Abstract

Vanadium is currently considered a critical material in the European Union, the U.S.A., and other jurisdictions. The vanadium mine production for 2021 is estimated at more than 120 000 tonnes; however, the market base is expected to grow rapidly due to the increase in the use of vanadium for redox flow batteries. Currently, world-wide, many projects are in the advanced stages of exploration and development. In the longer term, should vanadium cease to be a critical material and the law of supply and demand applies, the marginal mines will be decommissioned, and the best deposits will remain economic. Depending on the prevailing regulations in specific jurisdictions, geological settings, and the most up-to-date metallurgical research results, the main vanadium deposit types that could be considered as potential exploration and development targets are the vanadiferous titanomagnetite deposits, sandstone-hosted uranium-vanadium deposits (Salt Wash category), shale-hosted vanadium deposits, and base metal-related vanadate deposits. However, placer deposits, surficial uranium-vanadium type mineralisation, and the Minas Ragra type patrónite deposits should also be considered.

Introduction

We are living through tumultuous, and exciting times that represent extraordinary promotional opportunities for exploration and mining companies targeting materials required for reduction of greenhouse gas emissions by reducing our reliability on fossil fuels (Simandl et al. 2021). Vanadium is one of those materials. It belongs to the categories of ‘critical materials’ and ‘battery materials’ (U.S. Department of the Interior 2018 and European Commission 2020) and is predicted to benefit from high market growth projections because of its use in vanadium redox flow batteries (VRFBs) (Hund et al. 2020). Consequently, it is receiving a lot of attention from the exploration industry, governments, and the public. Since vanadium is also a ‘specialty material’ (i.e. global production does not exceed 200 000 tonnes per year), it is essential to consider the size of market base and the structure of the supply chain before and during the planning of exploration and development activities (Simandl et al. 2021). Environmental aspects and the circular economy are increasingly being considered (e.g. Kinnunen et al. 2022) and will have an increasing impact on the evaluation and planning of future projects. The high rate of anthropogenic enrichment of vanadium in the environment was brought forward by Watt et al. (2018). Of all the trace elements, vanadium has the highest and 4th highest anthropogenic enrichment factor in the atmosphere and global rivers, respectively (Viers et al. 2009; Schlesinger et al. 2017). At least partly because of this, and the increasing use of vanadium, most major jurisdictions, including the EU, U.S.A., and China are giving the environmental impacts of vanadium extra attention. For example, in the U.S.A., vanadium is one of the substances remaining on the fifth Contaminant Candidate List (CCL 5) issued by the United States Environmental Protection Agency (EPA) on July 19, 2021 (EPA 2021). The CCL identifies selected contaminants that are currently not subject to any national primary drinking water regulation but are known to occur in public water systems. These contaminants (including vanadium) may require future regulation under the Safe Drinking Water Act.

White and Levy (2021) touched upon the main sources of the vanadium released into the environment (mainly steel coproduction, 75%; crude oil processing related, 10%; and mining <10% of the total).

Today, approximately 88% of vanadium is produced from vanadiferous titanomagnetite ores (Rappleye and Haun 2021) including iron- and steel-slags, which represent more than 69% of the starting raw material in vanadium production (Lee et al. 2021). Historically, vanadium was also extracted from uranium-vanadium sandstone-hosted deposits in the U.S.A. and is currently, or was recently, extracted from related tailings solutions (Energy Fuels Inc. 2019). Combustion residues such as fly ash from coal-fired electricity generation plants (Sahoo et al. 2016; Rappleye and Haun 2021), fly ash from oil combustion (e.g. Navarro et al. 2007), and residues from crude oil refining and processing, represent examples of alternative vanadium sources. More research effort has recently been allocated to recovering vanadium from tailings and recycling (Wang et al. 2019; Petranikova et al. 2020) and to produce very high purity vanadium for specialised (niche) applications by electron beam melt refining of V–Al Alloys (Rappleye and Haun 2021).

The main objectives of this paper are to introduce the reader to the economic geology of vanadium and most importantly, discuss a selection of ore-deposit types as potential contributors to the future vanadium supply chain (as potential exploration and development targets). We achieve this by: (a) presenting background information on vanadium (physical, environmental, technical, political, criticality, market/use, and circular economy aspects; and (b) identifying potential exploration targets (deposit types).

Resources, uses, and market

Vanadium is the 22nd most abundant element in the continental crust and it accounts for approximately 0.014% of it (Rudnick and Gao 2003); however, concentrations of at least an order of magnitude higher, and preferably two orders of magnitude higher are required for the economic recovery of vanadium from ore deposits. Global vanadium resources and reserves are estimated at over 63 million tonnes and 22 or 24 million tonnes, respectively (sensu USGS; not according to NI-43-101, or JORC guidelines; Polyak 2021, 2022). The global annual mine productions for 2020 and 2021 are estimated at more than 105 000 tonnes and 110 000 tonnes of vanadium content, respectively (Polyak 2022). According to Polyak (2022), most of the known reserves, sensu USGS, occur in China (9.5 million tonnes), Australia (6 million tonnes), Russia (5 million tonnes), and South Africa (3.5 million tonnes). Many countries do not collect relevant data. For example, Canada, which is not recognised for its vanadium endowment, has more than 20 prospects and exploration/development projects where vanadium is listed either as the main product or co-product.

Currently, vanadium is used mainly as an alloying agent for iron and steel (>80%) with major market segments in the automotive and construction industries, as a titanium alloy additive, as a catalyst in sulphuric acid production, in battery applications (mainly VRFBs), and in other specialised applications (Polyak 2021). Manganese, Mo, Nb, Ti, and W may replace vanadium to some extent as alloying elements in iron and steel, while Pt and Ni can replace vanadium in applications where it is used for its catalytic properties. No good substitute is currently available for vanadium used in the production of aerospace titanium alloys (Polyak 2021). The VRFBs are used mainly in renewable energy storage where the energy density is not of prime importance and long lifespan and relative safety are required. Should shortage of high purity vanadium feedstock for VRFBs occur, other existing and developing technologies would become potential substitutes (Simandl et al. 2021); however, in short term, this is unlikely. Even under current market conditions, VRFBs are competing in renewable energy storage domain with other technologies such as pumped hydroelectric storage, compressed air energy storage, lead-acid, sodium-sulphur, and lithium-ion batteries (da Silva Lima et al. 2021).

Vanadium resources are not geographically constrained; however, the production of vanadium is. In 2020, China (61.6%), Russia (20.9%), South Africa (9.5%), and Brazil (7.7%) accounted for nearly all global vanadium production (Polyak 2021). It is notable that most vanadium is currently obtained as a byproduct from slags created during iron and steel production. This is likely to continue in the foreseeable future based on resource availability, metallurgical, environmental constraints, and the increasing importance of a circular economy.

