Abstract

The paper provides an overview of the Russian official plans of development of the international financial center (based primarily in Moscow) and tries to stimulate the discussion on the critical assessment of the perspectives in order to outline the efficient ways to achieve this ambitious goal.

Introduction

In the course of market transformation of the Russian Federation the country faces the big challenge of integration in the global economy. One aspect of such integration is the full-scale participation in the world financial system. The country has already done a lot in this direction – both the government and the private sector. High rates of economic growth in the 2000s created the new opportunities for financial development in Russia via high liquidity from the boom at commodities markets and inflows of private capital. Russia accumulated substantial international reserves and sovereign wealth funds which should be invested and efficiently managed.

Moscow has firmly established itself as the national financial center of the country which concentrates the bulk of the financial industry and of the financial flows. However from the international perspective the country is still dependent from the global international financial centers – primarily London and New York, then Frankfurt and now Hong Kong – with regard to big financial business (IPOs, long-term borrowings via syndications and Eurobonds, important M&A transactions). Moscow is still placed very low by the Corporation of London research team in the Global Financial Centers’ Index. Therefore the Russian authorities put forward the task to develop the Russian financial center of international standing which should be based in Moscow and probably later partially in St. Petersburg.

The present paper intends to start the discussion on the feasibility of such intentions and tries to assess critically the perspectives of the program from the present situation. The authors hope that such discussion would help the official circles in Russia and the international financial community to better understand the challenges and opportunities and find the efficient way forward. It proceeds as follows. Section 2 provides the brief overview of the Russian official program on the international financial center. Section 3 discusses the present level of Russia's involvement in international finance. Section 4 deals briefly with the issues of development of the Russian banking system. Section 5 goes on with the discussion of perspectives of further development of Russian banking and other financial sectors to meet the challenge of the international financial center. Section 6 deals with the specific issues of taxation and tax administration of the financial sector which is critically important for the endeavor of development of international finance. Finally, there is brief conclusion.

Official plans of the Russian authorities

The goal of development in the Russian Federation of the new international financial center was put forward by President Dmitry Medvedev in his first Presidential Address to the Federal Assembly of the Russian Federation in November 2008. Following the outbreak of the global economic and financial crisis the Russian authorities expressed the intention to open the new opportunities for financial innovation in Russia and try to increase the role of Russian ruble in the international settlements. 1

The principal official documents are the following ones: Government of the Russian Federation strategy, Government of the Russian Federation concept, Government of the Russian Federation action plan.

The starting point of official thinking is based on the view that Russia faces the dilemma: either it develops the financial market inline with the international standards and integrates it into the global financial market as one of its important parts or it loses the national financial market at all since the majority of financial transactions (including those of the Russian residents) move to other financial centers.

Since this is a complex task the more concrete policy guidelines were set in several official documents of the Russian government. These documents provide in-depth analysis of the practices of international financial centers and pre-requisites for their development and set the guidelines for development of international financial center in the Russian Federation. We will briefly outline the most important measures which Russian authorities are going to undertake on the way to achieve the goal.

The official documents specify the following pre-requisites for the development of Russian international financial center:

The large size of the national economy and its dynamic nature which should potentially create demand for the financial services; The high level of human capital which could be used in the financial services industry (since Russia has high level of education in mathematics, computer science, engineering and natural sciences, the people with such educational background should be able to successfully employ their skills in the most advanced areas of modern finance); The geographical location of Moscow between the European and Asian financial centers; Relatively high level of development of national financial market which already trades number of financial instruments including many derivatives, has two exchanges; Relatively close links with CIS countries and the absence of language barriers which opens the door for access of securities from those countries to the financial center in Russia.

However there is yet much to be done on the way to the financial center of international standing.

First, Russia should further develop its legislation and regulatory framework for financial markets and financial transactions. The most urgent laws which should be approved and implemented are those on exchanges, clearing, securitization and anti-inside measures. The Russian legislation should also be developed with regards to derivatives, collaterals, and infrastructure of the financial markets.

The development of financial center in Russia requires substantial development of national tax legislation and further improvement in tax administration. The financial sector is characterized by the relatively large scale of the volume of transactions in comparison with the financial result therefore the tax rules should be adjusted accordingly to put the tax burden on profit and not on turnover. The special measures should be taken to stimulate the long-tern savings of the population via the financial market which should create the long-term funds in the system to finance investments.

