Abstract

Metaphorically, altruistic acts, such as monetary donations, are said to be driven by the heart, whereas sound financial investments are guided by reason, embodied by the head. In a unique experiment, we tested the effects of these bodily metaphors using biofeedback and an incentivized economic decision-making paradigm. Participants played a repeated investment game with a simulated partner, alternating between tactical investor and altruistic investee. When making decisions, participants received counterbalanced visual feedback from their own or a simulated partner’s heart or head, as well as no feedback. As investor, participants transferred a greater proportion of their endowments when exposed to visual feedback from their own head than to feedback from their own heart or no feedback at all. These effects were not observed when the source of the feedback was the simulated partner. As investee, heart feedback predicted greater altruistic returns than head or no feedback, but this effect did not differ based on source (own vs partner). Consistent with a dual-process framework, we suggest that people may be encouraged to invest more or be more altruistic when receiving bodily feedback from conceptually diametric sources.

Introduction

“ . . . we have heads to get money, and hearts to spend it.”

For at least two millennia, humans have entertained a metaphorical polarisation between their heart and head. The ancient Greek philosophers were divided as to which represented the centre of the intellect, with Plato (ca. 427-347

A question of interest to modern-day scholars is the extent such conceptual metaphor represents and influences human behaviour. Experimental social psychology has provided evidence for the potential truth value of embodied metaphors, indicating in a number of related studies, for example, that physical cleansing may alter moral judgments (e.g., Kaspar, Krapp, & König, 2015; Schnall, Benton, & Harvey, 2008; Zhong, Strejcek, & Sivanathan, 2010) and that haptic roughness (vs smoothness) can enhance prosocial and empathic responses to others’ suffering (Ackerman, Nocera, & Bargh, 2010; Wang, Zhu, & Handy, 2016). Nor has the heart–head dichotomy escaped attention; Fetterman and Robinson (2013) asked people whether they located their sense of “self” in their heart or head. “Head locators” displayed better general knowledge and solved moral dilemmas more rationally than “heart locators.” Furthermore, priming attention to one’s heart or head, by having participants point to them, causally affected performance in the above tasks (see also Adam, Obodaru, & Galinsky, 2015). It is unclear, however, how people might choose to alter their decisions when they are ostensibly predicated on heart- or head-based feedback. In this study, we are the first to explore this, operationalised within incentivized socioeconomic behaviour.

The division between cognitively (i.e., head-led) and affectively (i.e., heart-led) mediated decisions is well established theoretically in psychology and behavioural economics. Daniel Kahneman—a psychologist whose work on decision-making under uncertainty earned him a Nobel Prize in Economics—is a notable proponent of the dual-process theory of decision-making. Kahneman differentiates an automatic, intuitive, and affective system of decision-making (“System 1”) from a system that is slower, deliberative, and rational (“System 2”), requiring greater mental effort (Kahneman, 2012). The dual-process theory can be extended in this context to conceptualise heart versus head decisions. Decisions from the heart (to be “kind-hearted”) are often associated with compassionate and altruistic acts, such as charitable donations, where people are thought to rely on an affect heuristic (Small, Loewenstein, & Slovic, 2007). Decisions from the head (to “use one’s head”), on the contrary, are associated with rational and deliberative thought, linked in economic theory to utility maximisation (i.e., invested self-interest; Sanfey, Loewenstein, McClure, & Cohen, 2006). Thus, based on a dual-process framework, we may expect people to make different economic decisions when predicated on feedback from their heart versus their head and for this to depend on whether decisions are framed to be altruistic or tactically self-invested.

Prior studies in the area have focused on the heart alone, neglecting comparative bodily sources and differential (altruistic vs invested) socioeconomic motivations. Van Lange, Finkenauer, Popma, and van Vugt (2011) assessed the mere effect of measuring one’s heart rate (vs a no heart rate control) in female dyads playing a one-shot anonymised paper-and-pencil version of the “investment game” (IG; Berg, Dickhaut, & McCabe, 1995) and reported significantly greater investments in the heart rate condition. Lenggenhager, Azevedo, Mancini, and Aglioti (2013) had people play repeated rounds of the “ultimatum game” (Güth, Schmittberger, & Schwarze, 1982) against computerised opponents. While playing, participants listened to their own heartbeat, someone else’s heartbeat, or footsteps. When listening to their own heartbeat (vs other conditions), participants rated unfair offers from others as less fair and made more unfair offers themselves. However, the participants’ acceptance rates of unfair offers did not significantly differ. The researchers reasoned that listening to one’s own heartbeat had increased participants’ interoceptive awareness of being treated unfairly, leading to more punitively unfair offers.

In this study, we developed a novel experimental paradigm to test the causal effects of receiving heart–head bodily feedback on changes in socioeconomic decision-making. Participants played a repeated IG against a simulated partner, alternating in blocks of trials between self-invested investor and altruistic investee. Participants had their heart (beats per minute [“BPM”]) and head (“attention”) monitored and received feedback on-screen that differed by origin (heart/head) and source (own/partner). Although investments were ostensibly viewable by one’s partner, returns as investee were masked to promote altruism. Based on a dual-process theory of decision-making, and its extension to heart–head metaphor, we predicted that (1) participants would invest more when predicated on head (rational) feedback, (2) participants would return more when predicated on heart (affective) feedback, and (3) to the extent that Hypotheses 1 and 2 were egocentric, the effects would be specific to participants’ own feedback, and not of the simulated partner.