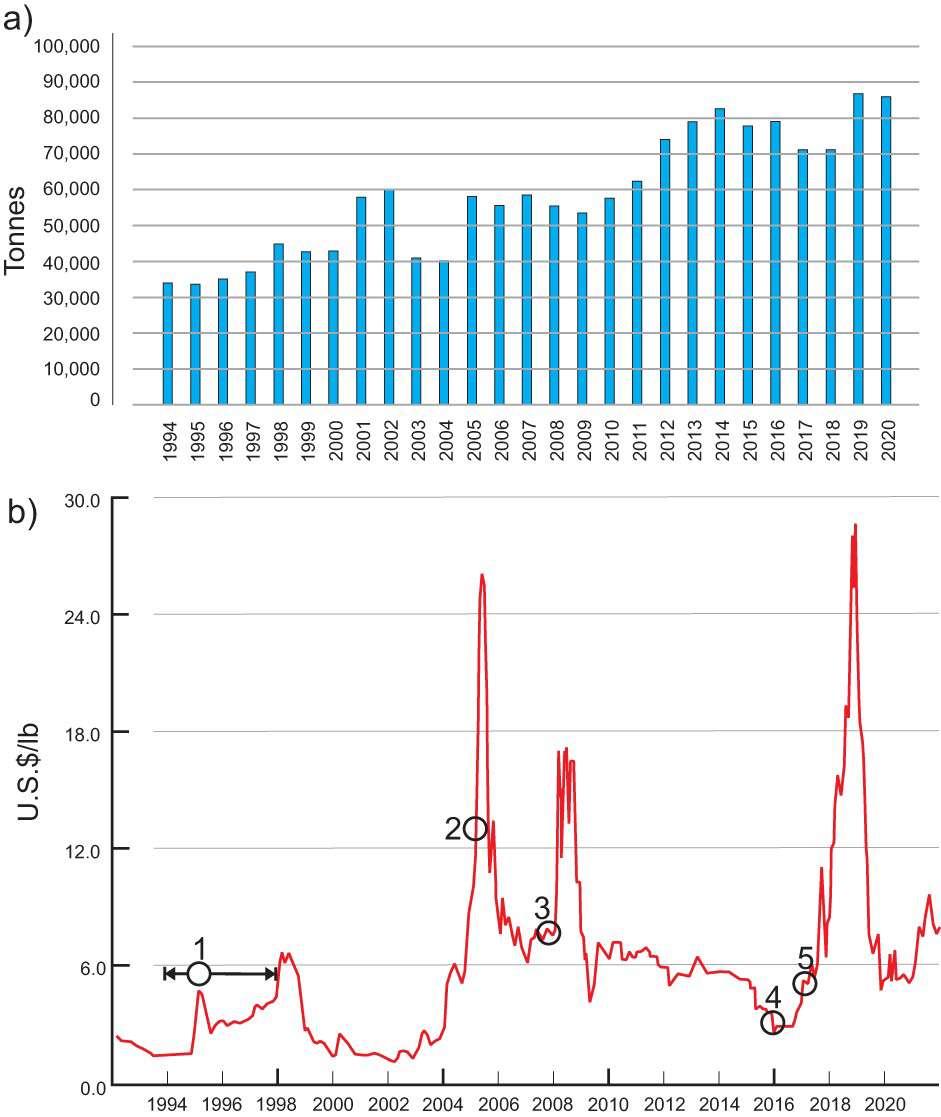

Historic variations in global mine production and V2O5 prices are shown in Figure 1(a, b), respectively. The gradual build-up of vanadium mine production from 1994 to 2003 resulted in an oversupply (Figure 1(a)). The reduction in global vanadium output in 2003 and 2004 reflects closures of the Windimura mine (Australia) and the Vantec mine (South Africa). The resumption of electric power shortages in South Africa (2008) and global economic downturn of 2009 resulted in a decrease in production. This was followed by a gradual increase in production from 2010 to 2014. The 2015 production drop reflects the closure of a major South African iron mine and closures of related vanadium-producing facilities in South Africa and Austria. A few Chinese vanadium producers had to shut down in 2017 following a series of environmental inspections. Updated regulations regarding high-strength steel in China were announced in February 2018; however, it appears that these regulations were not uniformly enforced across China (Polyak 2020), so the increase in demand for vanadium was less abrupt than originally anticipated. Years 2019 and 2020 were marked by an increase in production capacity in Brazil (Maracas Menchen Mine), and the reopening of the Vametco mine in South Africa (Bushveld Minerals Ltd.) and related production facilities.

Global vanadium mine production and prices. (a) Vanadium mine production (tonnes of contained vanadium) from 1994 to 2020. Data compiled from the USGS yearly commodity summaries. (b) Variation in prices of V2O5 from 1992 to 2021. Event 1 (Ev 1) – liquidation of the V2O5 from the U.S.A. strategic stockpiles; Ev 2 – Chinese vanadium steel standards are introduced; Ev 3 – rationing of electricity in South Africa reduces vanadium availability; Ev 4 – EVRAZ Highveld Steel and Vanadium Ltd. (S.A.) placed into receivership; Ev 5 China revises its standards for the tensile strength of rebar products – speculators expect vanadium shortages. Source of data: Vanadium Price.com (2021).

Because vanadium belongs to ‘specialty’ and ‘critical’ material categories (Simandl et al. 2021), the ferrovanadium and V205 prices are subject not only to variations reflecting the strength of the global economy, but also to wild fluctuations related to electric power shortages and weather conditions in vanadium producing regions, liquidations of stockpiles by major industrialised countries, shutdowns of individual production facilities, changes in government construction policies, levels of enforcement of environmental regulations, and a variety of other supply risks (Figure 1(b)). The ferrovanadium price fluctuations show the same pattern as V2O5.

Market projections

The Roskill (2021) report for 2021–2030 indicates that in the short term, the vanadium market is set to tighten as China's plants (those that are recovering vanadium from iron- and steel-slags) are running close to capacity. Numerous vanadium projects are at the planning stage or are currently under development. However, in the short term, outside of China and Russia, the increase in vanadium production is expected to come primarily from AMG Vanadium LLC's new facility in Ohio, U.S.A., and from Bushveld Mineral's Vametco operation, which is gradually increasing its production in South Africa. According to Roskill (2021), the use of vanadium as an alloying agent in steel will continue to dominate the market because of rising vanadium consumption in steel applications by emerging countries. There are also expectations of growing demand from the energy storage sector due to increased use of VRFBs (Hund et al. 2020; Roskill 2021; Simandl et al. 2021), and from the aerospace industry as it recovers from the impacts of the COVID-19 pandemic. These latter two applications are expected to generate an increase in demand for high-purity vanadium oxides (V2O5 or V2O3). New development projects are unlikely to significantly contribute to vanadium supply before 2024; however, the new International Maritime Organization's marine fuels regulation (which requires the reduction of sulphur content of ships’ fuel from 3.5% to 0.5%) is likely to create a new source of low-cost supply coming from oil spent catalysts (Roskill 2021). In the longer term, the study commissioned by the World Bank Group suggests that in 2050, the vanadium demand from the energy industry alone will represent between 175% and 250% of the 2019 global vanadium production (figure 4.3 in Hund et al. 2020). The study by International Energy Agency (2021) appears more conservative regarding commercialisation progress of VRFBs than the World Bank's study by Hund et al. (2020). Such differences in projections are not unexpected, and there is a need to continuously keep in mind ever increasing levels of research, incertitude associated with commercialisation, competing technologies, and the fact that a single major technological breakthrough could completely invalidate any long-term market projection in this domain (Simandl et al. 2021).

Main vanadium-bearing ore deposits

Four main deposit types from which vanadium was historically extracted, are currently produced from, or may be recovered from in the future are: (1) vanadiferous titanomagnetite (Figure 2(a)), (2) sandstone-hosted uranium-vanadium, (3) shale-hosted vanadium, and (4) vanadate deposits (Kelley et al. 2017; Brough et al. 2019). More detailed information for these four main vanadium-bearing deposit types, together with relevant examples are provided in the next four subsections. Remaining deposit types are described briefly in the section entitled “other deposit types”.

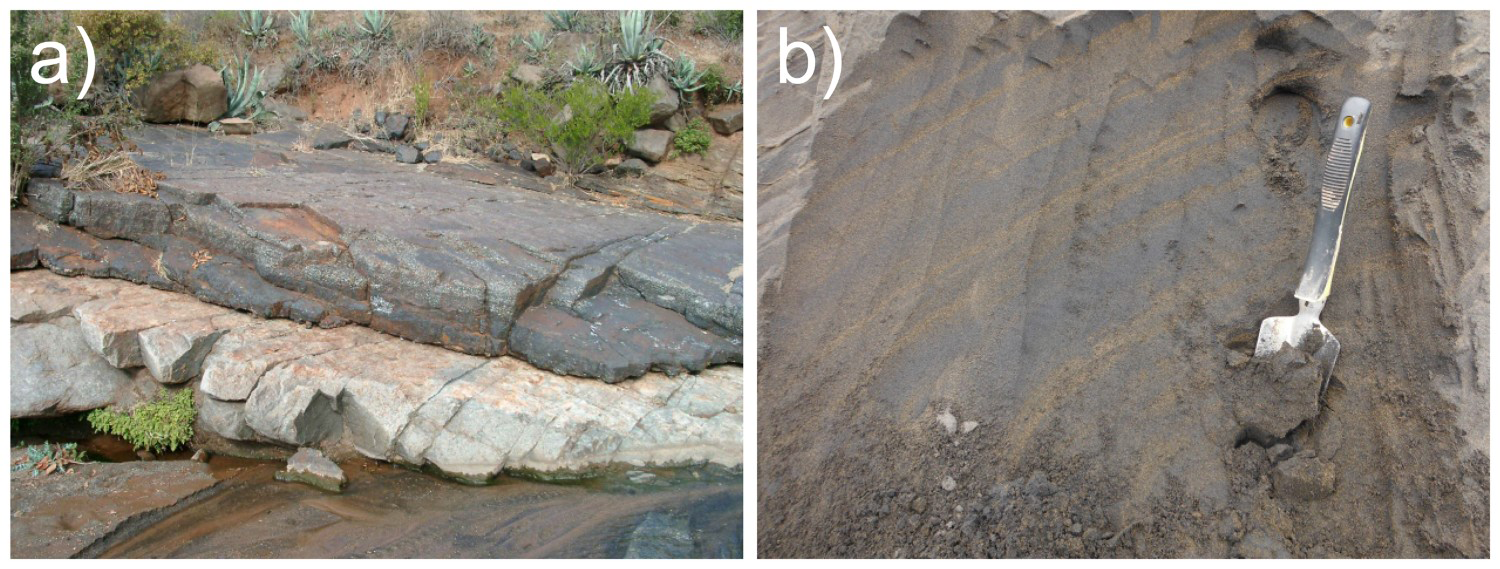

Vanadiferous titanomagnetite mineralisation; (a) Magnetitite Layer 1 (dark), approximately 30 cm thick, 2 m above the Main Magnetite Layer, Eastern Bushveld igneous complex, South Africa; photo curtesy of Paul, A.M. Nex; University of the Witwatersrand, South Africa. (b) Mine face exposing vanadiferous titanomagnetite (dark) in dune foreset bedding in the Waiuku Blacksand Member; scoop for scale;

Vanadiferous titanomagnetite deposits

Vanadiferous titanomagnetite deposits currently account for the bulk of raw materials for global vanadium production (Zhao 2002; Li et al. 2011; Gao et al. 2018). These orthomagmatic deposits (Figure 2(a)) are commonly hosted by, or associated with, layered mafic-ultramafic-igneous intrusions. Such intrusions are preferentially located in cratonic geotectonic settings (Maier et al. 2013) and there appears to be a broad geological time correlation between the ages of layered intrusions and amalgamation, and the breaking-up of the supercontinents (Smith and Maier 2021). Vanadiferous titanomagnetite sands (Figure 2(b)) are considered separately in the section entitled “other deposit types”.

