Abstract

The integration of financial markets is a fast growing phenomenon worldwide, but especially in the EU. Along with the positive aspects such as simplifying financial transactions, there are also negative implications attached to it. As was the case with the current economic and financial crisis, a problem which arose locally managed to spread to a global level at an impressive speed. After examining the US and European financial supervision models, the authors conclude that a direct supervisor of cross-border acquisitions would be a good, although somewhat unrealistic, solution. This paper puts forward arguments in favour of separating all financial supervision of individual financial institutions from that of the stability of the financial system as a whole, which would be known as European Financial Services Authority (EFSA) in the case of the EU.

Introduction

Although the current financial crisis has spread quickly around the world, it has unfortunately not led to sufficient debate on the structure of financial supervision at the EU level. This article argues in favour of an independent European Financial Services Authority (EFSA) that should be made responsible for the supervision of the entire financial sector in the EU. In this respect our solution differs from that offered by the High-Level Working Group chaired by Jacques de Larosiere, which only envisages the supranational supervision of the largest internationally operating financial institutions in Europe. The de Larosière group was set up to study the question of financial supervision at the EU level. It presented its report on 25 February 2009 [1]. The President of the European Central Bank (ECB), Jean-Claude Trichet, was briefed by his group. Moreover, the report was discussed in the meeting of the European Council in March 2009 and during the informal meeting of the ECOFIN Council (Ministers of Economic Affairs and Finance) in April 2009. The ECB is in the process of finalising its official position on the question. During the most recent monetary dialogue in the European Parliament on 21 January 2009, Trichet concluded his introductory remarks by saying that ‘as underlined in particular by a number of Members of Parliament, Article 105(6) of the Treaty explicitly mentions the possibility for the Member States to decide to confer upon the ECB specific tasks in the domain of financial supervision. Reflections have started on the specific role that could be played by the ECB and its Governing Council should this provision of the Treaty be activated. At this stage the Governing Council has not yet taken position on this topic. I will not fail to report to you the outcome of these reflections.’

The current financial and economic crisis has painfully exposed the failure of financial sector supervision in the US. The crisis started in the housing market with banks selling mortgages on a large scale to customers who borrowed on the expectation of rising house prices but who were barely able to service their debt. The mortgages were bundled into packages that were sold to other parties in the financial markets both in the US and elsewhere. Few parties were able to properly judge the inherent risk of these products. On top of this, the credit rating agencies, such as Moody's and Standard and Poor's, were themselves often involved in the design of these products, which obviously undermined the incentive to provide an adequate rating based on their perceived risk. The worldwide dissemination of these products and the uncertainty about which institutions ultimately owned them undermined confidence among banks about each other's creditworthiness and, hence, made them reluctant to lend to each other. As a result interbank borrowing rates shot up, and those higher rates were passed on to the banks’ customers. As well, banks became more reluctant to extend loans to firms, hampering their investment plans and production of goods and services. What started as a crisis in the US housing market became a worldwide credit crisis and is now becoming a worldwide crisis in the real economy. Unemployment is rising dramatically and most developed economies are shrinking. While inflation was initially on the high side, there is now a serious fear of deflation.

The events just described make clear that both the evolving integration of the financial markets and the ongoing financial innovation enhance the ease and speed with which crises that begin locally can spread globally. This has obvious policy implications. In the words of Nout Wellink, President of De Nederlandsche Bank (DNB) on the occasion of the award of his honorary doctorate at Tilburg University (12 June 2008), ‘It seems obvious that globalisation and financial innovations will continue, so that complexity in the economic and financial system will continue to increase. [] Obviously, there is a need to tailor our policies, for example supervision and monetary policy, to the dynamics that we have witnessed in the financial sector.’ The vast international capital movements and the difficulty of judging the risks associated with complex financial products imply that it will never be possible to completely exclude the possibility of a crisis. However, adequate supervision reduces its likelihood and, in case a crisis does emerge, the damage it produces will be limited. Current developments enhance the desirability of adequate supervision. This is also true of the interest that countries have in the quality of each other's supervision. The external effects of supervisory failure are more significant, as are the benefits from coordination of supervision.

