Abstract

In March 2010, the Europe 2020 strategy was released as the follow-up to the very ambitious Lisbon Strategy. Like its predecessor, the strategy aims to increase Europe's competitiveness in the world economy. Also like its predecessor, Europe 2020 is likely to be ineffectual. The strategy focuses too much on areas that are outside the EU's legal competence, it lacks recourse for non-compliance and it contains goals that have very little to do with increasing competitiveness. The probable failure of Europe 2020 could have been avoided had the European Commission focused on policy areas over which the EU has competence, and had been given the tools to accomplish the goals that were outside its competence.

The campaign for a ‘growth and competitiveness agenda’ for the European Union is once again gaining momentum. This time it is called the Europe 2020 strategy and it aims, modestly, to shepherd Europe into a new era of reforms to advance smart, sustainable and inclusive growth. European leaders have endorsed some of the broad ambitions of this strategy and will soon endow the agenda with more detailed targets.

It is about time, many would say, for Europe to focus on a growth policy. The European economy has trailed other developed economies over the past two decades. And the economic crisis, according to the official story, has forced governments to put long-term issues such as improving competitiveness on the back burner. But with the recovery looming, even if at slow speed in some European quarters, governments can now afford to look at policies to boost economic growth.

This is a rather sanitised version of history. The Lisbon Strategy, the predecessor to the Europe 2020 strategy, aimed to transform Europe into the most competitive economy in the world by 2010. We all know how well that turned out. What is less well known, however, is that the Lisbon Strategy was so badly designed that the EU would never have become the most competitive economy in the world even if governments had delivered on their promises. The Lisbon Strategy mixed high and low, and did not distinguish the really important reforms from the not-so-important ones.

For example, sustainable development was parachuted into the agenda as a key item for increased competitiveness. Few would disagree that sustainable development is important, but it is a symbol of the mess that was made of the pro-growth Lisbon Strategy, in which targets such as halting the loss of biodiversity and promotion of renewable energy became central issues on a policy agenda for competitiveness, while key growth areas such as international trade, where Europe has strong centralised policies and a record of success, were not even part of the initial Lisbon Strategy [2]. It took 6 years before a trade strategy was annexed to it.

So the Lisbon Agenda was a confused strategy with conflicting ambitions that silently disappeared from the centre of EU politics long before the crisis started. It existed as an item for discussion at many EU summits—and its importance was praised by everyone. But it was honoured in the breach rather than in the observance. It was, to use Alastair Campbell's memorable phrase about a recent leader of the British Conservatives, forgotten but not gone.

Misguided views

Only the childishly innocent think it will be different this time. The Europe 2020 strategy has fired up the chattering classes in Brussels. But it is a sign of the ambitions and the profile of the strategy that it panders mainly to those who believe governments can steer economies to growth and that the solution to every economic problem in Europe is stronger policy harmonisation.

Such views are mistaken. They hide three important aspects of the European growth experience—both recent and past.

First, economic performance in Europe before the crisis was diverse, including some high-growth countries and some laggards. The oft-expressed view of Europe as a declining region of sclerotic growth and a general lack of dynamism in the new world of globalisation and rising economic powers in the Far East is certainly true for some countries. But as a characterisation of all European countries, it is certainly false. Some countries in Europe, including those among ‘older’ Europe, have performed well over the past decade. They all tend to have taken economic reforms seriously and have concentrated on sectors and areas where they have well-developed skills, successful and outward-oriented companies and overall good comparative advantages. A fairly large group of countries have performed reasonably well, while seven or eight countries have been lagging behind, mainly due to political forces blocking attempts to reform their economies.

Second, the managerial approach to a European growth strategy neglects the important growth-enhancing role played by institutional competition among European countries over the past 50 years [1,7,8]. Most forcefully, institutional competition has been pushed by the reduction of barriers to trade within Europe. Such reforms, accomplished by policy harmonisation, have exposed domestic institutional structures to greater competition. They have been guided by a proscriptive view of harmonisation, a view that emphasises a ‘negative’ agenda: rules for what governments cannot do. This is in opposition to a prescriptive view of harmonisation, a view that underlines the ‘positive’ agenda: what countries should do and how actors should behave. It is policy harmonisation based on the latter view that has recently come to guide much of the integrationist agenda in Europe and, by accident or design, has diluted the forces of institutional competition.