Method

Participants

An a priori sample of 50 was determined based on practical considerations and an indicative a priori analysis on G*Power 3.1 (Faul, Erdfelder, Lang, & Buchner, 2007). For a repeated-measures analysis of variance (ANOVA) with a medium effect size (f = 0.25), α = .05, and a medium correlation between measures (r = .30), a minimum of 44 participants were required for 95% power. 1 After testing 18 participants, a fault was identified in the program that artificially reduced some participants’ investee decisions (depending on the display method). This problem was rectified and extra participants were recruited as replacements (until N = 49). 2 The 18 participants were subsequently quizzed over whether they experienced the problem, and nine explicitly stated that they did not and were included in analyses, giving a final sample of 58 undergraduate and postgraduate students (27 women, mean age = 22.76 years, standard deviation [SD] = 4.28). Participants were paid in Amazon.co.uk credit (mean payment = £12.41, SD = £2.41) for their time. Participants had no prior experience with physiological measures.

The modified IG

In the classic IG (also known as the “trust game”; Berg et al., 1995), two participants are anonymously paired and the first player is given the opportunity to send any (or none) of a monetary allowance to the second player, knowing that this amount will be tripled and the second player then has the opportunity to return any (or none) of this tripled endowment back to the first. Variations of the game are commonplace and include repeated IGs and versions where players play both roles (see Johnson & Mislin, 2011).