The functioning of the financial market is interlinked with the stability of property rights and the system of corporate governance. There is really much to be done in this area in Russia both in legislation and implementation via judiciary system. The high level of concentration of ownership in the hands of large shareholders put specific tasks for regulation of the relations between these subjects in addition to the protection of the interests of minority shareholders.

Second, Russian authorities find it important to stimulate the further development of the national market in terms of both variety and sophistication of financial instruments and financial market infrastructure. The wide range of measures includes such steps as IPOs in Russia, increase of free-float of shares of Russian companies (including those with the government controlling stake).

The country needs the modernization of exchanges, clearing and depositary institutions, payment systems towards more technically advanced level, centralization and transparency. However this could not be achieved efficiently via administrative pressure or legislative changes (e.g., forced merger of MICEX and RTC) but should be the logical outcome of the step-by-step development inline with the global trends.

Third, the Russian financial market should be gradually integrated in the global capital market. The foreign participants should get access to the Russian financial market, in particular, to exchanges more easily. At the moment such access is possible via two regimes – either registration of issue under Russian law or Russian depository receipts (RDRs). The Russian authorities don't see any distinctive advantage of any of these regimes and therefore are going to promote both of them.

At the moment, however, in order to trade at the Russian exchanges the foreign participants are required to register the legal entity under the Russian civil legislation and obtain the license of the professional participant of the securities market (otherwise they have to use the service of brokers). In the age of Internet and sophisticated IT this may create obstacles for foreign participants who wish to get the direct access to the Russian exchanges from their offshore offices and therefore undermine the competitiveness of Russia in the global financial market. The possible solution might be to grant the licenses of the professional participants to certain types of institutional investors which meet the requirements of the Russian legislation so that they escape the establishment of Russian subsidiaries.

Fourth, certain steps should be taken to provide the qualified personnel for the financial center. It's necessary to improve the quality of education in economics and finance in accordance with the modern international standards since at the moment only several advanced higher education institutions provide training of international standing. At the same time Russia needs to make easier immigration of foreign specialists and make steps to further improve quality of life in Moscow (rental costs, transportation, English-speaking personnel, etc.).

The Russian official documents don't set any quantitative targets for short-term perspectives since the global economic and financial crisis causes a lot of uncertainty at the financial market developments. The short-term priorities are focused on the technical issues of the financial infrastructure. However in the medium-term perspective (to 2012) the following economic and financial targets are set:

one of the Russian exchanged should be in top 12 exchanges in the world; the share of foreign securities at the Russian exchanges should be not less than 10% in terms of turnover; the share of financial sector to GDP should rise to 6%.

The further impetus to the project was done by President Medvedev in April 2010 when he had the special meeting with leading foreign financiers doing business in Russia and Russian officials in charge of economy and finance. The special task force led by former Chief of Presidential Administration and current Chairman of Board of Norilsk Nickel Alexander Voloshin was established to facilitate the legislative and regulatory changes and maintain the dialogue with the market actors.

The period of market transformation in Russia started in 1992 and was marked by development of international economic relations with the rest of the world, growing economic and financial openness and integration of the country in the global economy. These developments led to the growing role of the Russian Federation – through different institutional sectors – in the world finance.

The main features of Russia's financial international links by the start of the global economic and financial crisis could be described as follows. First, Russia accumulated the third largest foreign currency reserves in the world (after China and Japan) which mounted to 582 billion USD at September 1, 2008. 2

Central Bank of Russia.

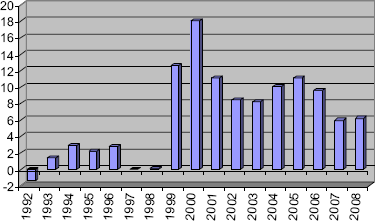

It's worth to note that during the whole period of market transformation Russia was the net creditor of the world economy since it maintained the positive current account balance (which means that gross national investment was less than gross national saving). In terms of gross figures the capital outflow from Russia in the past nearly two decades was more that 400 billion USD (Chart 1). 3

See Kozyrev & Berezanskaya, 2010.

Russia's current account as % of GDP, 1992–2008.