Finally, the belief that one central strategy can fit the entire European Union, with 27 disparate economies of different profiles and reform requirements, borders on a central-planning mentality that can only damage economic growth. Too often European policymakers fall victim to the view that Europe is a uniform economy and that its member economies all behave in the same way. Such a view has political appeal and panders to those countries that are poorer, less productive and less advanced overall in their industrial or services sectors. Nevertheless, it is an uninformed view. There are significant differences—even if all the new Member States are excluded from the analysis. While Germany has grown in the past years through an expansion of the industrial value added sector (up by 5% in the 5 years prior to the crisis), industrial production and expanded value added in services in the United Kingdom shrank (industrial value added fell by 15% in the 5 years prior to the crisis). The ratio of services to industrial exports fell in Germany and Sweden, while it increased rapidly in Spain and the United Kingdom. The profile of services exports in Spain and the United Kingdom, however, differs fundamentally, and the differences have increased over the past decade. This is good news: increasing specialisation in trade reflects increasing specialisation of production. The greater the divergences are within Europe, the more Europe stands to benefit from borderless trade. However, for those charged with forging an agenda for growth, such differences present political and administrative difficulties.

The fear of new economic powers

The Lisbon Strategy had some good targets that, if met, would have benefited all economies. It called for a borderless market for services and introduced some deregulation in sectors such as telecommunications. But if that agenda put too little emphasis on freeing up Europe for commerce, there is hardly anything of that calibre in the 2020 strategy. Once the 2020 strategy enters into concrete policy reforms, it is striking how woolly the language becomes. And when it does say something, it is notable how it contradicts many of the central elements of the commercial policy reforms in the Lisbon Strategy. There has clearly been a shift from soft market liberalisation to soft industrial policy activism.

Before we get to the policy initiatives discussed in the 2020 strategy, it is important to correct a misunderstanding or misconception that is at the heart of the thinking behind the strategy. The same misconception was also visible in the Lisbon Strategy and the grand trade strategy—Global Europe—that was ‘annexed’ to the previous growth agenda. Worryingly, this misconception has been growing in Europe (and other parts of the world). The misconception is that competitiveness and increasing competitiveness equal global commercial dominance in all sectors.

This is a perception that feasts on fear—a fear similar to the transatlantic doomsday notion in the 1980s that Japan would out-compete Europe and the United States. It comes across as a silly notion today that America and Europe in the 1980s feared that significant parts of production would move to Japan or in other ways cease to exist for American or European workers. But in the 1980s this perception caused widespread anxiety and guided Europe and the United States in a quasi-protectionist direction.

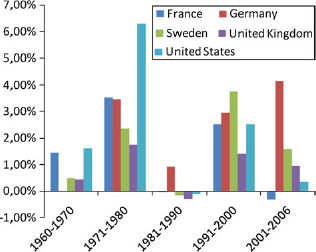

Voluntary export restraints (VERs), orderly market arrangements (OMAs) and other mostly non-tariff barriers were part of the response to the alleged Japanese commercial onslaught. In the 1980s, American car manufacturers were protected by VERs that restricted the number of Japanese cars exported to the United States. The European Community negotiated a similar agreement with Japan in 1983. To further restrict Japanese exports, some European governments imposed ‘local content requirements’ on the cars produced in Europe by companies such as Nissan and Toyota [4]. Many other products, such as semiconductors and videocassette recorders, were also protected by VERs or similar measures [5]. The European steel sector was awash in subsidies. British Steel, owned by the British government, received subsidies through the 1970s and early 1980s that averaged 40% of the export price. The United States defended its steel producers with higher tariffs against steel from emerging Asia and Brazil. The French government even demanded that Japanese VCR imports enter France via Poitiers, a town hundreds of miles from the nearest port. The use of antidumping measures in the United States and the EU also accelerated sharply in the 1980s and in the wake of the 1970s crises. All these measures had a contracting effect on global trade in the 1980s. The 1980s became the ‘lost decade’ for trade in many European countries (see Fig. 1). The trade-to-GDP ratio shrunk in major Western economies and contributed to overall slow GDP growth in that decade.