The consequences for US supervision

The US government now envisages another role for the Federal Reserve System (Fed). To protect financial stability, the Fed will primarily focus on macro-prudential supervision of financial institutions (banks, insurance companies, hedge funds and investment funds), while detailed supervision of solvency (micro-prudential supervision) will be assigned to a new authority that takes over the tasks of the various current supervisors. The envisaged design of the US system resembles that of the Dutch model, in which the Authority Financial Markets (AFM) and the DNB are jointly responsible for supervising the solvency of financial institutions. The model with two separate supervisors is sometimes called the ‘twin peaks’ model. Kremers and Schoenmaker [5] prefer this system not only at the national level but also at the European level. They support their position by referring to the coordination problems between the British Financial Services Authority (FSA) and the Bank of England (BoE) after the collapse of Northern Rock. The FSA became responsible for financial sector supervision about 12 years ago, while the BoE would only look after financial stability. However, the British Finance Minister has recently announced measures to adjust the British supervisory model. The BoE will be given more power to avert financial instability.

Financial supervision in the US is a patchwork that has spontaneously evolved since the civil war. However, decentralised supervision leads to fighting over competencies and hampers communication among the various authorities. While one might expect resistance from those who stand to lose responsibilities, in the longer run the consolidation of competences will lead to a better-working model. The potential weakness of the plan is the possible conflict between the traditional and new tasks of the Fed. In the case of a bank failure, the Fed might feel pressured to provide liquidity, while from the perspective of monetary stability this might be undesirable. This problem manifested itself during the Savings & Loans (S&L) crisis in the 1980s when the portfolios of the US savings banks featured a large share of weak debtors and the US federal government was forced into a large bailout ($600 billion or even more). After the S&L crisis the Fed kept the official interest rate (the Federal Funds Rate) low for longer than would have been desirable from the perspective of monetary stability. By keeping interest rates artificially low, interest rate margins and the reserves of the savings banks and loan associations could increase to improve their balances. In other words, financial sector supervision may have spillover effects on monetary policy. In fact, when banks realise that the Fed is both responsible for financial supervision and has the means to act as a lender of last resort, they may be tempted into taking on additional risks (moral hazard) from which they will reap the full benefits if things go well, while in the case of failure the losses will be limited because of intervention by the Fed. Moral hazard has also played a role in the emergence of the current crisis. Financial institutions that took on too much risk in providing mortgages are now being helped out by the Fed's interest rate decreases.

Given that US plans for the restructuring of financial supervision still need to be worked out in more detail, it is hard to judge them at the current moment. The preferred format would be one in which both macro- and micro-prudential supervision of individual institutions are brought under the roof of a single and independent authority that is not responsible for monetary policy and that is also not able to independently decide on the possible rescue of institutions in trouble. Given the potential risks to the financial system, this does not imply that a rescue will never take place. The Fed remains responsible for the stability of the financial system as a whole, but has no role in the prudential supervision of individual institutions. The likelihood of an individual rescue becomes smaller, which suppresses the incentive for moral hazard. Further, because an authority other than the supervisor needs to provide the resources for any rescue, the consequences for price stability will be more explicitly taken into account. Also, with the Fed and the new supervisor both having to assess the need for a rescue, errors in judgment will be reduced. Finally, the independence of both authorities limits the likelihood of interference by politicians.

Of course, separating the supervision of individual institutions from the Fed also has its disadvantages. In the event of a crisis, it will be important for the central bank to be able to immediately judge the amount of liquidity to be supplied to the banking sector. For these situations one could construct crisis scenarios. However, one might also consider the possibility of an obligation to provide the Fed with the necessary information about the liquidity of individual institutions without making it jointly responsible for the supervision of these institutions. As mentioned earlier, the British model of a separate financial supervisor (the FSA) also exists, exerts both macro- and micro-prudential supervision on the financial sector, while the BoE is only responsible for financial stability. This model of a separate supervisor is the legacy of the BCCI failure. BCCI was the only internationally operating, pan-Arabic bank, and it failed on a large scale. Because BCCI's headquarters were located in London, the BoE was the main supervisor involved, although it was hardly informed about problems with this bank. The failure had a negative effect on the BoE as a monetary policymaker, and for this reason the Finance Minister at the time decided to separate the responsibilities for financial and monetary stability by setting up the FSA and making it responsible for financial supervision in the UK.

