Abstract

Political and economic rapprochement is taking place between Russia and China in a number of fields: energy, arms production, trade in national currencies and strategic projects in transport and supporting infrastructure. This development, fostered by Western policies and actions, including sanctions related to Ukraine, appears to be strengthening despite reservations related to uneasy precedents, contrasting visions and uncertain economic projections. Chinese policies aiming at European markets via the revival of the Silk Road assist this development. The One Belt-One Road is projected as an alternative, or supplement, to the maritime routes made unsafe by contiguous countries’ unrest, criminality and the assertive control of the seas by the United States. While Russia, promoting friendly investment structures, moves eastwards to develop the Russian Far East bordering China, the latter expands westwards engaging in laborious negotiations with Central Asian countries and costly investments in infrastructure and logistics. In each area, the article maintains that both countries, despite economic and political competition and fear of losing control, have interest in cooperation and discusses the areas where this is taking place, albeit slowly and with difficulty. Whether economic cooperation can develop into a strategic alliance including defence is discussed in the light of joint military exercises, arms trade and plans to broaden the scope of the Collective Security Treaty Organisation, the Shanghai Cooperation Organisation (of which India and Pakistan have recently become members), and the Common ASEAN Community. This path is difficult and marred by members’ conflicting interests. But some positive outcomes should not be ruled out.

Keywords

For decades before and after transformation to market in both countries economic relations between geographically contiguous Russia and China have been lagging behind commercial ties with the rest of the world. Only now movement towards political rapprochement and economic cooperation in a number of fields is taking place, the importance of which is difficult to assess per se and for its possible development. These developments are observed with interest and some scepticism among Russian and foreign experts justified to a large extent by history.

Working out ambitious projects of development of backward territories eastwards is a strategy Russia developed from 2012, also looking for China's economic support. A more problematic area for cooperation is that of the Eurasian Economic Union (EAEU). Economic integration in Eurasia was originally pursued by Russia with no immediate concern and/or interest for China. It is becoming clear that both countries have developed strong interests in this region. While each country has pursued autonomously projects in Central Asia, where both are economically present and to a large extent competing, joint infrastructural projects may be convenient to both. China and Russia could either decide to strive one against the other for primacy in the region, or back down and engage in a process of cooperative networking. Judging from their comparative strengths and geo-economics neither could reasonably be a winner. But both could be losers to outsiders. Compromise may be the only way out in the short to medium term.

But compromise is not easy, either. First, Russia and China will need to find a common understanding on how to frame the contours of cooperation in a difficult region. The EAEU is a recent creation marred by internal difficulties through the entire process of its formation. Other complications have intervened after its starting. The main partner in the present structure is Kazakhstan. This is a country that can hardly be intimidated by either China or Russia and is able to play an important autonomous role in either fostering regional cooperation or stemming its inception. Agreements are also complicated by the interference of a number of outside players each with their own vested economic or extra-economic interests in the region.

Second, China's outreach to European markets is pursued autonomously through her Silk Road/One Belt-One Road fast transport project through Central Asia. This project, based on current and prospective cost-benefits, comprises a number of alternative transport infrastructures and routes compared to the legendary Silk Road. For China the transport route does not have to go through Russia. Any country in the region covets access to multimodal transport vehicles. China has already been building or renovating transport routes linking her western borders to Central Asian countries. By raising the prospect of a Free Trade Area between the EAEU and China that echoes Kazakhstan's earlier proposals Russia strives for a negotiation framework with China that would be more suitable to her interests, and perhaps easier to control. However, in light of the multifarious and often conflicting interests in a region exposed to ethnic animosities, unstable governance and social fracture, the final outcome is highly problematic.

Finally, the paper raises the question of whether sustainable economic cooperation can develop in the absence of more a comprehensive and forward looking alliance. Some developments suggest that the longstanding disengagement from coordination on defence is about to end. Important joint military exercises and efforts to work out a coordinated stance to regional conflicts could be a prelude to strategically-orientated cooperation in the future. It is too early to speculate whether Russia and China will move from economic cooperation to strategic alliance. Despite little evidence to date, this should not be ruled out on the basis of experience alone. While Russia moves eastwards turning her back to a generally antagonistic Europe, China's outreach westwards trespasses Asia, aiming at other markets, among which wealthy Europe emerges as a major attraction.

If, under the pressure of US-led policies of containment, China and Russia will both agree with ancient Sun Tzu that the best battle is the one that is not fought, their relations may take a new turn. In an optimistic scenario, Eurasia may provide both the motivation in the need for stability and an institutional framework for policy dialogue. At the practical level, interstate consultative bodies in the region may be made more effective by envisaging joint policy actions to preserve stability against common threats.

Economic cooperation with modern China: Work in progress

While China's transformation to market started in the eighties with Deng Xiao Ping's decision to turn the economy into a ‘socialist market economy’, Russia, before, during and after Gorbachev's inconclusive perestroika, ignored the tremendous changes at her eastern borders.

In agricultural China, the process of transformation was marked at its inception by Chinese features: on the one side, liberalisation of agriculture, farming and rural handicrafts, on the other, regulated openness to foreign investments. Large scale industry and banking remained under state control. These changes, together with further economic liberalisation, would take in a few decades China to the status of a dynamic world economy and a major strategic actor in the process of globalisation that the country was able to exploit to her advantage.

In industrialised Russia transformation to market was painful and systemic change deeper. While Soviet-type industry was slow to adapt to market and the debt burden inherited from the past constrained government policy, the resource-base of the economy strengthened (Malle, 2008). Economic recovery after the 1998 financial crisis was robustly helped by high commodity and hydrocarbon prices and demand from fast growing Europe. Russia's economic dependence from Europe increased spontaneously, helped by proximity of their relatively more developed regions and transport infrastructure.

Different transformation trajectories and market opportunities help explain why trade with China remained subdued for a long time despite two-digit growth in China after entry into the WTO in 2001 and robust growth in Russia. Russia's interest in China changed after the economic breakdown caused by the 2008 crisis and the successive collapse of commodity and energy prices. From 2008 China became the first trade partner for Russia replacing Germany. Slow and uncertain recovery after the crisis increased the perception of economic fragility among policy makers.

The 2008–2009 crisis was a cold shower for Russia. Not only the 7 percent annual growth from 2000 to mid-2008 that was hoped to bring about the doubling of the economy in ten years was interrupted, but subsequent developments proved that it could hardly be restored unless fundamental changes capable of upgrading and diversifying the economic structure intervened. Along a major policy rethinking forced by events and contrasting options regarding priorities, Russia's turn eastwards gained steam. President Putin's 7 May 2012 Edicts are an obligatory reference when marking the inception of a new approach to development and growth. Within this approach the focus fell on China as a privileged partner for trade and investment.

Moving away from the West

Two fundamental concerns are behind this turn in policies. Both are related to Russia's large exposure to the West. This paper does not discuss their soundness. But they are worth bringing to attention as a possible landmark in the development of a new system of economic and political relations that is presently taking shape.

In the first place, policy-makers realised for the first time that Russia's excessive dependence on her western economic partners, primarily on the EU, could seriously harm economic development if positive trends abruptly reversed. Russia had been exposed to other economic turmoil earlier, in particular the 1998 financial crisis, but owing to her own policies and failures. In 2008 it was a world-wide financial and economic crisis that hit Russia through falling foreign trade and via Russian big banks and companies’ large exposure to foreign loans facilitated by no control on capital movements (that China instead maintained). Economic openness that was beneficial for growth from 1999 onwards suddenly turned into a nightmare exposing the fragility of the whole economic construct. In the second place, the leadership was made aware, through the snowballing of interrelated feed-backs in the world scene that, despite the country's inclusion in the main international clubs (i.e. the UN security council, the G8 and the just accessed WTO), Russia continued to be an outsider, not a peer as looked for, but a guest at the table of world powers. The perception was that Russia had no safeguards against the rebounds of unexpected actions worked out and launched against her interests.