A recent compilation of mafic-ultramafic layered intrusions worldwide (Smith and Maier 2021) indicates that from 565 inventoried intrusions, 74 contain stratiform Fe–Ti–V mineralisation and some also contain stratiform PGE reef-style mineralisation (107), Ni-Cu-(PGE) mineralisation (138), and/or chromitite seams (≥35), and several apatite deposits. While most of vanadium-bearing, titaniferous mineralisation in layered intrusions is concordant, discordant bodies are also known (e.g. Kennedy's Vale discordant body in the Bushveld Complex; Scoon et al. 2017).

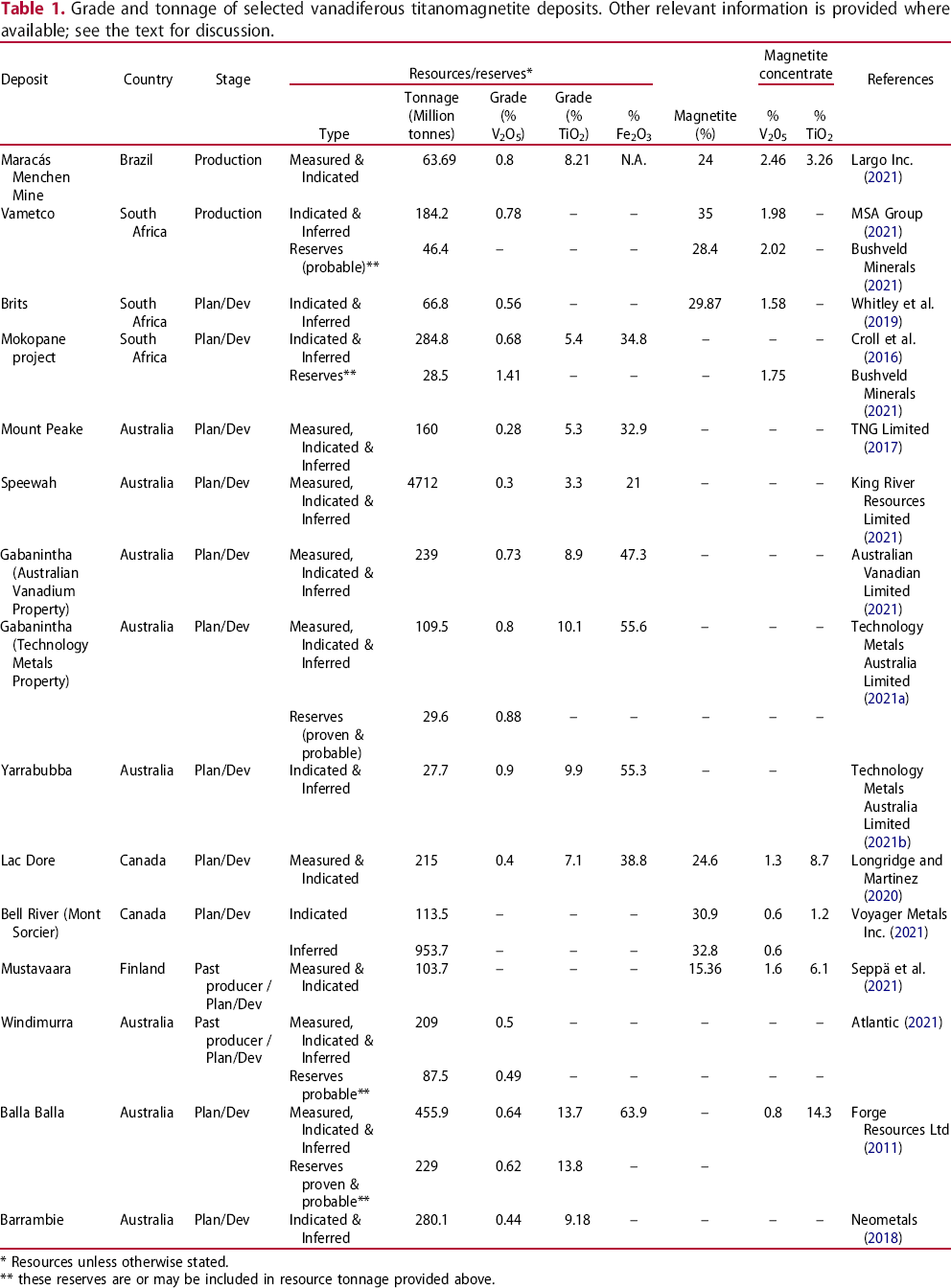

Grade and tonnage of selected vanadiferous titanomagnetite deposits. Other relevant information is provided where available; see the text for discussion.

* Resources unless otherwise stated.

** these reserves are or may be included in resource tonnage provided above.

Stratiform Fe–Ti–V oxide mineralisation is commonly located in the upper, more fractionated portions of mafic-ultramafic layered intrusions (e.g. Bushveld complex: Cawthorn and Molyneux 1986; Hughes et al. 2021; Smith and Maier 2021). However, this is not always the case. For example, the Rio Jacaré layered intrusion (Brazil) is reported to contain three Fe–Ti–V orebodies; two of them in the upper portion of the intrusion, and the third one in the lower portion of the intrusion (Sá et al. 2005).

The number, size, thickness, and grade of individual Fe–Ti–V layers vary from one intrusion to another and even within individual intrusions. For example, 16 Fe–Ti–V layers have been identified in the northern limb of the Bushveld complex (Barnes et al. 2004), and up to 26 layers were recognised in the eastern and western limbs of the same intrusion (Cawthorn and Molyneux 1986; Tegner et al. 2006). The oxide layers vary in thickness from few centimetres to >10 metres, some of them consisting almost entirely of vanadiferous titanomagnetite and ilmenite, whereas others contain substantial proportion of silicates (e.g. plagioclase and pyroxene) and anorthosite xenoliths. The Main Magnetite Layer (4th layer from the bottom in the eastern limb) is 1–2 m thick and historically accounted for more than half of the global vanadium yearly production (Crowson 2001). The magnetite layer 21 can reach a thickness of 60 m but is generally in the order of 10 m in thickness (Maier et al. 2013).

In contrast, at the Mustavaara Mine within the Koillismaa Intrusion (Finland), the 80 m thick mineralised zone was subdivided (based on grade) into ‘lower layer’ (5 m thick; 20–35 wt-% ilmenomagnetite), the ‘middle layer’ (15–50 m thick; 10–15 wt-% ilmenomagnetite), the upper layer (10–40 m thick; 15–25 wt-% ilmenomagnetite) and the upper-most ‘disseminated layer’ (<10 wt-% ilmenomagnetite). The term ‘ilmenomagnetite’ refers here to vanadiferous titanomagnetite containing fine ilmenite exsolutions (Karinen et al. 2015).

Vanadium is produced either directly from titanomagnetite ores and concentrates, or from the vanadium-enriched slags created by Fe or Ti extraction from smelting titanomagnetite ores (Gilligan and Nikoloski 2020). Vanadiferous titanomagnetite accumulation typically contain from 0.1 or 0.2% to 1% V2O5 (Cawthorn et al. 2005; Kelley et al. 2017), but in some cases their V2O5 content is higher. For example, the Highveld Steel and Vanadium Corp's past producing deposit, part of the Bushveld complex, had an average grade of 54.3% Fe, 1.6% V2O5 and 14.2% TiO2 (Taylor et al. 2006). Examples of grade and tonnage of selected vanadium-bearing titanomagnetite deposits with an established production track record or in an advanced stage of development are listed in Table 1.

Considering the V2O5 contents of the ore only, and neglecting related parameters, such as the vanadiferous magnetite content of the concentrate that can be successfully produced from the ore and the V2O5 content of the vanadiferous magnetite (mineral itself) during the relative ranking of these deposits, can lead to misleading or wrong conclusions.

Furthermore, in some of the deposits, V2O5 content of the vanadiferous magnetite grains is nearly constant, whereas in other deposits, non-negligible variations are observed depending on the sample location within the orebody.

When V2O5 content of titanomagnetite concentrate exceeds 1 wt-%, direct vanadium extraction could be considered (Gao et al. 2022). When V2O5 in the concentrate is below 1 wt-%, in a number of cases, vanadium can be economically extracted from the slag after iron is recovered. The V2O5 content of such slag may exceed 10% (Gao et al. 2018); however, commonly it is substantially lower. Thus, vanadium is, or potentially could be, directly recovered from Maracás Menchen Mine, Vametco, Brits, Lac Doré, and Mustavaara deposits, while Bell River deposit is a potential source of iron with the possible recovery of vanadium from related slag (Table 1). Serious efforts are underway, in the name of circular economy, to develop flux-less extraction methods that would lead to the recovery of all three valuable commodities (Fe, Ti, and V) from vanadiferous titanomagnetite ores (e.g. Geldenhuys 2020; Geldenhuys et al. 2020).