Annual average growth rate for trade as part of GDP.

The school of ‘New Protectionism’ came to dominate the trade debate, and scholars who favoured ‘managed trade’ rose to prominence [3]. Inspired by what was believed to be a miraculously efficient trade policy in the Far East—protecting and supporting domestic industries while aggressively pursuing export promotion—Europe and the US followed suit. Industrial policy of an activist stripe grew in practically all developed countries.

This time the fear is of China and other fast-growing economies that represent the outside threat. Their economic successes can only mean problems for business and labour in Europe, according to the mercantilist view that lies behind the concept of competitiveness. Competitiveness—as perceived in the Lisbon accord, the 2020 strategy and most other strategy documents from governments around the world—is largely a zero-sum philosophy that defines success by simple output and export measures. It is the sort of ‘pop internationalism’ that economist Paul Krugman ridiculed in his book from the early 1990s of the same name [6]. The idea that countries compete neck-and-neck with each other is a dangerous obsession that too often misguides policy. It is a view that helps politicians and policymakers sell political reforms at home; the commercial prowess of other countries is a source of motivation for offensive or defensive policy actions. In that regard, it is a perception that can leverage good economic reforms. However, it is more likely to push irrational economic policies and an overall defensive posture towards economic reforms and the global market.

This zero-sum economic mindset informs much of the thinking in the elements of the 2020 strategy that deals with commercial policy. As it has been set out so far, it is a programme that aims at beefing up the competitiveness of the agricultural, industrial (heavy, light and advanced) and services sectors—that is, all sectors in Europe. In the EU's 2020 paradigm this also involves a return of industrial policy activism, the idea that governments can pick winners by writing cheques to favoured sectors. The profile and extent of the new industrial policy that Europe envisions remain to be seen. The approach, however, is towards an industrial policy that is activist and micromanaging. Peter Mandelson and the British Labour government have recently turned British policy in that direction, towards what they are calling smart activist industrial policy, in contrast to the ‘dumb’ industrial policy of the kind Europe experienced in the 1970s and 1980s.

This is a dangerous turn of policy. Any growth agenda true to its ambition would cherish the economic success of other countries. Rising affluence abroad means more and richer consumers for firms at home. More often than not, the economic successes of other countries are driven by foreign investments and foreign firms, and such foreign establishment is most often done in a way that enriches all parties and countries involved. The better countries such as China fare at industrial production, the greater the opportunities are for Europe to shift to more high-yielding and high-paying production. In that spirit, rather than asking how policy can boost the competitiveness of the agriculture, light industry or other sectors in Europe, European leaders should ask: What area of domestic production would benefit us if it withered away in Europe?

Political suicide, they would call such a strategy. That may be true. Comparative advantage is what David Ricardo once called it. Any failure on the part of Europe to act on the basis of comparative advantage in its design of the 2020 strategy will dilute the growth-enhancing potential of its strategy.

Learning from past mistakes: the Lisbon Strategy

There are several reasons why the Lisbon Strategy failed to deliver on its ambition. It has already been mentioned that too many of its elements had little or no direct link to growth or pro-growth reforms. These items clouded the purpose of the agenda and the political abilities to deliver reforms. Another problem was that the Lisbon Agenda did not make proper use of the vehicle for market integration in Europe—the vehicle that in Europe's past has delivered progressive integration as well as increased productivity and economic growth.

Most of the core Lisbon targets concerned areas where the EU does not have any jurisdictional competence. The main mission for EU institutions, especially the European Commission, was to bring a more significant EU dimension to national policy arenas by monitoring and evaluating member countries. The underlying role of the EU was to be a ‘midwife of good policies’ and smooth reform processes by transferring benchmarks and experiences from one Member State to another.