The number of regional conflicts initiated or pursued disregarding Russia's position and concerns increased from the late nineties onwards. Fighting, carried out or assisted by NATO, moved from former Yugoslavia in 1999, to Iraq in 2003, Libya and Syria in 2011. In each case selective legitimacy for military action was found in instances of rebellion against the powers in place, claims of regime brutality and civil clashes that could evolve into civil war. No matter the underlying specificities for social unrest or fracture in each country, these facts were hailed by western supporters as a demand for democracy.

Time has shown not only that incursions from the outside against state sovereignty were doomed to failure, confirming Russia's views, but also that the evidence used to justify intervention was either unsubstantiated, as for the alleged weapons of mass destruction in Iraq, or paltry enough to suggest that alternative forms of pressure, if justified, would have been wiser than engaging in fighting. The most authoritative figure against such policies is Kissinger (2014). Eminent scholars have condemned selective wars in the alleged pursuit of democracy (Lieven, 2016a, 2016b; Mandelbaum, 2016). In the United States longstanding mutual disrespect between the old conservative school and neocons is amplifying and echoed in policy circles. President Obama's disavowal of the American intervention in Libya is the most significant example of such developments to date (The Atlantic, 2016).

Searching for dynamic partners in the East: An uneasy path

Before distancing from the West for the reasons outlined above, the Russian authorities had tried to find support in Europe for a proposal of economic cooperation from Lisbon to Vladivostok of which Russia would be the bridge. This idea that was outlined by Premier Putin in Germany in 2010 (The Spiegel, 2010) 1 was further developed by President Putin at the APEC meeting in Vladivostok in September 2012 after Russia had entered WTO by bringing into the picture the Eurasian Trade Custom Union (ECU) at that time associating Russia with Belarus and Kazakhstan. Putin evoked again a possible free trade area (FTA) between the EU and the ECU (Putin, 2012a, 2012b).

In his interview Putin said “We propose the creation of a harmonious economic community stretching from Lisbon to Vladivostok,” and “in the future, we could even consider a free trade zone or even more advanced forms of economic integration. The result would be a unified continental market with a capacity worth trillions of euros.”

By then Russia's relations with the West had already turned sour. President Obama did not take part in the APEC meeting, foreign media preferred to focus on the cost to Russia for the preparation of the meeting; Western circles manifested their dislike for Russia's economic projects for Eurasia and Hillary Clinton in the aftermath of the meeting accused Russia of promoting “a move to re-Sovietise the region” (APEC, 2012; Clinton, 2012). 2 On his part, Putin did not conceal his strong displeasure with western intervention in Syria's civil war (Putin, 2012b).

According to reports (APEC, 2012) the cost of the summit was allegedly $21 billion, see “Is Russia's APEC Summit A $21 Billion Waste?”

The APEC meeting gave Putin the opportunity to meet bilaterally with most Asian leaders, including the then Chinese President Hu Jintao, and focus on the potential of the large Asia Pacific Region (APR) comparing its dynamics with the grim economic state of the EU and OECD countries. Noting that world trade had fallen by 12 percent in 2009, Putin emphasised that APEC counted for 55 percent of the world's GDP and 45 percent of the cumulative world FDI, and that catching up with advanced economies had been very fast in the past 20 years (Putin, 2012c). Friendly gestures from New Zealand and Vietnam raised the hope that Asian countries could be interested in joining a FTA with Russia. Vietnam indeed joined a FTA with the EAEU: Russia also, after Kazakhstan, ratified the accession early May 2016 (Kazakhstan, 2016). New Zealand, opting for membership in the US-led Transpacific FTA, retreated.

That economic integration has political implications is becoming increasingly evident, although the agreements concern economic rules. Like in most clubs members are, or are hoped to be, politically friendly. China and Russia are not perceived like that. The US-run Pacific FTA was projected to exclude China from negotiations. The networking of a Transatlantic FTA with Europe, still pending, has been promoted by the US intentionally to exclude Russia. The antagonistic implications of exclusive economic partnerships are evident, discussed and likely to help shape Russia's foreign policy as deemed appropriate (Karaganov, 2016; Lavrov, 2016a; Lukyanov, 2016; Naryshkin, 2016; Xi, 2016). At the present stage one may assume that they have, at least, facilitated the rapprochement between China and Russia pushing both to adjust to new realities in searching alternative partnerships and trying to overcome their various geo-economic and political differences in regions of mutual interest.

In pursuing improved commercial relations with her powerful neighbour, Russian efforts to overcome obstacles look more demanding than similar efforts by China. Prima facie Russia/China economic cooperation would be a textbook case of trade driven by comparative advantages with Russia strong in resources and China in manufacturing. Trade, however, has lagged behind what could theoretically be envisaged in (earlier) fast developing large economies.

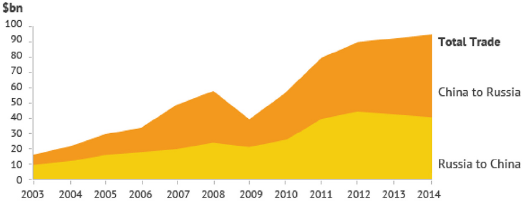

Trade increased rather slowly until 2008 when growth was robust in both countries and picked up later, after the crisis from 2009 onwards (Table 1), still remaining subdued compared with the EU. Bilateral trade volume between the two countries, which amounted to $15.8 billion in 2003, reached $95.3 billion in 2014 feeding Russia's hopes that it could soon reach $100 billion (Trade Statistics, 2016). While China had become by then Russia's first trade partner, China's volume of trade with wealthy EU had reached more than $500 billion by 2014 signalling how large the difference in the respective Russia and EU market capacity had remained (EU Trade, 2009; EUROSTAT, 2015). In 2014 the EU (28 countries) still counted for 45.8 percent of total Russian exports and 42.6 percent of total imports. China, in spite of having become Russia's first country trade partner, counted respectively 6.8 percent of Russian exports and 16.9 percent of imports (WTO, 2016).

Historical trading value trend.

Source: General Administration of Customs of People's Republic of China, 2015.

Despite an encouraging trend after 2009, the volume of trade between the two countries suffered sharply from the economic slowdown after 2014. Trade turnover between China and Russia dropped by 27.8 percent to $64.2 billion in 2015. The total value of Russia's exports to China declined in 2015 by 19.1 percent to $31.4 billion, according to Huang Songping, a spokesman for the Chinese customs department (The Moscow Times, 2016a). Russia's foreign trade fell not only with China but in general, due to a combination of falling demand and prices for hydrocarbons (Lukin, 2016), and, one can add, commodities as well. Nonetheless, if Russia had managed to effectively gear her economy eastwards and improve penetration of the Chinese market, the comparative fall in trade could have been restrained, but the downturn was bad exposing underlying significant problems.

Russia lacks the necessary infrastructure for transport and functioning of production capacity in the Far East. This was clear at the time of May 2012 Presidential Edict on the acceleration of development in the Far East. But it is unclear whether the authorities fully appreciated the extent of work and volume of investment that were necessary for just a slight take-off of regions burdened by longtime backwardness, poor governance and lack of skilled labour.

As mentioned above, the effects of the worldwide economic slow-down combined with economic and financial sanctions should be factored in when trying to assess the effective potential of the Russian eastwards strategy. A few noticeable trends appear from statistics in early 2016 that are used in what follows (ROSSTAT, 2016, 2017).

