/s10899–024-10312–8

24

David Barrett & Roberta Heale, What Are Delphi Studies? 23 Evidence-Based Nursing 68 (2020).

25

Coleen Toronto, Considerations When Conducting E-Delphi Research: A Case Study, 25

26

Adami et al., supra note 14; Deng, Lesch, and Clark, supra note 13.

27

S. M. Gainsbury et al., Reducing Internet Gambling Harms Using Behavioral Science: A Stakeholder Framework, 11

28

Lakew, supra note 18.

29

Kempson & Evans, New Zealand FWB Case Study, (2022).

30

Max Abbott et al., A Review of Research on Aspects of Problem Gambling, London: Responsibility in Gambling Trust (2004); Mary Tabor Griswold & Mark W. Nichols, Social Capital, and Casino Gambling in US Communities, 77 Social Indicators Research 369 (2006); Hilbrecht et al., supra note 7.

31

A. Furnham & H. Cheng, Socio-Demographic Indicators, Intelligence, and Locus of Control as Predictors of Adult Financial Well-Being, 5

32

Hilbrecht et al., supra note 8.

33

Adami et al., supra note 14; Braverman and Shaffer, supra note 14; Haeusler, supra note 14; Ghaharian et al., supra note 15.

34

E. C. Bruggen et al., Financial Well-Being: A Conceptualization and Research Agenda, 79

35

Lakew, N., Jonsson, J., & Lindner, P. Towards an Active Role of Financial Institutions in Preventing Problem Gambling: A Proposed Conceptual Framework and Taxonomy of Financial Wellbeing Indicators.,

36

Lakew, N., Jonsson, J., & Lindner, P. Probing the Role of Digital Payment Solutions in Gambling Behavior: Preliminary Results From an Exploratory Focus Group Session With Problem Gamblers,

37

Gainsbury and Blaszczynski, supra note 6; Thomas B Swanton, Sally M Gainsbury & Alex Blaszczynski, The Role of Financial Institutions in Gambling, 19

38

S. M. Gainsbury et al., Reducing Internet Gambling Harms Using Behavioral Science: A Stakeholder Framework, 11

39

Lakew, supra note 17.

40

L. Nower & J. Glynn, Adopting an Affordability Approach to Responsible Gambling and Harm Reduction: Considerations for Implementation in a North American Context, 6 Gaming Law review—Economics Regulations Compliance and Policy 466 (2022).

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.