The evolution of the international investment position of the Russian Federation is shown below in Table 1.

International investment position of the Russian Federation, 2001–2009 (million USD).

Source: Central Bank of Russia.

The data shows the significant increase of the Russian involvement in the global finance.

The commercial banking system turned out to be the first sector of the financial system which developed in the course of the market transformation in the Russian Federation. 4

The overview of the research on the Russian banking system is provided in Sherstnev (2009).

See Stiglitz & Greenwald, 2003.

The development of Russian banking system was subject to numerous criticisms in the past years. However it's worth to notice that the development path of the banking system in Russia followed the same pattern as that of more advanced transition economies (Poland, Hungary and Czech Republic) but with less involvement of foreign financial institutions. Russia managed to develop its national banking system which withstood both liquidity and systemic crises in the last nearly two decades and rebuilt itself in the post-crisis periods.

The distinctive features of the Russian banking system are:

The large number of the credit organizations; The small size of the banking system relatives to the economy.

These features really give ground for doubts on the capabilities of such system to perform all functions of financial intermediation in the growing economy and were the milestones of critical remarks of observers and researchers.

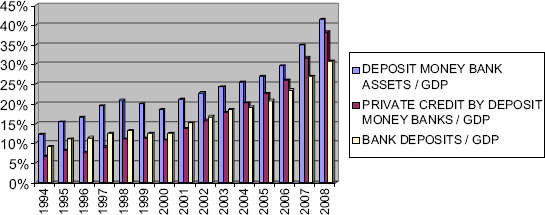

However the available data shows that the conventional financial depth indicators of the Russian banking system steadily increased in the course of market transformation. This process became even more pronounced in the 2000s when Russian authorities under President Vladimir Putin launched important institutional and legal changes in Russia and the boom at the commodities markets increased the available liquidity in the system (Chart 2).

Financial depth indicators of the Russian banking system, 1994–2008.

The increasing sophistication of the banking system in Russia which now offers wide range of services to both companies and private individuals forms the solid basis for further integration of the sector in the global financial market. At the same time these opportunities require further critical assessment which is provided below.

Talking about banking system we must remember that it is only a transmitter, an economy pump for forcing investment, savings, and money funds and for transforming them. Such a system helps to create an interconnection between government (an emission center and regulator), non-financial economy, financial market and general public. These connections should bring effective and rational economic growth, balanced economic structure, innovative development and rise in standard of living. That's why banking system status can tell us about the development of the whole economy. From this perspective we can state that Russian economy is seriously ill. Its heart – banking system – doesn't answer the purpose of economy modernization and positioning the Russian Federation as one of the global financial centers and economic leaders. Russia is like Hercules, who cannot stand up and walk normally because of weak heart. Our small research has for an object to answer the question – will Hercules be able to walk easily and if so, when and why will it happen.

For better understanding first we will determine the opportunities of the Russian Federation both existing and potential, afterwards we will emphasize obstacles on the formation of powerful international financial center in Russia. Let's make a reservation: the only megalopolis to be such a center is Moscow (64% Russian banking assets), other big Russian cities are not able to compete with Moscow and Russian officials have no plans of creation artificial megalopolis. It is one of Russian traditions – the capital is uncontestable political and administrative together with economic and financial center. In our opinion, it is country's “cancerous growth”, but to change this government position seems impossible (it is the object of a different research). We should also mention that we will take into consideration only banking system, because non-bank financial institutions in Russia are undeveloped and have no real influence on the economy. Therefore it's impossible (at least until a powerful banking system will be formed) to enter the global financial market and to occupy an advantage-ground with such institutions (investment funds, pension funds, insurance companies).

Opportunities

The Russian Federation attained status in geopolitical and geoeconomical space.

Russia as an active member of G8, G20, World Bank, Paris Club of Creditors, FATF, APEC, BRIC and others international organizations. This constructs the necessary institutional environment for the future international financial center. In spite of all disproportions Russia is acknowledged as a country with market economy and year in, year out the Russian Federation penetrates deeper into the global economic process. Undoubtedly Russian banks receive favorable institutional environment for a rise in their capitalization and widespread expansion on the world financial markets.

Significant factors of national wealth – background of banking system's generating.