Total Russia's foreign trade January–November 2016–2015 year-on-year continued to fall though at slower pace than January–November 2015–2014 down to $417,984 million from 480,545 (at 87.0 percent vs 66.4 percent respectively). Comparing foreign trade with the EU and China in the respective years/time frame one finds that trade with the EU continued to suffer while it improved year-on-year (2016/2015 vs 2015/2014) with China. Over this period, in absolute figures trade with the EU fell from $217,225 million to $179,940 million (from 45.2 percent to 43.0 percent of total trade) while that with China increased from $57,787 million to $58,745 million with China's share in total trade, then, increasing from 12.0 percent to 14.1 percent. While it is too early to reach definitive conclusions from such a short time framework, moderately positive trends seem to be valued by Chinese experts that look forward to better economic cooperation perspectives than in the recent past.

While in 2015 the perception in China was that Russia had fallen into a “systemic crisis” and her de-industrialisation had perverse effects on the economy, in early 2016 authoritative economists affirmed that the worst for Russia is over and “business with some Russian companies can be carried out”. Magnanimously noting that Russia is the only country in the world capable of living on her own resources (Nezavisimaya Gazeta, 2016a, 2016b, 2016c), China seemed purposely to echo Putin's call for Russia's economic sovereignty as an attainable national objective against the application of western sanctions in early 2014.

For Russia and China to become strong commercial partners will take a long time, judging from the current situation. To date the major trade partners of China are the US for exports and South Korea for imports. Comparative estimates (before the fall in oil prices) indicate that Russia was only the tenth trade partner with a trade turnover of $89.21 billion versus the US$521 billion and even lower than Brazil (2013 estimate) with $90.27 billion, while the first five partners for their shares in exports were the US with 16.9% followed by Hong Kong 15.5%, Japan 6.4%, South Korea 4.3% (2014 est.) and for their shares in imports South Korea with 9.7% followed by Japan 8.3%, US 8.1%, Taiwan 7.8%, Germany 5.4%, Australia 5% (2014 est.) (CIA World Fact Book, 2015).

The approach of this paper is based on three interacting analytical vectors that should help highlight the potential of sustainable rapprochement.

First, the analysis focuses primarily on the process of economic cooperation, taking for granted that outcomes will need time to materialise. The process is one of mutual exploration, cumbersome negotiation, institutional adaptation, an approach that is complicated by different, often contrasting, interests. There are some results to date. But progress is slow also on the backdrop of significant cultural differences.

Second, at a stage when actors are moved by different incentives and a definite comprehensive cooperation agreement between the two countries is missing, institutional changes and individual business projects or contracts need to be brought into the picture as they help highlight how strong mutual policy commitments are, and to which extent they are dependent on policy and economy-wide strategies.

Third, a medium to long term perspective is analytically instrumental to assess how sound and feasible commitments and policies are. Work in progress, also including an established schedule of high level meetings, may help assess how solid or ephemeral is the character of any preliminary bilateral state agreement and whether economic cooperation is broadly consistent with the vision each country has of herself on the world scene. Within this outlook, the paper assumes that the time framework needed to assess results, no matter how reasonable schedules and deadlines do appear, must be flexible since unpredictable obstacles, of endogenous or exogenous nature, cannot be factored in. Delays per se cannot be swiftly interpreted as failures.

Leaving aside projections and outcomes regarding the volume of trade with China (to which the paper returns later in discussing possible improvements), achievements to date can hardly be assessed comparing facts and figures to plans and/or indicators of development. On the one hand, the time frame for sharp policy reversals is short – at the time of this writing less than four years from the publication of Putin's May 2012 Edicts. On the other hand, exogenous factors – such as the worldwide economic slowdown and relative price shocks, as well as selective economic and financial sanctions aimed at isolating Russia from her commercial partners – have an impact that is difficult to quantify separately, regarding the Far East, and in total for the economy.

While the scale of overall economic progress in cooperation cannot be meaningfully assessed, specific developments and failures are discussed at a high level (Putin, 2016a). 3 Published reports help to single out initial results as well as unexpected challenges ahead. Among the most important deals that, despite widespread scepticism, have been concluded and look promising in the efforts of Russia to seal cooperation agreement, two deals – the first on gas and the second on aircraft – need to be kept in mind. Fast progress towards lesser dependence on the dollar is also noticeable. But also medium-long term joint projects are envisaged and are beginning to take shape, as described in what follows.

The working meeting with Galushka (Minister for the Far East) and Trutnev (Plenipotentiary for the Far East and Deputy Premier) in May 2016 reveals Putin's concerns about the pace of approval.

Cooperation may take different forms: state with state, branches with branches, companies with companies. Priorities may change in time: from hydrocarbons (oil and gas) to other branches and differentiated products. At each level of cooperation one finds different objectives and their relative proponents. While at the state level national strategies matter, at the business level economic interests prevail. Although both countries are market economies, the horizons of different actors may not coincide. Means and constraints are also of different importance.

Gas deal

Much has been written on the gas deal agreed in May 2014 and signed later on in the year. Under the deal worth some $400 billion China was promised the supply of as much as 38 billion cubic meters of gas annually from the developments of Eastern Siberia deposits around Kovytka over 30 years starting from 2018. According to Chinese authorities gas will provide more than 10 percent of energy consumption by 2020 up from 6 percent in 2014. It was assumed that once deliveries begin, China would replace Germany as Russia's biggest gas market. Although the Sila Siberi project linked to the deal has been inaugurated in September 2015, a number of obstacles, including funding and China's economic slowdown, have intervened delaying completion of drilling of a number of wells and attached inspections (Russia Today, 2015a, 2015b, 2015c: Gazprom, 2016a). 4 Due to the tremendous fall in oil price, to which gas prices are linked, it would not be surprising that, under China's pressure, the parties will renegotiate the terms of the deal, thus further delaying the implementation of project (Nezavisimaya Gazeta, 2016a). 5 In this context, speculations are that Russia could try involve Japan and South Korea perhaps negotiating an extra trunk pipeline that takes the gas to the coast (Moskovskye Novosti, 2016). 6

In May 2016 Gazprom announced that only half of the 800 km of pipelines earlier planned will be built in 2016 and just 115 km had already been constructed (Gazprom, 2016a).

Deadlines may even be postponed to after 2020 according to officials in charge (Nezavisimaya Gazeta, 2016a).

This point has been raised by Richard Connolly in an informal exchange on Russia's energy projects in the Far East as distinct from those planned in the Arctic. Indeed, while Japan is mainly interested in Sakhalin 1 and 2 projects, Premier Abe during his visit in Moscow early May 2016 also manifested Japan's interest in the construction, among others, of plants for the processing of liquefied natural gas in the Far East (Moskovskye Novosti, 2016).

Nonetheless one point is clear: notwithstanding all sorts of obstacles and delays, the project is on and Russia remains, by and large, in control. In March 2016 China intervened with a $2.2 billion loan to Gazprom to help realise the project (Gazprom, 2016b). In the meantime Russia has negotiated with Germany the doubling of the Northern Stream (NS2) that is planned to run under the Baltic Sea bypassing Ukraine and be completed in 2019. This project should ensure, in principle, a privileged gas outlet in Europe despite sanctions, the antagonistic stance of EU energy policy, and US opposition (European Parliament, 2016; Lavrov, 2016b) and vested interests, but it may also be a signal to China that Russia's move eastwards does not entail subjugation to new partnerships.

Economic partnership encompasses both civilian and military outputs. Infrastructure for transport and communication is needed in both cases. The issue of whether economic cooperation should primarily be based on military output where Russia is strong rather than in civilian businesses has been raised in Russia by defence experts knowledgeable on China. China has been historically one of Russia's main customers for armaments. In the present geopolitical context one may expect a deepening of such forms of cooperation.