The origin of Fe–Ti–V deposits is still debated. A recent review paper on the possible origin of Fe–Ti–V layers (e.g. Figure 2(a)) subdivided proposed layer-forming processes into dynamic (syn-magmatic, hydrodynamic, and late- to post-magmatic) and non-dynamic (related to fluctuations in temperature, pressure, and oxygen fugacity, etc.) (Namur et al. 2015; Smith and Maier 2021). Bai et al. (2021) indicate that some of these deposits, such as the Hongge intrusion (35% Fe–Ti–V oxides) in southwest China, may have a different origin. According to Bai et al. (2021), these Fe–Ti–V oxide deposits formed in feeder conduits (open system) to large igneous provinces, where the silicates cotectic with Fe–Ti–V oxides occur as phenocrysts in basalts. However, a detailed discussion on this topic is largely outside the scope of this paper.

Because many mafic-ultramafic intrusions hosting classical Fe–Ti–V deposits also contain significant chromite, PGE, Ni, Cu, Co, apatite and other resources (e.g. Von Gruenewaldt 1993; Naldrett et al. 2012; Maier et al. 2013; Prevec 2018; Smith and Maier 2021), such intrusions represent geological environment with an exceptional multi-commodity exploration potential.

Sandstone-hosted uranium-vanadium deposits

Sandstone-hosted uranium deposits represent an important source of uranium and some of them are enriched in Au, Cr, Mo, Re, Sc, Se, Te, and V (International Atomic Energy Agency 2018). Globally, there are more than 1560 known sandstone-hosted uranium deposits, and deposits have been identified on all continents (International Atomic Energy Agency 2018). Sandstone-hosted uranium deposits are subdivided into (i) basal channel (173), (ii) tabular (∼880), (iii) roll front (457), (iv) tectonic-lithologic feature associated (32), and (v) related dykes/sills in Proterozoic sandstones (10) (International Atomic Energy Agency 2009, 2018, 2020; Abzalov 2012). Most tabular uranium deposits are Palaeozoic to Coenozoic in age (International Atomic Energy Agency 2020) and can be subdivided into (a) continental fluvial, uranium associated variety with intrinsic reductant, (b) continental fluvial, uranium associated variety with extrinsic bitumen (commonly referred to as ‘Grants District’ category), and (c) continental fluvial vanadium-uranium variety, commonly referred to in literature as ‘Salt Wash’ category (International Atomic Energy Agency 2018). The details of the genesis of sandstone-hosted deposits are beyond the scope of this study; however, for the most recent review covering key mineralisation controls, the reader is referred to Cuney et al. (2022).

The deposits of the Salt Wash category have higher vanadium contents than other sandstone-hosted uranium deposits, including Grants subtype deposits (Northrop et al. 1990; International Atomic Energy Agency 2009, 2018, 2020). Consequently, vanadium has been recovered from several deposits belonging to this category as a primary product, or as a co-product of uranium (Hansley and Spirakis 1992; Dahlkamp 2010; Kelley et al. 2017; Barton et al. 2018a).

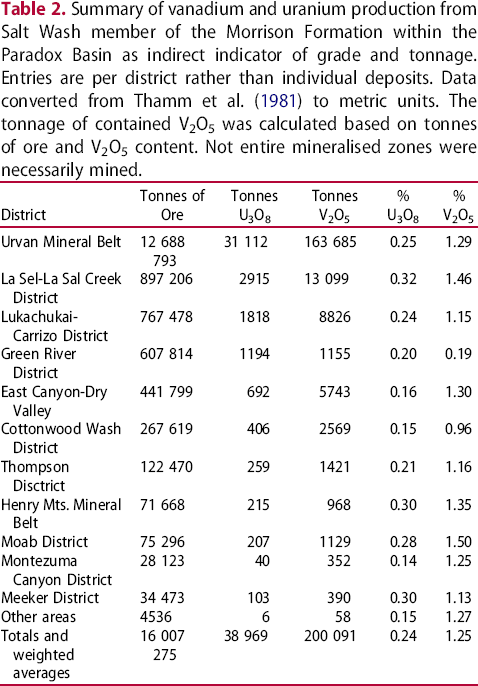

The Salt Wash category is named after the Salt Wash member of the Morrison Formation within the Paradox Basin, Colorado, U.S.A., which is hosted in selectively reduced (grey) continental fluvial sandstones within a sequence of continental red bed (oxidised) sediments. Distribution of vanadium-uranium mineralisation is mostly controlled by detrital carbonaceous (reducing) material and paleo-permeability and porosity within the sandstones. Individual, reduced, grey, organic material-rich zones enveloping vanadium-bearing zones are from 500 m to 4 km long, 50–300 m wide and up to 20 m thick. Vanadium-uranium deposits within these reduced zones are smaller and typically range from 100 to 500 m in length, 10–50 m in width, and 1–10 m in thickness (International Atomic Energy Agency 2009). Mineralisation commonly impregnates the sandstone matrix (Figure 3(a, b)) forming irregularly shaped lenticular masses oriented parallel to the bedding and following depositional trend within reduced (grey, lesivated) sediments. Consequently, the reserves of individual deposits rarely exceed 1 million tonnes of ore and are commonly much less (e.g. George R. Simpson and Gloria Emerson mines, Arizona; Chenoweth 2018). According to International Atomic Energy Agency (2018, 2020), individual deposits may contain from 1 to 2000 tonnes U grading 0.05–0.50% U, but the high vanadium content historically made these deposits attractive exploration and development targets. Vanadium-uranium weight ratios for the mineralisation of Salt Wash category range from 1:1 to 20:1 (Dahlkamp 2010) and deposits with the best potential for vanadium recovery generally exceed 1% V2O5 and some may have grades exceeding 2.5% V2O5 (Kelley et al. 2017). Because of large variations in grade and tonnage and in the vanadium-uranium ratio, and because several high-grade deposits of this type were artisanally-mined and records are not well preserved, Table 2 represents the most convenient way to show that under favourable conditions this deposit type may represent a viable exploration target. This table summarises the vanadium and uranium productions from Salt Wash member of the Morrison Formation within the Paradox Basin by district and indicates that uranium price may be a significant factor determining the desirability of this deposit type as a vanadium exploration/development target.