Expert judgements show that nowadays Russia uses its national wealth only by 8–10%. It includes rich deposits of mineral wealth, land, agricultural holding, real estate and intellectual property. If all these resources are involved in financial turnover particularly with the help of pledge mechanism used when crediting and issuing money supply, banking system will be able to raise its assets promoting qualitative economic growth of the whole country.

Favorable macroeconomic and financial situation in the country.

Brief description of the favorable situation:

available considerable gold and exchange currency reserves (448.6 billon $ on 15 April 2010); huge amount of state savings (about 190 billion $)

6

See Conception of Russian financial market development, 2008, table 10.

effective and consistent government policy: budgetary and fiscal, monetary and financial, capital flow regulations – on the one hand aimed at maximum liberalization of capital and operating balance of payment transactions, on the other hand – government support of national banking system;

permanent reduction of bank rate and inflation controls (Central bank inflation forecast – 6.5–7.5% in 2010 7 );

See Ignatiev, 2010.

relatively stable rate of exchange has sturdy consolidation factors; opportunity of transforming Russian oil and gas payments into rubles, creation of the raw materials exchanges (first – oil exchange in Saint-Petersburg) and movement towards free convertibility of rubles; possible creation of ruble zone in CIS countries and use of rubles as means of payment in BRIC;

good perspectives of private banking (the rich Russians have 300–350 billon $) 8

See Skogoreva, February 2006.

In 2009 in spite of crisis Russian banking system resisted in many respects owing to proactive government intervention particularly Central bank that allotted unsecured credits. Central bank efficiency is performed not only by stabilized system, but also by its income on such credits – about 200 billion rubles (net profit of all Russian banking system in 2009 – 205 billion rubles). 9

See State of Russian Banking Sector, 2010, pp. 4–7.

Foundation of significant universal state banks (banks with primary state interest) – Sberbank, VTB group, Rosselhozbank, Gazprombank.

These state banks form the base of Russian banking system; they own significant capital and assets together with confidence. Sberbank and VTB carried out successful IPO, actively enter the world money-market and market of capitals, carry out direct investment in foreign markets, including acquisition of non-financial assets (e.g. Sberbank purchasing claims in consortium with Magna to Opel, as a result GM on voluntary lines decided to pay an indemnity to Sberbank for fouled-up bargain). Listed Russian banks are able to compete with the key transnational banks from developed countries.

Besides government plans VEB IPO together with other development banks which today are state corporations.

Pent-up potential demand for bankroll from the direction of non-financial sector under the circumstances of essential thorough modernization of Russian economy and capital renewals.

President Medvedev declared this problem as issue of the day for our economy. Russia needs tremendous investment expenditures into industry, infrastructure, non-manufacturing business, housing and communal services. Banking system together with public and foreign investments at this juncture is supposed to become basic funding source while sources such as profit, depreciation and portfolio investment within the next 5–10 years right up to 2020 won't be of great importance in the investment process. Need for technoparks and technopolises, commercialization intellectual products, continuation of space technology, power engineering, and medicine and education development are of great concern for the Russian Federation. In this case appeal of Russian market for transnational banks of USA, France, United Kingdom, Switzerland, Italy and others is obvious.

Intense interest of first-rate world private banks in Russian credit market.

Number and weight of non-residents in Russian banking system permanently increases and at the end of 2009 makes up 24.53%. With all this going on according to the Russian laws foreign banks and insurance companies are not allowed to open branches and representative offices. Undoubtedly, foreign banks first of all give credits to ultimate consumers, general public (population), especially banks that are affiliated with transnational corporations. It is statistically corroborated. At the same time rise in standard of living and satisfaction of increased needs remains one of the critical goals of Russian economy. Therefore this factor cannot be referred solely to unfavorable factors.

Of course, the above-mentioned opportunities do not represent complete set, we emphasized only those of vital importance from our point of view.

Now let's turn to obstacles. They are greater and more serious than opportunities because they have already not potential but chronic substance starting with transfer Russian economy to market system in 1990s. All obstacles we may divide into external and exceptionally internal obstacles.