Arms trade with China dates back to the Soviet Union. Nonetheless, deals for the sale of more sophisticated weaponry to date suggest that political concerns may now be less of an obstacle to broadening the range and quality of deals formerly precluded under security concerns. In 2015, after more than four years of negotiations, a contract was signed with China for the supply of four or six battalions of S-400 anti-aircraft missile systems totalling around $1.9 billion. Following this deal a major, and surprising to some experts, deal was signed for the sale of 24 Su-35 fighters for $2 billion. Despite uncertain delivery schedules and the possibility that delivery will not start until 2017, this represents a path-breaking deal for its strategic implications against longstanding resistance in some circles vis-à-vis sales of advanced weapon systems. It has been noted that China was allowed to be the first customer in the field for both systems (Sputnik, 2016a, 2016b).

Cooperation in arms trade and investment is revisited below when discussing the possible upgrading of economic partnership to coordination on defence. Large scale joint projects in infrastructure and transport routes through Central Asia are also discussed below. These issues belong to a large extent to speculation about the future on the score of what has been achieved so far as well as foreign policy and security concerns. While, among experts, it is common to refer to slow progress in economic cooperation with China that this paper does not deny, it is also worth looking at some developments on the ground in the belief that cooperation can only be sustainable if it is supported by targeted institutions, profit-orientated business and peoples’ interests.

Moving out of the USD as a reserve currency

Concluding this section mention must be made of the new financial framework aiming at lowering dependence on the dollar and western financial institutions. This is pursued by China as well as a number of emerging market economies (EMEs) afraid to be caught in currency wars whether pulled by the depreciation of the USD carried out for some years ago after the crisis or the on-going depreciation of the Euro (with other reserve currencies trying to adjust). While EMEs could react by depreciating their own currencies – as many are – they still suffer greatly by either their trade structures or their external debt exposure. China has exploited this context to her own advantage, first by depreciating the renminbi (yuan), then by fostering measures aimed at upgrading the use of the yuan in international transactions.

In September 2015 the IMF finally agreed to the renminbi's status as a reserve currency. The effective inclusion scheduled for October 2016 entailed that the Chinese currency will contribute to the value of the IMF's SDR reserve asset and obviously have a voice on IMF's policy of disbursement (Knowledge Wharton, 2015; Rumny, 2016). As a reserve currency the yuan is expected to have a 10.92 percent weighting in the basket. Weightings are 41.73 percent for the dollar, 30.93 percent for the euro, 8.33 percent for the yen and 8.09 percent for the British pound. The dollar currently accounts for 41.9 percent of the basket, while the euro accounts for 37.4 percent, the pound 11.3 percent and the yen 9.4 percent (Bloomberg, 2015).

By end 2015 the yuan has been included among the Central Bank of Russia (CBR) reserve currencies (Kommersant, 2015) though the CBR was not yet planning to make use of them (TASS, 2015).

Currency swaps between Russia (ruble) and China (yuan) for an initial US$25 billion equivalent have been already implemented by end 2014 to allow direct transactions between the two countries. Similar swaps are under way between China and Russia with other countries, primarily the BRICS and the SCO (Shanghai Cooperation Organisation) members including four new members, Iran, Pakistan, India (also a BRICS member), and Mongolia (Koenig, 2015). Gazprom has already started accepting the renminbi for payment (Gazprom, 2015).

Both Russia and China have launched their own National Payment Systems to avert possible Swift-related sanctions/impediments. The Chinese cross-border renminbi settlement framework is complete and, although the currency in terms of value is far below (at less than 3 percent) the shares of the main western reserve currencies in the world, the intention is to gain world attention. In mid-September the People's Bank of China sent detailed instructions to 19 banks to start soon implementing the new China International Payments System (CIPS) (Wildau, 2015).

From her side, Russia has been working towards the implementation of her own National Payment System to escape the much feared Damocles’ sword that could have fallen on transactions by blocking access to the Swift international system; a fear justified by the interruption in March 2014 of the processing of payment via Visa and other cards under the sanctions regime. By the end of 2015 Russia had already launched its electronic payment card “Mir” to compete with Visa and Mastercard (The Wall Street Journal, 2015). Both cards have decided to access the Russian Payment System.

Russian banks may in a short time decide to connect with the Chinese inter-bank Payment system. That has been done by VTB (Foreign Trade Bank) via correspondent banks and test operations were successfully completed in late 2015 (Sputnik, 2016c). Efforts to debase the USD from important international payments may increase after Russia's access to Western banks was precluded by sanctions. Interesting from this point of view is that out of $12.1 billion credit allocated in April 2016 for 15 years by the Chinese Export-Import Bank and China Development Bank Corporation to the Arctic-based project of Yamal LNG (51 percent owned by the Russian Novatek) more than ten percent ($1.38 billion) is in yuan loans (9.8 billion renminbi) (Reuters, 2016; Vedomosti, 2016).

Such developments are often brushed away as irrelevant since international payments are still overwhelmingly dominated by the dollar. To put things in perspective however, it may be useful to recall that it took less than 40 years for the British pounds to be supplanted by the USD as shown by Aliber (1966) and Lindert (1969). In 1899 the share of the pound in foreign official holdings was paramount, with $105.1 million in pounds, $27.2 million in francs, $24.2 million in marks and $9.4 in other currencies. In 1913, the ranking was the same: $425.4 million in pounds, $275.1 million in francs, $136.9 million in marks, and $55.3 in other currencies. By 1945, however, the position of the dollar and pound, as measured by this statistic, had precisely reversed (Chinn & Frankel, 2008). The debasement of the pound occurred long after the US had conquered the largest share of world commercial transactions. China is not yet there, but approaching fast.

Business synergies

In the context of the programme of accelerated development of the Far East, to which the deals briefly discussed above refer, one should not underestimate the importance of independent business linkages through either investment from Chinese companies in Russia or Russian companies in China, and joint ventures. At this stage their value added is small, even financially or fiscally insignificant. What matters, however, is the cumulative process they may contribute to setting in motion. From this point of view business interest from other Asian countries also matters as it contributes to a certain degree of competition for capacity building in different branches among would-be investors and to the image of Russian Far East as a territory ready for taking off. While government policies and interstate agreements per se are necessary for a breakthrough in commercial relations and indicative of the direction of change, it is up to private investors to correctly interpret those signals when planning their businesses and trying to gauge profit prospects.

Government tried to do its part by setting up the so called Territories of Accelerated Developments (TORy) offering fiscal and administrative privileges beyond those generally accruing to the Special Economic Zones dispersed over the Russian Territories as access to leasing and/or ownership of land for productive use is to be made easier and an autonomous authority has been put in charge of the whole investment programme including networking with the local administrations for the provision of services to industry (Fortescue, 2015; Malle, 2016a). While on land provisions for investments there continue to be contentious problems that even the sharp and well-positioned plenipotentiary for the Far East and Deputy Premier, Igor Trutnev, has a hard time settling (Interfax, 2016a), 7 the federal government's intentions on the matter are clear and in principle beneficial for companies willing to establish their premises in loco since by law also services like electricity should be provided in a timely manner and on good terms. The law has been finally signed by Putin and entered into force the same day, on 2 May (Lenta, 2016). But implementation may still encounter obstacles if a system of incentives and sanctions acceptable to local administrators is not put in place and enforced. This may take time to develop.

Provisions concern relatively small plots of land that could be allotted to Russian citizens willing to exploit them productively in order to gain ownership titles after a few years. Local resistance from real estate speculators and their lobbies in local administrations is apparently the cause for delays in approving legislation according to Trutnev (Interfax, 2016a).