European supervision

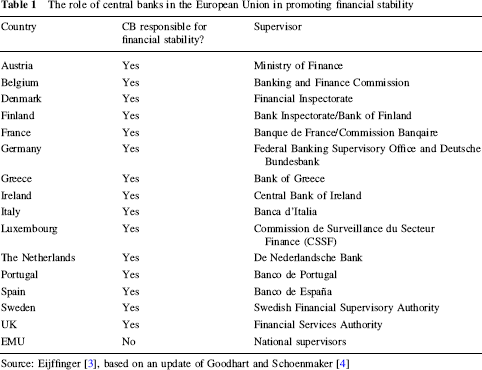

Europe too can draw a number of useful lessons from the current crisis. Financial supervision in Europe is even patchier than in the US. Responsibility for financial supervision rests at the national level in Europe. In principle, each country is free to design its supervisory system to its own liking. This should be clear from Table 1, which provides an overview of the national responsibilities for financial stability and financial supervision in the European Union. Clearly this patchwork supervision will become more and more difficult to maintain due to the ongoing economic and financial integration of Europe. Internationally operating financial institutions have to simultaneously fulfil requirements imposed by different national supervisors. It would be a missed opportunity not to exploit the current crisis and undertake a substantial step towards uniform financial supervision in Europe under the responsibility of a single authority. Below, the most recent developments in Europe as regards to financial supervision are discussed, after which arguments in favour of EFSA are laid out.

The role of central banks in the European Union in promoting financial stability

Current collaboration in Europe

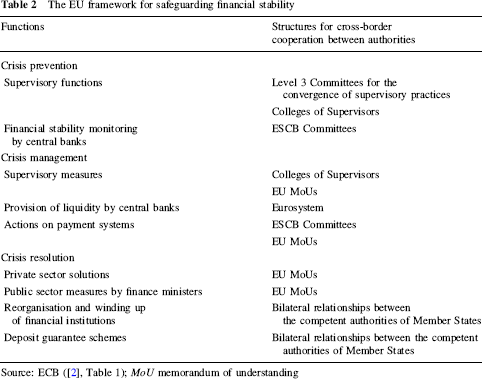

A number of developments, in particular the ongoing financial integration and the growing number of banks with cross-border activities, have led to initiatives to strengthen agreements at the EU level for maintaining financial stability in the medium term. These agreements are intended to bolster financial crisis management in line with the strategic framework of ECOFIN in October 2007 and the extension of the Lamfalussy framework for regulation and supervision. The framework came into effect in 2001 for the purpose of regulating the asset markets and was extended in 2004 to include the insurance sector and the banking sector. In 2007 the framework was evaluated from different angles (among others, by the European Commission and the ECB), resulting in a number of suggestions for improvement that were put on the ECOFIN agenda for December 2007. These proposals concerned in particular the Level 3 Committees of supervisors aimed at convergence and collaboration in supervision. These committees were to be reinforced in three ways. First, their legal basis will be strengthened. Second, their accountability will be enhanced by making their objectives explicit and requiring them to report annually to the Commission, ECOFIN and the European Parliament. The possibility of taking decisions by qualified majority will be introduced as well. These adjustments should lead to more convergence of supervision and improved international collaboration in this area. The current European framework to guard financial stability consists of three layers: crisis prevention, crisis management and crisis resolution. These are described in Table 2. Crisis prevention is initiated by the supervisors, who guard the solidity of financial institutions, and the central banks, who guard the stability of the financial system as a whole. There exist a number of instruments for crisis management. The supervisors may increase the amount of capital required to be held by a financial institution or they may impose a reorganisation, while the central bank may provide liquidity. Financial stability has a distinct international dimension, because the failure of one institution may have a domino effect of failures through the network of obligations financial institutions have towards each other. Hence collaboration at the EU level is inevitable. Currently this is based on a framework that has been largely harmonised via EU law and that is supported by the Level 3 Committees of the Lamfalussy framework.