Major external obstacle is a global financial crisis. Last time Russia felt already two shocks – 1998 and 2009 years. In 1998 our economy and its financial system found itself on the verge of collapse and default, however in 2008–2009, as shown Central Bank statistics and forecasting information of World Bank, Russian financial system held out and came to stronger than industrial and human services sectors of economy. As some world-famed analysts mentioned, Russia has come out of crisis and become stronger than before. In many respects it has become possible owing to accumulated state funds and reserves and weak dependence of Russian financial market from portfolio investment, derivatives and compound financial instruments. There is no significant financial market in Russia in respect to the world market; our financial market takes up only approximately 1% of global financial market. On the one hand, this situation deprive Russia many financial shakes, and downfall of Russian stock market and ruble devaluation related first of all to falling down of oil prices. Russian financial market and economy have fallen deeper than any global key countries (financial market approximately on 30%, economy on 7.1%), but have shown faster recovery (for example, capitalization of Russian stock market has doubled in 2009; in 2010 increase of MICEX index will be expected at the rate of 15–25%). Russian market and economy have shown us an extreme volatility. Even during last months the forecast concerning Russian economic growth are being constantly revising towards increasing. At the beginning of February it has been about 2%, but now, at the end of April, the official forecast of Ministry of Economic Development is 3.1%; but in the opinion of the Head of Citigroup in Russia and CIS countries, Zdenek Turek it's already 5–6%. 10

See Turek, 2010.

We may be glad to it. But in our opinion the last crisis has shown the weakness of Russian economy, first of all in financial sphere and banking system, which couldn't support industrial sector (downfall of industrial production in 2009 – 19.8%). Banking system was obliged to stay with extended hand to Central Bank and Government itself. As mentioned by S&P, in spite of positive movements the process of recovering banking sector in Russia will be long and will take at least 2 years. If we continue comparing Russia with Hercules, so Hercules has appeared by “the bludgeon” in the form of state reserves but he cannot pick up this bludgeon for the time present. His heart is pinking. But on the whole, it will be well to note that Russian Government found out a certain maturity at the fight against consequences of global financial crisis. Reserves were used correctly although it has lead to lowering the living standards of large quantity of Russian citizens. As an example, for the welfare of banking system only in aspect of operations with credit instruments there were spent 785 billion rubles of the state budget, at that time all budget expenditures for provision of pensions in 2009 were 275 billion rubles and for recapitalization of banks there were directed only 75 billion rubles. 11

See Sokolov, 2009.

Now let's turn to internal obstacles, which cannot allow creating in Russia international financial center.

Excess dependence of banking system from state banks.

This dependence can break the development of private banking sector and direct credit resources to inefficient and state-controlled firms. In this connection there will come a time of new Russian stagnation – “zastoi” (the so-called “scenarios 70–80”). In international practice there is already the example of Japan. Japan suffered the so-called “lost ten years” in 1990s which were provoked by making a large quantity of zombie-firms with the aid of state-banking credit mechanism.

Big share of bad debts (non-performing loans) and overcrediting of Russian borrowers.

By the assessment of S&P bad credits amount 40% over the banking system (coupled with restructuring credits). As a result of this the agency expects the rising of credit portfolio in 2010 to a level of about 10%, 12

See S&P, 2010.

The absence in Russia remarkable investment banking sector.

One might see that on a global financial scale the Russian investment banking sector is absent. On the one hand, Russian Government has not to puzzle over the decoupling of commercial banking and investment banking, not to feel direct consequences of crisis by the way of failure of national investment banks. On the other hand, without remarkable investment banking the transformation of Russia into international financial center is impossible. The accelerated economic growth on basis of innovation, technological great advance and development of small- and middle-sized business is also impossible.

In our opinion it's one of the key obstacles.

Poor development of institutional investors and lack of wide range of financial instruments in Russia.

Unfortunately, in Russian financial market the part of investment funds, pension funds and insurance companies is utterly small (about 10–15%). It hampers for allocation of household's savings and transformation to the investment resources. At the same time the lack of many contemporary financial instruments and small number of security's issuers are leading to that Russian market which is not attractive for global portfolio investors. Russian financial market is entirely oriented on raw materials sector, energy and communication (10 first-rate issuers, which has occupied 80% of the market). As mentioned by the President of Samara Currency Interbank Exchange Professor Dr. Mescherov, in the last 10 years the number of issuers on Russian stock market didn't practically change, which is a catastrophe on a local scale, “lost ten years” of Russian stock market.

It's also one of the key obstacles.