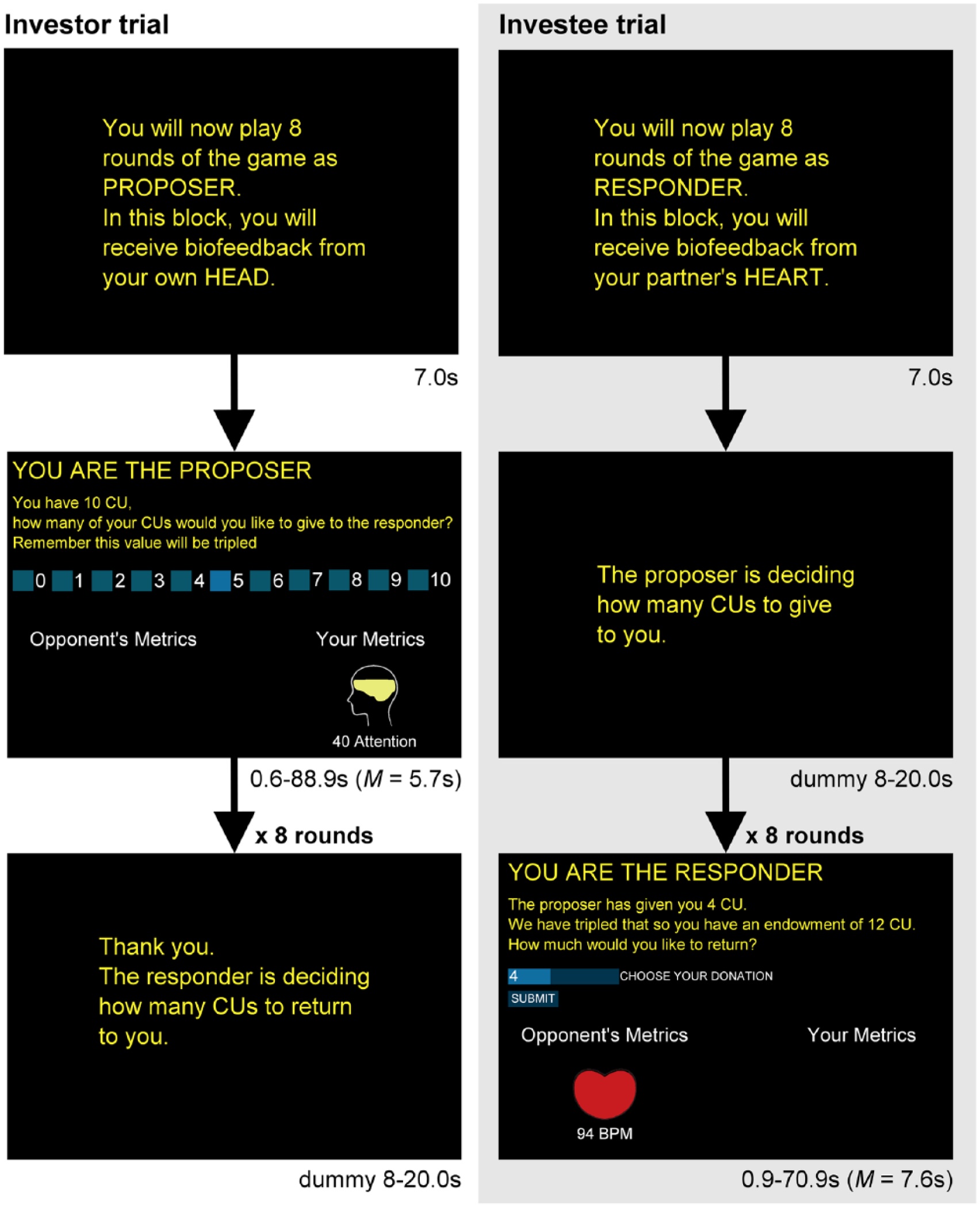

Our modified IG was programmed in Processing 2.1 (processing.org), a Java-based language, and run on an iMac (2.66GHz, interCore i5) machine with a 27-in display. Participants alternated in blocks as investor (“proposer”) and investee (“responder”) while receiving on-screen feedback from their own or a simulated partner’s heart or head (or no feedback). The program was designed to simulate a 2-player IG, but participants actually played with a computerised opponent. Once set up, participants received instructions and a test game, before clicking “ready” to indicate to their partner they were ready to start. Participants were told that both players were ready and that the computer would randomly decide which player would start as proposer (with a simulated 3,000 ms delay); in fact, participants were always chosen to be the proposer (to determine the simulated partner’s responses as proposer, see below). The game lasted for 80 trials, with eight trials in 10 blocks. At the start of each block, the participant was told whether they were the proposer or responder and what type of feedback they would receive. The game was counterbalanced, so the experimenter could input one of two schedules at set-up. In Schedule 1, participants received feedback in the order: head (own), head (partner), no feedback, heart (own), heart (partner), with two blocks for each feedback condition (eight trials as proposer, then eight trials as responder per block). In Schedule 2, the head and heart blocks were reversed. Figure 1 illustrates the game interface and an example trial as investor and investee, with bodily feedback.

The user interface of the modified investment game, featuring an example trial as investor, with head (own) feedback, and as investee, with heart (partner) feedback, with response times in seconds. In the control (no feedback) condition, the feedback metrics appeared blank. Font sizes have been adjusted for illustration purposes.

Investor (“proposer”) trial

For each trial as investor (“proposer”), participants were told they had 10 “currency units” (CU; 1 CU = 1p) and asked how many they wanted to give to the responder, while reminded this value would be tripled. Participants chose by clicking a square next to a number in a scale from left to right (0-10). After making their decision, a message said, “the responder is deciding how many CUs to return to you” with a variable time delay of 8 to 20 s (simulating the other player’s decision-making time). The participants were not told of their partner’s decision as investee. To calculate participants’ remuneration for taking part, the value of return was fixed at 0.37 of the investment (see Johnson & Mislin, 2011).

Investee (“responder”) trial

For each trial as investee (“responder”), prior to their decision, the participant was confronted with a screen that said “the proposer is deciding how many CUs to give to you” (with an 8- to 20-s delay). Participants were told how many CUs had been invested and asked how many (if any) CUs they would like to return on that investment with the prior knowledge that their partner would not be told. The investment was simulated based on IF-THEN rules (where i is the participant’s offers in the previous block as proposer):

IF

IF

IF

Thus, the simulated partner broadly reciprocated the participant’s own behaviour. The participant indicated how much of the investment they would like to return on a sliding scale from left to right (0 = invested endowment*3). If nothing was invested, participants were told they had no decision to make and had to click a button to acknowledge this.

Bodily feedback

Biofeedback was displayed on-screen as part of the IG window, as an interactive visualisation and digits of heart rate (“BPM”) or basic cognitive activity (“attention”), or nothing (in the no feedback condition). Head feedback was accompanied by a graphic of a head with a brain that filled up and changed colour (from green, yellow, to red) to correspond to the level of attention. The heart feedback was accompanied by a graphic of a heart that beat commensurate with the level of BPM recorded.

Head feedback was obtained using a Neurosky MindWave Mobile headset, a single dry electrode wireless EEG system used for consumer biofeedback and brain computer interface experiments (for further technical details, see Supplemental Material). The MindWave outputs a proprietary metric called “attention” (focused on the beta band; 0 = no attention, 100 = complete attention), which we used for feedback as it was conceptually understandable to participants. The attention metric broadly corresponds with fluctuations in the user’s task-related attentional demands (Crowley, Sliney, Pitt, & Murphy, 2010).

Heart feedback was obtained using photoplethysmography (PPG) from a Pulse Sensor optical heart rate monitor (pulsesensor.com) to obtain BPM (for further technical details, see Supplemental Material). Physiological data were recorded on the host computer and transmitted in real time to the experimenter’s computer. Participants saw their own bodily feedback in real time. For the simulated partner’s feedback, participants were exposed to the same, standardised pre-recorded dummy trace of a researcher playing the IG. Response times from presentation until decision (ms) were also recorded. For analyses, the measure of heart rate and attention recorded prior to each decision was used.

Self-reported covariates

We collected information on several demographic characteristics of the participants (gender, age, country of origin, departmental affiliation, and whether their parents had a higher education qualification, as a proxy of socioeconomic status), and they completed questionnaires assessing their levels of interoceptive awareness and empathy for others.

Interoceptive awareness

Interoceptive awareness was measured using the Multidimensional Assessment of Interoceptive Awareness (MAIA; Mehling et al., 2012). The MAIA is a 32-item scale assessing eight dimensions of interoceptive awareness (noticing, not-distracting, not-worrying, attention regulation, emotional awareness, self-regulation, body listening, and trusting). Participants rated how often each item applies to them on a 6-point Likert-type scale (1 = never, 5 = always). For analyses, a total interoceptive awareness score was computed using six of the eight dimensions, omitting the not-distracting and not-worrying subscales, which have been shown to be problematic (Mehling et al., 2013; Valenzuela-Moguillansky & Reyes-Reyes, 2015) and were negatively correlated with all other subscales in this study. The interoceptive awareness measure demonstrated excellent internal consistency (α = .90).