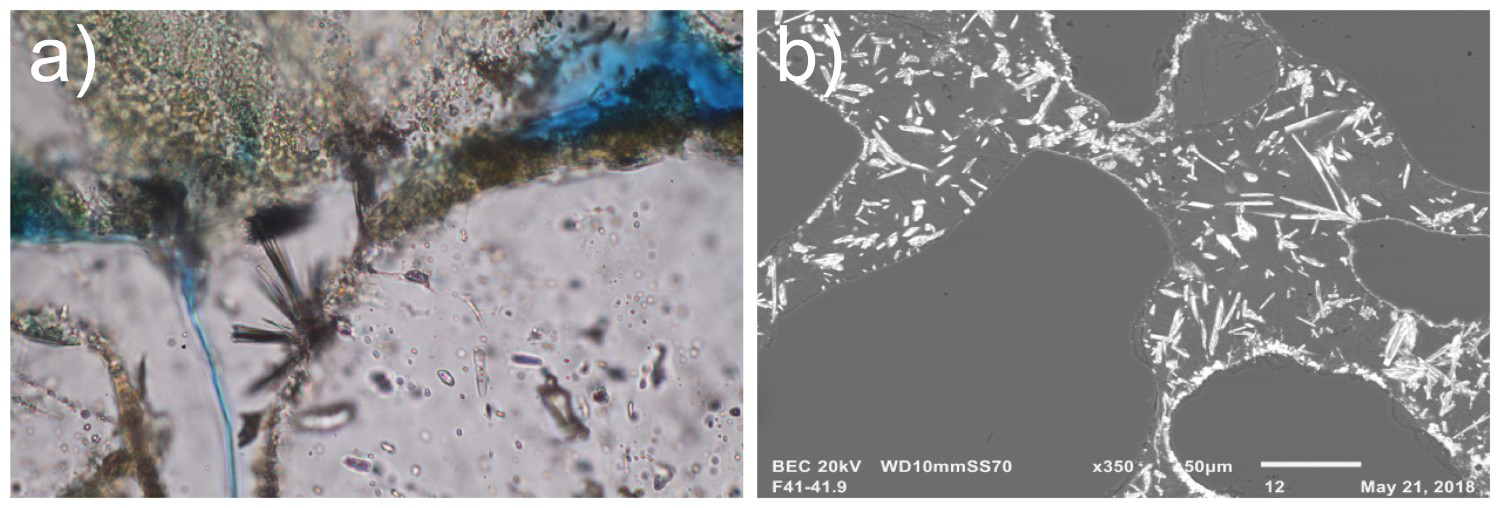

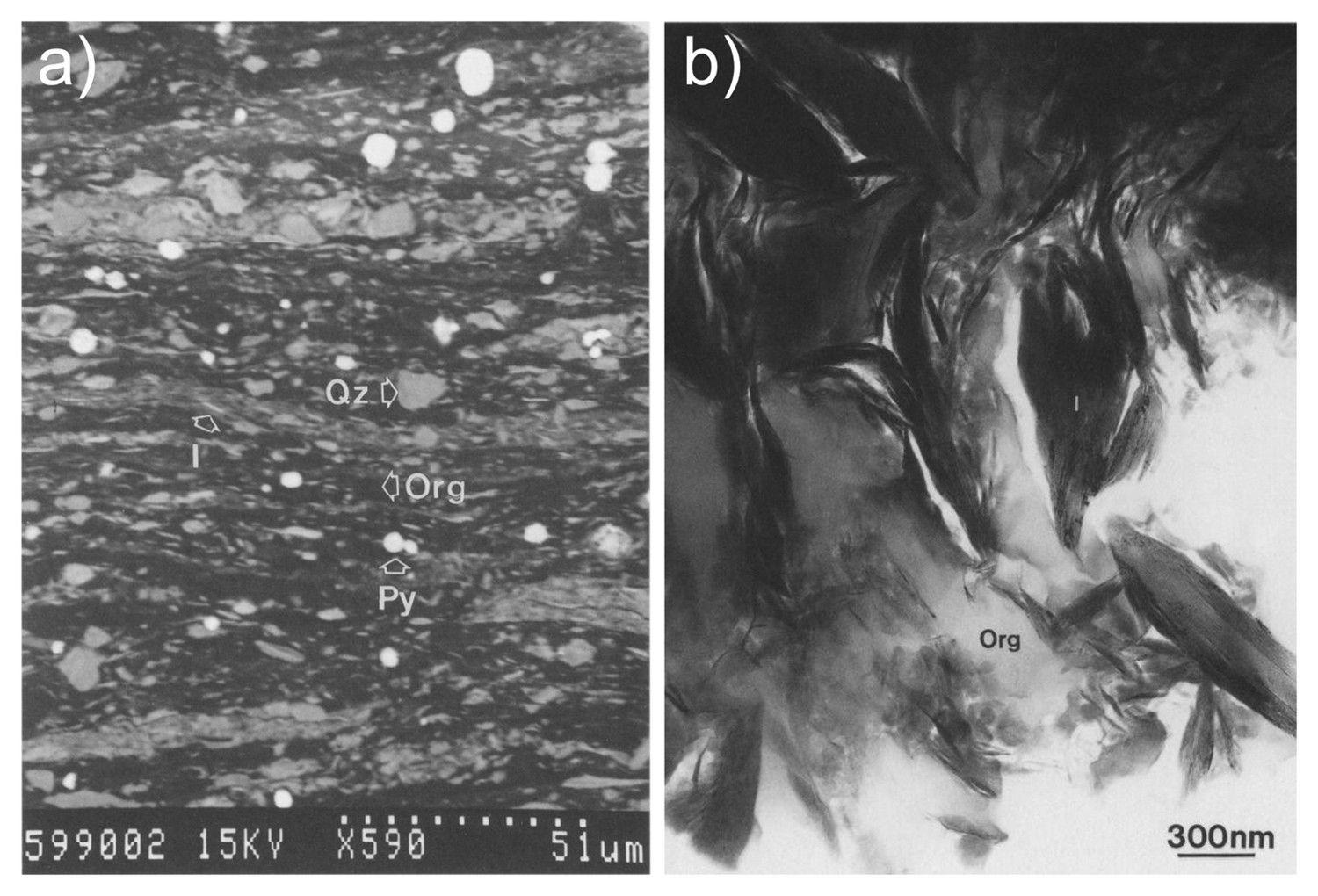

Salt Wash type vanadium-uranium deposit textures; (a) Montroseite needles growing on detrital quartz grain and forming inclusions in its euhedral overgrowth, 50× magnification, conoscopic light; vertical dimension of the photo is 150 microns; (b) Mixed montroseite and uraninite needles (possibly uvanite) in a matrix of vanadian chlorite, backscattered SEM image (from Barton et al. 2018a). Summary of vanadium and uranium production from Salt Wash member of the Morrison Formation within the Paradox Basin as indirect indicator of grade and tonnage. Entries are per district rather than individual deposits. Data converted from Thamm et al. (1981) to metric units. The tonnage of contained V2O5 was calculated based on tonnes of ore and V2O5 content. Not entire mineralised zones were necessarily mined.

The ore mineral assemblage in unoxidised mineralised zones consists mainly of uraninite (UO2), coffinite [U(SiO4)1-x(OH)4x], vanadian illite-smectite, roscoelite [K(V3+, Al)2(AlSi3O10)(OH)2], vanadian chlorite, montroseite [(V3+, Fe3+)O(OH)] and doloresite [V4+3O4(OH)4] (Meunier 1994; Shawe 2011). Where mineralised zones came into contact with oxidising meteoric waters, the original uranium mineralogy was at least partially converted to secondary uranium-vanadium bearing minerals (Chenoweth 1981; Shawe 2011) such as carnotite [K2(UO2)2(VO4)2·3H2O], tyuyamunite [Ca(UO2)2(VO4)2·6(H2O)] and pascoite [Ca2Ca(V10O28)·17H2O]. Vanadium-bearing clays, chlorite, and micas are the main vanadium minerals in both oxidised and unoxidised portions of Salt Wash category deposits.

Most of the well-documented examples of vanadium-uranium deposits where vanadium was/is recovered are in the Paradox Basin (Hansley and Spirakis 1992; Barton et al. 2018a) as summarised in Table 2. The Bigrlyi tabular sandstone-hosted U–V deposit, Ngalia Basin, Central Australia has also received significant attention (Schmid et al. 2020). The source of uranium in these deposits is widely accepted as originating from the leaching/weathering of igneous rocks; however, the timing of vanadium mineralisation, its source, and the nature of the mineralizing process, are still open for debate (Barton et al. 2018a, 2018b; Schmid et al. 2020).

The methods for extraction of vanadium and uranium from the Salt Wash category deposits are relatively well established and process flow charts from the cold war era are in the public domain (e.g. Merritt 1971; International Atomic Energy Agency 1993; Gao et al. 2022 and references herein). Where geological and hydrological conditions are appropriate, vanadium could also be recovered as a uranium co-product by in-situ leaching technologies assuming that it is environmentally acceptable (International Atomic Energy Agency 2001). Since 2018, the Energy Fuels’ White Mesa Mill (U.S.A.) was producing vanadium from solutions related to historic tailings (International Atomic Energy Agency 2020). However, it appears that all byproduct vanadium production in Utah ceased in early 2020 and was not restarted in 2021 (Polyak 2022).

Shale-hosted vanadium deposits

Black shales and bitumen contained within them are known to host anomalous concentrations of a variety of trace metals (Lewan and Maynard 1982; Huyck 1989; Hulbert et al. 1992; Coveney 2003; Jowitt and Keays 2011; Johnson et al. 2017; Gadd et al. 2019, 2020). Highly metalliferous black shales (HMBS), also known as hyper-enriched black shales (HEBS), are enriched in organic carbon and trace metals (e.g. Ni, Se, Mo, Ag, Au, Zn, Cu, Pb, V, As, Sb, Se, P, Cr, and U ± PGE) relative to common black shales (Johnson et al. 2017). These authors defined HMBS as shales where ∑Mo + Ni + Zn + Se + V > 1500 ppm. In comparison, the ∑Mo + Ni + Zn + Se + V for world average shale and average black shale are 280 and 434 ppm, respectively. According to this definition, globally, less than 5% of all known black shale stratigraphic units can be referred to as HBMS. The total organic carbon content of HMBS varies from 2 to 55 wt-%, averaging ∼10 wt-%, and their high S (1–10 wt-%) and P (500 ppm to 2 wt-%) contents overlap the upper limit of the black shale range (Johnson et al. 2017).

The elevated trace metals may have been introduced into HMBS through a variety of processes including detrital fraction related to continental weathering; trace metals assimilated by organisms which after their death accumulated in favourable reducing depositional settings; authigenic, seawater-derived metals incorporated into shales during diagenesis under redox conditions; interaction of metal-bearing hydrothermal brines with sediments during diagenesis, late hydrothermal (epigenetic activity); and any combination of above processes (Coveney 2003; Pagès et al. 2018; Henderson et al. 2019; Hints et al. 2021; Xu and Mao 2021, and references therein). Consequently, the trace element assemblages and the concentrations of enriched metals vary significantly by location and there is no universal explanation for these relationships. While there are hundreds, if not thousands, of studies addressing the origin of HMBS, there are only a few potentially economically mineable deposits under current market conditions outside of China. Despite its checkered mining history, the metamorphosed Talvivaara black schist-hosted Ni–Zn–Cu–Co (not producing V) deposit in Finland described by Kontinen and Hanski (2015) is probably the most important example currently in production outside of China.