The results to date indicate that the largest share of investors attracted by TORy (12 to date) is composed of Russians. As reported by the Minister for the Far East, Aleksandr Galushka, out of the first 166 applications for industry, only 8 have come from Chinese investors. The Chinese are interested in building materials, oil refineries, metal scrap processing, frozen fish and other food stuffs. Interested investors have applied from South Korea, Japan, Australia and Singapore. Work has just started or is in process. Other projects concern infrastructure. While many projects are based on private–public partnership, the contribution from the state is minimal: out of a total of 945.6 billion roubles of investment, 877.5 billion (c.$13.3 billion) are private. The expectation is to reach soon 1 trillion roubles of investment (Rossiiskaya Gazeta, 2016a). Hopes are to expand production in already industrialised areas, such as Komsomolsk-on-Amur, known for the production of civilian and military aircraft, and around Vladivostok that has gained the status of free port, but total investment as reported above is small on a Russian, or any large country, comparative scale. The issue of granting free port status to a number of other ports on the region has been discussed at the early May 2016 working meeting of Putin with the ministers in charge (Putin, 2016b).

The total of 148 billion roubles invested in Vladivostok from private investors alone may signal, however, an increase in interest from profit-seeking businesses and pressures from China to expand investment opportunities. By a Memorandum of Understanding (MOU) signed in early 2016, Russia and China agreed that Chinese companies could settle in the Far East in several priority branches (building, metallurgy, energy, machine building, ship building, chemical, textile, cement, telecommunications and agriculture) in order to “create export-orientated production”. The Chinese side also promised to stimulate state and private companies to engage in this project (Forbes, 2016; Minvostok, 2016). It is unclear whether this entails financial support from the state, or state banks, also for private businesses.

The preliminary agreement looks as a major breakthrough since Chinese have been by and large mostly interested in extractive industry. At the end of 2015, the Chinese company Sinopec bought a 10 percent stake in the Russian petrochemical company Sibur and a consortium of Chinese investors purchased a 13.3 percent share in the Bystrinsky gold and copper project of mining company Norilsk Nickel (The Moscow Times, 2016b). There were speculations that China would try to benefit from the privatisation of the 19.5% shares of Rosneft (Rapoza, 2016, RBK, 2016), but more interested investors from the Middle East were more rapid in seizing this opportunity, confirming perhaps that China is not anxious or needs to engage longer in serious deals.

Priorities are identifiable when looking at different regional territories and how fast work in progress proceeds. In the Russian Far East plans of accelerated development were drafted in 2012. These plans, as discussed above, aimed at attracting investments from Asian countries, were primarily focused on China. Tax and other benefits were envisaged to attract investment, but the effectiveness of the whole institutional framework is still unclear.

As is known, China is primarily interested in importing advanced technology and know-how and exporting comparatively low-cost manufactures. In these areas, Russia is not a promising partner for the time being and, likely so, in the near future. Concerning technology, the country not only lags behind most advanced economies but is also locked into an uncertain path of modernisation that is hampered by sanctions from the West on the one side, and limited capacity to develop at home in the field, on the other. From the point of view of outlets that China strives to increase and diversify, her exports of manufactures to Russia are constrained by a low rouble, falling disposable incomes and, to a variable extent, the very policy of import-substitution enacted by Russia in practically all fields, including food processing and other consumer goods to counteract western sanctions (Connolly, 2016). This policy not only works against imports of competitive products, but also turns people's sentiments against China. Complaints that Chinese badly imitate Russian products and sell their fakes that do not conform to Russian sanitary and other legal requirements have become common in many fields. Agricultural products are also included. The case of sales in Russia of China-made honey under a brand used for honey produced in Altai (considered by Russians as extraordinary quality) was raised at a meeting of the All Russian National Front (ONF) with Putin as typical of Chinese behaviour and a caveat that this practice not only damages Russian brands, but also may become a perverse trend that risks taking root by allowing Russian firms be sold to the Chinese and/or allowing them to set up their own firms in Russia's Far East (Kremlin, 2016a).

While China – projected to become the world's leading importer of corn by 2023 – is looking forward to ways of meeting the rapidly increasing domestic demand for food, the exploitation of agricultural land in the Far East is not likely to be easy. To date Chinese firms lease or control 600,000 hectares of land in the Far East the total area of which is 616,932,900 hectares (The BRICS Post, 2016). This probably includes a large share of forestry (that counts for about 82 percent of total land). Agriculture by Chinese farms is not developed. It may in the future, given strong interest and abundant workforce on the part of Chinese vis-à-vis shortage of Russian labour, but under strict production rules, processing and time constraints. Russia is not keen to surrender land ownership. This was made clear by Galushka after his April 2016 meeting with Chinese counterparts in Beijing and focused in the heading of his interview (Rossiiskaya Gazeta, 2016b). The Minister noted that the “Russian workers are the priority and then foreigners who will not have problems with adaptation; those who know the Russian language, and are close to us in history and culture.” Only in the event that those are not enough, the labour market will open to other sources. Galushka stressed that in the framework agreement with China for the creation of the Russian-Chinese Agrofond it was agreed that at least 80 percent of employees on joint projects – must be Russian workforce.

While such details are perhaps publicised to assuage Russian nationalist critics (Sivkov, 2016) 8 and de facto immigration is likely to take place, written clauses show Russia's hesitancy in opening up to her powerful neighbour. Welcoming in the Far East Chinese companies known for pollution and lasting environmental damage is a risky policy many bitterly object to (despite Russia's not exemplary record in this context) (Eurasian Daily Monitor, 2016). Similarly, claims that Chinese farming does not conform to ecological rules and its use could hamper Russia's pledge to abide by international agreements in this field are also recurrent. Large demonstrations took place in mid-2015 in the Baykal region against the leasing of more than 100,000 hectares for 49 years to a Chinese company – with provisions allowing the concession area to double in case of success (ABC net.au, 2015; Russia Beyond the Headlines (RBHL), 2015a, 2015b). 9 While economically sound in principle, the issue of land rights discussed in the Ministry for the Far East together with the project of TORy is one of the most sensitive and apparently more difficult to work out, agree and/or frame into a compromise with all interested parties as mentioned above.

Konstantin Sivkov (a leading specialist in military and strategic affairs of nationalist orientation) argues vehemently against TORy as the fifth column designed to annihilate Russia through dismissal of state property, privatisation and immigration (Sivkov, 2016).

The company promised to build a 100,000 cow-dairy farm, the biggest in the world according to Australian reports (ABC net.au, 2015).

The problem lies not only in developers’ and local bureaucracy's vested interests, but also in the institutional vacuum on property rights inherited from Soviet Russia as manifested by the lack of a proper cadastre. The cadastral value is carried out on only a small part of the Far East District – Trutnev admitted while trying to prevent a situation in which the new right holder shall be issued rights to land that is already owned. To move on, nonetheless, it was established that the allocation of one hectare to each individual claimant will start in the pilot regions of the Far Eastern territory, supposedly those possessing a cadastre (Interfax, 2016b). This problem has emerged in relation to individual property rights to land reserved to Russian citizens willing to invest in the Far East. It is hoped that a million young Russians will move to the Far East where they could exploit free land for any legal use. The time frame of such visionary hopes is not explicit. While the authorities clearly hope for major labour movements to the East, they try to dispel fears in the region. By February 2017 the authorities reported only 50,473 applications (Na Dal'nii Bostok, 2017). It is in 2017, however, that applications are expected to shoot up from Russians other than Far Easterners, who had priority in access (Galushka, 2017). To avoid speculation (of which such plans have been accused) the plots of land will be no closer than 20 kilometres to settlements with 300,000 or more residents; and no closer than 10 kilometres to towns with 50,000–300,000 residents (Siberian Times, 2016a). 10

Indeed not too dramatic distance preventing that land, eventually put together by single owners, could be developed into real estate as noted by Siberian observers.