Low level of household's savings, distrust for financial institutes and stagnation of consumption.

Distrust for financial institutes in Russia is deeply rooted; especially it had formed after the currency reform in 1991 when the depositors of Sberbank lost their savings. Despite the fact that these savings were returned it didn't offset even a half of damage. Another blow to the trust was happened in 1998 when the Government created the financial pyramid of short-term obligations itself. As a result of this there was the technical default and ruble devaluation three times more. Therefore the hope that today the trust for banks has been restored is not founded. Households actively invest in real estate overheating the market; or in foreign currency which leads to the withdrawal of these funds from national investment process. The number of households which have securities or shares in investment funds amount 8–10%. Banking system remains a sole alternative to consumption and quasi-investment demand, but household's savings are decreasing (25% of households has bank deposits – about 10% of all household's incomes) because of low incomes (average wages – 6500–7000$ per year) and low yield on savings deposits (keep within inflation).

And it's also one of the key obstacles.

There are also other obstacles which we may mention.

In conclusion, to sum up we can say that there are no chances for Russia to create an international financial center before 2020. In the best case it'll be possible to form a regional financial center for CIS and East Europe. The majority of opportunities are potential, and our society, business and the Government must work day-by-day, roll-up the sleeves and get down to work in order to transform potential into reality. As mentioned by Joseph Eugene Stiglitz, the objective is not to simply create strong healthy banks, it is necessary to create strong healthy banks which credit the economic growth. As an example, Argentina has shown that inability to do this can lead to macro instability in itself. Russia has not the right to do something similar.

Development of effective financial infrastructure within the concept of international financial center in the Russian Federation contemplates a reform of tax rules and procedures in respect of financial institutions, in particular, of the banks. At present there exist a number of issues of bank taxation that have a negative impact on the Russian banking system. 13

The discussion is based on the following sources (Goncharenko, 2008; Ignatova, 2008; Kalakov, 2008; Safonova & Zhukova, 2010; Tax Code of the Russian Federation).

First, in the opinion of majority of Russian economists, the main problem of bank taxation is an absence of effective mechanism that can stimulate banks to invest in a real sector of economy. Solution of this problem will gain a taxable capacity of economy, certain regions and industries, increase banking industry assets, enhance income of banks that will ultimately result in extra tax revenues received by Russia's budget system.

For increasing an interest of banks in long-term loans to real sector it is necessary to fix an opportunity for banks of tax deductions of income received from long-term loans to the priority industries.

Second, it is essential to amend the tax procedure of recognising an interest income on overdue loans originated by banks. The question at issue is a continuation of interest accrual in tax accounting on credits originated by the banks, even if the borrowers have stopped to return loans and pay interest. According to that, a tax charges on uncollected profit and effective banks yield decreases.

This problem becomes especially relevant in a period of crisis, when a lack of liquidity becomes pronounced and it is important to adhere to the Central Bank standards (especially, the bank standard of capital adequacy). There exist a number of methods to stop accrual of interest on overdue loans in tax accounting of credit organization, but each of them has its own disadvantages. These disadvantages can result in worsening of bank's financial statement (e.g., as in the course of write-off of non-received income by way of increasing the loan loss provisions (LLP) or in case of transfer of receivables to closed investment funds that requires extra LLP creation as well) or in recognition of severe losses on loans (in case of sale of lending portfolio to collection agencies) or in a very long and difficult process of recognition of overdue loans as non-recoverable in tax accounting.

Third, the financial derivatives play a key role in hedging of interest and exchange risks and contribute to financial result of banks. However, before 2010 there existed an uncertainty in the Tax Code of the Russian Federation with regard to the taxation of derivatives. The Tax Code has not contained an exact definition of a derivative and explanation of the differences between the derivative and the co tango transaction. Though the taxation of them differed, e.g. in respect of losses received from these operations executing: losses on co tango transactions reduced taxable profit of bank, losses on derivatives did not. The statutory tax provisions incompletely explained a market price determination of unquoted derivatives and a classification procedure of deals as hedging operations. These disadvantages have often resulted in tax risks uprising in banks.

Furthermore, the revaluation procedure for derivatives was not clearly defined in the tax legislation; in particular, there existed an ambiguity of the liability to revaluate derivatives on the reporting date. In this case, the banks face the tax risk in case of unrealised loss on derivatives.