The vanadium-bearing black shales of economic interest can be considered a subset of HMBS. They are found mainly in late Proterozoic and Phanerozoic marine successions and may contain more than 0.18 wt-% V2O5 and up to 1.7 wt-% V2O5 (Kelley et al. 2017). Regarding the origin of vanadium-rich horizons, recent research of black shales along the southeastern margin of the Yangtze Platform in South China suggests that these horizons formed under euxinic and intermittently suboxic to euxinic conditions at the basin slope, probably with some terrestrial input. Related, yet far less common, polymetallic (Ni-Mo-enriched) horizons are devoid of any signature of terrestrial input and appear to be constrained to iron-deficient euxinic conditions (Xu and Mao 2021). A recent study of the Alum Shale in Denmark, Sweden, Norway, and Estonia suggests that vanadium hyper-enrichment during the Lower Ordovician resulted from the upwelling of deep oceanic water (Bian et al. 2021). These examples, together with many other studies, clearly indicate that while there are fundamental similarities in the depositional environments, there may be more than one way to reach a favourable depositional environment for the formation of hyper-vanadium-enriched black shales.

In common geological settings, vanadium (V3+) substitutes for Al in the octahedral sites of 2:1 phylosilicates such as roscoelite (Gaines et al. 1997; Peacor et al. 2000), smectite, illite-smectite, illite, and muscovite (Meunier 1994; Peacor et al. 2000); however, more recently, it became evident that some shales consisting of trioctahedral mica such as phlogopite and biotite may also contain high concentrations of vanadium (Zheng et al. 2019). Besides some of the previously mentioned minerals, patrónite, chernykhite [phyllosilicate, muscovite subgroup (Ba, Na)(V3+,Al)2(Si, Al)4O10(OH)2], and phengite were reported as vanadium-bearing minerals at the Balasauskandyk V–Mo–U deposit in Kazakhstan (Komekova et al. 2017). Furthermore, vanadium is also found as V4+ in organic material attached on sedimentary particles (Breit and Wanty 1991) and depending on the nature of the thermal stability of organic material, vanadium may remain associated with organic material during diagenesis and low-grade metamorphism (Zhang et al. 2015). For example, at Mecca Quarry Shale at Velpen, Indiana (Figure 4(a, b)), illite is reported to account for 65% of the vanadium, whereas organic material accounts for the remaining 35% (Peacor et al. 2000). There is a lot of scientific speculation regarding the processes by which vanadium was incorporated into metalliferous black shales, as discussed by Peacor et al. (2000) and Hints et al. (2021). The effect of weathering distribution of vanadium on vanadium-bearing black shales is important, but not well-documented. Uncommon vanadium oxysalts [metahewettite (CaV6O16·H2O), bokite (KAl3Fe6V26O76·30 H2O)], compound phosphate minerals [schoderite (Al2PO4VO4·8 H2O), and metaschoderite (Al2PO4VO4·6–8 H2O)] were reported in oxidised zones of the Gibellini project (Hanson et al. 2018). At the Julia Creek vanadium deposit (Queensland, Australia) hosted by the Cretaceous organic-rich Toolebuc Formation, most of the vanadium (60%) was remobilised and incorporated into Fe oxide and oxyhydroxide phases during the supergene enrichment (Lewis et al. 2010).

Mecca Quarry Shale; (a) BSE image of a thin section. Bright round objects are pyrite (Py) framboids, black material is kerogen (Org). Most material of intermediate contrast is detrital quartz (Qz) and illite (I); (b) transmission electron microscopy (TEM) image showing the textural relationship between kerogen (Org; light grey), and authigenic V-rich illite (from Peacor et al. 2000).

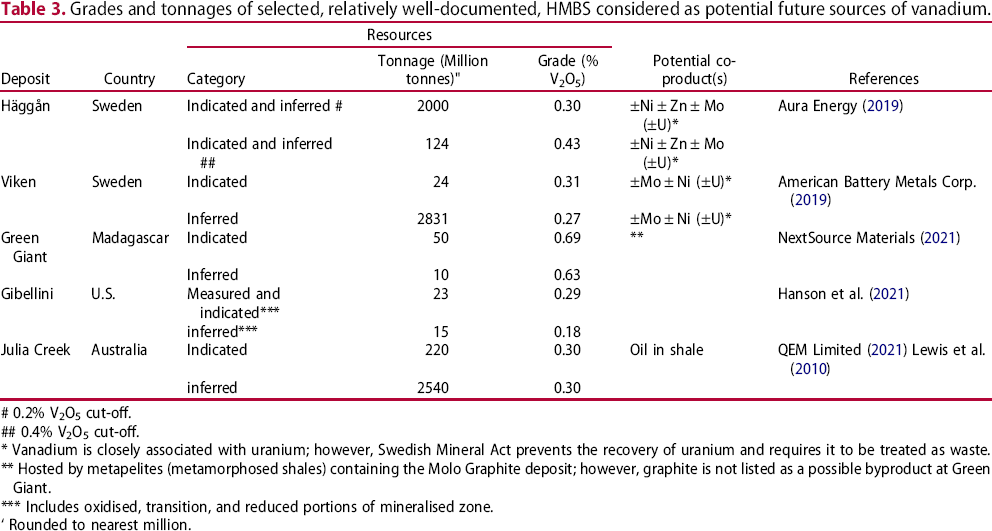

Grades and tonnages of selected, relatively well-documented, HMBS considered as potential future sources of vanadium.

# 0.2% V2O5 cut-off.

## 0.4% V2O5 cut-off.

* Vanadium is closely associated with uranium; however, Swedish Mineral Act prevents the recovery of uranium and requires it to be treated as waste.

** Hosted by metapelites (metamorphosed shales) containing the Molo Graphite deposit; however, graphite is not listed as a possible byproduct at Green Giant.

*** Includes oxidised, transition, and reduced portions of mineralised zone.

‘ Rounded to nearest million.

Vanadiferous black shales represent the largest vanadium resource in China (Li et al. 2010) and their vanadium content typically varies between 0.13% and 1.2% V2O5 (Qi 1999), leading to numerous attempts to extract commercially vanadium from black shales. Most of these attempts were at a small scale (less than 100 tonnes of V2O5 per year), focused on weathered ores (Zheng et al. 2019), and took place during periods of high vanadium prices and fewer environmental regulations relative to western industrialised countries (Zhang et al. 2011). The recovery of vanadium from black shales, which is commonly referred to by Chinese authors as ‘stone coal’ (Dai et al. 2018), was based on a roasting process emitting HCl and Cl2 into the environment (Li et al. 2010). A summary of the extraction methods used during those time periods is provided by Zhang et al. (2011). The intensity of ongoing research in this domain by China (e.g. Wang et al. 2020; Chen et al. 2021) and other countries (e.g. Olson 2019) combined with the fact that most of the previously mentioned Chinese plants closed suggests that an ideal method for extracting vanadium from shales at a commercial scale has not yet been developed, is not considered cost-competitive under current market conditions, or is not compatible with current environmental regulations in western industrialised countries. This assessment agrees with the most recent review by Li et al. (2021).

To our knowledge, currently there is no commercial vanadium recovery from black shales outside of China. There are very few authoritative studies addressing actual proportions of vanadium in aluminosilicates and in organic material from vanadium-rich shales. Many site-specific metallurgical, geological, and even review studies either sidestep this issue, do not discuss this issue, or simply assume that most, if not all vanadium are in phyllosilicates. However, this is not the case at the Mecca Quarry Shale (Indiana, U.S.A.; Peacor et al. 2000) and more importantly at the Gibellini vanadium project (Nevada, U.S.A.). The Gibellini project appears to differ significantly from most of the other above-listed deposits in terms of vanadium distribution. In the reduced portion of the Gibellini deposit, the vanadium is found largely in organic material consisting of fine-grained (<15 µm), flaky, and stringy organic fragments, while in the oxidised portion of the deposit, metahewettite, bokite, schoderite, and metaschoderite occur as fracture fillings (Hanson et al. 2018). Surprisingly, based on preliminary metallurgical studies, the highest recovery rates are expected from the transition zone separating the oxidised and reduced zones. The envisaged extraction process consists of heap leaching and solvent extraction followed by acid stripping and precipitation of final product (Hanson et al. 2018).

The development of the first successful operation extracting vanadium from a given vanadium-rich shale outside of China will require innovation, perseverance, and pioneering spirit. Determining if the vanadium is predominantly contained in phyllosilicates, compound phosphates, vanadium oxysalts, iron oxides, and oxyhydroxides or organic materials is essential before attempting to select the optimal extraction method for any given project and for project ranking according to development potential. Furthermore, the studies by Zheng et al. (2019) suggest that the distinction between shales consists of specific vanadium-bearing phyllosilicates such as dioctahedral mica (e.g. muscovite and illite) and trioctahedral mica (e.g. phlogopite and biotite) will be important, especially in the case of unweathered ores.