Empathy

Participants’ trait empathy was measured using the Basic Empathy Scale for Adults (BES-A; Carré, Stefaniak, D’Ambrosio, Bensalah, & Besche-Richard, 2013). The BES-A is a 19-item measure with nine items assessing cognitive empathy and 11 items assessing affective empathy. Participants rated their agreement with each item on a 5-point Likert-type scale (1 = strongly disagree, 5 = strongly agree). Both the cognitive empathy (α = .84) and affective empathy (α = .85) subscales demonstrated good internal consistency.

Procedure

Institutional ethical approval was acquired prior to data collection, and the research was conducted in a manner consistent with the British Psychological Society’s Code of Human Research Ethics. Participants were recruited for a study on “the effect of biofeedback on economic decisions” by email advertisements. Interested participants completed a “sign-up” survey, which included the demographic questions, MAIA, and BES-A. Participants were then contacted by the researcher to schedule an appointment at the lab. Upon arrival, all participants were greeted by the same female experimenter. They were told that their partner had already arrived and was being set up in an adjacent room. As participants were led to the testing room, they were walked past their ostensible partner’s room, which had an “experiment-in-progress” sign on the door. Participants were seated, introduced to the study, and provided their informed consent. Participants were then given instructions to read (see Supplemental Material), while the experimenter left the participant for 5 to 10 min to “check up on the other player and do a test game with them.” The physiological measures were then set up (for further details, see Supplemental Material), participants did a test game, and then played the IG. Approximately half of the participants (n = 28) completed the IG in order in Schedule 1 and the rest (n = 30) in Schedule 2. The progress of the IG and the physiological measurements were monitored by the experimenter on a computer outside the testing room. After the experiment, the equipment was removed and participants were fully debriefed.