The EU framework for safeguarding financial stability

Crisis management and crisis resolution mainly concern sharing information and procedures for collaboration among the various national supervisors. In this connection, in 2005 the various parties signed a memorandum of understanding (MoU) for collaboration during a crisis. A new MoU is in the pipeline as part of the aforementioned strategic framework of ECOFIN. One part will be a set of common principles for cross-border crisis management in the case of an internationally operating bank. For example, in solving the crisis, priority will be given to a private-sector solution and in those cases where public money is involved the direct costs will be shared among the Member States that are affected. The new MoU also foresees the use of a recently developed common analytical model that will be used to assess the effects of a potential crisis on the financial system and the real economy. This will facilitate the comparison of the views of various authorities on the consequences of the crisis. Finally, the MoU will provide a number of practical guidelines for crisis management, such as the exact procedures for sharing relevant information and the coordination of decisions. The recent turbulence on the financial markets has given rise to a number of new initiatives at both the EU and the global level. ECOFIN has agreed on a list of concrete actions aimed at enhancing transparency, improving valuation of financial instruments, strengthening the role of markets within various dimensions and improving risk management by banks (as expected, through adjustment in the Capital Requirements Directive). Parallel to this, and at the global level, the Financial Stability Forum (FSF), which is composed of representatives from national and international financial and monetary policy institutions, has recently published a report that recommends certain actions in the aforementioned and other areas. Unfortunately, these developments have been insufficient to generate a serious discussion about the restructuring of financial supervision in Europe. Although the very recent report by the High-Level Working Group chaired by de Larosière recommends common supervision of the largest internationally operating financial institutions in Europe, it falls short of our proposal discussed below. The Larosière report will be discussed later on.

Proposal for a European Financial Services Authority

Although there is cooperation at various levels in Europe, the responsibility for supervision is still at the national level. The increasing amount of cross-border activity by financial institutions and the ongoing process of financial innovation with the associated international spread of risks undermine the suitability of this supervisory model. Supervisors will increasingly be confronted by such questions as the following: Who is responsible for the activities of a foreign subsidiary of an international bank? Who will be held responsible in the event of a failure, the subsidiary or the parent company? Which one of the supervisors should intervene, that of the parent's or the subsidiary's country? The current crisis should have prompted a fundamental debate about the level (national or supranational) at which financial supervision should be organised in Europe. Unfortunately, this has not happened to a sufficient degree. This too is not very surprising, because national supervisors may be reluctant to lose decision powers. Hence, this is where European authorities such as ECOFIN, the European Commission and the ECB have to step in.

The ideal arrangement is probably worldwide and uniform financial supervision. However, this is unlikely to be achieved within the foreseeable future. Therefore we propose the establishment of a separate EFSA that has the overall responsibility for the prudential supervision of all cross-border financial services in Europe. The EFSA becomes the direct supervisor of internationally operating financial institutions and those nationally operating financial institutions that through their activities can also affect financial stability in other countries. The EFSA will also be the direct supervisor of cross-border acquisitions. Direct supervision of the smaller, nationally active institutions will be delegated to the national supervisors. Hence, the national supervisors will continue to exist, albeit under the eventual responsibility of the EFSA. They will retain their crucial role because they are in direct contact with the institutions under their direct supervision. Moreover, because they are very familiar with the situation in their own country, they will be able to provide the EFSA with useful information for the supervision of the large international institutions. Hence, the EFSA will serve as an umbrella under which the national supervisors will operate.

Besides the fact that the EFSA would exert direct supervision of international institutions and those institutions that pose a potential systemic risk, there are further advantages to setting up an EFSA. As the institution with final responsibility, it will impose uniform rules for supervision at the national level. This produces a level playing field, which prevents lax supervision at the national level for the purpose of providing national institutions with competitive advantages. Such regulatory competition has been one of the factors that has contributed to the lax supervision in the US [6]. Uniform supervision will reduce the reporting costs of financial institutions to the supervisor, because there will be a uniform reporting standard. In addition, national supervisors can no longer be played off against each other; indeed, the EFSA will have a stronger strategic position vis-à-vis US supervisors, who are primarily concerned with the interests of their own institutions. It will then become easier to strike agreements aimed at avoiding regulatory competition between US and European supervisors.

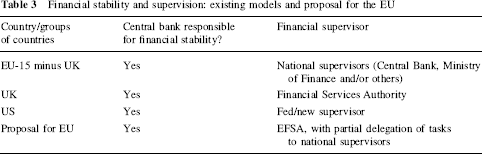

Our earlier discussion of the US situation showed that the EFSA needs to be a federal institution that is allowed to operate independently of the ECB or any other institution or forum. In this regard, it will resemble the British model (see Table 3). Moreover, the EFSA needs to operate at the level of the EU and not solely at that of the Eurozone. A framework in which some EU countries have their own national supervisor(s), while those of other countries are under the responsibility of the EFSA will be hard to maintain for the same reasons that a model with only national supervisors will become more and more cumbersome. It would also lead to complicated legal issues at the EU level. However, more important is that financial institutions are becoming increasingly active in the new EU Member States that in any case are supposed to join the Eurozone in the future. Hence, it will be better to do the entire restructuring of financial supervision in one go.