Base metal vanadate deposits

Base metal vanadate occurrences are characterised by lead-, zinc-, and copper-vanadate minerals in the oxidised portions of base metal deposits. They share spatial and genetic similarities with classical Pb–Zn supergene nonsulphide carbonate-hosted base-metal occurrences (Boni and Large 2003; Hitzman et al. 2003) which are relatively widespread (Fischer 1975). The classical carbonate-hosted Pb-Zn nonsulphide deposits do not contain abundant vanadate minerals. They are found in both arid and tropical environments/paleo-environments; however, many of the best supergene nonsulphide deposits recognised to date formed in semi-arid environments, and some are found in cold, wet climates at higher latitudes (Paradis and Simandl 2011). Where base metal vanadates occur within the mineralised nonsulphide zone, they appear to post-date both sulphide and nonsulphide base metal-bearing minerals. The vanadium required for crystallisation of vanadates is commonly believed to be brought in by late supergene fluids; however, the provenance of vanadium is not universally agreed upon.

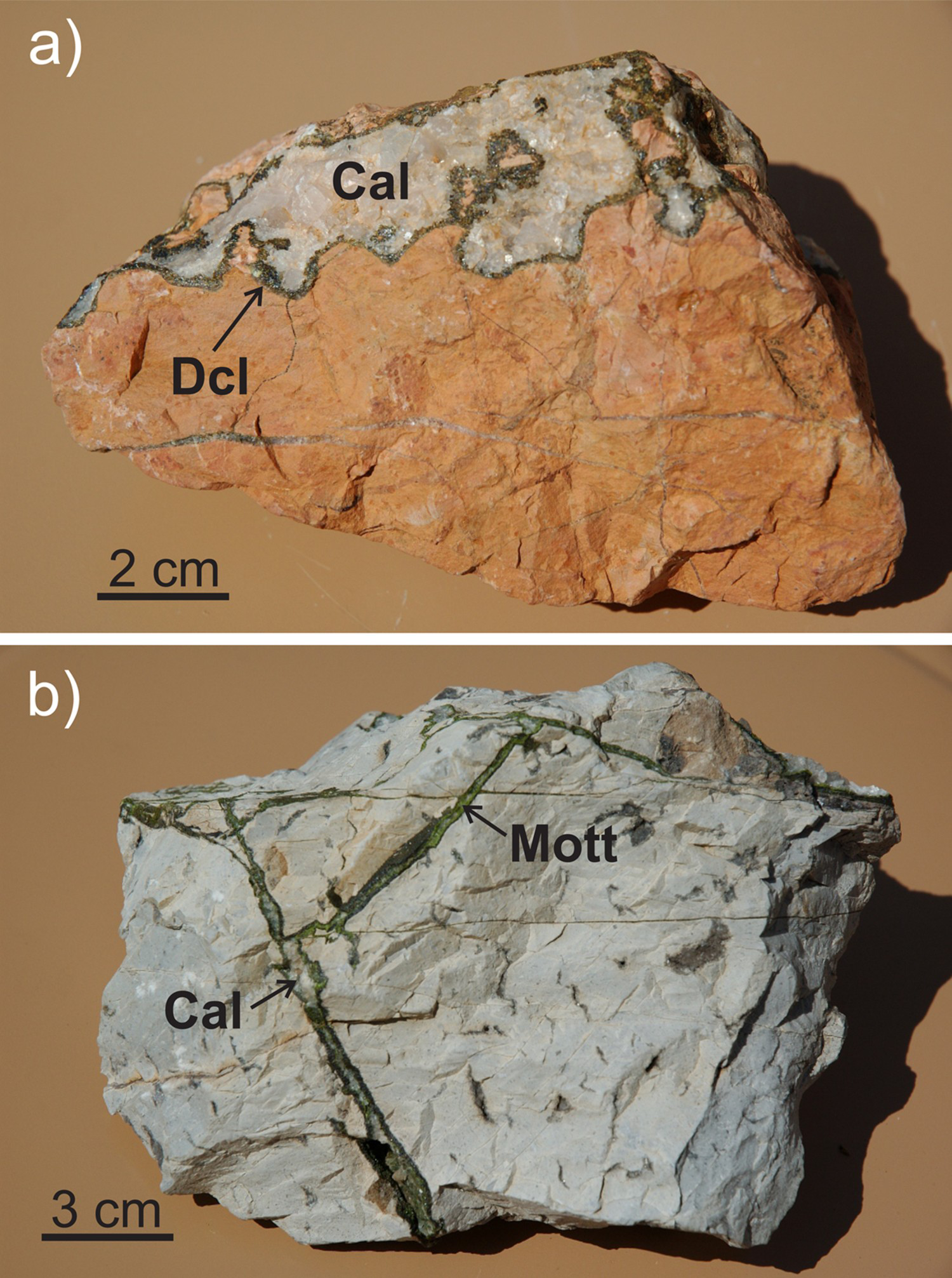

Deposits of the Otavi Mountainland, Namibia, hosted by Neoproterozoic carbonates of the Abenab and Tsumeb Subgroups of the Otavi Group in the Damara Supergroup (Boni et al. 2007; Kamona and Gunzel 2007) are the best-known examples of base metal vanadate mineralisation. They were first mined in 1919, with increasing production between 1943 and 1960 (Wartha and Schreuder 1992). Most vanadium mineralisation in the Otavi Mountainland is spatially associated with (overly) primary sulphide and nonsulphide Pb-Zn carbonate-hosted deposits, or other base metal deposits. Most prior Zn–Pb–V production came from the Berg Aukas and Abenab West dolostone-hosted deposits forming stratiform lenses, breccia zones, and cavity fillings (Figure 5(a)). The remaining ore reserves at Berg Aukas were reported to be at 1.65 million tonnes grading 17% Zn, 5% Pb and 0.6% V2O5 (Misiewicz 1988). The Abenab West deposit was a stratiform karst zone consisting mainly of nonsulphide Pb-Zn minerals, secondary copper minerals, descloizite, and vanadinite within unconsolidated, ferruginous clay (red mud) containing quartz and detrital galena (Boni and Large 2003) filled with fragments of collapsed country rocks and compacted red muds, cemented by coarse calcite and descloizite-vanadinite concretions. From 1939 to 1958, it supplied more than 50 000 tonnes of Pb, 5000 tonnes of V and an unknown quantity of Zn concentrates (Kamona and Gunzel 2007, and references herein). The pertinent geological information on these and other deposits in the Otavi area is summarised by Boni et al. (Boni and Large 2003; Boni et al. 2007) and Kamona and Gunzel (2007).

Base metal vanadate mineralisation from Otavi Mountainland, Namibia; (a) Cavity filled with descloizite (Dcl) crystals and sparry calcite (Cal) in limestone of the Maieberg Formation from the Okorundu pit, west of the Abenab mining area (Boni et al. 2007); (b) Veinlets of mottramite (Mott; green) and calcite (Cal; white) cutting the dolostone of the Hüttenberg Formation at Gross Otavi vanadium occurrence (from Boni et al. 2007).

The spatial association between vanadium mineralisation and nonsulphide Pb-Zn deposits in combination with field observations, textures, and mineral paragenesis led to the conclusion that the vanadium mineralisation in the Otavi Mountainland was supergene in origin, a hypothesis supported by studies from Boni et al. (2007) and Kamona and Gunzel (2007). According to Bannister and Hey (1933) and Palache et al. (1951), the vanadate mineralisation of the Otavi Mountainland commonly consisted of mineral species belonging to the isomorphic series between descloizite [PbZn(VO4)(OH)] and mottramite [PbCu(VO4)(OH)] and to a lesser extent vanadinite [Pb5(XO4)3Cl], where X represents the elements P, As, and V (Figure 5(b); from Boni et al. 2007). Also in the Otavi Land area, the Abenab vanadium deposit, hosted by the carbonate rocks of the Maieberg Formation which belongs to the Tsumeb Supergroup, produced 1.85 million tonnes of ore averaging 1.03% V2O5 (Cairncross 1997). The deposit is described as a cylindrical breccia pipe consisting of descloizite and vanadinite cemented by calcite (Kamona and Gunzel 2007). Other examples of the vanadate-bearing deposits include Kabwe Mine (formerly known as ‘Broken Hill’), Zambia (Skerl 1934; Taylor 1954; Southwood et al. 2019) and Kihabe Zn–Pb–V prospect, Botswana (Mondillo et al. 2020). The Kabwe Mine and related processing plant operated from 1906 to 1994 and produced 0.8 million tonnes of Pb, 1.8 million tonnes of Zn with silver (79 tonnes), V2O5 (7820 tonnes), cadmium (235 tonnes) and copper (64 tonnes) as a byproduct (Kamona and Friedrich 2007). The Kabwe area in Zambia is currently considered as one of the most polluted sites in the world, due largely to wind dispersion of dust from extensive piles of slag (Baieta et al. 2021). Non-African examples are the St. Anthony mine in Arizona (644 tonnes of vanadium, 1934–44; Fischer 1975), and Los Lamentos and San Antonio mines in Mexico (211 tonnes of vanadium, 1938–40; Fischer 1975).

Within relatively well-documented deposits of the Otavi Mountainland, vanadium was present only in the nonsulphide portions of the mineralised zones and is suspected to have been introduced into the nonsulphide Pb–Zn zones from outside by late supergene or hypogene fluid.