Data analysis

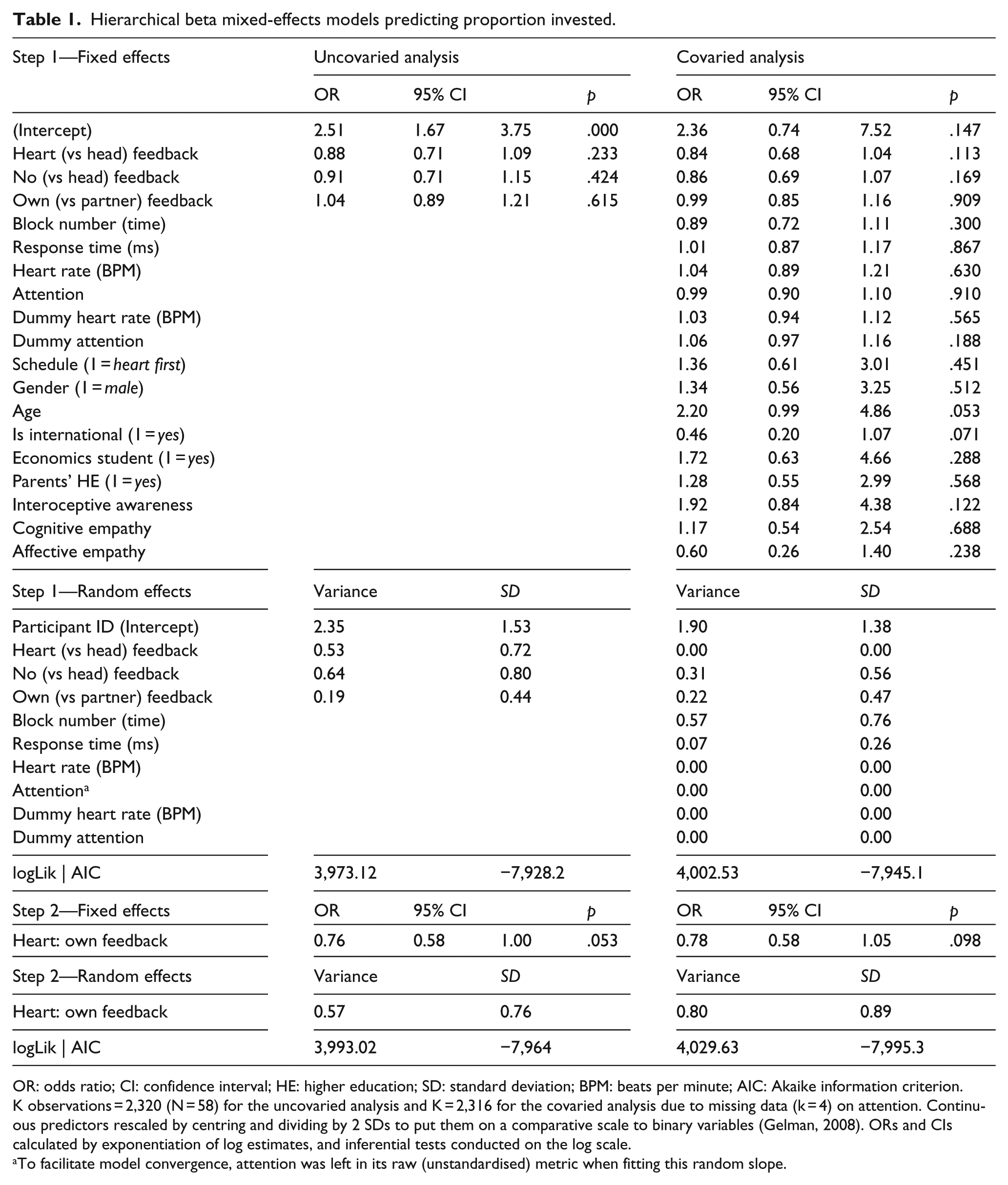

To account for the nested structure of the data, linear mixed-effects models with a random intercept were used to model repeated observations (Level 1) clustered at the participant level (Level 2; Aarts, Dolan, Verhage, & van der Sluis, 2015). Each model was fitted with a maximal random effects structure (as recommended by Barr, Levy, Scheepers, & Tily, 2013) to control for Type I error. The outcome variables did not follow a Gaussian distribution, but instead were a bounded proportion of the level of CU endowment and had levels of skewness and kurtosis consistent with a beta distribution, as illustrated by density and Cullen and Frey graphs (Cullen & Frey, 1999; Delignette-Muller & Dutang, 2015; see Figure S1 and S2 in Supplemental Material). Accordingly, generalised linear mixed-effects models with a beta distribution were used to model the data (see, for example, Ferrari & Cribari-Neto, 2004; Hunger, Döring, & Holle, 2012). These modelled the response variable as a proportion bounded between (0, 1) (i.e., the proportion of CUs transferred) and showed a superior fit to linear mixed-effects models with a standard Gaussian distribution (ΔAIC in the uncovaried beta models ranged from −6,479.8 to −8,691.2). The advantages of beta regression models over standard Gaussian models, when outcome variables deviate from the normal distribution, are noted in Smithson and Verkuilen (2006). To fit the beta models, the formula cited in Smithson and Verkuilen (2006) was used to convert [0, 1] to (0, 1) proportional data. We present models with and without a full set of observed covariates.

In each model, the omitted (reference) biofeedback category was the one hypothesised to be associated with the greatest proportion of CUs transferred. All models were estimated hierarchically, testing first the effects of bodily feedback (Hypotheses 1 and 2) and then the moderating effect of feedback source (through its interaction with feedback type; Hypothesis 3). All data were analysed in R 3.2.2 (R Core Team, 2015), using packages arm (Gelman & Su, 2015), fitdistrplus (Delignette-Muller & Dutang, 2015), and glmmADMB (Skaug, Fournier, Bolker, Magnusson, & Nielsen, 2016). As all models used a logit link, estimates are presented as odds ratios (OR; Ferrari & Cribari-Neto, 2004; Hunger et al., 2012), which, in a beta model, represent the ratio between two relative proportions ( pˆ), defined as the ratio of the expected proportion transferred (μ) to the full endowment minus the expected proportion transferred (1−μ) so that pˆ = μx/(1–μx). The OR is the ratio of the relative proportion estimated at a 1-unit increase in the predictor (x1) over that of the reference category (x0), such that OR = (μx1/(1–μx1))/(1–μx0) Accordingly, ORs in beta regression are sometimes known as “relative proportion ratios” (Smithson & Merkle, 2014). As they are on a logit scale, negative ORs can best be intuitively interpreted by reversing them to their positive equivalents (1/OR), which then represent the OR for x0 over x1. To facilitate meaningful comparisons in the magnitude of the estimates, all continuous covariates were grand-mean centred and divided by 2 SDs to be on a comparative scale to binary variables (Gelman, 2008).

Results

Participants responded to 2,320 decisions as investor and 2,278 as investee (42 investee trials had an endowment of zero, and thus, no decision was recorded). Participants invested an average of 6.50 CU, SD = 3.22, or 65% of their endowment, and returned an average of 3.39 CU, SD = 4.61, or 17% of their endowments, in each trial. Full distributions of responses in the investment and investee trials are provided in Supplemental Material (Figure S1), as are the means (and SDs) and medians (and interquartile ranges) for the proportions invested and returned in each feedback condition (Table S1).