At the end of 2009 the legislative act amended derivatives taxation procedures as follows:

A derivative definition has been introduced (including the definitions of a deliverable derivative and an estimated derivative); The derivatives taxation procedure has been improved (thus, the banks can reduce taxable profit on the amount of received loss on unquoted derivatives since 2010); The tax procedures of revaluation of claims and liabilities in respect of derivatives have been adjusted; The transfer pricing rules with regards to derivatives have been introduced.

These adjustments, that become effective since 1st January 2010, shall simplify the computation of taxable base on derivatives and significantly lower tax risks in case of detailed analysis of the advantages of mentioned amendments. However, there still remains a probability of tax risks upraise in banks on derivatives operations in the period from 2007 to 2009 (the time period that can cover a field tax audit).

Fourth, banks in Russia are the main participants of securities market. Effective taxation of securities trading can facilitate an establishment of friendly tax climate for investors, competitive growth of the national securities market and the international financial center development in the Russian Federation. Before 2010 the statutory tax provisions have not clearly explained the tax assessment in respect of operations with quoted and unquoted securities as well as market price determination of unquoted securities.

Changes in the legislation brought by the law in the end of 2009 and coming into effect since 1st January 2010 have amended these issues, improved transfer pricing rules in relation to securities trading, securities netting (clearing) procedure and the methods of sold securities cost deduction.

However, some ambiguities still remain. For example, the Tax Code of the RF doesn't clarify the possibility to use the securities prices fixed in negotiated deals mode & address orders of bidding process organizer for the purpose of market price determination when there are no deals in prime deals mode. Furthermore, it isn't clear, is it possible to consider the price of sale or another disposal of security as the market price based on the price of security deal that was the only registered by the bidding process organizer at the date.

Fifth, trading of precious stones and metals in the form of ingots by banks to legal entities and individuals is a subject to VAT. This suppresses a development of domestic physical precious metals market that is an instrument of currency risks hedging and making profits (e.g., in case of arbitrage and exchange transactions) for the investors. Tax legislation of the RF provides VAT exemption of precious metals sale by banks only in case of placing of purchased ingots to the metals account of the selling bank or, in other words, to the special bank storage. In such a case, when carrying out a physical transaction with the precious metal purchased to the account (e.g., a transfer of precious metals by client from the metals account in one bank to metal account of another bank or delivery of ingot to client in a physical form), bank shall ask for VAT charge. This procedure isn't clearly explained by the tax legislation and often it is very hard to work this in practice, since tax risks usually appear in banks hereof. As a result, banks often include VAT in initial price of precious metals to secure themselves from risks mentioned. Investors are usually not interested in investment in precious metals and stones in a form of ingots since losses occur at return sale to the banks, because a purchase by banks of precious metals and stones is not a subject to VAT regardless of seller.

The Russian Bankers’ Association is deeply involved in the process of reforming of bank taxation legislation by virtue of providing the roundtable discussions with the participation of the representatives of the Ministry of Finance and the banks members for the purpose of discussion of mentioned and other issues, working out draft laws and return them to the State Duma of the RF for the appraisal. It ought to be noted that these actions positively affect the tax legislation.

The development of the international financial center in the Russian Federation – the goal which was set by President Dmitry Medvedev – is really a big challenge. Though the Russian government put the concise program its practical implementation faces serious difficulties. The project of such scale and scope affects various sides of the functioning of the public and private sectors.

The most important obstacle is the insufficient level of financial development in the Russian Federation. Even the Russian banking system – the most advanced part of the national financial industry – provides less intermediation than its counterparts in developed and advanced emerging economies. Other sectors of financial industry – especially those providing the vehicles for long-term saving and financing – are even less developed. The other obstacle is the low level of public services and public administration (including corrupt practices of all level of state bureaucracy) which is the big issue for the whole Russian society.

However the 2000s economic growth allows also looking with some optimism for the project. Gradually Russian financial sector is developing and increasing its technical and instrumental sophistication. Russian government and business become more and more involved in the international financial markets – both as creditors (investors) and borrowers. There is no doubt that the commitment to such ambitious goal will have its own positive impact of the further financial development in Russia and the arrival of serious big international business will put new level of discipline on both national business practices and national administration.