Financial stability and supervision: existing models and proposal for the EU

Of course, an independent EFSA does not imply that it does not collaborate with the ECB. It will be of crucial importance that the EFSA inform the ECB about potential problems with financial institutions. Incomplete information provision by the financial supervisor to the central bank, as was the case with Northern Rock in the UK, needs to be prevented at all cost. By separating the responsibilities for monetary and financial stability, harmful interference in these two tasks will be avoided. However, this does not imply that the supervisor and the central bank do not properly inform each other. Indeed, the obligation to inform each other should be laid down legally. Moreover, a supranational supervisor does not imply that all EU Member States would need to provide resources when a financial institution in one of the Member States goes bankrupt. The EFSA will only be responsible for cross-border supervision, but will not have the financial means to save these institutions. These resources could be supplied directly by the Member States that are involved in a particular failure. However, the issue of how these costs should be shared (‘burden-sharing’) is a separate matter that requires separate arrangements. Most important in this context is the question of how problems of moral hazard can be avoided. Although the EFSA itself is not able to save an institution, in collaboration with the Member States involved and the ECB it can provide advice about the need and nature of a bailout. This will be important in view of the fact that countries may have different views on the best response to the failure of an internationally operating financial institution.

Concluding remarks

The main recommendations made by the High-Level Working Group chaired by Jacques de Larosière are a political compromise between the EC, the ECB, EU national central banks and supervisors and Ministers of Finance. A new body called the European Systemic Risk Council (ESRC), to be chaired by the ECB President, is to be set up under the auspices and with the logistical support of the ECB. The ESRC is to be composed of the members of the General Council of the ECB, the chairs of the Committee of European Banking Supervisors (CEBS), the Committee of European Insurance and Occupational Pensions Supervisors (CEIOPS) and the Committee of European Securities Regulators (CESR), as well as the European Commission. High-level alternates to the central bank governors should take part in the discussions, in particular when issues having to with the insurance or securities markets are discussed. An effective risk-warning system will be put in place under the auspices of the ESRC and the EFC. The ESRC is supposed to issue macro-prudential risk warnings: there should be mandatory follow-up and, where appropriate, action will be taken by the relevant competent authorities in the EU.

In a first stage, national supervisory authorities should be strengthened with a view to upgrading the quality of supervision in the EU. The European Commission should carry out, in cooperation with the Level 3 Committees, an examination of the degree of independence of all national supervisors. This should lead to concrete recommendations, including on the funding of national authorities. In a second stage, the EU should establish an integrated European System of Financial Supervision (ESFS). The Level 3 Committees should be transformed into three European Authorities: a European Banking Authority, a European Insurance Authority and a European Securities Authority. These authorities should be managed by a board comprised of the chairs of the national supervisory authorities. The chairs and general directors of the authorities should be full-time independent professionals. The appointment of the chairs should be confirmed by the Commission, the European Parliament and the Council, and should be valid for a period of 8 years. The authorities are to be responsible for micro-prudential supervision, while the ECB will take care of macro-prudential supervision by participating in the ESRC as suggested by the High-Level Working Group. This should be realised under clear mandatory arrangements for information and knowledge exchange. The recommendations of the Working Group are not path-breaking but very modest first steps towards fully responsible European supervisory authorities.

In this article, we have argued in favour of separating all financial supervision (both macro- and micro-prudential) of individual financial institutions from the supervision of the stability of the financial system as a whole. Given that the financial sector is becoming increasingly intertwined at the international level, we have provided arguments for setting up an EFSA at the EU level. The EFSA will carry the eventual responsibility for all financial supervision in the EU and will impose uniform rules on all national supervisors. Obviously, this structure would have to be embedded in the Treaty. This implies a long and complicated process with many details that need to be specified more precisely. It will be important, therefore, to start this process as soon as possible.

Footnotes