The lack of a cadastre may also impinge, through feeble contract enforcement, on the leasing of land for production (including agriculture). On the backdrop of shaky property rights to land bringing about high transaction costs, it is perhaps surprising that Chinese (and other) companies have settled in certain areas and are working in a variety of fields. More than 300 Chinese enterprises have investments in the Khabarovsk region, accounting for 45 percent of the regional FDI. At the beginning of 2016 total Chinese investment into joint projects on trade, catering, construction, wood processing and exploration work in Khabarovsk was 1.2 billion rubles ($16.5 million at the current exchange rate) (Siberian Times, 2016b). Resorting to joint projects is perhaps a sensible safeguard for contract enforcement by Chinese investors. One cannot exclude, however, that step by step (or bribe by bribe) this could evolve into full property rights. But more is needed to attract Chinese investment.

Despite long experience investing in different continents Chinese companies are reticent to invest in Russia. The local environment, of which Chinese companies have no control, is problematic.

A major impediment to investment is the state of infrastructure in Russia. This section deals with a general infrastructure plan considered, and approved in 2016, in support of investments in the Far East, before discussing the issue of transport routes in Central Asia in the context of the One-Belt-One Road Project pursued by China.

Important documents for the Far East were approved on 18 March 2016 (Government, 2016). A government bylaw (rasporozhenie) approved the budget for the creation and reconstruction of infrastructure in the framework of specific investment projects for the Far East and Baykal region. This is a field where private investment is discouraged by the long-term and risky time frame for returns, while Russian public investment is notoriously inefficient. It remains to be seen whether pressures from foreign investors succeed in mobilising both private and state energies. Chinese long and by and large successful experience in road building should be exploited. Infrastructure includes, among other things, transport (routes, bridges and railways), electricity networks and transformers, gas pipelines for a total amount of subsidies equal to 23,431 billion roubles for the realisation of 9 investment projects that include 7.19 billion roubles allocation in 2016. Unsurprisingly this infrastructure is projected mainly in support of extractive industry investment in ore mining and mineral processing, gold mining, coal mining, but also in support of the viability of the Vanino seaport and two food-related companies, one for the production of beer and the other a pig raising company both in Kamchatka, with the highest volume of subsidies allocated to gold mining and the Vanino port. The sum allotted in 2016 is much higher than the 2.7 billion roubles allocation in 2015, owing to the inclusion of three additional projects compared to a year earlier. The nine projects were selected from 54 applications.

According to Minister Galushka private investments add up to 218 billion roubles with expected fiscal revenues to the budget of 131.5 billion roubles in ten years (Kommersant, 2016a). It is known that China has invested in gold mining and that the Vanino seaport, one of the largest for cargo volumes in Russia, is instrumental for oil and other shipments to China. In 2014 China's CAMC Engineering Company considered funding its development. Close to the Strait of Tartary, the capacity of this port was projected to increase from the current 10 million tons to 100 million by 2020 (Eurasian Businesses, 2014). Shipments from Vanino reach Shanghai in 7 days serving also the closer ports in South Korea and Japan. In September 2015 Chinese officials promised to increase funding works to increase the capacity of Vanino port by assisting the China Yingkou Port Group already working for its development (RIA, 2015). Like other projects with Russia this is taking time, but there seems to be an authentic interest on the part of China that may bring fruit if the economic situation in both countries improves.

Improvements of Far East infrastructure are tied to specific production investment projects and extractive industry and aim at better linking the production facilities with already existing sea or railway outlets and adjusting the latter capacity to more ambitious targets. They are of direct interest to Russia and complementary, to a variable extent, to Chinese companies planning to invest in Russia depending on their actual prospects for growth and profit in fields of interest that may or may not be durable in the medium to long term.

Cooperation with China in the realisation of the Silk Road project is a much more complex issue and a more demanding project if Russia strives not to lose control of the region. It is of indirect economic interest to Russia, though surely a matter of security concern and an opportunity to better link with Asian partners not only in the realm of integration plans within the EAEU, but also in view of possible military or terroristic threats on a wider regional scale.

The project was aired just before the encounter of the Chinese and Russian leaders at the 9 May 2015 Victory parade in Moscow. No comprehensive route plans have yet been approved. A discussion still goes on as to whether it would be better for China to develop her maritime route to Europe rather than struggling to implement land routes that necessarily will touch upon the interests of the countries concerned by inclusion or omission. This does not mean, however, that segments of the One Road-One Belt are not being pursued by China through bilateral agreements with Central Asian countries and contiguous states in the Middle East.

An intricate network of motorways has been realised or planned jointly by China and Central Asian countries. As explained in detail by Mordvinova, China already invested and/or planned to invest more than $1 billion in reaching out to Central Asian countries with which active trade and investment plans have started ten years ago at least in some cases (Mordvinova, 2016). China focused on improving routes through impervious borders and connections with her own investments in the region.

China proceeded according to a plan allowing trade to reach more easily Central Asian countries. In the first stage motorways were extended from Chinese Kashgar in the province of Xinjiang to the borders with Tajikistan and Kyrgyzstan. In the second stage China contributed to the reconstruction and modernisation of motorways passing through the borders, including those situated on the mountains with both countries that allowed a sharp increase in trade. China invested $100 million to link Osh (in Kyrgyzstan's Fergana Valley) – Sary-Tash – Irkeshtam, a project completed in 2012. The third stage concerned the improvement of road transport from the borders to the two countries’ industrial centres and major markets. The reconstruction of the transport route, through high mountains, from Kulma through Korog and Kulyab to Dushanbe in Tajikistan as well as that linking Bishkek – Naryn – Torugart in Kyrgyzstan, on which China invested $200 million, is planned to be completed in 2016 also shortening transport times to Kazakhstan. A more strategic project is the motorway from Jalal-Abad to Balychki through Kazarman, Chaek and Kochkor in Kyrgyzstan, the cost of which is estimated altogether as $697 million, the sum of direct investment and credit to Kyrgyzstan. Work is in progress.

Concerning Central Asia, China also moved to better link Tajikistan to Uzbekistan supporting Tajikistan with a credit of $281.2 million at 2 percent interest rate for twenty years for the reconstruction of the motorway from Dushanbe to Chanak (on the Uzbek border) through Khudjand. This motorway is already functioning as is a 61.5 km highway linking Dushanbe to Uzbekistan through Tursunzade. While China did not directly invest in it, the building tender was carried out by China Road together with the Bridge Corporation.

These works are a prelude to the One Road-One Belt maxi project linking Western China to Western Europe through Kazakhstan that is projected to be completed by 2023, apparently also thanks to European funding. The construction of the highway through Xinjiang and Kazakhstan, which comes to the border with Russia in the Orenburg region, is already completed (Tkachuk, 2016).

The intricate network of transport routes in Central Asia, summarised in this paper from Mordvinova's presentation, shows that China's economic expansion, involving trade and investment in the region, started in the 2000s while enjoying two-digit growth rates with a view to expanding further depending on market opportunities. Transport routes are also fundamental for Chinese investment in the region, an issue often neglected by the literature on the subject (Kommersant, 2016b). 11 When this process started, growth was also robust in Central Asia and appreciable in wealthy Europe.

China's investment projects in the region as well as her barriers to trade raise concerns in both Russia and Kazakhstan as reported from the region (Kommersant, 2016b).

While China was actively aiming at the European market, Russia was just hoping to become the bridge from Europe to Asia through the Far East, bordering the North-Western Chinese provinces. Was the creation of the Eurasian Economic Union conceived as a barrier against China's expansion in the region? One cannot exclude that fast growing China's trade and investment in the region had provoked economic and security concerns in Russia that were further exacerbated by the 2008–09 financial crisis.

Developments to date suggest, nonetheless, that mutual interests in cooperation have improved along with both side perceptions that the room for policy coordination on a broader than economic scale should be further explored, if not consistently pursued.