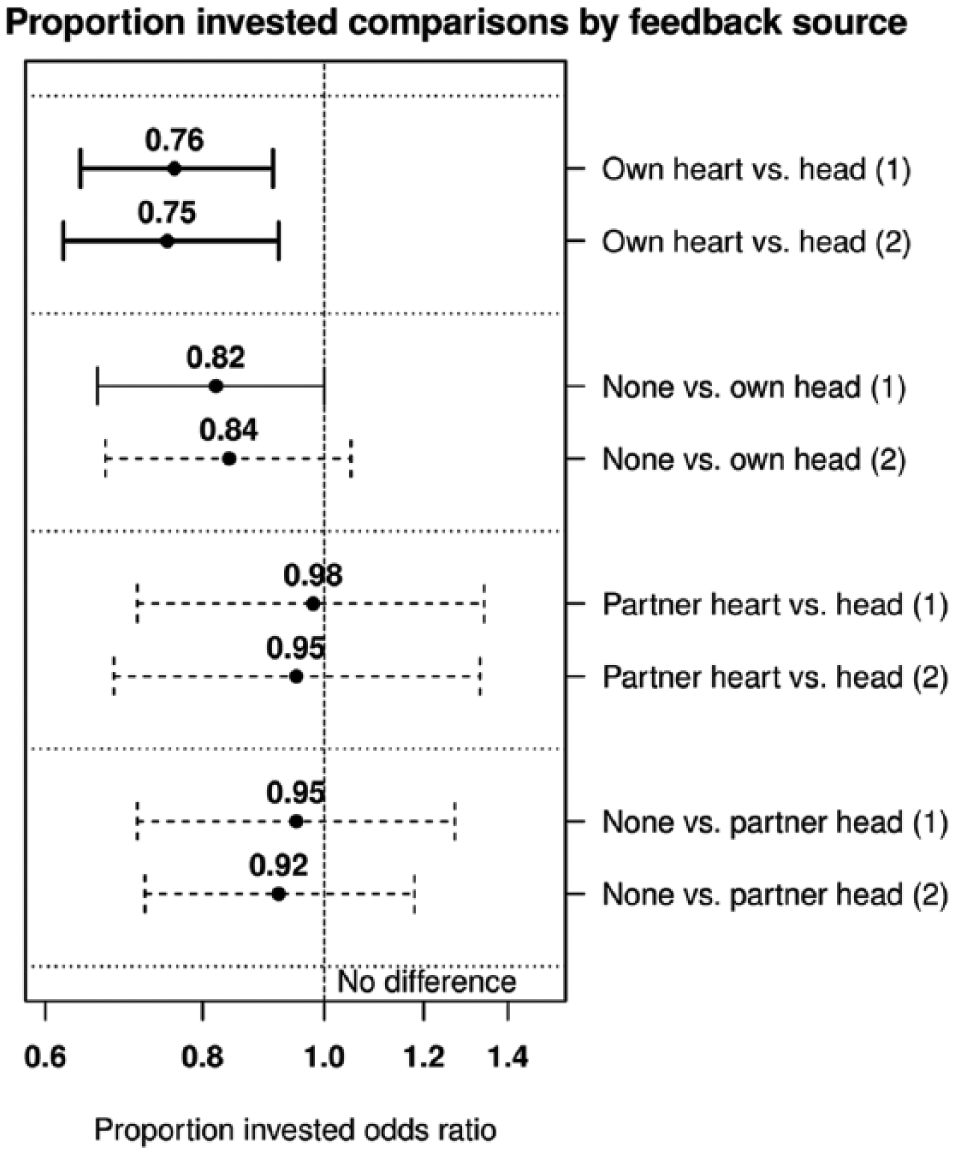

Full results of the beta models for investment decisions are provided in Table 1. Although participants did not invest significantly more when receiving head versus heart, OR = 0.88, 95% confidence interval [CI] = [0.71, 1.09], p = .233, or no, OR = 0.91, 95% CI = [0.71, 1.15], p = .424, feedback at the aggregate level, there was a near-significant interaction between feedback type and source, OR = 0.76, 95% CI = [0.58, 1.00], p = .053, which remained borderline significant when a full set of covariates (with a maximal random effects structure) were added to the model. Figure 2 expands upon this interaction, showing the effect of head feedback by re-running the models with the source of the feedback as either the self or the simulated partner. The ratio of the proportion transferred to the full endowment was approximately 1.32 times greater, 95% CI = [1.10, 1.56], p = .003, when receiving own head feedback than when receiving own heart feedback and an estimated 1.22 times greater, 95% CI = [1.00, 1.52], p = .054, than receiving no feedback at all. However, the latter effect was weaker when covariates were added to the model. No significant effects were observed when the source of the feedback was restricted to the simulated partner. Of the covariates, being older, OR = 2.20, 95% CI = [0.99, 4.86] p = .053, was associated with greater proportional investments and being an international student, OR = 0.46, 95% CI = [0.20, 1.07], p = .071, was associated with a lower proportional investment.

Hierarchical beta mixed-effects models predicting proportion invested.

OR: odds ratio; CI: confidence interval; HE: higher education; SD: standard deviation; BPM: beats per minute; AIC: Akaike information criterion.

K observations = 2,320 (N = 58) for the uncovaried analysis and K = 2,316 for the covaried analysis due to missing data (k = 4) on attention. Continuous predictors rescaled by centring and dividing by 2 SDs to put them on a comparative scale to binary variables (Gelman, 2008). ORs and CIs calculated by exponentiation of log estimates, and inferential tests conducted on the log scale.

To facilitate model convergence, attention was left in its raw (unstandardised) metric when fitting this random slope.

Comparisons between head vs heart and no feedback when the source of the feedback is either the participant (own) or the simulated partner. Estimates based on uncovaried (1) or covaried (2) models. K observations = 1,392 (N = 58) for own feedback. K observations = 1,392 (N = 58; K = 1,388 covaried) for partner feedback. Odds ratios and CIs were calculated by exponentiation of logs. Inferential tests were conducted on the log scale. X-axis is on the log scale. Bars represent 95% CIs. Bold solid bars are significant at p < .05. Non-bold solid bars are significant at p < .10.