The EU could at times also put pressure on Member States, but this was done to a very small degree and in a perfunctory way. Hence, the EU did not have the teeth to really push countries that did not deliver. This, however, does not necessarily translate into an ineffective role for the European institutions. An innovative and dedicated Commission can leverage reforms if it is sufficiently sensible and knows when and where to push for them. The history of the EU provides many examples of critical moments when EU institutions have helped to dissolve nationally based coalitions by introducing concerted reform packages in several or all Member States. True, this sort of political management is more difficult today than in the past, as the EU has expanded in membership and issue focus. Yet the Commission decided to take too much of a back-seat role in the Lisbon process. A few years into the agenda, the outside world and too many Member States had lost interest in it, and efforts by the Commission to advance the agenda often passed unnoticed.

Viewed from a historical perspective, the Lisbon Strategy could arguably be seen as a policy innovation. Of course, it was not the first attempt at beefing up competitiveness and growth. But in the institutional structure of European cooperation, the Lisbon Strategy was the first time that Member States agreed to set up an extensive growth agenda in areas largely outside the scope of centralised EU policy. The traditional model of EU growth promotion—or, if you wish, the political economy of European cooperation—has been increased competition by market expansion and economic integration. The basic idea of the European Community (along with many other international institutions) was to tie European countries closer together through increased economic integration. That is the genesis of the EU. Many other policy areas have progressively been integrated into the European cooperative structure, particularly after the Maastricht Treaty, but the backbone remains economic integration. One can therefore assert that the EU growth promotion strategy has largely been confined to market integration and the reduction of barriers to integration, the single market of 1992 being the premier example of this strategy.

The Lisbon Strategy had reform components of that ilk, most notably the programme to liberalise the energy, financial, telecommunications and transport sectors. The market liberalisation element of the Lisbon Strategy was, however, limited, and the reforms that were launched did not result in far-reaching de facto reforms. Rather, the Lisbon Agenda tried to venture into a different area of growth policy.

First, there was a change of economic mode. Instead of pursuing the traditional agenda of market liberalisation and integration, the agenda directed attention to the contributions to growth from research, technological change and innovation.

Second, there was a change in policy methodology. Rather than reducing barriers and establishing rules for what countries cannot do, the agenda aimed at instructing Member States what to do.

Third, there was a shift in governance structure. The Commission was never the vehicle of reform or in charge of the policy process; it was up to the Member States to set out reform agendas and deliver on them.

Analytically, there are good reasons speaking in favour of this change. The type of Schumpeterian growth the Lisbon Strategy aimed to promote is central to long-run growth and has not contributed as much to growth in Europe as it has in the United States. But as an EU agenda for policy reform, this strategy was flawed. It was doomed to run into difficulties because European institutions have little leverage on such national policies. It also masked the fact that many of the areas in which European institutions have power and can exercise a lot of influence on individual Member States were neglected by the Lisbon Strategy. Furthermore, policies like the EU budget, the common agricultural policy (CAP) and the regional support programme were left outside of the agenda. Reforms in these areas might not contribute as much to growth as labour-market reforms or deregulations of the telecommunications market, but they would enhance structural change and drive economic growth. Equally important, these areas are where the European institutions are in control of policy and can actually deliver policy change.

A new take on the 2020 strategy

Any common strategy for growth in Europe should start from two propositions. First, the basis for a growth strategy should be the reform of policies that Brussels controls and that fit into the already existing structure of jurisdictional competence. In these areas, the Commission can drive reforms without meddling with sensitivities about national sovereignties and can approach policy in a uniform matter (Member States have already transferred power to Brussels, and the EU already runs a uniform policy). Second, having policy components in a strategy that falls outside the structure of jurisdictional competence—and there are many such areas of importance to growth—only makes sense if European institutions have the courage and are granted the tools (benchmarking, empowering institutional competition, ‘naming and shaming’, fines, etc.) that could incentivise delivery of reforms by national governments.

How does the 2020 strategy fare in this context? Not well, is the answer. As far as is possible to determine at this point, it is more accurate to say that it does not fit at all. What are the problems?