Notwithstanding her shrinking budget, Russia is still considering financing the prolongation of the Chinese transport track from Central Asia to Russia. Estimates are that it could cost up to 780 billion roubles to which the state should participate with 400 billion (Izvestiya, 2016a). Within the One Road-One Belt project the high-speed rail link Moscow-Kazan was included stretching for 770 km through seven Russian regions and cutting time from 12 hours to 3.5 hours, in which China promised to invest $5.2 billion of an estimated total cost of $21.4 billion, and is planned for completion in 2020-01. A China-led consortium won a $375 million contract in 2015 to build a track of it (Financial Times, 2016; Kommersant, 2016c; Russia Today, 2015a, 2015b). 12

While one would assume that China's participation was looked for by Russia for financial reasons, on the contrary, according to Russian railways officials, Russia had to bow to Chinese pressures (Korostikov, 2016). Financial Times 10 May 2016 in “The New Trade Routes: Silk Road Corridor”, reports lower estimated cost of the Moscow-Kazan railways: some $16.7 billion.

This project also attracts interests from foreign investors (Russia Beyond the Headlines (RBHL), 2016). While the Silk Road track to Europe is not yet decided, it is unlikely that China remains indifferent to Russia's strong desiderata not to be cut off although lagging economic recovery in Russia remains an obstacle.

This section outlines two developments in cooperation that point to progress in previously neglected paths. The first points to a deepening arms trade with China and other Asian countries. The second discusses Russia's increased efforts to turn associations formerly used for occasional policy dialogue with Asian countries into bodies geared to single out threats and contribute to enhanced security in the region: a field where Russia could exploit her own skills and experience and coordinate ad hoc policies with China.

Developments in arm deals, which both countries do not hesitate to call strategic, that were formerly precluded, but are now conceded in the framework of partnership with China, have been discussed above. Taking into account China's overall dependence on Russian weapons, one notes that over 2011–15 the share of China's arm imports from Russia went up to 59 percent below that of India's imports from Russia (70 percent). Other exporters are France and Ukraine – 15 and 14 percent respectively over the period (Kofman & Sushentsov, 2016). In sum, China's dependence on Russia is strong. It may grow further as China is stepping up the modernisation of her army, fleet and air force under a new strategy aimed at ending longstanding isolationist policies and her neutral stance on international conflicts, becoming a more assertive military power in the world, as already manifested in rescue operations in Yemen and the establishment of military bases in the region. This strategy, already launched, should be fully implemented by 2020 (Kashin, 2016a; Manukov, 2016). 13 Time will show whether Ukraine, whose production chain is now detached from Russia, can remain a significant exporter, or will be supplanted by Russia. The deal went ahead despite strong doubts that it may not (Khramchinkin, 2016). Moreover the current geopolitical context does not suggest that partnership with NATO arms producers would be more welcome. Russia's notorious experience with the French ‘Mistral’ helicopter carrying landing craft must be a warning.

The strategy is exposed in China's 2015 White Book, a document considered to be of utmost importance by Russian experts (Kashin, 2016a; Manukov, 2016).

Cooperation on arms trade may even increase if both countries find it mutually advantageous and Russia drops her concerns on selling sensitive output that incorporate high tech IPR. Interesting in this regard is Vasily Kashin's argument that economic cooperation with China should not just leave room for military output, but focus and expand on arms where Russia's comparative advantages vis-à-vis China, as well as major arm dealers in the world, are strong (Kashin, 2016b). China should be approached as a strategic partner, not just as a peer among many, Kashin argues. In fifteen years from 1999 when bilateral trade was as low as $5.72 billion China has become Russia's largest trade partner despite economic difficulties in both countries. But commercial linkages and information, apart from defence and a few companies, are not as developed as they should be exposing business relations to the risks of variable economic trends.

Neither Russia's hydrocarbons nor Chinese manufactures can assure sustainable economic cooperation. On the one side, falling oil prices damage Russia, and, on the other, rising labour costs cause China's gradual loss of her role of ‘global assembly shop’. Traditional comparative advantages are falling apart. Thus, in Kashin's view, the countries may face a decline in economic relations in the long term. To counteract this development, a more consistent approach to cooperation should be built weighting the impact of threats common to both countries. Such threats are nested in the policy of sanctions that has become the standard response to foreign policy crises by the United States and its allies. Drawing from the March 2016 US restrictions on the purchase of American components by ZTE, a Chinese company in electronics, triggered by cooperation of ZTE with Iran, Kashin argues that China will be increasingly confronted with the threat of sanctions from the West.

To stem these risks, China's military-industrial complex should be seen as Russia's most promising partner in promoting cooperation on non-military industries as well. On the one hand, Russian inputs for a long time have been part of the supply chain for the manufacturing of part of Chinese defence industry; on the other, China is benefiting from import-substitution enacted by Russia against sanctions hitting her military complex. Sanctions have helped synergies to grow in the military complex. But these could be better exploited, Kashin argues, considering that Chinese manufacturing by defence corporations is much more diversified than in Russia, producing a wide range of civilian output, while Russia maintains large advantages in producing purely military output. Moreover Russian state and private companies have already been working with Chinese defence companies in the civilian sphere. The conclusion is that both countries could benefit from better industrial integration at the national level. A permanent Russia–Chinese coordination centre with the assistance of a specialised joint financial unit could foster such development. Cooperation in civilian industry will grow out of such synergies.

Kashin's approach to cooperation with China is unique and definitely opposed to that of Russia's nationalists. It may help explain the relative relaxation in selling high tech aircraft to China as well as the intensity of Russia's efforts to activate other partnerships and/or pursuing arms trade in the region. Indonesia, Pakistan and other countries in the region are reported to be interested in Russian aerospace and cooperation in military technologies (ARMSTRADE, 2016; RIA, 2016a).

Though not as important as deals with China, deals with other Asian countries described by Kashin, if successful, may help pre-empt or make more difficult the capture of profitable markets by western competitors also interested in exerting political influence. In sum, economic cooperation, in this optic, would be subject to Russia's and China's perceptions of common threats and interests in stemming antagonistic action.

Finally, Russia has increased her efforts to reach out to China through collective bodies for policy dialogue, which are seen as vehicles for communicating Russia's foreign policy and security concerns and attracting support (Cooper, 2016). It should also be noted that Russia does not want to put all the eggs in one basket, thus multiplying meetings on defence with other counterparts in the world, such as Egypt, primarily, in North Africa and Argentina and Uruguay in South America (Nezavisimaya Gazeta, 2016c).

To conclude this article, it is worth considering some developments during 2015 and 2016 which point the way to possible future policy dialogue with Asian countries.

The milestone of security cooperation between Russia and China is considered to be the Good Neighborly Treaty of Friendship and Cooperation signed on 16 July 2001. The Treaty was preceded by the Spring 1999 NATO's intervention in former Yugoslavia and the self-proclaimed independence of Kosovo and concluded two days after an interceptor missile test had been launched by the US in the Pacific (Symonds, 2001). 14 Though unbinding, the Treaty specified that the two parties will have immediate contact and consultations should any of the two parties perceive circumstances that may threaten and undermine peace or its security interests. Focus was on strengthening coordination with the UN and stability in the region, as well as on active cooperation in fighting terrorism, separatism and extremism (Cohen, 2001; Good Neighborly Treaty, 2001; Yu, 2001). 15 This document was seldom referred to subsequently, but Russian authorities, perhaps mindful of China's sensitivity regarding relations in Asia, exhumed the Treaty on the eve of the international meeting of the ASEAN countries in Sochi end May 2016 (Fenenko, 2016; Ivanov, 2016). With the turn to the East, the number of meetings where foreign policy and security issues are discussed has rapidly increased, as noted by a high level Chinese official, and, at a meeting with his Chinese counterpart, Shoigu stressed that Russia highly values contacts at both the state and military level announcing that more joint exercises and measures are planned than in the past (Kommersant, 2016c; Military, 2016a).