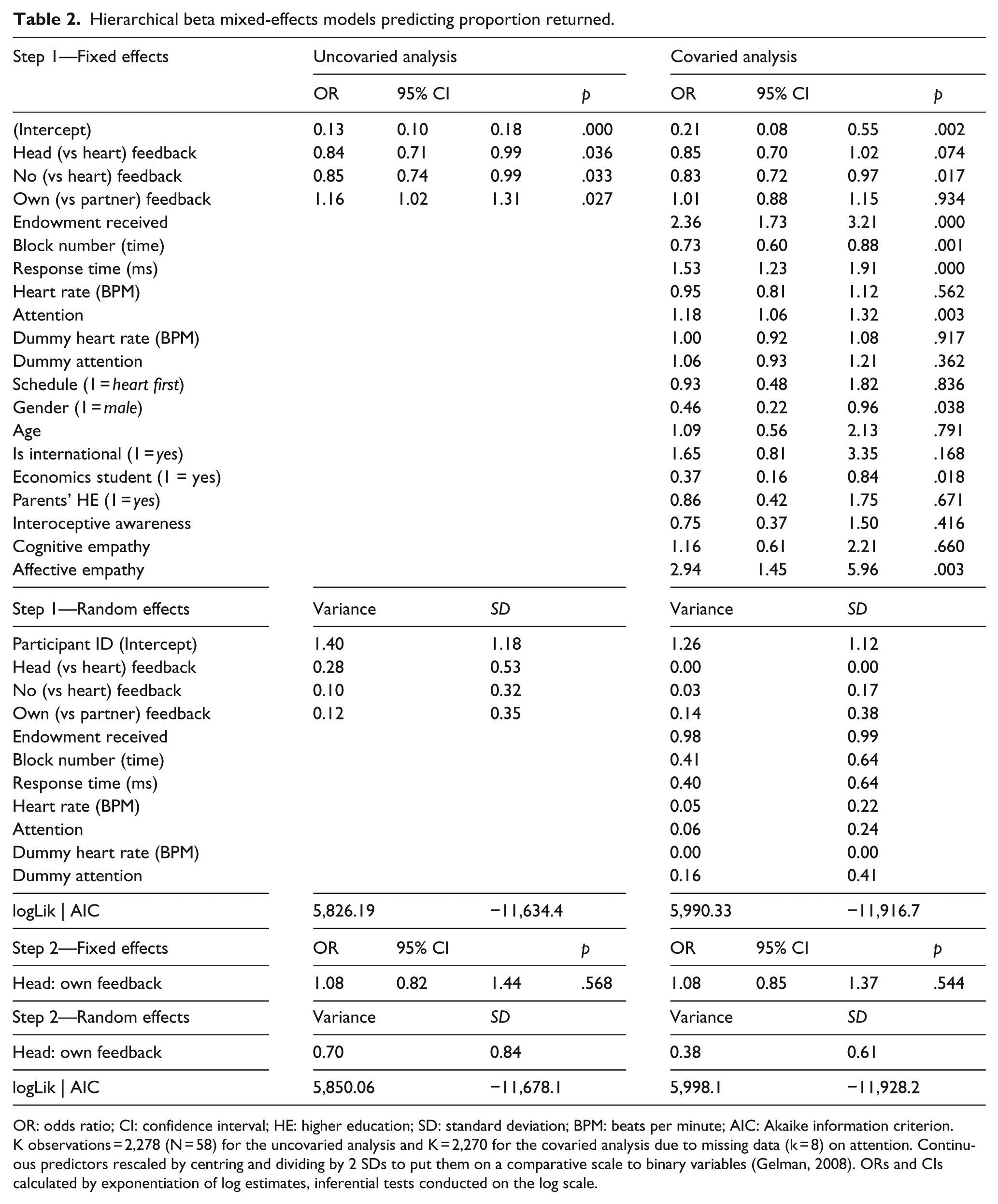

Full results of the beta models for investee decisions are provided in Table 2. The proportion transferred by participants was estimated to be 1.19 times greater, 95% CI = [1.01, 1.41], p = .036, in the heart than in head feedback conditions and 1.18 times greater, 95% CI = [1.01, 1.35], p = .033, in the heart than in no feedback conditions. These effects remained relatively consistent when covariates were added to the model. Without covariates, the proportion transferred was estimated to be 1.16 times greater, 95% = CI [1.02, 1.31], p = .027, when participants received their own rather than simulated partner feedback; however, this effect disappeared when covariates were added to the model. There was no significant interaction between type of feedback and feedback source for investee decisions.

Hierarchical beta mixed-effects models predicting proportion returned.

OR: odds ratio; CI: confidence interval; HE: higher education; SD: standard deviation; BPM: beats per minute; AIC: Akaike information criterion.

K observations = 2,278 (N = 58) for the uncovaried analysis and K = 2,270 for the covaried analysis due to missing data (k = 8) on attention. Continuous predictors rescaled by centring and dividing by 2 SDs to put them on a comparative scale to binary variables (Gelman, 2008). ORs and CIs calculated by exponentiation of log estimates, inferential tests conducted on the log scale.

The size of the endowment received, OR = 2.36, 95% CI = [1.73, 3.21], p < .001, response time, OR = 1.53, 95% CI = [1.23, 1.91], p < .001, level of attention, OR = 1.18, 95% CI = [1.06, 1.32], p = .003, and trait affective empathy, OR = 2.94, 95% = CI [1.45, 5.96], p = .003, significantly predicted a greater proportion returned as investee. Block number (time), OR = 0.73, 95% CI = [0.60, 0.88], p = .001, being a man, OR = 0.46, 95% CI = [0.22, 0.96], p = .038, and being an economics student, OR = 0.37, 95% CI = [0.16, 0.84] p = .018, significantly predicted a lower proportional return as investee.