First, the 2020 strategy does not approach reforms in areas where common European policies exist and the European institutions have a strong influence over the design and execution of policy. There are some vague references to reforms of and prioritisations in the EU budget. These may lead to good reforms, but the fact that they are not mentioned suggests the issues have been kicked into the long grass.

It could make sense, some would say, to wait with areas such as CAP reform until the current reform process has been concluded. I disagree. If a growth strategy is ever to be taken seriously, it needs to tackle the tough issues. Its success will depend upon the determination of political leaders to actually address the politically sensitive problems. Hence, no pain, no gain. Furthermore, excluding politically sensitive policies from the growth strategy de facto means that the EU is diluting the role the growth strategy can play for sectoral reforms. The CAP reform process has already lost the guiding strategies it had from the start and needs direction based on economic analysis and efficiency. The regional support programme, which also occupies a large portion of the EU budget and is in fact slowing down structural reforms in some areas of Europe, has no such reform direction at all.

The 2020 strategy does not present a trade strategy. It says that such a strategy will be presented later. The single market is mentioned only insofar as it suggests a digital single market. That is a good initiative, but single market reforms cannot be confined only to the digital area. There is much unfinished business with the single market for goods, and the attempt at setting up a single market for services has only marginally improved policy. Rules on state aid and government procurement have been under attack for quite some time, but the 2020 strategy is silent on those issues. Other important issues for growth, like non-EU labour migration, are absent from the strategy. Overall, commercial policy is very weak in the 2020 strategy. Improvements might come later, but it does not look good. The strategy is low on ambitions to that end and does not give a general approach that future commercial policy reforms easily could fit into. For the 2020 strategy to be respected and successful, these flaws need to be remedied. To neglect the central commercial policy areas where Brussels has strong power is to repeat the mistakes of the Lisbon Strategy.

Second, the 2020 strategy takes aim at policies which lie within national sovereignty of the Member States. How should one select such issues? In its proposal, the European Commission decided to put a lot of emphasis on an exit strategy from the crisis, which is a coordinated process for fiscal stabilisation and a return to a non-expansionary monetary policy. This is a sensible area for European cooperation, and it is central to overall stabilisation and the integrity of the Eurozone. But it is a strategy to replace or vitalise the Stability Pact rather than to succeed and improve the Lisbon Agenda.

There are some areas targeted in the 2020 strategy that make sense in an overall economic context of growth. Labour-market reform is one of them. Many of the labour-market regulations in Europe are difficult to change and prevent flexibility. Hiring and firing rules are typically restrictive, creating high entry barriers to the labour market for many groups. The 2020 strategy also underlies the important role of small and medium-sized enterprises for growth in Europe and emphasises research and development as key to long-term growth. This is fine. The problem, however, is that the strategy presents few if any ideas on how concrete policy reforms can be designed to achieve these ambitions, and how European institutions could manage the political process to ensure reform delivery. This takes us to the last area that requires serious rethinking.

Third, the 2020 strategy is weak on methodology to facilitate and incentivise reforms by Member States. The strategy sets out reporting models, but they are perfunctory and do not put the Commission in command of the reporting process. More worrying is that the strategy takes for granted that harmonisation of goals, targets and policy is a good strategy to achieve the larger aim of economic growth. This may be true for some areas, but far from all. Goals need to differ from country to country. Harmonisation of policy or of the policy process can in many instances be a hindrance to national reform processes, as it takes away an element of institutional competition. The idea that countries should move jointly and at the same speed, which is reflected in some of the thinking in the 2020 strategy, is more likely to slow down aggregate reforms. The strategy should rather aim at designing mechanisms that will increase competition among European governments over reform delivery. This requires a different approach to benchmarking and to the overall strategy of transmitting the news to some countries that they are underperforming.

The 2020 strategy requires rethinking to become operable and successful. Many elements in the current strategy need to be discarded because they have little to do with growth. The strategy must convey a stronger sense of policy reform methodology and how the entire agenda can be sequenced to make sense. It is not too late to save the strategy. But its future success depends on the choices made now by European leaders.