The most likely sources of vanadium were the siliciclastic country rocks, or mafic rocks of the underlying Paleoproterozoic basement (Boni et al. 2007). The need for external source of vanadium, in combination with a slightly higher temperature of formation for vanadates than for coexisting Zn–Pb–Cu nonsulphides, as suggested by stable isotope studies mentioned by Boni et al. (2007) may explain why vanadates are relatively uncommon in association with nonsulphide base metal deposits in other parts of the world.

The discovery of high-grade, large tonnage Pb–Zn vanadate mineralisation is not expected to happen by the exploration community; however, the possibility of a new discovery cannot be entirely discounted. In the meantime, efforts are underway to optimise the methods for the production of vanadium concentrate from small lead vanadate deposits (Silin et al. 2020a), metallurgical treatments of lead vanadate ores (Silin et al. 2020b), and potential recovery of vanadium from historic slags produced by smelting of African Pb–Zn ores (Ettler et al. 2020).

Other deposit types

As indicated by Kelley et al. (2017), vanadium was also reported in anomalous concentrations in a variety of ore deposit types including gold-telluride quartz veins (e.g. Mueller and Muhling 2020) and surficial uranium deposits. Surficial deposits are described by the International Atomic Energy Agency (2020) as mostly Tertiary to recent, near-surface uranium occurrences in sediments and soils and they share a number of similarities with sandstone-hosted uranium-vanadium deposits. The largest of the surficial uranium deposits are calcrete-hosted and occur in valley-fill sediments along drainage channels and in playa-style sediments in areas of deeply weathered, uranium-rich granites. Good examples of such surficial uranium deposits with significant vanadium content are Langer Heinrich uranium mine in Namibia (Hartleb 1988; Iilende 2012; World Nuclear News 2019), Amarillo Grande and Laguna Salada projects in Argentina (de Klerk et al. 2014; Edwards 2020), and Southern High Plains physiographic region in U.S.A. (Hall et al. 2019).

Heavy mineral sands (‘iron sands’) in New Zealand (Figure 2(b)), derived by weathering and sedimentary processes from volcanic rocks (Brathwaite et al. 2021), are a valuable source of vanadiferous titanomagnetite used by New Zealand Steel (2021a, 2021b) to produce iron and vanadium-bearing slag. Heavy mineral sand/placer deposits in other parts of the world may also contain recoverable vanadium resources (Perks and Mudd 2021). New discoveries, similar to high-grade Minas Ragra type patrónite (vanadium sulphide)-bearing deposit, Peru, described by Hillebrant (1907) and Lamey (1966), should not be discounted. The recovery of vanadium and/or other elements (e.g. REE, yttrium, and uranium) as byproducts of phosphoric acid from phosphate rock has been proposed many times in the past; more recently by Chen and Graedel (2015). While such recoveries are theoretically and technically possible (Weterings and Janssen 1985) and favourably looked upon from the circular economy and environmental points of view, it remains to be seen if such efforts are justifiable even after environmental and criticality benefits are accounted for, under current market conditions.

Summary

When located in favourable geopolitical and environmental settings near developed infrastructure and sources of inexpensive energy, vanadiferous magnetite, sandstone-hosted uranium-vanadium, shale-hosted vanadium, and lead-zinc–copper vanadate deposits may be acceptable exploration targets (Table 1).

Most vanadium is currently produced from vanadiferous titanomagnetite deposits hosted in mafic-ultramafic layered intrusions; extraction may be directly from vanadiferous titanomagnetite concentrate, or from vanadium-enriched slags. Some producers outside China exploiting this type of deposit currently have the flexibility to increase their production levels. Several known deposits of this type which are currently under exploration, or in development outside of China may come into production within the next 3 years. The reactivation of historic mines (e.g. Mustavaara V–Fe–Ti mine, Finland, which closed in 1985 due to low vanadium prices; Taipale 2013) represents additional options. Vanadiferous titanomagnetite deposits represent an attractive exploration and development target because they have relatively high grades and tonnages, vanadium extraction technology from vanadiferous magnetite is well-established, and because, a well-designed exploration programme targeting this deposit type may also result in the discovery of significant Ni, Cr, and PGE deposits within the same intrusive complex.

Tabular, Salt Wash type, sandstone-hosted uranium-vanadium deposits were historically a significant source of both vanadium and uranium and significant resources were identified outside of U.S.A. Depending on the future uranium and vanadium market conditions, they may become a highly sought-after exploration and development targets once again. However, most of the deposits where vanadium was (or is) successfully extracted as a byproduct of uranium have relatively small vanadium ore reserves in comparison to currently producing vanadiferous titanomagnetite type and some vanadium-rich black shale type deposits. This deposit type is a non-ideal exploration and development target in jurisdictions that have strict restrictions or a moratorium on uranium exploration or production. On the positive side, these deposit types typically occur in clusters and belts, respond well to inexpensive radiometric surveys, and where environmentally permissible, could be exploited by in-situ leaching technologies.

Vanadium-rich black shales, a subset of HMBS, represent the largest Chinese, and possibly global, vanadium resources. Under current market conditions and environmental constraints however, they represent a very small fraction of vanadium mine production. If ongoing intensive research into the optimisation of extracting vanadium from these rocks (currently concentrated in China based on the number of recently published scientific papers) is successful, and related environmental concerns are addressed, this deposit type may become truly competitive with the mafic-ultramafic layered intrusions vanadiferous titanomagnetite deposits. If the development of vanadium-bearing black shales goes ahead, in many cases, vanadium is likely to be a co-product of other metals. Important aspects in the early ranking of vanadium-rich black shales projects (relative to each other) are the mineralogy of the deposit, and the proportions of the vanadium within the crystal structure of minerals, to that adsorbed to mineral particles, and that found within or adsorbed to organic material (as was attempted for the Gibellini project). This has important implications on the need for ore sintering, the selection of vanadium extraction method, rate of recovery, and consequently, extraction costs.

Copper–lead–zinc vanadate deposits were historically, a significant source of vanadium. These deposits are spatially and genetically linked to traditional sulphide or nonsulphide base metal deposits (predominantly carbonate-hosted). They are not recommended as primary exploration targets; however, these deposits may be considered as valid secondary exploration targets within exploration programmes targeting sedimentary rock-hosted Cu–Pb–Zn-bearing sulphide and/or nonsulphide deposits assuming appropriate climatic or paleo-climatic settings.

Other deposit types that are potential vanadium sources that explorationists should be aware of are surficial vanadium-bearing uranium deposits (e.g. Langer Heinrich, Namibia), and high-grade patrónite-bearing deposits (e.g. Minas Ragra, Peru). The concepts and technical parameters used in project evaluations such as vanadium resource availability, market base, market projections, environmental aspects, social aspects, all technical economic aspects related to exploration and development (e.g. availability of infrastructure, ore tonnage/grade, proximity to the surface, geometry of the deposit, and mining, processing, and waste disposal aspects) remain extremely important in the traditional ranking of exploration and development projects under free market conditions.

Because vanadium is considered a ‘critical’, ‘battery’, and ‘specialty material’ (sensu Simandl et al. 2021), at least in some western jurisdictions, free-market conditions may not apply or could be curtailed to some extent by government initiatives and long-term contracts between producers and end-users to secure reliable supply chains. Furthermore, as the concept of the circular economy is increasingly evoked by governments, financial institutions, and multinational companies, projects involving recycling, and the rehabilitation of historic mines and processing sites (tailings and mine waste dumps) may benefit from preferential treatment by funding agencies. These aspects cannot be ignored during the short-term ranking of projects according to their development potential. However, history has shown us that in the long term, current geopolitical tensions and conflicts will subside and the law of supply and demand will be re-established. Therefore, regardless of current hype, fundamental technical and economic aspects of traditional project ranking should not be ignored, and development efforts should be concentrated on technically and economically sound projects located in stable, mining-friendly countries.

Footnotes

Acknowledgements

The earlier version of this manuscript benefited from editing by Laura Simandl from RDH Building Sciences Inc., Victoria, British Columbia, Canada. Johnathan Savard from the British Columbia Ministry of Energy, Mines and Low Carbon Innovation, Victoria, British Columbia, Canada, helped with the preparation of the tables and formatting of the document.

The authors are grateful to Dr David Huston (Geoscience Australia. Canberra) and two anonymous reviewers for their comments and suggestions and to the editor, Dr Simon Jowitt (University of Nevada, Las Vegas) for editorial handling of the manuscript. Dr Paul A.M. Nex, Associate Professor and director EGRI, School of Geosciences, University of the Witwatersrand, Johannesburg, SA; Dr. Isabel F. Barton, Department of Mining and Geological Engineering, University of Arizona, Tuscon, Arizona; Dr Donald R. Peacor, Department of Geological Sciences, University of Michigan, Ann Arbor, Michigan, USA; Dr Maria Boni, Professor, University Napoli, Naples, Italy; and Dr Anthony B. Christie, GNS Science, New Zealand are thanked for granting permission to use their photographic documentation. NRCAN contribution number: 20220188.

Disclosure statement

No potential conflict of interest was reported by the authors.