Discussion

Heart–head metaphors have existed since antiquity, the head being associated with rational, strategic decisions. Here, consistent with Hypothesis 1, participants invested significantly more in trials accompanied by feedback from their own (but not a simulated partner’s) head than feedback from their heart and marginally significantly more than no feedback at all. This effect is conceptually consistent with other head-based primes (e.g., Adam et al., 2015; Fetterman & Robinson, 2013). We suggest two theoretical explanations. First, to the extent sound financial decisions are rational and not emotional (e.g., Shiv, Loewenstein, Bechara, Damasio, & Damasio, 2005), participants may have felt justified investing more or taking economic risks when the decisions were predicated on visual feedback from their head, rather than their heart, or a no feedback alternative. Second, to the extent head-embodied rationality is associated with financial self-interest (Sanfey et al., 2006), such feedback may have primed greater imagined returns from investing more.

The heart is metaphorically associated with compassion. Here, in line with Hypothesis 2, feedback from the heart led to significantly more money returned than feedback from the head or no feedback at all. However, this effect did not differ as a function of feedback source (own vs partner). This adds to work showing effects of heart-based primes on charitable giving (e.g., Guéguen & Jacob, 2013; Guéguen, Jacob, & Charles-Sire, 2011). Thus, heart primes appear to be associated with greater altruistic behaviour, yet the precise mechanisms underlying this manipulation remain to be elucidated. In addition to priming compassionate giving, for example, it is possible that the heart feedback emphasised the partner’s feelings, and affective or “human” qualities, increasing the proportion returned. Alternatively, the heart may represent stress, associated, for example, with an anxious response when choosing not to return money, thus encouraging giving. Nevertheless, greater giving was not specific to feedback from either the participant’s own or the simulated partner’s heart, suggesting that the effect may have been more general, and we observed no effect of personal stress levels (i.e., levels of BPM) on giving. Thus, although it remains an empirical question for future study, our favoured interpretation remains that heart primes are associated with greater altruistic giving because of their conceptual association with compassionate and kind behaviour.

There was mixed evidence for Hypothesis 3. The effect of heart-based feedback did not depend on its source (cf., Lenggenhager et al., 2013), implying a degree of generalised conceptual priming. However, the effect for head feedback was specific to receiving feedback from one’s own head, and not that of the simulated partner, providing some evidence for an egocentric effect. This result suggests that there may have been something special about receiving feedback from one’s own head that led to participants investing greater proportions and that this was not the result of priming the concept of the “head” or “rationality” per se. This finding extends prior experimental manipulations of head (vs heart) salience that have exclusively focused on one’s own body (e.g., Fetterman & Robinson, 2013), suggesting that similar effects may not be achieved if the prime is directed elsewhere (i.e., pointing at somebody else’s head; Fetterman & Robinson, 2013).

Of the observed covariates in the study, our findings are consistent with several known effects, including, for example, that affective (but not cognitive) empathy predicts altruistic behaviour (Edele, Dziobek, & Keller, 2013), women are more generous than men (Engel, 2011), and economics students are more selfish than others (Bauman & Rose, 2011). Of particular interest is the positive effect of response time (or latency) on proportion returned as investee, which is consistent with the positive effect of greater attention. Initially, this appears counter-intuitive, given that altruism is typically associated with faster and more automatic decisions (e.g., Cone & Rand, 2014; Kahneman’s “System 1,” Kahneman, 2012). However, if the distribution of returns as investee is split into a decision about whether to give anything (a 0/1 binary outcome) and, conditional on giving something, a decision about the magnitude of the return (> 0), post hoc regressions regressing these variables on response time show that the significant effect of response time is confined to the decision of whether or not to give (p < .001), rather than the magnitude of the return (p = .319). In other words, people who decide to give something take longer to complete the task than those who decide to give nothing. Thus, it appears that the decision of whether or not to give something as investee is made relatively quickly, and response time does not affect the magnitude of the return over and above this decision.

Several limitations of the study should be noted. First, causal relationships can be inferred for the experimental manipulations, but other findings are less clear (e.g., the relationship between attention and giving). Second, as a psychological manipulation, the physiological measures were intended to be simple and non-invasive, but did not provide a high level of detail. Similarly, the use of “attention” for head (brain) activity may have been less familiar than “BPM”; it is possible that the effects may have differed if an alternative label was used. Third, relatively small CU values were used in each trial; that the observed effects would hold when amounts involved are altered is unclear. Fourth, participants’ awareness of the purpose of the experiment (demand characteristics) and/or their belief that they were playing the game against a real (not simulated) person were not assessed, and so we cannot estimate the size of these influences on the results obtained.

These limitations notwithstanding, we are the first to demonstrate differential effects of heart–head feedback on incentivised (financial) decision-making. This has implications for a number of areas, including the increasing proliferation of biofeedback devices (e.g., for investment decisions; Gardner, 2016) and in the charitable sector (e.g., using heart-based primes to encourage donations). Our results reinforce that the heart–head dichotomy is more than just literary metaphor, but may affect directly people’s choice of decision.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Engineering and Physical Sciences Research Council under grant number EP/L003635/1 and meets its expectations in regard to research data, which is available from the corresponding author upon request for up to 10 years following publication.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.