This event followed a more serious incident in March 2001 which caused the death of a Chinese pilot. On the crash in China of a US spy plane whose crew was taken into custody by Chinese and released only after the US apologised for the incident as reported in http://www.historycommons.org/timeline.jsp?timeline=us_military_tmln&us_military_specific_cases_and_issues=us_military_tmln_spy_plane_crash_in_china, accessed 31 March 2016. For a critical view of the US policy, see Symonds (2001).

The Treaty was ratified by the respective legislative bodies on 28 October 2001 in China and 26 December 2001 in Russia (http://www.freerepublic.com/focus/fr/558677/posts and http://www.pravdareport.com/news/world/26-12-2001/24277-0/ both accessed on 26 December 2015). Cohen (2001) argues that the motivations for the Treaty involve serious geopolitical, military, and economic considerations.

Russia has many arenas for policy dialogue on defence and security cooperation in Asia among which the CSTO (Collective Security Treaty Organisation, involving Russia, Armenia, Belarus, Kazakhstan, Kyrgyzstan and Tajikistan), and the Shanghai Cooperation Organisation (SCO) with China and other Central Asian countries are preeminent. The CSTO has formed groups of regional and interregional armies of up to 20,000 men. Exercises take place regularly trying to raise the standards to NATO – Allied Rapid Reaction Corps level (Periscope, 2016). 16 Members of the Shanghai Cooperation Organisation are Russia, China, Kazakhstan, Kyrgyzstan-Tajikistan, and Uzbekistan. Afghanistan, Iran, Belarus and Mongolia have observer status, while pending signature on a number of documents and ratification, India and Pakistan are already listed by SCO as members (Infoshos, 2016; RIA, 2016b).

Mobilisation plans were among the principal matters of discussion at the CSTO meeting in Moscow on 15 September 2015 (Kremlin, 2015).

Russia may be invited to become a member of the Common ASEAN Community (Association of South-East Asia) created at the meeting of the ASEAN group in Kuala Lumpur in November 2015. Members of the ASEAN are Brunei, Vietnam, Indonesia, Cambodia, Laos, Malaysia, Myanmar, Singapore, Thailand and Philippines (Izvestiya, 2015). This group may also develop in time some forms of military cooperation. A meeting of the Ministers of Defence of the member countries, with the participation of a Russian Delegation, took place in February 2016. The discussion focused on stability and security measures in land and sea areas and fighting terrorism (Military, 2016b). The meeting of ASEAN in May 2016 was used by Russia to strengthen bilateral cooperation with a number of countries, in particular Singapore and Indonesia, on economic matters (Kremlin, 2016b, Izvestiya 2016b). For her participation in several bodies definitely concerned with security in the region and thanks to a comparatively stronger defence apparatus and industrial complex Russia seems to be better placed than China in threading alliances, though disturbing China's complex foreign relations is a caveat.

The SCO could develop into a more important organisation for both China and Russia on security matters. Indeed, with the participation of Afghanistan in the Shanghai organisation as an observer from 2012, attention is increasingly focused on joint measures against terrorism (Infoshos, 2015a, 2015b; SECTSCO, 2014). 17 However, while pushing for a more focused role of SCO on security matters, Russia is attentive not to step into China's own strategy.

For many SCO should be a preferential arena for policy, rather than economic, dialogue as proposed by others (Infoshos, 2015a, 2015b).

At the Moscow International Conference on Security on April 2016 Russian defence minister Shoigu made three points: (i) Russia's military bases in Kyrgyzstan and Tajikistan are there to stay to fight terrorism as Russia is the guarantor of stability in the region; (ii) an institute of national military advisors at the SCO must be established and (iii) the SCO will not turn into a military political alliance. On the latter, both Russia and China have reservations. This may be due to nationalism that is on the rise in both countries and may turn into the main obstacle to partnership in defence as argued by Trenin (2015; Malle 2016a, 2016b). 18 Possibly, however, neither country is ready to concede much on foreign policy as long as each faces threats and concerns of different entity and intensity.

The patriotic role played by the All-Russian National Front (ONF) on several fronts is discussed in Malle (2016b).

Nonetheless, ties are hesitantly developing between CSTO and China. The issue of a possible merger between CSTO and SCO was raised at the Dushanbe meeting of SCO in June 2014. Military drills with China and other non-CSTO Asian countries were planned by CSTO in 2015 (CACI-analyst, 2014; Sputnik, 2014, 2015).

At the CSTO summit in September 2015 in Dushanbe, together with the approval of the CSTO's budget, cooperation was agreed among members regarding the transit of military formations and military goods; readiness inspections for carrying out the Collective Rapid Reaction Forces’ objectives, their composition and deployment (Putin, 2015). Measures to secure oil pipelines through the region are also being discussed (Infoshos, 2016). All these measures need participation and agreement by the EAEU and CSTO member countries and, obviously, financial commitment.

Financing broader security in the region is a challenge for low income countries. China's economic interest in stability may facilitate access to funding. The Silk Road transport network of which many tracks, as discussed above, are already implemented, has dual use. This is an asset that could make it easier to reach other agreements on security. The region hosts different, sometime antagonist players, and is getting crowded with outsiders whose vested interests are not always transparent. Disparate competition for control and threats of unrest are likely to bring Russia and China together.

There are remarkable challenges ahead to Russia's sustainable economic partnership with China. Nonetheless, measures to attract Chinese investments in regions contiguous with China and results to date do neither justify the critical assessment found in opposition circles, liberal and nationalist, in Russia, nor the hasty dismissal of Russia's turn to the East found among western commentators (Eder & Huotary, 2016; Gabuev, 2016; Khramchinkin, 2016).

Negotiations and deals agreed or in progress in a medium to long term prospect reveal difficulties, impediments and slow progress, but also determination on both sides to move forward. To a large extent, this is a reaction to trade policies overtly pursued against them by world powers. Interests do not coincide. Nonetheless the two countries are moving towards cooperative behaviour by threading a web of different paths: from interstate deals to companies’ joint ventures, from costly deals in energy and access of China to strategic branches to arms trade formerly banned, from coordination on infrastructural projects to joint participation in financing new transport routes in backward areas, from dependence on the dollar to national payment systems and increased use of own currencies in mutual transactions.

Turning eastwards entails institutional changes that need clear prioritisation under fiscal rules as well as large scale redistribution of land and reallocation of labour that face unfavourable legal and demographic contexts.

Some pillars of institutional change are already working and attracting investment though progress is slow, not least owing to economic slowdown in both Russia and China. Shipbuilding and military aircraft are now under the privileged umbrella of TORy (territories of accelerated development) and open to investment from China. Space-related R&D and output my also in time attract China's interest. The argument that partnerships with China should start from cooperation on military output where Russia is comparatively stronger has been prominently raised. It may or may not reach policy makers. But it comes out as an extraordinary proposal unthinkable until now.

In Eurasia Russia and China are competitors. But they do not need to fight each other. A process of policy dialogue has been put in place and is carried along with parallel initiatives in the Shanghai Cooperation Organisation and CSTO aimed at increasing security in the region. China might have preferred to be left alone to negotiate to her advantage on trade, investment and infrastructure with weak Central Asia in fostering her way to European markets, but Russia is not just a pawn in Eurasia's chess board. On the One Road-One Belt project a compromise with Russia that would take into account Russia's interests in the region has to be reached. A FTA with China through the EAEU would be welcome to Russia and Kazakhstan but long to materialise.

Far-reaching visions are not unusual among Russian leaders. China's approach is pragmatic and may be conducive to acceptable compromises. Before engaging in distant goals, joint projects and financing of high-speed links through Russia have been agreed with some tracks on the way to completion. Their possible dual use, if security concerns surge, would be an asset for both China and Russia.

Acknowledgements

The author is grateful to Julian Cooper and Stephen Fortescue for valuable comments on the first draft of this paper and to an anonymous reviewer for useful suggestions.